Critical Evaluation of Management Accounting for NCC Group PLC

VerifiedAdded on 2020/07/23

|10

|2746

|37

Report

AI Summary

This report provides a comprehensive analysis of management accounting, focusing on its application within NCC Group PLC. It begins by defining management accounting and highlighting its importance in cost control and decision-making. The report then explores a range of management accounting techniques, including financial planning, financial statement analysis, historical cost accounting, standard costing, budgetary control, marginal costing, fund flow statements, and cash flow statements. Each technique is critically evaluated for its suitability to NCC Group, with a particular emphasis on the Activity-Based Costing (ABC) technique, discussing its advantages and disadvantages. The report further delves into the technical procedures used in management accounting, including a detailed example comparing traditional and ABC costing methods for two products, Abta and Bapta. Finally, the report concludes with an assessment of the executability of the ABC technique for NCC Ltd, comparing its results with traditional costing methods.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................1

1. Define the management accounting and analysation of importance.......................................1

2. Range of management accounting techniques acquirable for NCC group.............................2

3. Critically evaluate each technique for NCC group.................................................................3

4. Detailed knowledge of the technical procedures used in management accounting................3

5. Advise whether ABC technique is executable for NCC Ltd...................................................5

CONCLUSION................................................................................................................................5

REFERENCES................................................................................................................................6

INTRODUCTION...........................................................................................................................1

1. Define the management accounting and analysation of importance.......................................1

2. Range of management accounting techniques acquirable for NCC group.............................2

3. Critically evaluate each technique for NCC group.................................................................3

4. Detailed knowledge of the technical procedures used in management accounting................3

5. Advise whether ABC technique is executable for NCC Ltd...................................................5

CONCLUSION................................................................................................................................5

REFERENCES................................................................................................................................6

INTRODUCTION

Organisations are adapting management accounting system subject to managing and

operating the departments of the organisation (Fullerton, Kenned and Widener, 2013). This

report is prepared to define the role of management accounting subject to controlling the cost and

determine the cost of product. With the use of management accounting system information and

cost problems are illustrated in this report. NCC group plc is chosen organisation to elaborate the

importance of management accounting to respond cost problems and issues.

1. Define the management accounting and analysation of importance

Management accounting is being used as supporting tool in respect of decision making

and strategic planning (Albelda, 2011). This is considered as a system, aspect, process or tool.

With the help of management accounting mangers and accountants become eligible to make

strategies and plans for better formulation and completion of tasks. It is considered as a process

of preparing management reports, accounts and provide accurate information to the managers. It

also helps the managers to make long-term and short term decisions. There are some essential

importance found in business and organisation in order to interpret ate the data, bifurcation the

information in various parts and helping the staff and teams to attain organisational goals.

Importance of management accounting

it is very important for the organisation to consolidate all the information and reports in

summarised way (Dillard and Roslender, 2011). These information helps the managers and the

accountants to finalise the financial statements, preparing cost records, managing the fund flow

and cash flow statements. Appropriation and allocation of overheads at various cost centres and

departments. Importance of management accounting information can be bifurcated in various

forms such as:

Forecasting and analysing future events and incidents

Assist managers and accountants in order to make effective decision making strategies

Forecasting cash flows and projected report

Analysing the performance of organisation by analysing the variances

To evaluate the rate of return

2. Range of management accounting techniques acquirable for NCC group

Various type of financial accounting techniques are used in organisational context such

as:

1

Organisations are adapting management accounting system subject to managing and

operating the departments of the organisation (Fullerton, Kenned and Widener, 2013). This

report is prepared to define the role of management accounting subject to controlling the cost and

determine the cost of product. With the use of management accounting system information and

cost problems are illustrated in this report. NCC group plc is chosen organisation to elaborate the

importance of management accounting to respond cost problems and issues.

1. Define the management accounting and analysation of importance

Management accounting is being used as supporting tool in respect of decision making

and strategic planning (Albelda, 2011). This is considered as a system, aspect, process or tool.

With the help of management accounting mangers and accountants become eligible to make

strategies and plans for better formulation and completion of tasks. It is considered as a process

of preparing management reports, accounts and provide accurate information to the managers. It

also helps the managers to make long-term and short term decisions. There are some essential

importance found in business and organisation in order to interpret ate the data, bifurcation the

information in various parts and helping the staff and teams to attain organisational goals.

