Management Accounting Report: Strategies for Nisa Ltd's Growth

VerifiedAdded on 2020/01/16

|20

|5916

|167

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles and their application to Nisa Ltd, a small-scale UK retail business. It explores essential requirements of management accounting systems, including job order, processing, and throughput costing, highlighting their role in price determination and operational efficiency. The report delves into various management accounting reporting methods, such as cost accounting reports, budgeting reports, cost variance analysis, and price optimization reports, emphasizing their significance in analyzing business performance and supporting strategic decision-making. Different costing methods, including marginal and absorption costing, are compared and contrasted, with illustrative examples demonstrating their impact on financial statements. The report also examines the merits and demerits of planning tools used for budgetary control, as well as various management accounting systems that can improve the financial position of the firm. The report concludes by emphasizing the importance of management accounting tools for effective business management and expansion, offering valuable insights for small-scale enterprises seeking to enhance their operational and financial strategies.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1) Management accounting and essential requirements of its different systems......................1

P2) Various methods applied for management accounting reporting.........................................3

TASK 2............................................................................................................................................5

P3) Different costing and their differences.................................................................................5

TASK 3............................................................................................................................................8

P4) Merits and demerits of planning tools used for budgetary control.......................................8

P5) Management accounting systems.......................................................................................11

CONCLUSION..............................................................................................................................14

REFERENCE.................................................................................................................................16

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1) Management accounting and essential requirements of its different systems......................1

P2) Various methods applied for management accounting reporting.........................................3

TASK 2............................................................................................................................................5

P3) Different costing and their differences.................................................................................5

TASK 3............................................................................................................................................8

P4) Merits and demerits of planning tools used for budgetary control.......................................8

P5) Management accounting systems.......................................................................................11

CONCLUSION..............................................................................................................................14

REFERENCE.................................................................................................................................16

INDEX OF TABLES

Table 1: Marginal costing vs. Absorption costing...........................................................................8

Table 1: Marginal costing vs. Absorption costing...........................................................................8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ILLUSTRATION INDEX

Illustration 1: Income statement through marginal costing.............................................................6

Illustration 2: Income statement through absorption costing...........................................................7

Illustration 1: Income statement through marginal costing.............................................................6

Illustration 2: Income statement through absorption costing...........................................................7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION

Management accounting is key component for systematic management of business

operations. In this regard, several accounting systems are included such as financial, cost,

inventory and performance of entity. The present report is based on understanding different

aspects of management accounting tools for expansion of Nisa Ltd. It is small scale retail sector

organization of UK that provides grocery and food items' services. In addition to this,

management accounting tools and systems for increasing quality services of entity can be

understood. However, costing methods to determine price as well presenting financial position of

organization is to express. Moreover, through this assignment, advantages and limitations of

budgetary control tools are to introduced. Apart from this, various management accounting

systems to solving out financial position of firm can be described. Thus, learners are able to

understand significant role of management accounting and its tools for effectiveness of small

scale enterprise.

TASK 1

P1) Management accounting and essential requirements of its different systems

To

General manager

Nisa Ltd

It is essential for Nisa Ltd to expand its business and effective financial management to

carrying out organization effectively. Therefore, proper planning and decision making is

required for operations of business entity. In this regard, management accountant of entity plays

crucial role by price determination and preparing strategies for further implementation (Anwar

and et.al., 2016). However, organization can enhance its efficiency by focusing on different

elements such as costing, budgeting, variance analysis and so on. Therefore, actual business

performance is recognized on the basis of which innovative ideas are generated related to entire

operations of business organization. In this regard, strategic and risk management for firm is

gained to run entity efficiently. Thus, overall organizational functions of small scale enterprise

get managed systematically. However, management accountant of entity analysis current

bruises performance through income statement and other financial statement analysis that leads

1

Management accounting is key component for systematic management of business

operations. In this regard, several accounting systems are included such as financial, cost,

inventory and performance of entity. The present report is based on understanding different

aspects of management accounting tools for expansion of Nisa Ltd. It is small scale retail sector

organization of UK that provides grocery and food items' services. In addition to this,

management accounting tools and systems for increasing quality services of entity can be

understood. However, costing methods to determine price as well presenting financial position of

organization is to express. Moreover, through this assignment, advantages and limitations of

budgetary control tools are to introduced. Apart from this, various management accounting

systems to solving out financial position of firm can be described. Thus, learners are able to

understand significant role of management accounting and its tools for effectiveness of small

scale enterprise.

