Management Accounting Report: Decision Making, Costing, and Planning

VerifiedAdded on 2020/07/23

|16

|4536

|129

Report

AI Summary

This report provides a comprehensive overview of management accounting, focusing on its importance for decision-making and improving organizational performance. It explores various management accounting systems, including job order costing, sales forecasting, and budget management reports. The report delves into the critical evaluation of these systems, highlighting their advantages and disadvantages. A significant portion is dedicated to comparative income statements using marginal and absorption costing methods, analyzing profit variations and reconciliation statements. The report also includes a case study on Nero Ltd, examining different planning tools and ways to prevent financial problems. Overall, the report aims to enhance understanding of management accounting principles and their application in real-world business scenarios.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

SECTION 1......................................................................................................................................1

1) Importance of management accounting for decision making process towards improving

organisation's performance..........................................................................................................1

2) Different management accounting systems for preparing reports..........................................2

3) Critical evaluation on management accounting systems........................................................4

4).................................................................................................................................................5

a) Comparative income statement using marginal and absorption costing.................................5

b) Reasons behind profit variation..............................................................................................8

c) Reconciled statement of profit and loss account.....................................................................8

SECTION 2 (Nero Ltd)...................................................................................................................9

Part (a) Different planning tools.................................................................................................9

Part (b) Ways to prevent financial problems obtained at Nero Ltd..........................................10

CONCLUSION..............................................................................................................................11

REFERENCE.................................................................................................................................12

INTRODUCTION...........................................................................................................................1

SECTION 1......................................................................................................................................1

1) Importance of management accounting for decision making process towards improving

organisation's performance..........................................................................................................1

2) Different management accounting systems for preparing reports..........................................2

3) Critical evaluation on management accounting systems........................................................4

4).................................................................................................................................................5

a) Comparative income statement using marginal and absorption costing.................................5

b) Reasons behind profit variation..............................................................................................8

c) Reconciled statement of profit and loss account.....................................................................8

SECTION 2 (Nero Ltd)...................................................................................................................9

Part (a) Different planning tools.................................................................................................9

Part (b) Ways to prevent financial problems obtained at Nero Ltd..........................................10

CONCLUSION..............................................................................................................................11

REFERENCE.................................................................................................................................12

INDEX OF TABLES

Table 1: Income statement using marginal costing method.............................................................6

Table 2: Income statement using absorption costing method..........................................................7

Table 3: Fixed and under absorbed costs for 1st and 2nd quarter...................................................8

Table 1: Income statement using marginal costing method.............................................................6

Table 2: Income statement using absorption costing method..........................................................7

Table 3: Fixed and under absorbed costs for 1st and 2nd quarter...................................................8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management accounting is composition of all accounting systems including financial,

cost, inventory and so on. It is essential for identifying actual position of business operations and

decision making for organisation's effectiveness. The present report is based on understanding

significance of management accounting regarding business activities of Nero Ltd. In this regard,

various types of management accounting reports, income statement for through marginal and

absorption costing is to be described. However, different budgetary control systems for

forecasting and decision making can be introduced through this assignment. Along with this,

financial tools for reducing economic problem of the entity is to express. Thus, learners are able

to understand importance of management accounting for decision making regarding business

operations of the organisation through this report.

SECTION 1

1) Importance of management accounting for decision making process towards improving

organisation's performance

Management accounting is multidisciplinary approach that evolves several tools for

decision making and organisation's effectiveness. For example; financial accounting, cost

accounting, inventory management accounting, performance management accounting and so on.

However, management accountant of the entity analyses all financial tools and further makes

decision regarding further business operations to improve its economic position. Moreover,

sevral tools are used for decision making such as costing, budgeting, variance analysis etc. In

which, organisation's performance is analysed at first and further strategies are prepared for

better quality services and enhancing effectiveness (Akhavan, Ward and Bozic, 2016). Along

with this, it remains helpful for optimum utilization of resources and fund that impacts on

productivity and profitability of the entity effectively. Therefore, various tools are recognised

that impacts on further operations and its competitiveness for longer time periodicity. Thus,

management accountancy reads, analysis and interprets the informations and data obtained from

the external and internal business environment and reports the data to the management. This

report helps the management in making policy related decisions in effective manner.

1

Management accounting is composition of all accounting systems including financial,

cost, inventory and so on. It is essential for identifying actual position of business operations and

decision making for organisation's effectiveness. The present report is based on understanding

significance of management accounting regarding business activities of Nero Ltd. In this regard,

various types of management accounting reports, income statement for through marginal and

absorption costing is to be described. However, different budgetary control systems for

forecasting and decision making can be introduced through this assignment. Along with this,

financial tools for reducing economic problem of the entity is to express. Thus, learners are able

to understand importance of management accounting for decision making regarding business

operations of the organisation through this report.

SECTION 1

1) Importance of management accounting for decision making process towards improving

organisation's performance

Management accounting is multidisciplinary approach that evolves several tools for

decision making and organisation's effectiveness. For example; financial accounting, cost

accounting, inventory management accounting, performance management accounting and so on.

