Management Accounting Report: Airdri Ltd Case Study and Analysis

VerifiedAdded on 2020/11/12

|22

|6470

|130

Report

AI Summary

This report provides a comprehensive overview of management accounting, focusing on its application within the context of Airdri Ltd, a small manufacturing company. It explores various management accounting systems, including cost accounting, inventory management, job costing, and price optimization systems, detailing their importance in decision-making processes. The report delves into different management accounting reporting methods such as cost reporting, budgeting, and execution reports, highlighting their roles in evaluating performance and aiding in financial planning. It also examines a range of management accounting techniques, including financial planning and financial statement analysis, and their application in achieving organizational goals. The report also discusses the significance of budgets as control tools and the use of planning tools to address financial problems and drive sustainable success. Overall, the report provides a detailed analysis of how management accounting principles and practices can be effectively utilized to support strategic decision-making and improve organizational performance.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION ..........................................................................................................................3

TASK 1............................................................................................................................................4

Management accounting and requirements of essential kind of management accounting

systems........................................................................................................................................4

Explain different methods used for management accounting reporting.....................................5

TASK 2............................................................................................................................................8

Range of management accounting techniques............................................................................8

TASK 3..........................................................................................................................................12

Budget an important tool for control.........................................................................................12

Use of different planning tools and their application for preparing and forecasting budget.. . .13

TASK 4..........................................................................................................................................13

Management accounting to respond to financial problems.......................................................13

How in responding to financial problems, management accounting can lead organisation to

sustainable success....................................................................................................................15

Planning tools for accounting help to solve problems and support organisations with

sustainable success....................................................................................................................15

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION ..........................................................................................................................3

TASK 1............................................................................................................................................4

Management accounting and requirements of essential kind of management accounting

systems........................................................................................................................................4

Explain different methods used for management accounting reporting.....................................5

TASK 2............................................................................................................................................8

Range of management accounting techniques............................................................................8

TASK 3..........................................................................................................................................12

Budget an important tool for control.........................................................................................12

Use of different planning tools and their application for preparing and forecasting budget.. . .13

TASK 4..........................................................................................................................................13

Management accounting to respond to financial problems.......................................................13

How in responding to financial problems, management accounting can lead organisation to

sustainable success....................................................................................................................15

Planning tools for accounting help to solve problems and support organisations with

sustainable success....................................................................................................................15

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management accounting which also known as managerial accounting, chain of activities

by evaluating business cost and operations helps in prepare financial reports, records. It helps to

manager in taking important decisions for achieving goals and objectives. On other hand it

means managing financial and costing of data then translate into useful information within

management and organisation. This report is based on Airdri which is an small manufacturing

company that produce or manufacture hair dryers and accessories to give major attributes to

consumers. This report is based on various management accounting system and their methods

with their critical evaluation. Further it evaluates about management accounting techniques and

practical evaluation of accounting terms. It also includes planning tools and techniques and their

advantages with disadvantage and at last how organisation respond to management accounting

system by defending various problems (Arroyo, 2012). It also includes budget as an important

planning tool and technique to control each and every activity in an effective manner.

TASK 1

Management accounting and requirements of essential kind of management accounting systems.

Management accounting use by managers for provisions of accounting knowledge and

information before making important decision within their organisation and it helpful for

management and their performance to control works and activities (Hasniza Haron, Kamal

Abdul Rahman and Smith, 2013.). In preparing management accounting organisation have to

build reports and accounts that helpful in taking accurate and timely financial and statical

decisions by managers in day to day operations. Management accounting enables to managers

and others in taking crucial decisions and provides cost of goods and services in both condition

profitability or non profitability. Management accounting essential while Airdri taking important

decision such as open a new venture and while building budget. There are kinds of management

accounting systems that are activity based costing, cost accounting system, inventory

management system, job costing system and price optimization system (Laine, Paranko and

Suomala, 2012).

There are some key areas in which management accounting systems plays very crucial role that

are as follows:

For long and short term planning:

Management accounting which also known as managerial accounting, chain of activities

by evaluating business cost and operations helps in prepare financial reports, records. It helps to

manager in taking important decisions for achieving goals and objectives. On other hand it

means managing financial and costing of data then translate into useful information within

management and organisation. This report is based on Airdri which is an small manufacturing

company that produce or manufacture hair dryers and accessories to give major attributes to

consumers. This report is based on various management accounting system and their methods

with their critical evaluation. Further it evaluates about management accounting techniques and

practical evaluation of accounting terms. It also includes planning tools and techniques and their

advantages with disadvantage and at last how organisation respond to management accounting

system by defending various problems (Arroyo, 2012). It also includes budget as an important

planning tool and technique to control each and every activity in an effective manner.

