Management Accounting Systems & Techniques: Nisa Case Study Report

VerifiedAdded on 2020/12/09

|21

|5601

|118

Report

AI Summary

This report provides a comprehensive analysis of management accounting systems and techniques, with a specific focus on their application within the Nisa retail chain. The report begins by defining management accounting and outlining different types of accounting systems, including single and double-entry systems, manual and computerized systems, and cost accounting systems. It then explores various management accounting reports, such as budget reports, accounts receivable aging reports, and job cost reports, highlighting their importance in providing information, aiding in decision-making, and facilitating control. The report also delves into the benefits of accounting systems, such as increased accuracy, automation, and compatibility, while also evaluating the critical aspects of management accounting systems and reporting within Nisa. Furthermore, the report examines absorption costing and marginal costing methods, including the preparation of income statements, and the applicability of the break-even formula. Planning tools for budgetary control are also discussed, including their advantages, disadvantages, and application in preparing, forecasting, and analyzing budgets. Finally, the report analyzes management accounting systems in response to financial problems and evaluates planning tools to solve financial problems, concluding with an overview of management accounting's key aspects.

Management Accounting

Systems & Techniques

Systems & Techniques

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

A. Management accounting and different types of accounting systems................................1

B. Different types of management accounting reports and its importance............................2

C. Benefits of Accounting System.........................................................................................3

D. Critical evaluation of management accounting systems and management accounting

reporting that are integrated in Nisa.......................................................................................5

TASK 2 ...........................................................................................................................................6

A.1. Absorption Costing and Marginal Costing Methods......................................................6

A.2. Production of income statement.....................................................................................7

B. Applicability of formula of break even..............................................................................9

C & D. .................................................................................................................................10

TASK 3..........................................................................................................................................10

A. Advantages and Disadvantages of planning tools for budgetary control........................10

B. Application of the planning tools for preparing, forecasting and analysing budgets......12

C. Management accounting systems to respond to financial problems................................13

D. Analysing management accounting techniques that could respond financial problems. 14

E. Evaluation of planning tools to solve financial problems................................................15

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................18

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

A. Management accounting and different types of accounting systems................................1

B. Different types of management accounting reports and its importance............................2

C. Benefits of Accounting System.........................................................................................3

D. Critical evaluation of management accounting systems and management accounting

reporting that are integrated in Nisa.......................................................................................5

TASK 2 ...........................................................................................................................................6

A.1. Absorption Costing and Marginal Costing Methods......................................................6

A.2. Production of income statement.....................................................................................7

B. Applicability of formula of break even..............................................................................9

C & D. .................................................................................................................................10

TASK 3..........................................................................................................................................10

A. Advantages and Disadvantages of planning tools for budgetary control........................10

B. Application of the planning tools for preparing, forecasting and analysing budgets......12

C. Management accounting systems to respond to financial problems................................13

D. Analysing management accounting techniques that could respond financial problems. 14

E. Evaluation of planning tools to solve financial problems................................................15

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................18

INTRODUCTION

Management Accounting is the process of preparing accounts and management reports

that provide company with timely and accurate information which is required by managers to

make day to day and short term decisions. In the presented report, research and study is being

conducted on the basis of Nisa, a retail chain in UK in retail industry. This assignment contains,

management accounting systems, reports, their benefits and needs, planning tools with their pros

and cons of budgetary control. Practical aspect of the project is fulfilled by income statement,

which was made on the basis of two methods of costing; adsorption and marginal. Further,

break-even point analysis is also done accompanied by application of cash budget with their

interpretation and suggestions. Moreover, this project also contains, comparison between Nisa

and Vectair holdings on the basis of using different financial systems to respond financial

problems. This project is concluded with the brief understanding of management accounting.

TASK 1

A. Management accounting and different types of accounting systems

According to IMA: Management accounting is a type of profession in which it involves,

devising planning, partnering in management decision making and performance management

systems (Schaltegger and Burritt, 2017). Following are different types of management

accounting systems:

Single Entry System: This is the most basic type of accounting system which is

commonly used in small businesses which have simple and few operations. In this there

are no journal entries made to balance accounts so there are high chances of errors.

Double Entry System: This system is more accurate as well as complicated too. This

system guides that each credit entry must be accompanied by an equal debit entry and

vice versa. This make error more visible and accounting process more accurate.

Manual System: This system has no involvement of computer in the whole accounting

process. It is the responsibility of accountant to record all journal entries in all kinds of

journals as well to record their corresponding adjustments and entries. The accountant

must file tax forms, make all calculations, prepare financial statements, etc.

1

Management Accounting is the process of preparing accounts and management reports

that provide company with timely and accurate information which is required by managers to

make day to day and short term decisions. In the presented report, research and study is being

conducted on the basis of Nisa, a retail chain in UK in retail industry. This assignment contains,

management accounting systems, reports, their benefits and needs, planning tools with their pros

and cons of budgetary control. Practical aspect of the project is fulfilled by income statement,

which was made on the basis of two methods of costing; adsorption and marginal. Further,

break-even point analysis is also done accompanied by application of cash budget with their

interpretation and suggestions. Moreover, this project also contains, comparison between Nisa

and Vectair holdings on the basis of using different financial systems to respond financial

problems. This project is concluded with the brief understanding of management accounting.