However, management accountant of the entity analyses all financial tools and further makes

decision regarding further business operations to improve its economic position. Moreover,

sevral tools are used for decision making such as costing, budgeting, variance analysis etc. In

which, organisation's performance is analysed at first and further strategies are prepared for

better quality services and enhancing effectiveness (Akhavan, Ward and Bozic, 2016). Along

with this, it remains helpful for optimum utilization of resources and fund that impacts on

productivity and profitability of the entity effectively. Therefore, various tools are recognised

that impacts on further operations and its competitiveness for longer time periodicity. Thus,

management accountancy reads, analysis and interprets the informations and data obtained from

the external and internal business environment and reports the data to the management. This

report helps the management in making policy related decisions in effective manner.

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Management accounting helps the management in comparing actual figures with the

already set standard figures to track deviations. This feature of management accounting

helps the management take further decisions.

All the business decisions and planning is done on the base of accounting information

applying budgeting and forecast techniques. All these techniques are woven together to

achieve the organisational objectives. These budgeting and forecasting techniques are

applied and implemented by the management accounting (Akyol, Tuncel and Bayhan,

2015).

Optimal utilization if the capital is made possible with the help of management

accounting. Management accounting help in effective running of the business.

Management accounting facilitates smooth coordination between al the departments

making running of business better. Coordination between the departments also make the

decision making process of the business swift.

Management accounting plays a significant role in organizing the business win an

efficient way (Chouhan, Soral and Chandra, 2017). Management accounting assists the

management via the tools of internal control and internal audit in fixation of targets and

responsibilities, appraisal of performance, problem identification and solutions to these

cost and profit centres and executing overall control of the business organisational

activities.

Management accounting through these activities of departmental coordination help the

management to motivate employees.

The inventory is a very important part of business, it is necessary to control the inventory

from the moment it is purchased to all the processes in the business. This control is does

with the help of the inventory control technique of the management accounting, this also

helps in the decision making process of the organisation.

The management accounting tools of forecasting budgeting and inventory control help

the management in cutting the cost and manage the cost at different stages.

2) Different management accounting systems for preparing reports

The Management accountant of an organisation maintains and develop different reports

which present various financially and non-economical execution of an organisation such as its

listing of management reports, analysis of different reports, cost for job ordering inventory,

2

already set standard figures to track deviations. This feature of management accounting

helps the management take further decisions.

All the business decisions and planning is done on the base of accounting information

applying budgeting and forecast techniques. All these techniques are woven together to

achieve the organisational objectives. These budgeting and forecasting techniques are

applied and implemented by the management accounting (Akyol, Tuncel and Bayhan,

2015).

Optimal utilization if the capital is made possible with the help of management

accounting. Management accounting help in effective running of the business.

Management accounting facilitates smooth coordination between al the departments

making running of business better. Coordination between the departments also make the

decision making process of the business swift.

Management accounting plays a significant role in organizing the business win an

efficient way (Chouhan, Soral and Chandra, 2017). Management accounting assists the

management via the tools of internal control and internal audit in fixation of targets and

responsibilities, appraisal of performance, problem identification and solutions to these

cost and profit centres and executing overall control of the business organisational

activities.

Management accounting through these activities of departmental coordination help the

management to motivate employees.

The inventory is a very important part of business, it is necessary to control the inventory

from the moment it is purchased to all the processes in the business. This control is does

with the help of the inventory control technique of the management accounting, this also

helps in the decision making process of the organisation.

The management accounting tools of forecasting budgeting and inventory control help

the management in cutting the cost and manage the cost at different stages.

2) Different management accounting systems for preparing reports

The Management accountant of an organisation maintains and develop different reports

which present various financially and non-economical execution of an organisation such as its

listing of management reports, analysis of different reports, cost for job ordering inventory,

2

manages and reports performance, and in setting up of different budgets. These managements

can be described as-

Job order costing report: - This reporting system helps in the analysis of cost which is

obtained in the manufacturing of company's products and services, which includes basic

sources such as raw materials, costing for labour and others. Regarding to this, Entity

determines the price of different products and services with the expanses of tools which

are required in the production (El and Lindefors, 2016). By analysing all these financial

records the expense's costing and revenues are developed in taking further decisions and

in their implementation.

Sale forecasting report: - This report helps in the analysis of financial data of an

organisation's marketing services and products. This report assist organisation in the

distribution of their products and services and in expenditures on production, further in

future decision making and building of strategies. Further through report marketing,

entity market position can be determined with last year performance analysis. It also

assists in allocation of funds and resources which can help in achieving systematic

management of goods.

Budget management report: - This report help in managing accounting techniques

which assist in forecasting of futures plans and in the making of decision with better

innovative ideas which increases service quality and management (Johnson, 2014).

Inventory management report: - This directly affects the liquidity of the company

which help in management of the operations in business. This method provides overall

goods' transaction and financial information. It can also affect the company to improves

its products and services more efficiently and effectively. Which helps in proper

management of manufacturing process and reduction of excess of waste.

Performance management report: - It involves and focuses on several activities

regarding to disciplinary approaches in company, such as workers performance

efficiencies and effectiveness. In this process different critical evaluation is taken which

improves work efficiency and encourages them to work and provide better contribution in

team work. According to workers ability and evaluation in performance the report is

developed for its management (Laviana and et.al., 2016).