TASK 1

Management accounting and requirements of essential kind of management accounting systems.

Management accounting use by managers for provisions of accounting knowledge and

information before making important decision within their organisation and it helpful for

management and their performance to control works and activities (Hasniza Haron, Kamal

Abdul Rahman and Smith, 2013.). In preparing management accounting organisation have to

build reports and accounts that helpful in taking accurate and timely financial and statical

decisions by managers in day to day operations. Management accounting enables to managers

and others in taking crucial decisions and provides cost of goods and services in both condition

profitability or non profitability. Management accounting essential while Airdri taking important

decision such as open a new venture and while building budget. There are kinds of management

accounting systems that are activity based costing, cost accounting system, inventory

management system, job costing system and price optimization system (Laine, Paranko and

Suomala, 2012).

There are some key areas in which management accounting systems plays very crucial role that

are as follows:

For long and short term planning:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Management accounting enables in both long term and short term planning and

implementation for taking future decisions. It helps for long term plans and policies, strategic

management and formulation of various strategies according to market trends and interest.

Managing information system:

The management accounting system helpful in managing and running information

management system at every level in organisational hierarchy.

Management accounting systems:

Management accounting systems are collection of information and statistics by taking

help of external parties such as stakeholders, regulators and various lenders by obeying

principles of accounting (Klychova, Faskhutdinova and Sadrieva, 2014.). For an organisation

they have to follow various kinds of accounting systems after accessing needs and wants of

clients of particular organisation.

There are kinds of management accounting systems that are as follows:

Cost accounting system:

Cost accounting system or product costing system that is a structural criteria use by

organisation to analyse cost, profitability and inventory valuation by controlling various kinds of

expenditure (DRURY, 2013).. Finding accurate cost of goods and services are significant in case

of Airdri Ltd to find out potentiality. So it require for estimation of various kinds of cost,

profitability and value of organisational products and services (Maskell, Baggaley and Grasso,

2016. ).

Inventory management system:

Inventory management system is a combination of technology and various kinds of

processes that helps in oversee maintenance of products which are stocked, assets of

organisation, raw materials and finished products (Boyns, Edwards and Nikitin, 2013.).

Inventory management system helps in evaluation of every item of inventory and information

that associated with it. In case of Airdri it uses inventory management system to record all

necessary information.

Job costing system:

In job costing system involves chain of activities for collecting information regarding

kinds of cost while production or service job. It is beneficial at time of producing different goods

that are totally different from each other.

implementation for taking future decisions. It helps for long term plans and policies, strategic

management and formulation of various strategies according to market trends and interest.

Managing information system:

The management accounting system helpful in managing and running information

management system at every level in organisational hierarchy.

Management accounting systems:

Management accounting systems are collection of information and statistics by taking

help of external parties such as stakeholders, regulators and various lenders by obeying

principles of accounting (Klychova, Faskhutdinova and Sadrieva, 2014.). For an organisation

they have to follow various kinds of accounting systems after accessing needs and wants of

clients of particular organisation.

There are kinds of management accounting systems that are as follows:

Cost accounting system:

Cost accounting system or product costing system that is a structural criteria use by

organisation to analyse cost, profitability and inventory valuation by controlling various kinds of

expenditure (DRURY, 2013).. Finding accurate cost of goods and services are significant in case

of Airdri Ltd to find out potentiality. So it require for estimation of various kinds of cost,

profitability and value of organisational products and services (Maskell, Baggaley and Grasso,

2016. ).

Inventory management system:

Inventory management system is a combination of technology and various kinds of

processes that helps in oversee maintenance of products which are stocked, assets of

organisation, raw materials and finished products (Boyns, Edwards and Nikitin, 2013.).

Inventory management system helps in evaluation of every item of inventory and information

that associated with it. In case of Airdri it uses inventory management system to record all

necessary information.

Job costing system:

In job costing system involves chain of activities for collecting information regarding

kinds of cost while production or service job. It is beneficial at time of producing different goods

that are totally different from each other.

