Detailed Management Accounting Report: NISA Retail Store Analysis

VerifiedAdded on 2023/03/24

|17

|4769

|54

Report

AI Summary

This report provides a comprehensive analysis of management accounting practices within NISA Retail Store, a UK-based grocery retailer and wholesaler. It explores the essential requirements of various management accounting systems, including activity, investment, cost, taxation, financial, and internal audit functions. The report details different management accounting reporting methods such as job cost reports, inventory and production reports, budget reports, and accounts receivable aging reports. It calculates costs using cost analysis to prepare income statements based on marginal and absorption costing, highlighting their differences. Furthermore, the report examines planning tools used for budgetary control, assessing their merits and demerits. It also evaluates how NISA adapts management accounting systems to address financial challenges, emphasizing the importance of these systems in achieving sustainable success and overcoming financial obstacles, including an analysis of planning tools. This report is a valuable resource for understanding management accounting in a retail setting.

MANAGEMENT ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Explaining management accounting and give the essential requirement of different types of

management accounting systems to NISA retail store................................................................1

P2 Explaining different methods used for management accounting reporting in NISA retail

store..............................................................................................................................................4

M1 Benefits and implication of the management accounting systems........................................5

D1 Critically examining the integration of management accounting reports and systems.........6

TASK 2............................................................................................................................................6

P3 Calculate cost using cost analysis to prepare income statements of marginal and absorption

costing explaining difference between them...............................................................................6

M2 Applying management accounting techniques and financial reporting documents..............8

D2 Interpretation of accurately applicable financial report for NISA Retail store......................9

TASK 3............................................................................................................................................9

P4 Explaining merits and demerits of types of planning tools used for budgetary control for

NISA............................................................................................................................................9

M3 use of various kinds of planning tools in producing adequate budgets for NISA Retail

store............................................................................................................................................11

D3 Analysing Planning tools leads to the sustainable success..................................................11

TASK 4..........................................................................................................................................11

P5 Comparing the ways in which NISA adapt management accounting systems to respond to

financial problems.....................................................................................................................11

M4 Evaluating the importance of management accounting systems in sustainable success and

overcoming financial obstacles..................................................................................................12

D4 Analysing the importance of planning tools in overcoming the financial problems of NISA

retail store..................................................................................................................................12

CONCLUSIONS...........................................................................................................................12

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Explaining management accounting and give the essential requirement of different types of

management accounting systems to NISA retail store................................................................1

P2 Explaining different methods used for management accounting reporting in NISA retail

store..............................................................................................................................................4

M1 Benefits and implication of the management accounting systems........................................5

D1 Critically examining the integration of management accounting reports and systems.........6

TASK 2............................................................................................................................................6

P3 Calculate cost using cost analysis to prepare income statements of marginal and absorption

costing explaining difference between them...............................................................................6

M2 Applying management accounting techniques and financial reporting documents..............8

D2 Interpretation of accurately applicable financial report for NISA Retail store......................9

TASK 3............................................................................................................................................9

P4 Explaining merits and demerits of types of planning tools used for budgetary control for

NISA............................................................................................................................................9

M3 use of various kinds of planning tools in producing adequate budgets for NISA Retail

store............................................................................................................................................11

D3 Analysing Planning tools leads to the sustainable success..................................................11

TASK 4..........................................................................................................................................11

P5 Comparing the ways in which NISA adapt management accounting systems to respond to

financial problems.....................................................................................................................11

M4 Evaluating the importance of management accounting systems in sustainable success and

overcoming financial obstacles..................................................................................................12

D4 Analysing the importance of planning tools in overcoming the financial problems of NISA

retail store..................................................................................................................................12

CONCLUSIONS...........................................................................................................................12

REFERENCES..............................................................................................................................14

INTRODUCTION

Management accounting is playing key role in organisation and helping decision

makers to understand in creating and using good management accounting information.

Management accounting help the management with providing them financial and non

financial information with assist them in making and implementing decisions. Good

management accounting system will include the techniques of accounting like that of cost to

volume profit analysis, marginal costing and absorption costing in producing the relevant

management report for informed decision making. The present report is based on NISA retail

store which is a small grocery store both retailer and wholesaler operating in UK. The report

will cover how NISA store is applying and using the management accounting techniques and

financial reporting. It will also cover the types of planning tools used for budgetary control

used and preparing income statements by calculating cost methods.

TASK 1

P1 Explaining management accounting and give the essential requirement of different types

of management accounting systems to NISA retail store.

From: Management accounting Officer

NISA store

To: GM

NISA store

Subject: Requirements within implicating the a variety of management accounting tools with

techniques

Introduction:

Sir,

It is hereby informed you that, NISA store is without fail generating positive earning

as well as creating a exclusive brand representation in the at hand opposition surroundings

where numerous huge retail store entity are making their existence. Therefore, in terms of

developing the working performances of NISA store the there is require to take on different

improvements in the budgetary systems, cost control technique with enhancing work

efficiency of the personnel. so, in keeping with various types of managements accounting

systems which are necessary used for following the NISA store operations such as:

1

Management accounting is playing key role in organisation and helping decision

makers to understand in creating and using good management accounting information.

