Analysis of Management Accounting Systems: Morrison Case Study

VerifiedAdded on 2020/10/23

|18

|6452

|124

Report

AI Summary

This report provides a comprehensive analysis of management accounting within an organization, focusing on the case study of Morrison. It begins with an executive summary highlighting the importance, benefits, and various types of management accounting systems. The report then delves into the specifics of management accounting systems, including cost accounting, budgeting, transfer pricing, and inventory management. It explores the differences between management and financial accounting. The report includes the preparation of income statements using both marginal and absorption costing. The report also examines the use of planning tools for budgetary control, evaluating their advantages and disadvantages. Furthermore, the report assesses how organizations adapt to management accounting systems and uses them to address financial problems and achieve sustainable success. Finally, the report concludes with recommendations based on the analysis.

UNIT 5 MANAGEMENT ACCOUNTING

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive summary

The study has evaluated the importance of management accounting in an organisation.

The study has evaluated the benefits and different types of management accounting

system used by Morrison. Advantages and disadvantages of planning tools have also

been discussed in the study. Application and integration of management accounting

techniques along with systems in the organisation has been assessed. The study has

outlined features and usage of various management accounting methods like budgetary

cost, marginal cost and many more in the study. Income statements have been

prepared based on marginal and absorption costing. Comparisons based on

management accounting system s adapted by Morrison have been also discussed in

detail.

2

The study has evaluated the importance of management accounting in an organisation.

The study has evaluated the benefits and different types of management accounting

system used by Morrison. Advantages and disadvantages of planning tools have also

been discussed in the study. Application and integration of management accounting

techniques along with systems in the organisation has been assessed. The study has

outlined features and usage of various management accounting methods like budgetary

cost, marginal cost and many more in the study. Income statements have been

prepared based on marginal and absorption costing. Comparisons based on

management accounting system s adapted by Morrison have been also discussed in

detail.

2

Table of Contents

Introduction....................................................................................................................................4

LO1: Management accounting systems .......................................................................................4

Brief description of organization................................................................................................4

Explanation of Management accounting and types of management accounting system (P1). .4

Different Methods of management accounting reporting [P2] ..................................................6

Benefits of management accounting system and its application (M1) ......................................6

Integration of management accounting system and reporting (D1)...........................................7

LO2 Range of Management accounting techniques.....................................................................7

Preparation of income statements using (P3) ...........................................................................7

a) Marginal costing [Refer to appendix 1]..............................................................................7

b) Absorption costing [Refer to appendix 2]............................................................................8

Application of range of management accounting techniques and production of financial

reports (M2) ..............................................................................................................................8

Financial reports (D2) ...............................................................................................................8

LO3 use of planning tools in management accounting ................................................................9

Advantages and disadvantages of planning tools that are used for budgetary control (P4) ....9

Analysis of planning tools usage and application (M3)...............................................................11

LO4 Using management accounting to respond financial problems...........................................12

Comparison of the ways in which organization adapt to management accounting system (P5)

.................................................................................................................................................12

Analysis of management accounting leading to sustainable success (M4) ............................14

Evaluation of planning tools usage to solve financial problems and lead to sustainable

success (D3) ...........................................................................................................................14

Recommendation and Conclusion .............................................................................................14

Reference list...............................................................................................................................16

Appendices..................................................................................................................................17

3

Introduction....................................................................................................................................4

LO1: Management accounting systems .......................................................................................4

Brief description of organization................................................................................................4

Explanation of Management accounting and types of management accounting system (P1). .4

Different Methods of management accounting reporting [P2] ..................................................6

Benefits of management accounting system and its application (M1) ......................................6

Integration of management accounting system and reporting (D1)...........................................7

LO2 Range of Management accounting techniques.....................................................................7

Preparation of income statements using (P3) ...........................................................................7

a) Marginal costing [Refer to appendix 1]..............................................................................7

b) Absorption costing [Refer to appendix 2]............................................................................8

Application of range of management accounting techniques and production of financial

reports (M2) ..............................................................................................................................8

Financial reports (D2) ...............................................................................................................8

LO3 use of planning tools in management accounting ................................................................9

Advantages and disadvantages of planning tools that are used for budgetary control (P4) ....9

Analysis of planning tools usage and application (M3)...............................................................11

LO4 Using management accounting to respond financial problems...........................................12

Comparison of the ways in which organization adapt to management accounting system (P5)

.................................................................................................................................................12

Analysis of management accounting leading to sustainable success (M4) ............................14

Evaluation of planning tools usage to solve financial problems and lead to sustainable

success (D3) ...........................................................................................................................14

Recommendation and Conclusion .............................................................................................14

Reference list...............................................................................................................................16

Appendices..................................................................................................................................17

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

Management accounting provides the managers of an organization with relevant and

important information which helps them in decision making process. The study has

evaluated different types of management accounting systems has provided an

explanation of its usage and application to achieve sustainable success. Preparation of

income statements using marginal costing and absorption costing has been done in the

study. In this study the management accounting system adopted by Morrisons have

been discussed. The problem statement of the study is to analyse the importance and

application of management accounting techniques.

LO1: Management accounting systems

Brief description of organization

Morrisons is one of the leading companies of the food retail sector and has its

headquarters in Bradford, UK. It is one the biggest and the fourth largest supermarket

established and made a revenue of 1631.7 crores GBP in the financial year of 2017

(morrisons.com, 2018). The Morrison Company belongs to the retail industry and

is headquartered at Bradford within province of England. It is taken as a public

limited company. The company has in present around 498 stores spread globally

(morrisons.com, 2018). The company has products differentiations in form of

clothing, magazines, books, DVDs and CDs and food and beverages. The

company is with favourable employee strength of 132,000 employees. Apart from

that, there company has a revenue generation in around GBP 16317 million

(morrisons.com, 2018). The company on other hand is having an operational

income in GBP 468 millions.

