Management Accounting: Costing, Budgeting, and Reporting Analysis

VerifiedAdded on 2020/07/23

|19

|4946

|24

Report

AI Summary

This report offers a detailed analysis of management accounting practices within Mwambi Ltd, a manufacturer of aerospace parts. The report begins by distinguishing between financial and management accounting, exploring various management accounting systems such as cost accounting, inventory management, job costing, and price optimization, along with their benefits. It then delves into costing techniques, including absorption and marginal costing, standard costing, and variance analysis. The report includes the preparation of income statements, calculation of unit costs, and variance analysis. Finally, the report critically analyzes budgetary planning tools, including the budgeting process, different budget types, and their advantages and disadvantages, along with recommendations for improvement. The report integrates various management accounting systems to generate crucial reports for effective decision-making, such as budgeting, job cost, and inventory reports.

Management accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION................................................................................................................................1

TASK 1.................................................................................................................................................1

LO1.......................................................................................................................................................1

P1 & P2 Management accounting, different kind of systems..........................................................1

Executive summary.................................................................................................................1

1.0 Management accounting...................................................................................................1

1.1 Distinguish between financial and management accounting............................................2

1.2 Management accounting systems......................................................................................2

1.3 Evaluate the benefits of management accounting systems...............................................3

1.4 Application and integration of management accounting systems in the organization......4

TASK 2.................................................................................................................................................5

LO2.......................................................................................................................................................5

P3 Calculation of costs using appropriate costing techniques..........................................................5

2.0 Executive summary...........................................................................................................5

2.1 Standard costing and variance analysis.............................................................................5

2.2 Application of management accounting techniques..........................................................5

2.3 Analysis and interpretation of financial reports................................................................7

2.4 Conclusion.........................................................................................................................8

2.5 Recommendations.............................................................................................................8

TASK 3.................................................................................................................................................9

LO3 & LO4..........................................................................................................................................9

P4 & P5 Critical analysis of budgetary planning tools.....................................................................9

Executive summary.................................................................................................................9

3.0 Planning tools: Budgetary control.....................................................................................9

3.1 Purpose of budgeting.........................................................................................................9

3.2 Budgeting process.............................................................................................................9

3.3 Different types of budget.................................................................................................10

3.4 Explaining the advantage and disadvantage of different planning tools for budgetary

control....................................................................................................................................12

4.1 & 4.2 Analyse the use of different planning tools in management accounting...............13

5.1 Conclusion.......................................................................................................................14

5.2 Recommendations...........................................................................................................14

INTRODUCTION................................................................................................................................1

TASK 1.................................................................................................................................................1

LO1.......................................................................................................................................................1

P1 & P2 Management accounting, different kind of systems..........................................................1

Executive summary.................................................................................................................1

1.0 Management accounting...................................................................................................1

1.1 Distinguish between financial and management accounting............................................2

1.2 Management accounting systems......................................................................................2

1.3 Evaluate the benefits of management accounting systems...............................................3

1.4 Application and integration of management accounting systems in the organization......4

TASK 2.................................................................................................................................................5

LO2.......................................................................................................................................................5

P3 Calculation of costs using appropriate costing techniques..........................................................5

2.0 Executive summary...........................................................................................................5

2.1 Standard costing and variance analysis.............................................................................5

2.2 Application of management accounting techniques..........................................................5

2.3 Analysis and interpretation of financial reports................................................................7

2.4 Conclusion.........................................................................................................................8

2.5 Recommendations.............................................................................................................8

TASK 3.................................................................................................................................................9

LO3 & LO4..........................................................................................................................................9

P4 & P5 Critical analysis of budgetary planning tools.....................................................................9

Executive summary.................................................................................................................9

3.0 Planning tools: Budgetary control.....................................................................................9

3.1 Purpose of budgeting.........................................................................................................9

3.2 Budgeting process.............................................................................................................9

3.3 Different types of budget.................................................................................................10

3.4 Explaining the advantage and disadvantage of different planning tools for budgetary

control....................................................................................................................................12

4.1 & 4.2 Analyse the use of different planning tools in management accounting...............13

5.1 Conclusion.......................................................................................................................14

5.2 Recommendations...........................................................................................................14

CONCLUSION..................................................................................................................................14

REFERENCES...................................................................................................................................16

REFERENCES...................................................................................................................................16

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Looking at the digitalized era, there is a significant shift in traditional managerial accounting

practices as paperwork is now replaced by computerized systems which maintain huge sort of data

and provide customized details as per the managerial requirement. Mwambi Ltd established in 2015

that specialises in manufacturing of aerospace parts for Airbus Ltd and it is operating at Romford,

Essex. The current research will investigate the use of important system and reporting which are

required by the managers for policymaking and strategic decisions. In despite of this, tools for

costing calculation and budgetary planning will be analyzed.

TASK 1

LO1

P1 & P2 Management accounting, different kind of systems

To: Line manager, Mwambi Ltd

From: Management Accountant

Date: 19th November 2017

Subject: Critical evaluation of management accounting system and management accounting

reporting within the business

Executive summary

The report is presenting here to clearly distinguish financial and management accounting.

