Unit 5: Management Accounting Application in Marks & Spencer

VerifiedAdded on 2023/01/11

|17

|4669

|56

Report

AI Summary

This report delves into the application of management accounting principles within Marks & Spencer, a prominent international retail organization. It examines the role of management accounting in enhancing organizational performance, highlighting the importance of cost accounting systems, inventory management, job costing methods, and price optimization systems. The report further explores various management accounting techniques such as marginal costing and absorption costing. It also discusses the essential requirements of management accounting systems and analyzes different management reporting methods, including budget reports, cost reports, performance reports, and inventory reports. The study emphasizes how Marks & Spencer can adapt its management accounting systems to effectively respond to financial challenges and improve overall operational efficiency. This detailed analysis provides valuable insights into the practical application of management accounting in the retail sector. Desklib provides access to a wealth of similar student-contributed documents and AI-powered study tools.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUTION..............................................................................................................................1

SCENARIO.....................................................................................................................................1

1. Role of management accounting in organisation.....................................................................1

Application of various management accounting techniques.......................................................6

Pros and cons of various types of planning tools........................................................................8

Adapting MA systems for responding to its financial problems...............................................10

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

APPENDIX....................................................................................................................................15

INTRODUTION..............................................................................................................................1

SCENARIO.....................................................................................................................................1

1. Role of management accounting in organisation.....................................................................1

Application of various management accounting techniques.......................................................6

Pros and cons of various types of planning tools........................................................................8

Adapting MA systems for responding to its financial problems...............................................10

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

APPENDIX....................................................................................................................................15

INTRODUTION

Management accounting pays attention on the accounting aimed at informing the

management on operational metrics of the business. It uses the information related to the cost of

goods or services that are purchased by company. The information is used for quantifying

decisions made on operational planning. Performance reports are prepared under the

management accounting for measuring the variances between budgeted and actual figures.

Management accounting is different from financial accounting for collection of the accounting

data for creating financial statements. Report is based over Marks & Spencer which is an

international retail industry. It will be providing about the requirement and benefits or different

management accounting systems and application to M&S. It will provide about the MA reporting

methods used by company. Study will also include different MA techniques. It will provide

about the different planning tools and management accounting systems for responding to the

financial problems.

SCENARIO

1. Role of management accounting in organisation

Management accounting

Management accounting could be describes as the method used for describing

accounting systems, methods and the techniques with the special knowledge & ability that assist

the management for maximising the profits and minimising the losses. MA involves the

application of the goods various concepts and techniques for processing projected and historical

data of the entity for assisting the management for establishing plan for the economic objectives

and making rational decisions in view towards achieving the objectives.

Management accounting systems and their essential requirements

There are various management accounting systems that are used by the organisation in

effective management of the operations of business. These systems are essential for the

management of business.

Cost accounting systems

It is a framework applied by company to approximate cost of the products for

profitability, inventory valuation and cost control. Cost account system involves the allocation of

cost based using traditional methods or the activity based method of costing (Bromwich and

Scapens, 2016). It is essential for approximating actual cost of the product is a crucial factor in

1

Management accounting pays attention on the accounting aimed at informing the

management on operational metrics of the business. It uses the information related to the cost of

goods or services that are purchased by company. The information is used for quantifying

decisions made on operational planning. Performance reports are prepared under the

management accounting for measuring the variances between budgeted and actual figures.

Management accounting is different from financial accounting for collection of the accounting

data for creating financial statements. Report is based over Marks & Spencer which is an

international retail industry. It will be providing about the requirement and benefits or different

management accounting systems and application to M&S. It will provide about the MA reporting

methods used by company. Study will also include different MA techniques. It will provide

about the different planning tools and management accounting systems for responding to the

financial problems.

SCENARIO

1. Role of management accounting in organisation

Management accounting

Management accounting could be describes as the method used for describing

accounting systems, methods and the techniques with the special knowledge & ability that assist

the management for maximising the profits and minimising the losses. MA involves the

application of the goods various concepts and techniques for processing projected and historical

data of the entity for assisting the management for establishing plan for the economic objectives

and making rational decisions in view towards achieving the objectives.

Management accounting systems and their essential requirements

There are various management accounting systems that are used by the organisation in

effective management of the operations of business. These systems are essential for the

management of business.

Cost accounting systems

It is a framework applied by company to approximate cost of the products for

profitability, inventory valuation and cost control. Cost account system involves the allocation of

cost based using traditional methods or the activity based method of costing (Bromwich and

Scapens, 2016). It is essential for approximating actual cost of the product is a crucial factor in

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

decision making. Costing system is focused over capturing production costs of the company by

weighing the input cost of the every step of production plus fixed cost like depreciation of the

capital equipments. This is a method used by organisation for recording the cost information of

products.

