Management Accounting Report: Analysis of Morphy Richards Company

VerifiedAdded on 2020/07/22

|18

|4706

|80

Report

AI Summary

This report provides a comprehensive overview of management accounting, focusing on its significance in the context of Morphy Richards, a UK-based electrical appliance manufacturer. The report begins by defining management accounting and its importance for effective decision-making, emphasizing its role in cost control and financial analysis. It then explores various management accounting systems, including cost accounting, price optimization, and inventory management, highlighting their practical applications within a manufacturing firm. The report also delves into different methods of management accounting reporting, such as performance reports, inventory management reports, and accounts receivable aging reports, and discusses their benefits. Furthermore, it analyzes marginal and absorption costing techniques, illustrating their differences through profit calculations. The report concludes by examining how management accounting systems can be utilized to address and resolve financial problems, making it a valuable resource for understanding the practical implications of management accounting in a business setting.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

Section 1...........................................................................................................................................1

P 1 Management accounting and requirements of management accounting in the company1

P2 Methods of management accounting reporting and benefits of management accounting

systems...................................................................................................................................3

P3 Marginal and absorption costing.......................................................................................5

Section 2...........................................................................................................................................7

P4 Discussing kinds of planning tools....................................................................................7

P5 Discussing how management accounting system is used to adapt to respond to financial

problems...............................................................................................................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................1

Section 1...........................................................................................................................................1

P 1 Management accounting and requirements of management accounting in the company1

P2 Methods of management accounting reporting and benefits of management accounting

systems...................................................................................................................................3

P3 Marginal and absorption costing.......................................................................................5

Section 2...........................................................................................................................................7

P4 Discussing kinds of planning tools....................................................................................7

P5 Discussing how management accounting system is used to adapt to respond to financial

problems...............................................................................................................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................13

INTRODUCTION

Management accounting is useful branch of accounting which provides required

information to management to take better decisions in effective way. The present report deals

with Morphy Richards Company which is engaged in manufacturing of electrical appliances in

UK and provides quality goods to customers to enhance their level of satisfaction. Importance of

management accounting is highlighted in this report along with various management accounting

systems which provides necessary information to manager so that better decisions can be made

with much ease. Moreover, different planning tools are discussed along with marginal and

absorption costing techniques which are required mainly in manufacturing firm. Furthermore,

financial problems are resolved by implementing management accounting systems which are

discussed as well. Thus, the report highlights significance of this branch of accounting for getting

desired results.

Section 1

P 1 Management accounting and requirements of management accounting in the company

Management accounting is essential tool for company as it help management to take

effective decisions with much ease. Management accounting uses financial information provided

by another branch of accounting which is known as financial accounting. The information

provided by this accounting system help management to draw interpretations about the company

and as such, better understanding of the effectiveness of the company is easily made. Thus,

management accounting is effective technique which help organisation to take enhanced

decisions with reference to cost control. Expenditures are carefully analysed and management

take measures so that it can be reduced up to high extent (Cooper, Ezzamel and Qu, 2017).

Management accounting is useful tool for Morphy Richards Company which is engaged

in manufacturing of electrical appliances and as such, this system is much useful for it to draw

meaningful information for making effective decisions with much ease. Furthermore, it is quite

essential tool for management as it aids in making decisions by supplying required information

in effectual manner. Applying techniques of absorption, marginal costing provides useful piece

of information to the management for taking decisions. Moreover, it is helpful for controlling

performance of the company by using various techniques such as standard costing, budgetary

1

Management accounting is useful branch of accounting which provides required

information to management to take better decisions in effective way. The present report deals

with Morphy Richards Company which is engaged in manufacturing of electrical appliances in

UK and provides quality goods to customers to enhance their level of satisfaction. Importance of

management accounting is highlighted in this report along with various management accounting

systems which provides necessary information to manager so that better decisions can be made

with much ease. Moreover, different planning tools are discussed along with marginal and

absorption costing techniques which are required mainly in manufacturing firm. Furthermore,

financial problems are resolved by implementing management accounting systems which are

discussed as well. Thus, the report highlights significance of this branch of accounting for getting

desired results.

Section 1

P 1 Management accounting and requirements of management accounting in the company

Management accounting is essential tool for company as it help management to take

effective decisions with much ease. Management accounting uses financial information provided

by another branch of accounting which is known as financial accounting. The information

provided by this accounting system help management to draw interpretations about the company

and as such, better understanding of the effectiveness of the company is easily made. Thus,

management accounting is effective technique which help organisation to take enhanced

decisions with reference to cost control. Expenditures are carefully analysed and management

take measures so that it can be reduced up to high extent (Cooper, Ezzamel and Qu, 2017).

Management accounting is useful tool for Morphy Richards Company which is engaged

in manufacturing of electrical appliances and as such, this system is much useful for it to draw

meaningful information for making effective decisions with much ease. Furthermore, it is quite

essential tool for management as it aids in making decisions by supplying required information

in effectual manner. Applying techniques of absorption, marginal costing provides useful piece

of information to the management for taking decisions. Moreover, it is helpful for controlling

performance of the company by using various techniques such as standard costing, budgetary

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

control which help management to have effective control on operational tasks of the

organisation.

Management accounting is also helpful for preparing and formulating policies for the

betterment of company so that it may be able to achieve common targets with much ease

(MONEM and SAEIDI, 2017). This is done by implementing regression analysis and time series

analysis which is helpful for forecasting and as such, objectives can be achieved with much ease.

