Management Accounting Report: Financial Analysis for Nisa (UK)

VerifiedAdded on 2020/06/06

|15

|5249

|44

Report

AI Summary

This report provides a detailed analysis of management accounting principles and their application within Nisa, a UK-based retail company. It begins with an introduction to management accounting, highlighting its importance in financial decision-making, and then delves into various essential requirements and methods, including cost accounting, inventory management, job costing, and budgetary control. The report explores different methods used in management accounting such as cost reports, budgeting, job costing, life cycle costing, standard costing, integrated cost and financial costing. It also discusses the practical application of these techniques within Nisa. Furthermore, the report outlines the differences between marginal costing and absorption costing. The analysis includes the advantages and disadvantages of planning tools and management accounting systems used to address financial problems within the organization, concluding with a summary of the key findings and references.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P.1 Management accounting and essential requirements of different types of management

accounting...............................................................................................................................1

P.2 Different method used in management accounting..........................................................3

D.1 How management accounting use in organisation..........................................................5

TASK 2............................................................................................................................................5

P.3 Difference between management accounting techniques................................................5

M.2 Management accounting techniques and produce appropriate financial reporting........7

D.2 Interpretation is help to business activity........................................................................7

TASK 3............................................................................................................................................7

P.4 Advantages and disadvantages of different types of planning tools that can be used for

budgetary control....................................................................................................................7

P.5 Management accounting systems to respond to financial problems................................9

M.3 Planning tools is help to find out any problem.............................................................10

M.4 Regarding financial problem and management accounting..........................................11

D.3 Planning is solved financial problems...........................................................................11

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P.1 Management accounting and essential requirements of different types of management

accounting...............................................................................................................................1

P.2 Different method used in management accounting..........................................................3

D.1 How management accounting use in organisation..........................................................5

TASK 2............................................................................................................................................5

P.3 Difference between management accounting techniques................................................5

M.2 Management accounting techniques and produce appropriate financial reporting........7

D.2 Interpretation is help to business activity........................................................................7

TASK 3............................................................................................................................................7

P.4 Advantages and disadvantages of different types of planning tools that can be used for

budgetary control....................................................................................................................7

P.5 Management accounting systems to respond to financial problems................................9

M.3 Planning tools is help to find out any problem.............................................................10

M.4 Regarding financial problem and management accounting..........................................11

D.3 Planning is solved financial problems...........................................................................11

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION

Management accounting is a process to manage financial factors in the working

environment. In this context, future decision making is based on the financial sector. On the

other hand, proper financial management is most essential with the help of some method to be

used in working state of affairs. This written report is based on Nisa which is an independent

grocers and has less than 50 employees. This company is basically located in United Kingdom

and provide different services in retail sector. Further, it covered income statement and cost

analysis management which is helpful to distribute income in various fielded of internal working

situations (Klychova and et.al 2015). In addition, administration accounting system is helpful to

improve internal environment so that business action can be carried out. In addition, financial

report and interpretative data is useful at the time to take new decision in working environment.

TASK 1

P.1 Management accounting and essential requirements of different types of management

accounting

Management accounting is most essential part of each and every organisation. It has

helped to manage finance at internal and external work, which gives positive result in future time

periods. Manager uses provision of accounting information in order to provide better information

and to take any decision in work place. It is one of the most important part to manage the growth

rate in market and to make some changes as per need of financial department. On the other side,

financial data and advice to the organisation is most essential part to improve the work and

modification in development rate in market (Coad and et.al , 2015). Moreover, management

accounting is a process to maintain all the transaction that are to be recorded and analyses in

order to be used in internal working environment. There are feature of management accounting is

used form development are as follows :

Management accounting is selected by the firm for little information in bulk. Only useful

information about the facts which is beneficial for overall development in market are

carried into action.

The financial accounting shows different basic and makes some correction in financial

sector (Hall, 2016). To be focused on proper planning and take a new decision for more

improvement in future development.

1

Management accounting is a process to manage financial factors in the working

environment. In this context, future decision making is based on the financial sector. On the

other hand, proper financial management is most essential with the help of some method to be

used in working state of affairs. This written report is based on Nisa which is an independent

grocers and has less than 50 employees. This company is basically located in United Kingdom

and provide different services in retail sector. Further, it covered income statement and cost

analysis management which is helpful to distribute income in various fielded of internal working

situations (Klychova and et.al 2015). In addition, administration accounting system is helpful to

improve internal environment so that business action can be carried out. In addition, financial

report and interpretative data is useful at the time to take new decision in working environment.