TASK 1

P1) Management accounting and essential requirements of its different systems

To

General manager

Nisa Ltd

It is essential for Nisa Ltd to expand its business and effective financial management to

carrying out organization effectively. Therefore, proper planning and decision making is

required for operations of business entity. In this regard, management accountant of entity plays

crucial role by price determination and preparing strategies for further implementation (Anwar

and et.al., 2016). However, organization can enhance its efficiency by focusing on different

elements such as costing, budgeting, variance analysis and so on. Therefore, actual business

performance is recognized on the basis of which innovative ideas are generated related to entire

operations of business organization. In this regard, strategic and risk management for firm is

gained to run entity efficiently. Thus, overall organizational functions of small scale enterprise

get managed systematically. However, management accountant of entity analysis current

bruises performance through income statement and other financial statement analysis that leads

1

to prepare budget related to preparing budget to gain effectiveness of small scale enterprise.

In this process, costing is benefited for price determination and reporting income

statement to create balance of production and distribution of goods as much increasing its

productivity and profitability at high level. In accordance to this, inventory management and

enhancement of Nisa Ltd can be achieved through this system (Armitage and Webb, 2013). For

increasing efficiency and varieties of tools related to financial and other sectors' growth in

systematic manner. Along with this, management accountant of organization prepares budget

for further business operations as well remains helpful for enlargement of entity with increasing

service qualities of business organization. Thus, management accounting and its tools are

essential to achieve entity's effectiveness through systematic planning procedure and decision

making process.

Essential requirements of different management accounting tools:- Some

management accounting tools such as; job order, processing and throughput costing are

involved in management accounting tools that is useful for effective price determination and

further business operations to increasing efficiency of small scale enterprise (Management

Accounting, 2016). Some important man accounting tools can be described as follows:- Job order costing:- Under this costing method, expenses incurred on manufacturing of

products are analysed. It includes raw material price and costing for creating products.

In this process, management accountant of Nisa Ltd analysis expenses on producing and

manufacturing process. Therefore, it is input process of organization to setting up prices

for providing goods and services to customers (Berman, 2015). Hence, job order

costing is considered as basis for deciding price of product related to expansion of small

business unit and increasing service qualities of firm efficiently. Processing costing:- It is next further process for price determination of product under

which management accountant of Nisa Ltd focuses on production and processing tool.

Under this system, quality used in product making are also obtained for setting price.

Therefore, on the basis of quality used in production process, cost of finished goods is

determined. Including this, processing costing proceed to deciding price for goods

obtained for outcome (Bucci, 2014). In this regard, several ideas are generated for

production and distribution of products services to gain effectiveness of small scale

2

In this process, costing is benefited for price determination and reporting income

statement to create balance of production and distribution of goods as much increasing its

productivity and profitability at high level. In accordance to this, inventory management and

enhancement of Nisa Ltd can be achieved through this system (Armitage and Webb, 2013). For

increasing efficiency and varieties of tools related to financial and other sectors' growth in

systematic manner. Along with this, management accountant of organization prepares budget

for further business operations as well remains helpful for enlargement of entity with increasing

service qualities of business organization. Thus, management accounting and its tools are

essential to achieve entity's effectiveness through systematic planning procedure and decision

making process.

Essential requirements of different management accounting tools:- Some

management accounting tools such as; job order, processing and throughput costing are

involved in management accounting tools that is useful for effective price determination and

further business operations to increasing efficiency of small scale enterprise (Management

Accounting, 2016). Some important man accounting tools can be described as follows:- Job order costing:- Under this costing method, expenses incurred on manufacturing of

products are analysed. It includes raw material price and costing for creating products.

In this process, management accountant of Nisa Ltd analysis expenses on producing and

manufacturing process. Therefore, it is input process of organization to setting up prices

for providing goods and services to customers (Berman, 2015). Hence, job order

costing is considered as basis for deciding price of product related to expansion of small

business unit and increasing service qualities of firm efficiently. Processing costing:- It is next further process for price determination of product under

which management accountant of Nisa Ltd focuses on production and processing tool.

Under this system, quality used in product making are also obtained for setting price.

Therefore, on the basis of quality used in production process, cost of finished goods is

determined. Including this, processing costing proceed to deciding price for goods

obtained for outcome (Bucci, 2014). In this regard, several ideas are generated for

production and distribution of products services to gain effectiveness of small scale

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

enterprise. Therefore, as per processing costing, different determinants are gained for

systematic management of products systematically.