TASK 1

A. Management accounting and different types of accounting systems

According to IMA: Management accounting is a type of profession in which it involves,

devising planning, partnering in management decision making and performance management

systems (Schaltegger and Burritt, 2017). Following are different types of management

accounting systems:

Single Entry System: This is the most basic type of accounting system which is

commonly used in small businesses which have simple and few operations. In this there

are no journal entries made to balance accounts so there are high chances of errors.

Double Entry System: This system is more accurate as well as complicated too. This

system guides that each credit entry must be accompanied by an equal debit entry and

vice versa. This make error more visible and accounting process more accurate.

Manual System: This system has no involvement of computer in the whole accounting

process. It is the responsibility of accountant to record all journal entries in all kinds of

journals as well to record their corresponding adjustments and entries. The accountant

must file tax forms, make all calculations, prepare financial statements, etc.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Computerized System: It is a use of a computer program to accomplish accounting

functions. This type of accounting with such system can only be done with an accountant

having specialisation in that software.

Cost Accounting System: It is an internal part of an entrepreneur's information system

and refers to the tracking of cost and costs and expenditure are tracked with the help of

allocation system.

Job Costing System: It involves the process of accumulating information about the costs

which is associated with a specific production or job service.

Price Optimisation: To determine response of customers to different prices for its

products and services companies take use of mathematical analysis through different

mediums (Adesina, Ikhu–Omoregbe and Aboaba, 2015). In simple words it is the process

of searching sweet spot of pricing or maximising price against customer's willingness to

pay.

Inventory System: Inventory in every company is the most valuable asset of that

company. These are of two types; perpetual and periodic. In periodic inventory system,

inventory is updated on a monthly or annual basis. Whereas, in perpetual inventory

system inventory is update alternative to a periodic system.

Examples of accounting systems: Manufacturers, Retailers, Distributors, Construction,

Non-profits, etc. Above mentioned accounting systems are used by Nisa to evaluate accounting

transactions.

B. Different types of management accounting reports and its importance

Types of accounting reports are as follows which are used by Nisa in recording their day

to day transactions:

Budget Report: This type of report help Nisa to analyse business performance and

enables managers to analyse their own department's control costs and performance.

Actual expensed from prior years is basically the base on which budget report of the year

is estimated. This reports can further be used by owners and managers in order to provide

employees with incentives.

Accounts Receivable Ageing: It is a tool which is used to manage cash flow in case if

credit to customers in business are expanded. Customers balances are break down with

2

functions. This type of accounting with such system can only be done with an accountant

having specialisation in that software.

Cost Accounting System: It is an internal part of an entrepreneur's information system

and refers to the tracking of cost and costs and expenditure are tracked with the help of

allocation system.

Job Costing System: It involves the process of accumulating information about the costs

which is associated with a specific production or job service.

Price Optimisation: To determine response of customers to different prices for its

products and services companies take use of mathematical analysis through different

mediums (Adesina, Ikhu–Omoregbe and Aboaba, 2015). In simple words it is the process

of searching sweet spot of pricing or maximising price against customer's willingness to

pay.

Inventory System: Inventory in every company is the most valuable asset of that

company. These are of two types; perpetual and periodic. In periodic inventory system,

inventory is updated on a monthly or annual basis. Whereas, in perpetual inventory

system inventory is update alternative to a periodic system.

Examples of accounting systems: Manufacturers, Retailers, Distributors, Construction,

Non-profits, etc. Above mentioned accounting systems are used by Nisa to evaluate accounting

transactions.

B. Different types of management accounting reports and its importance

Types of accounting reports are as follows which are used by Nisa in recording their day

to day transactions:

Budget Report: This type of report help Nisa to analyse business performance and

enables managers to analyse their own department's control costs and performance.

Actual expensed from prior years is basically the base on which budget report of the year

is estimated. This reports can further be used by owners and managers in order to provide

employees with incentives.

Accounts Receivable Ageing: It is a tool which is used to manage cash flow in case if

credit to customers in business are expanded. Customers balances are break down with

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the help of this report. Separate columns for invoices such as; 30 days late, 60 days late

and 90 days late or more are included in most of these ageing reports.

Job Cost Reports: The expenses for a specific report which is financed by Nisa are

shown in this kind of reports. Job's profitability could be evaluated by matching these

reports with estimated revenue (Agu, Nweze and Enekwe, 2016). Nisa was also assisted

in identifying higher earning areas of the business so more emphasis could be given by

company to focus additional efforts where they are needed instead of wasting time and

money on jobs with low profit margins.

Inventory and Manufacturing: Nisa can use managerial accounting reports if it

maintains a physical inventory or produces products.

Importance of Managerial Accounting Reports:

1. Provides Information: It is important as different levels of management are provided

with information.

2. Helps in Selection: It helps in bringing out many alternatives out one profitable

alternative is to be chosen by management.

3. Role in Control System: A management can take over control over organization with

help of this tool.

C. Benefits of Accounting System

Following are some benefits of management accounting system that Nisa experienced

after its implementation:

Accuracy: Nisa experienced that these accounting systems have increased their

efficiency as people make errors and a computerised accounting system minimises those

errors of people. These accounting systems reduces calculation errors, simplify the data

process and accurately account the required information such as general ledger, profit and

loss, balance sheet and tax.

