Mercury Inc. Management Accounting: Case Studies and Solutions

VerifiedAdded on 2023/06/13

|18

|3877

|288

Report

AI Summary

This assignment is a management accounting report for Mercury Inc., addressing various case studies within the company. It covers manufacturing cost flows, international issues in management accounting (specifically concerning Australian dairy products in China), comprehensive budgeting, cost concepts, and strategic management accounting. The report includes an ethics case study and provides advice and recommended actions. Numerical analysis such as cost of goods manufactured and sold schedules, income statements, and NPV calculations are presented. The report assesses the advantages and disadvantages of projects and recommends whether to accept them based on NPV and other factors. Desklib offers similar solved assignments and past papers for students.

MANAGEMENT ACCOUNTING

Management accounting

Name of the student

Name of the university

Student ID

Author note

Management accounting

Name of the student

Name of the university

Student ID

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1MANAGEMENT ACCOUNTING

Table of Contents

Question 1..................................................................................................................................2

Manufacturing cost flows.......................................................................................................2

Question 2..................................................................................................................................3

International issues in management account..........................................................................3

(i) Advantage of Australian dairy product in China............................................................3

(ii) Difference in western and Chinese approaches of management accounting..............4

(iii) Concepts of Guanxi and power distance.....................................................................4

Question 3..................................................................................................................................5

Comprehensive manufacturing budget..................................................................................5

(a) Five year budget..........................................................................................................5

(b) Increased production constraint...................................................................................7

(c) Report to CEO.............................................................................................................7

Question 4..................................................................................................................................8

(i) Distinguish between variable cost and fixed cost and product cost and period cost......8

(ii) Relevant range...........................................................................................................10

Question 5................................................................................................................................10

Strategic Management Accounting case study....................................................................10

(i) Before and after budget comparison.............................................................................10

(ii) Drop in sales for the competitor Death Star manufacturing......................................11

(iii) Report........................................................................................................................12

Table of Contents

Question 1..................................................................................................................................2

Manufacturing cost flows.......................................................................................................2

Question 2..................................................................................................................................3

International issues in management account..........................................................................3

(i) Advantage of Australian dairy product in China............................................................3

(ii) Difference in western and Chinese approaches of management accounting..............4

(iii) Concepts of Guanxi and power distance.....................................................................4

Question 3..................................................................................................................................5

Comprehensive manufacturing budget..................................................................................5

(a) Five year budget..........................................................................................................5

(b) Increased production constraint...................................................................................7

(c) Report to CEO.............................................................................................................7

Question 4..................................................................................................................................8

(i) Distinguish between variable cost and fixed cost and product cost and period cost......8

(ii) Relevant range...........................................................................................................10

Question 5................................................................................................................................10

Strategic Management Accounting case study....................................................................10

(i) Before and after budget comparison.............................................................................10

(ii) Drop in sales for the competitor Death Star manufacturing......................................11

(iii) Report........................................................................................................................12

2MANAGEMENT ACCOUNTING

Question 5................................................................................................................................12

Ethics case study..................................................................................................................12

(i) Advice to Burdon..........................................................................................................12

(ii) Recommended actions for Burdon............................................................................13

Reference..................................................................................................................................14

Question 5................................................................................................................................12

Ethics case study..................................................................................................................12

(i) Advice to Burdon..........................................................................................................12

(ii) Recommended actions for Burdon............................................................................13

Reference..................................................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3MANAGEMENT ACCOUNTING