Cost plus pricing:

Cost plus pricing refers to adding or including markup to cost of goods and services to

reach at selling price. In that pricing direct material cost, direct labour cost and overhead cost for

a product by adding to a markup percentage to reach at price of a product (Arroyo, 2012).. It

also be used within a consumer contract in which seller reimburse the seller for all costs that

incurred and pays negotiation profit with cost incurred.

Price optimization system :

Price optimization system used is an application that use for set prices and it is an

decision making process that uses employs data, software and algorithms to bring results in

proper manner (Malmmose, 2015.). It is most useful in determination of prices that helps in

attaining goals and objectives. Hence various kinds of management accounting system are

important for any organisation in taking important decision in terms of price, inventory and

many more.

Explain different methods used for management accounting reporting.

Management accounting which focus on collecting data and information with help of

financial accounting. It is very useful for preparing financial statements, income statements with

cash flow with balance sheet that helps in checking viability of a business project. Organisation

uses various kinds of methods or methodologies for accounting reporting that are as follows:

Cost reporting:

Cost reporting is one of important method in predetermined of price of products and

services. It helps in estimation of fixation of pricing, over head cost, labour cost and many more

pricing strategies comes under it (Cheng, 2012.). In cost reporting whole cost divides into total

items created into it and it helps to managers to oversee price of products and services with

selling cost. It is one source for planning and implementing various pricing strategies.

Budgets:

Budget is one of most important accounting tool that give direction and estimation of

spending plans and controlling measures of it (Burkhard and et.al ., 2012.). Budget managerial

accounting are very much critical for acquiring performance of an organisation and build as a

whole business in which department wise. Organisation build an overall budget to understand

their grand scheme of their business. In case of Airdri Ltd they build an effective budget by

evaluating income and expenditure so that important decisions should be taken.

Cost plus pricing refers to adding or including markup to cost of goods and services to

reach at selling price. In that pricing direct material cost, direct labour cost and overhead cost for

a product by adding to a markup percentage to reach at price of a product (Arroyo, 2012).. It

also be used within a consumer contract in which seller reimburse the seller for all costs that

incurred and pays negotiation profit with cost incurred.

Price optimization system :

Price optimization system used is an application that use for set prices and it is an

decision making process that uses employs data, software and algorithms to bring results in

proper manner (Malmmose, 2015.). It is most useful in determination of prices that helps in

attaining goals and objectives. Hence various kinds of management accounting system are

important for any organisation in taking important decision in terms of price, inventory and

many more.

Explain different methods used for management accounting reporting.

Management accounting which focus on collecting data and information with help of

financial accounting. It is very useful for preparing financial statements, income statements with

cash flow with balance sheet that helps in checking viability of a business project. Organisation

uses various kinds of methods or methodologies for accounting reporting that are as follows:

Cost reporting:

Cost reporting is one of important method in predetermined of price of products and

services. It helps in estimation of fixation of pricing, over head cost, labour cost and many more

pricing strategies comes under it (Cheng, 2012.). In cost reporting whole cost divides into total

items created into it and it helps to managers to oversee price of products and services with

selling cost. It is one source for planning and implementing various pricing strategies.

Budgets:

Budget is one of most important accounting tool that give direction and estimation of

spending plans and controlling measures of it (Burkhard and et.al ., 2012.). Budget managerial

accounting are very much critical for acquiring performance of an organisation and build as a

whole business in which department wise. Organisation build an overall budget to understand

their grand scheme of their business. In case of Airdri Ltd they build an effective budget by

evaluating income and expenditure so that important decisions should be taken.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Execution reports:

Management and accountants take benefit from various expenditure plans by contrasting

income and expenditure and by their sum (Allen and Desroches, Nyse Group, 2014). An

organisation implement budgets and procedures after analysing the entire data and statistics by

listed report performance.

Benefits of management accounting:

for an organisation management accounting plays crucial role that are as follows:

Management accounting helps in evaluating actual performance after comparing income and

expenditure with desirable performance (Leitner, 2013.).

It enables to manage and control by maximise capital employed that are crucial factor in

manufacturing of products and services.

In case of Airdri Ltd. To increase profitability they measure current position of an organisation

and evaluate by past performance also.