Moreover, this information is useful for making decisions as it interprets financial statements so

that results can be assessed and company may be able to manage upon activities to accomplish

desired outcome. In relation to this, cash flow statement, fund flow statement are useful

techniques aiding management for decision-making in effectual manner. The types of

management accounting systems are as follows-

1. Cost accounting system

It is useful method of management accounting system which deals with ascertaining costs

and take measures to control so that expenditures may not exceed revenue of the firm. Morphy

Richards Company effectively uses cost accounting in daily operations so that it may be able to

take better control over it. Cost accounting plays important role in the company particularly in

manufacturing concern which involves various costs such as fixed, variable, direct, indirect and

semi-variable costs. Thus, it is required by the company to evaluate these expenditures so that it

may not outreach revenue of the firm (What is cost accounting?, 2018). Therefore, it assists

management in taking better and effective decisions to control costs so that overall revenue may

be increased by reducing expenditures incurred on production.

2. Price optimisation

Price optimisation is another useful management system that deals with carrying out

mathematical analysis to assess consumer behaviour in effective manner. In simple words, price

of a particular commodity can be easily set with the help of this technique. Morphy Richards

Company should use the same so that it may be able to assess the behaviour of customers

towards commodity whether they prefer to purchase at a quoted price or not. Thus, customer

behaviour is easily extracted with the help of this management accounting system to derive

fruitful results. This is also essential so that customers are not attracted to rivals in any manner.

2

organisation.

Management accounting is also helpful for preparing and formulating policies for the

betterment of company so that it may be able to achieve common targets with much ease

(MONEM and SAEIDI, 2017). This is done by implementing regression analysis and time series

analysis which is helpful for forecasting and as such, objectives can be achieved with much ease.

Moreover, this information is useful for making decisions as it interprets financial statements so

that results can be assessed and company may be able to manage upon activities to accomplish

desired outcome. In relation to this, cash flow statement, fund flow statement are useful

techniques aiding management for decision-making in effectual manner. The types of

management accounting systems are as follows-

1. Cost accounting system

It is useful method of management accounting system which deals with ascertaining costs

and take measures to control so that expenditures may not exceed revenue of the firm. Morphy

Richards Company effectively uses cost accounting in daily operations so that it may be able to

take better control over it. Cost accounting plays important role in the company particularly in

manufacturing concern which involves various costs such as fixed, variable, direct, indirect and

semi-variable costs. Thus, it is required by the company to evaluate these expenditures so that it

may not outreach revenue of the firm (What is cost accounting?, 2018). Therefore, it assists

management in taking better and effective decisions to control costs so that overall revenue may

be increased by reducing expenditures incurred on production.

2. Price optimisation

Price optimisation is another useful management system that deals with carrying out

mathematical analysis to assess consumer behaviour in effective manner. In simple words, price

of a particular commodity can be easily set with the help of this technique. Morphy Richards

Company should use the same so that it may be able to assess the behaviour of customers

towards commodity whether they prefer to purchase at a quoted price or not. Thus, customer

behaviour is easily extracted with the help of this management accounting system to derive

fruitful results. This is also essential so that customers are not attracted to rivals in any manner.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

This is effective technique by which organisation quotes price with reference to desire of

customers and as such, satisfaction level of customers are maximised up to high extent.

3. Inventory management system

Inventory management system is quite essential system of management accounting which

is used to manage inventory in the best possible way. This is essential as resources are scarce and

it is required that effective utilisation of the same should be made to derive better results.

Numerous orders are received from customers on daily basis and as such, it is required that

Morphy Richards Company should use the resources in effective way so that demand can be met

of customers by providing required quantum of stock to production department. If there is less

quantity of inventory in the warehouse, then demand of production department cannot be

satisfied and as such, production cannot be achieved (Honggowati and et.al, 2017). On the other

hand, if excess inventory is present, then additional costs of handling is incurred. Thus, it is

required that inventory should be managed to accomplish production

P2 Methods of management accounting reporting and benefits of management accounting

systems

Management accounting reporting is quite significant for the company to generate

relevant information about internal operations of the company in the best possible way. The

various methods of management accounting reporting are as follows-

1. Performance report:

Performance report is quite essential reporting method used by the management to assess

performance of something in the organisation. Usually, employees performance is being assessed

by the company to check their progress towards work whether they are achieving productivity or

not. Morphy Richards Company also uses this report to evaluate performance of workers in the

organisation. This is necessary so that efficiency and productivity can be enhanced in the best

possible manner. This is important for company so that common goals may be accomplished in

effective way. It is essential for evaluating and monitoring performance of the company with

much ease (Bennett and James, 2017). Planned results can be compared with actual results by the

management and as such, desired outcomes can be achieved. This is important so that corrective

action can be taken so that performance of workers can be improved if deficiencies are found.

3

customers and as such, satisfaction level of customers are maximised up to high extent.

3. Inventory management system

Inventory management system is quite essential system of management accounting which

is used to manage inventory in the best possible way. This is essential as resources are scarce and

it is required that effective utilisation of the same should be made to derive better results.