3

can be described as-

Job order costing report: - This reporting system helps in the analysis of cost which is

obtained in the manufacturing of company's products and services, which includes basic

sources such as raw materials, costing for labour and others. Regarding to this, Entity

determines the price of different products and services with the expanses of tools which

are required in the production (El and Lindefors, 2016). By analysing all these financial

records the expense's costing and revenues are developed in taking further decisions and

in their implementation.

Sale forecasting report: - This report helps in the analysis of financial data of an

organisation's marketing services and products. This report assist organisation in the

distribution of their products and services and in expenditures on production, further in

future decision making and building of strategies. Further through report marketing,

entity market position can be determined with last year performance analysis. It also

assists in allocation of funds and resources which can help in achieving systematic

management of goods.

Budget management report: - This report help in managing accounting techniques

which assist in forecasting of futures plans and in the making of decision with better

innovative ideas which increases service quality and management (Johnson, 2014).

Inventory management report: - This directly affects the liquidity of the company

which help in management of the operations in business. This method provides overall

goods' transaction and financial information. It can also affect the company to improves

its products and services more efficiently and effectively. Which helps in proper

management of manufacturing process and reduction of excess of waste.

Performance management report: - It involves and focuses on several activities

regarding to disciplinary approaches in company, such as workers performance

efficiencies and effectiveness. In this process different critical evaluation is taken which

improves work efficiency and encourages them to work and provide better contribution in

team work. According to workers ability and evaluation in performance the report is

developed for its management (Laviana and et.al., 2016).

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Thus, management accountant of the organisation prepares and maintains above

mentioned reports that demon estate financial position and generates different ideas for better

quality services and improving monetary position. For this purpose, all business operations are

recorded which are identified and further decisions are made on these bases. Hence, maintaining

these reports affect management of entire business operations and its services for further years

and sustainability in market for longer time period.

3) Critical evaluation on management accounting systems

Critical evaluation essential management accounting systems can be understood as below

which can be balanced and improved regarding effective business operations for further years as:

Budget management accounting system: - This system promotes in forecasting future

plans in an organisation along with, it encourages planning orientation, review on

profitability, Assumption of reviews, helps in evaluating performance, in the allocation of

cash, bottleneck analysis and others (Najjar, Strickland and Kaplan, 2016). But along

with these advantages it is having several disadvantages to the company as well because

of, time requirement, blame for the outcomes, allocation in expenses, rigidity in strategic

formation and others.

Performance management accounting system: - This management system works as to

manage performance discipline in the work of employees of company. It assists on the

basis of conversation which are based on performance, targeted development and

encouragement of staff, rewarding when job is done well, and for the identification of

underperformance and their elimination. Whereas, this system is also very much time

consuming, it can discourage staff if not performed well and may give inconsistent

message or may promote biases behaviour in company (Sandborn, 2017).

Job order costing Management accounting system: - This management system helps

in the determination of products and services Costs of company. In the form of detailed

analysis of material cost, helps to determine production cost, in reduction of unprofitable

tasks, and in the controlling of extra material and labour cost and others. Whereas, by the

use of this system company can have several disadvantages like this system is based on

hectically cost, it is quite expensive as well because of separate records and jobs, it is also

4

mentioned reports that demon estate financial position and generates different ideas for better

quality services and improving monetary position. For this purpose, all business operations are

recorded which are identified and further decisions are made on these bases. Hence, maintaining

these reports affect management of entire business operations and its services for further years

and sustainability in market for longer time period.

3) Critical evaluation on management accounting systems

Critical evaluation essential management accounting systems can be understood as below

which can be balanced and improved regarding effective business operations for further years as:

Budget management accounting system: - This system promotes in forecasting future

plans in an organisation along with, it encourages planning orientation, review on

profitability, Assumption of reviews, helps in evaluating performance, in the allocation of

cash, bottleneck analysis and others (Najjar, Strickland and Kaplan, 2016). But along

with these advantages it is having several disadvantages to the company as well because

of, time requirement, blame for the outcomes, allocation in expenses, rigidity in strategic

formation and others.

Performance management accounting system: - This management system works as to

manage performance discipline in the work of employees of company. It assists on the

basis of conversation which are based on performance, targeted development and

encouragement of staff, rewarding when job is done well, and for the identification of

underperformance and their elimination. Whereas, this system is also very much time

consuming, it can discourage staff if not performed well and may give inconsistent

message or may promote biases behaviour in company (Sandborn, 2017).

Job order costing Management accounting system: - This management system helps

in the determination of products and services Costs of company. In the form of detailed

analysis of material cost, helps to determine production cost, in reduction of unprofitable

tasks, and in the controlling of extra material and labour cost and others. Whereas, by the

use of this system company can have several disadvantages like this system is based on

hectically cost, it is quite expensive as well because of separate records and jobs, it is also

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

difficult for calculation of exact cost, and methods also may not be suitable for company

sometimes (Yang and Hao, 2017).