Budget report:

Budget report is an internal report used by an management by comparing estimation,

budget and their projections by comparing actual performance with predetermined goals and

objectives (World Health Organization. Management of Substance Abuse Unit, 2014.)

Performance report:

These reports are prepared to assess all business and workers performance. It aids firm to

develop effective strategies for their growth (Johansen and et.al ., 2014.). Airdri Ltd manger

produce this report to examine that its enterprise are performing appropriately or not.

Inventory and manufacturing report:

This is considered as a summary of items which are connected to company. This

facilitates comprehensive accounts of inventory or many products or services which served

through Airdri Ltd to their clients (Bergman and Bowe, 2012.). With the assistance of this they

may minimise the complexity into supply chain management (Hilton and Platt, 2013.).

Integration of management accounting system and management reporting within

organisational process:

Management reporting Integration with organisational process

Budget report Budget report integrate with organisational

Management and accountants take benefit from various expenditure plans by contrasting

income and expenditure and by their sum (Allen and Desroches, Nyse Group, 2014). An

organisation implement budgets and procedures after analysing the entire data and statistics by

listed report performance.

Benefits of management accounting:

for an organisation management accounting plays crucial role that are as follows:

Management accounting helps in evaluating actual performance after comparing income and

expenditure with desirable performance (Leitner, 2013.).

It enables to manage and control by maximise capital employed that are crucial factor in

manufacturing of products and services.

In case of Airdri Ltd. To increase profitability they measure current position of an organisation

and evaluate by past performance also.

Budget report:

Budget report is an internal report used by an management by comparing estimation,

budget and their projections by comparing actual performance with predetermined goals and

objectives (World Health Organization. Management of Substance Abuse Unit, 2014.)

Performance report:

These reports are prepared to assess all business and workers performance. It aids firm to

develop effective strategies for their growth (Johansen and et.al ., 2014.). Airdri Ltd manger

produce this report to examine that its enterprise are performing appropriately or not.

Inventory and manufacturing report:

This is considered as a summary of items which are connected to company. This

facilitates comprehensive accounts of inventory or many products or services which served

through Airdri Ltd to their clients (Bergman and Bowe, 2012.). With the assistance of this they

may minimise the complexity into supply chain management (Hilton and Platt, 2013.).

Integration of management accounting system and management reporting within

organisational process:

Management reporting Integration with organisational process

Budget report Budget report integrate with organisational

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

process, in case of Airdri Ltd to reach at

accurate work and desirable outcome. With

help of budget an organisation can predict

about income and expenditure at every stage of

organisation and their respective process

(Contrafatto and Burns, 2013.).

Performance report Performance report is one of important aspect

in which organisational process should be

integrate with performance of an individual by

evaluating their key skills and accordingly

process and desirable results should be

accomplished (Grötsch, Blome and Schleper,

2013.).

Inventory and manufacturing report Inventory and manufacturing report is most

significant aspect that helps in allocation of

inventory and manufacture products and

services as require each step of organisational

success (Hoque, A. Covaleski and N.

Gooneratne, 2013). It gives direction for

accomplishing desirable goals and objectives.

Therefore, reporting within management accounting system that cover whole aspects of

company as well as integrates overall activities and crucial method for accomplishing all

organisational performance. Whole business concern process are interconnected with one

another in order to optimise their various costs of activity.

A) Job costing methods

Costing method:

Product costing method use for assigning cost for manufacturing products and services

(Allen and Desroches, Nyse Group, 2014). The major costing method are process costing,

accurate work and desirable outcome. With

help of budget an organisation can predict

about income and expenditure at every stage of

organisation and their respective process

(Contrafatto and Burns, 2013.).

Performance report Performance report is one of important aspect

in which organisational process should be

integrate with performance of an individual by

evaluating their key skills and accordingly

process and desirable results should be

accomplished (Grötsch, Blome and Schleper,

2013.).

Inventory and manufacturing report Inventory and manufacturing report is most

significant aspect that helps in allocation of

inventory and manufacture products and

services as require each step of organisational

success (Hoque, A. Covaleski and N.

Gooneratne, 2013). It gives direction for

accomplishing desirable goals and objectives.

Therefore, reporting within management accounting system that cover whole aspects of

company as well as integrates overall activities and crucial method for accomplishing all

organisational performance. Whole business concern process are interconnected with one

another in order to optimise their various costs of activity.

