Management Accounting Report: R.L. Maynard Company, Unit 5 Analysis

VerifiedAdded on 2020/02/17

|21

|5373

|338

Report

AI Summary

This report delves into the significance of management accounting within a business context, using R.L. Maynard Company as a case study. It explores the fundamentals of management accounting, including its role in decision-making and the essential requirements of various management accounting systems such as traditional cost accounting, lean accounting, throughput accounting, and transfer pricing. The report further examines different methods used for management accounting reporting, including job cost reports, sales reports, cost accounting, and budgetary reports. A key focus is on applying cost analysis techniques to prepare income statements using both marginal and absorption costing methods, comparing their approaches and outcomes. The report highlights the differences between these methods, emphasizing the importance of absorption costing for providing a comprehensive view of a company's financial position. The report also contains the calculation of income statements using marginal and absorption costing methods.

UNIT 5

MANAGEMENT

ACCOUNTING

MANAGEMENT

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Illustration Index

Illustration 1: Income statement on absorption costing basis..........................................................9

Illustration 1: Income statement on absorption costing basis..........................................................9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Index of Tables

Table 1: Income statement on the basis of marginal costing...........................................................9

Table 1: Income statement on the basis of marginal costing...........................................................9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION

Management accounting is a discipline of accounts which reflects professional side, just the

internal one and has a greater significance in decision making. Management accounting helps

in making decisions related with business after planning so that a systematic procedure of

identifying, measuring, analysing, interpreting and communicating can be followed. In a

business enterprise, there are different times when management must take decisions regarding

daily business as well as some essential works.

For this purpose, they must revise and go through various reports that can impact their

decisions (Kaplan and Atkinson, 2015). Hence, management accounting report presents the

accurate information to the management so that they can come to a decision. The present

report demonstrates significance of management accounting in business environment. For

this purpose, R.L. Maynard company of UK has been chosen as a referred organisation. This

is a construction based company whose strength is 24 workers. The report contains

information about different types of income statements that a company uses along with its

benefits and drawbacks. In addition to this, various issues related to management accounting

will be addressed.

LO 1: Demonstrate an understanding of management accounting systems

P1 Explain management accounting and give the essential requirements of different types

of management accounting systems

The management accounting system is a tool which helps the organisation to keep an eye on

various types of costs and expenses that can be incurred in the production of goods and

services (Macintosh and Quattrone, 2010). In context of R.L. Maynard, the organisation has

several expenses which are necessary to be tracked so that they can have better information

regarding different costs. This will also be helpful in keeping a track of business so that they

can manage their day to day works the management accounting has the more importance in

field of business as it includes various branches of finance as well as management because of

which business enterprises can have an overall control on activities of production.

Management accounting is a discipline of accounts which reflects professional side, just the

internal one and has a greater significance in decision making. Management accounting helps

in making decisions related with business after planning so that a systematic procedure of

identifying, measuring, analysing, interpreting and communicating can be followed. In a

business enterprise, there are different times when management must take decisions regarding

daily business as well as some essential works.

For this purpose, they must revise and go through various reports that can impact their

decisions (Kaplan and Atkinson, 2015). Hence, management accounting report presents the

accurate information to the management so that they can come to a decision. The present

report demonstrates significance of management accounting in business environment. For

this purpose, R.L. Maynard company of UK has been chosen as a referred organisation. This

is a construction based company whose strength is 24 workers. The report contains

information about different types of income statements that a company uses along with its

benefits and drawbacks. In addition to this, various issues related to management accounting

will be addressed.

LO 1: Demonstrate an understanding of management accounting systems

P1 Explain management accounting and give the essential requirements of different types

of management accounting systems

The management accounting system is a tool which helps the organisation to keep an eye on

various types of costs and expenses that can be incurred in the production of goods and

services (Macintosh and Quattrone, 2010). In context of R.L. Maynard, the organisation has

several expenses which are necessary to be tracked so that they can have better information

regarding different costs. This will also be helpful in keeping a track of business so that they

can manage their day to day works the management accounting has the more importance in

field of business as it includes various branches of finance as well as management because of

which business enterprises can have an overall control on activities of production.

This contains wide and accurate information which makes it easier for owner of business to

have a control over business activities and take effective decisions as well. In context of cited

organisation, the top management which consists of various managers, owners and board of

directors need reports on management accounting so that they can have an overview of

different types of expenses and revenues so that they can reach to a proper decision

(Baldvinsdottir, Mitchell and Nørreklit, 2010). The management accounting report contains

different amounts discussion like cash available, sales revenues, purchases, etc. which helps

in making decisions related to the organisation. The cost accounting and the financial

accounting reports are used as a base to make the management accounting reports.