Management accounting help the management with providing them financial and non

financial information with assist them in making and implementing decisions. Good

management accounting system will include the techniques of accounting like that of cost to

volume profit analysis, marginal costing and absorption costing in producing the relevant

management report for informed decision making. The present report is based on NISA retail

store which is a small grocery store both retailer and wholesaler operating in UK. The report

will cover how NISA store is applying and using the management accounting techniques and

financial reporting. It will also cover the types of planning tools used for budgetary control

used and preparing income statements by calculating cost methods.

TASK 1

P1 Explaining management accounting and give the essential requirement of different types

of management accounting systems to NISA retail store.

From: Management accounting Officer

NISA store

To: GM

NISA store

Subject: Requirements within implicating the a variety of management accounting tools with

techniques

Introduction:

Sir,

It is hereby informed you that, NISA store is without fail generating positive earning

as well as creating a exclusive brand representation in the at hand opposition surroundings

where numerous huge retail store entity are making their existence. Therefore, in terms of

developing the working performances of NISA store the there is require to take on different

improvements in the budgetary systems, cost control technique with enhancing work

efficiency of the personnel. so, in keeping with various types of managements accounting

systems which are necessary used for following the NISA store operations such as:

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

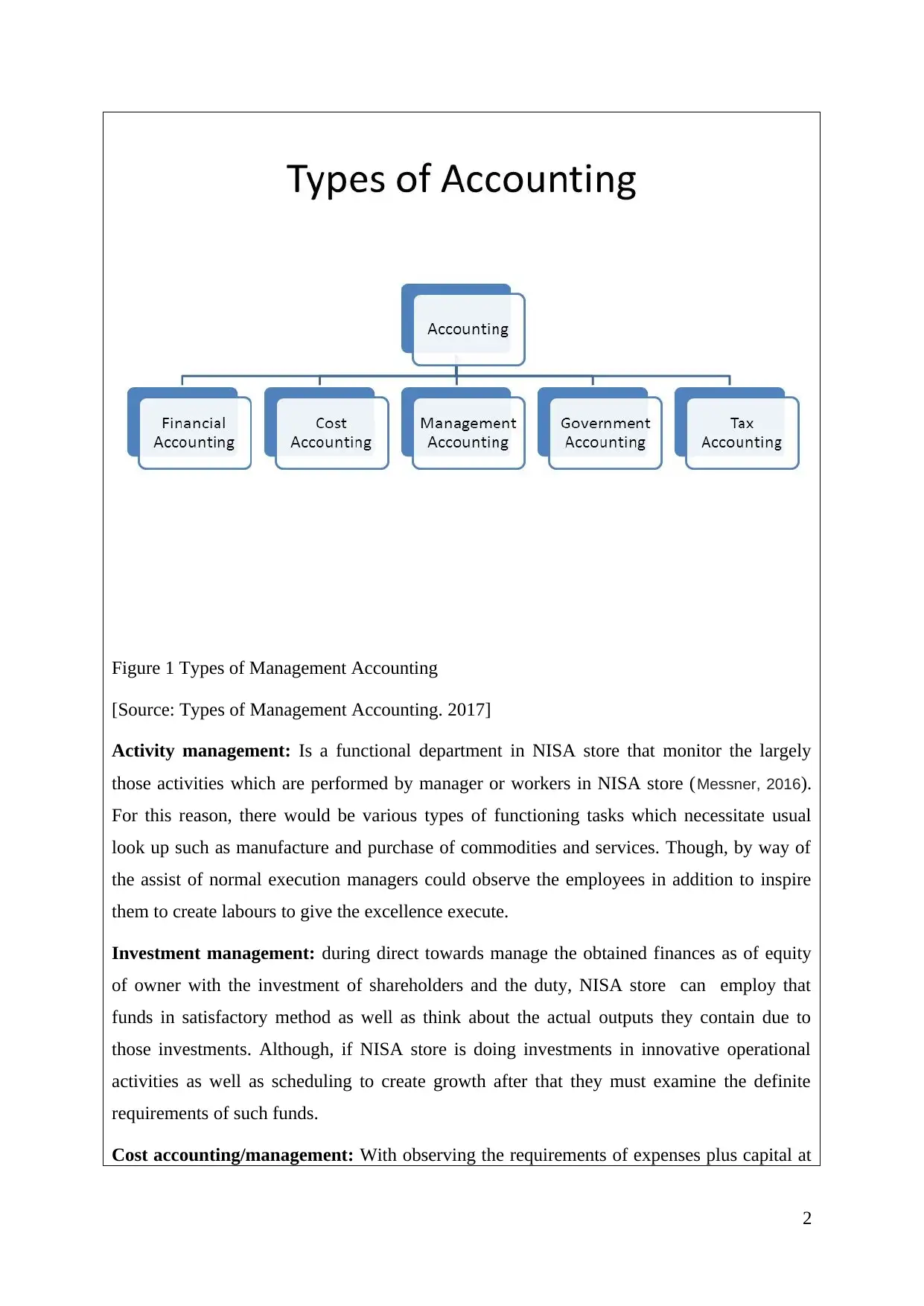

Figure 1 Types of Management Accounting

[Source: Types of Management Accounting. 2017]

Activity management: Is a functional department in NISA store that monitor the largely

those activities which are performed by manager or workers in NISA store (Messner, 2016).