Automation and Productivity: A computerised system eliminate unmanageable and

increases the productivity of Nisa. It is less time consuming as compared to manual

accounting (Ismail, Isa and Mia, 2018). As it was analysed that most of the times

accounting software are more reliable and have better task performance. It is also noticed

that by multiple number of authorised parties information regarding business accounts

could be independently entered into an automated system.

3

and 90 days late or more are included in most of these ageing reports.

Job Cost Reports: The expenses for a specific report which is financed by Nisa are

shown in this kind of reports. Job's profitability could be evaluated by matching these

reports with estimated revenue (Agu, Nweze and Enekwe, 2016). Nisa was also assisted

in identifying higher earning areas of the business so more emphasis could be given by

company to focus additional efforts where they are needed instead of wasting time and

money on jobs with low profit margins.

Inventory and Manufacturing: Nisa can use managerial accounting reports if it

maintains a physical inventory or produces products.

Importance of Managerial Accounting Reports:

1. Provides Information: It is important as different levels of management are provided

with information.

2. Helps in Selection: It helps in bringing out many alternatives out one profitable

alternative is to be chosen by management.

3. Role in Control System: A management can take over control over organization with

help of this tool.

C. Benefits of Accounting System

Following are some benefits of management accounting system that Nisa experienced

after its implementation:

Accuracy: Nisa experienced that these accounting systems have increased their

efficiency as people make errors and a computerised accounting system minimises those

errors of people. These accounting systems reduces calculation errors, simplify the data

process and accurately account the required information such as general ledger, profit and

loss, balance sheet and tax.

Automation and Productivity: A computerised system eliminate unmanageable and

increases the productivity of Nisa. It is less time consuming as compared to manual

accounting (Ismail, Isa and Mia, 2018). As it was analysed that most of the times

accounting software are more reliable and have better task performance. It is also noticed

that by multiple number of authorised parties information regarding business accounts

could be independently entered into an automated system.

3

Compatibility: By implementing computerised accounting system Nisa enabled itself to

share financial information more easily. It is also facilitated that one person can speak to

other if both companies are using same computerised accounting system.

Nisa was benefited by above mentioned all points which reduces the burden of

manual accounting and made it easier to be more connected and share information.

Cost accounting

Advantages Disadvantages

By fixing standard for everything, it

eliminates wastes.

Cost reduction could be achieved by

following new and improved methods

of production.

For price fixation of product, total price

which is available in costing records is

very useful. (Advantages and

Disadvantages of Cost Accounting,

2018).

Company could utilize past

performances which are available in

records but decision is taken on the

basis of future.

Cost is not same every year.

Problems related to work, study, time

and motion are not possible to solve in

costing system.

Job costing

Advantages Disadvantages

Job costing gives separate identity to

earned profit from each job.

Estimation could be taken on the basis

of past records of cost of job in job

costing. (Advantages and

Disadvantages of Job Costing, 2018).

In job costing the is no standardization

of job.

There are fewer chances of controlling

costs since only after incurring the

expenses in job costing the controlling

steps are taken.

Inventory system

Advantages Disadvantages

Reduction in Costs: Software can also Price: A lot of small and medium sized

4

share financial information more easily. It is also facilitated that one person can speak to

other if both companies are using same computerised accounting system.

Nisa was benefited by above mentioned all points which reduces the burden of

manual accounting and made it easier to be more connected and share information.

Cost accounting

Advantages Disadvantages

By fixing standard for everything, it

eliminates wastes.

Cost reduction could be achieved by

following new and improved methods

of production.

For price fixation of product, total price

which is available in costing records is

very useful. (Advantages and

Disadvantages of Cost Accounting,

2018).

Company could utilize past

performances which are available in

records but decision is taken on the

basis of future.

Cost is not same every year.

Problems related to work, study, time

and motion are not possible to solve in

costing system.

Job costing

Advantages Disadvantages

Job costing gives separate identity to

earned profit from each job.

Estimation could be taken on the basis

of past records of cost of job in job

costing. (Advantages and

Disadvantages of Job Costing, 2018).

In job costing the is no standardization

of job.

There are fewer chances of controlling

costs since only after incurring the

expenses in job costing the controlling

steps are taken.

Inventory system

Advantages Disadvantages

Reduction in Costs: Software can also Price: A lot of small and medium sized

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

help in avoiding lost sales as companies

have materials need on time.

High Efficiency: By using this system

business efficiency could be increased

and can lead to maximum productivity.

businesses are not able afford these

systems.

Complexity: Inventory management

software simplifies daily business

operations and make work easier, but it

is a quite a complicated tool.

Price optimization system

Advantages Disadvantages

Due to automation there is possibility

of large scale unemployment in

different market sectors. (The

advantages and disadvantages of the

price system, 2018).

Both good and bad products could be

sold side by side.

It enables consumers to decide what

they want to buy.

It allocates resources efficiency.