In addition to above the importance of management accounting, attempts to study those costs

which are related to the production of products and services. As per this, there are some

systems which are used under management accounting systems.

These systems are as follows:

Traditional cost accounting: This is the conventional method of accounting which

had a lot of different procedures as compared to modern accounting system. This

system is generally adopted by companies who are engaged in production sectors. For

keeping tracks related to costs, management uses job order process or costing

methods. These methods are mainly based on determining allocation of costs (Lukka

and Modell, 2010). About said firm, these allocations include different costs like

direct materials, direct labour and manufacturing expenses. The job orders are mainly

used by companies for large size projects so that wide number of expenses and

different costs related to each factor can be traced back easily. Apart from this, the

process costing refers to various costs that are related with procedures that are

undertaken to produce similar goods and services. The costs involved in this process

are difficult to identify as they are run in a continuous way.

Lean accounting: The Lean accounting is a modern concept in management

accounting which presents a very wider view in terms of considering costs. It is

evident that different accounting systems which are used in management system only

considers various costs and their calculations (Garrison and et.al., 2010). While Lean

accounting presents a different view where after taking into consideration about costs,

it also presents ways that can help in minimising costs which can lead to eliminating

wastages from production. In stated business entity, the finance department gives

financial information to the top management so that they can take decisions by

have a control over business activities and take effective decisions as well. In context of cited

organisation, the top management which consists of various managers, owners and board of

directors need reports on management accounting so that they can have an overview of

different types of expenses and revenues so that they can reach to a proper decision

(Baldvinsdottir, Mitchell and Nørreklit, 2010). The management accounting report contains

different amounts discussion like cash available, sales revenues, purchases, etc. which helps

in making decisions related to the organisation. The cost accounting and the financial

accounting reports are used as a base to make the management accounting reports.

In addition to above the importance of management accounting, attempts to study those costs

which are related to the production of products and services. As per this, there are some

systems which are used under management accounting systems.

These systems are as follows:

Traditional cost accounting: This is the conventional method of accounting which

had a lot of different procedures as compared to modern accounting system. This

system is generally adopted by companies who are engaged in production sectors. For

keeping tracks related to costs, management uses job order process or costing

methods. These methods are mainly based on determining allocation of costs (Lukka

and Modell, 2010). About said firm, these allocations include different costs like

direct materials, direct labour and manufacturing expenses. The job orders are mainly

used by companies for large size projects so that wide number of expenses and

different costs related to each factor can be traced back easily. Apart from this, the

process costing refers to various costs that are related with procedures that are

undertaken to produce similar goods and services. The costs involved in this process

are difficult to identify as they are run in a continuous way.

Lean accounting: The Lean accounting is a modern concept in management

accounting which presents a very wider view in terms of considering costs. It is

evident that different accounting systems which are used in management system only

considers various costs and their calculations (Garrison and et.al., 2010). While Lean

accounting presents a different view where after taking into consideration about costs,

it also presents ways that can help in minimising costs which can lead to eliminating

wastages from production. In stated business entity, the finance department gives

financial information to the top management so that they can take decisions by

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

measuring the profitability. However, they also make efforts which can aid in

elimination of costs that are proving to be of wastes by using given information.

Throughput accounting: Generally, the throughput accounting system is not seen as

individual accounting process and taken into traditional system. The major purpose of

this system is to determine different constraints that are acting as a barrier in

production system of company (What are the different types of management

accounting systems? 2017). In cited organisation, this system is used at a broad level

so that deficiency of any material, labour or other facilities can be ascertained as early

as possible. This helps in reduction of these constraints so that they can be removed

and throughputs can be increased for enhancing production capacity. This results in

reduction of costs of product.

Transfer pricing: The transfer pricing method includes various costs which are added

because of movement of good through each department and process. Thus, on each

stage, small portion of costs are added to the products which eventually gives benefit

to the organisation (Van der Stede, 2011). The calculation of transfer pricing is done

by including the expenditures that incurred for transferring the goods.

P2 Explain different methods used for management accounting reporting.

Job cost reports: The job costs report is a significant accounting report which are

maintained by organisation so that they can have an information about position of

firm in context of profits and losses. In addition to this, it is an internal report which

are required by the top management so that they can take decisions regarding

modifications. These decisions regarding alterations are taken based on present

condition of firm as expenses and revenues can be adjusted in efficient manner. These

reports also act as a monitoring work in which each job's cost is studied and further

planning is done accordingly.