A) Job costing methods

Costing method:

Product costing method use for assigning cost for manufacturing products and services

(Allen and Desroches, Nyse Group, 2014). The major costing method are process costing,

direct costing and throughout costing and that applies on different production and decision

environment.

Batch costing method

Batch costing method is adopted in areas by calculating cost of each batch in which

consist of advertisements that can be ascertained by dividing cost of a batch by no. of items that

produced in a particular batch (Hoque, A. Covaleski and N. Gooneratne, 2013.).

Contract costing method:

Contract costing is the method of tracking costs that associated with particular contract

from a customer. For an example if an organisation bids for a large construction project with

their consumers and two parties are agree in a contract for a certain kind of reimbursement

( Grötsch, Blome and Schleper, 2013.).

B) Process costing method:

Process costing is a significant cost that use for assigning costs to various units of

production in an organisation by producing products in large quantity in homogeneous way (

Contrafatto and Burns, 2013). Process costing is cost of a product in each and every process.

TASK 2

Range of management accounting techniques.

Management accounting to reach at desirable goals and objectives organisation have to

apply kinds of tools and techniques that are as follows:

Financial planning:

The first and foremost objective of financial planning is to gain maximum profit and

enlarge business opportunities. Main goal of financial planning is to plan every aspect and then

coordinate according to planning (Lukka and Vinnari, 2014.). Hence it is one of most important

tool to execute plans and policies in an organised form. In case of Airdri ltd. They record all

financial works and procedures to comply with changes (Baker and Ricciardi, 2014). Also

through this respective company can ascertain their long therm as well as short term objectives

and also build a balanced plan in order to accomplish that objectives.

Financial statement analysis:

In financial statement consist of profit and loss account and balance sheet which come

under important financial statements and evaluated under various time duration (Cederholm and

environment.

Batch costing method

Batch costing method is adopted in areas by calculating cost of each batch in which

consist of advertisements that can be ascertained by dividing cost of a batch by no. of items that

produced in a particular batch (Hoque, A. Covaleski and N. Gooneratne, 2013.).

Contract costing method:

Contract costing is the method of tracking costs that associated with particular contract

from a customer. For an example if an organisation bids for a large construction project with

their consumers and two parties are agree in a contract for a certain kind of reimbursement

( Grötsch, Blome and Schleper, 2013.).

B) Process costing method:

Process costing is a significant cost that use for assigning costs to various units of

production in an organisation by producing products in large quantity in homogeneous way (

Contrafatto and Burns, 2013). Process costing is cost of a product in each and every process.

TASK 2

Range of management accounting techniques.

Management accounting to reach at desirable goals and objectives organisation have to

apply kinds of tools and techniques that are as follows:

Financial planning:

The first and foremost objective of financial planning is to gain maximum profit and

enlarge business opportunities. Main goal of financial planning is to plan every aspect and then

coordinate according to planning (Lukka and Vinnari, 2014.). Hence it is one of most important

tool to execute plans and policies in an organised form. In case of Airdri ltd. They record all

financial works and procedures to comply with changes (Baker and Ricciardi, 2014). Also

through this respective company can ascertain their long therm as well as short term objectives

and also build a balanced plan in order to accomplish that objectives.

Financial statement analysis:

In financial statement consist of profit and loss account and balance sheet which come

under important financial statements and evaluated under various time duration (Cederholm and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

et.al ., 2015.). It helps in analysis of management activities with growth of organisation (Leitner,

2013.).. It can be possible by various statements, financial accounting and profit and loss

analysis. Through this techniques Airdri Ltd can examine the activities of management with

their organisational growth by preparing the balance sheet, profit and loss statement and many

more.

Cost accounting:

Cost accounting is an significant tool and technique that enables in capture companies

cost of production by product wise, process, department and branch wise and many more. In that

cost data should be evaluated by predetermined goals and objectives (Modell, 2014.). In cost

accounting comparison between two costs helps them to finalise factors or reasons that bring

difference between two costs. With the assistance of cost accounting techniques respective

company can obtain manufacturing costs by evaluating the cost information through pre planned

objectives.

Income statement:

Income statement or profit and loss statement is one of most important financial

statement of an organisation that shows about revenue and expenditure in a particular time frame

(Lavia López and Hiebl, 2014.). It shows about how revenue and income should be transform

into net income or net profit. With the assistance of this Airdri Ltd can get to know that whether

firm is in profit or in loss.