Explanation of Management accounting and types of management

accounting system (P1)

The origin of management accounting can be traced back to 300 years ago. It first

emerged during the industrial revolution period. It was used in the European merchant

trading ventures and it was looked at from two perspectives (businessperspectives.org,

2018). One was economic perspective and the other was non-economic perspective.

From the economic viewpoint it was assumed that management accounting originated

from the private sector. Whereas the non-economic approach suggests that it originated

from the public sector. Management accounting is the system of identifying, measuring

and analysing the financial as well as non financial information. It utilises different

techniques like cost accounting, break even analysis, standard costing and many others

to analyse expenses and revenues. As per the opinion of Kaplan & Atkinson (2015:23-

29), it plays a significant role in the decision making process since managers are able to

identify variances by comparing actual with expected costs. Moreover it also helps in

setting budgets and choosing the most profitable orders.

4

Management accounting provides the managers of an organization with relevant and

important information which helps them in decision making process. The study has

evaluated different types of management accounting systems has provided an

explanation of its usage and application to achieve sustainable success. Preparation of

income statements using marginal costing and absorption costing has been done in the

study. In this study the management accounting system adopted by Morrisons have

been discussed. The problem statement of the study is to analyse the importance and

application of management accounting techniques.

LO1: Management accounting systems

Brief description of organization

Morrisons is one of the leading companies of the food retail sector and has its

headquarters in Bradford, UK. It is one the biggest and the fourth largest supermarket

established and made a revenue of 1631.7 crores GBP in the financial year of 2017

(morrisons.com, 2018). The Morrison Company belongs to the retail industry and

is headquartered at Bradford within province of England. It is taken as a public

limited company. The company has in present around 498 stores spread globally

(morrisons.com, 2018). The company has products differentiations in form of

clothing, magazines, books, DVDs and CDs and food and beverages. The

company is with favourable employee strength of 132,000 employees. Apart from

that, there company has a revenue generation in around GBP 16317 million

(morrisons.com, 2018). The company on other hand is having an operational

income in GBP 468 millions.

Explanation of Management accounting and types of management

accounting system (P1)

The origin of management accounting can be traced back to 300 years ago. It first

emerged during the industrial revolution period. It was used in the European merchant

trading ventures and it was looked at from two perspectives (businessperspectives.org,

2018). One was economic perspective and the other was non-economic perspective.

From the economic viewpoint it was assumed that management accounting originated

from the private sector. Whereas the non-economic approach suggests that it originated

from the public sector. Management accounting is the system of identifying, measuring

and analysing the financial as well as non financial information. It utilises different

techniques like cost accounting, break even analysis, standard costing and many others

to analyse expenses and revenues. As per the opinion of Kaplan & Atkinson (2015:23-

29), it plays a significant role in the decision making process since managers are able to

identify variances by comparing actual with expected costs. Moreover it also helps in

setting budgets and choosing the most profitable orders.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Different types of management accounting system are discussed as follows;

Cost accounting

Cost accounting deals with recording and managing costs. It refers to the system of

recording costs and comparison of inputs and outputs from the production process. As

suggested by Kihn & Ihantola (2015:230-255), it helps in comparing results against

standards set with the application of standard costing and also helps in choosing

between different projects. Marginal costing and activity based costing are one of its

subtypes. In case of Morrisons, marginal costing and standard costing is used to control

different types of cost. The efficiency of this system lies in the fact that cost allocation is

done appropriately, moreover it also helps in indentifying the drivers and cost pools.