Importance of management accounting

it is very important for the organisation to consolidate all the information and reports in

summarised way (Dillard and Roslender, 2011). These information helps the managers and the

accountants to finalise the financial statements, preparing cost records, managing the fund flow

and cash flow statements. Appropriation and allocation of overheads at various cost centres and

departments. Importance of management accounting information can be bifurcated in various

forms such as:

Forecasting and analysing future events and incidents

Assist managers and accountants in order to make effective decision making strategies

Forecasting cash flows and projected report

Analysing the performance of organisation by analysing the variances

To evaluate the rate of return

2. Range of management accounting techniques acquirable for NCC group

Various type of financial accounting techniques are used in organisational context such

as:

1

Financial planing: this is the technique which helps to analyse the impact and activities

in respect of activities and attaining prime objectives (Management accounting

techniques, 2017). It helps to determine both the short term and long term financial

requirement with in the organisation. This technique basically used to emphasise the rate

of return and utilisation of equity and debts in effective manner.

Analysing financial statements: this is one of the technique which helps to determine

the conflicts and issues which create difference between assets and liabilities. It helps to

forecast the financial statement and data in order to determine the cost of capital and

profitability of organisation.

Historical cost accounting: this is the technique which is used by the accountants to

record the transactions and events at the cost when they were incurred (Contrafatto and

Burns, 2013). It provides the past data to manage the cost of each job and process of

departments. There is an comparison done between actual costa and standard cost in

order to control the cost and future planning.

Standard costing: this is one of the accounting technique which helps to estimate the

cost of product as per actual and projected information. There is an analysation of

variances and difference between actual and standard data and information. Positive

figures are considered as favourable and negative figures are considered as adverse

results.

Budgetary control: to control the cost of production and planing if the various activities

are considered in budgetary control process. It is considered as an important technique

which helps to direct the accountants and mangers to make decision and strategies. There

is a satisfactory return on capital investment are analysed in this subject.

Marginal costing: this technique used by the organisation to evaluate the cost of product

and analysing the profit in respect of evaluate the profit (Albelda, Caglio and Ditillo,

2012). All the variable expenses such as direct material, direct expenses and direct lobar,

variable overheads are considered in this technique.

Fund flow statement: this technique helps to analyse the fluctuation and variation in

financial position of a business enterprise (Fullerton, Kennedy and Widener, 2014).

Funds and capital structure is analysed in respect of define the capital structure and

2

in respect of activities and attaining prime objectives (Management accounting

techniques, 2017). It helps to determine both the short term and long term financial

requirement with in the organisation. This technique basically used to emphasise the rate

of return and utilisation of equity and debts in effective manner.

Analysing financial statements: this is one of the technique which helps to determine

the conflicts and issues which create difference between assets and liabilities. It helps to

forecast the financial statement and data in order to determine the cost of capital and

profitability of organisation.

Historical cost accounting: this is the technique which is used by the accountants to

record the transactions and events at the cost when they were incurred (Contrafatto and

Burns, 2013). It provides the past data to manage the cost of each job and process of

departments. There is an comparison done between actual costa and standard cost in

order to control the cost and future planning.

Standard costing: this is one of the accounting technique which helps to estimate the

cost of product as per actual and projected information. There is an analysation of

variances and difference between actual and standard data and information. Positive

figures are considered as favourable and negative figures are considered as adverse

results.

Budgetary control: to control the cost of production and planing if the various activities

are considered in budgetary control process. It is considered as an important technique

which helps to direct the accountants and mangers to make decision and strategies. There

is a satisfactory return on capital investment are analysed in this subject.

Marginal costing: this technique used by the organisation to evaluate the cost of product

and analysing the profit in respect of evaluate the profit (Albelda, Caglio and Ditillo,

2012). All the variable expenses such as direct material, direct expenses and direct lobar,

variable overheads are considered in this technique.

Fund flow statement: this technique helps to analyse the fluctuation and variation in

financial position of a business enterprise (Fullerton, Kennedy and Widener, 2014).

Funds and capital structure is analysed in respect of define the capital structure and

2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

analysing the financial position of the organisation. It helps to control the cost and

analysing the net inflow and out flow of funds.