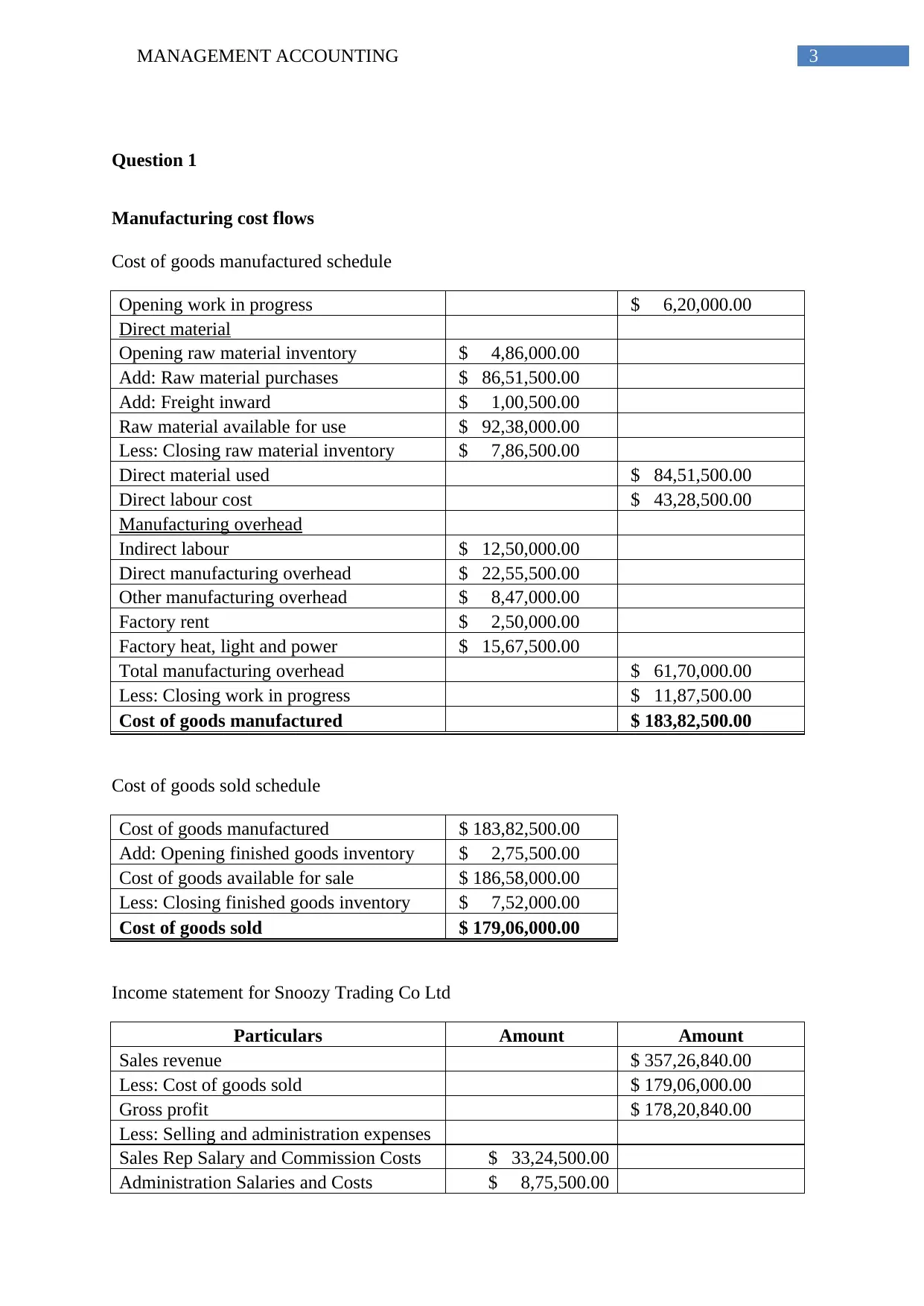

Question 1

Manufacturing cost flows

Cost of goods manufactured schedule

Opening work in progress $ 6,20,000.00

Direct material

Opening raw material inventory $ 4,86,000.00

Add: Raw material purchases $ 86,51,500.00

Add: Freight inward $ 1,00,500.00

Raw material available for use $ 92,38,000.00

Less: Closing raw material inventory $ 7,86,500.00

Direct material used $ 84,51,500.00

Direct labour cost $ 43,28,500.00

Manufacturing overhead

Indirect labour $ 12,50,000.00

Direct manufacturing overhead $ 22,55,500.00

Other manufacturing overhead $ 8,47,000.00

Factory rent $ 2,50,000.00

Factory heat, light and power $ 15,67,500.00

Total manufacturing overhead $ 61,70,000.00

Less: Closing work in progress $ 11,87,500.00

Cost of goods manufactured $ 183,82,500.00

Cost of goods sold schedule

Cost of goods manufactured $ 183,82,500.00

Add: Opening finished goods inventory $ 2,75,500.00

Cost of goods available for sale $ 186,58,000.00

Less: Closing finished goods inventory $ 7,52,000.00

Cost of goods sold $ 179,06,000.00

Income statement for Snoozy Trading Co Ltd

Particulars Amount Amount

Sales revenue $ 357,26,840.00

Less: Cost of goods sold $ 179,06,000.00

Gross profit $ 178,20,840.00

Less: Selling and administration expenses

Sales Rep Salary and Commission Costs $ 33,24,500.00

Administration Salaries and Costs $ 8,75,500.00

Question 1

Manufacturing cost flows

Cost of goods manufactured schedule

Opening work in progress $ 6,20,000.00

Direct material

Opening raw material inventory $ 4,86,000.00

Add: Raw material purchases $ 86,51,500.00

Add: Freight inward $ 1,00,500.00

Raw material available for use $ 92,38,000.00

Less: Closing raw material inventory $ 7,86,500.00

Direct material used $ 84,51,500.00

Direct labour cost $ 43,28,500.00

Manufacturing overhead

Indirect labour $ 12,50,000.00

Direct manufacturing overhead $ 22,55,500.00

Other manufacturing overhead $ 8,47,000.00

Factory rent $ 2,50,000.00

Factory heat, light and power $ 15,67,500.00

Total manufacturing overhead $ 61,70,000.00

Less: Closing work in progress $ 11,87,500.00

Cost of goods manufactured $ 183,82,500.00

Cost of goods sold schedule

Cost of goods manufactured $ 183,82,500.00

Add: Opening finished goods inventory $ 2,75,500.00

Cost of goods available for sale $ 186,58,000.00

Less: Closing finished goods inventory $ 7,52,000.00

Cost of goods sold $ 179,06,000.00

Income statement for Snoozy Trading Co Ltd

Particulars Amount Amount

Sales revenue $ 357,26,840.00

Less: Cost of goods sold $ 179,06,000.00

Gross profit $ 178,20,840.00

Less: Selling and administration expenses

Sales Rep Salary and Commission Costs $ 33,24,500.00

Administration Salaries and Costs $ 8,75,500.00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4MANAGEMENT ACCOUNTING