TASK 1

P.1 Management accounting and essential requirements of different types of management

accounting

Management accounting is most essential part of each and every organisation. It has

helped to manage finance at internal and external work, which gives positive result in future time

periods. Manager uses provision of accounting information in order to provide better information

and to take any decision in work place. It is one of the most important part to manage the growth

rate in market and to make some changes as per need of financial department. On the other side,

financial data and advice to the organisation is most essential part to improve the work and

modification in development rate in market (Coad and et.al , 2015). Moreover, management

accounting is a process to maintain all the transaction that are to be recorded and analyses in

order to be used in internal working environment. There are feature of management accounting is

used form development are as follows :

Management accounting is selected by the firm for little information in bulk. Only useful

information about the facts which is beneficial for overall development in market are

carried into action.

The financial accounting shows different basic and makes some correction in financial

sector (Hall, 2016). To be focused on proper planning and take a new decision for more

improvement in future development.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Under commercial enterprise accounting system, net income and loss relationship is

prepared to know the quantity of net income earned or loss endured. It does not reveal the

ground for such quantity of profit attained or loss experience.

There are some essential features that must be uses to improve internal working environment and

make some correction as per the need (Coad and et.al , 2015). On the other side, some essential

features are as follows :-

Cost accounting :- In cost accounting system is focused on approximate cost is to be

used in a working environment. In this way it includes, inventory management, cost

analyses, cost control and profit analyses. All such analyses are most important part and

manage the growth rate in market (Wouters and Kirchberger, 2015). To manage

inventory in the business it is required to manage the growth rate in the marketplace.

Director relies on business concerns and explanation data in unspecific and specific on

expenditure for any task of the troupe may be explained via its outlay.

Inventory management :- To manage inventory is most essential parts and it controls,

overseeing the order, storage of compound. In this context, dominant and visual

perception of amount of the finished corking for sale (Wouters, and Kirchberger, 2015).

The subjective of stock lists management is to accurately realize present inventory levels

and decreases overstock and under-stock determines. The inventory of the business is the

most important part and uses them in a productive way.

Job costing system :- This is another most essential part of the organisation. Job costing

system is the use of system of allocation of manufacturing cost to be used in the

organisation (Hall, 2016). To be used each and every data regarding to manufacture and

other factor cost is to be used in service and production job.

Tax accounting :- In tax accounting is most important for the business growth and

increase the revenue that makes is as a tax. There are different kinds of tax like corporate

tax, duty's and transportation charge is to be used in a working environment.

Budgetary control :- To manage budget, it is helpful to solve any problem in working

environment. In internal department is focus to prepare a budget for each activity as per

the need of organisation (Nitzl, 2016). This is assistance to find out how much money is

invested to internal department and manage the work in organisation.

2

prepared to know the quantity of net income earned or loss endured. It does not reveal the

ground for such quantity of profit attained or loss experience.

There are some essential features that must be uses to improve internal working environment and

make some correction as per the need (Coad and et.al , 2015). On the other side, some essential

features are as follows :-

Cost accounting :- In cost accounting system is focused on approximate cost is to be

used in a working environment. In this way it includes, inventory management, cost

analyses, cost control and profit analyses. All such analyses are most important part and

manage the growth rate in market (Wouters and Kirchberger, 2015). To manage

inventory in the business it is required to manage the growth rate in the marketplace.

Director relies on business concerns and explanation data in unspecific and specific on

expenditure for any task of the troupe may be explained via its outlay.

Inventory management :- To manage inventory is most essential parts and it controls,

overseeing the order, storage of compound. In this context, dominant and visual

perception of amount of the finished corking for sale (Wouters, and Kirchberger, 2015).

The subjective of stock lists management is to accurately realize present inventory levels

and decreases overstock and under-stock determines. The inventory of the business is the

most important part and uses them in a productive way.

Job costing system :- This is another most essential part of the organisation. Job costing

system is the use of system of allocation of manufacturing cost to be used in the

organisation (Hall, 2016). To be used each and every data regarding to manufacture and

other factor cost is to be used in service and production job.

Tax accounting :- In tax accounting is most important for the business growth and

increase the revenue that makes is as a tax. There are different kinds of tax like corporate

tax, duty's and transportation charge is to be used in a working environment.

Budgetary control :- To manage budget, it is helpful to solve any problem in working

environment. In internal department is focus to prepare a budget for each activity as per

the need of organisation (Nitzl, 2016). This is assistance to find out how much money is

invested to internal department and manage the work in organisation.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

All essential features are most important in management accounting and make some changes as

per the need of future development. In administration accounting price, budget and tax all three

factors are most useful.