Numerous orders are received from customers on daily basis and as such, it is required that

Morphy Richards Company should use the resources in effective way so that demand can be met

of customers by providing required quantum of stock to production department. If there is less

quantity of inventory in the warehouse, then demand of production department cannot be

satisfied and as such, production cannot be achieved (Honggowati and et.al, 2017). On the other

hand, if excess inventory is present, then additional costs of handling is incurred. Thus, it is

required that inventory should be managed to accomplish production

P2 Methods of management accounting reporting and benefits of management accounting

systems

Management accounting reporting is quite significant for the company to generate

relevant information about internal operations of the company in the best possible way. The

various methods of management accounting reporting are as follows-

1. Performance report:

Performance report is quite essential reporting method used by the management to assess

performance of something in the organisation. Usually, employees performance is being assessed

by the company to check their progress towards work whether they are achieving productivity or

not. Morphy Richards Company also uses this report to evaluate performance of workers in the

organisation. This is necessary so that efficiency and productivity can be enhanced in the best

possible manner. This is important for company so that common goals may be accomplished in

effective way. It is essential for evaluating and monitoring performance of the company with

much ease (Bennett and James, 2017). Planned results can be compared with actual results by the

management and as such, desired outcomes can be achieved. This is important so that corrective

action can be taken so that performance of workers can be improved if deficiencies are found.

3

2. Inventory management report:

Inventory is integral part of the company and without it, production cannot be

accomplished. Inventory plays important role in the company and as such, desired production

can be achieved. Inventory is required to be ordered in adequate quantity so that demand of

production department can be easily achieved. This is important so that desired production can

be done without any wastage. If more than required quantity is ordered from suppliers, then it

will lead to unnecessary addition to handling inventory in the warehouse. Thus, excess quantum

of stock leads to addition in expenses of the organisation (Christ and Burritt, 2017). It is required

that production department should prepare inventory report in which need and demand of

required inventory should be stated. This report is then forwarded to management to analyse the

need of production department and as such, adequate inventory can be ordered without leading to

spoilage.

3. Accounts receivables ageing report:

Accounts receivables ageing report is another useful management accounting reporting

method which is used to derive effective results. Customers are allowed credit facilities so that

payment can be made afterwards. This is essential for the company so that customers may be

benefited by paying after and purchasing before the payment. This enhances customer

satisfaction and they become loyal to the company. Morphy Richards Company also provides

credit facilities to consumers so that they may become loyal towards it. Management prepares

accounts receivables ageing report which is based on unpaid customer invoices from which

outstanding amount need to be recovered.

This report paves the way for the organisation to recover amount pending from credit

customers. Thus, management analyses unpaid invoices and customers are contacted by concern

workers to pay the same. If credit is more outstanding, then organisation need to formulate well-

structures and strict strategies so that timely payments can be done by the customers (Ax and

Greve, 2017).

There are various benefits of management accounting systems which are already

discussed. It includes inventory management system, cost accounting system and price

optimisation. These are important aspect of the company so that benefits can be gained out of the

4

Inventory is integral part of the company and without it, production cannot be

accomplished. Inventory plays important role in the company and as such, desired production

can be achieved. Inventory is required to be ordered in adequate quantity so that demand of

production department can be easily achieved. This is important so that desired production can

be done without any wastage. If more than required quantity is ordered from suppliers, then it

will lead to unnecessary addition to handling inventory in the warehouse. Thus, excess quantum

of stock leads to addition in expenses of the organisation (Christ and Burritt, 2017). It is required

that production department should prepare inventory report in which need and demand of

required inventory should be stated. This report is then forwarded to management to analyse the

need of production department and as such, adequate inventory can be ordered without leading to

spoilage.

3. Accounts receivables ageing report:

Accounts receivables ageing report is another useful management accounting reporting

method which is used to derive effective results. Customers are allowed credit facilities so that

payment can be made afterwards. This is essential for the company so that customers may be

benefited by paying after and purchasing before the payment. This enhances customer

satisfaction and they become loyal to the company. Morphy Richards Company also provides

credit facilities to consumers so that they may become loyal towards it. Management prepares

accounts receivables ageing report which is based on unpaid customer invoices from which

outstanding amount need to be recovered.

This report paves the way for the organisation to recover amount pending from credit

customers. Thus, management analyses unpaid invoices and customers are contacted by concern

workers to pay the same. If credit is more outstanding, then organisation need to formulate well-

structures and strict strategies so that timely payments can be done by the customers (Ax and

Greve, 2017).

There are various benefits of management accounting systems which are already

discussed. It includes inventory management system, cost accounting system and price

optimisation. These are important aspect of the company so that benefits can be gained out of the

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

same. Starting from inventory management system which is used for managing inventory in the

best possible manner so that wastage of inventory can be minimised up to high extent. This help

production department to accomplish desired production and as such, customers are being

satisfied with much ease. This enhances overall productivity of organisation and timely goods

can be produced Morphy Richards Company with much ease.

On the other hand, cost accounting is beneficial for the company as it assess costs and

implements measures to reduce the same (ALIFARI and et.al, 2017). This help to have better

control and monitoring of expenses in effectual manner. Moreover, it is beneficial for making

budgets in effective way. This is done by comparing actual costs incurred over the budgeted

costs and as such, corrective actions are taken if costs are more than planned costs so that it can

be reduced quite effectively.

Price optimisation is also beneficial for the company as it help it to assess customer

behaviour in effective manner. Thus, it is quite essential for the organisation to check over

customers' attitude whether they are ready to purchase goods or not at quoted price. Thus, it is

beneficial for Morphy Richards Company so that it may set price in accordance to preference of

customers.

P3 Marginal and absorption costing

A) Difference in profits

Absorption Q1

Particulars Amount (in £)

Sales revenue 66000

Cost of goods manufactured (78000*.85) 66300

Closing stock (12000*.85) 10200

56100

5

best possible manner so that wastage of inventory can be minimised up to high extent. This help

production department to accomplish desired production and as such, customers are being

satisfied with much ease. This enhances overall productivity of organisation and timely goods

can be produced Morphy Richards Company with much ease.