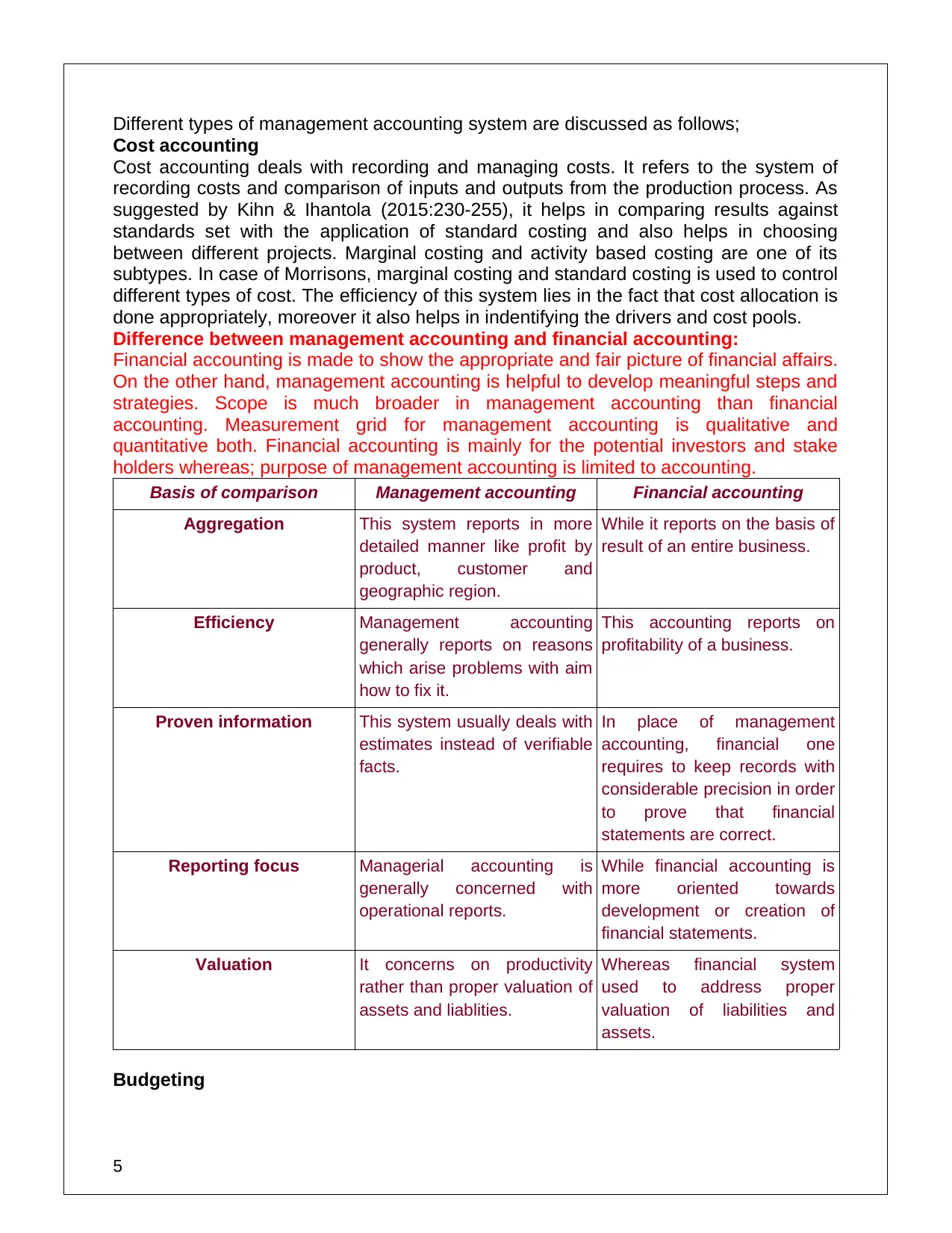

Difference between management accounting and financial accounting:

Financial accounting is made to show the appropriate and fair picture of financial affairs.

On the other hand, management accounting is helpful to develop meaningful steps and

strategies. Scope is much broader in management accounting than financial

accounting. Measurement grid for management accounting is qualitative and

quantitative both. Financial accounting is mainly for the potential investors and stake

holders whereas; purpose of management accounting is limited to accounting.

Basis of comparison Management accounting Financial accounting

Aggregation This system reports in more

detailed manner like profit by

product, customer and

geographic region.

While it reports on the basis of

result of an entire business.

Efficiency Management accounting

generally reports on reasons

which arise problems with aim

how to fix it.

This accounting reports on

profitability of a business.

Proven information This system usually deals with

estimates instead of verifiable

facts.

In place of management

accounting, financial one

requires to keep records with

considerable precision in order

to prove that financial

statements are correct.

Reporting focus Managerial accounting is

generally concerned with

operational reports.

While financial accounting is

more oriented towards

development or creation of

financial statements.

Valuation It concerns on productivity

rather than proper valuation of

assets and liablities.

Whereas financial system

used to address proper

valuation of liabilities and

assets.

Budgeting

5

Cost accounting

Cost accounting deals with recording and managing costs. It refers to the system of

recording costs and comparison of inputs and outputs from the production process. As

suggested by Kihn & Ihantola (2015:230-255), it helps in comparing results against

standards set with the application of standard costing and also helps in choosing

between different projects. Marginal costing and activity based costing are one of its

subtypes. In case of Morrisons, marginal costing and standard costing is used to control

different types of cost. The efficiency of this system lies in the fact that cost allocation is

done appropriately, moreover it also helps in indentifying the drivers and cost pools.

Difference between management accounting and financial accounting:

Financial accounting is made to show the appropriate and fair picture of financial affairs.

On the other hand, management accounting is helpful to develop meaningful steps and

strategies. Scope is much broader in management accounting than financial

accounting. Measurement grid for management accounting is qualitative and

quantitative both. Financial accounting is mainly for the potential investors and stake

holders whereas; purpose of management accounting is limited to accounting.

Basis of comparison Management accounting Financial accounting

Aggregation This system reports in more

detailed manner like profit by

product, customer and

geographic region.

While it reports on the basis of

result of an entire business.

Efficiency Management accounting

generally reports on reasons

which arise problems with aim

how to fix it.

This accounting reports on

profitability of a business.

Proven information This system usually deals with

estimates instead of verifiable

facts.

In place of management

accounting, financial one

requires to keep records with

considerable precision in order

to prove that financial

statements are correct.

Reporting focus Managerial accounting is

generally concerned with

operational reports.

While financial accounting is

more oriented towards

development or creation of

financial statements.

Valuation It concerns on productivity

rather than proper valuation of

assets and liablities.

Whereas financial system

used to address proper

valuation of liabilities and

assets.

Budgeting

5

It comes to use in the preparation of budgets. It helps in assessing the departmental

needs and budgets and then prepares an overall budget for the organization. Expenses

are allocated on the basis of units to be produced and also department or function wise.

Preparation of budgets in Morrisons is done on quarterly basis so that cost control is

done effectively. It’s essential requirement is that it helps in controlling costs related to

an organisation and keeps helps in removing unnecessary expenses.

Transfer pricing

According to the definition given by Mittendorf (2015:121-122), it helps in setting prices

for the goods or raw material transferred within an organisation. It also helps in

comparing the costs of accepting orders from outside and producing it internally.