P.2 Different method used in management accounting

Organisation is focus on some function like, finance. It is most of the essence function

which is used in overall improvement of market growth. Management accounting is focused on

controlling, planning and decision making in work place. All three factors are most plays

essential part in managerial work (Nitzl, 2016). Proper planning is helping in future performance

and makes a plan with the help of management accounting and increase the growth rate in future

markets. Also, it applied for price which is useful in the future alteration and modification profit

market. To be understand the maximization of each and every activity is to be used in the work

place. Some method used in management accounting are as follows :-

Cost report :- In this context, it is to be focused on management accounting so as to

calculate cost for each unit. To manage cost is most for the essence part and increases the

market share. In this way it also includes, overheads cost, labour cost etc. all such is most

of the essence part before production start in working environment. On the other hand,

cost report is one of the most crucial part decide the cost as per need in market.

Budget :- Management accounting is to be a focal point on budget and make some

improvement in level of carrying actions. To set budget, each and every activity as per

the need of adjustment should be carried into action report (Wouters and Kirchberger,

2015). The divergence computed are evaluated when process new programme plus all

subject matter concerning the amount of money is catalogued on the carrying into activity

written document.

Job costing :- In job costing main focus of this method is to be used in recording

manufacturing cost. The project management and accounting department is to be focused

on to track cost in work environment (Nitzl, 2016). It is one of the most important

department in the process of costing and allocation of cost as per the need of working

environment. Some changes as per the need of market and follow new trends.

Life cycle costing :- In life cycle costing is use economic factor and some changes as per

the need of organisation. Economic factor is most important part to manage the growth

rate of organisation. Cost is to be decides as per the need of market demand and follows

3

per the need of future development. In administration accounting price, budget and tax all three

factors are most useful.

P.2 Different method used in management accounting

Organisation is focus on some function like, finance. It is most of the essence function

which is used in overall improvement of market growth. Management accounting is focused on

controlling, planning and decision making in work place. All three factors are most plays

essential part in managerial work (Nitzl, 2016). Proper planning is helping in future performance

and makes a plan with the help of management accounting and increase the growth rate in future

markets. Also, it applied for price which is useful in the future alteration and modification profit

market. To be understand the maximization of each and every activity is to be used in the work

place. Some method used in management accounting are as follows :-

Cost report :- In this context, it is to be focused on management accounting so as to

calculate cost for each unit. To manage cost is most for the essence part and increases the

market share. In this way it also includes, overheads cost, labour cost etc. all such is most

of the essence part before production start in working environment. On the other hand,

cost report is one of the most crucial part decide the cost as per need in market.

Budget :- Management accounting is to be a focal point on budget and make some

improvement in level of carrying actions. To set budget, each and every activity as per

the need of adjustment should be carried into action report (Wouters and Kirchberger,

2015). The divergence computed are evaluated when process new programme plus all

subject matter concerning the amount of money is catalogued on the carrying into activity

written document.

Job costing :- In job costing main focus of this method is to be used in recording

manufacturing cost. The project management and accounting department is to be focused

on to track cost in work environment (Nitzl, 2016). It is one of the most important

department in the process of costing and allocation of cost as per the need of working

environment. Some changes as per the need of market and follow new trends.

Life cycle costing :- In life cycle costing is use economic factor and some changes as per

the need of organisation. Economic factor is most important part to manage the growth

rate of organisation. Cost is to be decides as per the need of market demand and follows

3

economic factor. To manage wok as per the need of marketing environment and

improvement in different factor in work place (Messner and et.al 2016). It compares the

initial investments option and identifies the list cost to be used in marketing.

Standard costing :- In standard cost is to be used the submitting the expected cost for

and the annual cost to be used in on the job environment. There are to be used cost

accounting records are most essential part to bring off the growth rate in the market (Hall,

2016). The actual costs which are used and expected cost are those costs, which were

used at the time of future time period. The Organisation is to be engrossed on some cost

to be set as per the need of marketing essential and need of market growth.

Integrated cost :- In integrated cost is to be focus on risk analyse and provide the good

quality of working environment. To reduce the level of risk and to manage as per the

need of marketing environment. Organisation is to be decide cost which is useful and

compare with demand in market. Cost is one of the most important part and increase the

growth rate in market (Andersén and Samuelsson 2016). To analyse risk is useful to

future development and make some changes which is useful for internal working

situation.

Financial costing :- Financial costing is one of the most important method to manage the

cost as per need of organisation (Hall, 2016). It is also called cost of finance and some

other interest and tax is to be included in the work place. On the other side, some

different complaint, participating in the appropriation of medium of exchange to build or

acquisition quality.

All these methods are used in management accounting for improving the growth rate in the

market. All method is most essential and plastic new monetary funds plus all substance

concerning the amount of money is listed on the carrying into action written report.