On the other hand, cost accounting is beneficial for the company as it assess costs and

implements measures to reduce the same (ALIFARI and et.al, 2017). This help to have better

control and monitoring of expenses in effectual manner. Moreover, it is beneficial for making

budgets in effective way. This is done by comparing actual costs incurred over the budgeted

costs and as such, corrective actions are taken if costs are more than planned costs so that it can

be reduced quite effectively.

Price optimisation is also beneficial for the company as it help it to assess customer

behaviour in effective manner. Thus, it is quite essential for the organisation to check over

customers' attitude whether they are ready to purchase goods or not at quoted price. Thus, it is

beneficial for Morphy Richards Company so that it may set price in accordance to preference of

customers.

P3 Marginal and absorption costing

A) Difference in profits

Absorption Q1

Particulars Amount (in £)

Sales revenue 66000

Cost of goods manufactured (78000*.85) 66300

Closing stock (12000*.85) 10200

56100

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

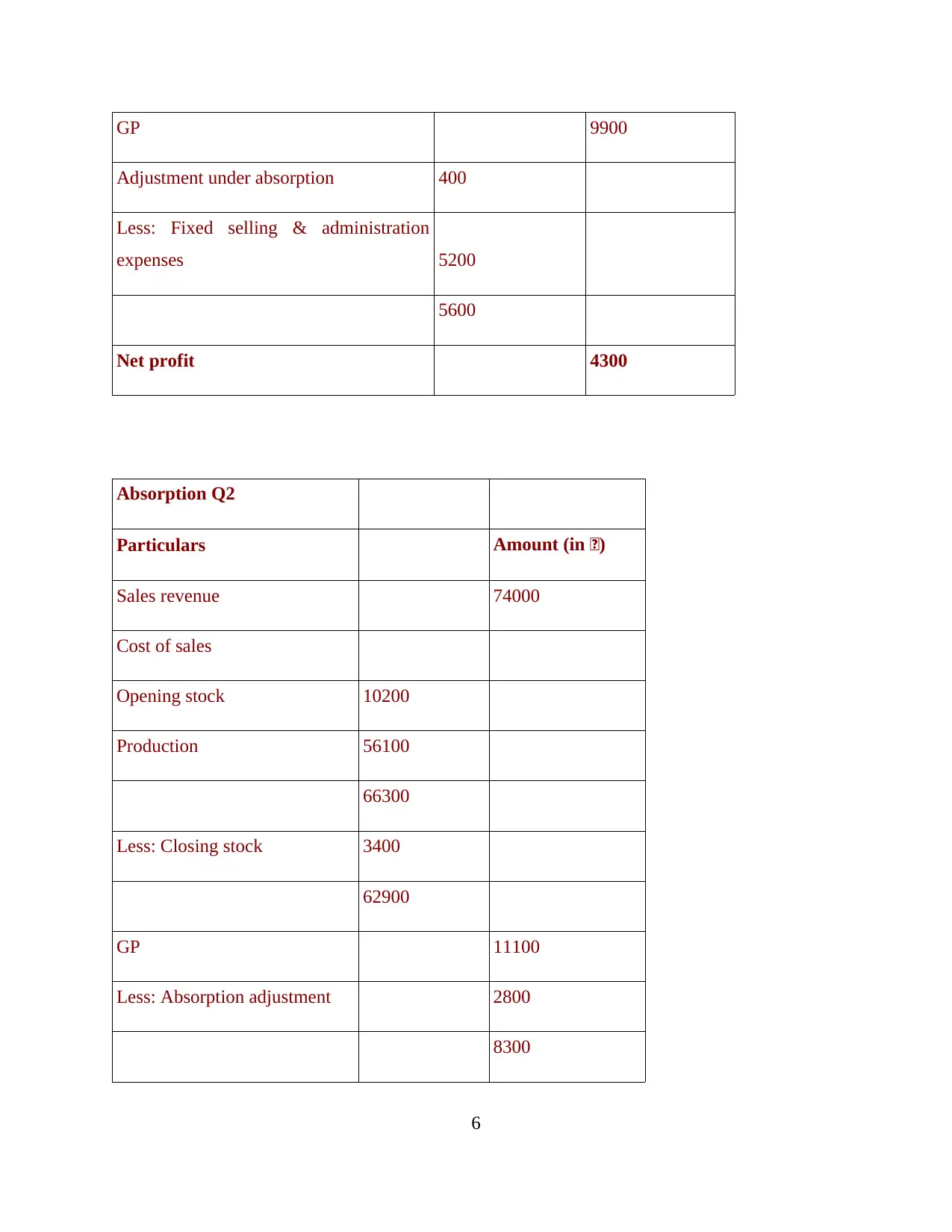

GP 9900

Adjustment under absorption 400

Less: Fixed selling & administration

expenses 5200

5600

Net profit 4300

Absorption Q2

Particulars Amount (in £)

Sales revenue 74000

Cost of sales

Opening stock 10200

Production 56100

66300

Less: Closing stock 3400

62900

GP 11100

Less: Absorption adjustment 2800

8300

6

Adjustment under absorption 400

Less: Fixed selling & administration

expenses 5200

5600

Net profit 4300

Absorption Q2

Particulars Amount (in £)