Sales forecasting reports:- Sales forecast a report which is prepared by the company to

forecast the sales of the next quarter on the basis of the sales trend. The property of sales

forecasting is that it gives company the power to monitor and track its sales after the current

period. This strategy helps the management to formulate business strategy for the future on the

basis of sales growth. The preparation of sales forecast is dependent on historic data or sales of

the prior period, this limits its properties, as, if the business is new there is not enough prior data

so a forecast can't be prepared.

Inventory management report:-Inventory management report is prepared by the

business to track the coming and usage of inventory in the business. This report count and collect

data on all the inventory.

This report helps the business to keep a track of all the inventory items thus there is no

chance of theft and misplacement can be identified easily.

Book keeping of inventory is a hectic and lengthy process and takes too much time

(Agrawal, 2013).

4)

a) Comparative income statement using marginal and absorption costing

Costing is a process of price determination and setting cost associated on business

operations. It influences productivity and profitability of the organisation as well competitiveness

and further operations. However, income statement is prepared on the basis of incurred expenses

and gained revenue regarding business activities. This costing is created on behalf of different

tools such as; expenses incurred for manufacturing and production process, market demand,

competitiveness and so on. Including this, several methods are used for costing as marginal,

absorption, activity based costing etc (Akhavan, Ward and Bozic, 2016). For preparing income

statement through marginal and absorption costing for organisation, entity's profitability is

identified as below:

Income statement through different costing methods: Income statement through

marginal costing is different from absorption cost because of profit variation. It can be

understood as follows:

5

sometimes (Yang and Hao, 2017).

Sales forecasting reports:- Sales forecast a report which is prepared by the company to

forecast the sales of the next quarter on the basis of the sales trend. The property of sales

forecasting is that it gives company the power to monitor and track its sales after the current

period. This strategy helps the management to formulate business strategy for the future on the

basis of sales growth. The preparation of sales forecast is dependent on historic data or sales of

the prior period, this limits its properties, as, if the business is new there is not enough prior data

so a forecast can't be prepared.

Inventory management report:-Inventory management report is prepared by the

business to track the coming and usage of inventory in the business. This report count and collect

data on all the inventory.

This report helps the business to keep a track of all the inventory items thus there is no

chance of theft and misplacement can be identified easily.

Book keeping of inventory is a hectic and lengthy process and takes too much time

(Agrawal, 2013).

4)

a) Comparative income statement using marginal and absorption costing

Costing is a process of price determination and setting cost associated on business

operations. It influences productivity and profitability of the organisation as well competitiveness

and further operations. However, income statement is prepared on the basis of incurred expenses

and gained revenue regarding business activities. This costing is created on behalf of different

tools such as; expenses incurred for manufacturing and production process, market demand,

competitiveness and so on. Including this, several methods are used for costing as marginal,

absorption, activity based costing etc (Akhavan, Ward and Bozic, 2016). For preparing income

statement through marginal and absorption costing for organisation, entity's profitability is

identified as below:

Income statement through different costing methods: Income statement through

marginal costing is different from absorption cost because of profit variation. It can be

understood as follows:

5

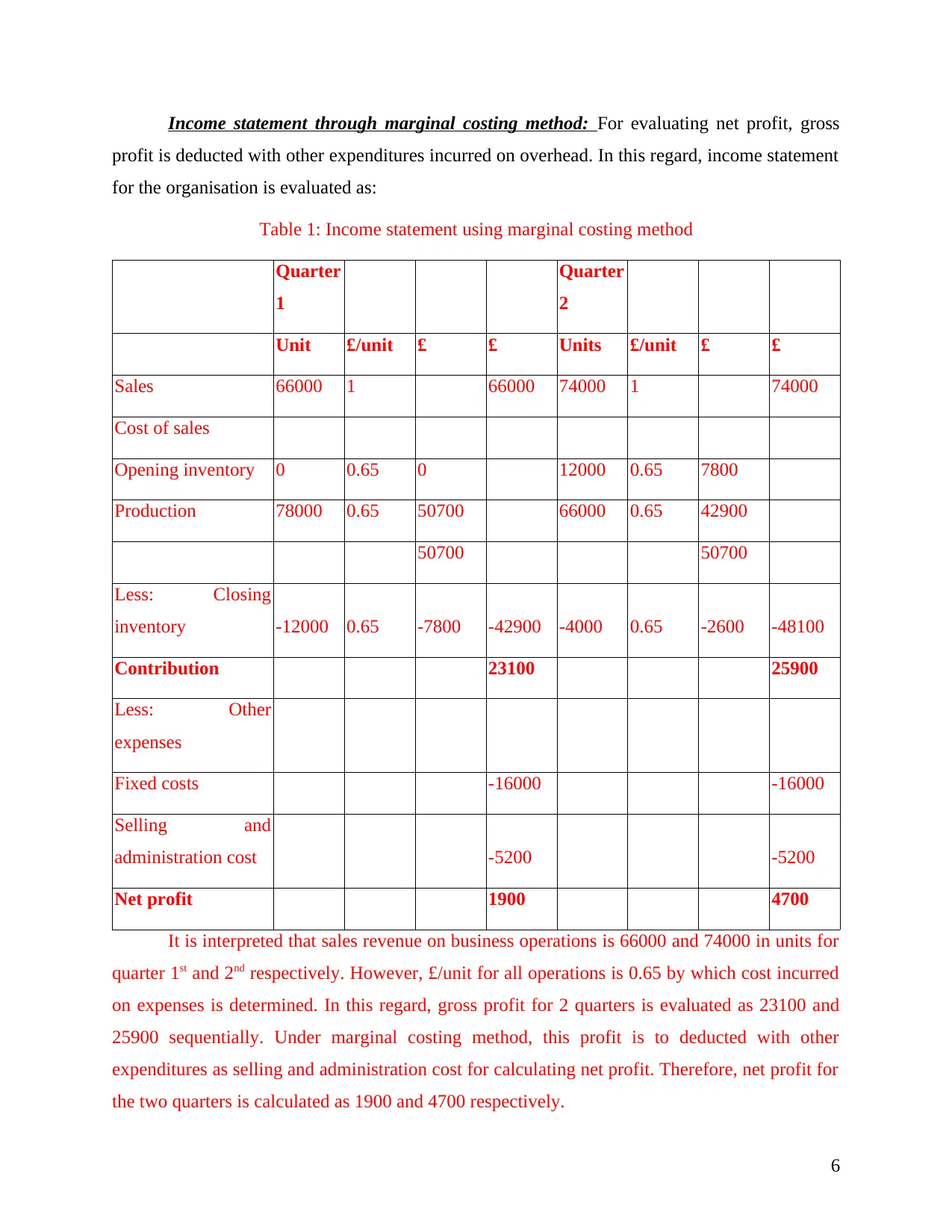

Income statement through marginal costing method: For evaluating net profit, gross

profit is deducted with other expenditures incurred on overhead. In this regard, income statement

for the organisation is evaluated as:

Table 1: Income statement using marginal costing method

Quarter

1

Quarter

2

Unit £/unit £ £ Units £/unit £ £

Sales 66000 1 66000 74000 1 74000

Cost of sales

Opening inventory 0 0.65 0 12000 0.65 7800

Production 78000 0.65 50700 66000 0.65 42900

50700 50700

Less: Closing

inventory -12000 0.65 -7800 -42900 -4000 0.65 -2600 -48100

Contribution 23100 25900

Less: Other

expenses

Fixed costs -16000 -16000

Selling and

administration cost -5200 -5200

Net profit 1900 4700

It is interpreted that sales revenue on business operations is 66000 and 74000 in units for

quarter 1st and 2nd respectively. However, £/unit for all operations is 0.65 by which cost incurred

on expenses is determined. In this regard, gross profit for 2 quarters is evaluated as 23100 and

25900 sequentially. Under marginal costing method, this profit is to deducted with other

expenditures as selling and administration cost for calculating net profit. Therefore, net profit for

the two quarters is calculated as 1900 and 4700 respectively.

6

profit is deducted with other expenditures incurred on overhead. In this regard, income statement

for the organisation is evaluated as:

Table 1: Income statement using marginal costing method

Quarter

1

Quarter

2

Unit £/unit £ £ Units £/unit £ £

Sales 66000 1 66000 74000 1 74000

Cost of sales

Opening inventory 0 0.65 0 12000 0.65 7800

Production 78000 0.65 50700 66000 0.65 42900

50700 50700

Less: Closing

inventory -12000 0.65 -7800 -42900 -4000 0.65 -2600 -48100

Contribution 23100 25900

Less: Other

expenses

Fixed costs -16000 -16000

Selling and

administration cost -5200 -5200

Net profit 1900 4700

It is interpreted that sales revenue on business operations is 66000 and 74000 in units for

quarter 1st and 2nd respectively. However, £/unit for all operations is 0.65 by which cost incurred

on expenses is determined. In this regard, gross profit for 2 quarters is evaluated as 23100 and

25900 sequentially. Under marginal costing method, this profit is to deducted with other

expenditures as selling and administration cost for calculating net profit. Therefore, net profit for

the two quarters is calculated as 1900 and 4700 respectively.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