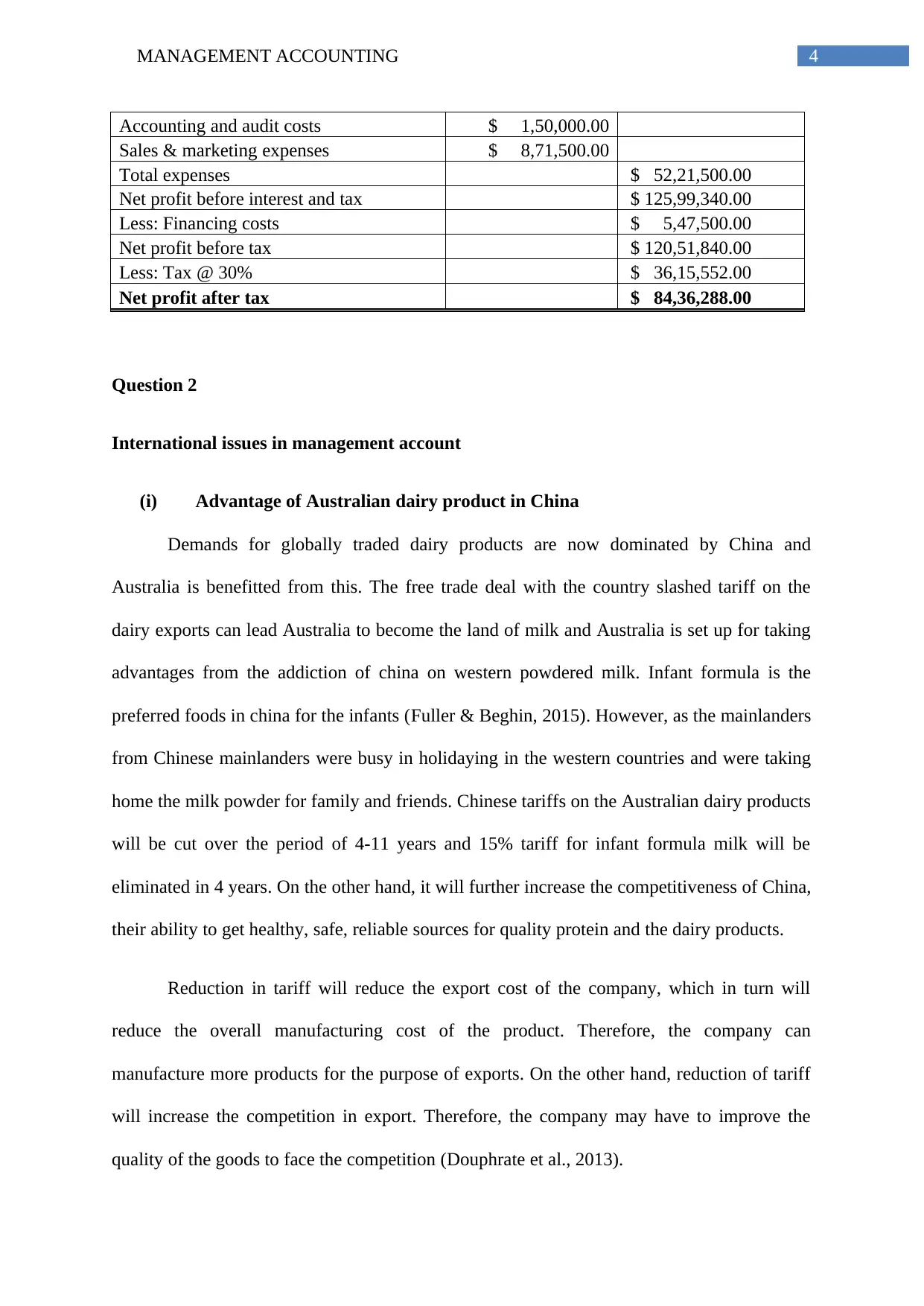

Accounting and audit costs $ 1,50,000.00

Sales & marketing expenses $ 8,71,500.00

Total expenses $ 52,21,500.00

Net profit before interest and tax $ 125,99,340.00

Less: Financing costs $ 5,47,500.00

Net profit before tax $ 120,51,840.00

Less: Tax @ 30% $ 36,15,552.00

Net profit after tax $ 84,36,288.00

Question 2

International issues in management account

(i) Advantage of Australian dairy product in China

Demands for globally traded dairy products are now dominated by China and

Australia is benefitted from this. The free trade deal with the country slashed tariff on the

dairy exports can lead Australia to become the land of milk and Australia is set up for taking

advantages from the addiction of china on western powdered milk. Infant formula is the

preferred foods in china for the infants (Fuller & Beghin, 2015). However, as the mainlanders

from Chinese mainlanders were busy in holidaying in the western countries and were taking

home the milk powder for family and friends. Chinese tariffs on the Australian dairy products

will be cut over the period of 4-11 years and 15% tariff for infant formula milk will be

eliminated in 4 years. On the other hand, it will further increase the competitiveness of China,

their ability to get healthy, safe, reliable sources for quality protein and the dairy products.

Reduction in tariff will reduce the export cost of the company, which in turn will

reduce the overall manufacturing cost of the product. Therefore, the company can

manufacture more products for the purpose of exports. On the other hand, reduction of tariff

will increase the competition in export. Therefore, the company may have to improve the

quality of the goods to face the competition (Douphrate et al., 2013).

Accounting and audit costs $ 1,50,000.00

Sales & marketing expenses $ 8,71,500.00

Total expenses $ 52,21,500.00

Net profit before interest and tax $ 125,99,340.00

Less: Financing costs $ 5,47,500.00

Net profit before tax $ 120,51,840.00

Less: Tax @ 30% $ 36,15,552.00

Net profit after tax $ 84,36,288.00

Question 2

International issues in management account

(i) Advantage of Australian dairy product in China

Demands for globally traded dairy products are now dominated by China and

Australia is benefitted from this. The free trade deal with the country slashed tariff on the

dairy exports can lead Australia to become the land of milk and Australia is set up for taking

advantages from the addiction of china on western powdered milk. Infant formula is the

preferred foods in china for the infants (Fuller & Beghin, 2015). However, as the mainlanders

from Chinese mainlanders were busy in holidaying in the western countries and were taking

home the milk powder for family and friends. Chinese tariffs on the Australian dairy products

will be cut over the period of 4-11 years and 15% tariff for infant formula milk will be

eliminated in 4 years. On the other hand, it will further increase the competitiveness of China,

their ability to get healthy, safe, reliable sources for quality protein and the dairy products.

Reduction in tariff will reduce the export cost of the company, which in turn will

reduce the overall manufacturing cost of the product. Therefore, the company can

manufacture more products for the purpose of exports. On the other hand, reduction of tariff

will increase the competition in export. Therefore, the company may have to improve the

quality of the goods to face the competition (Douphrate et al., 2013).

5MANAGEMENT ACCOUNTING

(ii) Difference in western and Chinese approaches of management accounting

The accounting profession for China is headed by Law of People’s Republic of China

on the Certified Public Accounts. China does not follow the international accounting

guidelines and policies. However, they are moving to the direction with the accession to

World Trade Organization that will be fully complied within few years. As the Chinese

government implemented the reform and opened up various policies during 1978, various

western concepts of management accounting and techniques are introduced in China. The

main issues with implementation of the western methods are not the political sensitivity

issues, but the issues are technical constraints. While essential data for MIS is developed in

Chinese companies for usage of the western techniques like Activity Based costing, it is not

possible to collect the data easily under the present situation (Hu, Chand & Evans, 2013).

Moreover, the changes in the management accounting can be experienced in few areas like

promotion of the products, profitability and usage of responsibility accounting as major

criteria for choosing investment projects. Further, the Chinese are generally comfortable with

grey areas and not with the black and white areas of the business. Learning these navigations

requires patients and observance. Taking time for understanding Chinese way is rewarding in

professional as well as personal ways (Hilton & Platt, 2013).

(iii) Concepts of Guanxi and power distance

Guanxi is based on the concepts of loyalty, reciprocity, trust and dedication that helps

in developing the non-familial and interpersonal relations and mirroring concepts of filial

piety that is used for ground level familial relations. Eventually the relationships established

by guanxi are not transferrable and personal (Kaynak, Wong & Leung, 2013).

On the other hand, power distance is the way in which the power is unequally

allocated. In simple words, people from some cultures accept the higher degree of the power

that is unequally distributed as compared to the people from other cultures (Sriramesh, 2013).

(ii) Difference in western and Chinese approaches of management accounting

The accounting profession for China is headed by Law of People’s Republic of China

on the Certified Public Accounts. China does not follow the international accounting

guidelines and policies. However, they are moving to the direction with the accession to

World Trade Organization that will be fully complied within few years. As the Chinese

government implemented the reform and opened up various policies during 1978, various

western concepts of management accounting and techniques are introduced in China. The

main issues with implementation of the western methods are not the political sensitivity

issues, but the issues are technical constraints. While essential data for MIS is developed in

Chinese companies for usage of the western techniques like Activity Based costing, it is not

possible to collect the data easily under the present situation (Hu, Chand & Evans, 2013).