Sales revenue 74000

Cost of sales

Opening stock 10200

Production 56100

66300

Less: Closing stock 3400

62900

GP 11100

Less: Absorption adjustment 2800

8300

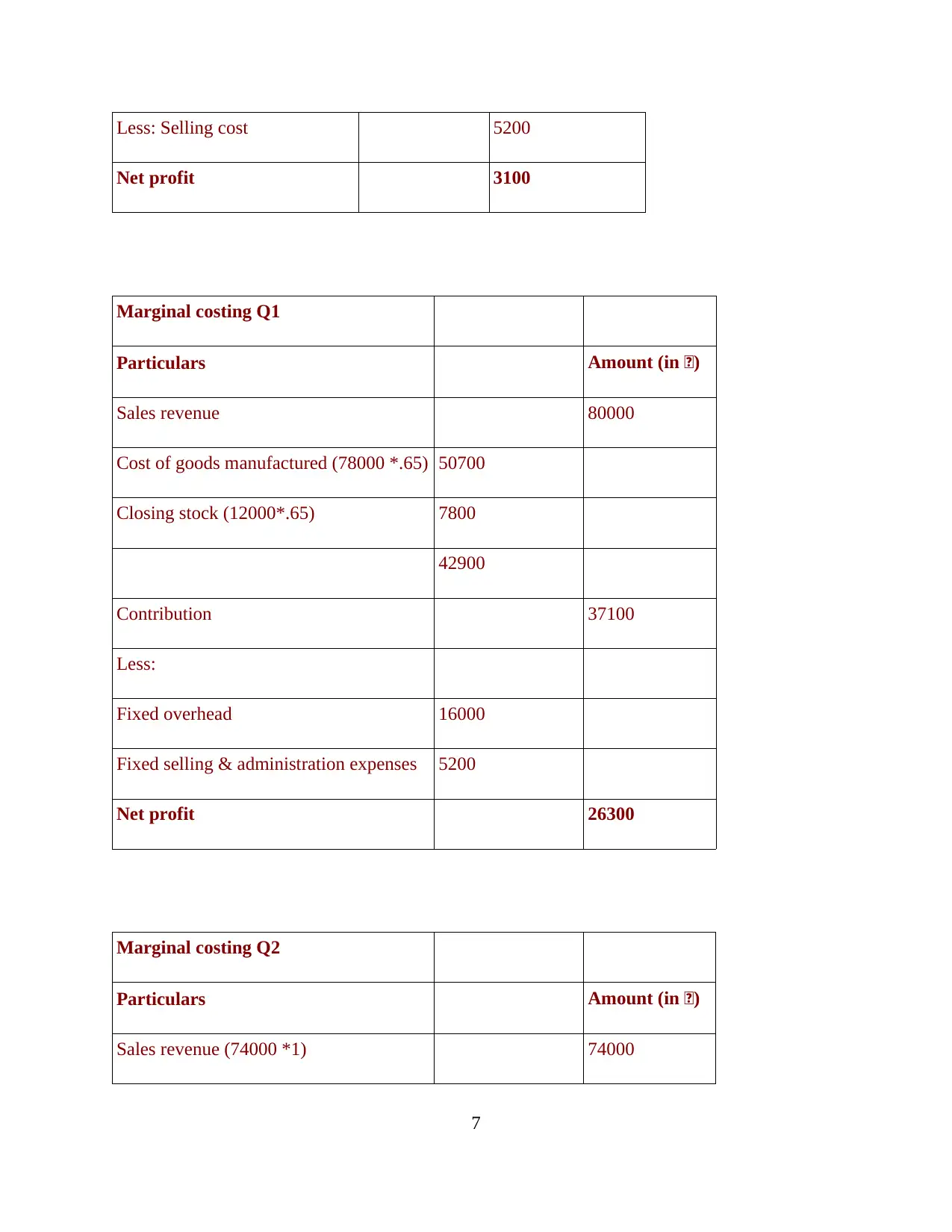

6

Less: Selling cost 5200

Net profit 3100

Marginal costing Q1

Particulars Amount (in £)

Sales revenue 80000

Cost of goods manufactured (78000 *.65) 50700

Closing stock (12000*.65) 7800

42900

Contribution 37100

Less:

Fixed overhead 16000

Fixed selling & administration expenses 5200

Net profit 26300

Marginal costing Q2

Particulars Amount (in £)

Sales revenue (74000 *1) 74000

7

Net profit 3100

Marginal costing Q1

Particulars Amount (in £)

Sales revenue 80000

Cost of goods manufactured (78000 *.65) 50700

Closing stock (12000*.65) 7800

42900

Contribution 37100

Less:

Fixed overhead 16000

Fixed selling & administration expenses 5200

Net profit 26300

Marginal costing Q2

Particulars Amount (in £)