Management accounting is focused on control, planning and decision making in the work

place. All three factors are most essential part in managerial work. Management accounting is

selecting only little information from the bulk (Somalia and et.al 2014). In working environment

future development and make some changes which are useful for internal working situations.

Management accounting is the most important part to improve the growth rate in the market and

make some changes in the working environment.

4

improvement in different factor in work place (Messner and et.al 2016). It compares the

initial investments option and identifies the list cost to be used in marketing.

Standard costing :- In standard cost is to be used the submitting the expected cost for

and the annual cost to be used in on the job environment. There are to be used cost

accounting records are most essential part to bring off the growth rate in the market (Hall,

2016). The actual costs which are used and expected cost are those costs, which were

used at the time of future time period. The Organisation is to be engrossed on some cost

to be set as per the need of marketing essential and need of market growth.

Integrated cost :- In integrated cost is to be focus on risk analyse and provide the good

quality of working environment. To reduce the level of risk and to manage as per the

need of marketing environment. Organisation is to be decide cost which is useful and

compare with demand in market. Cost is one of the most important part and increase the

growth rate in market (Andersén and Samuelsson 2016). To analyse risk is useful to

future development and make some changes which is useful for internal working

situation.

Financial costing :- Financial costing is one of the most important method to manage the

cost as per need of organisation (Hall, 2016). It is also called cost of finance and some

other interest and tax is to be included in the work place. On the other side, some

different complaint, participating in the appropriation of medium of exchange to build or

acquisition quality.

All these methods are used in management accounting for improving the growth rate in the

market. All method is most essential and plastic new monetary funds plus all substance

concerning the amount of money is listed on the carrying into action written report.

Management accounting is focused on control, planning and decision making in the work

place. All three factors are most essential part in managerial work. Management accounting is

selecting only little information from the bulk (Somalia and et.al 2014). In working environment

future development and make some changes which are useful for internal working situations.

Management accounting is the most important part to improve the growth rate in the market and

make some changes in the working environment.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

D.1 How management accounting use in organisation

Nisa need to make use of some new techniques which is used in management accounting

and improve the growth rate in the market. Standard cost is to be used the submitting the

expected cost for and the annual cost to be used in on the job environment. In this way,

integrated, cost is to be decide cost which is useful and comparable with demand in the market.

TASK 2

P.3 Difference between management accounting techniques

Management accounting techniques is one of the most important part that is help to

manage the growth rate in market. These techniques are used to solve any problem in cost

statement and income statement. To manage income statements as per the need of internal and

external factor. They most important reason to analysis marginal costing techniques to allows

attraction of management to be focused on the changes which results from the decisions which

are on the part of thought. For example, material cost, working cost, production overhead costs.

In this way two management accounting techniques are as follows :-

Difference

Marginal costing Absorption costing

In this costing is to be focus on decision

making techniques is to be used for the total

cost of production.

In this context appropriate to the total cost to

the cost center in order to determine the total

cost of production.

The variable cost is to be considered a product

cost and fixed cost as a period cost.

In this way, both the cost is to be considered a

period cost.

To be measuring the profit with the help of

profit volume ratio. (Andersén and

Samuelsson, 2016.)

In these techniques fixed cost is to be used, so

profit will be affected in market share.

To be focus on contribution per unit is the

main highlighted of these techniques.

Net profit per unit will be measure.(Suomala

and et.al 2014)

To be contributed each and every product in

working environment.

To be concentration on presented in

conversational way.

5

Nisa need to make use of some new techniques which is used in management accounting

and improve the growth rate in the market. Standard cost is to be used the submitting the

expected cost for and the annual cost to be used in on the job environment. In this way,

integrated, cost is to be decide cost which is useful and comparable with demand in the market.

TASK 2

P.3 Difference between management accounting techniques

Management accounting techniques is one of the most important part that is help to

manage the growth rate in market. These techniques are used to solve any problem in cost

statement and income statement. To manage income statements as per the need of internal and

external factor. They most important reason to analysis marginal costing techniques to allows

attraction of management to be focused on the changes which results from the decisions which

are on the part of thought. For example, material cost, working cost, production overhead costs.

In this way two management accounting techniques are as follows :-

Difference

Marginal costing Absorption costing

In this costing is to be focus on decision

making techniques is to be used for the total

cost of production.

In this context appropriate to the total cost to

the cost center in order to determine the total

cost of production.

The variable cost is to be considered a product

cost and fixed cost as a period cost.

In this way, both the cost is to be considered a

period cost.

To be measuring the profit with the help of

profit volume ratio. (Andersén and

Samuelsson, 2016.)

In these techniques fixed cost is to be used, so

profit will be affected in market share.

To be focus on contribution per unit is the

main highlighted of these techniques.