To calculate various income and expenditure organisation have to evaluate various kinds of costs

that are as follows:

Techniques:

Absorption costing: Absorption costing in a managerial accounting cost method of all cost that

associated with production of a particular goods and services (Fisher and Krumwiede, 2015.).

In that cost not only includes cost of materials and labour cost but also includes variable and

fixed cost. It is also known as full costing.

Marginal costing:

Marginal cost of production refers to change in total cost that brings after producing an

additional unit or item (Talley, 2017.). The main motive of marginal cost is to evaluate at which

point organisation can gain economies of scale. In marginal cost includes all types of cost that

varies from level of production.

2013.).. It can be possible by various statements, financial accounting and profit and loss

analysis. Through this techniques Airdri Ltd can examine the activities of management with

their organisational growth by preparing the balance sheet, profit and loss statement and many

more.

Cost accounting:

Cost accounting is an significant tool and technique that enables in capture companies

cost of production by product wise, process, department and branch wise and many more. In that

cost data should be evaluated by predetermined goals and objectives (Modell, 2014.). In cost

accounting comparison between two costs helps them to finalise factors or reasons that bring

difference between two costs. With the assistance of cost accounting techniques respective

company can obtain manufacturing costs by evaluating the cost information through pre planned

objectives.

Income statement:

Income statement or profit and loss statement is one of most important financial

statement of an organisation that shows about revenue and expenditure in a particular time frame

(Lavia López and Hiebl, 2014.). It shows about how revenue and income should be transform

into net income or net profit. With the assistance of this Airdri Ltd can get to know that whether

firm is in profit or in loss.

To calculate various income and expenditure organisation have to evaluate various kinds of costs

that are as follows:

Techniques:

Absorption costing: Absorption costing in a managerial accounting cost method of all cost that

associated with production of a particular goods and services (Fisher and Krumwiede, 2015.).

In that cost not only includes cost of materials and labour cost but also includes variable and

fixed cost. It is also known as full costing.

Marginal costing:

Marginal cost of production refers to change in total cost that brings after producing an

additional unit or item (Talley, 2017.). The main motive of marginal cost is to evaluate at which

point organisation can gain economies of scale. In marginal cost includes all types of cost that

varies from level of production.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