Moreover, important details about various new managerial accounting systems along with their key

benefits will be provided. Moreover, it presents key reports that are extremely used by managers in

extracting and assessing performance of an undertaking and to make sound decisions.

1.0 Management accounting

Meaning: Management accounting, as its name, is about managing all the business aspect for

ensuring a successful and long-run survival. Institute of Chartered Accountants of England & Wales

defined it as an accounting form that enable firm to carry out their day-to-day business in an

efficient manner. Institute of Cost and Management Accountants, London stated that it is about

applying professional knowledge in the area of preparing accounting information to assist Mwambi

Ltd’s managers for formation of internal planning, policies and control operations.

Purpose: To make sound strategic plans and decisions for the business growth

1 | P a g e

Looking at the digitalized era, there is a significant shift in traditional managerial accounting

practices as paperwork is now replaced by computerized systems which maintain huge sort of data

and provide customized details as per the managerial requirement. Mwambi Ltd established in 2015

that specialises in manufacturing of aerospace parts for Airbus Ltd and it is operating at Romford,

Essex. The current research will investigate the use of important system and reporting which are

required by the managers for policymaking and strategic decisions. In despite of this, tools for

costing calculation and budgetary planning will be analyzed.

TASK 1

LO1

P1 & P2 Management accounting, different kind of systems

To: Line manager, Mwambi Ltd

From: Management Accountant

Date: 19th November 2017

Subject: Critical evaluation of management accounting system and management accounting

reporting within the business

Executive summary

The report is presenting here to clearly distinguish financial and management accounting.

Moreover, important details about various new managerial accounting systems along with their key

benefits will be provided. Moreover, it presents key reports that are extremely used by managers in

extracting and assessing performance of an undertaking and to make sound decisions.

1.0 Management accounting

Meaning: Management accounting, as its name, is about managing all the business aspect for

ensuring a successful and long-run survival. Institute of Chartered Accountants of England & Wales

defined it as an accounting form that enable firm to carry out their day-to-day business in an

efficient manner. Institute of Cost and Management Accountants, London stated that it is about

applying professional knowledge in the area of preparing accounting information to assist Mwambi

Ltd’s managers for formation of internal planning, policies and control operations.

Purpose: To make sound strategic plans and decisions for the business growth

1 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Scope: It covers key areas such as financial accounting, cost accounting and their analysis

Roles and principles: It plays an important role in examinine entity’s performance and make plans

and decisions to overcome the risk. Its principles includes focus on internal business management,

control mechanism and performance evaluation. Standard costing, break-even analysis, job costing,

pricing decisions, budgeting and others are the top tools used in the area of managerial accounting.

1.1 Distinguish between financial and management accounting

Financial accounting is about preparation, interpretation and analysis of financial statements

only, in contrast, later has widen scope as it includes financial and cost accounting, analysis

of annual statements, interpretation, preparing managerial reports and all others that are

concerned with planning, managing and controlling of an undertaking’s key activities.

The key purpose of financial accounting is to communicate financial health of the enterprise

whereas later aims at sound decisions and formation of excellent policies.

FA communicate information to all the stakeholders i.e. employees, shareholders,

government, tax authorities (HMRC) and others as primary audience. Unlike it, only internal

stakeholders are involved in management accounting i.e. executives, CEO, CFO, board of

directors, departmental heads and workforce.

Accounts are prepared following UK GAAP, IFRS and IAS, however, there are no

mandatory rules for management accounting

1.2 Management accounting systems

Cost accounting system: It is specially developed for manufacturers in order to track

inventory flow during different stages of production.Being a manufacturing concern of aerospace

parts, Mwambi Ltd can use this system to record their production functions through following a

perpetual inventory system (Freedman, 2015). It track material from the beginning stage to the final

stage till final product is made by automatically adjusting the transactions through computerized

system and help Mwambi Ltd’s production manager to know available inventory balance at given

point time.

Inventory management system: It comprises application software that is useful to organize,

track and manage sales, purchase and other manufacturing processes of Mwambi Ltd. In earlier,

inventory was managed through paperwork, while now, barcode or RFID (Radio Frequency

Identification) are the popular ways to track shipments that are received and sent to other with the

use of software and help manager in rational internal decisions (Trujillo, 2015).

2 | P a g e

Roles and principles: It plays an important role in examinine entity’s performance and make plans

and decisions to overcome the risk. Its principles includes focus on internal business management,

control mechanism and performance evaluation. Standard costing, break-even analysis, job costing,

pricing decisions, budgeting and others are the top tools used in the area of managerial accounting.

1.1 Distinguish between financial and management accounting

Financial accounting is about preparation, interpretation and analysis of financial statements

only, in contrast, later has widen scope as it includes financial and cost accounting, analysis

of annual statements, interpretation, preparing managerial reports and all others that are

concerned with planning, managing and controlling of an undertaking’s key activities.

The key purpose of financial accounting is to communicate financial health of the enterprise

whereas later aims at sound decisions and formation of excellent policies.

FA communicate information to all the stakeholders i.e. employees, shareholders,

government, tax authorities (HMRC) and others as primary audience. Unlike it, only internal

stakeholders are involved in management accounting i.e. executives, CEO, CFO, board of

directors, departmental heads and workforce.