For this reason, there would be various types of functioning tasks which necessitate usual

look up such as manufacture and purchase of commodities and services. Though, by way of

the assist of normal execution managers could observe the employees in addition to inspire

them to create labours to give the excellence execute.

Investment management: during direct towards manage the obtained finances as of equity

of owner with the investment of shareholders and the duty, NISA store can employ that

funds in satisfactory method as well as think about the actual outputs they contain due to

those investments. Although, if NISA store is doing investments in innovative operational

activities as well as scheduling to create growth after that they must examine the definite

requirements of such funds.

Cost accounting/management: With observing the requirements of expenses plus capital at

2

[Source: Types of Management Accounting. 2017]

Activity management: Is a functional department in NISA store that monitor the largely

those activities which are performed by manager or workers in NISA store (Messner, 2016).

For this reason, there would be various types of functioning tasks which necessitate usual

look up such as manufacture and purchase of commodities and services. Though, by way of

the assist of normal execution managers could observe the employees in addition to inspire

them to create labours to give the excellence execute.

Investment management: during direct towards manage the obtained finances as of equity

of owner with the investment of shareholders and the duty, NISA store can employ that

funds in satisfactory method as well as think about the actual outputs they contain due to

those investments. Although, if NISA store is doing investments in innovative operational

activities as well as scheduling to create growth after that they must examine the definite

requirements of such funds.

Cost accounting/management: With observing the requirements of expenses plus capital at

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

hand will be need to monitor the expenditure requirements in the NISA store. Therefore,

there will be diverse functional departments which involve enhancement by the skilled in

creation of sufficient requirements of the expenses and finance for NISA store (Renz, 2016).

So, there will be a mixture of costing techniques for example activity based costing which

indicate the costs incurred at what time producing a component of manufactured goods such

as wages, compensation, rewards, gratuity above the workers or labours as well as pay for of

material, transactions among supplier etc be the major operational areas which requisite high

pricing or appraisal.

Taxation: There have been a range of functioning activities so as to take place throughout

the year like profits collecting and spending. Hence, these are the responsibilities of the NISA

store in filing the expected tax returns as well as remain up to date with the altering policies

and procedures in such manners. As a consequence, in favour of NISA store there will be

transactions connected with a range of products and service plus in background with that they

all contain diverse tax rates which are legislated by confined or central government in UK.

Thus, it will be essential in support of the accounting managers to formulate analysis of all

the levy charge has been rewarded by them as well as check such business.

Financial accounting: Management accounting is also the division of financial accounting

systems. From now, it can be said with the intention of if the inner authority of NISA store is

improved and strong than the firm be able to convene the outside requirements. Thats why,

with the aid of management accounting tools convenient will be augment in presentation and

competence of NISA store as well as it will assist in getting better the output of business and

attractive employees to create the precious hard work in the background with attaining the

goals.

Internal Audit: frequently monitoring the company transaction on the source of periodical

audit which have to be prearranged twice or thrice in a year will help out NISA store to make

the enhanced study over the revenue and expenditures of all. So, there may be requirements

of different managers, auditor and book-keeping professionals in performing such tasks

(Fullerton, Kennedy and Widener, 2014). It might be supposed such techniques will facilitate

professionals in making adequate decisions to carry-on any duty or stop investing in non

profitable business operations.

3

there will be diverse functional departments which involve enhancement by the skilled in

creation of sufficient requirements of the expenses and finance for NISA store (Renz, 2016).

So, there will be a mixture of costing techniques for example activity based costing which

indicate the costs incurred at what time producing a component of manufactured goods such

as wages, compensation, rewards, gratuity above the workers or labours as well as pay for of

material, transactions among supplier etc be the major operational areas which requisite high

pricing or appraisal.

Taxation: There have been a range of functioning activities so as to take place throughout

the year like profits collecting and spending. Hence, these are the responsibilities of the NISA

store in filing the expected tax returns as well as remain up to date with the altering policies

and procedures in such manners. As a consequence, in favour of NISA store there will be

transactions connected with a range of products and service plus in background with that they

all contain diverse tax rates which are legislated by confined or central government in UK.

Thus, it will be essential in support of the accounting managers to formulate analysis of all

the levy charge has been rewarded by them as well as check such business.

Financial accounting: Management accounting is also the division of financial accounting

systems. From now, it can be said with the intention of if the inner authority of NISA store is

improved and strong than the firm be able to convene the outside requirements. Thats why,

with the aid of management accounting tools convenient will be augment in presentation and

competence of NISA store as well as it will assist in getting better the output of business and

attractive employees to create the precious hard work in the background with attaining the

goals.