Throughput costing:- It includes cost incurred on advertisement and developing product

in market. Therefore, it is related with output and costing for finished goods. On the

basis of expenses incurred in manufacturing, processing, production and launching

products in market, this costing is determined. Hence, actual revenue gained and profit

earning capacity of Nisa Ltd is gained through this process system. In this regard,

several tools and techniques are used for promoting products in market that impacts on

company’s market value and its efficiency to face competition (Burke, Corman and

Story, 2016). Thus, accurate price determination is done through applying throughput

costing that presents income statement and financial performance of organization to

provide affordable products to customers efficiently.

P2) Various methods applied for management accounting reporting

To

General manager

Nisa Ltd

There are several methods of management accounting which are used for reporting

relating to analyse business performance of Nisa Ltd. In this system, cost effectiveness, balance

of production and distribution of products, performance of business organization is created.

However, reports are prepared on the basis of current business activities that generates various

ideas for implementation in future time (Kreibich and et.al., 2014). Therefore, different reports

to be prepared and maintained for management accounting reporting are as follows:-

Cost accounting reports:- It is key component for analysing actual production and

distribution system of organization linked with financial position of Nisa Ltd. Therefore, by

using this tool, systematic approach is generated for increasing profitability and expansion of

entity at maximum level. In accordance to this, management accountant of small scale

enterprise prepares this report and further makes decision for further business operations. It is

helpful for optimum allocation of resources analysing management accounting report. Hence,

3

systematic management of products systematically.

Throughput costing:- It includes cost incurred on advertisement and developing product

in market. Therefore, it is related with output and costing for finished goods. On the

basis of expenses incurred in manufacturing, processing, production and launching

products in market, this costing is determined. Hence, actual revenue gained and profit

earning capacity of Nisa Ltd is gained through this process system. In this regard,

several tools and techniques are used for promoting products in market that impacts on

company’s market value and its efficiency to face competition (Burke, Corman and

Story, 2016). Thus, accurate price determination is done through applying throughput

costing that presents income statement and financial performance of organization to

provide affordable products to customers efficiently.

P2) Various methods applied for management accounting reporting

To

General manager

Nisa Ltd

There are several methods of management accounting which are used for reporting

relating to analyse business performance of Nisa Ltd. In this system, cost effectiveness, balance

of production and distribution of products, performance of business organization is created.

However, reports are prepared on the basis of current business activities that generates various

ideas for implementation in future time (Kreibich and et.al., 2014). Therefore, different reports

to be prepared and maintained for management accounting reporting are as follows:-

Cost accounting reports:- It is key component for analysing actual production and

distribution system of organization linked with financial position of Nisa Ltd. Therefore, by

using this tool, systematic approach is generated for increasing profitability and expansion of

entity at maximum level. In accordance to this, management accountant of small scale

enterprise prepares this report and further makes decision for further business operations. It is

helpful for optimum allocation of resources analysing management accounting report. Hence,

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

cost accounting system is considered as one of the great component for recognizing profit

earning capacity of firm to increase its business and competitive strategies for expansion of

small business entity and enhancing service qualities at maximum level (Lavia and Hiebl,

2014).

Budgeting report:- Management accounting tool as budgeting is related to forecasting

and decision making for implementing further business operations. Under this system,

management accountant of Nisa Ltd analyses all business operations and prepares budgetary

report to present organisation's performance. Further, as per current position of entity, budget is

prepared and strategic plans to made for in further years' operations systematically. Thus,

control over excess of production and wastage of raw materials is managed through this

process. It is determined that budgeting report is one of the great tool for reducing risk occur at

workplace (McLaughlin and et.al., 2014). Similarly, various tools and techniques are obtained

for further business operations at high level. It is a systematic reporting process that remains

helpful to gain optimum allocation of resources and fund. Thus, management of entire business

activities is gained through this system procedure.

Cost variance analysis report:- It is related to cost effectiveness which remains helpful

for sustaining product value in market at maximum level. Through this reporting, differences

between standard and actual cost is recognised and further planning procedure is implemented

for further years’ business operations. However, it affects productivity and profitability of firm

to increase its business and competitive strategies at large scale (Moriarty and et.al., 2015). It is

obtained that cost variance analysis report is beneficial for analysing cost incurred on business

operation as well several ideas are generated for enlargement of small business unit adequately.

Therefore, systematic management of all business operations can achieve through this reporting.