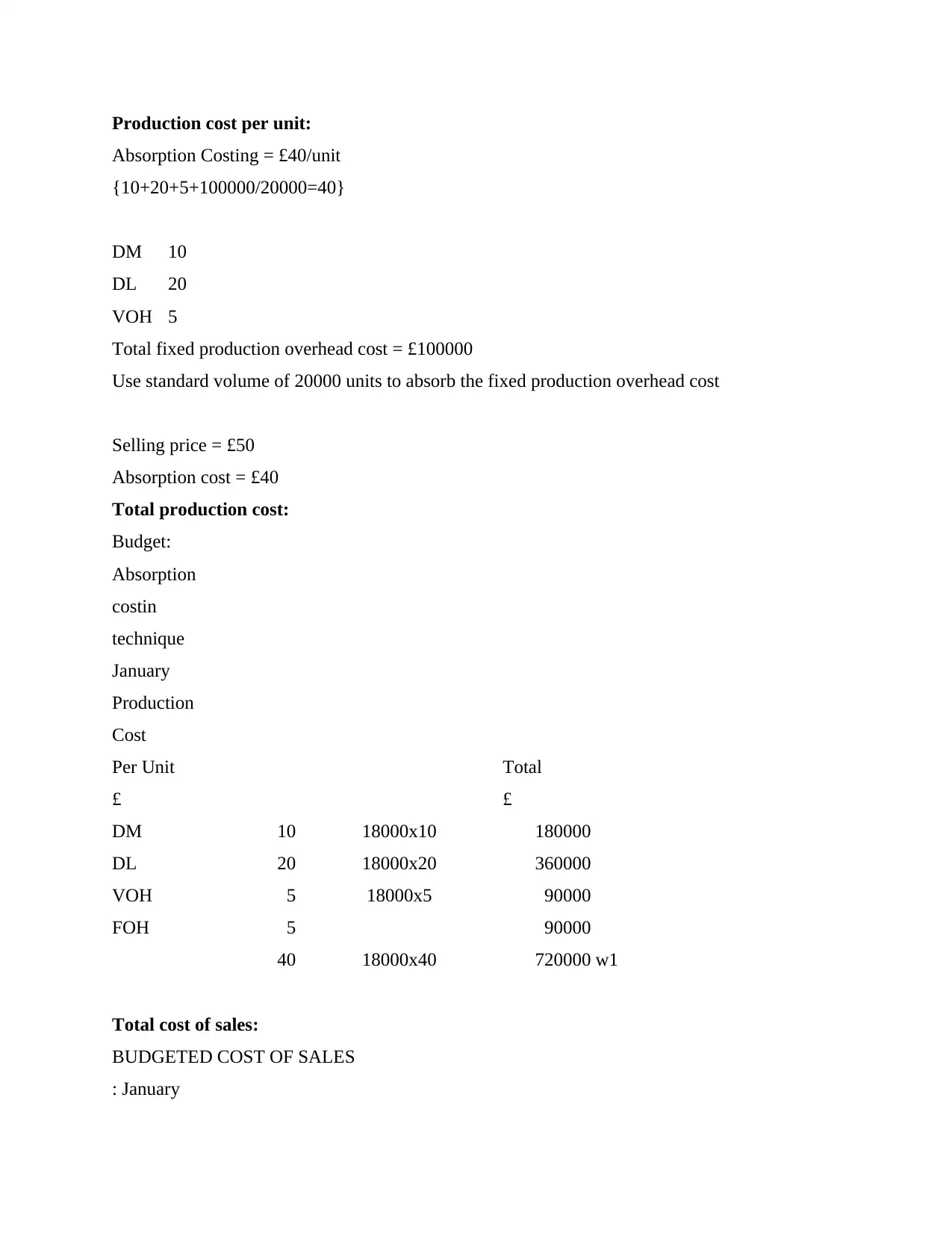

Production cost per unit:

Absorption Costing = £40/unit

{10+20+5+100000/20000=40}

DM 10

DL 20

VOH 5

Total fixed production overhead cost = £100000

Use standard volume of 20000 units to absorb the fixed production overhead cost

Selling price = £50

Absorption cost = £40

Total production cost:

Budget:

Absorption

costin

technique

January

Production

Cost

Per Unit Total

£ £

DM 10 18000x10 180000

DL 20 18000x20 360000

VOH 5 18000x5 90000

FOH 5 90000

40 18000x40 720000 w1

Total cost of sales:

BUDGETED COST OF SALES

: January

Absorption Costing = £40/unit

{10+20+5+100000/20000=40}

DM 10

DL 20

VOH 5

Total fixed production overhead cost = £100000

Use standard volume of 20000 units to absorb the fixed production overhead cost

Selling price = £50

Absorption cost = £40

Total production cost:

Budget:

Absorption

costin

technique

January

Production

Cost

Per Unit Total

£ £

DM 10 18000x10 180000

DL 20 18000x20 360000

VOH 5 18000x5 90000

FOH 5 90000

40 18000x40 720000 w1

Total cost of sales:

BUDGETED COST OF SALES

: January

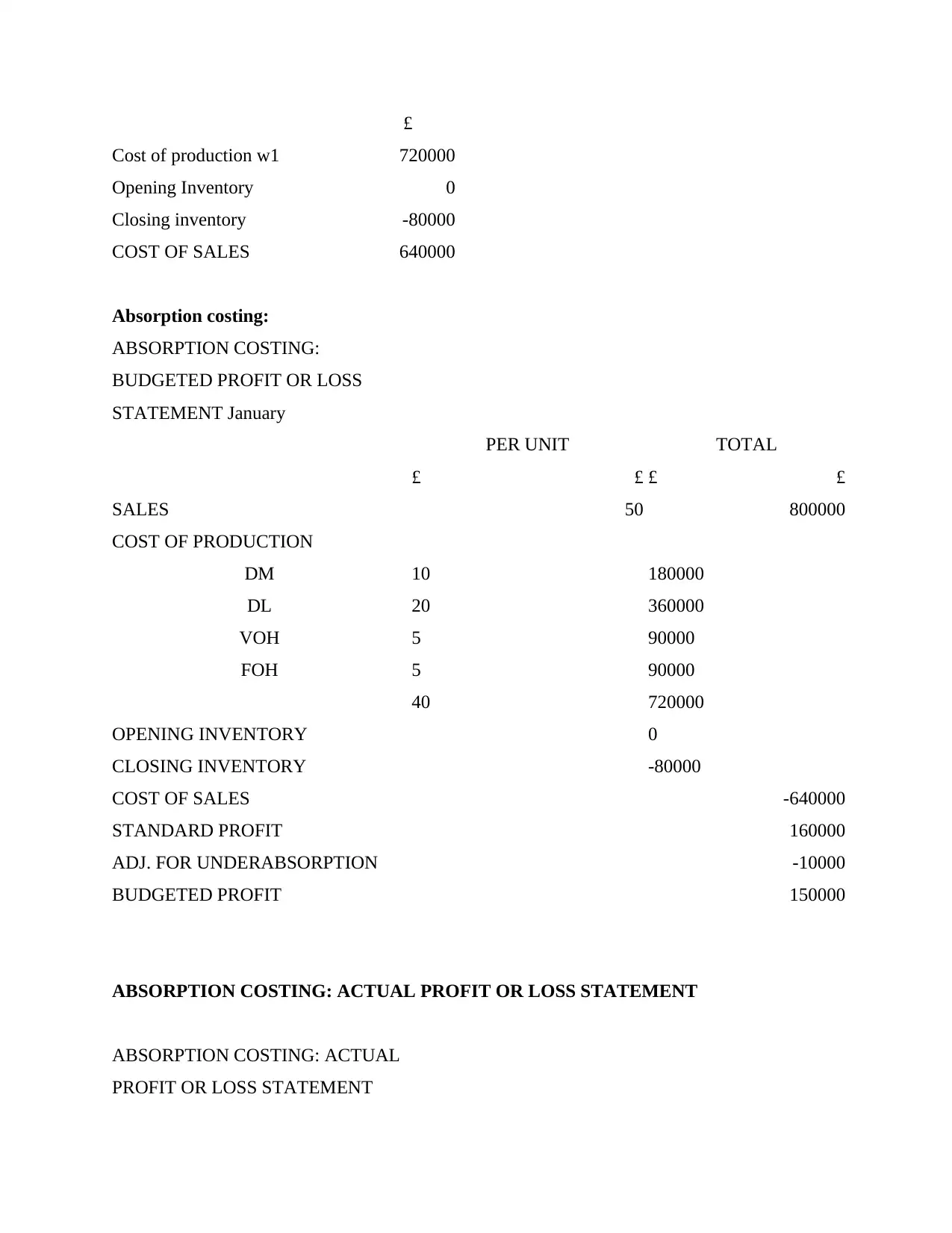

£

Cost of production w1 720000

Opening Inventory 0

Closing inventory -80000

COST OF SALES 640000

Absorption costing:

ABSORPTION COSTING:

BUDGETED PROFIT OR LOSS

STATEMENT January

PER UNIT TOTAL

£ £ £ £

SALES 50 800000

COST OF PRODUCTION

DM 10 180000

DL 20 360000

VOH 5 90000

FOH 5 90000

40 720000

OPENING INVENTORY 0

CLOSING INVENTORY -80000

COST OF SALES -640000

STANDARD PROFIT 160000

ADJ. FOR UNDERABSORPTION -10000

BUDGETED PROFIT 150000

ABSORPTION COSTING: ACTUAL PROFIT OR LOSS STATEMENT

ABSORPTION COSTING: ACTUAL

PROFIT OR LOSS STATEMENT

Cost of production w1 720000

Opening Inventory 0

Closing inventory -80000

COST OF SALES 640000

Absorption costing:

ABSORPTION COSTING:

BUDGETED PROFIT OR LOSS

STATEMENT January

PER UNIT TOTAL

£ £ £ £

SALES 50 800000

COST OF PRODUCTION

DM 10 180000

DL 20 360000

VOH 5 90000

FOH 5 90000

40 720000

OPENING INVENTORY 0

CLOSING INVENTORY -80000

COST OF SALES -640000

STANDARD PROFIT 160000

ADJ. FOR UNDERABSORPTION -10000

BUDGETED PROFIT 150000

ABSORPTION COSTING: ACTUAL PROFIT OR LOSS STATEMENT

ABSORPTION COSTING: ACTUAL

PROFIT OR LOSS STATEMENT

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.