Management Accounting Report: Nisa Retail Case Study Analysis

VerifiedAdded on 2020/09/17

|18

|5456

|49

Report

AI Summary

This report analyzes management accounting principles and their application within the context of Nisa Retail. It begins with an introduction to management accounting, differentiating it from financial accounting, and then delves into the calculation of costs and the preparation of income statements using both marginal and absorption costing techniques. The report explores the role of management accounting systems, highlighting their importance in forecasting, decision-making, and cash flow management. It also examines the principles of management accounting, including influence, relevance, value, and trust, along with various management accounting systems like cost accounting and inventory management. Furthermore, the report covers the integration of management accounting into an organization, the benefits of these systems, and compares different planning tools used in management accounting. It concludes with a discussion of pricing strategies, costing systems, and methods for identifying and resolving financial shortfalls, and the skills required of an effective management accountant, all illustrated through the case study of Nisa Retail.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1: ASSIGNMENT 1.............................................................................................................1

PART A...........................................................................................................................................1

P3. Calculation of costs and preparation of income statement...............................................1

PART B............................................................................................................................................2

P1. Role of Management Accounting System........................................................................2

P2. Principles of Management accounting System................................................................4

M1. Benefits of Management accounting system..................................................................5

D1. Integration of management accounting into the organisation.........................................6

M2. Techniques and methods used in management accounting:...........................................8

TASK 2: ASSIGNMENT 2.............................................................................................................8

PART C............................................................................................................................................8

P4 Comparing and contrasting three planning tools which are used under management

accounting...............................................................................................................................8

M3 Pricing strategies as well as common costing systems..................................................10

PART D.........................................................................................................................................11

P5 Comparing different ways through which financial shortfalls identified and resolved in

firm.......................................................................................................................................11

M4 Skills of an effective management accountant...............................................................13

D3 Effective strategies and systems.....................................................................................14

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................16

INTRODUCTION...........................................................................................................................1

TASK 1: ASSIGNMENT 1.............................................................................................................1

PART A...........................................................................................................................................1

P3. Calculation of costs and preparation of income statement...............................................1

PART B............................................................................................................................................2

P1. Role of Management Accounting System........................................................................2

P2. Principles of Management accounting System................................................................4

M1. Benefits of Management accounting system..................................................................5

D1. Integration of management accounting into the organisation.........................................6

M2. Techniques and methods used in management accounting:...........................................8

TASK 2: ASSIGNMENT 2.............................................................................................................8

PART C............................................................................................................................................8

P4 Comparing and contrasting three planning tools which are used under management

accounting...............................................................................................................................8

M3 Pricing strategies as well as common costing systems..................................................10

PART D.........................................................................................................................................11

P5 Comparing different ways through which financial shortfalls identified and resolved in

firm.......................................................................................................................................11

M4 Skills of an effective management accountant...............................................................13

D3 Effective strategies and systems.....................................................................................14

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................16

INTRODUCTION

Management accounting as the name suggests is basically for the use of management.

Management accounting uses accounting principles, this aids them in managing the activities and

performance of control functions. This includes management accounting tools that helps

management in making future economic decisions. The present report will shed some light on

practical approach of management accounting by preparing income statement using marginal and

absorption costing techniques along with the description of various types costing system.

Management accounting is mostly confused with financial accounting, in this report a clear

difference between management accounting and financial accounting has been provided. The

report also includes planning tools that are used for budgetary control with its advantages and

disadvantages. For the purpose of pricing and costing goods and services, management can also

use various pricing in costing system explained in this report. The present report also explains

the use of management accounting in responding to various financial problems. Management

accounting is the combination of accounting, finance, business skills, techniques and

management that adds real value to the organisation. For the better understanding of the study,

SME Nisa Retail store has been taken into account.