Sales revenue (74000 *1) 74000

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

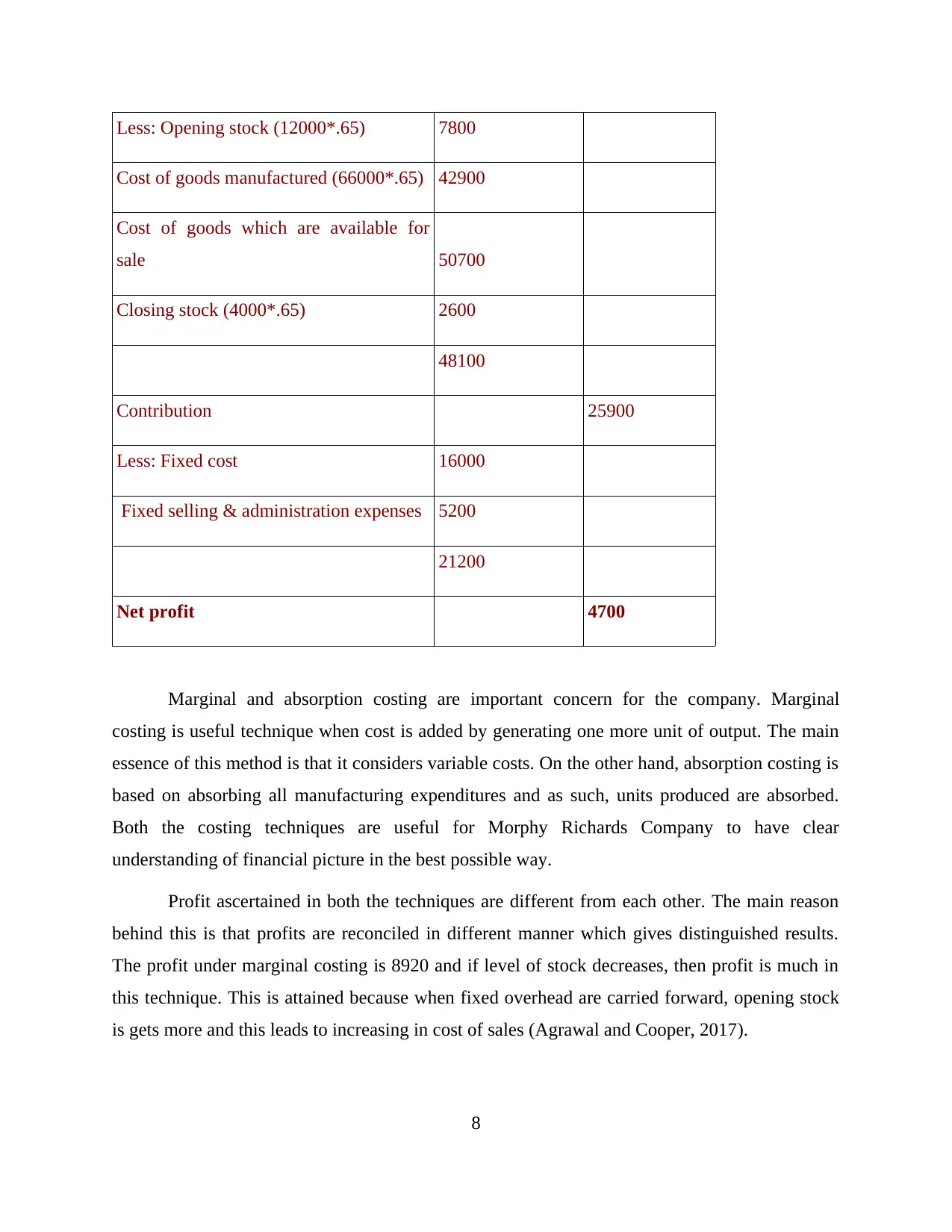

Less: Opening stock (12000*.65) 7800

Cost of goods manufactured (66000*.65) 42900

Cost of goods which are available for

sale 50700

Closing stock (4000*.65) 2600

48100

Contribution 25900

Less: Fixed cost 16000

Fixed selling & administration expenses 5200

21200

Net profit 4700

Marginal and absorption costing are important concern for the company. Marginal

costing is useful technique when cost is added by generating one more unit of output. The main

essence of this method is that it considers variable costs. On the other hand, absorption costing is

based on absorbing all manufacturing expenditures and as such, units produced are absorbed.

Both the costing techniques are useful for Morphy Richards Company to have clear

understanding of financial picture in the best possible way.

Profit ascertained in both the techniques are different from each other. The main reason

behind this is that profits are reconciled in different manner which gives distinguished results.

The profit under marginal costing is 8920 and if level of stock decreases, then profit is much in

this technique. This is attained because when fixed overhead are carried forward, opening stock

is gets more and this leads to increasing in cost of sales (Agrawal and Cooper, 2017).

8

Cost of goods manufactured (66000*.65) 42900

Cost of goods which are available for

sale 50700

Closing stock (4000*.65) 2600

48100

Contribution 25900

Less: Fixed cost 16000

Fixed selling & administration expenses 5200

21200

Net profit 4700

Marginal and absorption costing are important concern for the company. Marginal

costing is useful technique when cost is added by generating one more unit of output. The main

essence of this method is that it considers variable costs. On the other hand, absorption costing is

based on absorbing all manufacturing expenditures and as such, units produced are absorbed.

Both the costing techniques are useful for Morphy Richards Company to have clear

understanding of financial picture in the best possible way.

Profit ascertained in both the techniques are different from each other. The main reason

behind this is that profits are reconciled in different manner which gives distinguished results.

The profit under marginal costing is 8920 and if level of stock decreases, then profit is much in

this technique. This is attained because when fixed overhead are carried forward, opening stock

is gets more and this leads to increasing in cost of sales (Agrawal and Cooper, 2017).