Cash flow statement: this is one of the technique which is used to analyse the net cash in

flow and out flow with in the organisation. There is an analysation of cash inflow from

operating activity, financing activities and investing activities. All the cash items are

considered while making cash flow statements.

Decision making: this techniques is basically used at managerial level respond to

financial problems and forecasting the plans. Managers become eligible to make and

forecast the future plans in order to improve the capacity and profitability.

3. Critically evaluate each technique for NCC group

ABC technique: this is considered as Activity Based Costing technique. this is one of the

technique which helps to manager the inventories and cost of production in respect of controlling

the cost (Chenhall and Smith, 2011). It helps to bifurcate the cost of production as per the

priority. There is a significant impact found in respect of analysing the profitability and margin.

Advantages of ABC technique

NCC would get following benefits if it applies ABC costing technique with in the

organisation;

It is considered more frequent controlling on high priority inventory control system.

It helps managers to better control on high priory inventories based upon customer's

request.

It helps to bifurcate the class of products and material used to manufacturing goods and

products. With the help of this techniques NCC would be eligible to priorities control of high

priorities inventories subject to lower impact on bottom line.

Disadvantages of ABC technique

There are some drawback of this accounting technique also there which are as follows:

ABC stock valuation is not considered valid as per GAAP and it has also problems and

conflicts with traditional costing system.

It requires more resources in order to maintain traditional costing system.

It only remain focused upon high priority inventories due to which less priority

inventories remain aside.

3

analysing the net inflow and out flow of funds.

Cash flow statement: this is one of the technique which is used to analyse the net cash in

flow and out flow with in the organisation. There is an analysation of cash inflow from

operating activity, financing activities and investing activities. All the cash items are

considered while making cash flow statements.

Decision making: this techniques is basically used at managerial level respond to

financial problems and forecasting the plans. Managers become eligible to make and

forecast the future plans in order to improve the capacity and profitability.

3. Critically evaluate each technique for NCC group

ABC technique: this is considered as Activity Based Costing technique. this is one of the

technique which helps to manager the inventories and cost of production in respect of controlling

the cost (Chenhall and Smith, 2011). It helps to bifurcate the cost of production as per the

priority. There is a significant impact found in respect of analysing the profitability and margin.

Advantages of ABC technique

NCC would get following benefits if it applies ABC costing technique with in the

organisation;

It is considered more frequent controlling on high priority inventory control system.

It helps managers to better control on high priory inventories based upon customer's

request.

It helps to bifurcate the class of products and material used to manufacturing goods and

products. With the help of this techniques NCC would be eligible to priorities control of high

priorities inventories subject to lower impact on bottom line.

Disadvantages of ABC technique

There are some drawback of this accounting technique also there which are as follows:

ABC stock valuation is not considered valid as per GAAP and it has also problems and

conflicts with traditional costing system.

It requires more resources in order to maintain traditional costing system.

It only remain focused upon high priority inventories due to which less priority

inventories remain aside.

3

Traditional technique: this technique is one of the popular cost evaluating technique in

which cost of the product is analysed in as per the volume cost and cost drivers. There is a direct

cost bifurcated at various cost centres (Christ and Burritt, 2013).

Absorption costing: this costing technique helps to analyse value of inventories by

considering all the variable and fixed cost. Selling and distribution expenses are absorbed on

periodic basis. This is also known as full costing. Full absorption of costing is another aspect of

this costing technique cause it includes all material, labour and overhead to calculate profit and

valuation of stock.

Advantages of absorption costing

it consider all the cost which remain associated with manufacturing and non

manufacturing process.

It helps to analyse the seasonal sales and evaluate the profit for the sale of product. It connects accrual and matching concepts for specific accounting period.

Disadvantages of absorption costing

Only periodic fixed cost are considered in this while calculating cost.

Appropriation of overhead cost depends upon allocation of overheads cost

Triple costing: triple bottom line costing is known as evidenced based economic method

which helps to create combine efforts if cost benefit analysis and life cycle cost analysis. It helps

to determine net present value, project payback and return on investment. It helps to compute

both financial results and monetary values for environmental and social design impacts.

Advantages of triple costing

this is considered one of the complex techniques to evaluate the cost of product and sale

price of product. This technique helps manager to align operations and management of organisation as per

socially and environment friendly

Disadvantages of triple costing

scope of this technique is found in limited areas such as bottom line reporting of social

and environmental aspects.