Benefits and application

Cost accounting is applied in the production department for recording all the cost and

expenses incurred for manufacturing goods and services. Benefits of the cost accounting include

identifying the accurate costs incurred to manufacture products on per unit basis. It enables

managers to decide the profit margins and prices. It provides different costing methods that are

used for measuring the costs and recording transactions. There are different costing methods

using which organisations are more accurately reporting the financial operations of business.

Inventory Management

It refers to method of overseeing and controlling ordering, storage and use of the

components that are used by the organisation for production of goods and services sold by it.

Inventory management system combines application of the desktop software, barcode scanners,

barcode printers and mobile devices for streamlining inventory management of goods, stock,

consumables and supplies. It is practice of overseeing and controlling the quantities of finished

goods. Objective of the inventory management is id accurately understanding the present

inventory levels and minimising the overstock and under stock situations (Ax and Greve, 2017).

Managers through efficient tracking of the quantities across stocking location have the insight

and capable to make the sufficient decisions of inventory. Inventory of the M& S are the key

assets & accounts of investment that is tied to the products sold.

Benefits and application

Inventory management is applied by M&S for effectively managing the inventory

records. Being a retail industry it has to deal with large variety of inventory everyday. Systems

used in inventory management enables the managers in tracking the records of inventories.

Company using the inventory management system is effectively enabling the management to be

informed about the movement of each inventory. Systems make the count of inventory and

update the records continuously that provide managers with accurate information about the

inventory stocks.

Job Costing Method

2

weighing the input cost of the every step of production plus fixed cost like depreciation of the

capital equipments. This is a method used by organisation for recording the cost information of

products.

Benefits and application

Cost accounting is applied in the production department for recording all the cost and

expenses incurred for manufacturing goods and services. Benefits of the cost accounting include

identifying the accurate costs incurred to manufacture products on per unit basis. It enables

managers to decide the profit margins and prices. It provides different costing methods that are

used for measuring the costs and recording transactions. There are different costing methods

using which organisations are more accurately reporting the financial operations of business.

Inventory Management

It refers to method of overseeing and controlling ordering, storage and use of the

components that are used by the organisation for production of goods and services sold by it.

Inventory management system combines application of the desktop software, barcode scanners,

barcode printers and mobile devices for streamlining inventory management of goods, stock,

consumables and supplies. It is practice of overseeing and controlling the quantities of finished

goods. Objective of the inventory management is id accurately understanding the present

inventory levels and minimising the overstock and under stock situations (Ax and Greve, 2017).

Managers through efficient tracking of the quantities across stocking location have the insight

and capable to make the sufficient decisions of inventory. Inventory of the M& S are the key

assets & accounts of investment that is tied to the products sold.

Benefits and application

Inventory management is applied by M&S for effectively managing the inventory

records. Being a retail industry it has to deal with large variety of inventory everyday. Systems

used in inventory management enables the managers in tracking the records of inventories.

Company using the inventory management system is effectively enabling the management to be

informed about the movement of each inventory. Systems make the count of inventory and

update the records continuously that provide managers with accurate information about the

inventory stocks.

Job Costing Method

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Job costing is the accounting system which describes allocation of the manufacturing cost

to individual items or batches of products. System is applied where the goods and services

processed differ from each other. this involves practice of accumulating the data on costs

relating to particular services or the production job. This information is important for submitting

the cost data to the consumers under contract where the costs will be refunded.

Benefits and Application

Job costing is used by the M&S when dealing with special orders placed by the

customers. It is useful by the management for evaluating the cost of producing a particular job. It

enables the company to identity the cost associated with each job separately

Price Optimisation System

The system refers to application of the mathematical analysis to corporations for

determining the reactions of consumers over the various prices for the goods and services

through different channels (Christ and Burritt, 2017). The demand of the product changes at

different price levels and managers using price optimisation method evaluate the optimum prices

to be set for the products and services.

Benefits and application

Price optimisation is applied in planning and decision making process by the

management. It provides the management with insight and results of evaluating the demand at

different price levels. Benefits of price optimisation enable the company to set optimum prices of

the product.

Essential requirements of management accounting systems

Cost accounting System

It individually measures and record cost then comparing the inputs with the actual

outcomes or results for assisting the management to measures the financial performance.

Managers of the Business rely over the accounting data n specific or general on the cost as the

tasks of company could be explained through its costs. It is key concept used in management

accounting as analytical tools like the marginal costing, budgetary control, standard costing and

operating costing that are applied by managers for making the production process more efficient.