Moreover, the changes in the management accounting can be experienced in few areas like

promotion of the products, profitability and usage of responsibility accounting as major

criteria for choosing investment projects. Further, the Chinese are generally comfortable with

grey areas and not with the black and white areas of the business. Learning these navigations

requires patients and observance. Taking time for understanding Chinese way is rewarding in

professional as well as personal ways (Hilton & Platt, 2013).

(iii) Concepts of Guanxi and power distance

Guanxi is based on the concepts of loyalty, reciprocity, trust and dedication that helps

in developing the non-familial and interpersonal relations and mirroring concepts of filial

piety that is used for ground level familial relations. Eventually the relationships established

by guanxi are not transferrable and personal (Kaynak, Wong & Leung, 2013).

On the other hand, power distance is the way in which the power is unequally

allocated. In simple words, people from some cultures accept the higher degree of the power

that is unequally distributed as compared to the people from other cultures (Sriramesh, 2013).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6MANAGEMENT ACCOUNTING

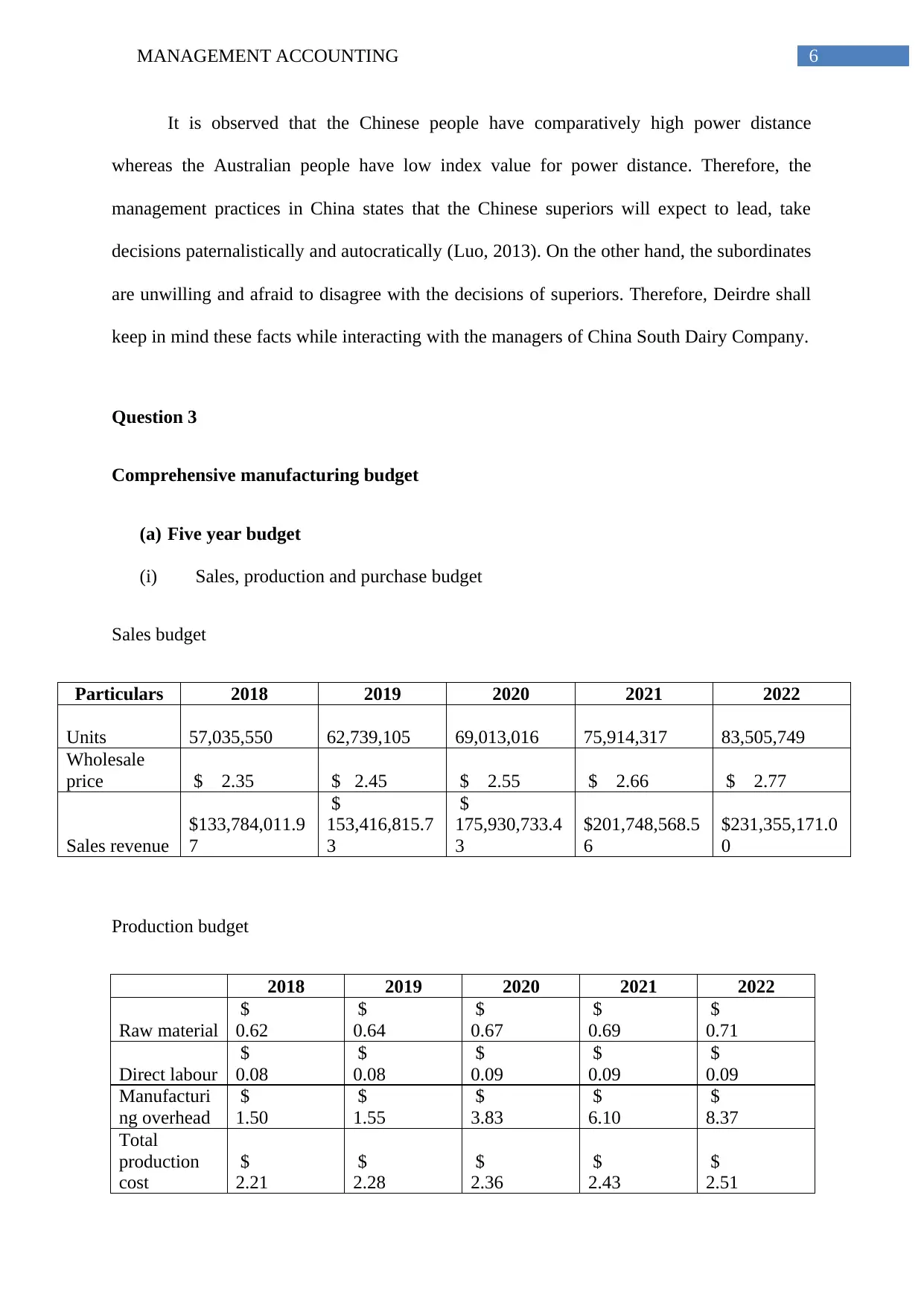

It is observed that the Chinese people have comparatively high power distance

whereas the Australian people have low index value for power distance. Therefore, the

management practices in China states that the Chinese superiors will expect to lead, take

decisions paternalistically and autocratically (Luo, 2013). On the other hand, the subordinates

are unwilling and afraid to disagree with the decisions of superiors. Therefore, Deirdre shall

keep in mind these facts while interacting with the managers of China South Dairy Company.

Question 3

Comprehensive manufacturing budget

(a) Five year budget

(i) Sales, production and purchase budget

Sales budget

Particulars 2018 2019 2020 2021 2022

Units 57,035,550 62,739,105 69,013,016 75,914,317 83,505,749

Wholesale

price $ 2.35 $ 2.45 $ 2.55 $ 2.66 $ 2.77

Sales revenue

$133,784,011.9

7

$

153,416,815.7

3

$

175,930,733.4

3

$201,748,568.5

6

$231,355,171.0

0

Production budget

2018 2019 2020 2021 2022

Raw material

$

0.62

$

0.64

$

0.67

$

0.69

$

0.71

Direct labour

$

0.08

$

0.08

$

0.09

$

0.09

$

0.09

Manufacturi

ng overhead

$

1.50

$

1.55

$

3.83

$

6.10

$

8.37

Total

production

cost

$

2.21

$

2.28

$

2.36

$

2.43

$

2.51

It is observed that the Chinese people have comparatively high power distance

whereas the Australian people have low index value for power distance. Therefore, the

management practices in China states that the Chinese superiors will expect to lead, take

decisions paternalistically and autocratically (Luo, 2013). On the other hand, the subordinates

are unwilling and afraid to disagree with the decisions of superiors. Therefore, Deirdre shall

keep in mind these facts while interacting with the managers of China South Dairy Company.