Net profit per unit will be measure.(Suomala

and et.al 2014)

To be contributed each and every product in

working environment.

To be concentration on presented in

conversational way.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

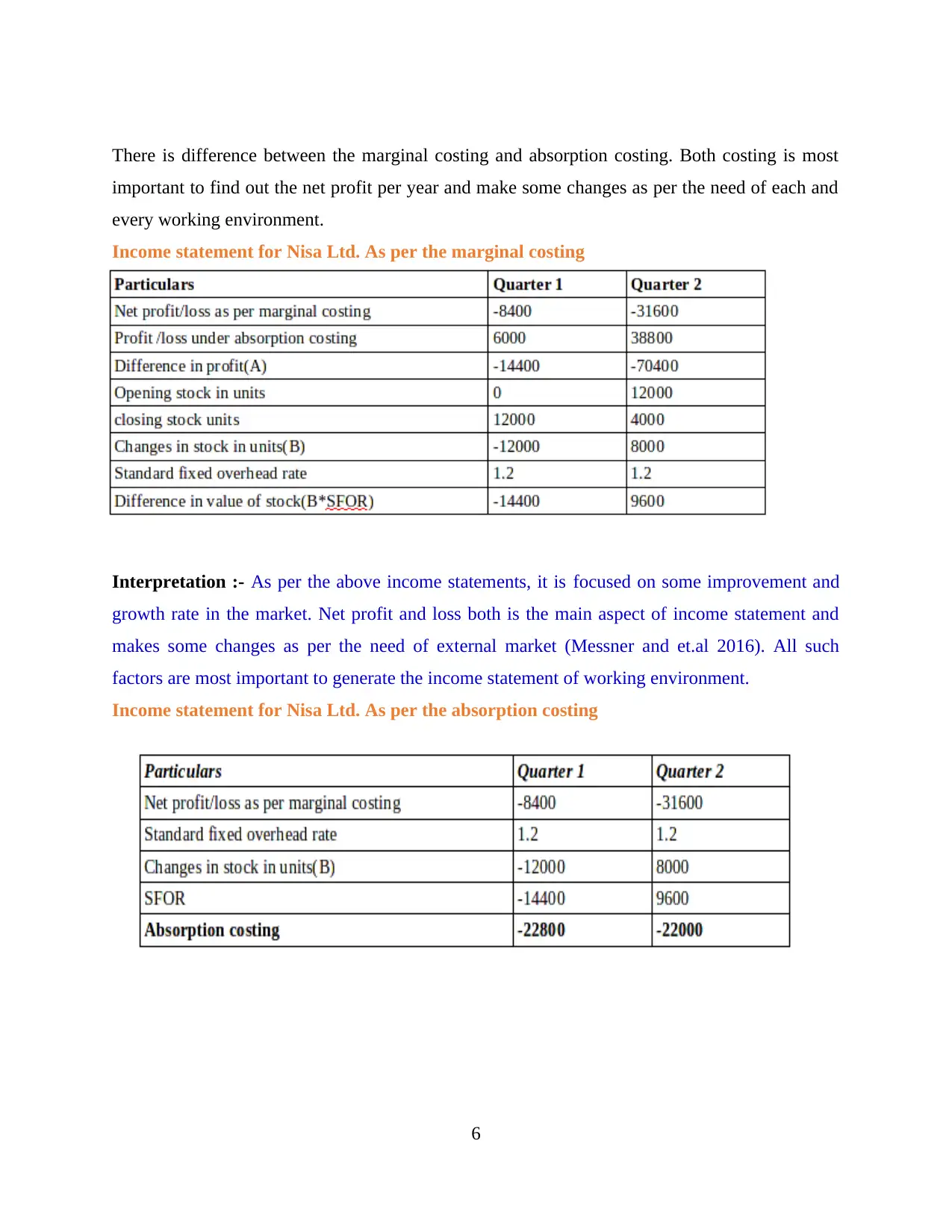

There is difference between the marginal costing and absorption costing. Both costing is most

important to find out the net profit per year and make some changes as per the need of each and

every working environment.

Income statement for Nisa Ltd. As per the marginal costing

Interpretation :- As per the above income statements, it is focused on some improvement and

growth rate in the market. Net profit and loss both is the main aspect of income statement and

makes some changes as per the need of external market (Messner and et.al 2016). All such

factors are most important to generate the income statement of working environment.

Income statement for Nisa Ltd. As per the absorption costing

6

important to find out the net profit per year and make some changes as per the need of each and

every working environment.

Income statement for Nisa Ltd. As per the marginal costing

Interpretation :- As per the above income statements, it is focused on some improvement and

growth rate in the market. Net profit and loss both is the main aspect of income statement and

makes some changes as per the need of external market (Messner and et.al 2016). All such

factors are most important to generate the income statement of working environment.