Sales report: The sales report gives information about the sales of company as per a

specific time. This report is essential in taking a decision for top level management as

any increase or decrease in the sales units can have a considerable impact (Pipan and

Czarniawska, 2010). The sales report gives a detailed information regarding the

increase or decrease in organisation's sales for a period along with its causes. Any

positive changes in the sales are studied and continued for maintaining the current

elimination of costs that are proving to be of wastes by using given information.

Throughput accounting: Generally, the throughput accounting system is not seen as

individual accounting process and taken into traditional system. The major purpose of

this system is to determine different constraints that are acting as a barrier in

production system of company (What are the different types of management

accounting systems? 2017). In cited organisation, this system is used at a broad level

so that deficiency of any material, labour or other facilities can be ascertained as early

as possible. This helps in reduction of these constraints so that they can be removed

and throughputs can be increased for enhancing production capacity. This results in

reduction of costs of product.

Transfer pricing: The transfer pricing method includes various costs which are added

because of movement of good through each department and process. Thus, on each

stage, small portion of costs are added to the products which eventually gives benefit

to the organisation (Van der Stede, 2011). The calculation of transfer pricing is done

by including the expenditures that incurred for transferring the goods.

P2 Explain different methods used for management accounting reporting.

Job cost reports: The job costs report is a significant accounting report which are

maintained by organisation so that they can have an information about position of

firm in context of profits and losses. In addition to this, it is an internal report which

are required by the top management so that they can take decisions regarding

modifications. These decisions regarding alterations are taken based on present

condition of firm as expenses and revenues can be adjusted in efficient manner. These

reports also act as a monitoring work in which each job's cost is studied and further

planning is done accordingly.

Sales report: The sales report gives information about the sales of company as per a

specific time. This report is essential in taking a decision for top level management as

any increase or decrease in the sales units can have a considerable impact (Pipan and

Czarniawska, 2010). The sales report gives a detailed information regarding the

increase or decrease in organisation's sales for a period along with its causes. Any

positive changes in the sales are studied and continued for maintaining the current

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

level. While the decrease in a sales and productions are studied so that necessary

improvements can be done. By having a report on sales figures, the company can

match its revenues earned in that specific time so that a right status of organisation

can be determined.

Cost accounting: The cost accounting presents a report which consists of various

types of costs that are incurred by said company. This report helps in making various

decisions which are useful in making changes in the cost structures. These changes

can help in attaining minimum cost of operations for company. This accounting report

also gives information about the company's performance as well as transfer pricing,

variance and standard costing which are used by internal management to take

significant information related to firm (Weißenberger and Angelkort, 2011).

Budgetary report: The budgets are the basic requirement for any firm which includes

information about planning that is done by companies for allocation of funds. The

budgetary report includes planning in which management makes the standards for

performance as well as determine targets that are to be achieved by employees in a

particular period. Thus, the management takes decision after comparing the actual

results with planned ones based on which action plans are made if required. The

deviations occurring in results are attempted to remove with the help of corrective

measures. The budgets made in initial stages also help in keeping the cash outflow of

firm in control as due to strict budget, any unproductive investments can be avoided.

improvements can be done. By having a report on sales figures, the company can

match its revenues earned in that specific time so that a right status of organisation

can be determined.

Cost accounting: The cost accounting presents a report which consists of various

types of costs that are incurred by said company. This report helps in making various

decisions which are useful in making changes in the cost structures. These changes

can help in attaining minimum cost of operations for company. This accounting report

also gives information about the company's performance as well as transfer pricing,

variance and standard costing which are used by internal management to take

significant information related to firm (Weißenberger and Angelkort, 2011).

Budgetary report: The budgets are the basic requirement for any firm which includes

information about planning that is done by companies for allocation of funds. The

budgetary report includes planning in which management makes the standards for

performance as well as determine targets that are to be achieved by employees in a

particular period. Thus, the management takes decision after comparing the actual

results with planned ones based on which action plans are made if required. The

deviations occurring in results are attempted to remove with the help of corrective

measures. The budgets made in initial stages also help in keeping the cash outflow of

firm in control as due to strict budget, any unproductive investments can be avoided.