TASK 1: ASSIGNMENT 1

PART A

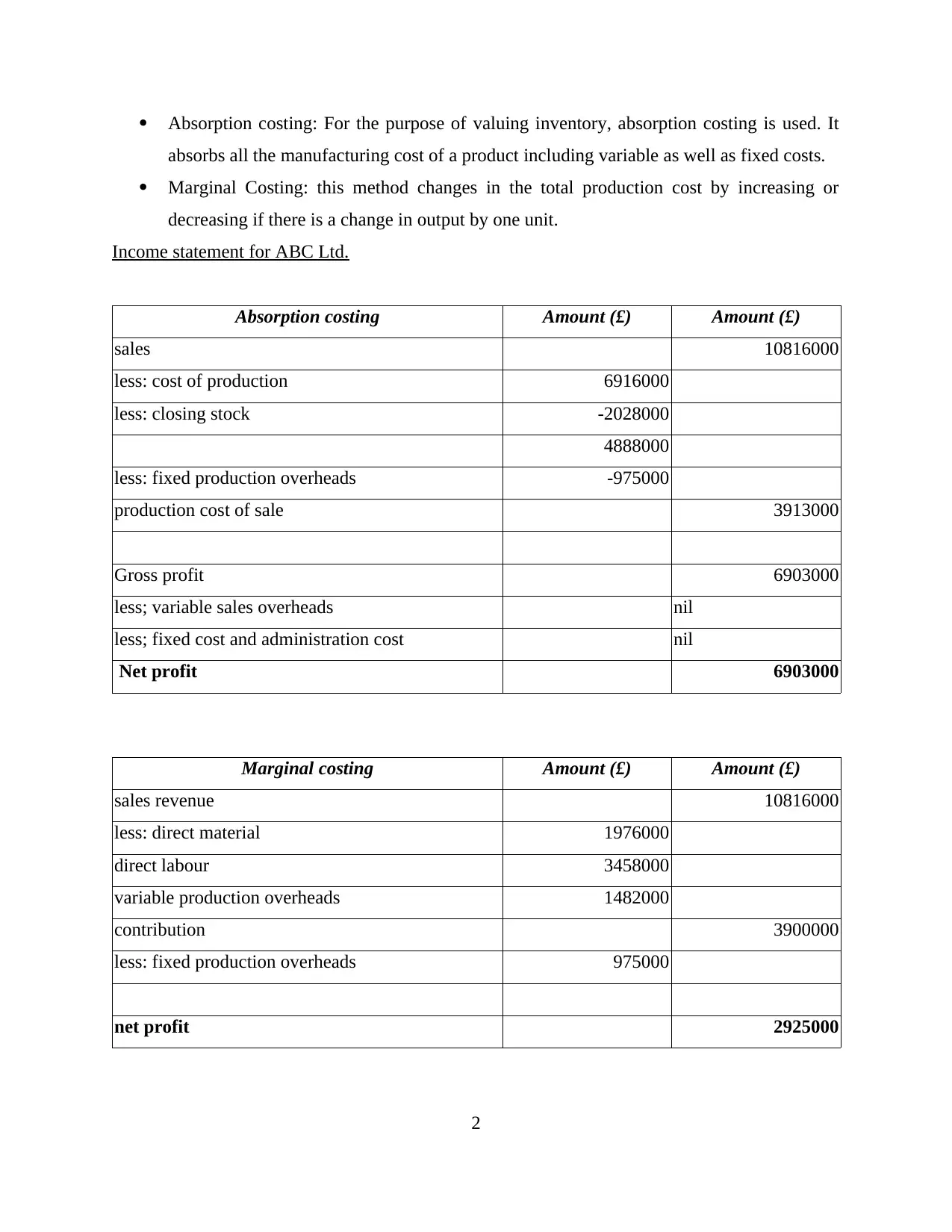

P3. Calculation of costs and preparation of income statement

Cost is an amount that is given up for the exchange of receiving an asset. It includes all

the related amounts of an asset to make that asset ready for use. Accounting of cost aids to

decision making by providing the relevant information of cost to the management. For the

purpose of calculating the cost of the products, Nisa Retail have a choice to adopt any method

from marginal costing and absorption costing.

Cost- volume Profit: Cost volume profit analysis helps in determining the impact of

changes in the cost and volume to the operating income of the organisation (Joshi and Li,

2016).

Flexible budgeting: flexible budgeting refers to the preparation of flexible budget that

adjusts the changes in the volume of the activities.

1

Management accounting as the name suggests is basically for the use of management.

Management accounting uses accounting principles, this aids them in managing the activities and

performance of control functions. This includes management accounting tools that helps

management in making future economic decisions. The present report will shed some light on

practical approach of management accounting by preparing income statement using marginal and

absorption costing techniques along with the description of various types costing system.

Management accounting is mostly confused with financial accounting, in this report a clear

difference between management accounting and financial accounting has been provided. The

report also includes planning tools that are used for budgetary control with its advantages and

disadvantages. For the purpose of pricing and costing goods and services, management can also

use various pricing in costing system explained in this report. The present report also explains

the use of management accounting in responding to various financial problems. Management

accounting is the combination of accounting, finance, business skills, techniques and

management that adds real value to the organisation. For the better understanding of the study,

SME Nisa Retail store has been taken into account.