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

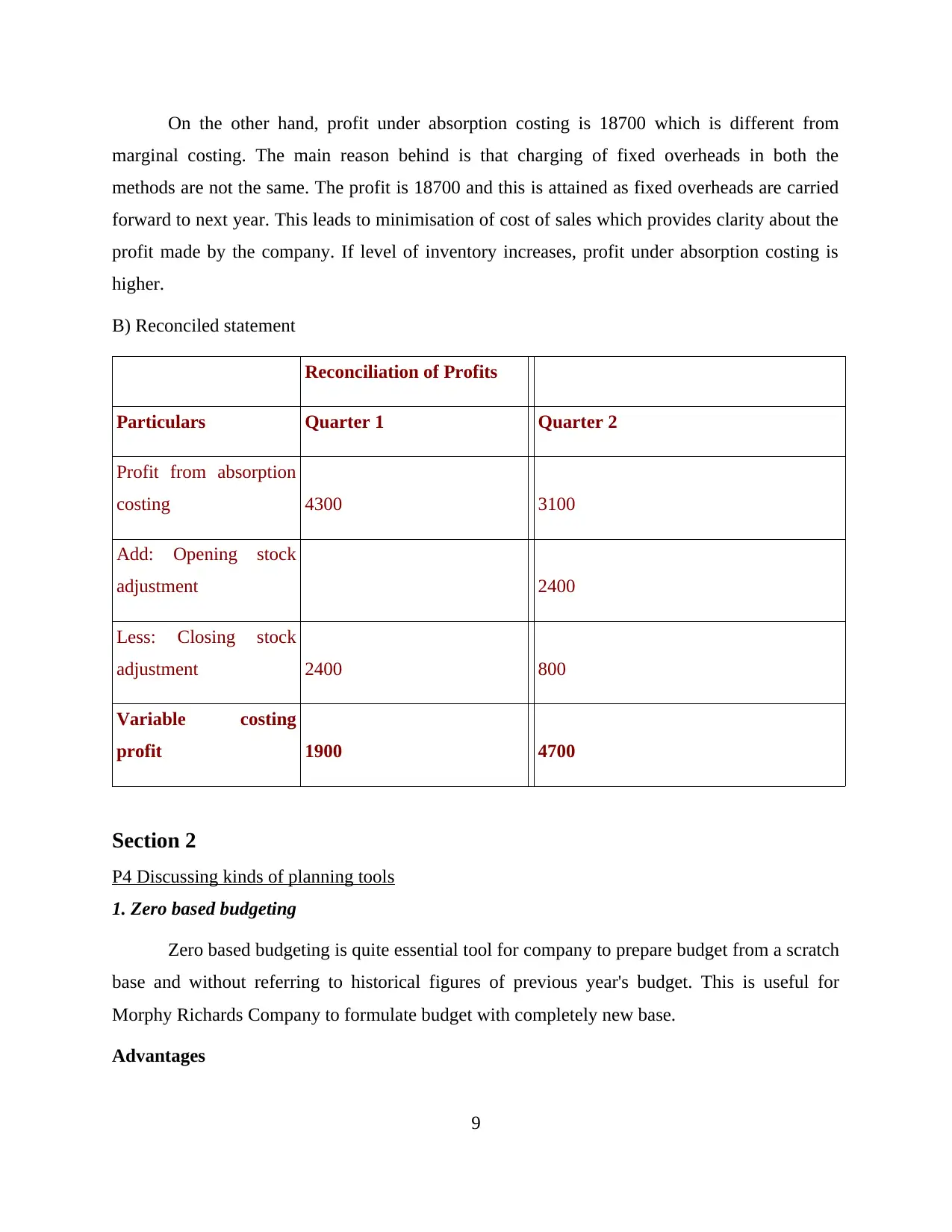

On the other hand, profit under absorption costing is 18700 which is different from

marginal costing. The main reason behind is that charging of fixed overheads in both the

methods are not the same. The profit is 18700 and this is attained as fixed overheads are carried

forward to next year. This leads to minimisation of cost of sales which provides clarity about the

profit made by the company. If level of inventory increases, profit under absorption costing is

higher.

