Management Accounting Report: Cost Analysis and Methods

VerifiedAdded on 2023/01/12

|11

|2304

|93

Report

AI Summary

This report delves into the realm of management accounting, exploring its fundamental concepts and practical applications within a business context. It begins by defining management accounting and outlining its essential requirements, differentiating it from financial accounting and highlighting various management accounting systems such as job costing, price optimizing, cost accounting, and inventory management. The report then examines different management accounting reporting methods, including budgeting reports, accounts receivable aging, job cost reports, and performance reports, emphasizing their benefits for informed decision-making. A key focus is the calculation of costs using cost analysis techniques to prepare income statements, utilizing both marginal and absorption costing methods for two hypothetical projects, X and Y. Through detailed calculations and interpretations, the report illustrates the impact of these costing methods on profitability and provides insights into their strategic implications. The report concludes by summarizing the importance of management accounting systems for organizational planning and performance evaluation, emphasizing the roles of marginal and absorption costing in financial reporting and strategic decision-making.

B11362

MANAGEMENT

ACCOUNTING

MANAGEMENT

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

PART A...........................................................................................................................................3

P1. Explanation of management accounting and essential requirements of different types of

management accounting systems:....................................................................................................3

P2. Explain different methods used for management accounting reporting....................................5

M1. Benefits and application of management accounting system:.................................................6

P3. Calculation of costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs...............................................................................8

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................3

PART A...........................................................................................................................................3

P1. Explanation of management accounting and essential requirements of different types of

management accounting systems:....................................................................................................3

P2. Explain different methods used for management accounting reporting....................................5

M1. Benefits and application of management accounting system:.................................................6

P3. Calculation of costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs...............................................................................8

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

Management accounting system involves process of creating and organizing goals of a

firm through identifying, measuring, analyzing, interpreting and communicating data to

each department heads. It generally focuses on information management system; it

differs from financial accountant, as accounts shows reports and figures but managerial

accounting attach some meaning to it for making it understandable by other project

heads. Seeing a figure is not enough for strategic managerial to make some conclusion

due to missing of accounting knowledge; but if report generated based on data provided

by accountant than mangers could easily reach to proper conclusion and make strategy

accordingly.

This project report will discuss how different accounting method of managerial

accounting system affects overall earnings of company. Report covers two parts; Part A

and B, where part A will discuss about measurement of outcomes of different applied

strategies through managerial accounting tools.

PART A

P1. Explanation of management accounting and essential

requirements of different types of management accounting

systems:

Management Accounting: Management accounting or managerial accounting

involves internal systems which help organization in measuring, evaluating and

analyzing process of management of the business structure. The major

components of managerial accounting are budgets, internal performance reports,

financial reports of income statement and balance sheet, reports on return on

investment and earnings per share and trend analyses. It also uses cost of goods

Management accounting system involves process of creating and organizing goals of a

firm through identifying, measuring, analyzing, interpreting and communicating data to

each department heads. It generally focuses on information management system; it

differs from financial accountant, as accounts shows reports and figures but managerial

accounting attach some meaning to it for making it understandable by other project

heads. Seeing a figure is not enough for strategic managerial to make some conclusion

due to missing of accounting knowledge; but if report generated based on data provided

by accountant than mangers could easily reach to proper conclusion and make strategy

accordingly.

This project report will discuss how different accounting method of managerial

accounting system affects overall earnings of company. Report covers two parts; Part A

and B, where part A will discuss about measurement of outcomes of different applied

strategies through managerial accounting tools.

PART A

P1. Explanation of management accounting and essential

requirements of different types of management accounting

systems:

Management Accounting: Management accounting or managerial accounting

involves internal systems which help organization in measuring, evaluating and

analyzing process of management of the business structure. The major

components of managerial accounting are budgets, internal performance reports,

financial reports of income statement and balance sheet, reports on return on

investment and earnings per share and trend analyses. It also uses cost of goods

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

sold and activity-based cost analyses for making proper product pricing strategies

(Oliver, 2018).

Different types of management accounting system:

Job costing system: Cost bookkeeping framework that gathers producing costs

independently for each assignment. It is the process of assigning cost according to

the type of job or activity. This practice helps management in knowing which jobs

having much cost and how much value it is added to production process

(Hoggett, and et. al., 2018).