Inventory management

Following constitutes the function of inventory management system for creating the

purchase orders, relocating, receiving, adjusting and disposal of inventory. Inventory

3

to individual items or batches of products. System is applied where the goods and services

processed differ from each other. this involves practice of accumulating the data on costs

relating to particular services or the production job. This information is important for submitting

the cost data to the consumers under contract where the costs will be refunded.

Benefits and Application

Job costing is used by the M&S when dealing with special orders placed by the

customers. It is useful by the management for evaluating the cost of producing a particular job. It

enables the company to identity the cost associated with each job separately

Price Optimisation System

The system refers to application of the mathematical analysis to corporations for

determining the reactions of consumers over the various prices for the goods and services

through different channels (Christ and Burritt, 2017). The demand of the product changes at

different price levels and managers using price optimisation method evaluate the optimum prices

to be set for the products and services.

Benefits and application

Price optimisation is applied in planning and decision making process by the

management. It provides the management with insight and results of evaluating the demand at

different price levels. Benefits of price optimisation enable the company to set optimum prices of

the product.

Essential requirements of management accounting systems

Cost accounting System

It individually measures and record cost then comparing the inputs with the actual

outcomes or results for assisting the management to measures the financial performance.

Managers of the Business rely over the accounting data n specific or general on the cost as the

tasks of company could be explained through its costs. It is key concept used in management

accounting as analytical tools like the marginal costing, budgetary control, standard costing and

operating costing that are applied by managers for making the production process more efficient.

Inventory management

Following constitutes the function of inventory management system for creating the

purchase orders, relocating, receiving, adjusting and disposal of inventory. Inventory

3

management makes the sales order packaging, picking and shipping of the products. Managers

performs physical counts of inventory, cycle counts, creating, managing, sharing and scheduling

the reports including printing of barcode labels (Soderstrom, Soderstrom and Stewart, 2017).

Benefits of inventory management to the organisation include improving bottom line of M&S,

enhancing the inventory accuracy to improve the company workflow.

Job Costing Method

Job costing system is required for providing important decisions to determine accuracy of

estimating systems of company which is capable to quote the prices that permits for reasonable

income. Information is also used by Marks & Spencer for assigning the inventorial cost to the

processed products. Job costing requires accumulation of information related to direct materials,

labour and the overheads.

Price Optimisation System

The optimisation systems enables the company and managers to be applied for

determining prices which company uses in the best manner for achieving the required goals and

objective and to maximise operating profits. Discovering alternatives via the highest achievable

method or the cost effective method under constraint provided by maximising the desired aspects

and minimising undesired ones. Benefits of price optimisation enable the company to set

optimum prices of the product.

Different methods used for the management reporting.

Managerial accounting focus over internal information received through the financial

accounting. MA is applied for planning, controlling and the decision making. Management

accountants depend over the financial statements that comprises of income statement, balance

sheet and the cash flow statements. Managers use different forms of the internal accounting

reports for evaluating the corporate information. It includes the budgets cost report, products and

the performance report.

Budget Reports

Preparation of the budgets is the key element in the management accounting. These budgets

established by using the prior budgets and adjust them to the future forecast. Budgets of the

company list all the sources of revenues and expenses. Corporations attempts for attaining the

objective and goals while staying within budgeted amounts (Alawattage, Wickramasinghe and

4

performs physical counts of inventory, cycle counts, creating, managing, sharing and scheduling

the reports including printing of barcode labels (Soderstrom, Soderstrom and Stewart, 2017).

Benefits of inventory management to the organisation include improving bottom line of M&S,

enhancing the inventory accuracy to improve the company workflow.

Job Costing Method

Job costing system is required for providing important decisions to determine accuracy of

estimating systems of company which is capable to quote the prices that permits for reasonable

income. Information is also used by Marks & Spencer for assigning the inventorial cost to the

processed products. Job costing requires accumulation of information related to direct materials,

labour and the overheads.

Price Optimisation System

The optimisation systems enables the company and managers to be applied for

determining prices which company uses in the best manner for achieving the required goals and

objective and to maximise operating profits. Discovering alternatives via the highest achievable

method or the cost effective method under constraint provided by maximising the desired aspects

and minimising undesired ones. Benefits of price optimisation enable the company to set

optimum prices of the product.

Different methods used for the management reporting.

Managerial accounting focus over internal information received through the financial

accounting. MA is applied for planning, controlling and the decision making. Management

accountants depend over the financial statements that comprises of income statement, balance

sheet and the cash flow statements. Managers use different forms of the internal accounting

reports for evaluating the corporate information. It includes the budgets cost report, products and

the performance report.