D. Critical evaluation of management accounting systems and management accounting reporting

that are integrated in Nisa

Management Accounting Reporting plays vital role in Nisa as it helps in supporting,

controlling, decision making and planning. Management accounting systems and reporting

integrates in each and every level of management in Nisa as all the information which are related

to the company whether they are financial or not, they are related to internal environment of Nisa

or external environment of it. Management Accounting System helps Nisa in tracking cost and

expenditure that involves in manufacturing processes and product sale, it also assists firm in

accumulating information about the costs which is associated with a specific production or job

service (Khan, 2015). These accounting systems have made it easier for Nisa to conduct day to

day business activities in effective manner.

Management Accounting Reports enabled Nisa to analyse business performance and to

estimate yearly budgets. It has also helped Nisa to evaluate job profitability and in identifying

higher earning areas of the business. By implementing accounting reports Nisa was able to make

5

have materials need on time.

High Efficiency: By using this system

business efficiency could be increased

and can lead to maximum productivity.

businesses are not able afford these

systems.

Complexity: Inventory management

software simplifies daily business

operations and make work easier, but it

is a quite a complicated tool.

Price optimization system

Advantages Disadvantages

Due to automation there is possibility

of large scale unemployment in

different market sectors. (The

advantages and disadvantages of the

price system, 2018).

Both good and bad products could be

sold side by side.

It enables consumers to decide what

they want to buy.

It allocates resources efficiency.

D. Critical evaluation of management accounting systems and management accounting reporting

that are integrated in Nisa

Management Accounting Reporting plays vital role in Nisa as it helps in supporting,

controlling, decision making and planning. Management accounting systems and reporting

integrates in each and every level of management in Nisa as all the information which are related

to the company whether they are financial or not, they are related to internal environment of Nisa

or external environment of it. Management Accounting System helps Nisa in tracking cost and

expenditure that involves in manufacturing processes and product sale, it also assists firm in

accumulating information about the costs which is associated with a specific production or job

service (Khan, 2015). These accounting systems have made it easier for Nisa to conduct day to

day business activities in effective manner.

Management Accounting Reports enabled Nisa to analyse business performance and to

estimate yearly budgets. It has also helped Nisa to evaluate job profitability and in identifying

higher earning areas of the business. By implementing accounting reports Nisa was able to make

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

manufacturing processes more efficient and saved time and money from jobs with low profit

margins. Management Accounting Reports helped Nisa in providing information to various

levels of management, helped in bringing out many alternatives out of which management could

choose one which is most profitable and assist in taking control over management.

However, there are some criticism on management accounting system as both financial

and cost accounting information are used in the management accounting system. The accuracy is

dependent on the accuracy of financial and cost record and these records determine weaknesses

and strengths of management accounting. So, it would require by Nisa to maintain accuracy of

these records in order to maintain management accounting systems. Personal prejudices and bias

of an individual can also affect the objectivity and effectiveness of the conclusions and

recommendations. These systems will only be providing Nisa with data to solve the problem

before the management.