Morrison practices this method in order to determine minimum transfer prices. The

essential requirement of this system is that it helps in choosing between selling goods

outside and transferring between different departments within a company.

Inventory management system

It is the system which is useful in managing large amount of inventory in an entity. The

efficiency of this system is defined by the way it helps in evaluating the amount of

inventory required to meet the production or sales process. It also creates a balance

between demands and supplies. Morrisons uses this type of management accounting in

order to manage its large and varied range of inventories (morrisons.com, 2018). LIFO

method assumes that last stock which has entered is sold out first. Whereas, FIFO

method assumes that first stock which has entered is sold out first. AVCO on the other

hand, measures cost of closing stock at weighted average cost of purchases.

Figure 1: Management accounting system

(Source: learner)

Essential elements related to Management accounting system:

Government and risk management are associated with management accounting

system. Additionally, it is necessary to develop a strategic planning and execution with

the help of balanced scorecard, operational dashboard. Measuring performance

management is another necessary aspect that has to be based on the performance of

the management accounting system. Planning, forecasting, service delivery and value

recognition are among the other essential elements in management accounting system.

Different Methods of management accounting reporting [P2]

Budget report

As opined by Cooper et al. (2017:991-1025), it is a form of an internal report which is

prepared in order to show the different types of budgets prepared. It provides with

information which help managers compare between the estimated costs and the actual

costs incurred. The management of Morrisons prepare reports on a quarterly basis. Its

importance lies in the fact that it helps in controlling costs and highlighting cost items

which are required to be managed.

Capital appraisal methods

This method helps in evaluating the best investment opportunity that could be

undertaken by the company and involves measures like IRR, ARR, and NPV. It

6

needs and budgets and then prepares an overall budget for the organization. Expenses

are allocated on the basis of units to be produced and also department or function wise.

Preparation of budgets in Morrisons is done on quarterly basis so that cost control is

done effectively. It’s essential requirement is that it helps in controlling costs related to

an organisation and keeps helps in removing unnecessary expenses.

Transfer pricing

According to the definition given by Mittendorf (2015:121-122), it helps in setting prices

for the goods or raw material transferred within an organisation. It also helps in

comparing the costs of accepting orders from outside and producing it internally.

Morrison practices this method in order to determine minimum transfer prices. The

essential requirement of this system is that it helps in choosing between selling goods

outside and transferring between different departments within a company.

Inventory management system

It is the system which is useful in managing large amount of inventory in an entity. The

efficiency of this system is defined by the way it helps in evaluating the amount of

inventory required to meet the production or sales process. It also creates a balance

between demands and supplies. Morrisons uses this type of management accounting in

order to manage its large and varied range of inventories (morrisons.com, 2018). LIFO

method assumes that last stock which has entered is sold out first. Whereas, FIFO

method assumes that first stock which has entered is sold out first. AVCO on the other

hand, measures cost of closing stock at weighted average cost of purchases.

Figure 1: Management accounting system

(Source: learner)

Essential elements related to Management accounting system:

Government and risk management are associated with management accounting

system. Additionally, it is necessary to develop a strategic planning and execution with

the help of balanced scorecard, operational dashboard. Measuring performance

management is another necessary aspect that has to be based on the performance of

the management accounting system. Planning, forecasting, service delivery and value

recognition are among the other essential elements in management accounting system.

Different Methods of management accounting reporting [P2]

Budget report

As opined by Cooper et al. (2017:991-1025), it is a form of an internal report which is

prepared in order to show the different types of budgets prepared. It provides with

information which help managers compare between the estimated costs and the actual

costs incurred. The management of Morrisons prepare reports on a quarterly basis. Its

importance lies in the fact that it helps in controlling costs and highlighting cost items

which are required to be managed.

Capital appraisal methods

This method helps in evaluating the best investment opportunity that could be

undertaken by the company and involves measures like IRR, ARR, and NPV. It

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

provides the managers with range of times period within which initial investment done

could return. The project which takes the least amount of time is selected by the

managers.

Benefits of management accounting system and its application (M1)

Cost accounting

It helps in setting standards and also provides a benchmark to compare against.

This in turn helps in analysing the variances and costs are controlled (Hague,

2018:6-9).

It is significant in calculation of contributions made by different machines or

project. Therefore it helps in making decisions related to buying or manufacturing

and accepting or rejecting orders.

Morrisons uses standard costing and marginal costing in order to manage costs

effectively.

Budgeting

It also helps in cost control process.

It helps in allocating different costs as per their importance and functions.

Morrisons prepares budgets quarterly and uses it as an effective tool to control

expenses.

Transfer pricing

Transfer pricing helps in comparing situations of transferring raw material

internally and selling it outside the organisations.

Minimum transfer prices can also be calculated with the application of transfer

pricing and it makes the internal process smooth (Van der Stede, 2016:100-102).

Inventory management system

It provides with different measures to determine the level and direction of using

stocks in an organization.

Inventory management system is used by Morrisons to analyse the level of inventory so

that the organization does not suffer from lack resources.

Integration of management accounting system and reporting (D1)

Since the management of Morrison uses budgeting, cost accounting and inventory

management system hence the managers are required to prepare reports related to

these. Budgeting reports preparation is integrated well with the budgeting system of

management accounting. Budgeting reports are prepared as part of budgeting system

and it is prepared on a quarterly basis by Morrisons. Managers report on facts outlining

the estimated expenses and revenues to be received. On the other hand, expenses and

revenues are compared with the actual performance of the company on a quarterly

term. As a part of cost accounting system cost reports are prepared which helps in

outlining cost related to specific activities. Standard costing is used by Morrisons, which

helps in evaluating the performances of the company based on costs saved or incurred.