Budget Reports

Preparation of the budgets is the key element in the management accounting. These budgets

established by using the prior budgets and adjust them to the future forecast. Budgets of the

company list all the sources of revenues and expenses. Corporations attempts for attaining the

objective and goals while staying within budgeted amounts (Alawattage, Wickramasinghe and

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Uddin, 2017). Managers consider new vendors for employing the suppliers of raw materials for

saving the money. It also looks for increasing the sales for reducing the expenses.

Cost Reports

Management accounting measures the costs of items manufactured. The costs of the

products and services are calculated taking the overhead costs of the raw materials, labour costs

plus the extra costs in the consideration. Sum of all the costs are divided in the amounts of the

goods produced. All data are summarised in form of cost reports. Reports provide the managers

with capability of viewing cost values of the product versus selling price. This assists the

managers in effective control and planning for the profit margins. Cost reports provide the

detailed cost information about the products and services that are produced and manufactured by

the company. The cost report provides information that are essential for decision making by the

cost account related to the costs and incomes that are produced. They allow the managers to

decide the profit margins of products and services after analysing the costs.

Performance Reports

Management accountant apply budgets for making comparison between the budgeted

amounts with actual incomes and expenditures. Management evaluates the differences that are

computed when shaping the new budgets and all the information concerning amounts are listed

over performance reports. Performance reports are computed by the company every year but

there are corporations that are establishing them quarterly or half yearly. Reports assist the

managers to plan for future demand in the production and costs increases (Nørreklit, 2017).

Performance reports are used by the organisation to evaluate the performance of different

departments of company. By identifying performance it could focus over more productive areas

that are profitable for the company and reducing the areas that are consuming cost. It enables the

company to change the structures of operations for increasing the productivity and efficiency of

management.

Inventory Reports

Inventory reports are prepared by the organisation for effectively managing the inventory.

This is applicable to the management of different products. Inventory reports provide all the

information about the different inventories that are used by the organisation including raw

material, company assets or the raw materials. Inventory report includes the information about

the frequency of inventory movements within the organisation. The information is used by the

5

saving the money. It also looks for increasing the sales for reducing the expenses.

Cost Reports

Management accounting measures the costs of items manufactured. The costs of the

products and services are calculated taking the overhead costs of the raw materials, labour costs

plus the extra costs in the consideration. Sum of all the costs are divided in the amounts of the

goods produced. All data are summarised in form of cost reports. Reports provide the managers

with capability of viewing cost values of the product versus selling price. This assists the

managers in effective control and planning for the profit margins. Cost reports provide the

detailed cost information about the products and services that are produced and manufactured by

the company. The cost report provides information that are essential for decision making by the

cost account related to the costs and incomes that are produced. They allow the managers to

decide the profit margins of products and services after analysing the costs.

Performance Reports

Management accountant apply budgets for making comparison between the budgeted

amounts with actual incomes and expenditures. Management evaluates the differences that are

computed when shaping the new budgets and all the information concerning amounts are listed

over performance reports. Performance reports are computed by the company every year but

there are corporations that are establishing them quarterly or half yearly. Reports assist the

managers to plan for future demand in the production and costs increases (Nørreklit, 2017).

Performance reports are used by the organisation to evaluate the performance of different

departments of company. By identifying performance it could focus over more productive areas

that are profitable for the company and reducing the areas that are consuming cost. It enables the

company to change the structures of operations for increasing the productivity and efficiency of

management.

Inventory Reports

Inventory reports are prepared by the organisation for effectively managing the inventory.

This is applicable to the management of different products. Inventory reports provide all the

information about the different inventories that are used by the organisation including raw

material, company assets or the raw materials. Inventory report includes the information about

the frequency of inventory movements within the organisation. The information is used by the

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

business to make inventory reports for making timely order for raw materials and other

components used in the organisation for production of goods or services. Using the inventory

reports projections for the future requirements of the inventory are made by the management.

Application of various management accounting techniques

There are various types of management accounting techniques which are used by the

organization. The two most widely used methods are stated below.

Marginal Costing System

It is used to determine the per unit cost of the additional product produced. This method

helps in determining the optimum production quantity of the company which helps in evaluating

the least price at which the product can be produced (Nespeca and Chiucchi, 2018). It determines

the break-even point after which the company will start earning profits.

Absorption Costing System

This technique is also known as full absorption costing as it indicates that the all the

manufacturing cost whether it is fixed or variable are assigned to eh cost of production of the

product produced (Ray and Gramlich, 2016). Thus, the cost of finished goods includes, direct

material and labour and variable and fixed production overhead cost. This method is required for

external financial reporting.

