Management Accounting Report: Costing, Budgeting and Analysis

VerifiedAdded on 2023/01/12

|10

|1066

|38

Report

AI Summary

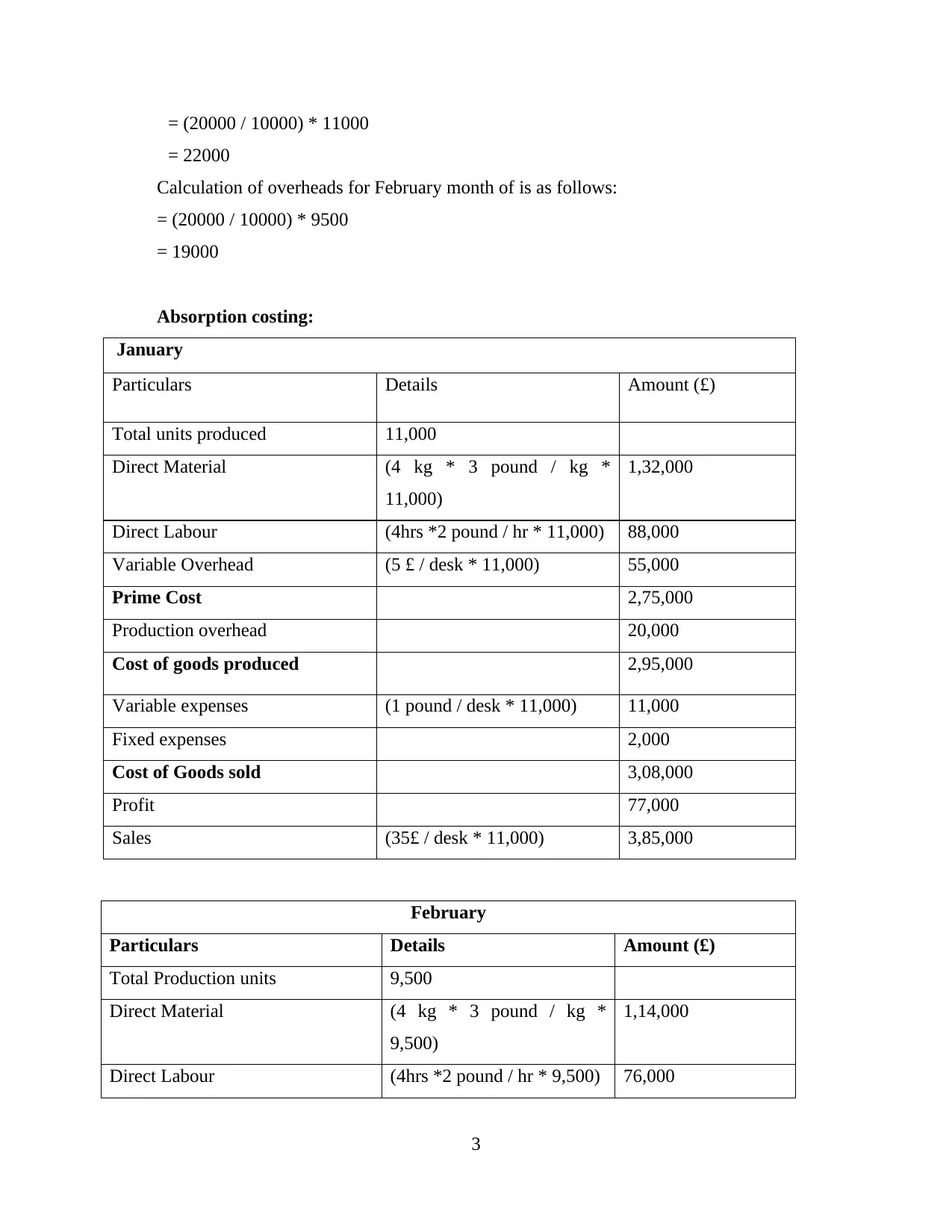

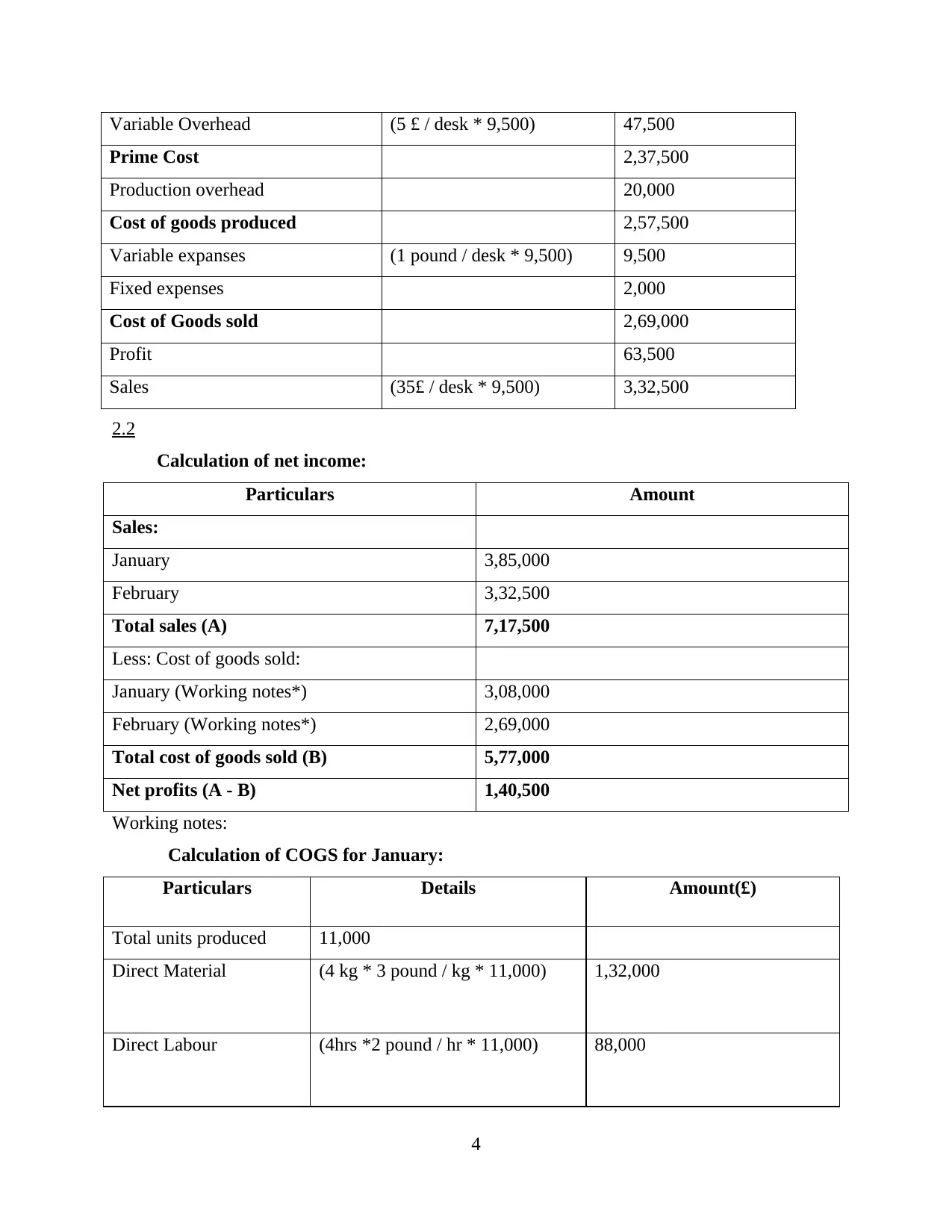