LO 2: Apply a range of management accounting techniques

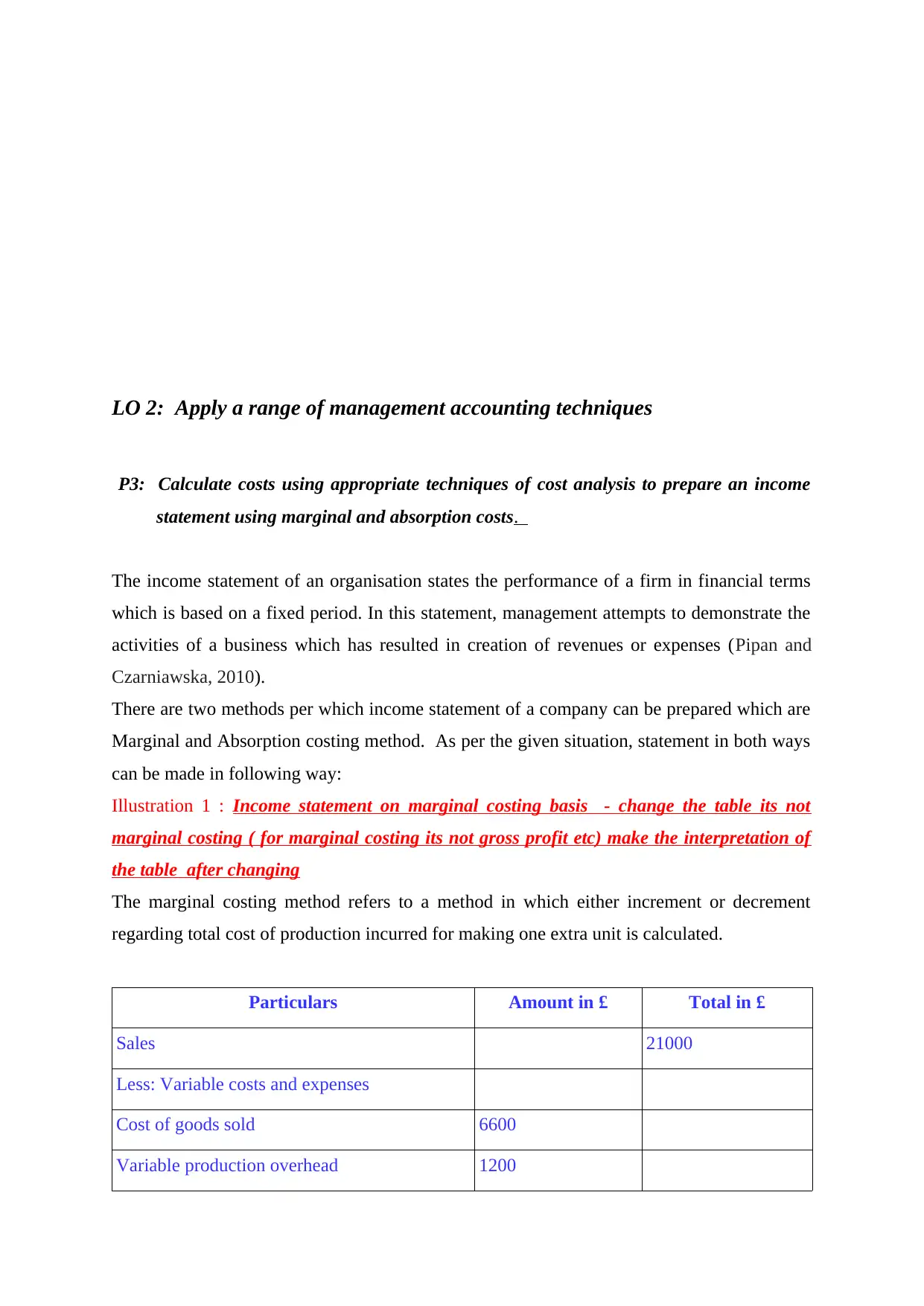

P3: Calculate costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs.

The income statement of an organisation states the performance of a firm in financial terms

which is based on a fixed period. In this statement, management attempts to demonstrate the

activities of a business which has resulted in creation of revenues or expenses (Pipan and

Czarniawska, 2010).

There are two methods per which income statement of a company can be prepared which are

Marginal and Absorption costing method. As per the given situation, statement in both ways

can be made in following way:

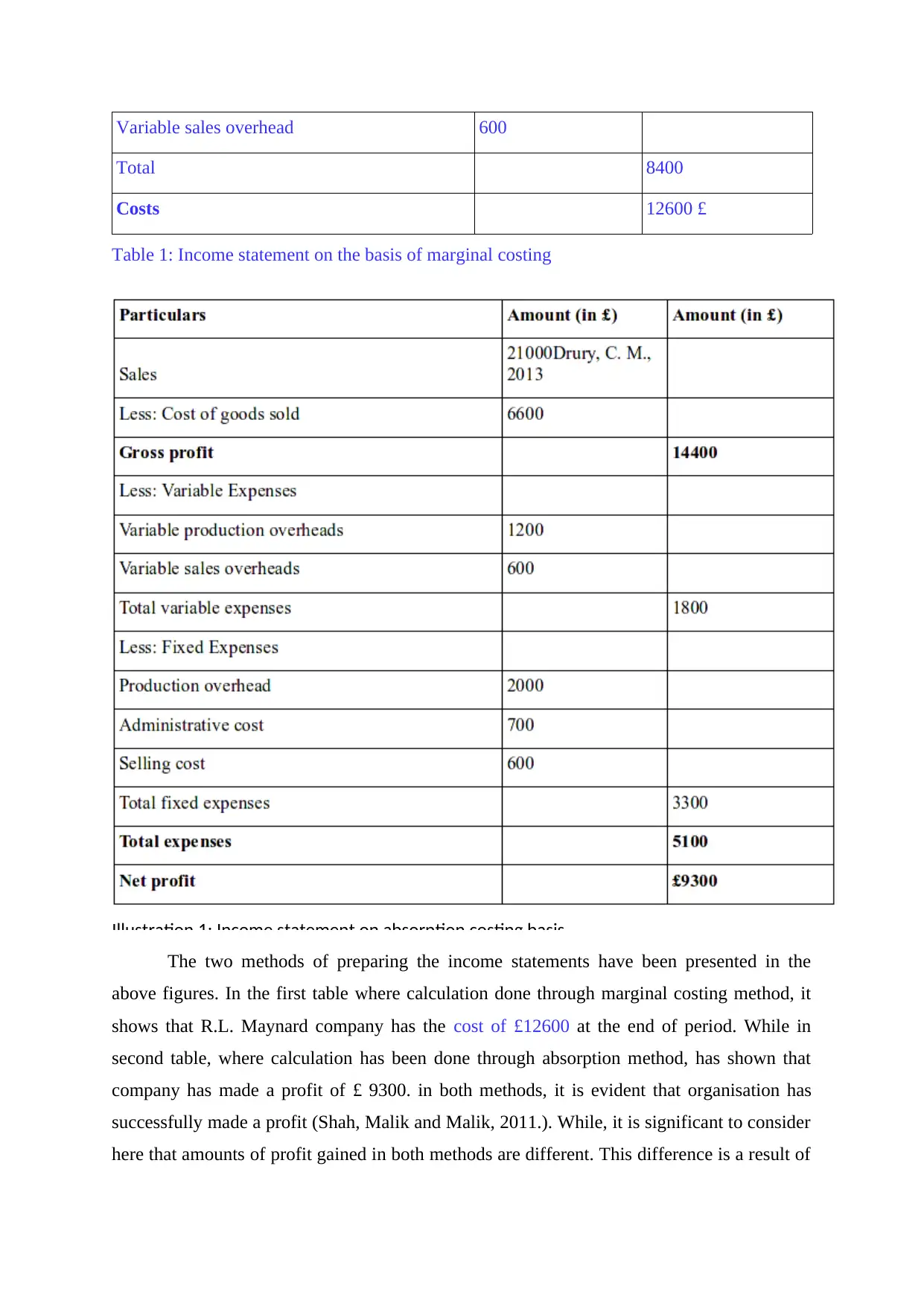

Illustration 1 : Income statement on marginal costing basis - change the table its not

marginal costing ( for marginal costing its not gross profit etc) make the interpretation of

the table after changing

The marginal costing method refers to a method in which either increment or decrement

regarding total cost of production incurred for making one extra unit is calculated.

Particulars Amount in £ Total in £

Sales 21000

Less: Variable costs and expenses

Cost of goods sold 6600

Variable production overhead 1200

P3: Calculate costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs.

The income statement of an organisation states the performance of a firm in financial terms

which is based on a fixed period. In this statement, management attempts to demonstrate the

activities of a business which has resulted in creation of revenues or expenses (Pipan and

Czarniawska, 2010).

There are two methods per which income statement of a company can be prepared which are

Marginal and Absorption costing method. As per the given situation, statement in both ways

can be made in following way:

Illustration 1 : Income statement on marginal costing basis - change the table its not

marginal costing ( for marginal costing its not gross profit etc) make the interpretation of

the table after changing

The marginal costing method refers to a method in which either increment or decrement

regarding total cost of production incurred for making one extra unit is calculated.