Internal Audit: frequently monitoring the company transaction on the source of periodical

audit which have to be prearranged twice or thrice in a year will help out NISA store to make

the enhanced study over the revenue and expenditures of all. So, there may be requirements

of different managers, auditor and book-keeping professionals in performing such tasks

(Fullerton, Kennedy and Widener, 2014). It might be supposed such techniques will facilitate

professionals in making adequate decisions to carry-on any duty or stop investing in non

profitable business operations.

3

P2 Explaining different methods used for management accounting reporting in NISA retail

store.

From: Management accounting Officer

NISA retail store

To: GM

NISA retail store

Subject: Requirements of implementing different reporting systems

Introduction:

Sir,

Within consideration by the various functional performances of the NISA Store it can

be supposed that readily available are requirements of having usual exposure from all the

department in NISA store which in turn obliging for business in utilising the effectual efforts

in company operation such as:

Illustration 2: Kinds of various accounting reports

Job Cost Report: This report is equipped on the source of analyse the job or routine made

throughout the phase as well as the operation of expenses for such functioning performance.

Hence, these techniques aid in recording each and every one the transactions which be

supposed to create the moving business activities. Accordingly, around will be expenses

which are applicable by means of the job cost report.

Inventory and Production Reports: book-keeping professionals require recording all the

transaction which are applicable to the manufacture and bring in of raw materials. for this

reason it would be helpful for NISA Retail store to carry out the real requirement of the

resources in the functioning conduct of NISA Retail store. It will be productive for

4

Job cost report

Accounts receivable aging

report

Inventory and

production report

Budget report

Management accounting

store.

From: Management accounting Officer

NISA retail store

To: GM

NISA retail store

Subject: Requirements of implementing different reporting systems

Introduction:

Sir,

Within consideration by the various functional performances of the NISA Store it can

be supposed that readily available are requirements of having usual exposure from all the

department in NISA store which in turn obliging for business in utilising the effectual efforts

in company operation such as:

Illustration 2: Kinds of various accounting reports

Job Cost Report: This report is equipped on the source of analyse the job or routine made

throughout the phase as well as the operation of expenses for such functioning performance.

Hence, these techniques aid in recording each and every one the transactions which be

supposed to create the moving business activities. Accordingly, around will be expenses

which are applicable by means of the job cost report.

Inventory and Production Reports: book-keeping professionals require recording all the

transaction which are applicable to the manufacture and bring in of raw materials. for this

reason it would be helpful for NISA Retail store to carry out the real requirement of the

resources in the functioning conduct of NISA Retail store. It will be productive for

4

Job cost report

Accounts receivable aging

report

Inventory and

production report

Budget report

Management accounting

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

supervision the capital as well as dropping the wastage. On the other side in background with

the requirements and stress in NISA Retail store about products and services that there is

require containing appropriate storage of such goods (Pemsel and Wiewiora, 2013). As a

consequence, these information surround every single of the correlated in command linked

with the value or commodities and their price as well as the nature such as fresh or non

perishable. Consequently, these tasks need the staffing of the fit scrutiny teams who seem for

such requirements of products as well as evidence all the dealings of unit.

Budget Report: This technique belong to the evidence of the business which be to be made

surrounded by the decided restrictions as well as get-together the sufficient quantity of

earnings for making the extended term investments in the prospect. for this reason, this

method reimbursement managers in monitor all the working budgets such as currency, sale,

purchase etc. which in turn helps the definite in manufacture spending in the pertinent time

period.

Accounts Receivable Aging Report: There always will be a choice of debtors NISA Retail

store which are growing the amount overdue in the company's financial records. Hence, these

technique assist the firm in measuring the short term and long term amount outstanding that

be to be monitored by the professional as well as construct the effectual solution which in

turn helps in gaining the payments for such debts. Hence, it can be said that these reports

reimbursement NISA Store in manufacture the sufficient accounts of all the applicable

receivables for instance distributors, supplier and an assortment of functioning unit.

M1 Benefits and implication of the management accounting systems

Within agreement with the a mixture of remuneration of the management accounting

systems which be ready to lend a hand in attaining the business NISA Retail store objectives.

Therefore, readily available know how to be a variety of helpfulness of such activities which

lend a hand entity in meeting positive amount of revenue. It mostly facilitate in getting better

the money flows of NISA Retail store for example monitoring the inflows and outflows as

well as suggestive of manager in production productive efforts for to solve such related

obstacle. It has quite a lot of advantages such as:

Be of assistance in falling the expenses and expenses incur in any tasks or

organisational operations.

5

the requirements and stress in NISA Retail store about products and services that there is

require containing appropriate storage of such goods (Pemsel and Wiewiora, 2013). As a

consequence, these information surround every single of the correlated in command linked

with the value or commodities and their price as well as the nature such as fresh or non

perishable. Consequently, these tasks need the staffing of the fit scrutiny teams who seem for

such requirements of products as well as evidence all the dealings of unit.