Price optimizing system: Each market is different and the thing that is beneficial

for one market may be the same opposite for another market. Mimicking goals in

different markets can disrupt your performance or even cause losses beyond

profit. User price, competition, and cost of goods sold may vary by location, so

these variations must be taken into account when identifying performance goals.

Lastly, although it is good to have a stable goal, but if you see real results, do not

hesitate to revise your performance goals. (Pratt, 2016).

Cost accounting system:

Cost accounting generates concern so that investigations can be continued on

operations aimed at maximizing the benefits and efficiency of the concern. In

contrast, the financial day traces the financial results for the accounting period and

the position of assets and liabilities on the last day of the accounting period. There

is no comparison between these two as they are equally important to users. This

article presents you the difference between cost accounting and financial

accounting in tabular form (Flower, 2016).

Cost Accounting can be additionally partitioned into two sections; Job request

costing and Process costing.

Inventory management system: The importance of inventory management,

especially for ecommerce and online retail brands, cannot be stressed enough

(Oliver, 2018).

Different types of management accounting system:

Job costing system: Cost bookkeeping framework that gathers producing costs

independently for each assignment. It is the process of assigning cost according to

the type of job or activity. This practice helps management in knowing which jobs

having much cost and how much value it is added to production process

(Hoggett, and et. al., 2018).

Price optimizing system: Each market is different and the thing that is beneficial

for one market may be the same opposite for another market. Mimicking goals in

different markets can disrupt your performance or even cause losses beyond

profit. User price, competition, and cost of goods sold may vary by location, so

these variations must be taken into account when identifying performance goals.

Lastly, although it is good to have a stable goal, but if you see real results, do not

hesitate to revise your performance goals. (Pratt, 2016).

Cost accounting system:

Cost accounting generates concern so that investigations can be continued on

operations aimed at maximizing the benefits and efficiency of the concern. In

contrast, the financial day traces the financial results for the accounting period and

the position of assets and liabilities on the last day of the accounting period. There

is no comparison between these two as they are equally important to users. This

article presents you the difference between cost accounting and financial

accounting in tabular form (Flower, 2016).

Cost Accounting can be additionally partitioned into two sections; Job request

costing and Process costing.

Inventory management system: The importance of inventory management,

especially for ecommerce and online retail brands, cannot be stressed enough

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(equipment and programming). Precise inventory tracking only allows brands to

complete orders on time and correctly. Inventory management in businesses

should grow as the company expands (Maynard, 2017).

Essential requirements of different accounting systems are:

It is used by entities to keep track of their financial transactions. Financial

accounting and management accounting are two branches of accounting. Financial

accounting emphasizes giving a fair and unbiased view of the company's financial

position to various parties (Bromwich and Bhimani, 2005). Different management

accounting systems are essentially required for business because:

It requires improving the efficiency of business operations.

It facilitates control to translate available objectives and strategy into

specific goals.

Provides accounting information’s and data interoperated in simple

language.

Provides liaison between top managers and accountants.

Helps in taking critical decisions for business expansion and risk

undertakings (Hansen, Mowen and Guan, 2007).

P2. Explain different methods used for management accounting

reporting

Different types of management accounting reports help management in

preparation of financial statement and forecasting past data’s to critically evaluate

its impact on overall performance of organization. It supports managers by

providing accurate and genuine data and information for helping in decision

making (Clatworthy, 2005). The various types of reports and their benefits are

discussed below:

Budgeting Reports: The budget is a plan made for the future, which is made by

estimating the revenue and other income and expenses for the whole year. In

which the financial minister, after estimating his expenditure before the

complete orders on time and correctly. Inventory management in businesses

should grow as the company expands (Maynard, 2017).

Essential requirements of different accounting systems are:

It is used by entities to keep track of their financial transactions. Financial

accounting and management accounting are two branches of accounting. Financial

accounting emphasizes giving a fair and unbiased view of the company's financial

position to various parties (Bromwich and Bhimani, 2005). Different management

accounting systems are essentially required for business because:

It requires improving the efficiency of business operations.

It facilitates control to translate available objectives and strategy into

specific goals.

Provides accounting information’s and data interoperated in simple

language.

Provides liaison between top managers and accountants.

Helps in taking critical decisions for business expansion and risk

undertakings (Hansen, Mowen and Guan, 2007).