TASK 1: ASSIGNMENT 1

PART A

P3. Calculation of costs and preparation of income statement

Cost is an amount that is given up for the exchange of receiving an asset. It includes all

the related amounts of an asset to make that asset ready for use. Accounting of cost aids to

decision making by providing the relevant information of cost to the management. For the

purpose of calculating the cost of the products, Nisa Retail have a choice to adopt any method

from marginal costing and absorption costing.

Cost- volume Profit: Cost volume profit analysis helps in determining the impact of

changes in the cost and volume to the operating income of the organisation (Joshi and Li,

2016).

Flexible budgeting: flexible budgeting refers to the preparation of flexible budget that

adjusts the changes in the volume of the activities.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Absorption costing: For the purpose of valuing inventory, absorption costing is used. It

absorbs all the manufacturing cost of a product including variable as well as fixed costs.

Marginal Costing: this method changes in the total production cost by increasing or

decreasing if there is a change in output by one unit.

Income statement for ABC Ltd.

Absorption costing Amount (£) Amount (£)

sales 10816000

less: cost of production 6916000

less: closing stock -2028000

4888000

less: fixed production overheads -975000

production cost of sale 3913000

Gross profit 6903000

less; variable sales overheads nil

less; fixed cost and administration cost nil

Net profit 6903000

Marginal costing Amount (£) Amount (£)

sales revenue 10816000

less: direct material 1976000

direct labour 3458000

variable production overheads 1482000

contribution 3900000

less: fixed production overheads 975000

net profit 2925000

2

absorbs all the manufacturing cost of a product including variable as well as fixed costs.

Marginal Costing: this method changes in the total production cost by increasing or

decreasing if there is a change in output by one unit.

Income statement for ABC Ltd.

Absorption costing Amount (£) Amount (£)

sales 10816000

less: cost of production 6916000

less: closing stock -2028000

4888000

less: fixed production overheads -975000

production cost of sale 3913000

Gross profit 6903000

less; variable sales overheads nil

less; fixed cost and administration cost nil

Net profit 6903000

Marginal costing Amount (£) Amount (£)

sales revenue 10816000

less: direct material 1976000

direct labour 3458000

variable production overheads 1482000

contribution 3900000

less: fixed production overheads 975000

net profit 2925000

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Reason between the results of two is because, under absorption costing all the costs are

included while in marginal costing only variable costs are considered.

PART B

P1. Role of Management Accounting System

Management accounting or managerial accounting are the same thing. These refers to the

decision making tool that is used by management. This helps in assisting the management in

achieving control over the organisation and better planning. Management accounting provides

timely and accurate financial and statistical information to the management for the purpose of

short-term and long-term decisions by preparing management reports and accounts. Following

are the roles of management accounting in Nisa Retail:

Helps in forecasting the future: Management accounting helps in forecasting that aids in

decision making like whether the company need to make more investments or is there is a

need to diversify the products or should acquire or merge with another company (Groot

and Selto, 2013).

Make or Buy Decisions: It also helps in determining whether it is cheaper to produce a

product or it will be economical to buy from the outside market. Management accounting

helps in making insights for decision making at both the level i.e. strategic and

operational level.

Cash Flow Forecast: Impact of flow of cash to the business is essential. Therefore, it

helps in predicting the cash flow. This includes answer to the questions like the estimated

cost of future, increase or decrease of revenue in the future and the source of revenue.

Management accounting tools includes budgets and trend charts, these are used to decide

the allocation of resources and money.

Rate of return: Nisa Retail needs to analyse the expected rate of return before

commencing any project that requires heavy investments. Management accounting tools

helps the management in choosing the best investment opportunity that will provide

better profitability (Khodzytska and Ivchenko, 2014). It also helps in determining the

break even sales and in how much time the company will be able to reach its break even

point of sales.

3

included while in marginal costing only variable costs are considered.

PART B

P1. Role of Management Accounting System

Management accounting or managerial accounting are the same thing. These refers to the

decision making tool that is used by management. This helps in assisting the management in

achieving control over the organisation and better planning. Management accounting provides

timely and accurate financial and statistical information to the management for the purpose of

short-term and long-term decisions by preparing management reports and accounts. Following

are the roles of management accounting in Nisa Retail:

Helps in forecasting the future: Management accounting helps in forecasting that aids in

decision making like whether the company need to make more investments or is there is a

need to diversify the products or should acquire or merge with another company (Groot

and Selto, 2013).