Particulars Amount in £ Total in £

Sales 21000

Less: Variable costs and expenses

Cost of goods sold 6600

Variable production overhead 1200

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Variable sales overhead 600

Total 8400

Costs 12600 £

Table 1: Income statement on the basis of marginal costing

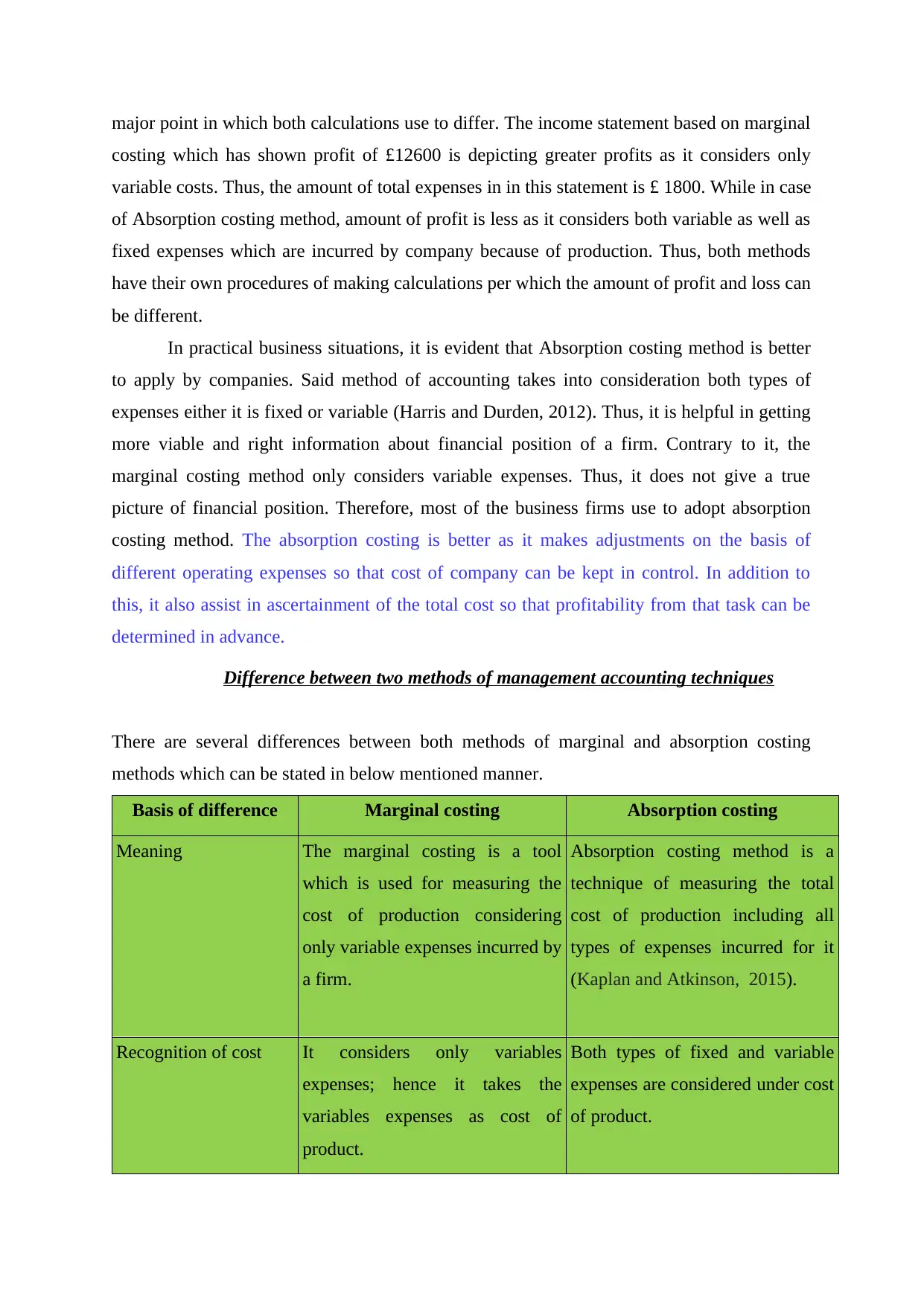

Illustration 1: Income statement on absorption costing basis

The two methods of preparing the income statements have been presented in the

above figures. In the first table where calculation done through marginal costing method, it

shows that R.L. Maynard company has the cost of £12600 at the end of period. While in

second table, where calculation has been done through absorption method, has shown that

company has made a profit of £ 9300. in both methods, it is evident that organisation has

successfully made a profit (Shah, Malik and Malik, 2011.). While, it is significant to consider

here that amounts of profit gained in both methods are different. This difference is a result of

Total 8400

Costs 12600 £

Table 1: Income statement on the basis of marginal costing

Illustration 1: Income statement on absorption costing basis

The two methods of preparing the income statements have been presented in the

above figures. In the first table where calculation done through marginal costing method, it

shows that R.L. Maynard company has the cost of £12600 at the end of period. While in

second table, where calculation has been done through absorption method, has shown that

company has made a profit of £ 9300. in both methods, it is evident that organisation has

successfully made a profit (Shah, Malik and Malik, 2011.). While, it is significant to consider

here that amounts of profit gained in both methods are different. This difference is a result of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

major point in which both calculations use to differ. The income statement based on marginal

costing which has shown profit of £12600 is depicting greater profits as it considers only

variable costs. Thus, the amount of total expenses in in this statement is £ 1800. While in case

of Absorption costing method, amount of profit is less as it considers both variable as well as

fixed expenses which are incurred by company because of production. Thus, both methods

have their own procedures of making calculations per which the amount of profit and loss can

be different.