Principles remain complex to calculate financial aspects such as earning, costs and

revenues to qualify social and environmental aspects.

4

which cost of the product is analysed in as per the volume cost and cost drivers. There is a direct

cost bifurcated at various cost centres (Christ and Burritt, 2013).

Absorption costing: this costing technique helps to analyse value of inventories by

considering all the variable and fixed cost. Selling and distribution expenses are absorbed on

periodic basis. This is also known as full costing. Full absorption of costing is another aspect of

this costing technique cause it includes all material, labour and overhead to calculate profit and

valuation of stock.

Advantages of absorption costing

it consider all the cost which remain associated with manufacturing and non

manufacturing process.

It helps to analyse the seasonal sales and evaluate the profit for the sale of product. It connects accrual and matching concepts for specific accounting period.

Disadvantages of absorption costing

Only periodic fixed cost are considered in this while calculating cost.

Appropriation of overhead cost depends upon allocation of overheads cost

Triple costing: triple bottom line costing is known as evidenced based economic method

which helps to create combine efforts if cost benefit analysis and life cycle cost analysis. It helps

to determine net present value, project payback and return on investment. It helps to compute

both financial results and monetary values for environmental and social design impacts.

Advantages of triple costing

this is considered one of the complex techniques to evaluate the cost of product and sale

price of product. This technique helps manager to align operations and management of organisation as per

socially and environment friendly

Disadvantages of triple costing

scope of this technique is found in limited areas such as bottom line reporting of social

and environmental aspects.

Principles remain complex to calculate financial aspects such as earning, costs and

revenues to qualify social and environmental aspects.