Marks and Spencer is producing a unique clothing range made from organic raw material for its

retail outlets. The costs pertaining to it are stated in the appendix.

Working note

Unit product cost

Particulars Amount in

£

Direct material 8

Direct labour 5

Variable production cost 2

Total variable production

cost

15

6

components used in the organisation for production of goods or services. Using the inventory

reports projections for the future requirements of the inventory are made by the management.

Application of various management accounting techniques

There are various types of management accounting techniques which are used by the

organization. The two most widely used methods are stated below.

Marginal Costing System

It is used to determine the per unit cost of the additional product produced. This method

helps in determining the optimum production quantity of the company which helps in evaluating

the least price at which the product can be produced (Nespeca and Chiucchi, 2018). It determines

the break-even point after which the company will start earning profits.

Absorption Costing System

This technique is also known as full absorption costing as it indicates that the all the

manufacturing cost whether it is fixed or variable are assigned to eh cost of production of the

product produced (Ray and Gramlich, 2016). Thus, the cost of finished goods includes, direct

material and labour and variable and fixed production overhead cost. This method is required for

external financial reporting.

Marks and Spencer is producing a unique clothing range made from organic raw material for its

retail outlets. The costs pertaining to it are stated in the appendix.

Working note

Unit product cost

Particulars Amount in

£

Direct material 8

Direct labour 5

Variable production cost 2

Total variable production

cost

15

6

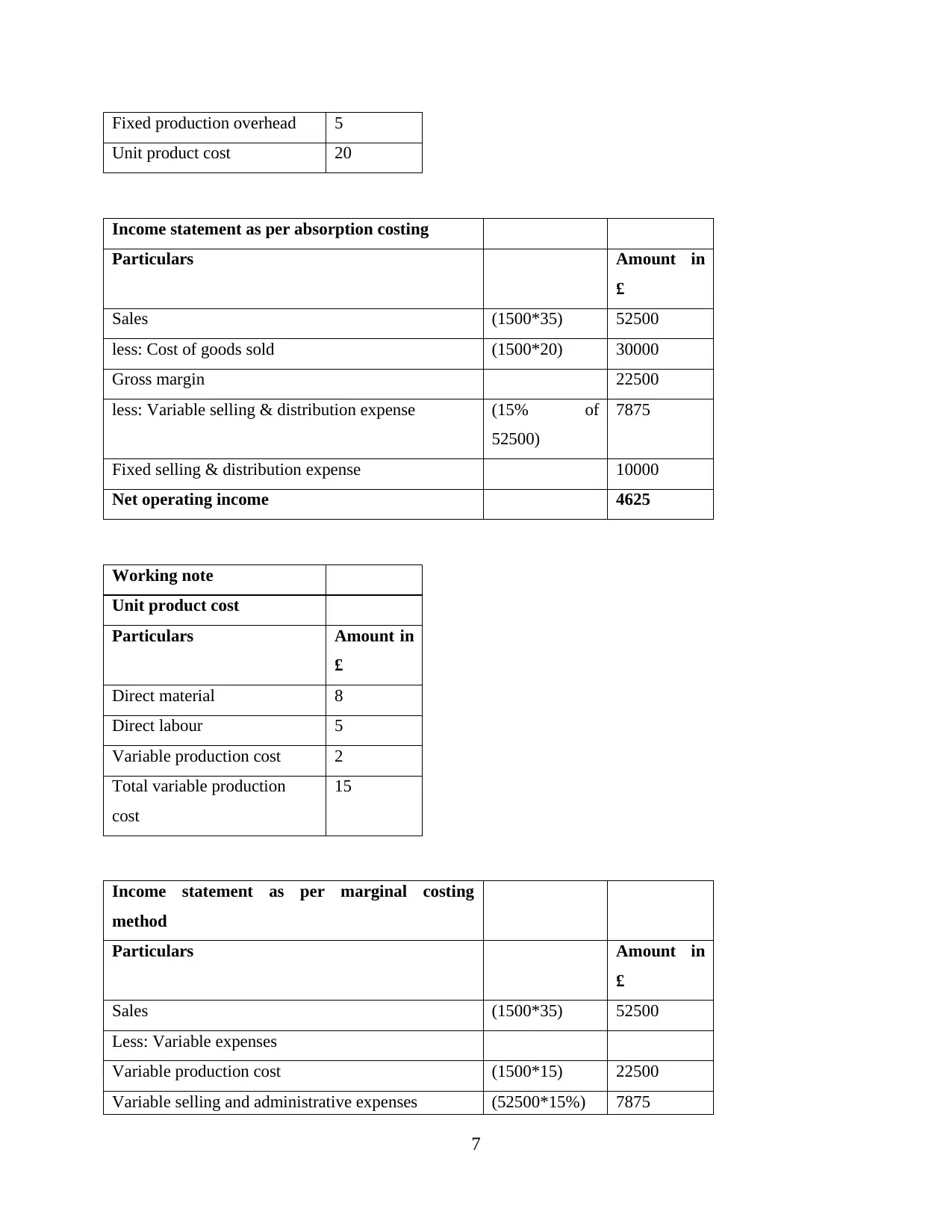

Fixed production overhead 5

Unit product cost 20

Income statement as per absorption costing

Particulars Amount in

£

Sales (1500*35) 52500

less: Cost of goods sold (1500*20) 30000

Gross margin 22500

less: Variable selling & distribution expense (15% of

52500)

7875

Fixed selling & distribution expense 10000

Net operating income 4625

Working note

Unit product cost

Particulars Amount in

£

Direct material 8

Direct labour 5

Variable production cost 2

Total variable production

cost

15

Income statement as per marginal costing

method

Particulars Amount in

£

Sales (1500*35) 52500

Less: Variable expenses

Variable production cost (1500*15) 22500

Variable selling and administrative expenses (52500*15%) 7875

7

Unit product cost 20

Income statement as per absorption costing

Particulars Amount in

£

Sales (1500*35) 52500

less: Cost of goods sold (1500*20) 30000

Gross margin 22500

less: Variable selling & distribution expense (15% of

52500)