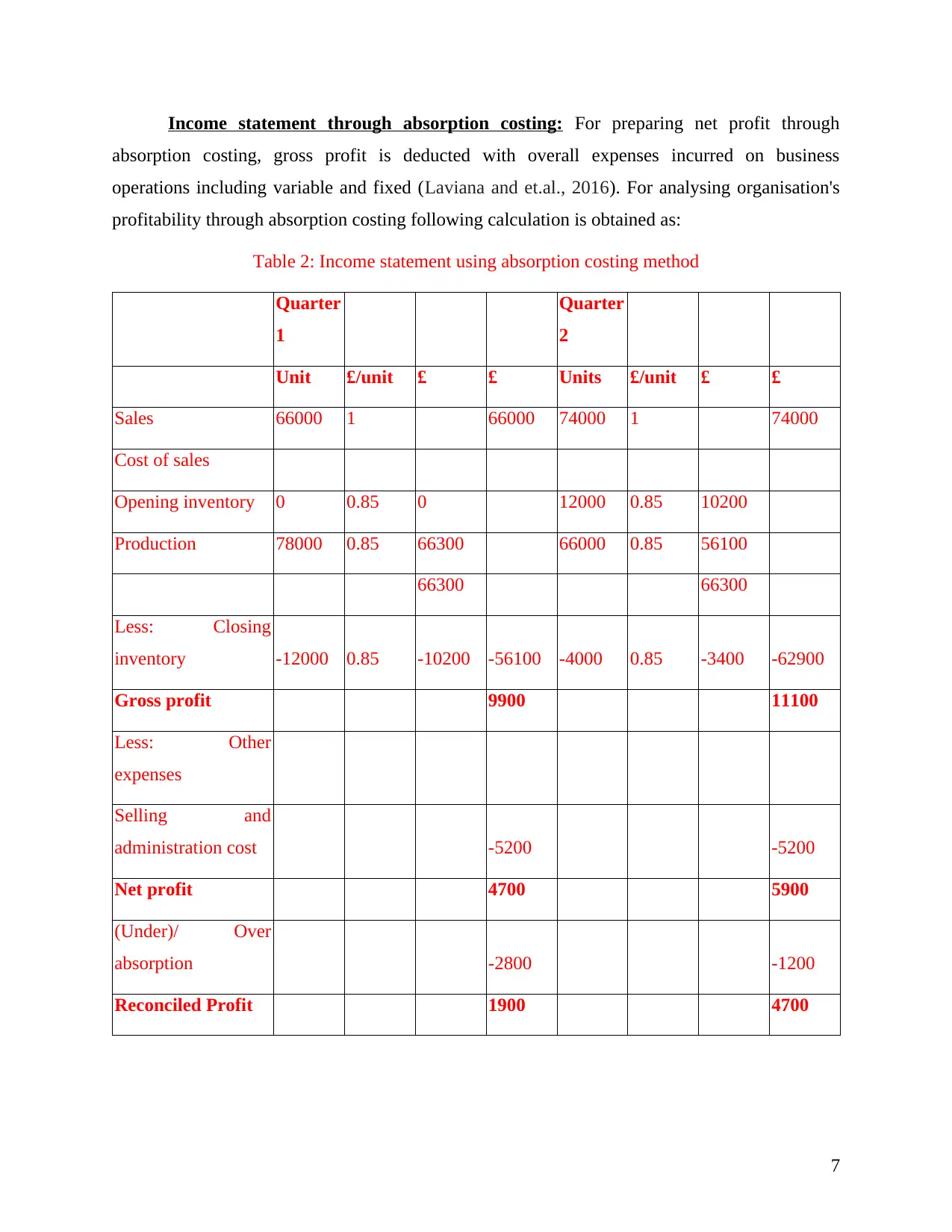

Income statement through absorption costing: For preparing net profit through

absorption costing, gross profit is deducted with overall expenses incurred on business

operations including variable and fixed (Laviana and et.al., 2016). For analysing organisation's

profitability through absorption costing following calculation is obtained as:

Table 2: Income statement using absorption costing method

Quarter

1

Quarter

2

Unit £/unit £ £ Units £/unit £ £

Sales 66000 1 66000 74000 1 74000

Cost of sales

Opening inventory 0 0.85 0 12000 0.85 10200

Production 78000 0.85 66300 66000 0.85 56100

66300 66300

Less: Closing

inventory -12000 0.85 -10200 -56100 -4000 0.85 -3400 -62900

Gross profit 9900 11100

Less: Other

expenses

Selling and

administration cost -5200 -5200

Net profit 4700 5900

(Under)/ Over

absorption -2800 -1200

Reconciled Profit 1900 4700

7

absorption costing, gross profit is deducted with overall expenses incurred on business

operations including variable and fixed (Laviana and et.al., 2016). For analysing organisation's

profitability through absorption costing following calculation is obtained as:

Table 2: Income statement using absorption costing method

Quarter

1

Quarter

2

Unit £/unit £ £ Units £/unit £ £

Sales 66000 1 66000 74000 1 74000

Cost of sales

Opening inventory 0 0.85 0 12000 0.85 10200

Production 78000 0.85 66300 66000 0.85 56100

66300 66300

Less: Closing

inventory -12000 0.85 -10200 -56100 -4000 0.85 -3400 -62900

Gross profit 9900 11100

Less: Other

expenses

Selling and

administration cost -5200 -5200

Net profit 4700 5900

(Under)/ Over

absorption -2800 -1200

Reconciled Profit 1900 4700

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Under absorption costing method, for evaluating net profit, overall expenditures incurred

on fixed and variable overhead are included. However, £ per unit for both 1st and 2nd quarter is

0.85 on which gross profit is determined as 9900 and 11100 respectively. It is to deducted with

overall expenses incurred on additional expenditures evaluated as 4700 and 5900 for both

quarters. Including this, by deducting net profit with under or over absorption, reconciled profit

is evaluated that is 1900 and 4700 for 1st and 2nd quarter respectively.