Make or Buy Decisions: It also helps in determining whether it is cheaper to produce a

product or it will be economical to buy from the outside market. Management accounting

helps in making insights for decision making at both the level i.e. strategic and

operational level.

Cash Flow Forecast: Impact of flow of cash to the business is essential. Therefore, it

helps in predicting the cash flow. This includes answer to the questions like the estimated

cost of future, increase or decrease of revenue in the future and the source of revenue.

Management accounting tools includes budgets and trend charts, these are used to decide

the allocation of resources and money.

Rate of return: Nisa Retail needs to analyse the expected rate of return before

commencing any project that requires heavy investments. Management accounting tools

helps the management in choosing the best investment opportunity that will provide

better profitability (Khodzytska and Ivchenko, 2014). It also helps in determining the

break even sales and in how much time the company will be able to reach its break even

point of sales.

3

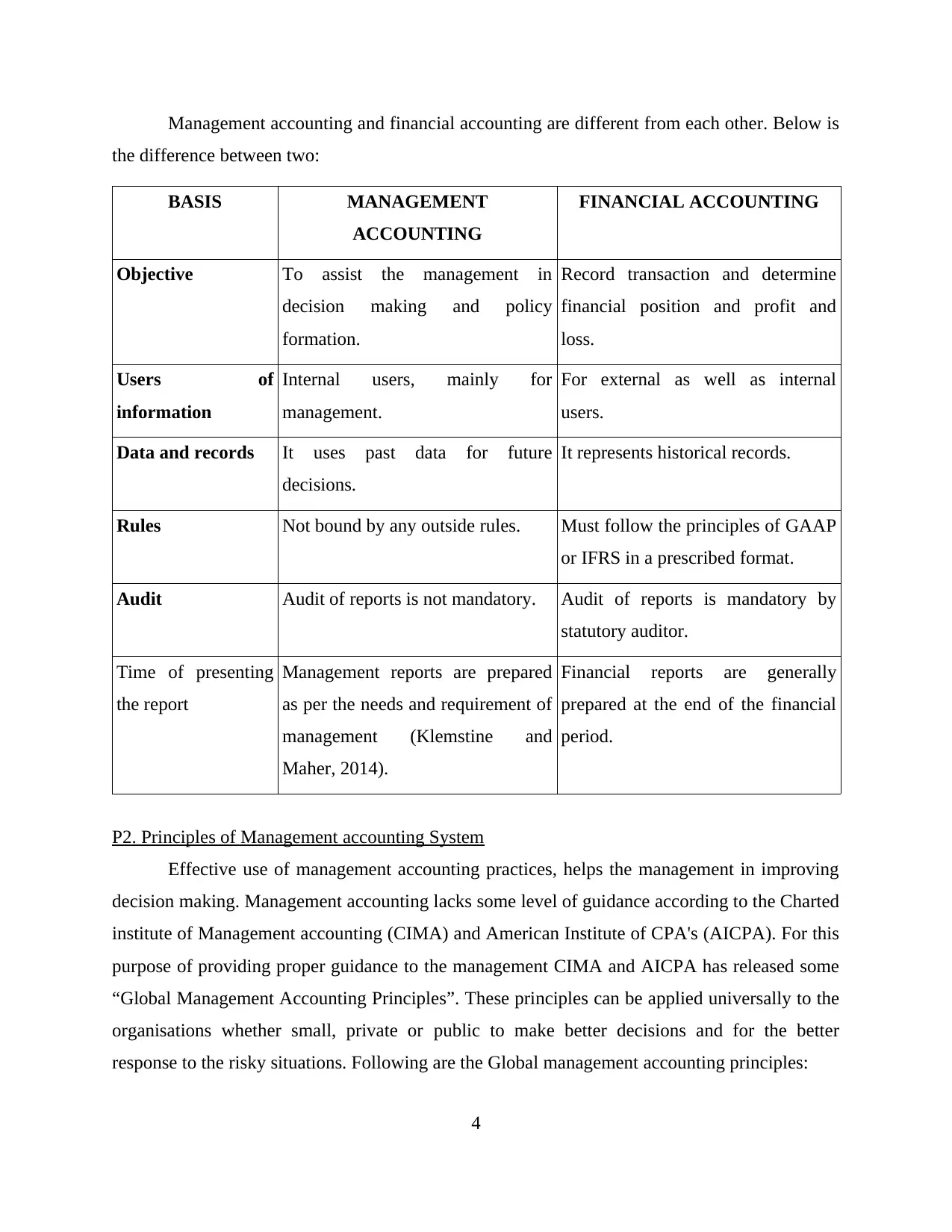

Management accounting and financial accounting are different from each other. Below is

the difference between two:

BASIS MANAGEMENT

ACCOUNTING

FINANCIAL ACCOUNTING

Objective To assist the management in

decision making and policy

formation.