Thus, management accounting tool as cost variance analysis is able to understand comparison

between standard and actual price for production and distribution of services provided by entity

at high level.

Price optimizing report: It is one of the great management accounting reporting that is

suitable for optimizing price on expenditures of operations for Nisa Ltd. However, effective

cost can be utilized for creating balance between production and distribution system for

producing services. In addition to this, several ideas are generated for further business

operations. Moreover, preparing and maintaining report related to pricing optimizing is

4

earning capacity of firm to increase its business and competitive strategies for expansion of

small business entity and enhancing service qualities at maximum level (Lavia and Hiebl,

2014).

Budgeting report:- Management accounting tool as budgeting is related to forecasting

and decision making for implementing further business operations. Under this system,

management accountant of Nisa Ltd analyses all business operations and prepares budgetary

report to present organisation's performance. Further, as per current position of entity, budget is

prepared and strategic plans to made for in further years' operations systematically. Thus,

control over excess of production and wastage of raw materials is managed through this

process. It is determined that budgeting report is one of the great tool for reducing risk occur at

workplace (McLaughlin and et.al., 2014). Similarly, various tools and techniques are obtained

for further business operations at high level. It is a systematic reporting process that remains

helpful to gain optimum allocation of resources and fund. Thus, management of entire business

activities is gained through this system procedure.

Cost variance analysis report:- It is related to cost effectiveness which remains helpful

for sustaining product value in market at maximum level. Through this reporting, differences

between standard and actual cost is recognised and further planning procedure is implemented

for further years’ business operations. However, it affects productivity and profitability of firm

to increase its business and competitive strategies at large scale (Moriarty and et.al., 2015). It is

obtained that cost variance analysis report is beneficial for analysing cost incurred on business

operation as well several ideas are generated for enlargement of small business unit adequately.

Therefore, systematic management of all business operations can achieve through this reporting.

Thus, management accounting tool as cost variance analysis is able to understand comparison

between standard and actual price for production and distribution of services provided by entity

at high level.

Price optimizing report: It is one of the great management accounting reporting that is

suitable for optimizing price on expenditures of operations for Nisa Ltd. However, effective

cost can be utilized for creating balance between production and distribution system for

producing services. In addition to this, several ideas are generated for further business

operations. Moreover, preparing and maintaining report related to pricing optimizing is

4

benefited for organisation to create innovation efficiently.

TASK 2

P3) Different costing and their differences

Managing Director

Nisa Ltd

Costing: It is one of the most essential tool of management accounting for price

determination of products. Under this process, proper report is prepared for reporting expenses

incurred for manufacturing and production process. Including this, income earned is also

determined as per which, different ideas are created for deciding cost of goods (Nishizaki,

Matoba and Nitta, 2014). In this regard, costing is considered as a technique to gain cost

effectiveness as well increasing in demand for product that impacts on productivity and

profitability of firm effectively. There are several costing methods applied such as; marginal

and absorption. Their description can be expressed as below:-

Marginal costing:- Under this costing method, for measuring net profit margin, gross

profit is deducted to variable cost of goods only. Therefore, it is suitable for short decision

making process due to profit variation. In accordance to this, marginal costing is benefited for

deciding pricing and cost effectiveness tools for further business operations (Sugimoto and

et.al., 2015). Thus, marginal costing is interrelated with decision making tool for effectiveness

of small business unit to increase its efficiency in market.

5

TASK 2

P3) Different costing and their differences

Managing Director

Nisa Ltd

Costing: It is one of the most essential tool of management accounting for price

determination of products. Under this process, proper report is prepared for reporting expenses

incurred for manufacturing and production process. Including this, income earned is also

determined as per which, different ideas are created for deciding cost of goods (Nishizaki,

Matoba and Nitta, 2014). In this regard, costing is considered as a technique to gain cost

effectiveness as well increasing in demand for product that impacts on productivity and

profitability of firm effectively. There are several costing methods applied such as; marginal

and absorption. Their description can be expressed as below:-

Marginal costing:- Under this costing method, for measuring net profit margin, gross

profit is deducted to variable cost of goods only. Therefore, it is suitable for short decision

making process due to profit variation. In accordance to this, marginal costing is benefited for

deciding pricing and cost effectiveness tools for further business operations (Sugimoto and

et.al., 2015). Thus, marginal costing is interrelated with decision making tool for effectiveness

of small business unit to increase its efficiency in market.