Income statement for Nisa Ltd. As per the absorption costing

6

Interpretation :- As per the above table, this is most important and make some improvement in

growth rate. In absorption costing is focus is to inventory valuation and manufacturing expenses

is used fixed costs as well as variable cost (Coad and et.al, 2015). Both the cost is most important

and makes some changes as per the need of internal working environment.

M.2 Management accounting techniques and produce appropriate financial reporting

In this context management accounting techniques is one of the most important part to

manage the growth rate in market. These techniques are used to solve any problem in cost

statement and income statement (Messner and et.al 2016). Income statement and cost statement

both is most important part to increase the appropriate to the total cost to the cost centre in order

to determine the total cost of production. To be focus on net profit is most important and make

some changes in internal working environment.

D.2 Interpretation is help to business activity

In this way, both management accounting techniques are most important to find out the

any problem and make some changes' in working environment. Both fixed and variable cost has

given direct impact on performance and growth rate in the organisation. On the other side, the

fixed cost is fixed at the end of the production in a working environment and variable cost is to

be changed, as per the change in production activity. To be contributed each and every product in

a working environment.

TASK 3

P.4 Advantages and disadvantages of different types of planning tools that can be used for

budgetary control

Budgetary control is one of the most important parts to increase the market share and

manage the work as per the need of the organisation. To be focused on budget in each and every

department as per the need of internal work. Planning is the most important part to manage

budgets in a working environment and make some changes in the overall environment. The

comparison of the monetary fund sum of money with the actual magnitude wills assistance the

administration to locate deviation and make disciplinary actions quickly (Somalia and et.al

2014). Budget is helping to improve the profitability in the market. To be fixed then Some

planning tools is to be used the working environment are as follows ;-

Pricing :- In price is one of the most important part to set a price strategies help to

apprehension how the challenger ascertain their commodity or work damage and demand

7

growth rate. In absorption costing is focus is to inventory valuation and manufacturing expenses

is used fixed costs as well as variable cost (Coad and et.al, 2015). Both the cost is most important

and makes some changes as per the need of internal working environment.

M.2 Management accounting techniques and produce appropriate financial reporting

In this context management accounting techniques is one of the most important part to

manage the growth rate in market. These techniques are used to solve any problem in cost

statement and income statement (Messner and et.al 2016). Income statement and cost statement

both is most important part to increase the appropriate to the total cost to the cost centre in order

to determine the total cost of production. To be focus on net profit is most important and make

some changes in internal working environment.

D.2 Interpretation is help to business activity

In this way, both management accounting techniques are most important to find out the

any problem and make some changes' in working environment. Both fixed and variable cost has

given direct impact on performance and growth rate in the organisation. On the other side, the

fixed cost is fixed at the end of the production in a working environment and variable cost is to

be changed, as per the change in production activity. To be contributed each and every product in

a working environment.

TASK 3

P.4 Advantages and disadvantages of different types of planning tools that can be used for

budgetary control

Budgetary control is one of the most important parts to increase the market share and

manage the work as per the need of the organisation. To be focused on budget in each and every

department as per the need of internal work. Planning is the most important part to manage

budgets in a working environment and make some changes in the overall environment. The

comparison of the monetary fund sum of money with the actual magnitude wills assistance the

administration to locate deviation and make disciplinary actions quickly (Somalia and et.al

2014). Budget is helping to improve the profitability in the market. To be fixed then Some

planning tools is to be used the working environment are as follows ;-

Pricing :- In price is one of the most important part to set a price strategies help to

apprehension how the challenger ascertain their commodity or work damage and demand

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

and provision thought process (Coad and et.al , 2015). Demand and supply to most

important factor that is based on price. It is decides increase and decrease the demand

level in market and make some changes in overall number management activity.

Costing system :- In costing system natural cost, normal cost and standard cost is help to

find out the cost to be used in overall working environment and make some change as per

the need of job costing and process costing is to be used in environment factor. On the

other side, all costing is most important to find out the financial statements of the

organisation.

Strategies planning :- In strategic planning is the most important part and organisation

strength, weakness, opportunities and threats is find out any problem in administration.

The company financial position has helped to management activity to understand the

business grow and make some change as per the utilities of the organisation. It is helping

to define the strategy and direction to make some improvement and help at the time to

take a new decision in the working environment (Somalia and et.al 2014). All such

factors is help at the time when the organisation is grown in new field and make some

improvement in market share.