In practical business situations, it is evident that Absorption costing method is better

to apply by companies. Said method of accounting takes into consideration both types of

expenses either it is fixed or variable (Harris and Durden, 2012). Thus, it is helpful in getting

more viable and right information about financial position of a firm. Contrary to it, the

marginal costing method only considers variable expenses. Thus, it does not give a true

picture of financial position. Therefore, most of the business firms use to adopt absorption

costing method. The absorption costing is better as it makes adjustments on the basis of

different operating expenses so that cost of company can be kept in control. In addition to

this, it also assist in ascertainment of the total cost so that profitability from that task can be

determined in advance.

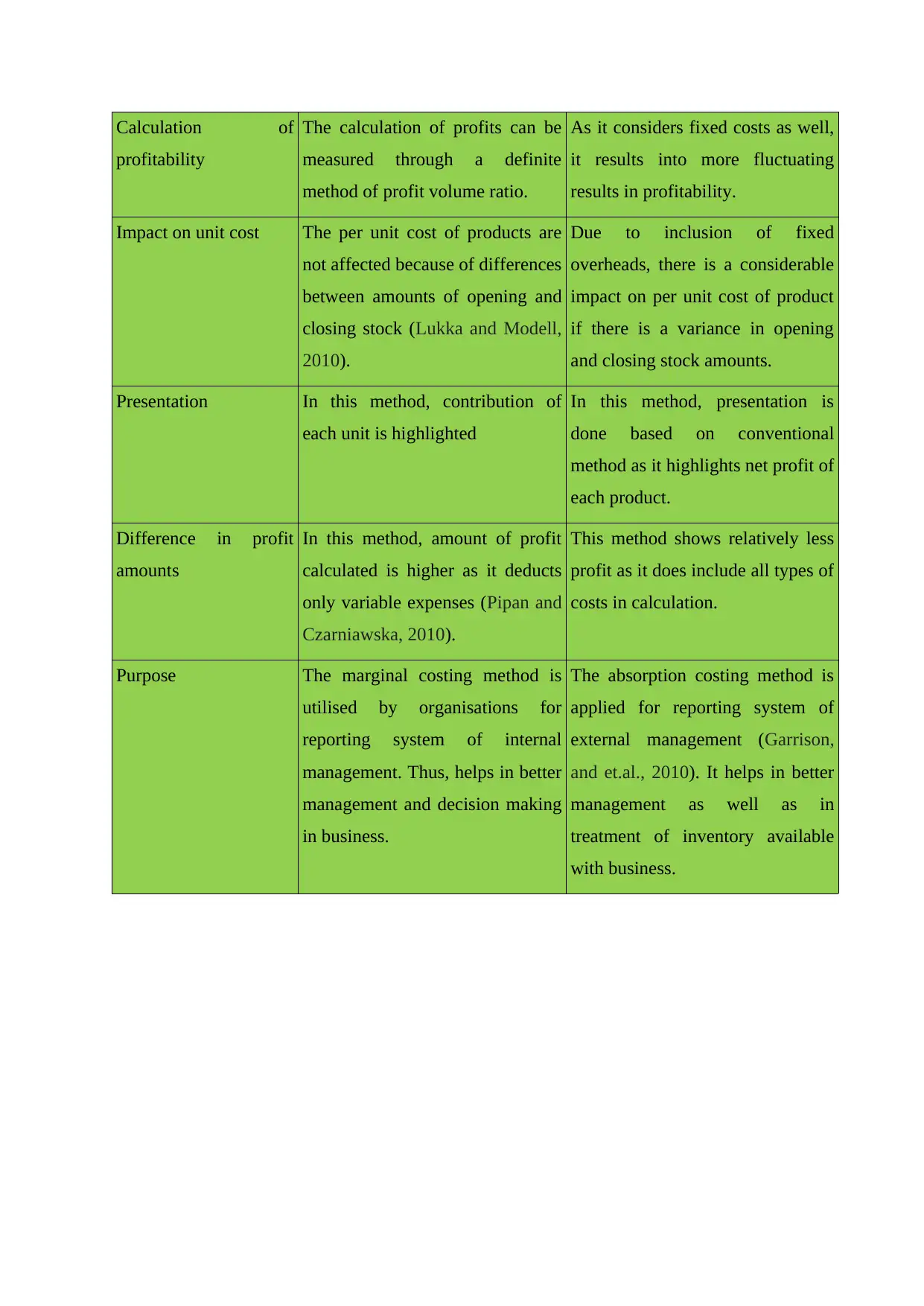

Difference between two methods of management accounting techniques

There are several differences between both methods of marginal and absorption costing

methods which can be stated in below mentioned manner.