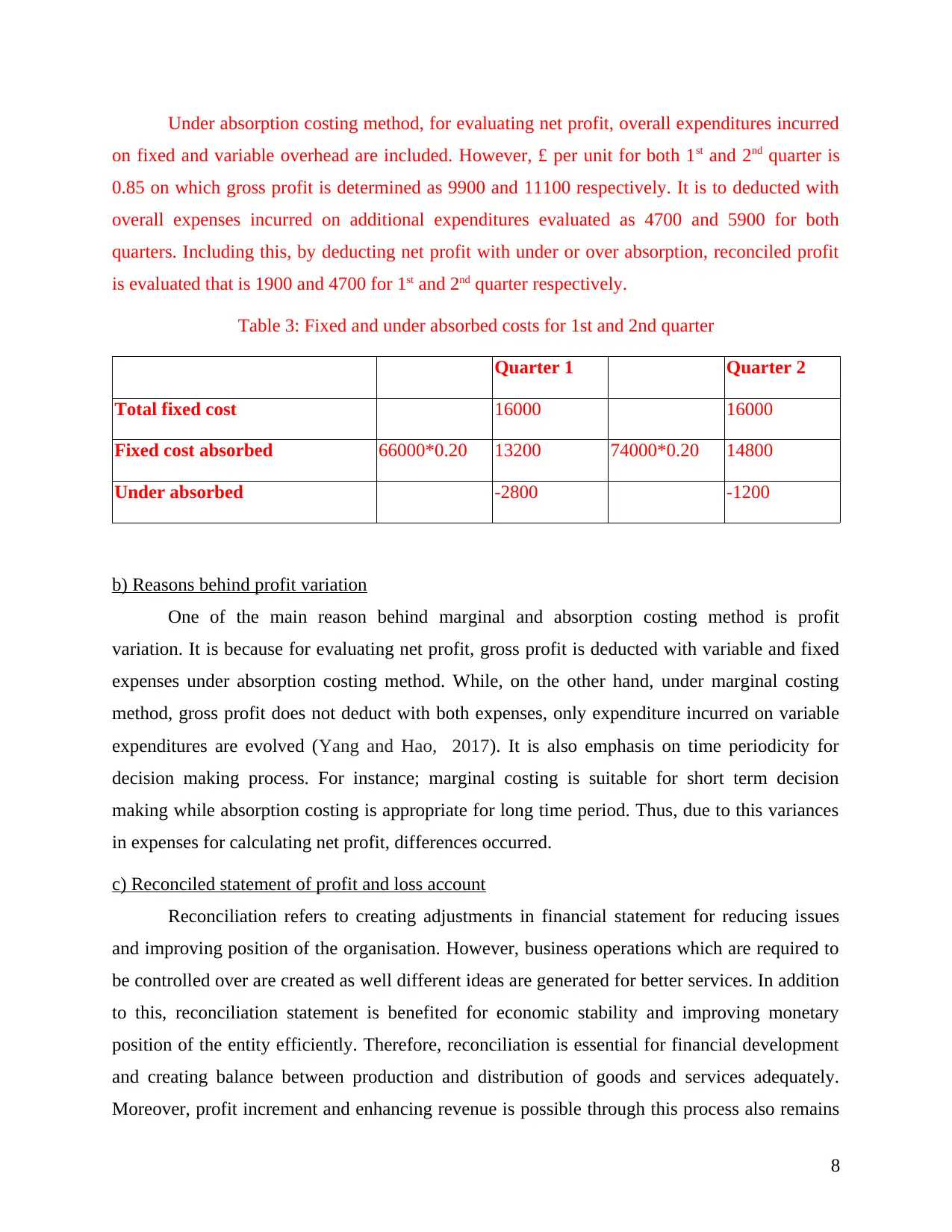

Table 3: Fixed and under absorbed costs for 1st and 2nd quarter

Quarter 1 Quarter 2

Total fixed cost 16000 16000

Fixed cost absorbed 66000*0.20 13200 74000*0.20 14800

Under absorbed -2800 -1200

b) Reasons behind profit variation

One of the main reason behind marginal and absorption costing method is profit

variation. It is because for evaluating net profit, gross profit is deducted with variable and fixed

expenses under absorption costing method. While, on the other hand, under marginal costing

method, gross profit does not deduct with both expenses, only expenditure incurred on variable

expenditures are evolved (Yang and Hao, 2017). It is also emphasis on time periodicity for

decision making process. For instance; marginal costing is suitable for short term decision

making while absorption costing is appropriate for long time period. Thus, due to this variances

in expenses for calculating net profit, differences occurred.

c) Reconciled statement of profit and loss account

Reconciliation refers to creating adjustments in financial statement for reducing issues

and improving position of the organisation. However, business operations which are required to

be controlled over are created as well different ideas are generated for better services. In addition

to this, reconciliation statement is benefited for economic stability and improving monetary

position of the entity efficiently. Therefore, reconciliation is essential for financial development

and creating balance between production and distribution of goods and services adequately.

Moreover, profit increment and enhancing revenue is possible through this process also remains

8

on fixed and variable overhead are included. However, £ per unit for both 1st and 2nd quarter is

0.85 on which gross profit is determined as 9900 and 11100 respectively. It is to deducted with

overall expenses incurred on additional expenditures evaluated as 4700 and 5900 for both

quarters. Including this, by deducting net profit with under or over absorption, reconciled profit

is evaluated that is 1900 and 4700 for 1st and 2nd quarter respectively.