B) Reconciled statement

Reconciliation of Profits

Particulars Quarter 1 Quarter 2

Profit from absorption

costing 4300 3100

Add: Opening stock

adjustment 2400

Less: Closing stock

adjustment 2400 800

Variable costing

profit 1900 4700

Section 2

P4 Discussing kinds of planning tools

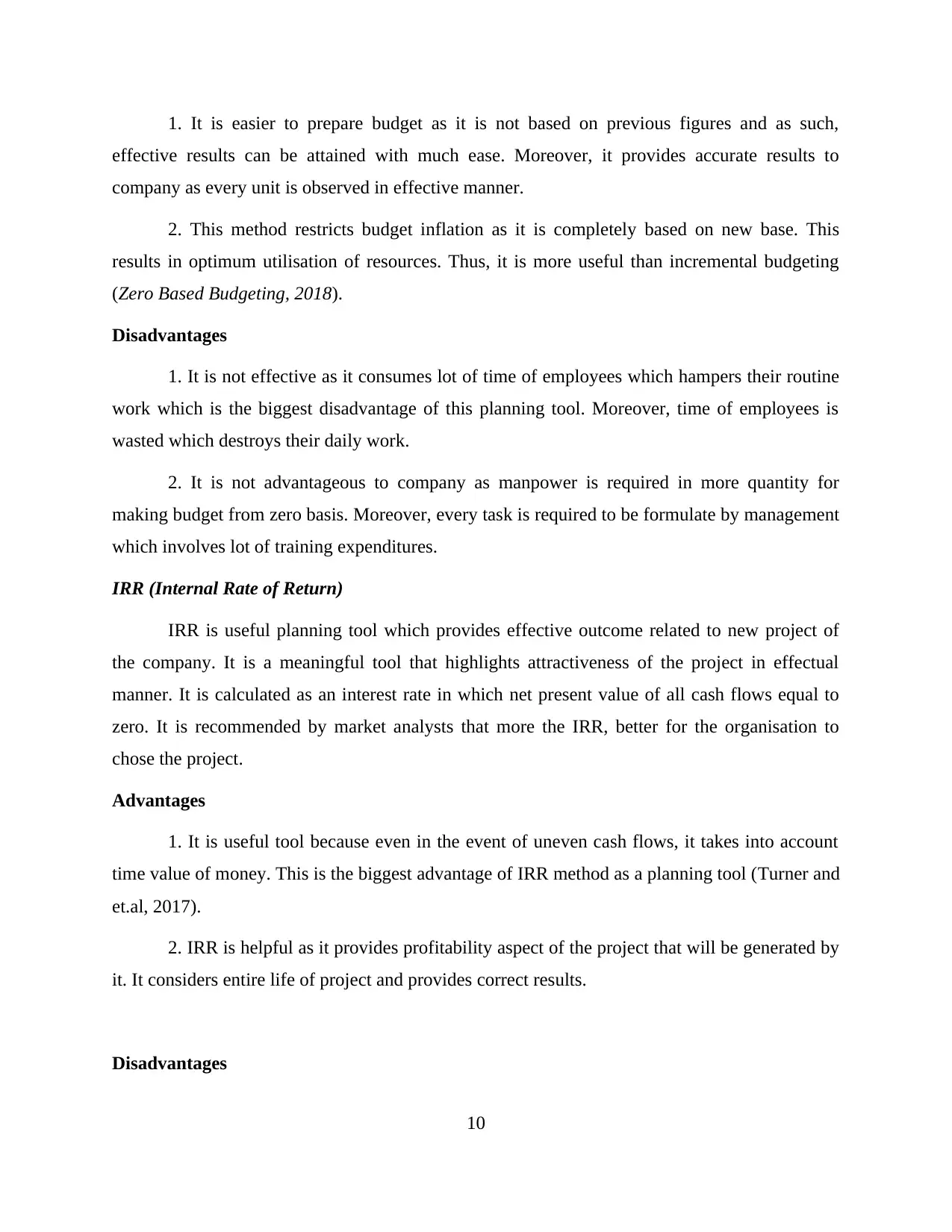

1. Zero based budgeting

Zero based budgeting is quite essential tool for company to prepare budget from a scratch

base and without referring to historical figures of previous year's budget. This is useful for

Morphy Richards Company to formulate budget with completely new base.

Advantages

9

marginal costing. The main reason behind is that charging of fixed overheads in both the

methods are not the same. The profit is 18700 and this is attained as fixed overheads are carried

forward to next year. This leads to minimisation of cost of sales which provides clarity about the

profit made by the company. If level of inventory increases, profit under absorption costing is

higher.

B) Reconciled statement

Reconciliation of Profits

Particulars Quarter 1 Quarter 2

Profit from absorption

costing 4300 3100

Add: Opening stock

adjustment 2400

Less: Closing stock

adjustment 2400 800

Variable costing

profit 1900 4700

Section 2

P4 Discussing kinds of planning tools

1. Zero based budgeting

Zero based budgeting is quite essential tool for company to prepare budget from a scratch

base and without referring to historical figures of previous year's budget. This is useful for

Morphy Richards Company to formulate budget with completely new base.

Advantages

9

1. It is easier to prepare budget as it is not based on previous figures and as such,

effective results can be attained with much ease. Moreover, it provides accurate results to

company as every unit is observed in effective manner.

2. This method restricts budget inflation as it is completely based on new base. This

results in optimum utilisation of resources. Thus, it is more useful than incremental budgeting

(Zero Based Budgeting, 2018).

Disadvantages

1. It is not effective as it consumes lot of time of employees which hampers their routine

work which is the biggest disadvantage of this planning tool. Moreover, time of employees is

wasted which destroys their daily work.

2. It is not advantageous to company as manpower is required in more quantity for

making budget from zero basis. Moreover, every task is required to be formulate by management

which involves lot of training expenditures.

IRR (Internal Rate of Return)

IRR is useful planning tool which provides effective outcome related to new project of

the company. It is a meaningful tool that highlights attractiveness of the project in effectual

manner. It is calculated as an interest rate in which net present value of all cash flows equal to

zero. It is recommended by market analysts that more the IRR, better for the organisation to

chose the project.

Advantages

1. It is useful tool because even in the event of uneven cash flows, it takes into account

time value of money. This is the biggest advantage of IRR method as a planning tool (Turner and

et.al, 2017).

2. IRR is helpful as it provides profitability aspect of the project that will be generated by

it. It considers entire life of project and provides correct results.

Disadvantages

10

effective results can be attained with much ease. Moreover, it provides accurate results to

company as every unit is observed in effective manner.

2. This method restricts budget inflation as it is completely based on new base. This

results in optimum utilisation of resources. Thus, it is more useful than incremental budgeting

(Zero Based Budgeting, 2018).

Disadvantages

1. It is not effective as it consumes lot of time of employees which hampers their routine

work which is the biggest disadvantage of this planning tool. Moreover, time of employees is

wasted which destroys their daily work.

2. It is not advantageous to company as manpower is required in more quantity for

making budget from zero basis. Moreover, every task is required to be formulate by management

which involves lot of training expenditures.

IRR (Internal Rate of Return)

IRR is useful planning tool which provides effective outcome related to new project of

the company. It is a meaningful tool that highlights attractiveness of the project in effectual

manner. It is calculated as an interest rate in which net present value of all cash flows equal to

zero. It is recommended by market analysts that more the IRR, better for the organisation to

chose the project.

Advantages

1. It is useful tool because even in the event of uneven cash flows, it takes into account

time value of money. This is the biggest advantage of IRR method as a planning tool (Turner and

et.al, 2017).

2. IRR is helpful as it provides profitability aspect of the project that will be generated by

it. It considers entire life of project and provides correct results.

Disadvantages

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.