4

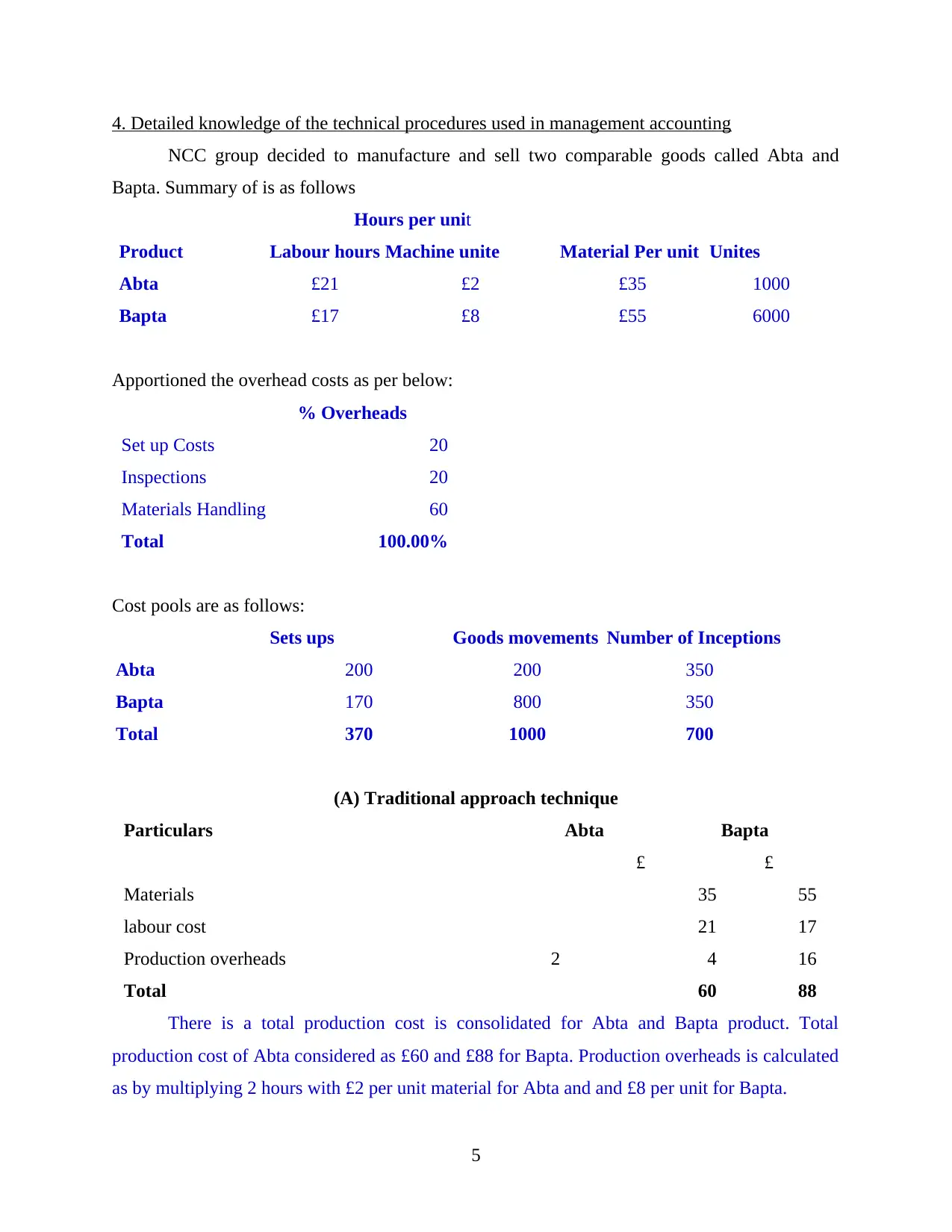

4. Detailed knowledge of the technical procedures used in management accounting

NCC group decided to manufacture and sell two comparable goods called Abta and

Bapta. Summary of is as follows

Hours per unit

Product Labour hours Machine unite Material Per unit Unites

Abta £21 £2 £35 1000

Bapta £17 £8 £55 6000

Apportioned the overhead costs as per below:

% Overheads

Set up Costs 20

Inspections 20

Materials Handling 60

Total 100.00%

Cost pools are as follows:

Sets ups Goods movements Number of Inceptions

Abta 200 200 350

Bapta 170 800 350

Total 370 1000 700

(A) Traditional approach technique

Particulars Abta Bapta

£ £

Materials 35 55

labour cost 21 17

Production overheads 2 4 16

Total 60 88

There is a total production cost is consolidated for Abta and Bapta product. Total

production cost of Abta considered as £60 and £88 for Bapta. Production overheads is calculated

as by multiplying 2 hours with £2 per unit material for Abta and and £8 per unit for Bapta.

5

NCC group decided to manufacture and sell two comparable goods called Abta and

Bapta. Summary of is as follows

Hours per unit

Product Labour hours Machine unite Material Per unit Unites

Abta £21 £2 £35 1000

Bapta £17 £8 £55 6000

Apportioned the overhead costs as per below:

% Overheads

Set up Costs 20

Inspections 20

Materials Handling 60

Total 100.00%

Cost pools are as follows:

Sets ups Goods movements Number of Inceptions

Abta 200 200 350

Bapta 170 800 350

Total 370 1000 700

(A) Traditional approach technique

Particulars Abta Bapta

£ £

Materials 35 55

labour cost 21 17

Production overheads 2 4 16

Total 60 88

There is a total production cost is consolidated for Abta and Bapta product. Total

production cost of Abta considered as £60 and £88 for Bapta. Production overheads is calculated

as by multiplying 2 hours with £2 per unit material for Abta and and £8 per unit for Bapta.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