P2. Explain different methods used for management accounting

reporting

Different types of management accounting reports help management in

preparation of financial statement and forecasting past data’s to critically evaluate

its impact on overall performance of organization. It supports managers by

providing accurate and genuine data and information for helping in decision

making (Clatworthy, 2005). The various types of reports and their benefits are

discussed below:

Budgeting Reports: The budget is a plan made for the future, which is made by

estimating the revenue and other income and expenses for the whole year. In

which the financial minister, after estimating his expenditure before the

government, makes several plans for the coming year and presents it to the public

during every financial year (Bratton and Gold, 2017).

Accounts Receivable Aging:

Recipients are ranked higher on the property list because of their ability to convert

to cash. Account receivables are shown on the company's balance sheet, as the

outstanding amounts are treated as assets as soon as they are paid - we hope - they

become cash (Flower and Ebbers, 2018).

Job Costs Reports: A order-specific costing technique is used when each product

is tailor-made and customized to the customer's needs. Job costs include direct

and indirect costs in one account. In addition, both types of costs are related to

each other (a job involves a substantial amount of labor and material that requires

close monitoring of power, machine time, inspection time, and moreover).

Performance reports: These reports show difference between actual

performance and budgeted performance; it shows the deviation between two

figures either in percentage form or in amount. This analysis helps managers to

take initiate step to control these variances at prime stage (Kaplan and Atkinson,

2015).

M1. Benefits and application of management accounting system:

Benefits:

Management accounting offers better Services to Customers. Management

accounting means the presentation of accounting information to assist in the

management of management accounting policy formulation and assist in the day-

to-day operations of the undertaking affect functions, benefits, and limitations of

management accounting. Thus, it deals with the use of consolidated accounting

data with the help of financial accounting and cost accounting for the purpose of

planning, planning, control and decision making by management. Management

accounting links with accounting as any accounting information required to make

during every financial year (Bratton and Gold, 2017).

Accounts Receivable Aging:

Recipients are ranked higher on the property list because of their ability to convert

to cash. Account receivables are shown on the company's balance sheet, as the

outstanding amounts are treated as assets as soon as they are paid - we hope - they

become cash (Flower and Ebbers, 2018).

Job Costs Reports: A order-specific costing technique is used when each product

is tailor-made and customized to the customer's needs. Job costs include direct

and indirect costs in one account. In addition, both types of costs are related to

each other (a job involves a substantial amount of labor and material that requires

close monitoring of power, machine time, inspection time, and moreover).

Performance reports: These reports show difference between actual

performance and budgeted performance; it shows the deviation between two

figures either in percentage form or in amount. This analysis helps managers to

take initiate step to control these variances at prime stage (Kaplan and Atkinson,

2015).

M1. Benefits and application of management accounting system:

Benefits:

Management accounting offers better Services to Customers. Management

accounting means the presentation of accounting information to assist in the

management of management accounting policy formulation and assist in the day-

to-day operations of the undertaking affect functions, benefits, and limitations of

management accounting. Thus, it deals with the use of consolidated accounting

data with the help of financial accounting and cost accounting for the purpose of

planning, planning, control and decision making by management. Management

accounting links with accounting as any accounting information required to make

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

management managerial decisions is the subject of management accounting

(Narayanaswamy, 2017).

Applications:

Measurement of performance: Management accounting system applied for

measuring the actual performance with budgeted one and analyzing factors that

impact actual performance and increases variations. It also supports organization

in analyzing difference between standard and actual performance sets out of

deviations on which necessary steps should be taken and implemented.

Assessment of risk: Another application of different management accounting

method is assessing future risks and their impact on overall business. Through

analyzing and evaluating various risk factors management accounting system

helps organization in building responsive attitude towards any miss happening in

business. For instance; analyzing past information a managerial accountant finds

that sales are moving downwards. Hence if not response at initial stage could

increase the risk of collapse of business and will not survive in long run.

Managerial reports shows which part of business needs maintenance and

improvement to boost overall sales of company.

Allocation of resources: Organizations can apply management accounting

system to achieve desired objectives through efficiency and effectively utilization

of its current resources in maximization of profit. Management accounting

systems method named cost analyses helps firm in identifying the movement of its

fund on different expenses; also it shows the way by which these expenses could

be minimized permanently or for long period of time (Quinn and Strauss, 2017).