Accounts are prepared following UK GAAP, IFRS and IAS, however, there are no

mandatory rules for management accounting

1.2 Management accounting systems

Cost accounting system: It is specially developed for manufacturers in order to track

inventory flow during different stages of production.Being a manufacturing concern of aerospace

parts, Mwambi Ltd can use this system to record their production functions through following a

perpetual inventory system (Freedman, 2015). It track material from the beginning stage to the final

stage till final product is made by automatically adjusting the transactions through computerized

system and help Mwambi Ltd’s production manager to know available inventory balance at given

point time.

Inventory management system: It comprises application software that is useful to organize,

track and manage sales, purchase and other manufacturing processes of Mwambi Ltd. In earlier,

inventory was managed through paperwork, while now, barcode or RFID (Radio Frequency

Identification) are the popular ways to track shipments that are received and sent to other with the

use of software and help manager in rational internal decisions (Trujillo, 2015).

2 | P a g e

Job costing: It is a system for cost-accounting that is often used by small and medium sized

manufacturing firms who produce job work comprising some number of units in a particular batch

(Lukka, 2010).Mwambi Ltd manufacture aerospace as per the order of Airbus Ltd, therefore, this

system is useful for the enterprise to account their material, labor and allocation of overheads and

derive total cost at the end.

Price optimization: This software is used in corporate world with the aim to set maximum

prices for the goods that match consumers’ willingness to pay. In ultra-competitive period, firms

devote a massive time in pricing decisions to assure quick sales with decent profit at acceptable

prices (Chenhall and Moers, 2015).The software runs mathematical programming on the available

data to know consumers responsiveness and charge right price in dynamic market.

1.3 Evaluate the benefits of management accounting systems

Cost accounting systems

Check available inventory balance

Cost determination

Aggregated reports

Ordering on right time saves storage, security and cost of obsolescence

Inventory management systems:

Updated data set

Save time and cost

Reduce inefficiency

Reduce lead time

Warehouse organizing and management

Data security

Job costing

Determine total cost of a job

Computerized record keeping

Smart decisions i.e. cost control, productivity maximizing and others

Price optimization

Price fixing : Initial prices, promotional prices and discounted prices

High sales

Value preposition

Monitoring helps to improve pricing accuracy

3 | P a g e

manufacturing firms who produce job work comprising some number of units in a particular batch

(Lukka, 2010).Mwambi Ltd manufacture aerospace as per the order of Airbus Ltd, therefore, this

system is useful for the enterprise to account their material, labor and allocation of overheads and

derive total cost at the end.

Price optimization: This software is used in corporate world with the aim to set maximum

prices for the goods that match consumers’ willingness to pay. In ultra-competitive period, firms

devote a massive time in pricing decisions to assure quick sales with decent profit at acceptable

prices (Chenhall and Moers, 2015).The software runs mathematical programming on the available

data to know consumers responsiveness and charge right price in dynamic market.

1.3 Evaluate the benefits of management accounting systems

Cost accounting systems

Check available inventory balance

Cost determination

Aggregated reports

Ordering on right time saves storage, security and cost of obsolescence

Inventory management systems:

Updated data set

Save time and cost

Reduce inefficiency

Reduce lead time

Warehouse organizing and management

Data security

Job costing

Determine total cost of a job

Computerized record keeping

Smart decisions i.e. cost control, productivity maximizing and others

Price optimization

Price fixing : Initial prices, promotional prices and discounted prices

High sales

Value preposition

Monitoring helps to improve pricing accuracy

3 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1.4 Application and integration of management accounting systems in the organization

Above-mentioned management accounting system can be integrated by Mwambi Ltd to

generate different reports to analyze entity’s performance.

Budgeting reports: The most common report that Mwambi Ltd’s managers uses is budget

which is a formal quantitative plan about future. It helps managerial team in identifying possible

revenues and understands various cost elements which facilitate them in resource allocation and its

sound utilization to fulfil their goals (Zimmerman and Yahya-Zadeh, 2011). Besides this, it also

provides base to the managers to compare actual results and perform comparison against the results

of preceding period which helps in cost-control efforts.

Job cost reports: Job-costing system maintain details about material, labor and other

overheads in the production functions and generate cost reports for every job automatically. By this,

MwambiLtd’s managers can examine cost of each spare part and also analyze change in the all the

cost elements as a result of inflation, poor negotiation practices and others (Horngren and

et.al.,2010). Its thorough evaluation assists firm in taking good decisions for controlling

overrunning cost of raw material, staff wages and other overheads as a result of poor monitoring.

Inventory reports: Inventory management system generates such kind of reports and present

summarized details about goods received and shipped, order placed, obsolescence, frequency of

material usage in the production along with the time and available balance (Ward, 2012). By this,

production manager of Mwambi Ltd can create smart policies such as follow just-in-time technique

to control storing, caring and obsolescence cost by placing order, when material is required to

continue the manufacturing activities.