Budget Report: This technique belong to the evidence of the business which be to be made

surrounded by the decided restrictions as well as get-together the sufficient quantity of

earnings for making the extended term investments in the prospect. for this reason, this

method reimbursement managers in monitor all the working budgets such as currency, sale,

purchase etc. which in turn helps the definite in manufacture spending in the pertinent time

period.

Accounts Receivable Aging Report: There always will be a choice of debtors NISA Retail

store which are growing the amount overdue in the company's financial records. Hence, these

technique assist the firm in measuring the short term and long term amount outstanding that

be to be monitored by the professional as well as construct the effectual solution which in

turn helps in gaining the payments for such debts. Hence, it can be said that these reports

reimbursement NISA Store in manufacture the sufficient accounts of all the applicable

receivables for instance distributors, supplier and an assortment of functioning unit.

M1 Benefits and implication of the management accounting systems

Within agreement with the a mixture of remuneration of the management accounting

systems which be ready to lend a hand in attaining the business NISA Retail store objectives.

Therefore, readily available know how to be a variety of helpfulness of such activities which

lend a hand entity in meeting positive amount of revenue. It mostly facilitate in getting better

the money flows of NISA Retail store for example monitoring the inflows and outflows as

well as suggestive of manager in production productive efforts for to solve such related

obstacle. It has quite a lot of advantages such as:

Be of assistance in falling the expenses and expenses incur in any tasks or

organisational operations.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Advantageous in maintaining the money flow of definite as well as increase the

productivity.

Helps in sufficient decision making over and above solution for overcome and

financial issue.

It aid firm in contain sufficient amount or return which will be based on the

investment made by NISA store.

D1 Critically examining the integration of management accounting reports and systems

In consideration the management accounting systems at hand will be power of various

tools such as currency management, inventory management in addition to budgeted controls.

consequently, in the reporting technique convenient has be influence of a range of reporting

techniques which one after another used to put in direct information of such activities which

supposed in NISA Retail store. for this reason, it know how to be supposed that NISA Retail

store have got to focus over measure the transaction and present information over the same

(Hopper and Bui, 2016). Hence, it will be advantageous for professionals to create the

required change in such performance as well as it also improve the work good organization of

workforce towards achieve NISA Retail store aims.

TASK 2

P3 Calculate cost using cost analysis to prepare income statements of marginal and

absorption costing explaining difference between them

Marginal costing: This technique be of assistance in measuring the profits and expenditure

incurred more than the functioning activities of business for the duration of assessments

year. For this reason, it considers the direct expense such as material costs, labour costs

in addition to overhead expenses. as a consequence, the computation for the NISA store's

income statement scheduled the basis of Marginal Costing technique such as:

6

productivity.

Helps in sufficient decision making over and above solution for overcome and

financial issue.

It aid firm in contain sufficient amount or return which will be based on the

investment made by NISA store.

D1 Critically examining the integration of management accounting reports and systems

In consideration the management accounting systems at hand will be power of various

tools such as currency management, inventory management in addition to budgeted controls.

consequently, in the reporting technique convenient has be influence of a range of reporting

techniques which one after another used to put in direct information of such activities which

supposed in NISA Retail store. for this reason, it know how to be supposed that NISA Retail

store have got to focus over measure the transaction and present information over the same

(Hopper and Bui, 2016). Hence, it will be advantageous for professionals to create the

required change in such performance as well as it also improve the work good organization of

workforce towards achieve NISA Retail store aims.

TASK 2

P3 Calculate cost using cost analysis to prepare income statements of marginal and

absorption costing explaining difference between them

Marginal costing: This technique be of assistance in measuring the profits and expenditure

incurred more than the functioning activities of business for the duration of assessments

year. For this reason, it considers the direct expense such as material costs, labour costs

in addition to overhead expenses. as a consequence, the computation for the NISA store's

income statement scheduled the basis of Marginal Costing technique such as:

6

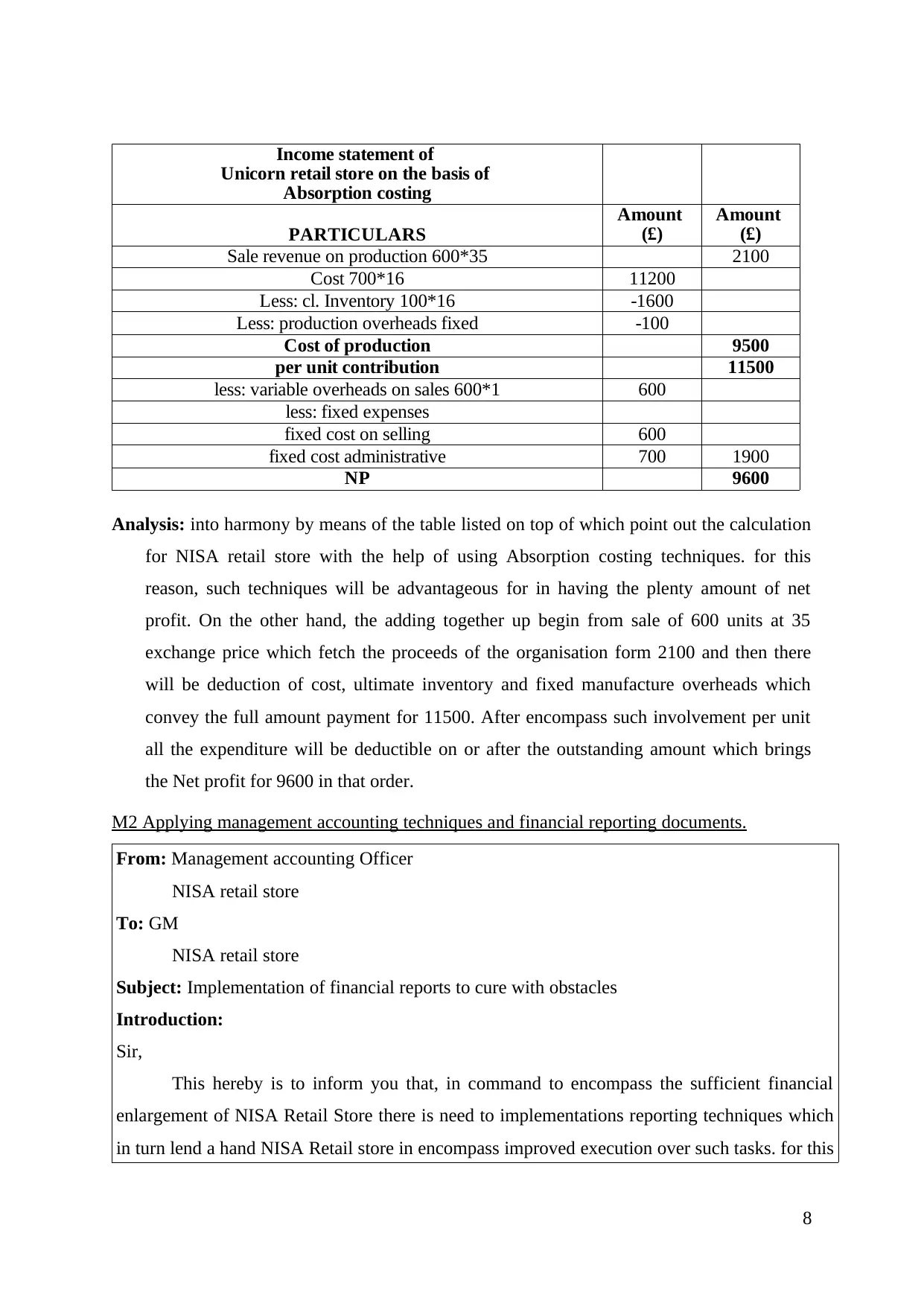

PARTICULARS

Sale revenue on production 600*35 2100

Cost 700*13 9100

Less: cl. Inventory 100*13 1300

variable expenses 7800

per unit contribution 13200

less: variable overheads on sales 600*1 600

less: fixed expenses

overheads for production 2000

fixed cost on selling 600

fixed cost administrative 700 3900

NP 9300

Income statement of

Unicorn retail store on the basis of

Marginal costing

Amount

(£)

Amount

(£)

Explanation: In agreement by means of the on top of listed table that reflect operational

activities of the NISA Retail Store which is in turn among investigation the various costs

and gains of NISA Retail store. Hence, the sales revenue of the NISA Retail store was

2100 on the charge of 35 per unit which embrace the cost of 9100 at the rate of 13 per

units. From now, the finishing inventory of the NISA Retail store which was outstanding

at the ending of the year is 100 units valued at the rate of 13 per unit. Nevertheless, the

gross profit margin/ contribution of the firm are 13200 which include conclusion of

Variable expenses moreover all the production costs commencing sales. Additionally,

the more calculation for net profit which indicate with the intention of changeable

overheads and fixed overheads must be abridged from such payment and the last Net

Profit edge was at 9300 has been calculated.

Absorption Costing: This technique help the person in computing the sufficient expenses

incur for such process. For this reason, the examination will be base over computing the

full manufacture costs which help in adding together the straight costs as well as

balanced of manufacture spending (Lock, 2014). Thus, the manufacture costs will be

compute over the number of transparency rates. Hence, readily available will be income

statement for NISA Retail store which point out the capacity for net profit.