TASK 2

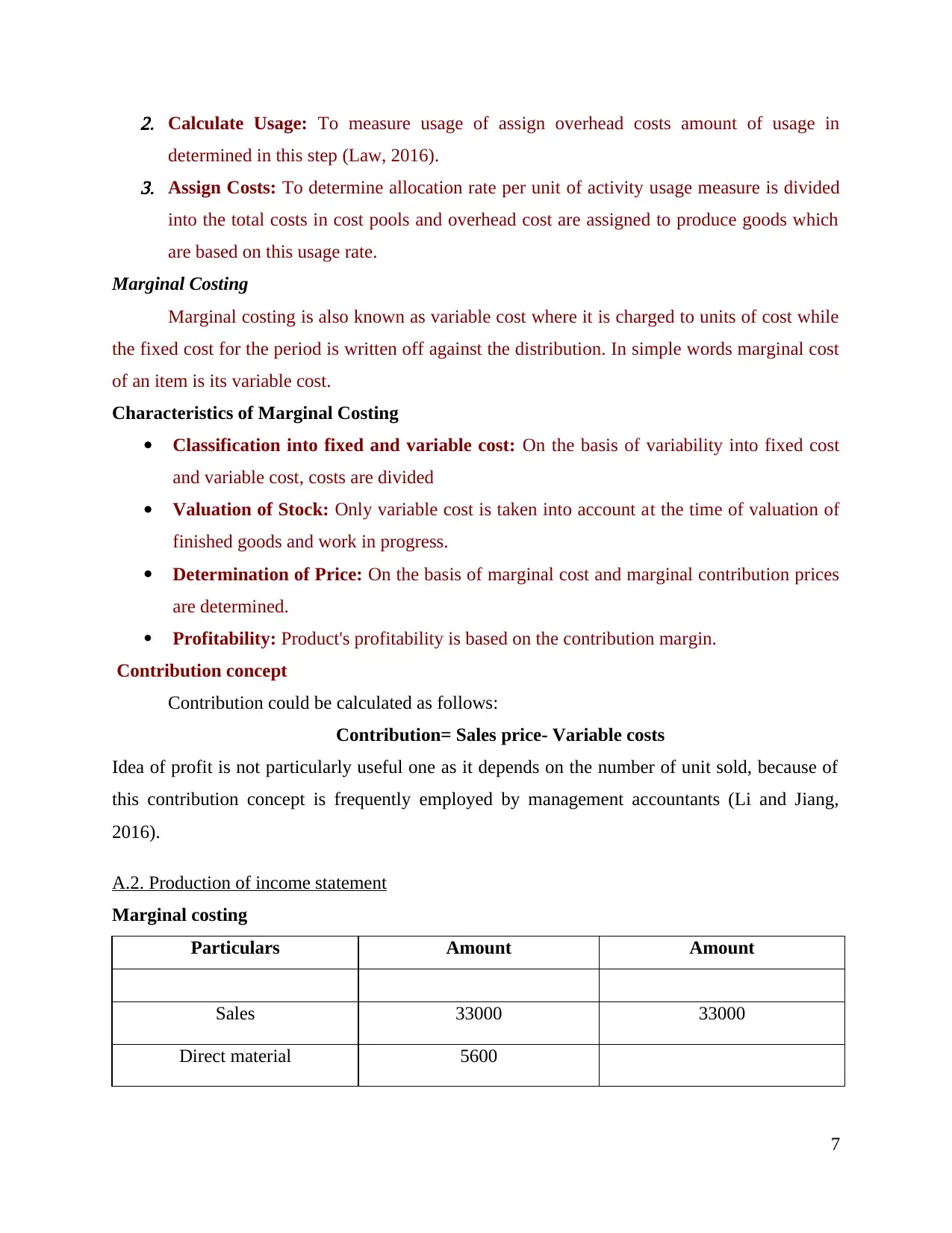

A.1. Absorption Costing and Marginal Costing Methods

Absorption Costing

Absorption Costing is a method of cost accounting in which all cost associated with

manufacturing a particular product is expended and is significantly required for all GAAP to

create an inventory valuation that are stated in balance sheet of Nisa.

Components of absorption costing Direct Materials: These are those materials which are enclosed within finished product. Direct Labour: Manufacturing a product needs costs for labour, these are those labour

costs. Variable manufacturing overhead: Costs which may vary with change in production

volume of operating manufacturing facility. Fixed manufacturing overhead: Costs which do not vary with change in production

volume of operating manufacturing facility.

Absorption Costing Steps1. Assigning costs to cost pools: This step consists of cost pools that includes standard set

of accounts which are changed rarely.

6

margins. Management Accounting Reports helped Nisa in providing information to various

levels of management, helped in bringing out many alternatives out of which management could

choose one which is most profitable and assist in taking control over management.

However, there are some criticism on management accounting system as both financial

and cost accounting information are used in the management accounting system. The accuracy is

dependent on the accuracy of financial and cost record and these records determine weaknesses

and strengths of management accounting. So, it would require by Nisa to maintain accuracy of

these records in order to maintain management accounting systems. Personal prejudices and bias

of an individual can also affect the objectivity and effectiveness of the conclusions and

recommendations. These systems will only be providing Nisa with data to solve the problem

before the management.

TASK 2

A.1. Absorption Costing and Marginal Costing Methods

Absorption Costing

Absorption Costing is a method of cost accounting in which all cost associated with

manufacturing a particular product is expended and is significantly required for all GAAP to

create an inventory valuation that are stated in balance sheet of Nisa.

Components of absorption costing Direct Materials: These are those materials which are enclosed within finished product. Direct Labour: Manufacturing a product needs costs for labour, these are those labour

costs. Variable manufacturing overhead: Costs which may vary with change in production

volume of operating manufacturing facility. Fixed manufacturing overhead: Costs which do not vary with change in production

volume of operating manufacturing facility.

Absorption Costing Steps1. Assigning costs to cost pools: This step consists of cost pools that includes standard set

of accounts which are changed rarely.

6

2. Calculate Usage: To measure usage of assign overhead costs amount of usage in

determined in this step (Law, 2016).3. Assign Costs: To determine allocation rate per unit of activity usage measure is divided

into the total costs in cost pools and overhead cost are assigned to produce goods which

are based on this usage rate.

Marginal Costing

Marginal costing is also known as variable cost where it is charged to units of cost while

the fixed cost for the period is written off against the distribution. In simple words marginal cost

of an item is its variable cost.

Characteristics of Marginal Costing

Classification into fixed and variable cost: On the basis of variability into fixed cost

and variable cost, costs are divided

Valuation of Stock: Only variable cost is taken into account at the time of valuation of

finished goods and work in progress.

Determination of Price: On the basis of marginal cost and marginal contribution prices

are determined.

Profitability: Product's profitability is based on the contribution margin.

Contribution concept

Contribution could be calculated as follows:

Contribution= Sales price- Variable costs

Idea of profit is not particularly useful one as it depends on the number of unit sold, because of

this contribution concept is frequently employed by management accountants (Li and Jiang,

2016).