Accounts receivable report: In the business relationship, many-times, Mwambi Ltd offer

credit to the Airbus for different duration decided after mutual discussion. It is important for the

credit collecting authority to regularly check, track and monitor their debtors and take decisions to

receive unpaid money from them (Bennett, Schaltegger and Zvezdov, 2013). This report is

extremely useful to examine and to determine the debtors balance; outstanding trade receivables for

a long period must be legally enforced to make payments while other must be delivered with a

notice to get payments. It also helps in revising credit collection policies and terms consider

Mwambi Ltd’s cash and liquidity requirement.

4 | P a g e

Above-mentioned management accounting system can be integrated by Mwambi Ltd to

generate different reports to analyze entity’s performance.

Budgeting reports: The most common report that Mwambi Ltd’s managers uses is budget

which is a formal quantitative plan about future. It helps managerial team in identifying possible

revenues and understands various cost elements which facilitate them in resource allocation and its

sound utilization to fulfil their goals (Zimmerman and Yahya-Zadeh, 2011). Besides this, it also

provides base to the managers to compare actual results and perform comparison against the results

of preceding period which helps in cost-control efforts.

Job cost reports: Job-costing system maintain details about material, labor and other

overheads in the production functions and generate cost reports for every job automatically. By this,

MwambiLtd’s managers can examine cost of each spare part and also analyze change in the all the

cost elements as a result of inflation, poor negotiation practices and others (Horngren and

et.al.,2010). Its thorough evaluation assists firm in taking good decisions for controlling

overrunning cost of raw material, staff wages and other overheads as a result of poor monitoring.

Inventory reports: Inventory management system generates such kind of reports and present

summarized details about goods received and shipped, order placed, obsolescence, frequency of

material usage in the production along with the time and available balance (Ward, 2012). By this,

production manager of Mwambi Ltd can create smart policies such as follow just-in-time technique

to control storing, caring and obsolescence cost by placing order, when material is required to

continue the manufacturing activities.

Accounts receivable report: In the business relationship, many-times, Mwambi Ltd offer

credit to the Airbus for different duration decided after mutual discussion. It is important for the

credit collecting authority to regularly check, track and monitor their debtors and take decisions to

receive unpaid money from them (Bennett, Schaltegger and Zvezdov, 2013). This report is

extremely useful to examine and to determine the debtors balance; outstanding trade receivables for

a long period must be legally enforced to make payments while other must be delivered with a

notice to get payments. It also helps in revising credit collection policies and terms consider

Mwambi Ltd’s cash and liquidity requirement.