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

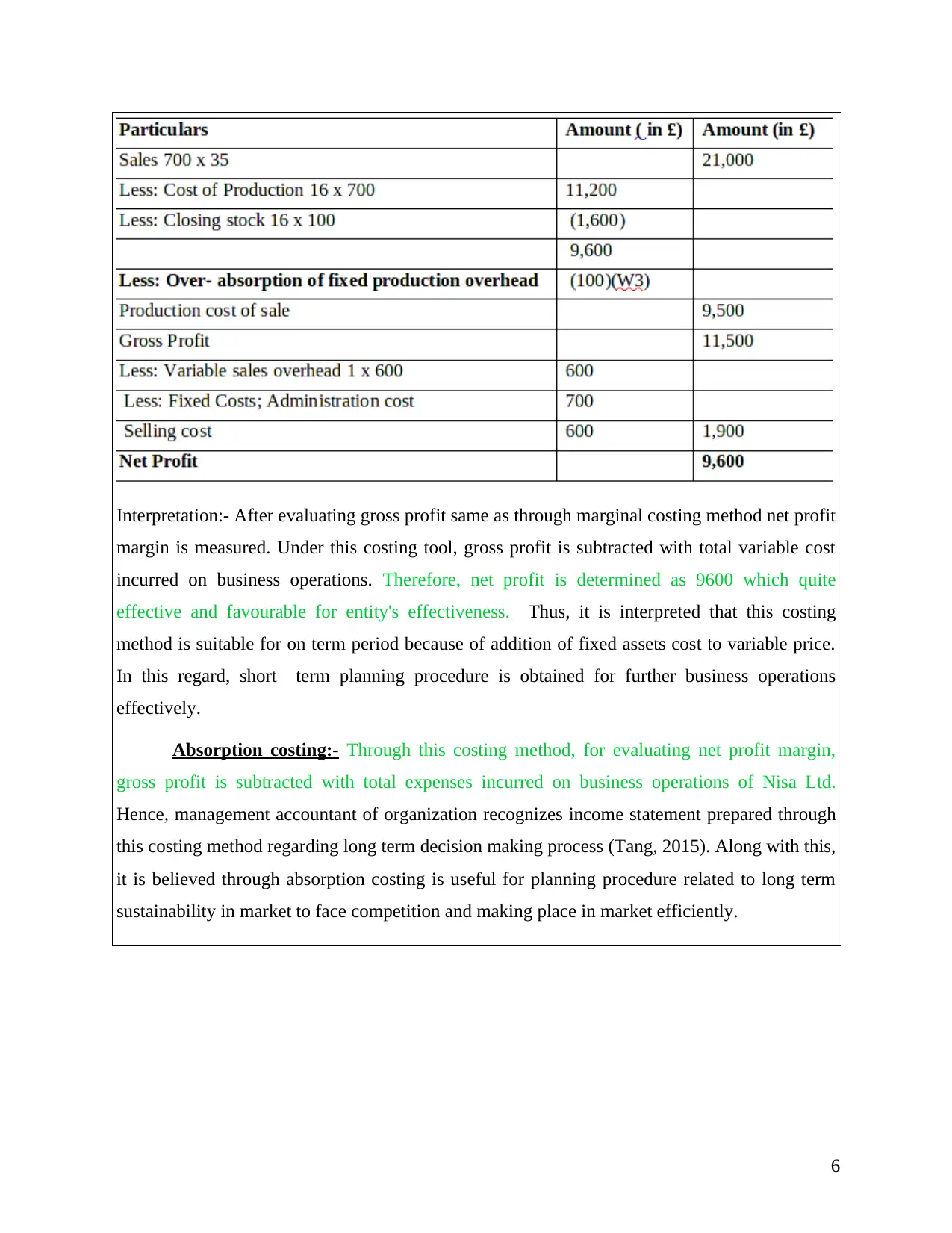

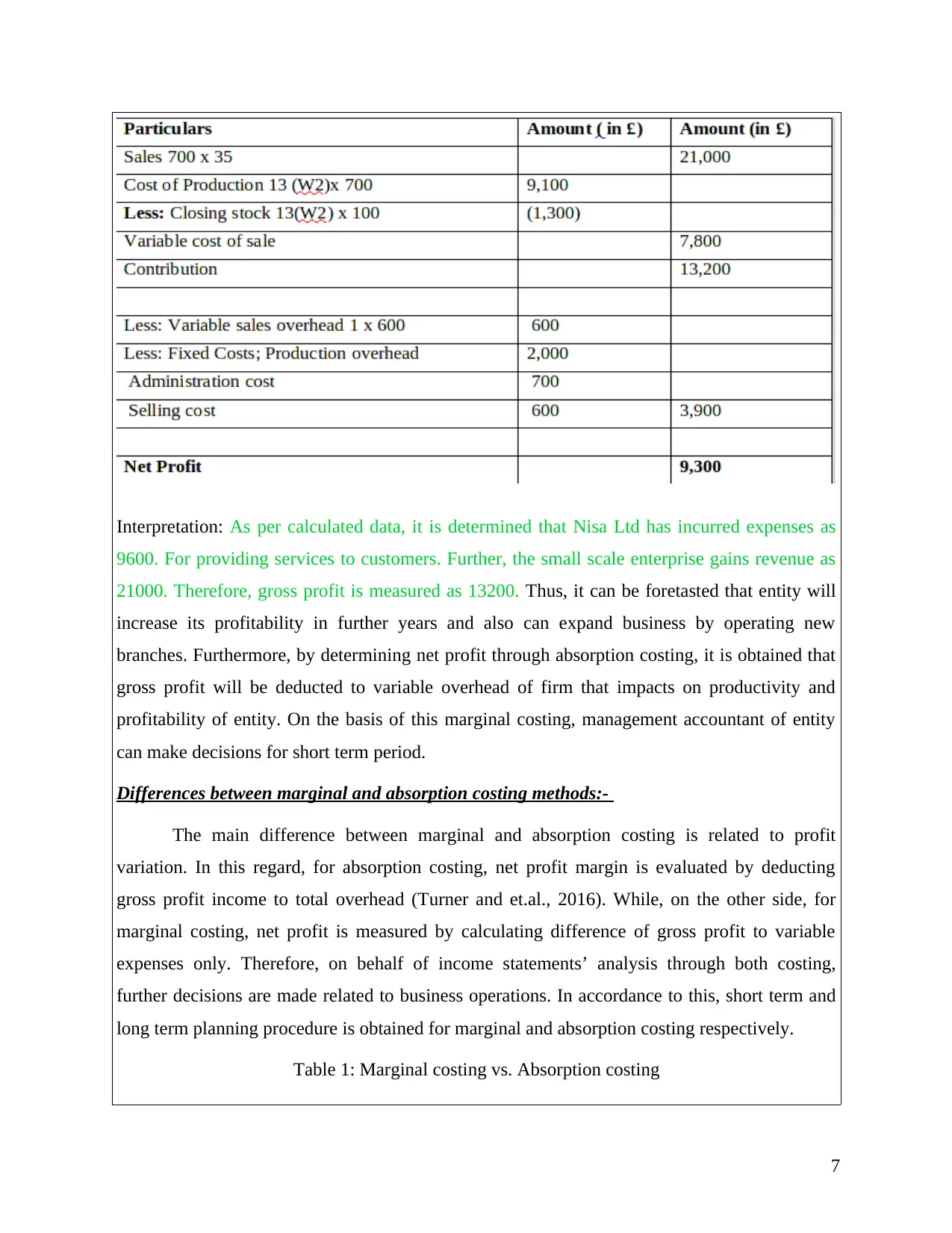

Interpretation:- After evaluating gross profit same as through marginal costing method net profit

margin is measured. Under this costing tool, gross profit is subtracted with total variable cost

incurred on business operations. Therefore, net profit is determined as 9600 which quite

effective and favourable for entity's effectiveness. Thus, it is interpreted that this costing

method is suitable for on term period because of addition of fixed assets cost to variable price.

In this regard, short term planning procedure is obtained for further business operations

effectively.

Absorption costing:- Through this costing method, for evaluating net profit margin,

gross profit is subtracted with total expenses incurred on business operations of Nisa Ltd.

Hence, management accountant of organization recognizes income statement prepared through

this costing method regarding long term decision making process (Tang, 2015). Along with this,

it is believed through absorption costing is useful for planning procedure related to long term

sustainability in market to face competition and making place in market efficiently.

6

margin is measured. Under this costing tool, gross profit is subtracted with total variable cost

incurred on business operations. Therefore, net profit is determined as 9600 which quite

effective and favourable for entity's effectiveness. Thus, it is interpreted that this costing

method is suitable for on term period because of addition of fixed assets cost to variable price.