7875

Fixed selling & distribution expense 10000

Net operating income 4625

Working note

Unit product cost

Particulars Amount in

£

Direct material 8

Direct labour 5

Variable production cost 2

Total variable production

cost

15

Income statement as per marginal costing

method

Particulars Amount in

£

Sales (1500*35) 52500

Less: Variable expenses

Variable production cost (1500*15) 22500

Variable selling and administrative expenses (52500*15%) 7875

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

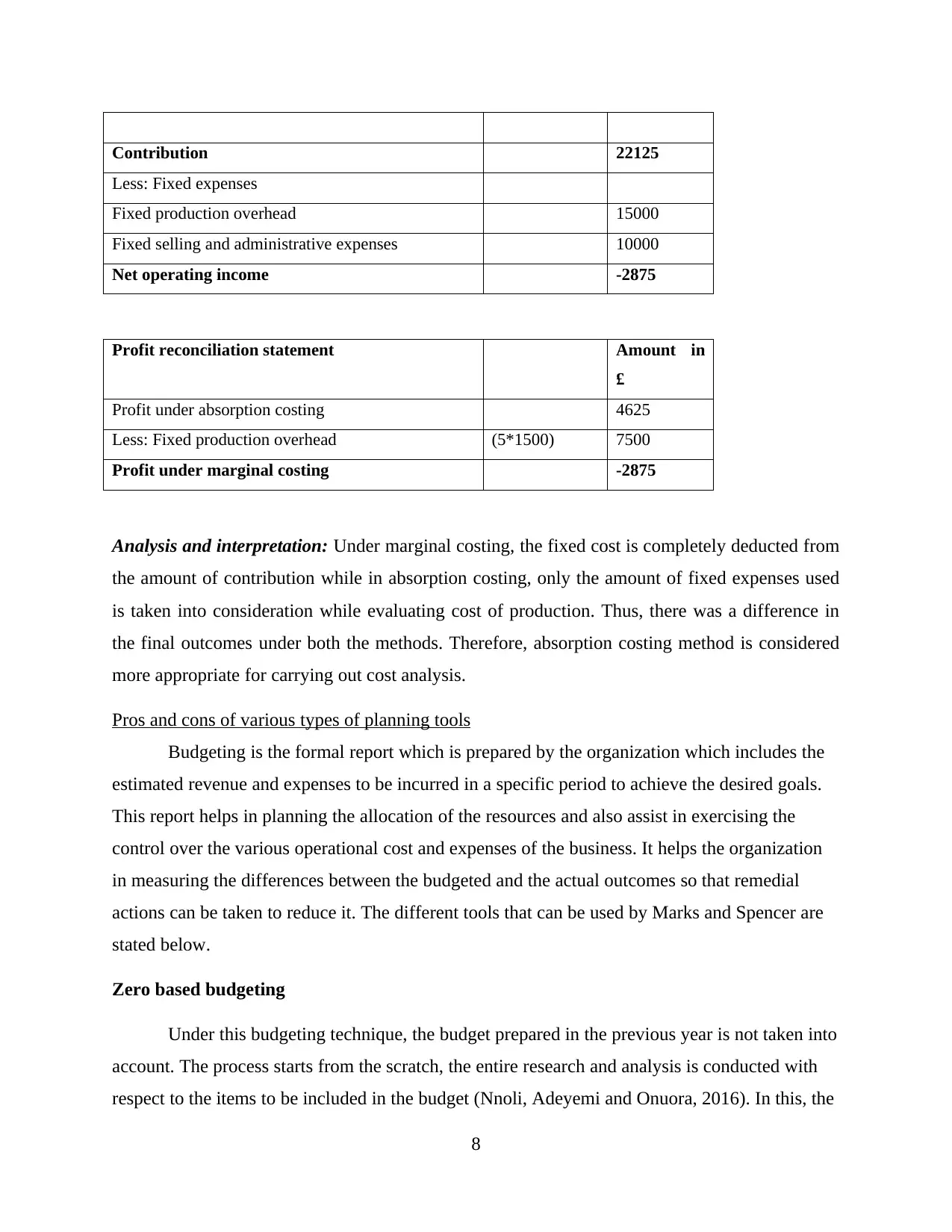

Contribution 22125

Less: Fixed expenses

Fixed production overhead 15000

Fixed selling and administrative expenses 10000

Net operating income -2875

Profit reconciliation statement Amount in

£

Profit under absorption costing 4625

Less: Fixed production overhead (5*1500) 7500

Profit under marginal costing -2875

Analysis and interpretation: Under marginal costing, the fixed cost is completely deducted from

the amount of contribution while in absorption costing, only the amount of fixed expenses used

is taken into consideration while evaluating cost of production. Thus, there was a difference in

the final outcomes under both the methods. Therefore, absorption costing method is considered

more appropriate for carrying out cost analysis.

Pros and cons of various types of planning tools

Budgeting is the formal report which is prepared by the organization which includes the

estimated revenue and expenses to be incurred in a specific period to achieve the desired goals.

This report helps in planning the allocation of the resources and also assist in exercising the

control over the various operational cost and expenses of the business. It helps the organization

in measuring the differences between the budgeted and the actual outcomes so that remedial

actions can be taken to reduce it. The different tools that can be used by Marks and Spencer are

stated below.

Zero based budgeting

Under this budgeting technique, the budget prepared in the previous year is not taken into

account. The process starts from the scratch, the entire research and analysis is conducted with

respect to the items to be included in the budget (Nnoli, Adeyemi and Onuora, 2016). In this, the

8

Less: Fixed expenses

Fixed production overhead 15000

Fixed selling and administrative expenses 10000

Net operating income -2875

Profit reconciliation statement Amount in

£

Profit under absorption costing 4625