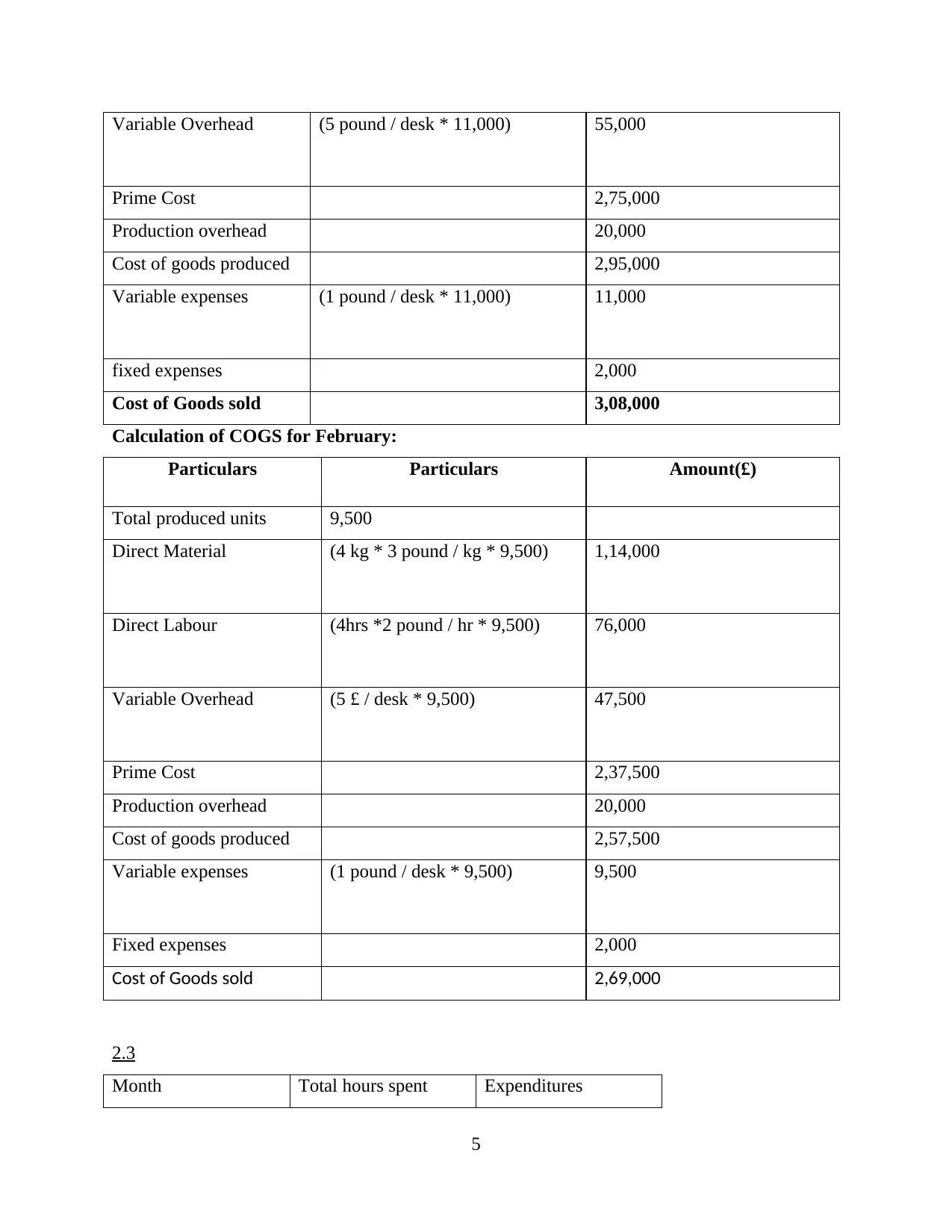

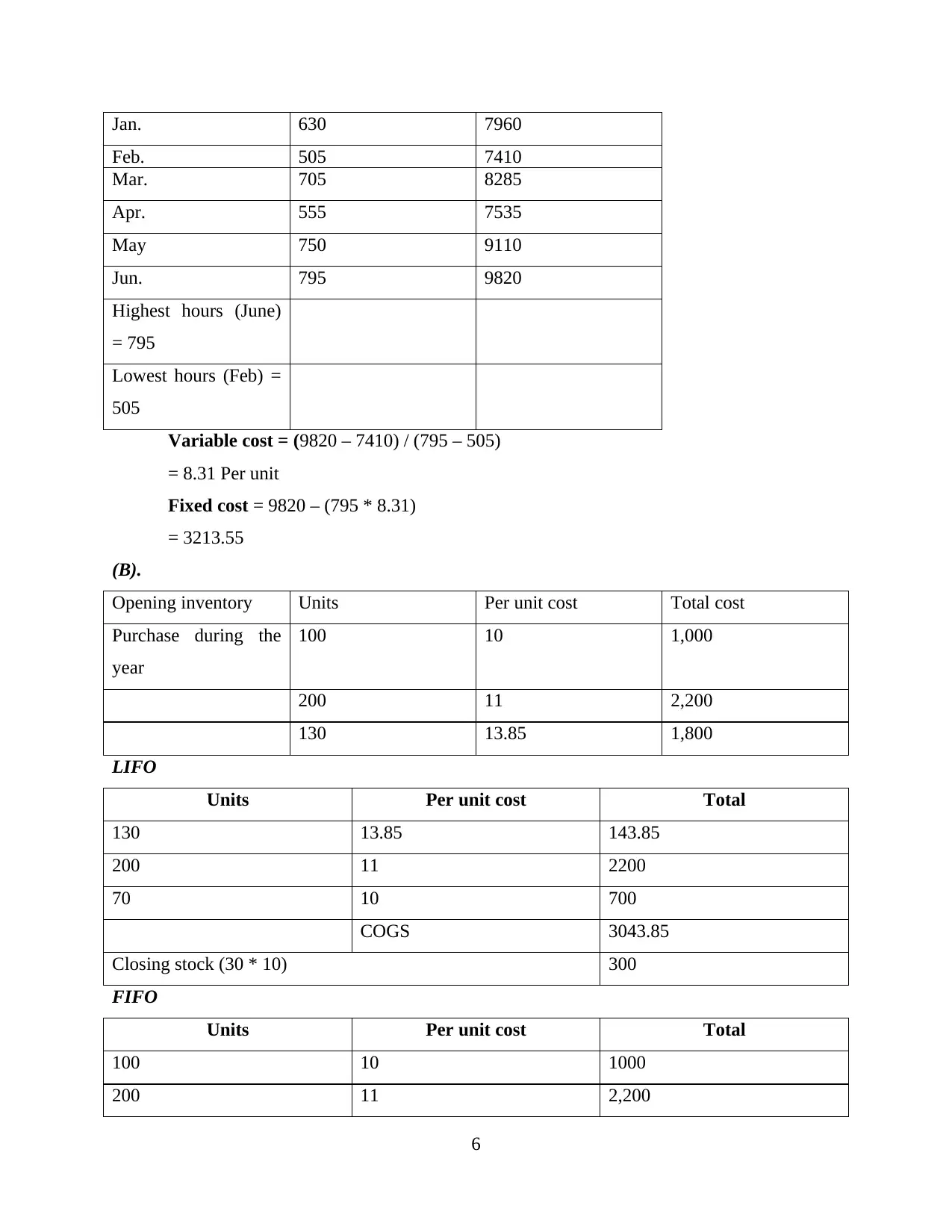

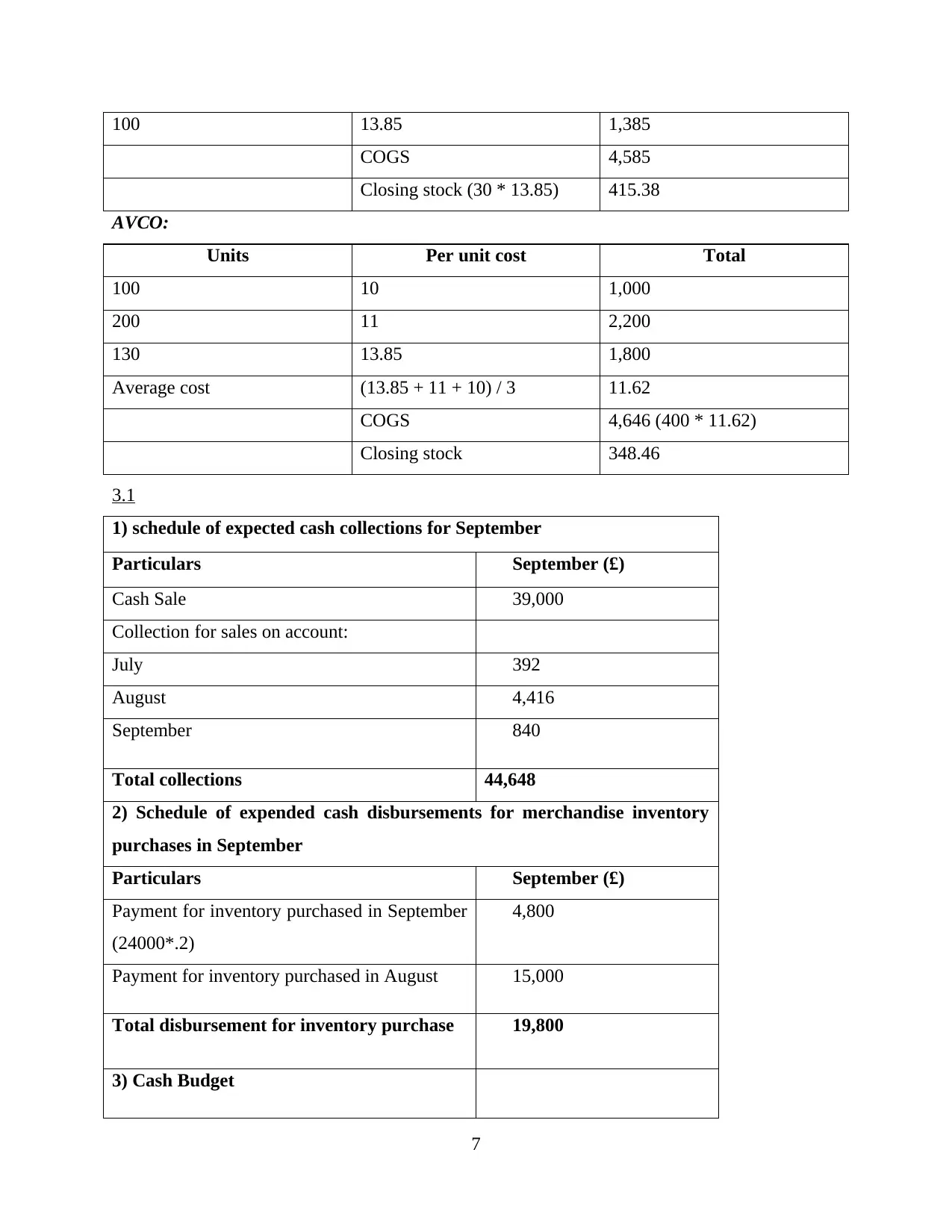

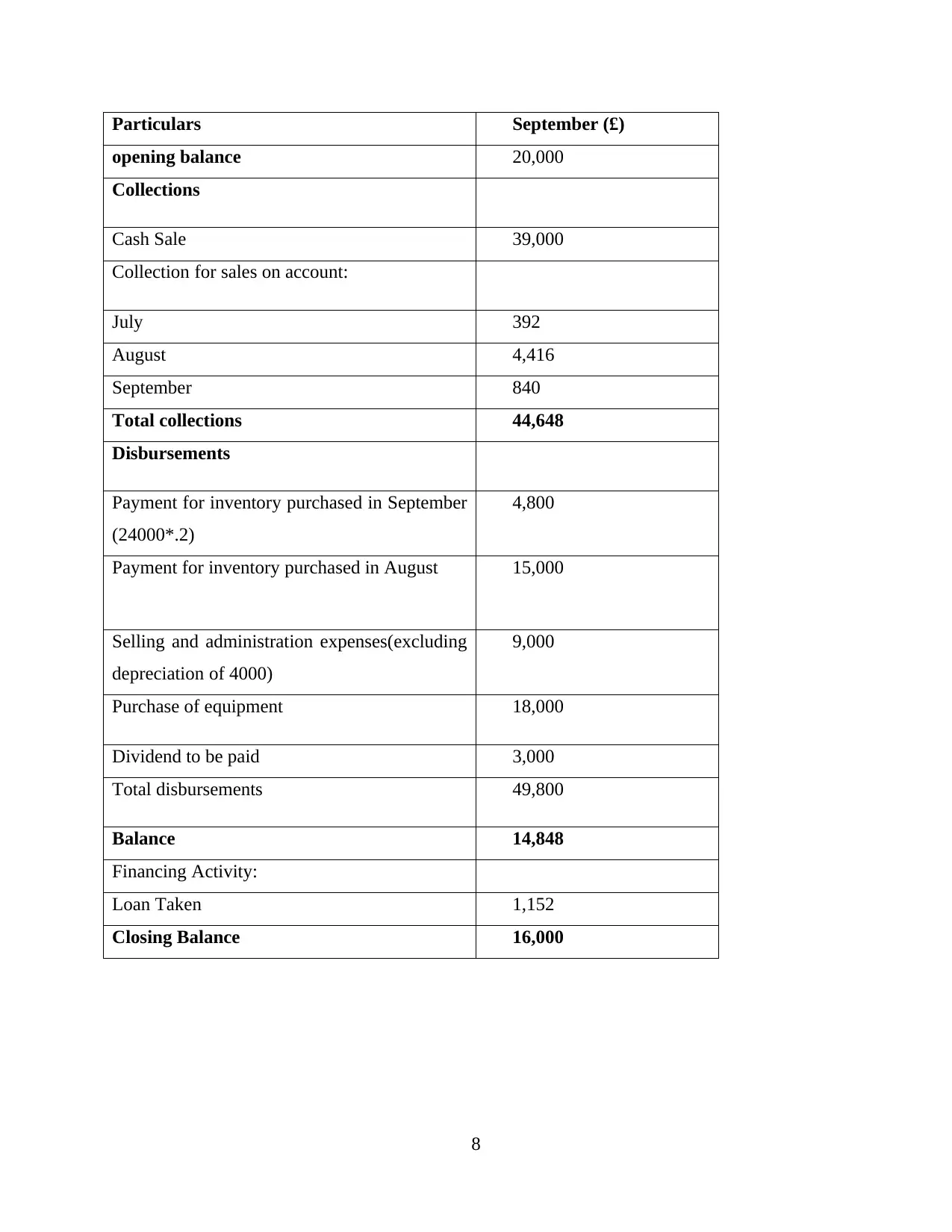

This report provides a comprehensive analysis of management accounting principles and techniques. It begins with an examination of costing methods, including marginal and absorption costing, providing detailed calculations and comparisons for January and February production periods. The report then delves into the calculation of net income using absorption costing, followed by an analysis of cost behavior, specifically focusing on variable and fixed costs using high-low method and the calculation of the variable and fixed costs. Furthermore, it explores inventory valuation methods, such as LIFO, FIFO, and AVCO, providing calculations for each method to determine cost of goods sold and closing stock. Finally, the report concludes with a cash budget analysis, including expected cash collections, cash disbursements, and financing activities, to assess the financial performance and cash flow management of a business.

1 out of 10

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.