Financial statement presentation: Management accounting provides proper

presentation of financial position of organization with necessary information and

data. Many different cost and financial information simplifies present good and

financial reports which provides key advantage to strategic department of firm.

(Narayanaswamy, 2017).

Applications:

Measurement of performance: Management accounting system applied for

measuring the actual performance with budgeted one and analyzing factors that

impact actual performance and increases variations. It also supports organization

in analyzing difference between standard and actual performance sets out of

deviations on which necessary steps should be taken and implemented.

Assessment of risk: Another application of different management accounting

method is assessing future risks and their impact on overall business. Through

analyzing and evaluating various risk factors management accounting system

helps organization in building responsive attitude towards any miss happening in

business. For instance; analyzing past information a managerial accountant finds

that sales are moving downwards. Hence if not response at initial stage could

increase the risk of collapse of business and will not survive in long run.

Managerial reports shows which part of business needs maintenance and

improvement to boost overall sales of company.

Allocation of resources: Organizations can apply management accounting

system to achieve desired objectives through efficiency and effectively utilization

of its current resources in maximization of profit. Management accounting

systems method named cost analyses helps firm in identifying the movement of its

fund on different expenses; also it shows the way by which these expenses could

be minimized permanently or for long period of time (Quinn and Strauss, 2017).

Financial statement presentation: Management accounting provides proper

presentation of financial position of organization with necessary information and

data. Many different cost and financial information simplifies present good and

financial reports which provides key advantage to strategic department of firm.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