This is reported with the help of standard cost income statements. Moreover inventory

control system has been applied within the organization and it uses LIFO method. In

order to report about the quantities used through inventory valuation summary reports.

7

could return. The project which takes the least amount of time is selected by the

managers.

Benefits of management accounting system and its application (M1)

Cost accounting

It helps in setting standards and also provides a benchmark to compare against.

This in turn helps in analysing the variances and costs are controlled (Hague,

2018:6-9).

It is significant in calculation of contributions made by different machines or

project. Therefore it helps in making decisions related to buying or manufacturing

and accepting or rejecting orders.

Morrisons uses standard costing and marginal costing in order to manage costs

effectively.

Budgeting

It also helps in cost control process.

It helps in allocating different costs as per their importance and functions.

Morrisons prepares budgets quarterly and uses it as an effective tool to control

expenses.

Transfer pricing

Transfer pricing helps in comparing situations of transferring raw material

internally and selling it outside the organisations.

Minimum transfer prices can also be calculated with the application of transfer

pricing and it makes the internal process smooth (Van der Stede, 2016:100-102).

Inventory management system

It provides with different measures to determine the level and direction of using

stocks in an organization.

Inventory management system is used by Morrisons to analyse the level of inventory so

that the organization does not suffer from lack resources.

Integration of management accounting system and reporting (D1)

Since the management of Morrison uses budgeting, cost accounting and inventory

management system hence the managers are required to prepare reports related to

these. Budgeting reports preparation is integrated well with the budgeting system of

management accounting. Budgeting reports are prepared as part of budgeting system

and it is prepared on a quarterly basis by Morrisons. Managers report on facts outlining

the estimated expenses and revenues to be received. On the other hand, expenses and

revenues are compared with the actual performance of the company on a quarterly

term. As a part of cost accounting system cost reports are prepared which helps in

outlining cost related to specific activities. Standard costing is used by Morrisons, which

helps in evaluating the performances of the company based on costs saved or incurred.

This is reported with the help of standard cost income statements. Moreover inventory

control system has been applied within the organization and it uses LIFO method. In

order to report about the quantities used through inventory valuation summary reports.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

LO2 Range of Management accounting techniques

Preparation of income statements using (P3)

a) Marginal costing [Refer to appendix 1]

Marginal costing is one of the most effective cost accounting methods which can be

used under different situations. Income statements prepared under this shows the

amount of sales deducted by variable cost to give contribution amount. Machines or

projects are compared in terms of contribution (Armitage et al. 2016:31-69). Project or

order is ranked on the basis of contribution and the least one is rejected. In this case

fixed expenses are deducted at last from the contribution amount in order to calculate

net profit. The method is usually applied in situations where decisions related to make

or buy are required to be taken. It is also applied in situations of accepting or rejecting

export order. According to the view of Otley (2016:45-62), marginal costing is more

accurate than absorption costing as it does not allocate fixed expenses in terms of units

produced.

b) Absorption costing [Refer to appendix 2]

This method takes into account all directs costs such direct material costs, direct labour

cost and variable overheads. It does not take fixed expenses and it assumes full costing

method. Sales are deducted with all forms of direct costs and fixed cost is also divided

in terms of number of units produced. After this the over or under absorbed costs is

deducted with all forms of administrative expenses or selling expenses to determine net

profit. It is of more realistic approach as it assumes that all inventories are not sold out

and that some are left as closing stock in the organisation (Hall, 2016:63-74).

The net profit as calculated under both the methods is £ 794230. The reason for same

profits obtained under both absorption costing and marginal costing is that there have

been no changes in the levels of inventory. Furthermore there was no inventory at the

beginning of the period as well as at the end of the period.

Application of range of management accounting techniques and

production of financial reports (M2)

Cost volume analysis

It measures the amount of impact variable cost; sales and fixed expense have on the

amount of profits. It helps the organisation to reduce costs effectively since the level of

impact is known. On the other hand it also helps in evaluating the level of profits

required to cover all variable expenses incurred by an organization.

Budgeting

Morrisons uses the technique of budgeting to control costs and prepares budget reports

quarterly to help it analyse the variances. Budgets are prepared for all departments

present in the organisation. The expected level of expenses makes the management

8

Preparation of income statements using (P3)

a) Marginal costing [Refer to appendix 1]

Marginal costing is one of the most effective cost accounting methods which can be

used under different situations. Income statements prepared under this shows the

amount of sales deducted by variable cost to give contribution amount. Machines or

projects are compared in terms of contribution (Armitage et al. 2016:31-69). Project or

order is ranked on the basis of contribution and the least one is rejected. In this case

fixed expenses are deducted at last from the contribution amount in order to calculate

net profit. The method is usually applied in situations where decisions related to make

or buy are required to be taken. It is also applied in situations of accepting or rejecting

export order. According to the view of Otley (2016:45-62), marginal costing is more

accurate than absorption costing as it does not allocate fixed expenses in terms of units

produced.

b) Absorption costing [Refer to appendix 2]

This method takes into account all directs costs such direct material costs, direct labour

cost and variable overheads. It does not take fixed expenses and it assumes full costing

method. Sales are deducted with all forms of direct costs and fixed cost is also divided

in terms of number of units produced. After this the over or under absorbed costs is

deducted with all forms of administrative expenses or selling expenses to determine net

profit. It is of more realistic approach as it assumes that all inventories are not sold out

and that some are left as closing stock in the organisation (Hall, 2016:63-74).