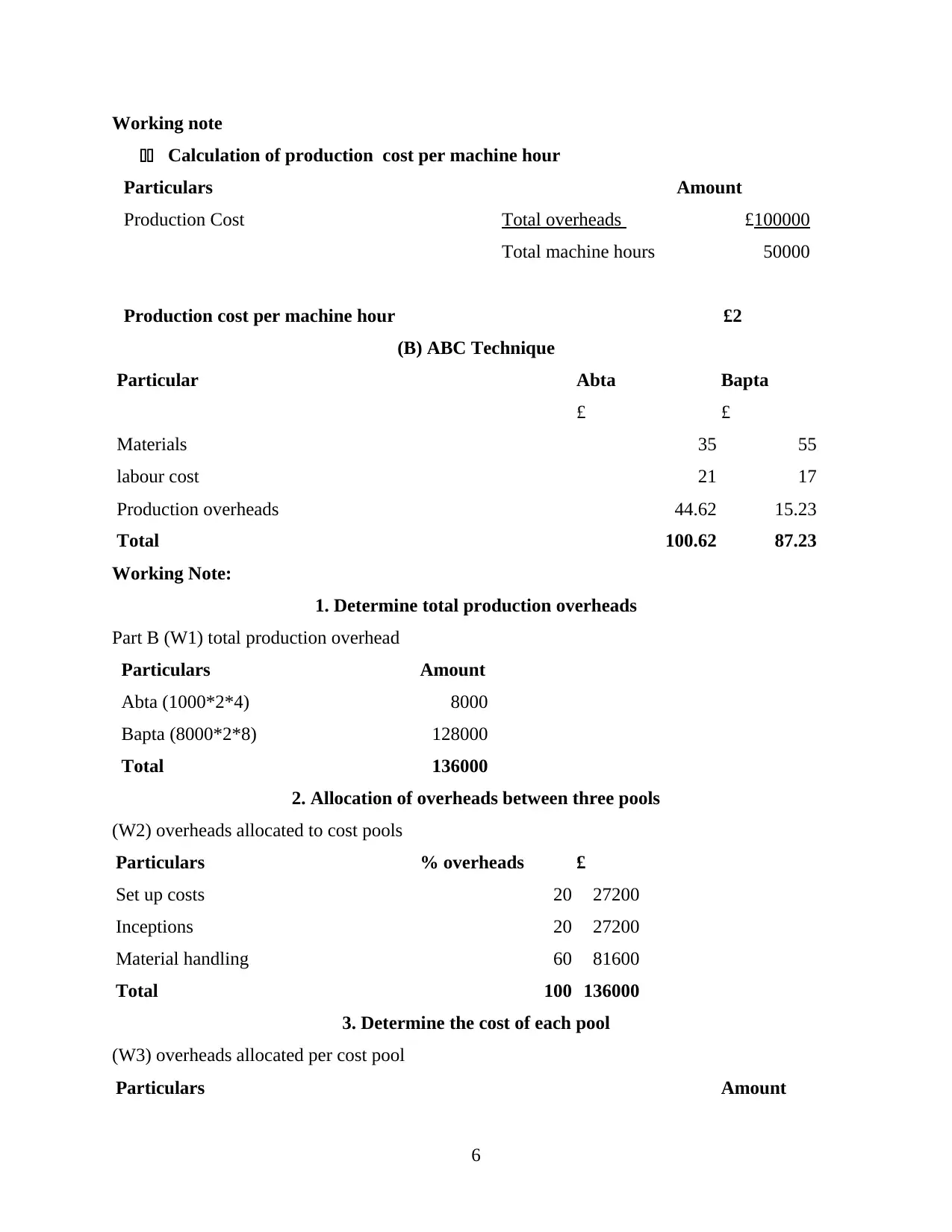

Working note

11 Calculation of production cost per machine hour

Particulars Amount

Production Cost Total overheads £100000

Total machine hours 50000

Production cost per machine hour £2

(B) ABC Technique

Particular Abta Bapta

£ £

Materials 35 55

labour cost 21 17

Production overheads 44.62 15.23

Total 100.62 87.23

Working Note:

1. Determine total production overheads

Part B (W1) total production overhead

Particulars Amount

Abta (1000*2*4) 8000

Bapta (8000*2*8) 128000

Total 136000

2. Allocation of overheads between three pools

(W2) overheads allocated to cost pools

Particulars % overheads £

Set up costs 20 27200

Inceptions 20 27200

Material handling 60 81600

Total 100 136000

3. Determine the cost of each pool

(W3) overheads allocated per cost pool

Particulars Amount

6

11 Calculation of production cost per machine hour

Particulars Amount

Production Cost Total overheads £100000

Total machine hours 50000

Production cost per machine hour £2

(B) ABC Technique

Particular Abta Bapta

£ £

Materials 35 55

labour cost 21 17

Production overheads 44.62 15.23

Total 100.62 87.23

Working Note:

1. Determine total production overheads

Part B (W1) total production overhead

Particulars Amount

Abta (1000*2*4) 8000

Bapta (8000*2*8) 128000

Total 136000

2. Allocation of overheads between three pools

(W2) overheads allocated to cost pools

Particulars % overheads £

Set up costs 20 27200

Inceptions 20 27200

Material handling 60 81600

Total 100 136000

3. Determine the cost of each pool

(W3) overheads allocated per cost pool

Particulars Amount

6

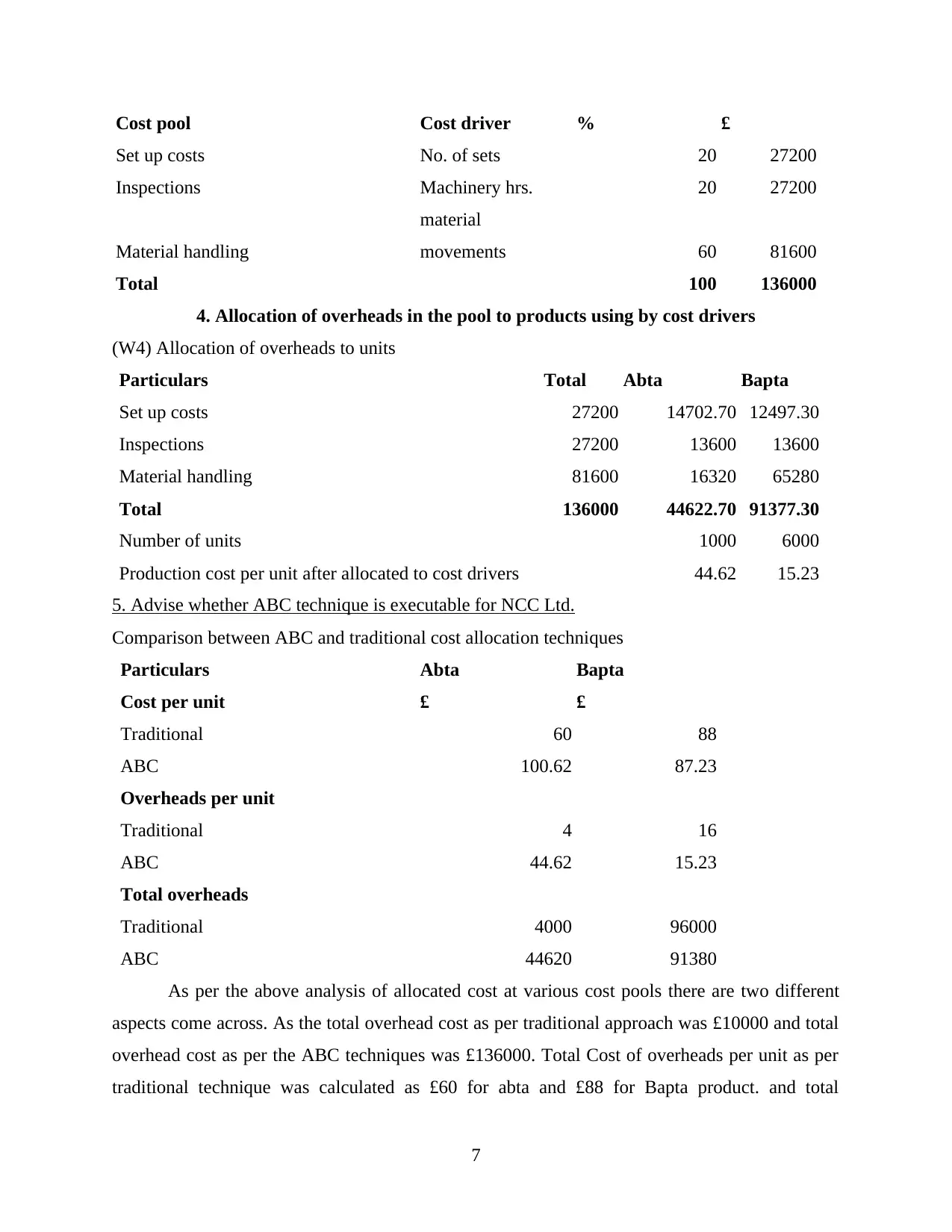

Cost pool Cost driver % £

Set up costs No. of sets 20 27200

Inspections Machinery hrs. 20 27200

Material handling

material

movements 60 81600

Total 100 136000

4. Allocation of overheads in the pool to products using by cost drivers

(W4) Allocation of overheads to units

Particulars Total Abta Bapta

Set up costs 27200 14702.70 12497.30

Inspections 27200 13600 13600

Material handling 81600 16320 65280

Total 136000 44622.70 91377.30

Number of units 1000 6000

Production cost per unit after allocated to cost drivers 44.62 15.23

5. Advise whether ABC technique is executable for NCC Ltd.

Comparison between ABC and traditional cost allocation techniques

Particulars Abta Bapta

Cost per unit £ £

Traditional 60 88

ABC 100.62 87.23

Overheads per unit

Traditional 4 16

ABC 44.62 15.23

Total overheads

Traditional 4000 96000

ABC 44620 91380

As per the above analysis of allocated cost at various cost pools there are two different