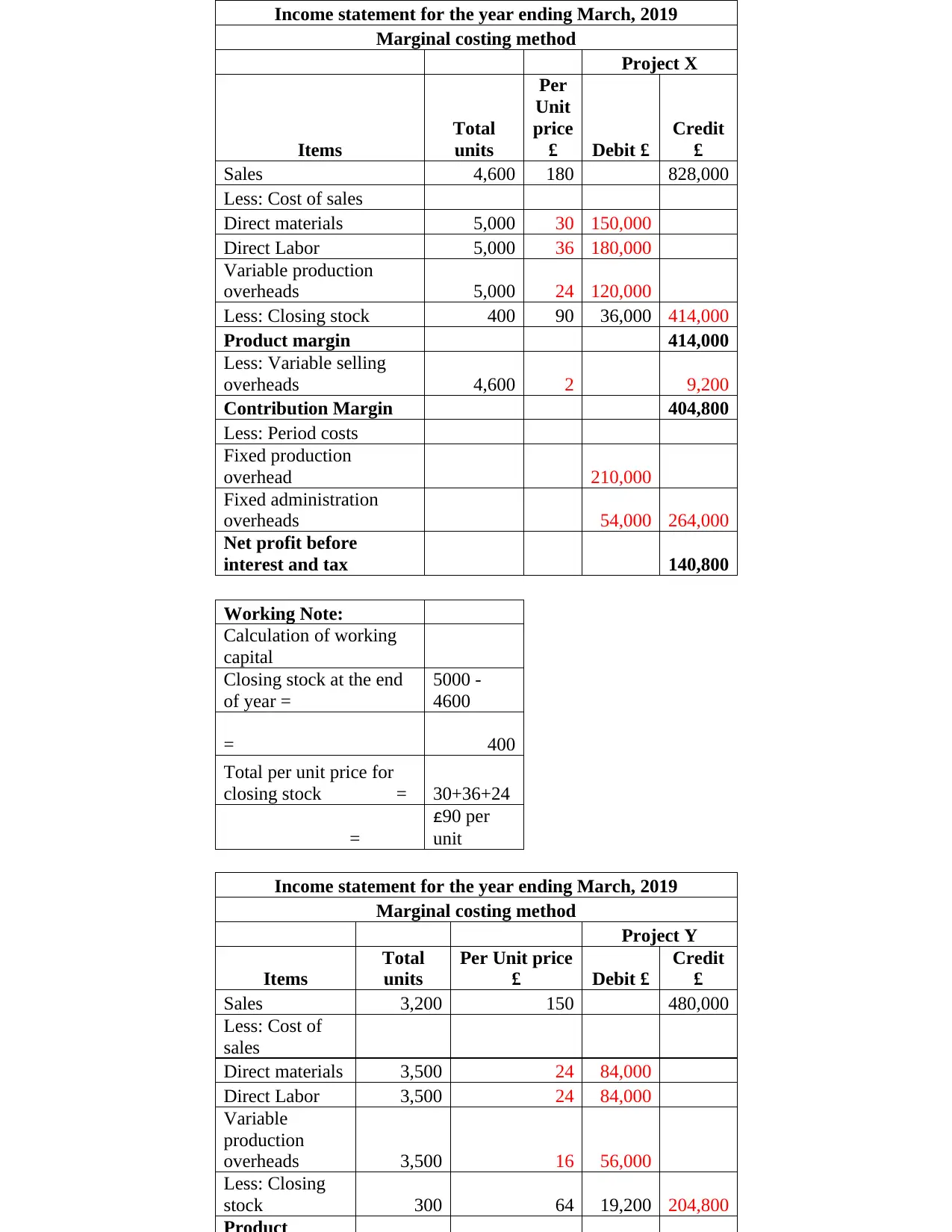

P3. Calculation of costs using appropriate techniques of cost

analysis to prepare an income statement using marginal and

absorption costs

Calculation of Income statement for both the Projects X and Y through marginal

costing and absorption costing methods:

analysis to prepare an income statement using marginal and

absorption costs

Calculation of Income statement for both the Projects X and Y through marginal

costing and absorption costing methods:

Income statement for the year ending March, 2019

Marginal costing method

Project X

Items

Total

units

Per

Unit

price

£ Debit £

Credit

£

Sales 4,600 180 828,000

Less: Cost of sales

Direct materials 5,000 30 150,000

Direct Labor 5,000 36 180,000

Variable production

overheads 5,000 24 120,000

Less: Closing stock 400 90 36,000 414,000

Product margin 414,000

Less: Variable selling

overheads 4,600 2 9,200

Contribution Margin 404,800

Less: Period costs

Fixed production

overhead 210,000

Fixed administration

overheads 54,000 264,000

Net profit before

interest and tax 140,800

Working Note:

Calculation of working

capital

Closing stock at the end

of year =

5000 -

4600

= 400

Total per unit price for

closing stock = 30+36+24

=

£90 per

unit

Income statement for the year ending March, 2019

Marginal costing method

Project Y

Items

Total

units

Per Unit price

£ Debit £

Credit

£

Sales 3,200 150 480,000

Less: Cost of

sales

Direct materials 3,500 24 84,000

Direct Labor 3,500 24 84,000

Variable

production

overheads 3,500 16 56,000

Less: Closing

stock 300 64 19,200 204,800

Marginal costing method

Project X

Items

Total

units

Per

Unit

price

£ Debit £

Credit

£

Sales 4,600 180 828,000

Less: Cost of sales

Direct materials 5,000 30 150,000

Direct Labor 5,000 36 180,000

Variable production

overheads 5,000 24 120,000

Less: Closing stock 400 90 36,000 414,000

Product margin 414,000

Less: Variable selling

overheads 4,600 2 9,200

Contribution Margin 404,800

Less: Period costs

Fixed production

overhead 210,000

Fixed administration

overheads 54,000 264,000

Net profit before

interest and tax 140,800

Working Note:

Calculation of working

capital

Closing stock at the end

of year =

5000 -

4600

= 400

Total per unit price for

closing stock = 30+36+24

=

£90 per

unit

Income statement for the year ending March, 2019

Marginal costing method

Project Y

Items

Total

units

Per Unit price

£ Debit £

Credit

£

Sales 3,200 150 480,000

Less: Cost of

sales

Direct materials 3,500 24 84,000

Direct Labor 3,500 24 84,000

Variable

production

overheads 3,500 16 56,000

Less: Closing

stock 300 64 19,200 204,800

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Interpretation: On the basis of calculation done above; it can be interpreted that

project X is giving more return than project Y not only through high amount but

return on investment of Project X is higher than Y. As the income statement is

prepared after consider two cost methods; marginal costing and absorption

costing. Where net profit calculated through marginal costing is showing lesser

amount than absorption costing; the reason behind this difference is calculation of

closing stock on other principles. For instance; in marginal costing method

closing stock is calculated only for production cost associated with it; while on the

other hand in absorption costing method, fixed overheads during the year were

considered for identifying overall cost of the product and thus results in increasing

the total closing stock at the end of year. The variation is mainly due to difference

occurring in closing stock figure (Corbett, 1998).