The net profit as calculated under both the methods is £ 794230. The reason for same

profits obtained under both absorption costing and marginal costing is that there have

been no changes in the levels of inventory. Furthermore there was no inventory at the

beginning of the period as well as at the end of the period.

Application of range of management accounting techniques and

production of financial reports (M2)

Cost volume analysis

It measures the amount of impact variable cost; sales and fixed expense have on the

amount of profits. It helps the organisation to reduce costs effectively since the level of

impact is known. On the other hand it also helps in evaluating the level of profits

required to cover all variable expenses incurred by an organization.

Budgeting

Morrisons uses the technique of budgeting to control costs and prepares budget reports

quarterly to help it analyse the variances. Budgets are prepared for all departments

present in the organisation. The expected level of expenses makes the management

8

measure all pros and cons. Effective steps are taken to prevent losses in the future.

Budget reports are useful if this technique is applied by an organization.

Capital appraisal techniques

Capital appraising techniques such NPV, IRR and ARR are used by Morrisons. NPV

provide the managers with present value of all future returns from the investment. IRR

on the other hand, ranks the projects in terms of profitability that can be derived from it.

The project which returns higher profits from the investment and takes the least time tin

cover initial investment is chosen. ARR is the average rate of return earned and time

me value of money is ignored by the method hence it is used less.

Here, NPV i.e. Net present value consider as difference between present value

of cash outflows and inflows. This analysis is sensitive towards reliability of future cash

inflows which is used in further capital budgeting for assessing the profitability of an

investment. Similarly, IRR (Internal rate of return) is taken as discounted rate and used

in capital budgeting for making NPV of all cash flows from a specific project equal to

zero. In management accounting, managers of Morrisons use concept of NPV for

estimating the future cash flows, which store may generate. While IRR is used to

estimate rate of growth which may generate after executing a project.

Financial reports (D2)

Financial reports that are required to be produced in case of inventory valuation and

standard costing are discussed as follows;

Variance report

It is the report which helps in compared planned or estimated outcomes against the

actual outcomes. The results are compared so that variances can be found out. The

variances are differences or deviations in the expected results (Weygandt et al.

2015:96-101). The reports prepared to show variances help the managers know in

which respect or department costs control is required to be applied. It shows all material

items and their expected as well as actual costs for a quarter. It will be helpful for

Morrison to identify the factors that are affecting on the cost controlling system.

Additionally, the managers can access idea about the company expenses and division

according to the department.

Inventory valuation reports

Inventory valuation reports as asserted by Malmi (2016:31-44), shoes or depicts the

quantity of raw material of stock used or sold for a given accounting period. Iis is

essential for the determination of cost of goods sold by the entity and is also used as

collateral by any organization. Since it deals with the most important current asset of an

organization hence the preparation of it report becomes essential and should be

manage it properly. Morrison can use reports for its current planning in the future

purposes.

Budgetary reports

Budgetary reports show the budget of all departments present in an organization. It

assists in analysing trends of revenues and projection of expenses. Preparation of

budget reports enables the management to know about the expenses which have gone

out of control and which are under the control of an organisation. With the help of

budgetary reports, Morrison can make its strategy for future expenses. The firm can be

9

Budget reports are useful if this technique is applied by an organization.

Capital appraisal techniques

Capital appraising techniques such NPV, IRR and ARR are used by Morrisons. NPV

provide the managers with present value of all future returns from the investment. IRR

on the other hand, ranks the projects in terms of profitability that can be derived from it.

The project which returns higher profits from the investment and takes the least time tin

cover initial investment is chosen. ARR is the average rate of return earned and time

me value of money is ignored by the method hence it is used less.

Here, NPV i.e. Net present value consider as difference between present value

of cash outflows and inflows. This analysis is sensitive towards reliability of future cash

inflows which is used in further capital budgeting for assessing the profitability of an

investment. Similarly, IRR (Internal rate of return) is taken as discounted rate and used

in capital budgeting for making NPV of all cash flows from a specific project equal to

zero. In management accounting, managers of Morrisons use concept of NPV for

estimating the future cash flows, which store may generate. While IRR is used to

estimate rate of growth which may generate after executing a project.

Financial reports (D2)

Financial reports that are required to be produced in case of inventory valuation and

standard costing are discussed as follows;

Variance report

It is the report which helps in compared planned or estimated outcomes against the

actual outcomes. The results are compared so that variances can be found out. The

variances are differences or deviations in the expected results (Weygandt et al.

2015:96-101). The reports prepared to show variances help the managers know in

which respect or department costs control is required to be applied. It shows all material

items and their expected as well as actual costs for a quarter. It will be helpful for

Morrison to identify the factors that are affecting on the cost controlling system.

Additionally, the managers can access idea about the company expenses and division

according to the department.

Inventory valuation reports

Inventory valuation reports as asserted by Malmi (2016:31-44), shoes or depicts the

quantity of raw material of stock used or sold for a given accounting period. Iis is

essential for the determination of cost of goods sold by the entity and is also used as

collateral by any organization. Since it deals with the most important current asset of an

organization hence the preparation of it report becomes essential and should be

manage it properly. Morrison can use reports for its current planning in the future

purposes.

Budgetary reports

Budgetary reports show the budget of all departments present in an organization. It

assists in analysing trends of revenues and projection of expenses. Preparation of

budget reports enables the management to know about the expenses which have gone

out of control and which are under the control of an organisation. With the help of

budgetary reports, Morrison can make its strategy for future expenses. The firm can be

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

focused on the money goals in order to avoid unnecessary spending. It will be

beneficial to attain the financial goals of the company.