4 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 2

LO2

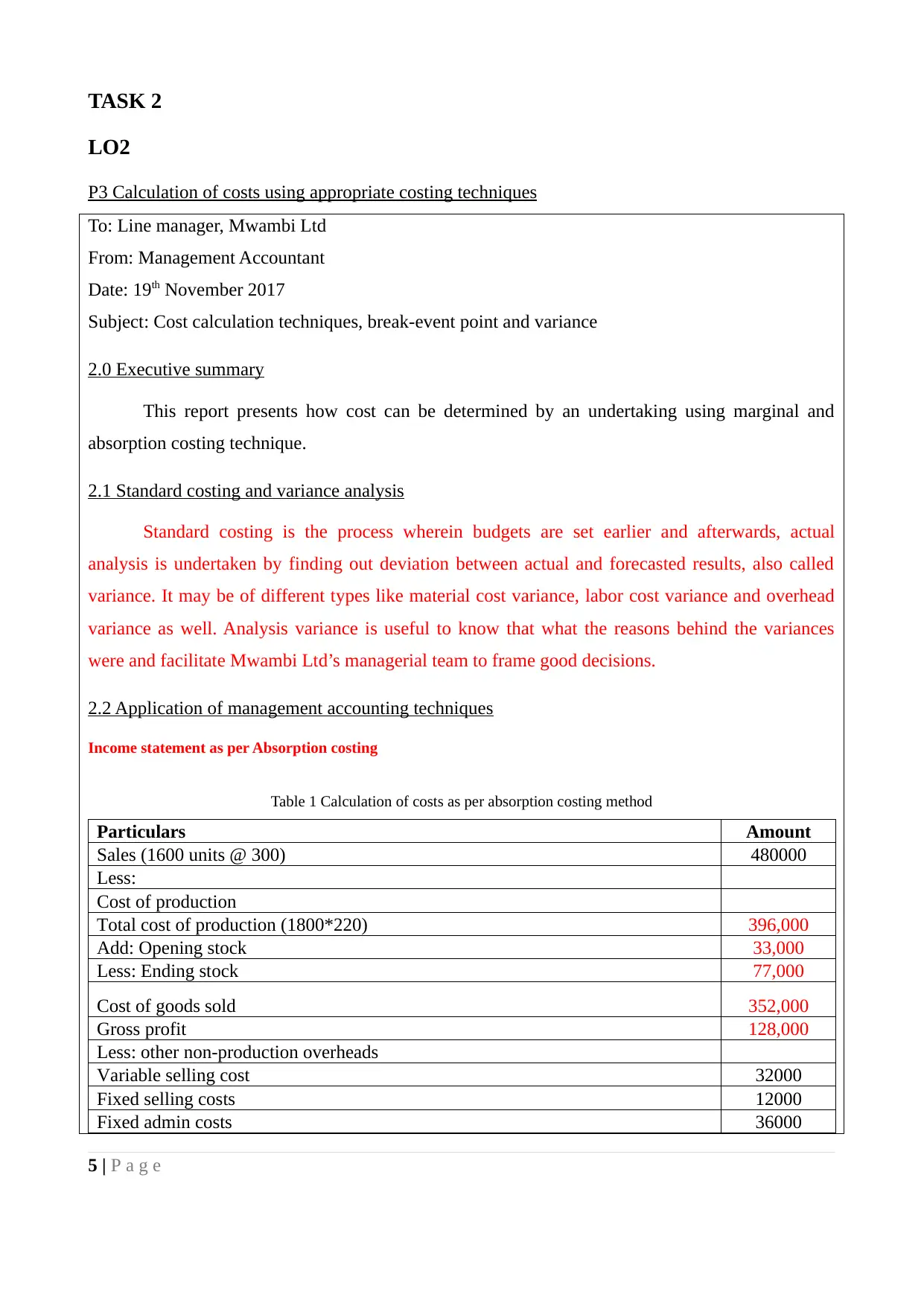

P3 Calculation of costs using appropriate costing techniques

To: Line manager, Mwambi Ltd

From: Management Accountant

Date: 19th November 2017

Subject: Cost calculation techniques, break-event point and variance

2.0 Executive summary

This report presents how cost can be determined by an undertaking using marginal and

absorption costing technique.

2.1 Standard costing and variance analysis

Standard costing is the process wherein budgets are set earlier and afterwards, actual

analysis is undertaken by finding out deviation between actual and forecasted results, also called

variance. It may be of different types like material cost variance, labor cost variance and overhead

variance as well. Analysis variance is useful to know that what the reasons behind the variances

were and facilitate Mwambi Ltd’s managerial team to frame good decisions.

2.2 Application of management accounting techniques

Income statement as per Absorption costing

Table 1 Calculation of costs as per absorption costing method

Particulars Amount

Sales (1600 units @ 300) 480000

Less:

Cost of production

Total cost of production (1800*220) 396,000

Add: Opening stock 33,000

Less: Ending stock 77,000

Cost of goods sold 352,000

Gross profit 128,000

Less: other non-production overheads

Variable selling cost 32000

Fixed selling costs 12000

Fixed admin costs 36000

5 | P a g e

LO2

P3 Calculation of costs using appropriate costing techniques

To: Line manager, Mwambi Ltd

From: Management Accountant

Date: 19th November 2017

Subject: Cost calculation techniques, break-event point and variance

2.0 Executive summary

This report presents how cost can be determined by an undertaking using marginal and

absorption costing technique.

2.1 Standard costing and variance analysis

Standard costing is the process wherein budgets are set earlier and afterwards, actual

analysis is undertaken by finding out deviation between actual and forecasted results, also called

variance. It may be of different types like material cost variance, labor cost variance and overhead

variance as well. Analysis variance is useful to know that what the reasons behind the variances

were and facilitate Mwambi Ltd’s managerial team to frame good decisions.

2.2 Application of management accounting techniques

Income statement as per Absorption costing

Table 1 Calculation of costs as per absorption costing method

Particulars Amount

Sales (1600 units @ 300) 480000

Less:

Cost of production

Total cost of production (1800*220) 396,000

Add: Opening stock 33,000

Less: Ending stock 77,000

Cost of goods sold 352,000

Gross profit 128,000

Less: other non-production overheads

Variable selling cost 32000

Fixed selling costs 12000

Fixed admin costs 36000

5 | P a g e

Total 80000

Net profit (Gross profit - total non-production expenses) 48,000

Income statement as per marginal costing

Table 2 Calculation of costs as marginal costing method

Particulars Amount

Sales (1600 units @ 300) 480000

Less:

Cost of production

Total cost of production (1800*200) 360,000

Add: Opening stock 30,000

Less: Ending stock 70,000

Cost of goods sold 320,000

Add: Other variable selling cost 32000

Total variable costs 352,000

Contribution (Sales - TVC) 128000

Less: other fixed costs

Fixed selling costs 12000

Fixed admin costs 36000

Fixed production overhead 36000

Total fixed costs 84,000

Net profit (Contribution - total fixed costs) 44,000

Reconciliation statement

Particulars Amount

Profit as per Marginal costing 44000

Add: Fixed production overhead on closing inventory (350*20) 7000

Less: Fixed production overhead on opening inventory (150*20) 3000

Calculation of unit costs

Table 3 Calculation of full costs per unit

Cost each unit

Cost of material 80

Cost of labor 90

Cost of variable production overheads 30

Cost of fixed production overheads (40,000/2000) units 20

Total costs per unit 220

Table 4 Calculation of variable cost per unit

Cost each unit

Cost of material 80

Cost of labor 90

Cost of variable production overheads 30

6 | P a g e

Net profit (Gross profit - total non-production expenses) 48,000

Income statement as per marginal costing

Table 2 Calculation of costs as marginal costing method

Particulars Amount

Sales (1600 units @ 300) 480000

Less:

Cost of production

Total cost of production (1800*200) 360,000

Add: Opening stock 30,000

Less: Ending stock 70,000

Cost of goods sold 320,000

Add: Other variable selling cost 32000

Total variable costs 352,000

Contribution (Sales - TVC) 128000

Less: other fixed costs

Fixed selling costs 12000

Fixed admin costs 36000

Fixed production overhead 36000

Total fixed costs 84,000

Net profit (Contribution - total fixed costs) 44,000

Reconciliation statement

Particulars Amount

Profit as per Marginal costing 44000

Add: Fixed production overhead on closing inventory (350*20) 7000

Less: Fixed production overhead on opening inventory (150*20) 3000

Calculation of unit costs

Table 3 Calculation of full costs per unit

Cost each unit

Cost of material 80

Cost of labor 90

Cost of variable production overheads 30

Cost of fixed production overheads (40,000/2000) units 20

Total costs per unit 220

Table 4 Calculation of variable cost per unit

Cost each unit

Cost of material 80

Cost of labor 90

Cost of variable production overheads 30

6 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

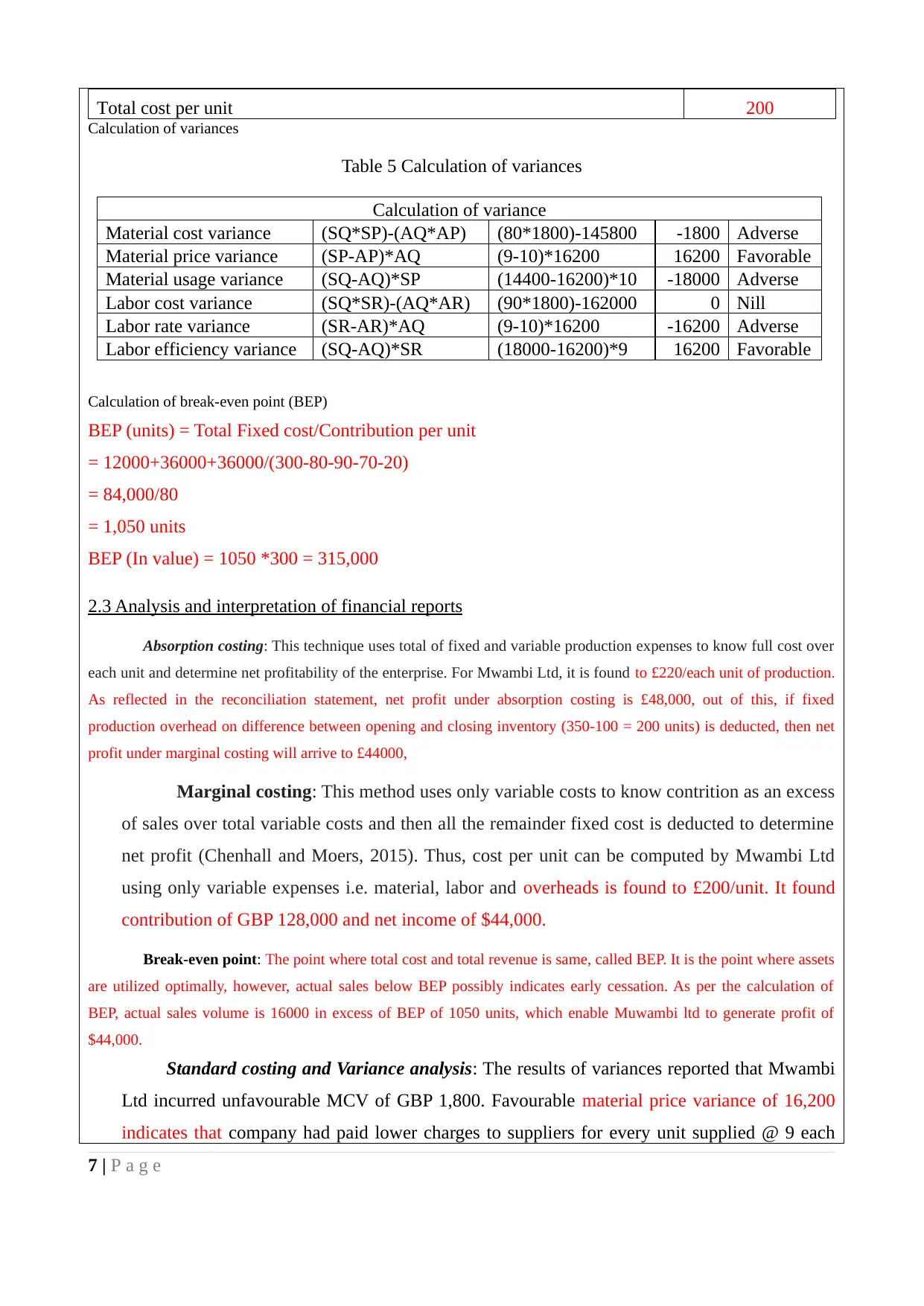

Total cost per unit 200

Calculation of variances

Table 5 Calculation of variances

Calculation of variance

Material cost variance (SQ*SP)-(AQ*AP) (80*1800)-145800 -1800 Adverse

Material price variance (SP-AP)*AQ (9-10)*16200 16200 Favorable

Material usage variance (SQ-AQ)*SP (14400-16200)*10 -18000 Adverse

Labor cost variance (SQ*SR)-(AQ*AR) (90*1800)-162000 0 Nill

Labor rate variance (SR-AR)*AQ (9-10)*16200 -16200 Adverse

Labor efficiency variance (SQ-AQ)*SR (18000-16200)*9 16200 Favorable

Calculation of break-even point (BEP)