In budgetary control is to be focus on improvement in organisation culture and internal working

environment. On the other side, budgetary control main aim is to achieve profit and generate

more revenue in work place. Some techniques are to be used in budgetary control are as

follows :-

Zero based budgeting :- In zero based budgeting is focus on all the expenses must be

justified for each period (Somalia and et.al 2014). In working environment each and

every function is to be performance the cost and make some change as per the need of

market share. In each activity budget is to be set and main aim is work is to be done in

effective way.

Incremental Budgeting :- In this kind of budget is to be set actual use of budget and

supervises work environment of budget to increase the market share. An additive budget

is a budget embattled using a previous period's monetary fund or actual carrying into

action as a basis with additive amounts added for the brand-new monetary fund time

period.

8

important factor that is based on price. It is decides increase and decrease the demand

level in market and make some changes in overall number management activity.

Costing system :- In costing system natural cost, normal cost and standard cost is help to

find out the cost to be used in overall working environment and make some change as per

the need of job costing and process costing is to be used in environment factor. On the

other side, all costing is most important to find out the financial statements of the

organisation.

Strategies planning :- In strategic planning is the most important part and organisation

strength, weakness, opportunities and threats is find out any problem in administration.

The company financial position has helped to management activity to understand the

business grow and make some change as per the utilities of the organisation. It is helping

to define the strategy and direction to make some improvement and help at the time to

take a new decision in the working environment (Somalia and et.al 2014). All such

factors is help at the time when the organisation is grown in new field and make some

improvement in market share.

In budgetary control is to be focus on improvement in organisation culture and internal working

environment. On the other side, budgetary control main aim is to achieve profit and generate

more revenue in work place. Some techniques are to be used in budgetary control are as

follows :-

Zero based budgeting :- In zero based budgeting is focus on all the expenses must be

justified for each period (Somalia and et.al 2014). In working environment each and

every function is to be performance the cost and make some change as per the need of

market share. In each activity budget is to be set and main aim is work is to be done in

effective way.

Incremental Budgeting :- In this kind of budget is to be set actual use of budget and

supervises work environment of budget to increase the market share. An additive budget

is a budget embattled using a previous period's monetary fund or actual carrying into

action as a basis with additive amounts added for the brand-new monetary fund time

period.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Rolling budget :- In rolling budget is to be focus on extension of the existing budget is to

be paperboard and some extra budget is to be added in previous budget. In this way, use

some time in growth rate and doing some extra work in organisation. Thus, the resonating

budgets come to the additive postponement of the existent programme model. By doing

so, a business concern forever has a programme that extends one time period into the

forthcoming.

Some advantages of disadvantage of budgetary control which is used in internal organisation at

the time to set a budget in organisation.

Advantages :- Budgetary control is turned out the essentialist tools in organisation. To be

manage the cost and improve the level of carrying into action in market. To be help to

find out the policy, plan and objective to be used in next year. It is most important part on

manage the growth rate in market (Wouters and Kirchberger, 2015). In this way, each

and every department is to be focused on work effectiveness to complete the work on

time. It is one of the most important parts to find out any problem in a working

environment and make some changes as per the need of market value. In organisation

employees budget is helping to increase the awareness about the cost and make some

changes as per the need of the market.

Disadvantages :- In this way, some disadvantages of budgetary control is to manage the

growth rate, but take long time. Inside the organisation many employees are not support

budget control. Hence, forthcoming risks maximise the use of monetary fund control

system (Andersén, and Samuelsson, 2016.). Monetary fund control is a governing body

tool. The monetary fund control occurrence relies upon the topmost administration assist.

When there is non-existence top administration activity, then it will go wrong.

There are all advantage and disadvantage of the organisation and make some changes as per the

need of working environment. Both point is most important part to cover such kind of activity

and manage the growth rate in market (Somalia and et.al 2014). To be help to find out the

policy, plan and objective to be used in next year.

P.5 Management accounting systems to respond to financial problems

Management accounting tools are most important to find out the any problem which in

faced by the organisation and make some changes to increase market share. These are the

position which is demand to acquaint and concerned past the paid as to make the equal to

9

be paperboard and some extra budget is to be added in previous budget. In this way, use

some time in growth rate and doing some extra work in organisation. Thus, the resonating

budgets come to the additive postponement of the existent programme model. By doing

so, a business concern forever has a programme that extends one time period into the

forthcoming.

Some advantages of disadvantage of budgetary control which is used in internal organisation at

the time to set a budget in organisation.

Advantages :- Budgetary control is turned out the essentialist tools in organisation. To be

manage the cost and improve the level of carrying into action in market. To be help to

find out the policy, plan and objective to be used in next year. It is most important part on

manage the growth rate in market (Wouters and Kirchberger, 2015). In this way, each

and every department is to be focused on work effectiveness to complete the work on

time. It is one of the most important parts to find out any problem in a working

environment and make some changes as per the need of market value. In organisation

employees budget is helping to increase the awareness about the cost and make some

changes as per the need of the market.