Less: Fixed production overhead (5*1500) 7500

Profit under marginal costing -2875

Analysis and interpretation: Under marginal costing, the fixed cost is completely deducted from

the amount of contribution while in absorption costing, only the amount of fixed expenses used

is taken into consideration while evaluating cost of production. Thus, there was a difference in

the final outcomes under both the methods. Therefore, absorption costing method is considered

more appropriate for carrying out cost analysis.

Pros and cons of various types of planning tools

Budgeting is the formal report which is prepared by the organization which includes the

estimated revenue and expenses to be incurred in a specific period to achieve the desired goals.

This report helps in planning the allocation of the resources and also assist in exercising the

control over the various operational cost and expenses of the business. It helps the organization

in measuring the differences between the budgeted and the actual outcomes so that remedial

actions can be taken to reduce it. The different tools that can be used by Marks and Spencer are

stated below.

Zero based budgeting

Under this budgeting technique, the budget prepared in the previous year is not taken into

account. The process starts from the scratch, the entire research and analysis is conducted with

respect to the items to be included in the budget (Nnoli, Adeyemi and Onuora, 2016). In this, the

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

mistakes that were occurred in the previous year will not be repeated in the current year. This

method helps in making more accurate and appropriate budget with very least difference from

the actuals as everything is taken from the zero level. Proper justification is not required as in

case of traditional form of budgeting as each and every item is included after carrying out proper

research and its impact.

Advantages

This approach does not take into account the past year’s budget.

Complete research is conducted whenever the budget is prepared. It helps in lowering the cost as it carries out complete analysis.

It is preferred mostly in case of products which are prone to frequent market changes.

Disadvantages

It involves a lot of time and efforts for preparing the budget.

It is little expensive as market research is conducted entirely.

Data manipulation can be done by managers to get more resource to their departments.