BEP (units) = Total Fixed cost/Contribution per unit

= 12000+36000+36000/(300-80-90-70-20)

= 84,000/80

= 1,050 units

BEP (In value) = 1050 *300 = 315,000

2.3 Analysis and interpretation of financial reports

Absorption costing: This technique uses total of fixed and variable production expenses to know full cost over

each unit and determine net profitability of the enterprise. For Mwambi Ltd, it is found to £220/each unit of production.

As reflected in the reconciliation statement, net profit under absorption costing is £48,000, out of this, if fixed

production overhead on difference between opening and closing inventory (350-100 = 200 units) is deducted, then net

profit under marginal costing will arrive to £44000,

Marginal costing: This method uses only variable costs to know contrition as an excess

of sales over total variable costs and then all the remainder fixed cost is deducted to determine

net profit (Chenhall and Moers, 2015). Thus, cost per unit can be computed by Mwambi Ltd

using only variable expenses i.e. material, labor and overheads is found to £200/unit. It found

contribution of GBP 128,000 and net income of $44,000.

Break-even point: The point where total cost and total revenue is same, called BEP. It is the point where assets

are utilized optimally, however, actual sales below BEP possibly indicates early cessation. As per the calculation of

BEP, actual sales volume is 16000 in excess of BEP of 1050 units, which enable Muwambi ltd to generate profit of

$44,000.

Standard costing and Variance analysis: The results of variances reported that Mwambi

Ltd incurred unfavourable MCV of GBP 1,800. Favourable material price variance of 16,200

indicates that company had paid lower charges to suppliers for every unit supplied @ 9 each

7 | P a g e

Calculation of variances

Table 5 Calculation of variances

Calculation of variance

Material cost variance (SQ*SP)-(AQ*AP) (80*1800)-145800 -1800 Adverse

Material price variance (SP-AP)*AQ (9-10)*16200 16200 Favorable

Material usage variance (SQ-AQ)*SP (14400-16200)*10 -18000 Adverse

Labor cost variance (SQ*SR)-(AQ*AR) (90*1800)-162000 0 Nill

Labor rate variance (SR-AR)*AQ (9-10)*16200 -16200 Adverse

Labor efficiency variance (SQ-AQ)*SR (18000-16200)*9 16200 Favorable

Calculation of break-even point (BEP)

BEP (units) = Total Fixed cost/Contribution per unit

= 12000+36000+36000/(300-80-90-70-20)

= 84,000/80

= 1,050 units

BEP (In value) = 1050 *300 = 315,000

2.3 Analysis and interpretation of financial reports

Absorption costing: This technique uses total of fixed and variable production expenses to know full cost over

each unit and determine net profitability of the enterprise. For Mwambi Ltd, it is found to £220/each unit of production.

As reflected in the reconciliation statement, net profit under absorption costing is £48,000, out of this, if fixed

production overhead on difference between opening and closing inventory (350-100 = 200 units) is deducted, then net

profit under marginal costing will arrive to £44000,

Marginal costing: This method uses only variable costs to know contrition as an excess

of sales over total variable costs and then all the remainder fixed cost is deducted to determine

net profit (Chenhall and Moers, 2015). Thus, cost per unit can be computed by Mwambi Ltd

using only variable expenses i.e. material, labor and overheads is found to £200/unit. It found

contribution of GBP 128,000 and net income of $44,000.

Break-even point: The point where total cost and total revenue is same, called BEP. It is the point where assets

are utilized optimally, however, actual sales below BEP possibly indicates early cessation. As per the calculation of

BEP, actual sales volume is 16000 in excess of BEP of 1050 units, which enable Muwambi ltd to generate profit of

$44,000.

Standard costing and Variance analysis: The results of variances reported that Mwambi

Ltd incurred unfavourable MCV of GBP 1,800. Favourable material price variance of 16,200

indicates that company had paid lower charges to suppliers for every unit supplied @ 9 each

7 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

against expected rate @ 10/unit may be due to excessive supply, less demand and substitute

products also. However, actual usage is comparatively high to 16200 Kg against decided usage

of 14,400 Kg. It indicates ineffective usage, wastage and obsolescence may be its reason,

caused adverse variance of GBP18,000 (Chenhall and Moers, 2015). Thus, production

department manager need to track its usage and reduce the risk of theft by proper security i.e.

guard, CCTV cameras and strict policies.

Unlike it, LCV is zero which perfectly meets targeted cost, although, workers are

paid at high rate @ 10/hour against set wages rate @ 9/hour, still, efficient labor completed

production just within 16,200 hours against expected period of 18,000 hours resulted

favourable variance of GBP 16,200. Thus, from the analysis, it can be suggested to Mwambi

Ltd to use this technique to compare and match their targets with actual performance to know

deviations and look over key concerns to ensure sustainable success.