LO3 use of planning tools in management accounting

Advantages and disadvantages of planning tools that are used for

budgetary control (P4)

Budgeting is the process of determining forecasted expenses, revenues and profits. it is

of different types for example there are sales budget, expenditure budget cash budget

and master budget. The steps in the budgeting process are discussed as follows;

Using different departmental budgets and reconciling them. Based on the departmental

budgets an overall organisational budget is prepared. Allocation of costs and expenses

are done after analysis of the liquidity position of the company. Concerning to that of

planning tools used for budgetary controls, there are present majorly three of their types

namely zero budget cash budget and product budget; Zero budgets, product budgets

and cash budget work as budgetary planning tools because these budgets help in

outlining the expected level of expenses in particular financial period. Zero budgets

helps in calculating expense from the base level and this helps in removing the gaps in

determination of overall expenditures (Cooper et al. 2017:991). On the other hand, cash

budgets help in outlining the liquidity level of the organisations. Product budgets

determine the amount or units of good that would be produced or sold by the company.

Forecasting Planning Tool- Forecasting also works like that of trend analysis and

helps the management in preparing the budgets according to the forecasted level of

expenses. It is the most scientific method of predicting trends and forecasting the

amount of expenses that a company would require to be incurred. It takes into account

the historical data and applies the current changes that are inherent in the market.

Forecasted amount is then used to prepare budgets. This planning tool is considered as

mapping tool which helps in predicting uncertainty future demand of business. In context with

Morrisons, its managers use forecasting tool to make plans for managing future risks. For this

process, they develop effective strategies in order to recover from those situations which might

affect business in future.

Advantage Disadvantages

Morrisons can apply this forecasting tool for

anticipating the potential risks which may

happen within business in future.

As Morrison deal in retail sector where

competition is more. Therefore, to make future

plans is rarely possible due to qualitative

nature of forecasting.

Contingency Planning Tools- This tool is used to deal with those situations which

might affect business in large manner. It includes terrorism, natural calamities and hardware

failures etc. Thus, using this planning tool, Morrisons can increase ability of business.

10

beneficial to attain the financial goals of the company.

LO3 use of planning tools in management accounting

Advantages and disadvantages of planning tools that are used for

budgetary control (P4)

Budgeting is the process of determining forecasted expenses, revenues and profits. it is

of different types for example there are sales budget, expenditure budget cash budget

and master budget. The steps in the budgeting process are discussed as follows;

Using different departmental budgets and reconciling them. Based on the departmental

budgets an overall organisational budget is prepared. Allocation of costs and expenses

are done after analysis of the liquidity position of the company. Concerning to that of

planning tools used for budgetary controls, there are present majorly three of their types

namely zero budget cash budget and product budget; Zero budgets, product budgets

and cash budget work as budgetary planning tools because these budgets help in

outlining the expected level of expenses in particular financial period. Zero budgets

helps in calculating expense from the base level and this helps in removing the gaps in

determination of overall expenditures (Cooper et al. 2017:991). On the other hand, cash

budgets help in outlining the liquidity level of the organisations. Product budgets

determine the amount or units of good that would be produced or sold by the company.

Forecasting Planning Tool- Forecasting also works like that of trend analysis and

helps the management in preparing the budgets according to the forecasted level of

expenses. It is the most scientific method of predicting trends and forecasting the

amount of expenses that a company would require to be incurred. It takes into account

the historical data and applies the current changes that are inherent in the market.

Forecasted amount is then used to prepare budgets. This planning tool is considered as

mapping tool which helps in predicting uncertainty future demand of business. In context with

Morrisons, its managers use forecasting tool to make plans for managing future risks. For this

process, they develop effective strategies in order to recover from those situations which might

affect business in future.

Advantage Disadvantages

Morrisons can apply this forecasting tool for

anticipating the potential risks which may

happen within business in future.

As Morrison deal in retail sector where

competition is more. Therefore, to make future

plans is rarely possible due to qualitative

nature of forecasting.

Contingency Planning Tools- This tool is used to deal with those situations which

might affect business in large manner. It includes terrorism, natural calamities and hardware

failures etc. Thus, using this planning tool, Morrisons can increase ability of business.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Advantage Disadvantages

Having a contingency tool helps Morrisons in

maintaining the best state of business. It also

empowered staff by informing them how to

react in such conditions and protect as well.

This tool is reactive in nature not proactive

therefore, managers of Morrisons are

responsible for managing the situations in

such a manner that they have to avoid

undesirable aspects of the same.

Budgetary control tools:

Morrison requires developing budgetary control tools including setting of objectives,

assign proper responsibility, planning different activities. Based on these factors, the

company requires planning the activities and bringing corrective actions in the system.

Morrison can track the costs with developing large number of products. It can meet the

inventory requirements within the time.

Analysis of planning tools usage and application (M3)

The planning tools that are used by Morrisons to forecast and plan budgets are

discussed as follows;

Trend analysis, cash flow analysis and forecasting are considered to be an effective

planning tool. This is because these tools help in analysing, the forecasted expenses

which in turn help in reducing the risk of incurring future losses.

Trend analysis

This planning tools help in predicting the pattern of cost structure and expenses that

may be incurred in future. Thus it is considered an effective planning tool. It works as a

budgetary planning tool by providing the management with an expected level of

incomes, costs and expenses. This is used in preparing budgets. It analyses the past

expenses made and revenues earned by the company. Based on the past 10 or 5 years

analysis of pattern future expenses or revenues receipt is predicted. This helps in

making the company more proactive and prevents future losses (Jack, 2016:89). It

helps to plan actions and budgets are also prepared accordingly. The estimation of

expenses takes into account uncertainties and thus cost appears to be more enhanced.