Question 3

Comprehensive manufacturing budget

(a) Five year budget

(i) Sales, production and purchase budget

Sales budget

Particulars 2018 2019 2020 2021 2022

Units 57,035,550 62,739,105 69,013,016 75,914,317 83,505,749

Wholesale

price $ 2.35 $ 2.45 $ 2.55 $ 2.66 $ 2.77

Sales revenue

$133,784,011.9

7

$

153,416,815.7

3

$

175,930,733.4

3

$201,748,568.5

6

$231,355,171.0

0

Production budget

2018 2019 2020 2021 2022

Raw material

$

0.62

$

0.64

$

0.67

$

0.69

$

0.71

Direct labour

$

0.08

$

0.08

$

0.09

$

0.09

$

0.09

Manufacturi

ng overhead

$

1.50

$

1.55

$

3.83

$

6.10

$

8.37

Total

production

cost

$

2.21

$

2.28

$

2.36

$

2.43

$

2.51

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MANAGEMENT ACCOUNTING

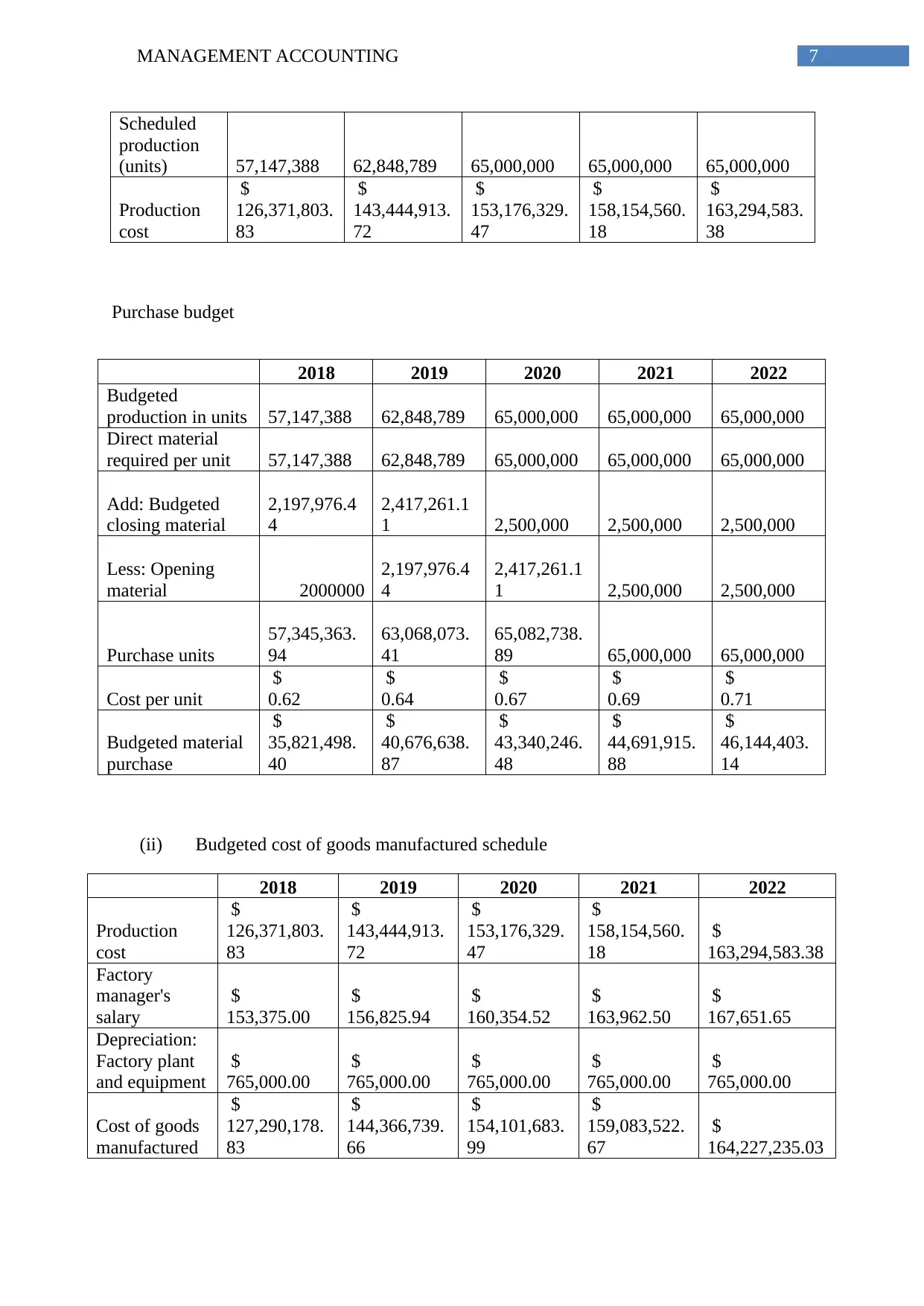

Scheduled

production

(units) 57,147,388 62,848,789 65,000,000 65,000,000 65,000,000

Production

cost

$

126,371,803.

83

$

143,444,913.

72

$

153,176,329.

47

$

158,154,560.

18

$

163,294,583.

38

Purchase budget

2018 2019 2020 2021 2022

Budgeted

production in units 57,147,388 62,848,789 65,000,000 65,000,000 65,000,000

Direct material

required per unit 57,147,388 62,848,789 65,000,000 65,000,000 65,000,000

Add: Budgeted

closing material

2,197,976.4

4

2,417,261.1

1 2,500,000 2,500,000 2,500,000

Less: Opening

material 2000000

2,197,976.4

4

2,417,261.1

1 2,500,000 2,500,000

Purchase units

57,345,363.

94

63,068,073.

41

65,082,738.

89 65,000,000 65,000,000

Cost per unit

$

0.62

$

0.64

$

0.67

$

0.69

$

0.71

Budgeted material

purchase

$

35,821,498.

40

$

40,676,638.

87

$

43,340,246.

48

$

44,691,915.

88

$

46,144,403.

14

(ii) Budgeted cost of goods manufactured schedule

2018 2019 2020 2021 2022

Production

cost

$

126,371,803.

83

$

143,444,913.

72

$

153,176,329.

47

$

158,154,560.

18

$

163,294,583.38

Factory

manager's

salary

$

153,375.00

$

156,825.94

$

160,354.52

$

163,962.50

$

167,651.65

Depreciation:

Factory plant

and equipment

$

765,000.00

$

765,000.00

$

765,000.00

$

765,000.00

$

765,000.00

Cost of goods

manufactured

$

127,290,178.

