MAA262 Management Accounting Individual Assignment Report, 2019

VerifiedAdded on 2023/03/17

|6

|717

|28

Report

AI Summary

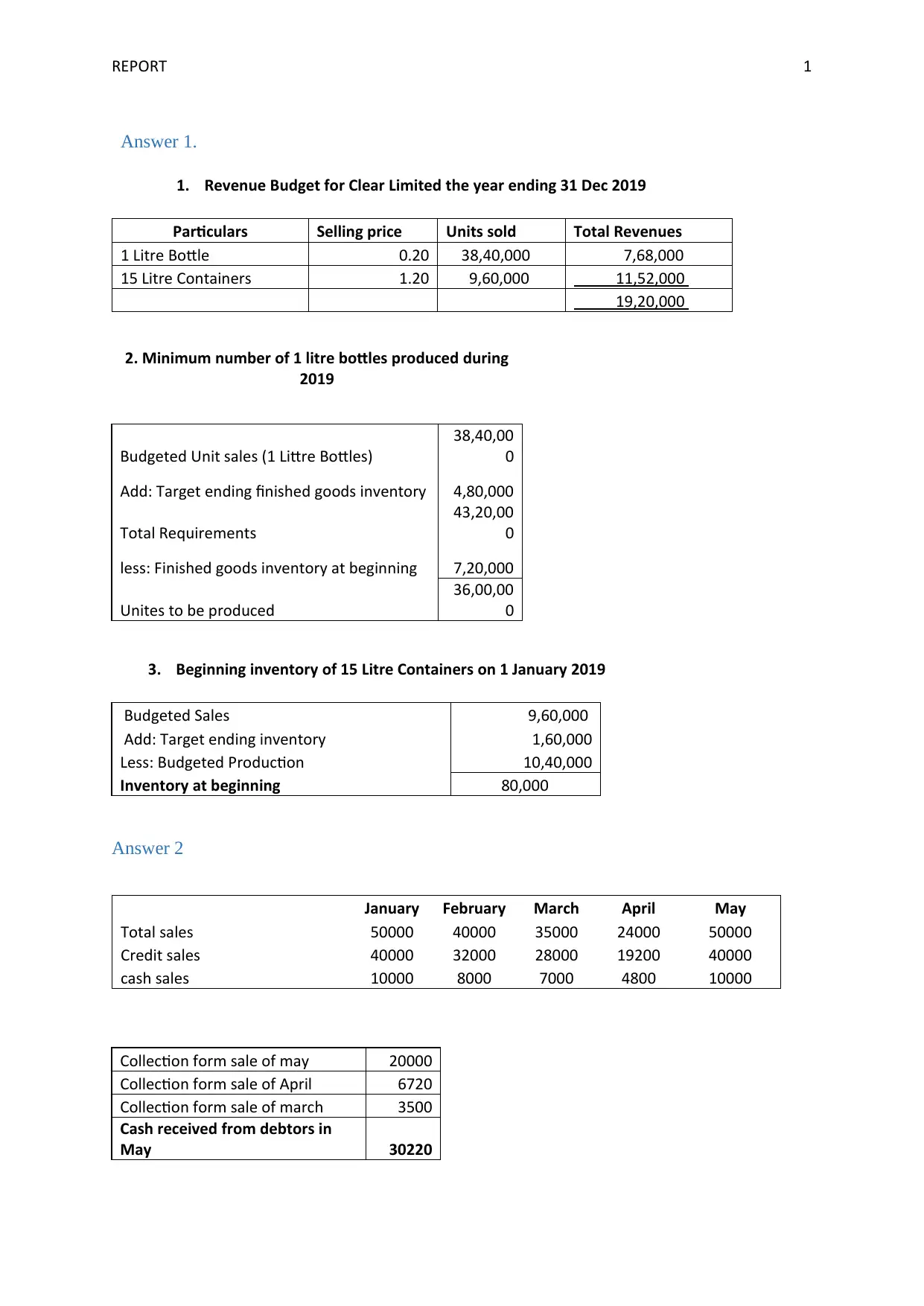

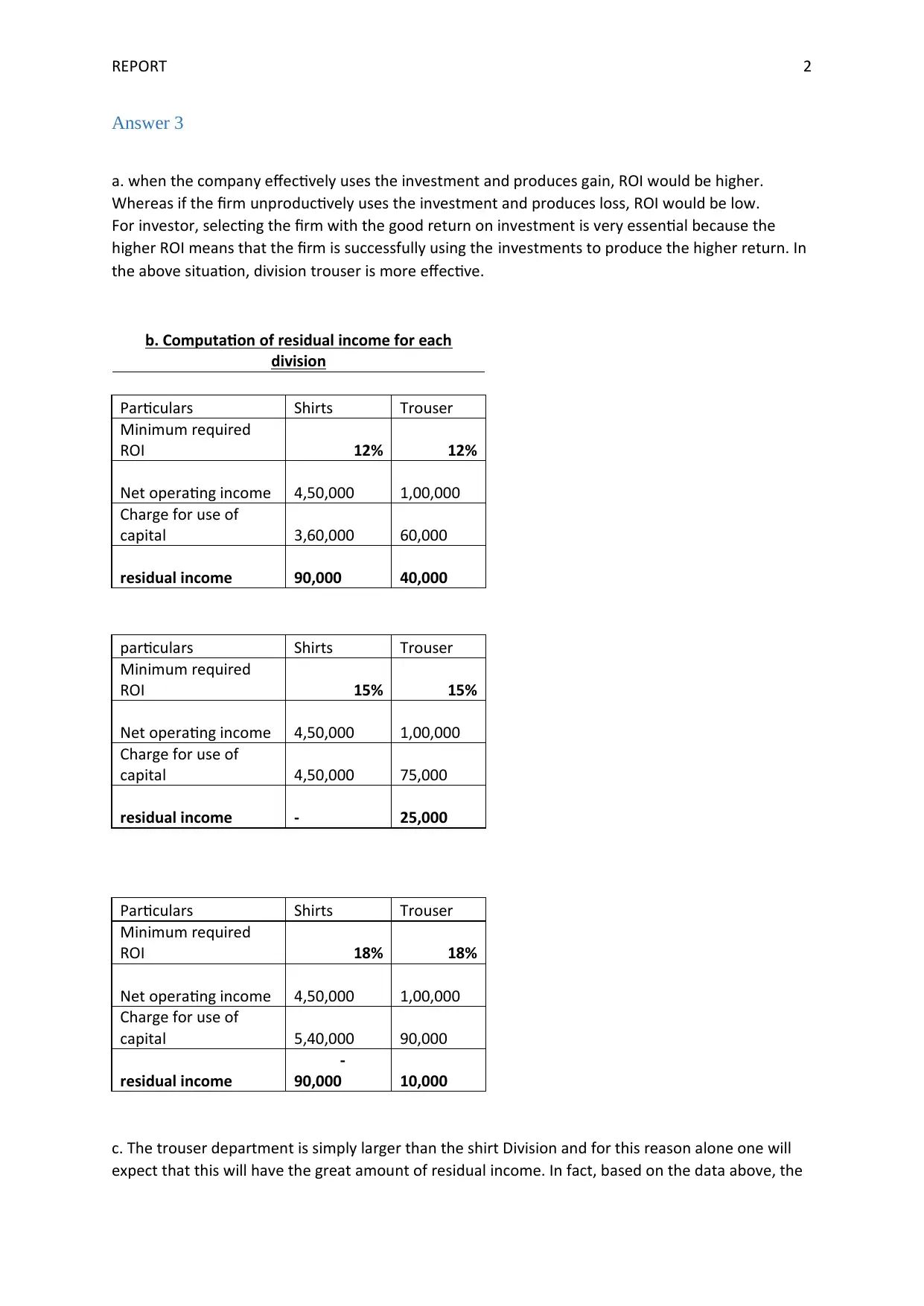

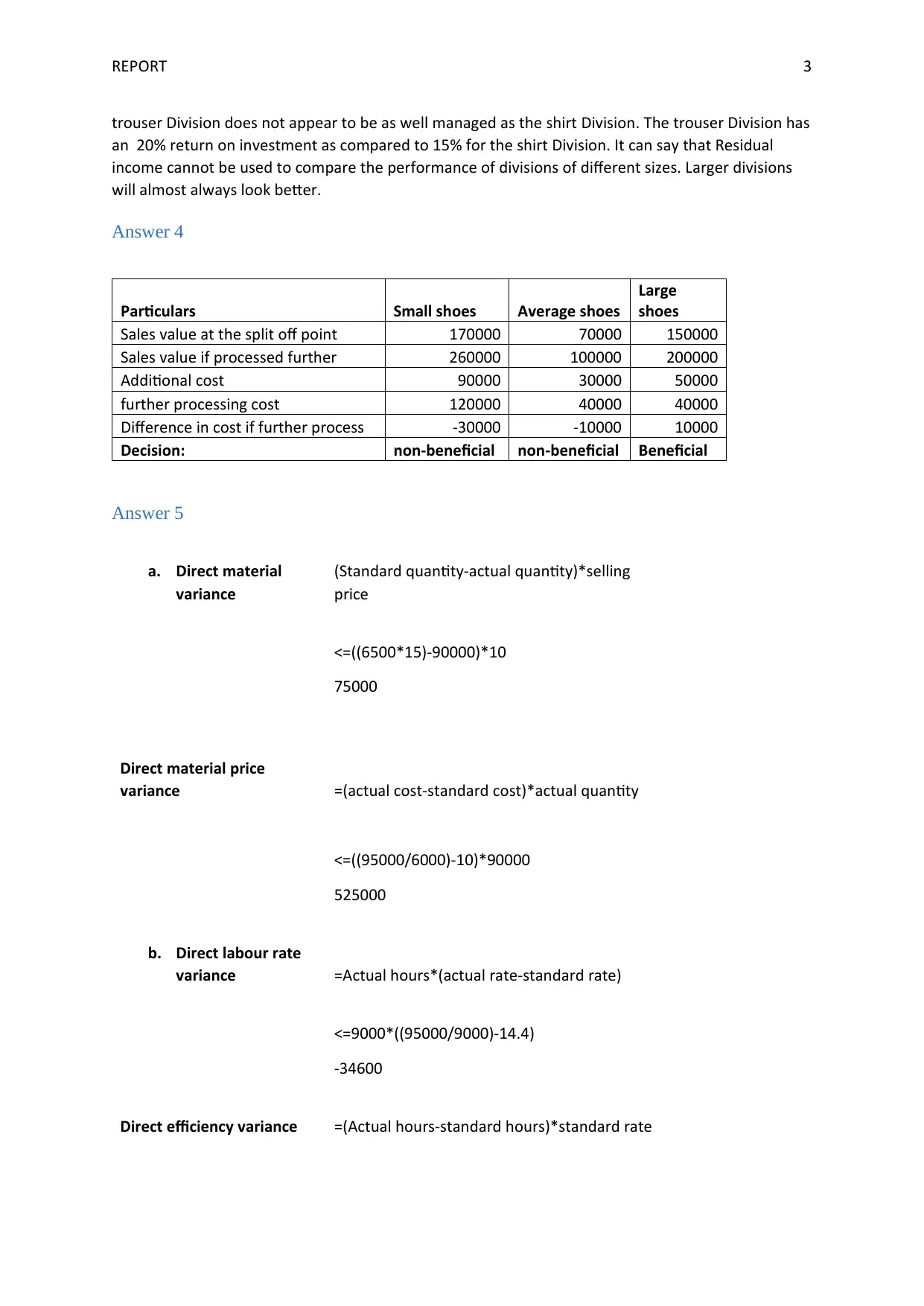

This report presents solutions to a management accounting assignment (MAA262) focusing on financial analysis and decision-making. It begins with a revenue budget for Clear Limited, calculating total revenues based on unit sales and selling prices for different bottle sizes. The report then addresses inventory management, determining the minimum number of bottles to be produced. Further, it analyzes cash collection from sales, providing a breakdown of cash received from debtors over several months. The report also delves into profitability analysis, computing Return on Investment (ROI) and residual income for different divisions. It evaluates whether to process products further, comparing sales values and additional costs. Finally, the report examines variance analysis, calculating direct material and labor variances. The report includes calculations for direct material price and quantity variances, as well as direct labor rate and efficiency variances, highlighting the interrelation of these variances.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.