Advantages Disadvantages

Trend analysis help Morrison in making a

proper comparison with other retailers to

evaluate own strengths and weaknesses. It

also aid in understanding the short-term and

long-term liquidity position of business at

marketplace.

It is difficult for managers of Morrison to follow

a consistent principle and policy of

management accounting in case of changing

period of trend analysis.

Cash flow analysis

11

Having a contingency tool helps Morrisons in

maintaining the best state of business. It also

empowered staff by informing them how to

react in such conditions and protect as well.

This tool is reactive in nature not proactive

therefore, managers of Morrisons are

responsible for managing the situations in

such a manner that they have to avoid

undesirable aspects of the same.

Budgetary control tools:

Morrison requires developing budgetary control tools including setting of objectives,

assign proper responsibility, planning different activities. Based on these factors, the

company requires planning the activities and bringing corrective actions in the system.

Morrison can track the costs with developing large number of products. It can meet the

inventory requirements within the time.

Analysis of planning tools usage and application (M3)

The planning tools that are used by Morrisons to forecast and plan budgets are

discussed as follows;

Trend analysis, cash flow analysis and forecasting are considered to be an effective

planning tool. This is because these tools help in analysing, the forecasted expenses

which in turn help in reducing the risk of incurring future losses.

Trend analysis

This planning tools help in predicting the pattern of cost structure and expenses that

may be incurred in future. Thus it is considered an effective planning tool. It works as a

budgetary planning tool by providing the management with an expected level of

incomes, costs and expenses. This is used in preparing budgets. It analyses the past

expenses made and revenues earned by the company. Based on the past 10 or 5 years

analysis of pattern future expenses or revenues receipt is predicted. This helps in

making the company more proactive and prevents future losses (Jack, 2016:89). It

helps to plan actions and budgets are also prepared accordingly. The estimation of

expenses takes into account uncertainties and thus cost appears to be more enhanced.

Advantages Disadvantages

Trend analysis help Morrison in making a

proper comparison with other retailers to

evaluate own strengths and weaknesses. It

also aid in understanding the short-term and

long-term liquidity position of business at

marketplace.

It is difficult for managers of Morrison to follow

a consistent principle and policy of

management accounting in case of changing

period of trend analysis.

Cash flow analysis

11

Cash flow analysis works as a budgetary planning tool since it provides the

management with the information related to required amount of funds. Budgets are then

prepared according to the level of cash available with the firm. Cash flow analysis help

in understanding and evaluating the liquidity position of the company. The first step in

the preparation of budgets is determining the amount of cash or funds available. The

amount of available cash is then evaluated to analyse whether funds is able to cover

expenses.

Advantages Disadvantages

This concept aid managers of Morrison to

make a cash forecast for future within

business i.e. a detailed information about how

much cash is required for particular project. It

also reveals the cash position also.

As cash flow analysis shows only cash-

position then it is not possible for arriving at

actual loss and profitability within business.

In case of Morrisons, there is a variance between actual and estimation of

production cost i.e. near about £80,000. This variance has rise due to expectation of

high standard of production cost in certain budgetary process. While, in after financial

period, it has acquired less cost as compared.

LO4 Using management accounting to respond financial problems

Comparison of the ways in which organization adapt to management

accounting system (P5)

Adapting to management accounting system has been compared against the types of

management accounting system Asda stores uses which is also a supermarket giant in

UK.

Morrisons Asda Stores

Benchmarking Morrisons compares its

actual expenses based on

industry standards. The

benchmarking technique it

has used is more relevant

and useful (morrisons.com,

2018). Since comparison

made as per industry

standards make the

company more competitive

(springer.com, 2018).

Asda stores evaluates cost

of all it activities based on

the costs it has estimated.

Comparing internal

activities make the overall

functioning of the

organization smooth

(asda.com, 2018).

However as per the view of

Kihn & Ihantola (2015:230-

255), since activities are of

different nature hence

comparisons are

12

management with the information related to required amount of funds. Budgets are then

prepared according to the level of cash available with the firm. Cash flow analysis help

in understanding and evaluating the liquidity position of the company. The first step in

the preparation of budgets is determining the amount of cash or funds available. The

amount of available cash is then evaluated to analyse whether funds is able to cover

expenses.

Advantages Disadvantages

This concept aid managers of Morrison to

make a cash forecast for future within

business i.e. a detailed information about how

much cash is required for particular project. It

also reveals the cash position also.

As cash flow analysis shows only cash-

position then it is not possible for arriving at

actual loss and profitability within business.

In case of Morrisons, there is a variance between actual and estimation of

production cost i.e. near about £80,000. This variance has rise due to expectation of

high standard of production cost in certain budgetary process. While, in after financial

period, it has acquired less cost as compared.

LO4 Using management accounting to respond financial problems

Comparison of the ways in which organization adapt to management

accounting system (P5)

Adapting to management accounting system has been compared against the types of

management accounting system Asda stores uses which is also a supermarket giant in

UK.

Morrisons Asda Stores

Benchmarking Morrisons compares its

actual expenses based on

industry standards. The

benchmarking technique it

has used is more relevant

and useful (morrisons.com,

2018). Since comparison

made as per industry

standards make the

company more competitive

(springer.com, 2018).

Asda stores evaluates cost

of all it activities based on

the costs it has estimated.

Comparing internal

activities make the overall

functioning of the

organization smooth

(asda.com, 2018).

However as per the view of

Kihn & Ihantola (2015:230-

255), since activities are of

different nature hence

comparisons are

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.