83

$

144,366,739.

66

$

154,101,683.

99

$

159,083,522.

67

$

164,227,235.03

Scheduled

production

(units) 57,147,388 62,848,789 65,000,000 65,000,000 65,000,000

Production

cost

$

126,371,803.

83

$

143,444,913.

72

$

153,176,329.

47

$

158,154,560.

18

$

163,294,583.

38

Purchase budget

2018 2019 2020 2021 2022

Budgeted

production in units 57,147,388 62,848,789 65,000,000 65,000,000 65,000,000

Direct material

required per unit 57,147,388 62,848,789 65,000,000 65,000,000 65,000,000

Add: Budgeted

closing material

2,197,976.4

4

2,417,261.1

1 2,500,000 2,500,000 2,500,000

Less: Opening

material 2000000

2,197,976.4

4

2,417,261.1

1 2,500,000 2,500,000

Purchase units

57,345,363.

94

63,068,073.

41

65,082,738.

89 65,000,000 65,000,000

Cost per unit

$

0.62

$

0.64

$

0.67

$

0.69

$

0.71

Budgeted material

purchase

$

35,821,498.

40

$

40,676,638.

87

$

43,340,246.

48

$

44,691,915.

88

$

46,144,403.

14

(ii) Budgeted cost of goods manufactured schedule

2018 2019 2020 2021 2022

Production

cost

$

126,371,803.

83

$

143,444,913.

72

$

153,176,329.

47

$

158,154,560.

18

$

163,294,583.38

Factory

manager's

salary

$

153,375.00

$

156,825.94

$

160,354.52

$

163,962.50

$

167,651.65

Depreciation:

Factory plant

and equipment

$

765,000.00

$

765,000.00

$

765,000.00

$

765,000.00

$

765,000.00

Cost of goods

manufactured

$

127,290,178.

83

$

144,366,739.

66

$

154,101,683.

99

$

159,083,522.

67

$

164,227,235.03

8MANAGEMENT ACCOUNTING

(iii) Budgeted cost of goods sold schedule

2018 2019 2020 2021 2022

Cost of

goods

manufacture

d

$

127,290,178.

83

$

144,366,739.

66

$

154,101,683.

99

$

159,083,522.

67

$

164,227,235.

03

Add:

Opening

stock of

finished

goods

$

985,000.00

$

1,096,837.50

$

1,206,521.25

$

1,327,173.38

$

1,459,890.71

Less:

Closing

stock of

finished

goods

$

1,096,837.50

$

1,206,521.25

$

1,327,173.38

$

1,459,890.71

$

1,605,879.78

Cost of

goods sold

$

127,178,341.

33

$

144,257,055.

91

$

153,981,031.

86

$

158,950,805.

34

$

164,081,245.

96

Gross profit schedule

2018 2019 2020 2021 2022

Sales revenue

$

133,784,011.

97

$

153,416,815.

73

$

175,930,733.

43

$

201,748,568.

56

$

231,355,171.0

0

Less: Cost of

goods sold

$

127,178,341.

33

$

144,257,055.

91

$

153,981,031.

86

$

158,950,805.

34

$

164,081,245.9

6

Gross profit

$

6,605,670.63

$

9,159,759.82

$

21,949,701.5

7

$

42,797,763.2

3

$

67,273,925.04

(b) Increased production constraint

Computation of NPV

Year 2019 2019 2020 2021 2022

Cash outflow

$

(5,000,000.00)

Cash inflow

$

4,146,181.87

$

6,280,279.19

$

8,877,442.64 $ 16,249,545.43

Cash $ $ $ $ $ 16,249,545.43

(iii) Budgeted cost of goods sold schedule

2018 2019 2020 2021 2022

Cost of

goods

manufacture

d

$

127,290,178.

83

$

144,366,739.

66

$

154,101,683.

99

$

159,083,522.

67

$

164,227,235.

03

Add:

Opening

stock of

finished

goods

$

985,000.00

$

1,096,837.50

$

1,206,521.25

$

1,327,173.38

$

1,459,890.71

Less:

Closing

stock of

finished

goods

$

1,096,837.50

$

1,206,521.25

$

1,327,173.38

$

1,459,890.71

$

1,605,879.78

Cost of

goods sold

$

127,178,341.

33

$

144,257,055.

91

$

153,981,031.

86

$

158,950,805.

34

$

164,081,245.

96

Gross profit schedule

2018 2019 2020 2021 2022

Sales revenue

$

133,784,011.

97

$

153,416,815.

73

$

175,930,733.

43

$

201,748,568.

56

$

231,355,171.0

0

Less: Cost of

goods sold

$

127,178,341.

33

$

144,257,055.

91

$

153,981,031.

86

$

158,950,805.

34

$

164,081,245.9

6

Gross profit

$

6,605,670.63

$

9,159,759.82

$

21,949,701.5

7

$

42,797,763.2

3

$

67,273,925.04

(b) Increased production constraint

Computation of NPV

Year 2019 2019 2020 2021 2022

Cash outflow

$

(5,000,000.00)