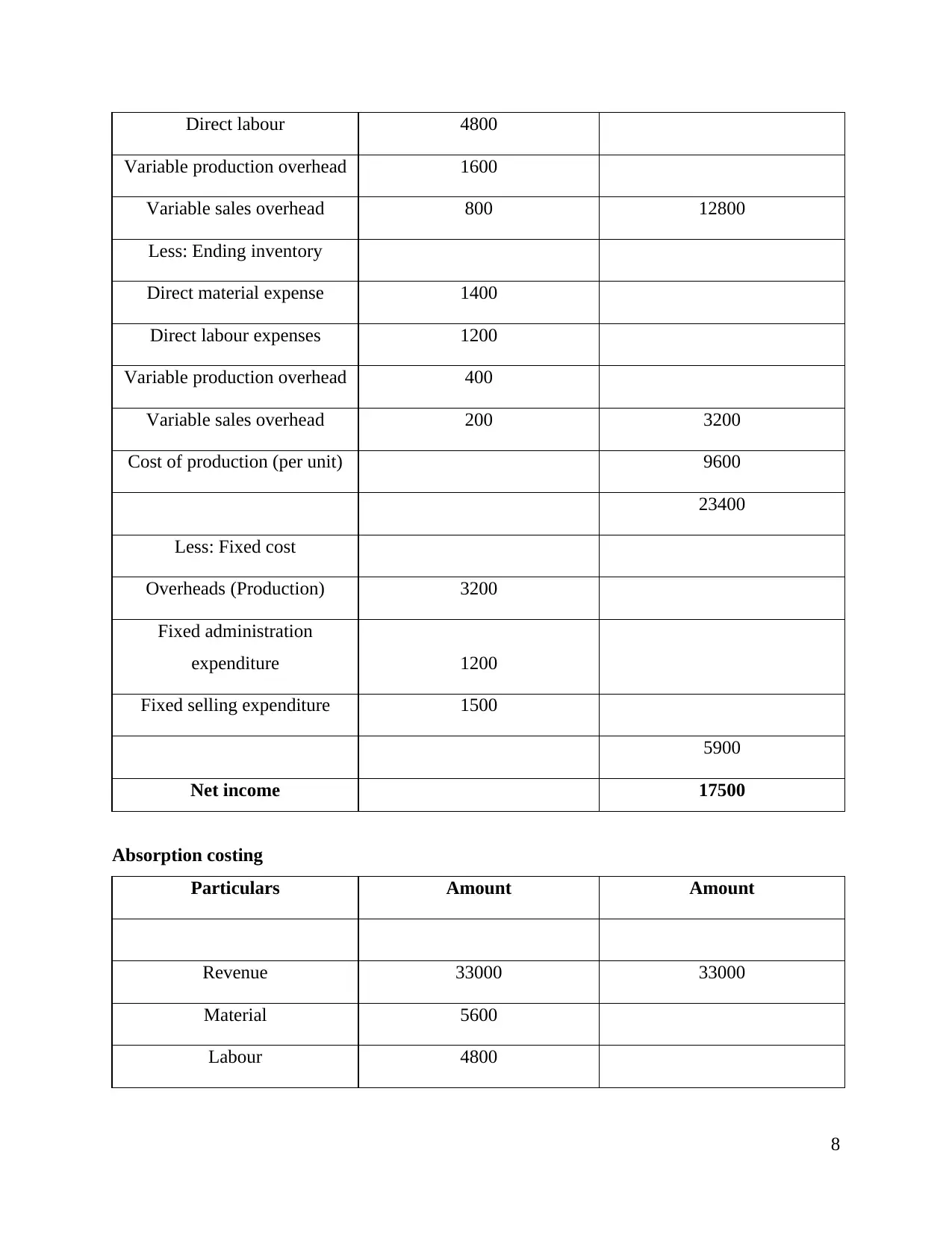

A.2. Production of income statement

Marginal costing

Particulars Amount Amount

Sales 33000 33000

Direct material 5600

7

determined in this step (Law, 2016).3. Assign Costs: To determine allocation rate per unit of activity usage measure is divided

into the total costs in cost pools and overhead cost are assigned to produce goods which

are based on this usage rate.

Marginal Costing

Marginal costing is also known as variable cost where it is charged to units of cost while

the fixed cost for the period is written off against the distribution. In simple words marginal cost

of an item is its variable cost.

Characteristics of Marginal Costing

Classification into fixed and variable cost: On the basis of variability into fixed cost

and variable cost, costs are divided

Valuation of Stock: Only variable cost is taken into account at the time of valuation of

finished goods and work in progress.

Determination of Price: On the basis of marginal cost and marginal contribution prices

are determined.

Profitability: Product's profitability is based on the contribution margin.

Contribution concept

Contribution could be calculated as follows:

Contribution= Sales price- Variable costs

Idea of profit is not particularly useful one as it depends on the number of unit sold, because of

this contribution concept is frequently employed by management accountants (Li and Jiang,

2016).