Record transaction and determine

financial position and profit and

loss.

Users of

information

Internal users, mainly for

management.

For external as well as internal

users.

Data and records It uses past data for future

decisions.

It represents historical records.

Rules Not bound by any outside rules. Must follow the principles of GAAP

or IFRS in a prescribed format.

Audit Audit of reports is not mandatory. Audit of reports is mandatory by

statutory auditor.

Time of presenting

the report

Management reports are prepared

as per the needs and requirement of

management (Klemstine and

Maher, 2014).

Financial reports are generally

prepared at the end of the financial

period.

P2. Principles of Management accounting System

Effective use of management accounting practices, helps the management in improving

decision making. Management accounting lacks some level of guidance according to the Charted

institute of Management accounting (CIMA) and American Institute of CPA's (AICPA). For this

purpose of providing proper guidance to the management CIMA and AICPA has released some

“Global Management Accounting Principles”. These principles can be applied universally to the

organisations whether small, private or public to make better decisions and for the better

response to the risky situations. Following are the Global management accounting principles:

4

the difference between two:

BASIS MANAGEMENT

ACCOUNTING

FINANCIAL ACCOUNTING

Objective To assist the management in

decision making and policy

formation.

Record transaction and determine

financial position and profit and

loss.

Users of

information

Internal users, mainly for

management.

For external as well as internal

users.

Data and records It uses past data for future

decisions.

It represents historical records.

Rules Not bound by any outside rules. Must follow the principles of GAAP

or IFRS in a prescribed format.

Audit Audit of reports is not mandatory. Audit of reports is mandatory by

statutory auditor.

Time of presenting

the report

Management reports are prepared

as per the needs and requirement of

management (Klemstine and

Maher, 2014).

Financial reports are generally

prepared at the end of the financial

period.

P2. Principles of Management accounting System

Effective use of management accounting practices, helps the management in improving

decision making. Management accounting lacks some level of guidance according to the Charted

institute of Management accounting (CIMA) and American Institute of CPA's (AICPA). For this

purpose of providing proper guidance to the management CIMA and AICPA has released some

“Global Management Accounting Principles”. These principles can be applied universally to the

organisations whether small, private or public to make better decisions and for the better

response to the risky situations. Following are the Global management accounting principles:

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

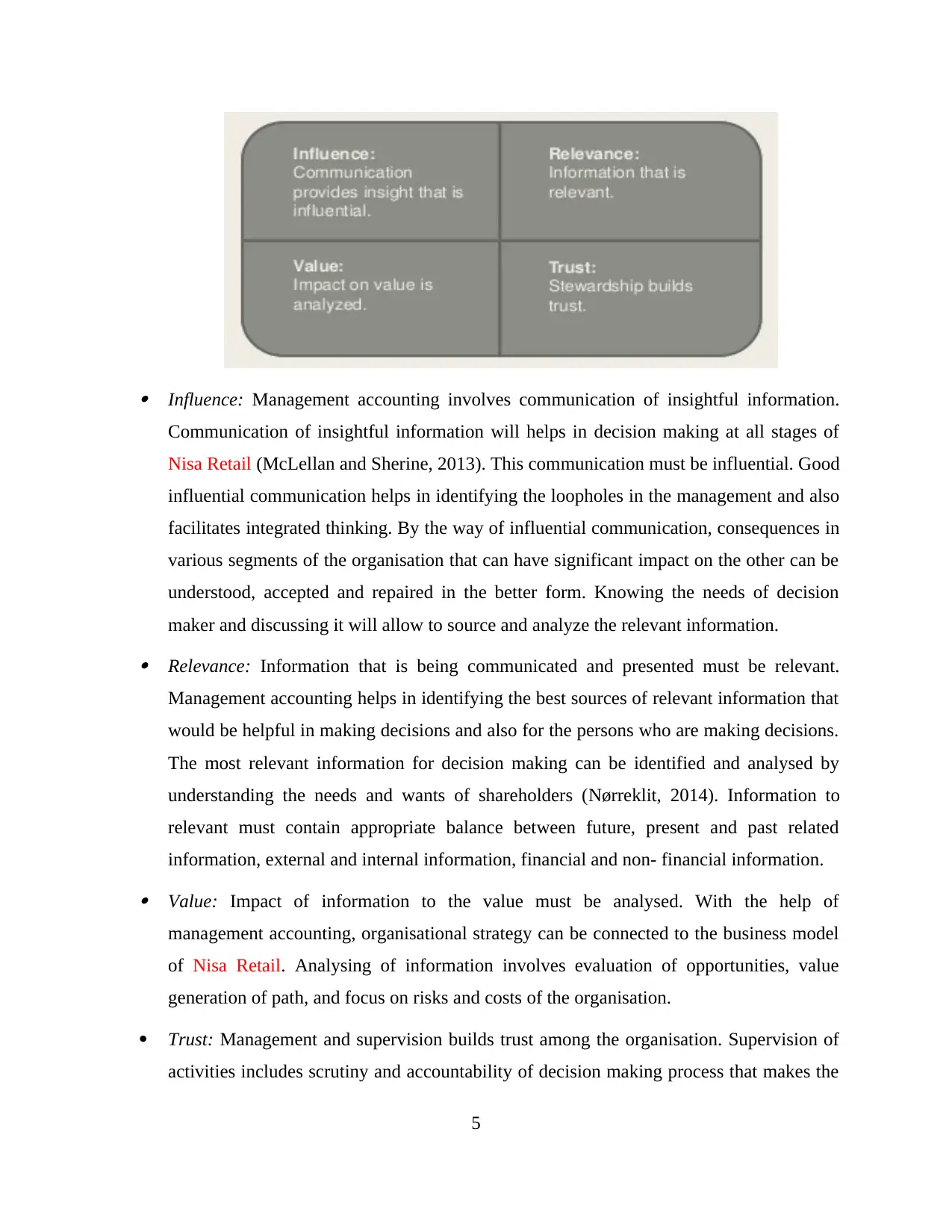

Influence: Management accounting involves communication of insightful information.

Communication of insightful information will helps in decision making at all stages of

Nisa Retail (McLellan and Sherine, 2013). This communication must be influential. Good

influential communication helps in identifying the loopholes in the management and also

facilitates integrated thinking. By the way of influential communication, consequences in

various segments of the organisation that can have significant impact on the other can be

understood, accepted and repaired in the better form. Knowing the needs of decision

maker and discussing it will allow to source and analyze the relevant information. Relevance: Information that is being communicated and presented must be relevant.

Management accounting helps in identifying the best sources of relevant information that

would be helpful in making decisions and also for the persons who are making decisions.

The most relevant information for decision making can be identified and analysed by

understanding the needs and wants of shareholders (Nørreklit, 2014). Information to

relevant must contain appropriate balance between future, present and past related

information, external and internal information, financial and non- financial information. Value: Impact of information to the value must be analysed. With the help of

management accounting, organisational strategy can be connected to the business model

of Nisa Retail. Analysing of information involves evaluation of opportunities, value

generation of path, and focus on risks and costs of the organisation.

Trust: Management and supervision builds trust among the organisation. Supervision of

activities includes scrutiny and accountability of decision making process that makes the

5

Communication of insightful information will helps in decision making at all stages of

Nisa Retail (McLellan and Sherine, 2013). This communication must be influential. Good

influential communication helps in identifying the loopholes in the management and also

facilitates integrated thinking. By the way of influential communication, consequences in

various segments of the organisation that can have significant impact on the other can be

understood, accepted and repaired in the better form. Knowing the needs of decision

maker and discussing it will allow to source and analyze the relevant information. Relevance: Information that is being communicated and presented must be relevant.

Management accounting helps in identifying the best sources of relevant information that

would be helpful in making decisions and also for the persons who are making decisions.

The most relevant information for decision making can be identified and analysed by

understanding the needs and wants of shareholders (Nørreklit, 2014). Information to

relevant must contain appropriate balance between future, present and past related

information, external and internal information, financial and non- financial information. Value: Impact of information to the value must be analysed. With the help of

management accounting, organisational strategy can be connected to the business model

of Nisa Retail. Analysing of information involves evaluation of opportunities, value

generation of path, and focus on risks and costs of the organisation.

Trust: Management and supervision builds trust among the organisation. Supervision of

activities includes scrutiny and accountability of decision making process that makes the

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

process more objective. Management accounting makes a balance between short-term

organisational interests and long-run interests of stakeholders that increases the trust and

credibility (Ward, 2012).