In this regard, short term planning procedure is obtained for further business operations

effectively.

Absorption costing:- Through this costing method, for evaluating net profit margin,

gross profit is subtracted with total expenses incurred on business operations of Nisa Ltd.

Hence, management accountant of organization recognizes income statement prepared through

this costing method regarding long term decision making process (Tang, 2015). Along with this,

it is believed through absorption costing is useful for planning procedure related to long term

sustainability in market to face competition and making place in market efficiently.

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Interpretation: As per calculated data, it is determined that Nisa Ltd has incurred expenses as

9600. For providing services to customers. Further, the small scale enterprise gains revenue as

21000. Therefore, gross profit is measured as 13200. Thus, it can be foretasted that entity will

increase its profitability in further years and also can expand business by operating new

branches. Furthermore, by determining net profit through absorption costing, it is obtained that

gross profit will be deducted to variable overhead of firm that impacts on productivity and

profitability of entity. On the basis of this marginal costing, management accountant of entity

can make decisions for short term period.

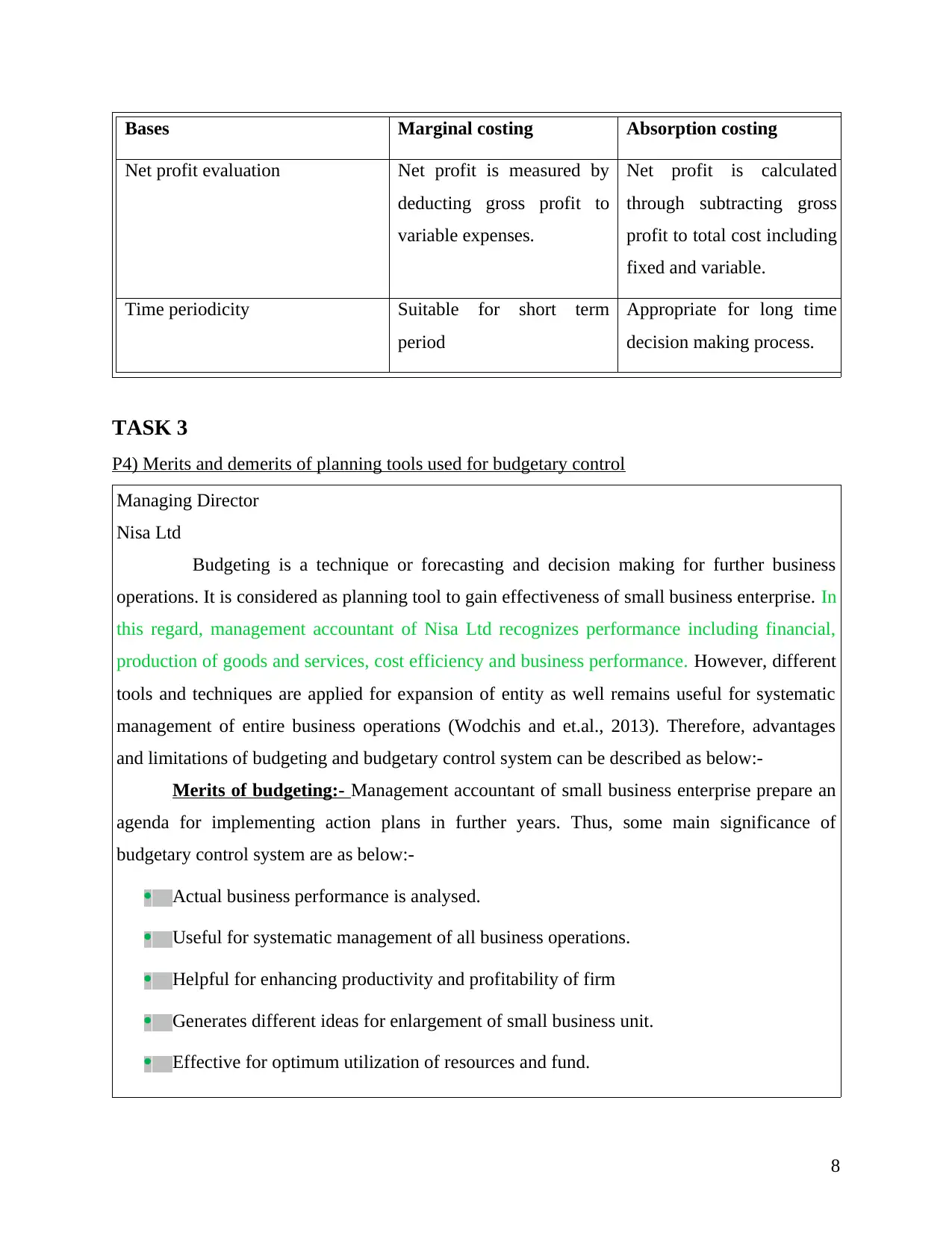

Differences between marginal and absorption costing methods:-

The main difference between marginal and absorption costing is related to profit

variation. In this regard, for absorption costing, net profit margin is evaluated by deducting