aspects come across. As the total overhead cost as per traditional approach was £10000 and total

overhead cost as per the ABC techniques was £136000. Total Cost of overheads per unit as per

traditional technique was calculated as £60 for abta and £88 for Bapta product. and total

7

Set up costs No. of sets 20 27200

Inspections Machinery hrs. 20 27200

Material handling

material

movements 60 81600

Total 100 136000

4. Allocation of overheads in the pool to products using by cost drivers

(W4) Allocation of overheads to units

Particulars Total Abta Bapta

Set up costs 27200 14702.70 12497.30

Inspections 27200 13600 13600

Material handling 81600 16320 65280

Total 136000 44622.70 91377.30

Number of units 1000 6000

Production cost per unit after allocated to cost drivers 44.62 15.23

5. Advise whether ABC technique is executable for NCC Ltd.

Comparison between ABC and traditional cost allocation techniques

Particulars Abta Bapta

Cost per unit £ £

Traditional 60 88

ABC 100.62 87.23

Overheads per unit

Traditional 4 16

ABC 44.62 15.23

Total overheads

Traditional 4000 96000

ABC 44620 91380

As per the above analysis of allocated cost at various cost pools there are two different

aspects come across. As the total overhead cost as per traditional approach was £10000 and total

overhead cost as per the ABC techniques was £136000. Total Cost of overheads per unit as per

traditional technique was calculated as £60 for abta and £88 for Bapta product. and total

7

overhead cost per unit as per ABC technique was calculated as £100.62 for for the product and

£87.23 for the Bapta product. It is difficult to judge that which method will be beneficial for the

organisation in terms of evaluating the effective method. Abpta product have low cost as per

traditional whereas Bapta product has a high cost in comparison to ABC techniques and vise

versa.

To determine the optimum evaluating techniques the overhead cost would be taken to

decision making. Total overheads as per traditional approach was £100000 and as per ABC

technique total overhead cost was calculated as £136000. that is the reason that ABC technique

of allocating cost is not appropriate.

CONCLUSION

This reports is prepared to elaborate the aspects of management accoutring. Measurement

of cost and profitability with the use of ABC technique and traditional technique are defined in

this report. Cost bifurcation techniques are used subject to practical scenario. NCC group Plc's

cost bifurcation is illustrated in this context. Management accounting and analysation of

information done in respect of NCC group. Wide range of management accounting techniques

defined in respect of chosen organisation. Techniques are critically evaluated in respect of NCC

group. Detailed knowledge is utilised in respect of demonstrating the information provided for

acknowledgement. There is a comparison between ABC technique and Traditional technique.

8

£87.23 for the Bapta product. It is difficult to judge that which method will be beneficial for the

organisation in terms of evaluating the effective method. Abpta product have low cost as per

traditional whereas Bapta product has a high cost in comparison to ABC techniques and vise

versa.

To determine the optimum evaluating techniques the overhead cost would be taken to

decision making. Total overheads as per traditional approach was £100000 and as per ABC

technique total overhead cost was calculated as £136000. that is the reason that ABC technique

of allocating cost is not appropriate.

CONCLUSION

This reports is prepared to elaborate the aspects of management accoutring. Measurement

of cost and profitability with the use of ABC technique and traditional technique are defined in

this report. Cost bifurcation techniques are used subject to practical scenario. NCC group Plc's

cost bifurcation is illustrated in this context. Management accounting and analysation of

information done in respect of NCC group. Wide range of management accounting techniques

defined in respect of chosen organisation. Techniques are critically evaluated in respect of NCC

group. Detailed knowledge is utilised in respect of demonstrating the information provided for

acknowledgement. There is a comparison between ABC technique and Traditional technique.

8

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.