Table 3: Fixed and under absorbed costs for 1st and 2nd quarter

Quarter 1 Quarter 2

Total fixed cost 16000 16000

Fixed cost absorbed 66000*0.20 13200 74000*0.20 14800

Under absorbed -2800 -1200

b) Reasons behind profit variation

One of the main reason behind marginal and absorption costing method is profit

variation. It is because for evaluating net profit, gross profit is deducted with variable and fixed

expenses under absorption costing method. While, on the other hand, under marginal costing

method, gross profit does not deduct with both expenses, only expenditure incurred on variable

expenditures are evolved (Yang and Hao, 2017). It is also emphasis on time periodicity for

decision making process. For instance; marginal costing is suitable for short term decision

making while absorption costing is appropriate for long time period. Thus, due to this variances

in expenses for calculating net profit, differences occurred.

c) Reconciled statement of profit and loss account

Reconciliation refers to creating adjustments in financial statement for reducing issues

and improving position of the organisation. However, business operations which are required to

be controlled over are created as well different ideas are generated for better services. In addition

to this, reconciliation statement is benefited for economic stability and improving monetary

position of the entity efficiently. Therefore, reconciliation is essential for financial development

and creating balance between production and distribution of goods and services adequately.

Moreover, profit increment and enhancing revenue is possible through this process also remains

8

suitable for making adjustment and finding out reasons behind the difference (Akyol, Tuncel and

Bayhan, 2015). Thus, reconciliation of profit and loss account impacts on economic position of

entity and further operations effectively.

Implications of under and over absorption: Under and over absorption impacts

negatively on profitability and business operations. It is recognised that actual and expected costs

are not remained same therefore all planning and strategies get affected on decision making and

further business operations. In addition to this, basis of allocation may be incorrect as well there

can be error in data and calculation for costing and income statements (Yang and Hao, 2017).

Thus, these implications are required to be reduced affect further business activities.

SECTION 2 (Nero Ltd)

Part (a) Different planning tools

Budgetary control can be considered as the management of future budgets and plans

which are going to be applied by Nero Ltd company. It works in such a way to compare current

policies to actual helpful policies, to remove defects and work in progressive direction without

making any type of delay. Some tools which helps in Budgetary control system are: -

Cash budget: In this budget process, cash incurred on expenditures are planned for

effective management of all business operations. However, different ideas are generated

for effective cash inflows and outflows for decision making regarding future business

operations. It is helpful for optimum utilization of fund impacts on monetary position of

Nero Ltd as well adequate decisions are made for cash management and allocating fund

appropriately (Akyol, Tuncel and Bayhan, 2015). Therefore, cash budget remains useful

for effective expenditures and increasing sales revenue of the organisation.

Zero based budgeting: - The management of Nero Ltd company can develop budgets on

the basis of Zero based budgeting, which is in this method budgeting is done putting Zero

as base and then analysing the needs and cost budget which is associated in each

function. This provides real figures which helps management to develop future plans

more effectively and eliminates unnecessary actions which promotes saving (El and

Lindefors, 2016). It provides real figures which affects more efficient Judgement, with

assisting in suitable planning. But having all these advantages it has some disadvantages

too such as, It consumes lot of time and the requirement of big amount of funding.

9

Bayhan, 2015). Thus, reconciliation of profit and loss account impacts on economic position of

entity and further operations effectively.

Implications of under and over absorption: Under and over absorption impacts

negatively on profitability and business operations. It is recognised that actual and expected costs

are not remained same therefore all planning and strategies get affected on decision making and

further business operations. In addition to this, basis of allocation may be incorrect as well there

can be error in data and calculation for costing and income statements (Yang and Hao, 2017).

Thus, these implications are required to be reduced affect further business activities.

SECTION 2 (Nero Ltd)

Part (a) Different planning tools

Budgetary control can be considered as the management of future budgets and plans

which are going to be applied by Nero Ltd company. It works in such a way to compare current

policies to actual helpful policies, to remove defects and work in progressive direction without

making any type of delay. Some tools which helps in Budgetary control system are: -

Cash budget: In this budget process, cash incurred on expenditures are planned for

effective management of all business operations. However, different ideas are generated

for effective cash inflows and outflows for decision making regarding future business

operations. It is helpful for optimum utilization of fund impacts on monetary position of

Nero Ltd as well adequate decisions are made for cash management and allocating fund

appropriately (Akyol, Tuncel and Bayhan, 2015). Therefore, cash budget remains useful

for effective expenditures and increasing sales revenue of the organisation.

Zero based budgeting: - The management of Nero Ltd company can develop budgets on

the basis of Zero based budgeting, which is in this method budgeting is done putting Zero

as base and then analysing the needs and cost budget which is associated in each

function. This provides real figures which helps management to develop future plans

more effectively and eliminates unnecessary actions which promotes saving (El and

Lindefors, 2016). It provides real figures which affects more efficient Judgement, with

assisting in suitable planning. But having all these advantages it has some disadvantages

too such as, It consumes lot of time and the requirement of big amount of funding.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.