Disadvantages :- In this way, some disadvantages of budgetary control is to manage the

growth rate, but take long time. Inside the organisation many employees are not support

budget control. Hence, forthcoming risks maximise the use of monetary fund control

system (Andersén, and Samuelsson, 2016.). Monetary fund control is a governing body

tool. The monetary fund control occurrence relies upon the topmost administration assist.

When there is non-existence top administration activity, then it will go wrong.

There are all advantage and disadvantage of the organisation and make some changes as per the

need of working environment. Both point is most important part to cover such kind of activity

and manage the growth rate in market (Somalia and et.al 2014). To be help to find out the

policy, plan and objective to be used in next year.

P.5 Management accounting systems to respond to financial problems

Management accounting tools are most important to find out the any problem which in

faced by the organisation and make some changes to increase market share. These are the

position which is demand to acquaint and concerned past the paid as to make the equal to

9

growing in skilfulness and the revenue assemblage of them. There are some keys carrying into

action indicators is the most essential part and increase the market share and help to identify the

level of carrying into action in the market(Messner and et.al 2016). To manage work and to

improve work administration accounting techniques is to be help and find out the any difficulty

in working environment. There are some most important skills is to be used in working

environment are follows ;-

Financial governance :- In this context is to be focused on the organisation is used each

and every issue related to the financial activity and make some changes as per the need of

market growth (Klychova and et.al 2015). On the other hand, monitoring authority is the

most important part to find out any problem and make some changes in the market. Some

strategy is to be used in a maker environment to increase profit rate.

Effective strategies :- In effective strategies is most important part to find out problem

and solve with the help of effectiveness and use strategies to each and every problem.

The physical process of instrumentality and plan of action that necessity well timed and

effective coverage, full revelation financial, government and are irresponsibly citizenry

and closely-held by the administration (Coad and et.al, 2015). Use more and more

strategies as per the need of market growth and make some changes as per the need of

overall carrying into action in the market.

Manufacturing plants use these systems to help in costing and managing the manufacturing

process. Hospitals implement systems to assist them in insurance billing and other in-house

requirements. The main objective of an internal managerial accounting system is to provide

information to managers so they can make sound decisions. The goal is not to comply with

outside demands, such as those of bankers, but rather to capture valuable data that can be used to

manage and control a business better. For example, a business needs to acquire an expensive

machine, and a management financial system may help the business in timing the purchase when

cash flows are planned to be the highest, avoiding debt.

M.3 Planning tools is help to find out any problem

In management accounting planning tools is one of the most important part to manage the

growth rate in market. Strategies planning is most important part and organisation strength,

weakness, opportunities and threats is find out any problem in administration. To be use some

strategies to increase the market share and make some change internal and external working

10

action indicators is the most essential part and increase the market share and help to identify the

level of carrying into action in the market(Messner and et.al 2016). To manage work and to

improve work administration accounting techniques is to be help and find out the any difficulty

in working environment. There are some most important skills is to be used in working

environment are follows ;-

Financial governance :- In this context is to be focused on the organisation is used each

and every issue related to the financial activity and make some changes as per the need of

market growth (Klychova and et.al 2015). On the other hand, monitoring authority is the

most important part to find out any problem and make some changes in the market. Some

strategy is to be used in a maker environment to increase profit rate.

Effective strategies :- In effective strategies is most important part to find out problem

and solve with the help of effectiveness and use strategies to each and every problem.

The physical process of instrumentality and plan of action that necessity well timed and

effective coverage, full revelation financial, government and are irresponsibly citizenry

and closely-held by the administration (Coad and et.al, 2015). Use more and more

strategies as per the need of market growth and make some changes as per the need of

overall carrying into action in the market.

Manufacturing plants use these systems to help in costing and managing the manufacturing

process. Hospitals implement systems to assist them in insurance billing and other in-house

requirements. The main objective of an internal managerial accounting system is to provide

information to managers so they can make sound decisions. The goal is not to comply with

outside demands, such as those of bankers, but rather to capture valuable data that can be used to

manage and control a business better. For example, a business needs to acquire an expensive

machine, and a management financial system may help the business in timing the purchase when

cash flows are planned to be the highest, avoiding debt.

M.3 Planning tools is help to find out any problem

In management accounting planning tools is one of the most important part to manage the

growth rate in market. Strategies planning is most important part and organisation strength,

weakness, opportunities and threats is find out any problem in administration. To be use some

strategies to increase the market share and make some change internal and external working

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.