M1. Benefits of Management accounting system

Before evaluating the benefits of management accounting system, types of management

accounting system must be known. Following are the different types of management accounting

system that can be used by Nisa Retail:

Cost- accounting system: For the purpose of reporting accurate cost and amounts to the

financial statements, cost accounting is used which includes methods of evaluating costs

of products and services. It is also known as product costing system. Basically, cost

accounting system is used by the management in order to estimate the cost of products

and services, control of cost and for the valuation of inventories. It also helps in

identifying the profitable operations and non profitable operations of the organisation by

estimating the actual cost of products.

Inventory management system: Inventory management system helps to Nisa retail in

controlling and supervising the stock orders and storage management of finished goods

and raw material. Unlike the old times, the inventory management system in today's time

can be managed by any available inventory management software (Weil, Schipper and

Francis, 2013.).

Job costing system: Job costing system accumulates all the manufacturing cost and then

assign this manufacturing cost to the individual products or batches of products. This

method is used where there are significant differences in the manufactured products.

Price optimising system: A Mathematical system is used in order to calculate the

variations among the demand of product at different price levels. Information derived

from the mathematical system is then combined with the inventory levels and the

information of cost to provide the best price of the product.

Benefits of these accounting systems to Nisa retail store:

These accounting systems will help the management in estimating the cost of their

products and will also help in identifying the profitable operations of the company.

6

organisational interests and long-run interests of stakeholders that increases the trust and

credibility (Ward, 2012).

M1. Benefits of Management accounting system

Before evaluating the benefits of management accounting system, types of management

accounting system must be known. Following are the different types of management accounting

system that can be used by Nisa Retail:

Cost- accounting system: For the purpose of reporting accurate cost and amounts to the

financial statements, cost accounting is used which includes methods of evaluating costs

of products and services. It is also known as product costing system. Basically, cost

accounting system is used by the management in order to estimate the cost of products

and services, control of cost and for the valuation of inventories. It also helps in

identifying the profitable operations and non profitable operations of the organisation by

estimating the actual cost of products.

Inventory management system: Inventory management system helps to Nisa retail in

controlling and supervising the stock orders and storage management of finished goods

and raw material. Unlike the old times, the inventory management system in today's time

can be managed by any available inventory management software (Weil, Schipper and

Francis, 2013.).

Job costing system: Job costing system accumulates all the manufacturing cost and then

assign this manufacturing cost to the individual products or batches of products. This

method is used where there are significant differences in the manufactured products.

Price optimising system: A Mathematical system is used in order to calculate the

variations among the demand of product at different price levels. Information derived

from the mathematical system is then combined with the inventory levels and the

information of cost to provide the best price of the product.

Benefits of these accounting systems to Nisa retail store:

These accounting systems will help the management in estimating the cost of their

products and will also help in identifying the profitable operations of the company.

6

Management accounting system will enable the management to manage the inventory.

Availability of the volume of finished goods and raw material can also be determined.

Actual manufacturing cost of different products of different segments can also be known

(Weygandt, Kimmel and Kieso, 2015).

D1. Integration of management accounting into the organisation

Nisa Retail can integrate Management accounting by:

Price setting

Cost centres

Decision making

Departmental Budget

Central Budget

The information present in the financial report must be relevant and understandable to its

users. Along with the quantitative characteristics, information must also contain some qualitative

characteristics. Qualitative characteristics of information includes:

Understandability: The information presented in the report must be in such a form that could be

understandable. A financial report having no understandability would be of no use to both

internal users and external users (Zimmerman and Yahya-Zadeh, 2011).

Reliability: The information must be reliable to the organisation and not hypothetical. Only

reliable information can present the actual view of the organisation.