CONCLUSION

On the basis of report analysis and data research finding; it can be concluded that

management accounting systems provides pillars to every organizational strategic

planning and essentially required by every business owners. Due diligence reports

support identify gap between standard costing and actual performance. Both costing

methods; marginal and absorption play important role for income statement preparation.

Where absorption costing is important to know actual profit; on the other hand marginal

costing is useful to get breakeven point and minimum stock level requirement.

project X is giving more return than project Y not only through high amount but

return on investment of Project X is higher than Y. As the income statement is

prepared after consider two cost methods; marginal costing and absorption

costing. Where net profit calculated through marginal costing is showing lesser

amount than absorption costing; the reason behind this difference is calculation of

closing stock on other principles. For instance; in marginal costing method

closing stock is calculated only for production cost associated with it; while on the

other hand in absorption costing method, fixed overheads during the year were

considered for identifying overall cost of the product and thus results in increasing

the total closing stock at the end of year. The variation is mainly due to difference

occurring in closing stock figure (Corbett, 1998).

CONCLUSION

On the basis of report analysis and data research finding; it can be concluded that

management accounting systems provides pillars to every organizational strategic

planning and essentially required by every business owners. Due diligence reports

support identify gap between standard costing and actual performance. Both costing

methods; marginal and absorption play important role for income statement preparation.

Where absorption costing is important to know actual profit; on the other hand marginal

costing is useful to get breakeven point and minimum stock level requirement.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Bratton, J. and Gold, J., 2017. Human resource management: theory and practice. Palgrave.

Bromwich, M. and Bhimani, A., 2005. Management accounting: Pathways to progress. Cima

publishing.

Clatworthy, M., 2005. Transnational equity analysis. John Wiley & Sons.

Corbett, T., 1998. Throughput accounting: TOC's management accounting system (pp. 41-80).

Great Barrington: North river press.

Flower, J. and Ebbers, G., 2018. Global financial reporting. Macmillan International Higher

Education.

Flower, J., 2016. European financial reporting: adapting to a changing world. Springer.

Hansen, D., Mowen, M. and Guan, L., 2007. Cost management: accounting and control.

Cengage Learning.

Hoggett, J., and et. al., 2018. Financial accounting. Wiley.

Kaplan, R.S. and Atkinson, A.A., 2015. Advanced management accounting. PHI Learning.

Maynard, J., 2017. Financial accounting, reporting, and analysis. Oxford University Press.

Narayanaswamy, R., 2017. Financial accounting: a managerial perspective. PHI Learning Pvt.

Ltd..

Oliver, G.R., 2018. Managerial Accountant’s Compass: Research Genesis and Development.

Routledge.

Pratt, J., 2016. Financial accounting in an economic context. John Wiley & Sons.

Quinn, M. and Strauss, E., 2017. The Routledge Companion to Accounting Information Systems.

Routledge.

Books and Journals

Bratton, J. and Gold, J., 2017. Human resource management: theory and practice. Palgrave.

Bromwich, M. and Bhimani, A., 2005. Management accounting: Pathways to progress. Cima

publishing.

Clatworthy, M., 2005. Transnational equity analysis. John Wiley & Sons.

Corbett, T., 1998. Throughput accounting: TOC's management accounting system (pp. 41-80).

Great Barrington: North river press.

Flower, J. and Ebbers, G., 2018. Global financial reporting. Macmillan International Higher

Education.

Flower, J., 2016. European financial reporting: adapting to a changing world. Springer.

Hansen, D., Mowen, M. and Guan, L., 2007. Cost management: accounting and control.

Cengage Learning.

Hoggett, J., and et. al., 2018. Financial accounting. Wiley.

Kaplan, R.S. and Atkinson, A.A., 2015. Advanced management accounting. PHI Learning.

Maynard, J., 2017. Financial accounting, reporting, and analysis. Oxford University Press.

Narayanaswamy, R., 2017. Financial accounting: a managerial perspective. PHI Learning Pvt.

Ltd..

Oliver, G.R., 2018. Managerial Accountant’s Compass: Research Genesis and Development.

Routledge.

Pratt, J., 2016. Financial accounting in an economic context. John Wiley & Sons.

Quinn, M. and Strauss, E., 2017. The Routledge Companion to Accounting Information Systems.

Routledge.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.