A.2. Production of income statement

Marginal costing

Particulars Amount Amount

Sales 33000 33000

Direct material 5600

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Direct labour 4800

Variable production overhead 1600

Variable sales overhead 800 12800

Less: Ending inventory

Direct material expense 1400

Direct labour expenses 1200

Variable production overhead 400

Variable sales overhead 200 3200

Cost of production (per unit) 9600

23400

Less: Fixed cost

Overheads (Production) 3200

Fixed administration

expenditure 1200

Fixed selling expenditure 1500

5900

Net income 17500

Absorption costing

Particulars Amount Amount

Revenue 33000 33000

Material 5600

Labour 4800

8

Variable production overhead 1600

Variable sales overhead 800 12800

Less: Ending inventory

Direct material expense 1400

Direct labour expenses 1200

Variable production overhead 400

Variable sales overhead 200 3200

Cost of production (per unit) 9600

23400

Less: Fixed cost

Overheads (Production) 3200

Fixed administration

expenditure 1200

Fixed selling expenditure 1500

5900

Net income 17500

Absorption costing

Particulars Amount Amount

Revenue 33000 33000

Material 5600

Labour 4800

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

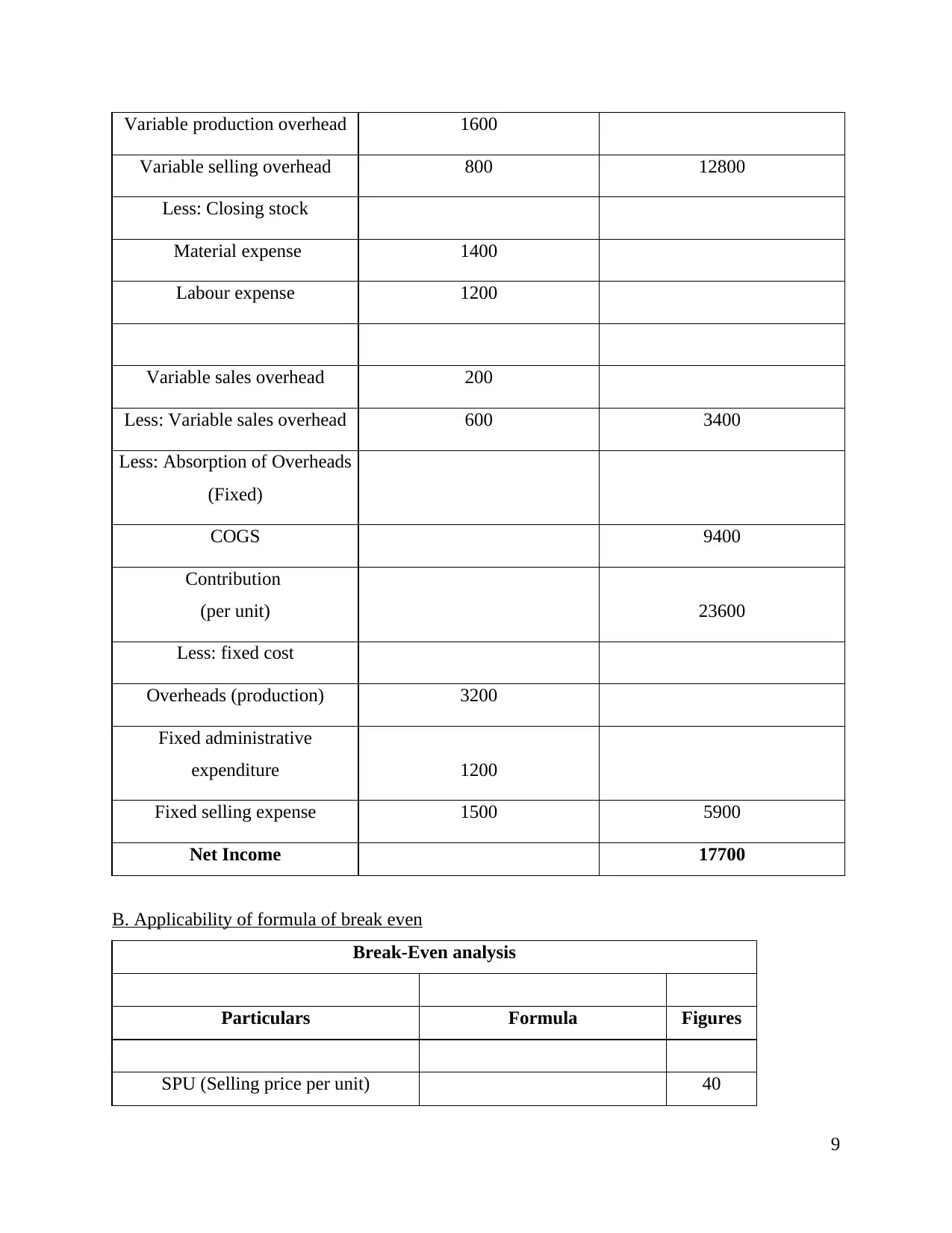

Variable production overhead 1600

Variable selling overhead 800 12800

Less: Closing stock

Material expense 1400

Labour expense 1200

Variable sales overhead 200

Less: Variable sales overhead 600 3400

Less: Absorption of Overheads

(Fixed)

COGS 9400

Contribution

(per unit) 23600

Less: fixed cost

Overheads (production) 3200

Fixed administrative

expenditure 1200

Fixed selling expense 1500 5900

Net Income 17700

B. Applicability of formula of break even

Break-Even analysis

Particulars Formula Figures

SPU (Selling price per unit) 40

9

Variable selling overhead 800 12800

Less: Closing stock

Material expense 1400

Labour expense 1200

Variable sales overhead 200

Less: Variable sales overhead 600 3400

Less: Absorption of Overheads

(Fixed)