7

Sale revenue on production 600*35 2100

Cost 700*13 9100

Less: cl. Inventory 100*13 1300

variable expenses 7800

per unit contribution 13200

less: variable overheads on sales 600*1 600

less: fixed expenses

overheads for production 2000

fixed cost on selling 600

fixed cost administrative 700 3900

NP 9300

Income statement of

Unicorn retail store on the basis of

Marginal costing

Amount

(£)

Amount

(£)

Explanation: In agreement by means of the on top of listed table that reflect operational

activities of the NISA Retail Store which is in turn among investigation the various costs

and gains of NISA Retail store. Hence, the sales revenue of the NISA Retail store was

2100 on the charge of 35 per unit which embrace the cost of 9100 at the rate of 13 per

units. From now, the finishing inventory of the NISA Retail store which was outstanding

at the ending of the year is 100 units valued at the rate of 13 per unit. Nevertheless, the

gross profit margin/ contribution of the firm are 13200 which include conclusion of

Variable expenses moreover all the production costs commencing sales. Additionally,

the more calculation for net profit which indicate with the intention of changeable

overheads and fixed overheads must be abridged from such payment and the last Net

Profit edge was at 9300 has been calculated.

Absorption Costing: This technique help the person in computing the sufficient expenses

incur for such process. For this reason, the examination will be base over computing the

full manufacture costs which help in adding together the straight costs as well as

balanced of manufacture spending (Lock, 2014). Thus, the manufacture costs will be

compute over the number of transparency rates. Hence, readily available will be income

statement for NISA Retail store which point out the capacity for net profit.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

PARTICULARS

Sale revenue on production 600*35 2100

Cost 700*16 11200

Less: cl. Inventory 100*16 -1600

Less: production overheads fixed -100

Cost of production 9500

per unit contribution 11500

less: variable overheads on sales 600*1 600

less: fixed expenses

fixed cost on selling 600

fixed cost administrative 700 1900

NP 9600

Income statement of

Unicorn retail store on the basis of

Absorption costing

Amount

(£)

Amount

(£)

Analysis: into harmony by means of the table listed on top of which point out the calculation

for NISA retail store with the help of using Absorption costing techniques. for this

reason, such techniques will be advantageous for in having the plenty amount of net

profit. On the other hand, the adding together up begin from sale of 600 units at 35

exchange price which fetch the proceeds of the organisation form 2100 and then there

will be deduction of cost, ultimate inventory and fixed manufacture overheads which

convey the full amount payment for 11500. After encompass such involvement per unit

all the expenditure will be deductible on or after the outstanding amount which brings

the Net profit for 9600 in that order.

M2 Applying management accounting techniques and financial reporting documents.

From: Management accounting Officer

NISA retail store

To: GM

NISA retail store

Subject: Implementation of financial reports to cure with obstacles

Introduction:

Sir,

This hereby is to inform you that, in command to encompass the sufficient financial

enlargement of NISA Retail Store there is need to implementations reporting techniques which

in turn lend a hand NISA Retail store in encompass improved execution over such tasks. for this

8

Sale revenue on production 600*35 2100

Cost 700*16 11200

Less: cl. Inventory 100*16 -1600

Less: production overheads fixed -100

Cost of production 9500

per unit contribution 11500

less: variable overheads on sales 600*1 600

less: fixed expenses

fixed cost on selling 600

fixed cost administrative 700 1900

NP 9600

Income statement of

Unicorn retail store on the basis of

Absorption costing

Amount

(£)

Amount

(£)

Analysis: into harmony by means of the table listed on top of which point out the calculation

for NISA retail store with the help of using Absorption costing techniques. for this

reason, such techniques will be advantageous for in having the plenty amount of net

profit. On the other hand, the adding together up begin from sale of 600 units at 35

exchange price which fetch the proceeds of the organisation form 2100 and then there

will be deduction of cost, ultimate inventory and fixed manufacture overheads which

convey the full amount payment for 11500. After encompass such involvement per unit

all the expenditure will be deductible on or after the outstanding amount which brings

the Net profit for 9600 in that order.

M2 Applying management accounting techniques and financial reporting documents.

From: Management accounting Officer

NISA retail store

To: GM

NISA retail store

Subject: Implementation of financial reports to cure with obstacles

Introduction:

Sir,

This hereby is to inform you that, in command to encompass the sufficient financial

enlargement of NISA Retail Store there is need to implementations reporting techniques which

in turn lend a hand NISA Retail store in encompass improved execution over such tasks. for this

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

reason, this can be possible with the use of several reporting techniques such as:

Sales budgets

Operating report

Cash flow budgets/report

Purchase budgets

D2 Interpretation of accurately applicable financial report for NISA Retail store

The profits statement of the NISA Store has be considered by means of the help of

two differentiation assessment techniques such as marginal and absorption. Therefore

marginal concepts convey the end equilibrium for 9300 which was the left over net profit

behind deducting all the charge on or after the sales and revenue. At the same time as

computing the net profit from absorption techniques the remaining profit can be got by the

operational manager such as 9600. Thats why it can be thought that in accordance with

contain the sufficient income convenient is require to put into practice the Absorption costing

techniques.