Cash inflow

$

4,146,181.87

$

6,280,279.19

$

8,877,442.64 $ 16,249,545.43

Cash $ $ $ $ $ 16,249,545.43

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9MANAGEMENT ACCOUNTING

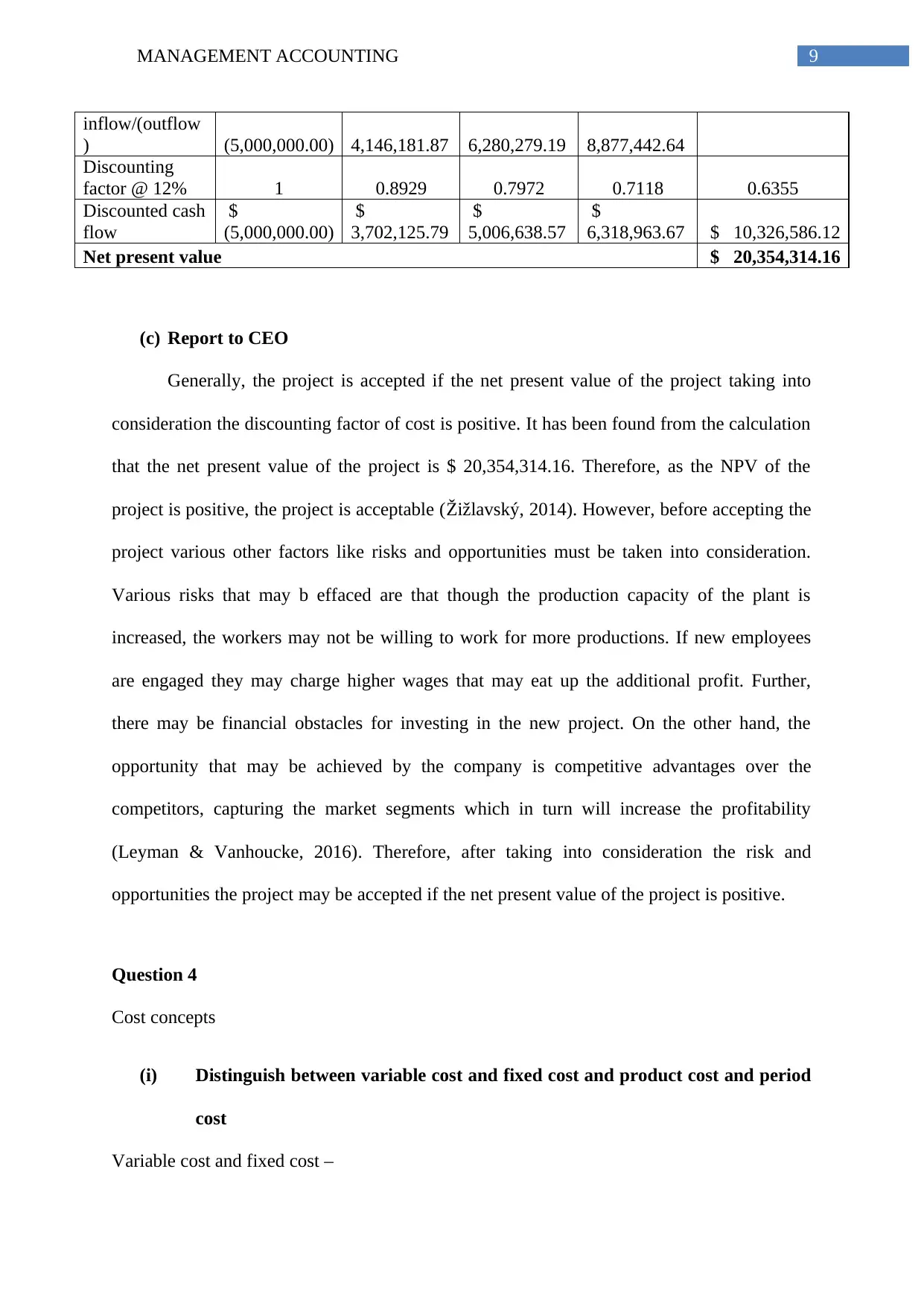

inflow/(outflow

) (5,000,000.00) 4,146,181.87 6,280,279.19 8,877,442.64

Discounting

factor @ 12% 1 0.8929 0.7972 0.7118 0.6355

Discounted cash

flow

$

(5,000,000.00)

$

3,702,125.79

$

5,006,638.57

$

6,318,963.67 $ 10,326,586.12

Net present value $ 20,354,314.16

(c) Report to CEO

Generally, the project is accepted if the net present value of the project taking into

consideration the discounting factor of cost is positive. It has been found from the calculation

that the net present value of the project is $ 20,354,314.16. Therefore, as the NPV of the

project is positive, the project is acceptable (Žižlavský, 2014). However, before accepting the

project various other factors like risks and opportunities must be taken into consideration.

Various risks that may b effaced are that though the production capacity of the plant is

increased, the workers may not be willing to work for more productions. If new employees

are engaged they may charge higher wages that may eat up the additional profit. Further,

there may be financial obstacles for investing in the new project. On the other hand, the

opportunity that may be achieved by the company is competitive advantages over the

competitors, capturing the market segments which in turn will increase the profitability

(Leyman & Vanhoucke, 2016). Therefore, after taking into consideration the risk and

opportunities the project may be accepted if the net present value of the project is positive.

Question 4

Cost concepts

(i) Distinguish between variable cost and fixed cost and product cost and period

cost

Variable cost and fixed cost –

inflow/(outflow

) (5,000,000.00) 4,146,181.87 6,280,279.19 8,877,442.64

Discounting

factor @ 12% 1 0.8929 0.7972 0.7118 0.6355

Discounted cash

flow

$

(5,000,000.00)

$

3,702,125.79

$

5,006,638.57

$

6,318,963.67 $ 10,326,586.12

Net present value $ 20,354,314.16

(c) Report to CEO

Generally, the project is accepted if the net present value of the project taking into

consideration the discounting factor of cost is positive. It has been found from the calculation

that the net present value of the project is $ 20,354,314.16. Therefore, as the NPV of the

project is positive, the project is acceptable (Žižlavský, 2014). However, before accepting the

project various other factors like risks and opportunities must be taken into consideration.

Various risks that may b effaced are that though the production capacity of the plant is

increased, the workers may not be willing to work for more productions. If new employees

are engaged they may charge higher wages that may eat up the additional profit. Further,

there may be financial obstacles for investing in the new project. On the other hand, the

opportunity that may be achieved by the company is competitive advantages over the

competitors, capturing the market segments which in turn will increase the profitability

(Leyman & Vanhoucke, 2016). Therefore, after taking into consideration the risk and

opportunities the project may be accepted if the net present value of the project is positive.

Question 4

Cost concepts

(i) Distinguish between variable cost and fixed cost and product cost and period

cost

Variable cost and fixed cost –

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10MANAGEMENT ACCOUNTING

Fixed cost is the cost that remains same irrespective of production volume whereas

the variable costs change when there is a change in the output. Fixed cost includes building,

machinery and rent. On the other hand, variable cost includes wages, utilities, material cost

for production (Drury, 2013). The main differences among 2 types of costs are as follows –

Basis of difference Fixed cost Variable cost

Nature This costs are time related These costs are volume

related

Unit cost It changes with the units as

the fixed cost per unit

reduces with the increase in

production. Therefore, per

unit fixed cost is inversely

proportional with produced

units.

Per unit variable cost remains

same

Incurred when These costs are definite and

are incurred even if there is

no production

These costs are incurred only

when production takes place

Combination It is the combination of fixed

administration overhead,

production, distribution and

selling overhead

It includes direct material,

labour, expenses, variable

production overhead, and

distribution and selling

overhead

Product cost and period cost –

Fixed cost is the cost that remains same irrespective of production volume whereas

the variable costs change when there is a change in the output. Fixed cost includes building,

machinery and rent. On the other hand, variable cost includes wages, utilities, material cost

for production (Drury, 2013). The main differences among 2 types of costs are as follows –

Basis of difference Fixed cost Variable cost

Nature This costs are time related These costs are volume

related

Unit cost It changes with the units as

the fixed cost per unit

reduces with the increase in

production. Therefore, per

unit fixed cost is inversely

proportional with produced

units.