2.4 Conclusion

As per the analusis, it is found that Mwambi Ltd had implemented good cost recording

system by classifying cost into both fixed and variable segments which facilitate company to make

their financial statements and cost reports in a proper manner. Variance analysis found some adverse

deviation with respect to labor efficiency and material actual usage in the business.

2.5 Recommendations

Variance analysis suggests that production manager must design suitable plans like training,

tracking workers activities; reduce exploitation of material by workers for their own benefits and

others. In addition, it is necessary to maintain proper documentation and keep up to date their data

set so as to generate reports regularly and utilize for the business planning.

TASK 3

LO3 & LO4

P4 & P5 Critical analysis of budgetary planning tools

To: Line manager, Mwambi Ltd

From: Management Accountant

Date: 19th November 2017

Subject: Critical evaluation of different kind of budgetary planning tools and its use to respond

8 | P a g e

products also. However, actual usage is comparatively high to 16200 Kg against decided usage

of 14,400 Kg. It indicates ineffective usage, wastage and obsolescence may be its reason,

caused adverse variance of GBP18,000 (Chenhall and Moers, 2015). Thus, production

department manager need to track its usage and reduce the risk of theft by proper security i.e.

guard, CCTV cameras and strict policies.

Unlike it, LCV is zero which perfectly meets targeted cost, although, workers are

paid at high rate @ 10/hour against set wages rate @ 9/hour, still, efficient labor completed

production just within 16,200 hours against expected period of 18,000 hours resulted

favourable variance of GBP 16,200. Thus, from the analysis, it can be suggested to Mwambi

Ltd to use this technique to compare and match their targets with actual performance to know

deviations and look over key concerns to ensure sustainable success.

2.4 Conclusion

As per the analusis, it is found that Mwambi Ltd had implemented good cost recording

system by classifying cost into both fixed and variable segments which facilitate company to make

their financial statements and cost reports in a proper manner. Variance analysis found some adverse

deviation with respect to labor efficiency and material actual usage in the business.

2.5 Recommendations

Variance analysis suggests that production manager must design suitable plans like training,

tracking workers activities; reduce exploitation of material by workers for their own benefits and

others. In addition, it is necessary to maintain proper documentation and keep up to date their data

set so as to generate reports regularly and utilize for the business planning.

TASK 3

LO3 & LO4

P4 & P5 Critical analysis of budgetary planning tools

To: Line manager, Mwambi Ltd

From: Management Accountant

Date: 19th November 2017

Subject: Critical evaluation of different kind of budgetary planning tools and its use to respond

8 | P a g e

financial problems

Executive summary

This report discusses details about importance of budgetary planning as a tool of decisions

making for Mwambi Ltd. Along with this, different kind of budgets will be examined critically with

their strength and benefits associated. Moreover, various tools that business can use to take

decisions and overcome financial problems will be highlighted and studied thoroughly.

3.0 Planning tools: Budgetary control

Budgeting is a fundamental tool that every company makes regardless their sizes. It is used

as an integral tool to forecast financial plan for a specified time, includes sales projection, resource

requirement, cost, cash flows and others (Macintosh and Quattrone, 2010). It is used to express

strategic plan in measurable or quantifiable terms.

3.1 Purpose of budgeting

To determine expenditures and income for a specified period of time

To know net availability of cash in the business enterprise

To monitor performance of an undertakings by matching actual financial outcome against

the set targets

3.2 Budgeting process

1. Setting business plans and goals

2. Projecting future revenues

3. Projection of fixed and variable cost

4. Presenting budget to the board for approval

5. Budget review

6. Finding out variances between actual and budgeted figures

7. Reporting to the boards

8. Corrective actions and its implementation

3.3 Different types of budget

Fixed budgets: As its name, budget prepared following this method can’t be flexed or

adjusted in line with the actual production level.

Benefits

9 | P a g e

Executive summary

This report discusses details about importance of budgetary planning as a tool of decisions

making for Mwambi Ltd. Along with this, different kind of budgets will be examined critically with

their strength and benefits associated. Moreover, various tools that business can use to take

decisions and overcome financial problems will be highlighted and studied thoroughly.

3.0 Planning tools: Budgetary control

Budgeting is a fundamental tool that every company makes regardless their sizes. It is used

as an integral tool to forecast financial plan for a specified time, includes sales projection, resource

requirement, cost, cash flows and others (Macintosh and Quattrone, 2010). It is used to express

strategic plan in measurable or quantifiable terms.

3.1 Purpose of budgeting

To determine expenditures and income for a specified period of time

To know net availability of cash in the business enterprise

To monitor performance of an undertakings by matching actual financial outcome against

the set targets

3.2 Budgeting process

1. Setting business plans and goals

2. Projecting future revenues

3. Projection of fixed and variable cost

4. Presenting budget to the board for approval

5. Budget review

6. Finding out variances between actual and budgeted figures

7. Reporting to the boards

8. Corrective actions and its implementation

3.3 Different types of budget

Fixed budgets: As its name, budget prepared following this method can’t be flexed or

adjusted in line with the actual production level.

Benefits

9 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.