Basis of difference Marginal costing Absorption costing

Meaning The marginal costing is a tool

which is used for measuring the

cost of production considering

only variable expenses incurred by

a firm.

Absorption costing method is a

technique of measuring the total

cost of production including all

types of expenses incurred for it

(Kaplan and Atkinson, 2015).

Recognition of cost It considers only variables

expenses; hence it takes the

variables expenses as cost of

product.

Both types of fixed and variable

expenses are considered under cost

of product.

costing which has shown profit of £12600 is depicting greater profits as it considers only

variable costs. Thus, the amount of total expenses in in this statement is £ 1800. While in case

of Absorption costing method, amount of profit is less as it considers both variable as well as

fixed expenses which are incurred by company because of production. Thus, both methods

have their own procedures of making calculations per which the amount of profit and loss can

be different.

In practical business situations, it is evident that Absorption costing method is better

to apply by companies. Said method of accounting takes into consideration both types of

expenses either it is fixed or variable (Harris and Durden, 2012). Thus, it is helpful in getting

more viable and right information about financial position of a firm. Contrary to it, the

marginal costing method only considers variable expenses. Thus, it does not give a true

picture of financial position. Therefore, most of the business firms use to adopt absorption

costing method. The absorption costing is better as it makes adjustments on the basis of

different operating expenses so that cost of company can be kept in control. In addition to

this, it also assist in ascertainment of the total cost so that profitability from that task can be

determined in advance.

Difference between two methods of management accounting techniques

There are several differences between both methods of marginal and absorption costing

methods which can be stated in below mentioned manner.

Basis of difference Marginal costing Absorption costing

Meaning The marginal costing is a tool

which is used for measuring the

cost of production considering

only variable expenses incurred by

a firm.

Absorption costing method is a

technique of measuring the total

cost of production including all

types of expenses incurred for it

(Kaplan and Atkinson, 2015).

Recognition of cost It considers only variables

expenses; hence it takes the

variables expenses as cost of

product.

Both types of fixed and variable

expenses are considered under cost

of product.

Calculation of

profitability

The calculation of profits can be

measured through a definite

method of profit volume ratio.

As it considers fixed costs as well,

it results into more fluctuating

results in profitability.

Impact on unit cost The per unit cost of products are

not affected because of differences

between amounts of opening and

closing stock (Lukka and Modell,

2010).

Due to inclusion of fixed

overheads, there is a considerable

impact on per unit cost of product

if there is a variance in opening

and closing stock amounts.

Presentation In this method, contribution of

each unit is highlighted

In this method, presentation is

done based on conventional

method as it highlights net profit of

each product.

Difference in profit

amounts

In this method, amount of profit

calculated is higher as it deducts

only variable expenses (Pipan and

Czarniawska, 2010).

This method shows relatively less

profit as it does include all types of

costs in calculation.

Purpose The marginal costing method is

utilised by organisations for

reporting system of internal

management. Thus, helps in better

management and decision making

in business.

The absorption costing method is

applied for reporting system of

external management (Garrison,

and et.al., 2010). It helps in better

management as well as in

treatment of inventory available

with business.

profitability

The calculation of profits can be

measured through a definite

method of profit volume ratio.

As it considers fixed costs as well,

it results into more fluctuating

results in profitability.

Impact on unit cost The per unit cost of products are

not affected because of differences

between amounts of opening and

closing stock (Lukka and Modell,

2010).

Due to inclusion of fixed

overheads, there is a considerable

impact on per unit cost of product

if there is a variance in opening

and closing stock amounts.

Presentation In this method, contribution of

each unit is highlighted

In this method, presentation is

done based on conventional

method as it highlights net profit of

each product.

Difference in profit

amounts

In this method, amount of profit

calculated is higher as it deducts

only variable expenses (Pipan and

Czarniawska, 2010).

This method shows relatively less

profit as it does include all types of

costs in calculation.

Purpose The marginal costing method is

utilised by organisations for

reporting system of internal

management. Thus, helps in better

management and decision making

in business.

The absorption costing method is

applied for reporting system of

external management (Garrison,

and et.al., 2010). It helps in better

management as well as in

treatment of inventory available

with business.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.