Per unit variable cost remains

same

Incurred when These costs are definite and

are incurred even if there is

no production

These costs are incurred only

when production takes place

Combination It is the combination of fixed

administration overhead,

production, distribution and

selling overhead

It includes direct material,

labour, expenses, variable

production overhead, and

distribution and selling

overhead

Product cost and period cost –

11MANAGEMENT ACCOUNTING

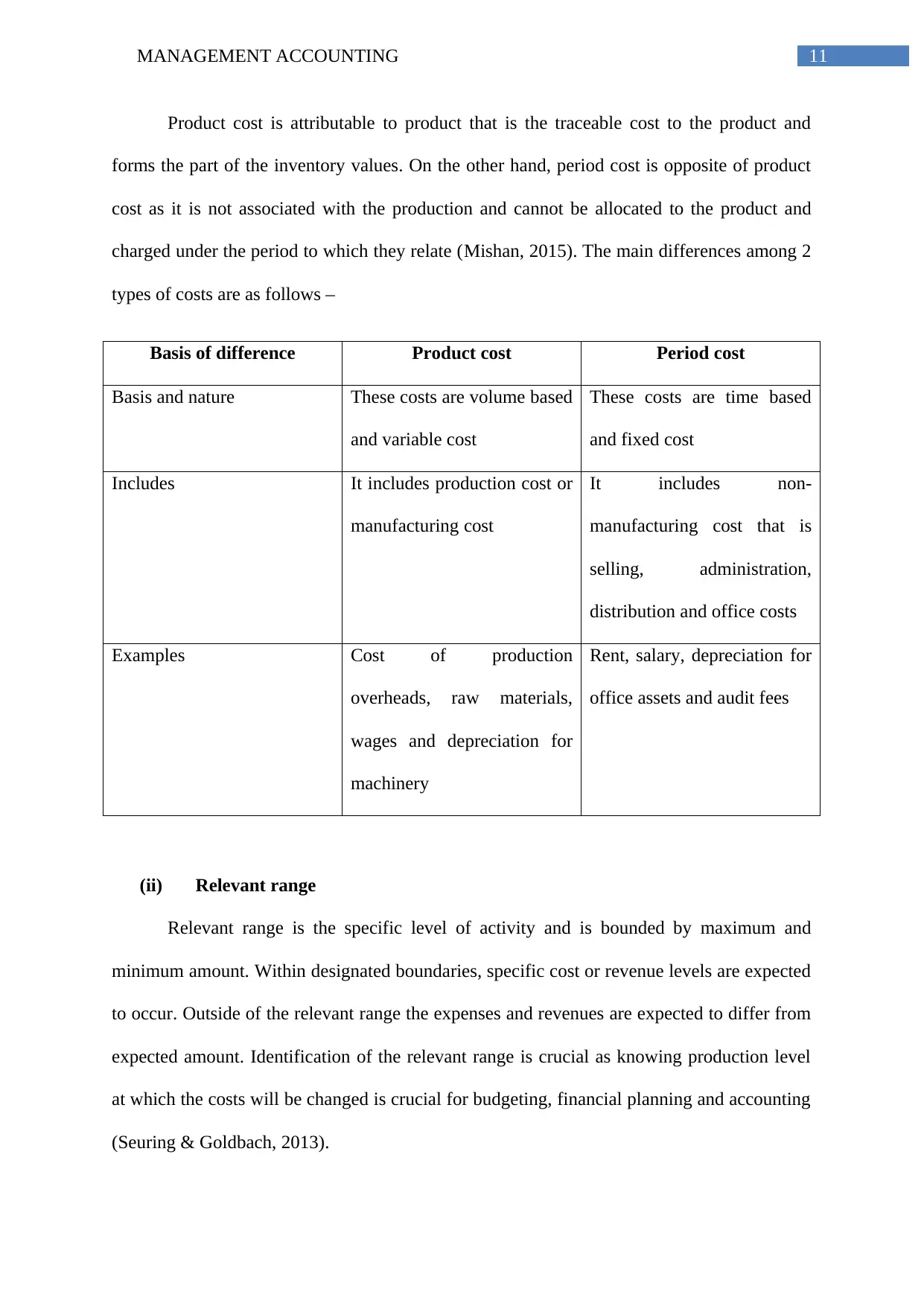

Product cost is attributable to product that is the traceable cost to the product and

forms the part of the inventory values. On the other hand, period cost is opposite of product

cost as it is not associated with the production and cannot be allocated to the product and

charged under the period to which they relate (Mishan, 2015). The main differences among 2

types of costs are as follows –

Basis of difference Product cost Period cost

Basis and nature These costs are volume based

and variable cost

These costs are time based

and fixed cost

Includes It includes production cost or

manufacturing cost

It includes non-

manufacturing cost that is

selling, administration,

distribution and office costs

Examples Cost of production

overheads, raw materials,

wages and depreciation for

machinery

Rent, salary, depreciation for

office assets and audit fees

(ii) Relevant range

Relevant range is the specific level of activity and is bounded by maximum and

minimum amount. Within designated boundaries, specific cost or revenue levels are expected

to occur. Outside of the relevant range the expenses and revenues are expected to differ from

expected amount. Identification of the relevant range is crucial as knowing production level

at which the costs will be changed is crucial for budgeting, financial planning and accounting

(Seuring & Goldbach, 2013).

Product cost is attributable to product that is the traceable cost to the product and

forms the part of the inventory values. On the other hand, period cost is opposite of product

cost as it is not associated with the production and cannot be allocated to the product and

charged under the period to which they relate (Mishan, 2015). The main differences among 2

types of costs are as follows –

Basis of difference Product cost Period cost

Basis and nature These costs are volume based

and variable cost

These costs are time based

and fixed cost

Includes It includes production cost or

manufacturing cost

It includes non-

manufacturing cost that is

selling, administration,

distribution and office costs

Examples Cost of production

overheads, raw materials,

wages and depreciation for

machinery

Rent, salary, depreciation for

office assets and audit fees

(ii) Relevant range

Relevant range is the specific level of activity and is bounded by maximum and

minimum amount. Within designated boundaries, specific cost or revenue levels are expected

to occur. Outside of the relevant range the expenses and revenues are expected to differ from

expected amount. Identification of the relevant range is crucial as knowing production level

at which the costs will be changed is crucial for budgeting, financial planning and accounting

(Seuring & Goldbach, 2013).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.