COGS 9400

Contribution

(per unit) 23600

Less: fixed cost

Overheads (production) 3200

Fixed administrative

expenditure 1200

Fixed selling expense 1500 5900

Net Income 17700

B. Applicability of formula of break even

Break-Even analysis

Particulars Formula Figures

SPU (Selling price per unit) 40

9

Variable cost (per unit) 13

Contribution (per unit) SPU - variable cost per unit 27

Fixed cost 6000

BEP (in units) Fixed cost / CPU 222

BEP (in value or monetary terms) BEP in units * SPU 8888.89

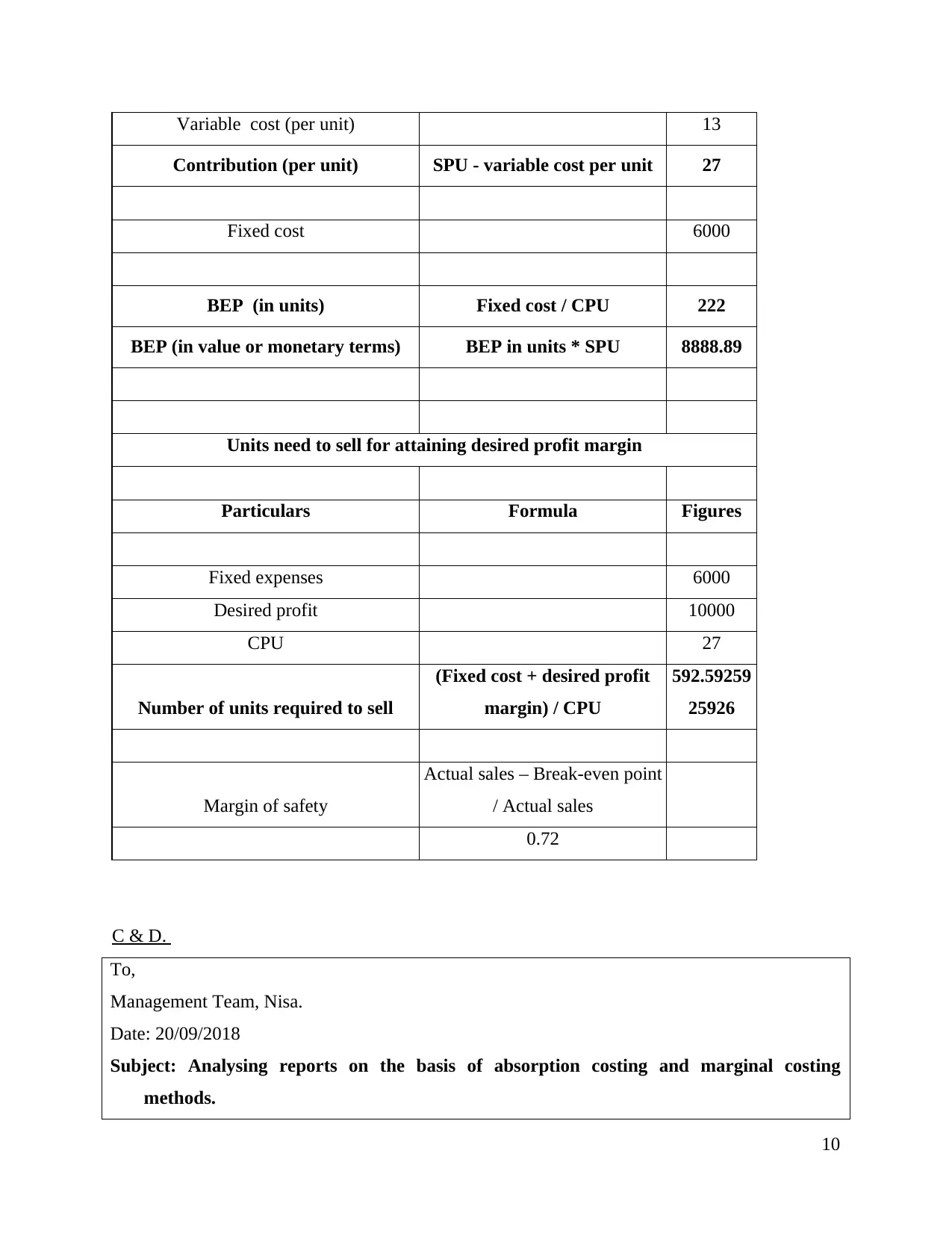

Units need to sell for attaining desired profit margin

Particulars Formula Figures

Fixed expenses 6000

Desired profit 10000

CPU 27

Number of units required to sell

(Fixed cost + desired profit

margin) / CPU

592.59259

25926

Margin of safety

Actual sales – Break-even point

/ Actual sales

0.72

C & D.

To,

Management Team, Nisa.

Date: 20/09/2018

Subject: Analysing reports on the basis of absorption costing and marginal costing

methods.

10

Contribution (per unit) SPU - variable cost per unit 27

Fixed cost 6000

BEP (in units) Fixed cost / CPU 222

BEP (in value or monetary terms) BEP in units * SPU 8888.89

Units need to sell for attaining desired profit margin

Particulars Formula Figures

Fixed expenses 6000

Desired profit 10000

CPU 27

Number of units required to sell

(Fixed cost + desired profit

margin) / CPU

592.59259

25926

Margin of safety

Actual sales – Break-even point

/ Actual sales

0.72

C & D.

To,

Management Team, Nisa.

Date: 20/09/2018

Subject: Analysing reports on the basis of absorption costing and marginal costing

methods.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.