Activity Based Budgeting

It is another form of budgeting method in which the organization prepares the budget

based on the activities carried out by it. The budget is completely dependent on the estimation

made in respect to the resources to be used along with amount of productivity it will generate

(Dhubea and Al-Riami, 2017). This method does not consider the previous year budget for

preparing the current year budget. This method assists the organization in identifying the various

costs and expenditures in association with various business activities which is being carried out

in the production process. This form of budgeting tool helps in identifying any discrepancy in the

system which leads to costs and wastages so that timely actions can be taken to correct it.

Advantages

This planning tool can be easily implemented with less time and effort.

It provides assistance to the organization in determining any production in the activities

and the production process.

It is prepared without considered past year budget.

9

method helps in making more accurate and appropriate budget with very least difference from

the actuals as everything is taken from the zero level. Proper justification is not required as in

case of traditional form of budgeting as each and every item is included after carrying out proper

research and its impact.

Advantages

This approach does not take into account the past year’s budget.

Complete research is conducted whenever the budget is prepared. It helps in lowering the cost as it carries out complete analysis.

It is preferred mostly in case of products which are prone to frequent market changes.

Disadvantages

It involves a lot of time and efforts for preparing the budget.

It is little expensive as market research is conducted entirely.

Data manipulation can be done by managers to get more resource to their departments.

Activity Based Budgeting

It is another form of budgeting method in which the organization prepares the budget

based on the activities carried out by it. The budget is completely dependent on the estimation

made in respect to the resources to be used along with amount of productivity it will generate

(Dhubea and Al-Riami, 2017). This method does not consider the previous year budget for

preparing the current year budget. This method assists the organization in identifying the various

costs and expenditures in association with various business activities which is being carried out

in the production process. This form of budgeting tool helps in identifying any discrepancy in the

system which leads to costs and wastages so that timely actions can be taken to correct it.

Advantages

This planning tool can be easily implemented with less time and effort.

It provides assistance to the organization in determining any production in the activities

and the production process.

It is prepared without considered past year budget.

9

Disadvantages

It requires exercising the professional knowledge and skills.

It is an expensive process for the purpose of implementation.

Operational Budgets

This budget is mainly prepared for the operational activities of the business entity. It

provides estimation of the revenue and expenses of the organization which is based on the

previous year trend (Tsofa, Molyneux and Goodman, 2016). It considers the past yar budget for

preparing the new budget. It provides assistance to the organization with respect to the proper

allocation of the resources among the various organizational departments.

Advantages

This budget is very easy to prepared and simple to understand.

Provides helps in effective allocation of financial resources.

Effective in exercising control over the cost and expenses of the organization as per the

set plan.

Disadvantages

It is based on the past year’s budget, thus, chance of getting errors increases.

It is impossible to make the accurate forecasting about the future business activities.

Adapting MA systems for responding to its financial problems

With the changing working scenarios, the importance of information has increased over

the period of time as it helps in measuring the performance of the organization. Some of the

budgetary control methods are stated below.

Benchmarking

This budgetary control method is used for measuring the performance of the business

with the best rated firm in the industry. The actual performance of the organization is compared

with the performance of the competitor in the industry (Tee, 2016). The deviation in the form of

process, technology, activity is determined and remedial steps are taken to improve the

performance of the organization. Benchmarking has number of benefits such as competitive

10

It requires exercising the professional knowledge and skills.

It is an expensive process for the purpose of implementation.

Operational Budgets

This budget is mainly prepared for the operational activities of the business entity. It

provides estimation of the revenue and expenses of the organization which is based on the

previous year trend (Tsofa, Molyneux and Goodman, 2016). It considers the past yar budget for

preparing the new budget. It provides assistance to the organization with respect to the proper

allocation of the resources among the various organizational departments.

Advantages

This budget is very easy to prepared and simple to understand.

Provides helps in effective allocation of financial resources.

Effective in exercising control over the cost and expenses of the organization as per the

set plan.

Disadvantages

It is based on the past year’s budget, thus, chance of getting errors increases.

It is impossible to make the accurate forecasting about the future business activities.

Adapting MA systems for responding to its financial problems

With the changing working scenarios, the importance of information has increased over

the period of time as it helps in measuring the performance of the organization. Some of the

budgetary control methods are stated below.

Benchmarking

This budgetary control method is used for measuring the performance of the business

with the best rated firm in the industry. The actual performance of the organization is compared

with the performance of the competitor in the industry (Tee, 2016). The deviation in the form of

process, technology, activity is determined and remedial steps are taken to improve the

performance of the organization. Benchmarking has number of benefits such as competitive

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.