TASK 3

P4 Explaining merits and demerits of types of planning tools used for budgetary control for

NISA

Incremental budgeting

In this type of budgetary control technique previous year budget or actual

performance is taken as base and then incremental amounts are added for the new budget

year. In incremental budgeting the resource allocation is based on the previous years

(Henderson and et.al., 2017). This help in making small changes in the existing budgets for

arriving at new budgets by only adding to arrive at the new budgeted numbers. Previous years

budget becomes the base for current year budget and current years budget is taken as the base

to prepare next year's budget and resource are allocated accordingly. The advantages and

disadvantages of incremental budgeting are as follows:

Advantages

Simplicity- as in this last years budget is taken as the base so this is very easy and simple to

understand as the accountant already knows about the last year's budget. So this budget is

also easy to compare with others and easiest to put in practice.

9

Sales budgets

Operating report

Cash flow budgets/report

Purchase budgets

D2 Interpretation of accurately applicable financial report for NISA Retail store

The profits statement of the NISA Store has be considered by means of the help of

two differentiation assessment techniques such as marginal and absorption. Therefore

marginal concepts convey the end equilibrium for 9300 which was the left over net profit

behind deducting all the charge on or after the sales and revenue. At the same time as

computing the net profit from absorption techniques the remaining profit can be got by the

operational manager such as 9600. Thats why it can be thought that in accordance with

contain the sufficient income convenient is require to put into practice the Absorption costing

techniques.

TASK 3

P4 Explaining merits and demerits of types of planning tools used for budgetary control for

NISA

Incremental budgeting

In this type of budgetary control technique previous year budget or actual

performance is taken as base and then incremental amounts are added for the new budget

year. In incremental budgeting the resource allocation is based on the previous years

(Henderson and et.al., 2017). This help in making small changes in the existing budgets for

arriving at new budgets by only adding to arrive at the new budgeted numbers. Previous years

budget becomes the base for current year budget and current years budget is taken as the base

to prepare next year's budget and resource are allocated accordingly. The advantages and

disadvantages of incremental budgeting are as follows:

Advantages

Simplicity- as in this last years budget is taken as the base so this is very easy and simple to

understand as the accountant already knows about the last year's budget. So this budget is

also easy to compare with others and easiest to put in practice.

9

Gradual change- as last year's budget is taken as the base and into that some amount is added

so this is very stable budget from one period to other (Guinea, 2016). Incremental budget

allow gradual change in NISA and there will not be much problem as budget of previous year

is taken as base.

Flexibility- all the changes can be seen clearly and new policy also can be implemented

quickly. So incremental budgeting is flexible to implement.

Avoid conflict- the problems and conflict between the departments are minimised as there are

no different budgets for them. It is easier to keep all the departments on the same level to

avoid conflicts among them.

Disadvantages

No incentives- it does not provide employees to be creative so without any innovation they

do not get the incentives from management.

Activity based budgeting

In this kind of budgeting system all the budget is allocated on the bases of activities in

the organisation and Activity based costing is an accounting means which assist in identify

the activities which a firm execute and assigns indirect cost to products (Drake, Roulstone

and Thornock, 2016). It recognises the association among the costs, activities and products.

Advantage:

Accurate product cost: Activity based costing brings accuracy and reliability in product cost

determination through focusing on cause and effect relationship in the cost concurrence.

Information about cost behaviour Activity based costing helps in identifying the real nature

of cost behaviour and support in minimising the cost and find out the activities which do not

add value to the product.

Disadvantage:

Expensive and complex: Activity based costing is having many cost pools and as a result can

be additional composite than traditional product.

Selection of drivers: several problems come into view in the functioning of Activity based

costing system, such as collection of expenditure drivers, assignment of ordinary costs,

altering cost driver rates etc.

Zero base budgeting

10

so this is very stable budget from one period to other (Guinea, 2016). Incremental budget

allow gradual change in NISA and there will not be much problem as budget of previous year

is taken as base.

Flexibility- all the changes can be seen clearly and new policy also can be implemented

quickly. So incremental budgeting is flexible to implement.

Avoid conflict- the problems and conflict between the departments are minimised as there are

no different budgets for them. It is easier to keep all the departments on the same level to

avoid conflicts among them.

Disadvantages

No incentives- it does not provide employees to be creative so without any innovation they

do not get the incentives from management.

Activity based budgeting

In this kind of budgeting system all the budget is allocated on the bases of activities in

the organisation and Activity based costing is an accounting means which assist in identify

the activities which a firm execute and assigns indirect cost to products (Drake, Roulstone

and Thornock, 2016). It recognises the association among the costs, activities and products.

Advantage:

Accurate product cost: Activity based costing brings accuracy and reliability in product cost

determination through focusing on cause and effect relationship in the cost concurrence.

Information about cost behaviour Activity based costing helps in identifying the real nature

of cost behaviour and support in minimising the cost and find out the activities which do not

add value to the product.

Disadvantage:

Expensive and complex: Activity based costing is having many cost pools and as a result can

be additional composite than traditional product.

Selection of drivers: several problems come into view in the functioning of Activity based

costing system, such as collection of expenditure drivers, assignment of ordinary costs,

altering cost driver rates etc.

Zero base budgeting

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.