gross profit income to total overhead (Turner and et.al., 2016). While, on the other side, for

marginal costing, net profit is measured by calculating difference of gross profit to variable

expenses only. Therefore, on behalf of income statements’ analysis through both costing,

further decisions are made related to business operations. In accordance to this, short term and

long term planning procedure is obtained for marginal and absorption costing respectively.

Table 1: Marginal costing vs. Absorption costing

7

9600. For providing services to customers. Further, the small scale enterprise gains revenue as

21000. Therefore, gross profit is measured as 13200. Thus, it can be foretasted that entity will

increase its profitability in further years and also can expand business by operating new

branches. Furthermore, by determining net profit through absorption costing, it is obtained that

gross profit will be deducted to variable overhead of firm that impacts on productivity and

profitability of entity. On the basis of this marginal costing, management accountant of entity

can make decisions for short term period.

Differences between marginal and absorption costing methods:-

The main difference between marginal and absorption costing is related to profit

variation. In this regard, for absorption costing, net profit margin is evaluated by deducting

gross profit income to total overhead (Turner and et.al., 2016). While, on the other side, for

marginal costing, net profit is measured by calculating difference of gross profit to variable

expenses only. Therefore, on behalf of income statements’ analysis through both costing,

further decisions are made related to business operations. In accordance to this, short term and

long term planning procedure is obtained for marginal and absorption costing respectively.

Table 1: Marginal costing vs. Absorption costing

7

Bases Marginal costing Absorption costing

Net profit evaluation Net profit is measured by

deducting gross profit to

variable expenses.

Net profit is calculated

through subtracting gross

profit to total cost including

fixed and variable.

Time periodicity Suitable for short term

period

Appropriate for long time

decision making process.

TASK 3

P4) Merits and demerits of planning tools used for budgetary control

Managing Director

Nisa Ltd

Budgeting is a technique or forecasting and decision making for further business

operations. It is considered as planning tool to gain effectiveness of small business enterprise. In

this regard, management accountant of Nisa Ltd recognizes performance including financial,

production of goods and services, cost efficiency and business performance. However, different

tools and techniques are applied for expansion of entity as well remains useful for systematic

management of entire business operations (Wodchis and et.al., 2013). Therefore, advantages

and limitations of budgeting and budgetary control system can be described as below:-

Merits of budgeting:- Management accountant of small business enterprise prepare an

agenda for implementing action plans in further years. Thus, some main significance of

budgetary control system are as below:-

Actual business performance is analysed.

Useful for systematic management of all business operations.

Helpful for enhancing productivity and profitability of firm

Generates different ideas for enlargement of small business unit.

Effective for optimum utilization of resources and fund.

8

Net profit evaluation Net profit is measured by

deducting gross profit to

variable expenses.

Net profit is calculated

through subtracting gross

profit to total cost including

fixed and variable.

Time periodicity Suitable for short term

period

Appropriate for long time

decision making process.

TASK 3

P4) Merits and demerits of planning tools used for budgetary control

Managing Director

Nisa Ltd

Budgeting is a technique or forecasting and decision making for further business

operations. It is considered as planning tool to gain effectiveness of small business enterprise. In

this regard, management accountant of Nisa Ltd recognizes performance including financial,

production of goods and services, cost efficiency and business performance. However, different

tools and techniques are applied for expansion of entity as well remains useful for systematic

management of entire business operations (Wodchis and et.al., 2013). Therefore, advantages

and limitations of budgeting and budgetary control system can be described as below:-

Merits of budgeting:- Management accountant of small business enterprise prepare an

agenda for implementing action plans in further years. Thus, some main significance of

budgetary control system are as below:-

Actual business performance is analysed.

Useful for systematic management of all business operations.

Helpful for enhancing productivity and profitability of firm

Generates different ideas for enlargement of small business unit.

Effective for optimum utilization of resources and fund.

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.