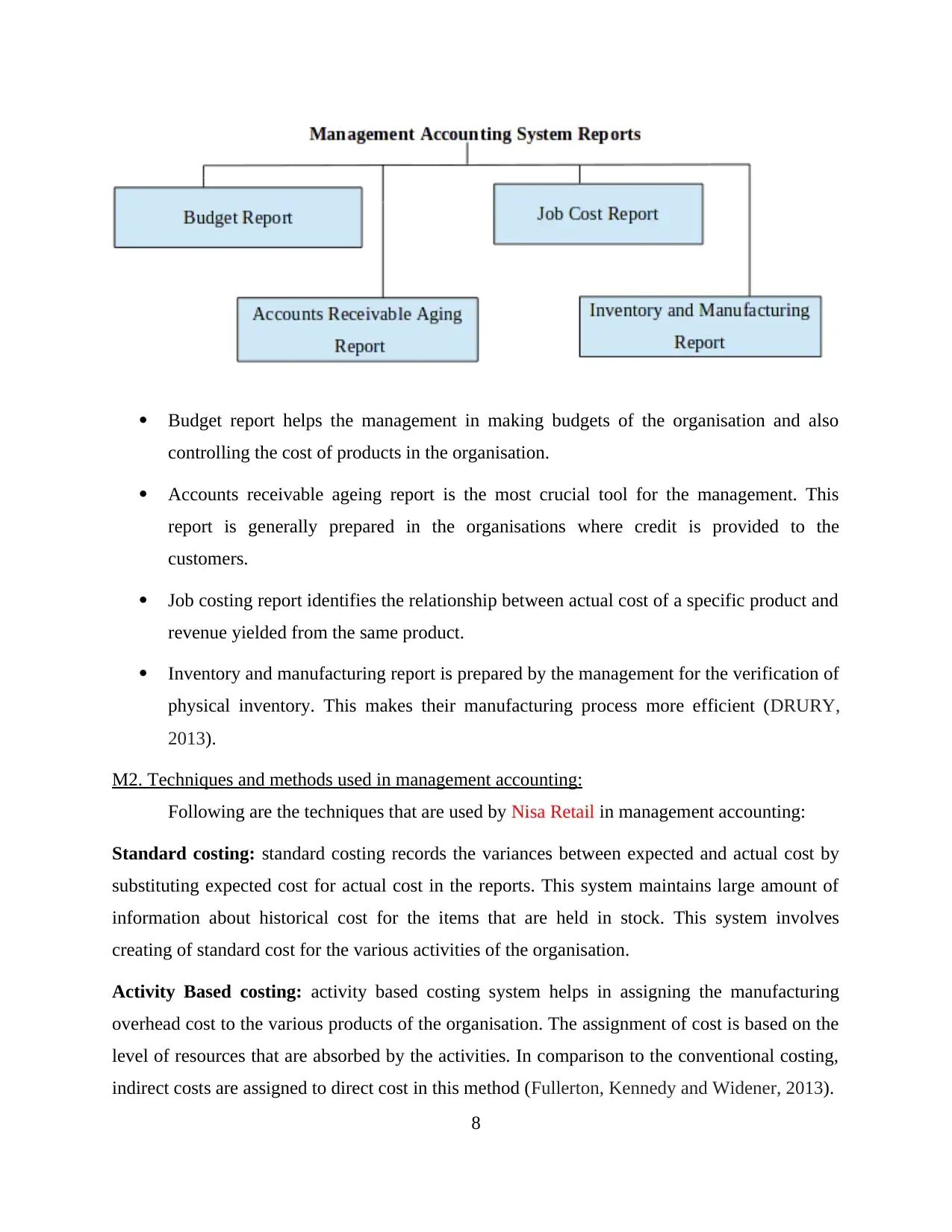

Managerial accounting reports can be of various types:

7

Availability of the volume of finished goods and raw material can also be determined.

Actual manufacturing cost of different products of different segments can also be known

(Weygandt, Kimmel and Kieso, 2015).

D1. Integration of management accounting into the organisation

Nisa Retail can integrate Management accounting by:

Price setting

Cost centres

Decision making

Departmental Budget

Central Budget

The information present in the financial report must be relevant and understandable to its

users. Along with the quantitative characteristics, information must also contain some qualitative

characteristics. Qualitative characteristics of information includes:

Understandability: The information presented in the report must be in such a form that could be

understandable. A financial report having no understandability would be of no use to both

internal users and external users (Zimmerman and Yahya-Zadeh, 2011).

Reliability: The information must be reliable to the organisation and not hypothetical. Only

reliable information can present the actual view of the organisation.

Managerial accounting reports can be of various types:

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Budget report helps the management in making budgets of the organisation and also

controlling the cost of products in the organisation.

Accounts receivable ageing report is the most crucial tool for the management. This

report is generally prepared in the organisations where credit is provided to the

customers.

Job costing report identifies the relationship between actual cost of a specific product and

revenue yielded from the same product.

Inventory and manufacturing report is prepared by the management for the verification of

physical inventory. This makes their manufacturing process more efficient (DRURY,

2013).

M2. Techniques and methods used in management accounting:

Following are the techniques that are used by Nisa Retail in management accounting:

Standard costing: standard costing records the variances between expected and actual cost by

substituting expected cost for actual cost in the reports. This system maintains large amount of

information about historical cost for the items that are held in stock. This system involves

creating of standard cost for the various activities of the organisation.

Activity Based costing: activity based costing system helps in assigning the manufacturing

overhead cost to the various products of the organisation. The assignment of cost is based on the

level of resources that are absorbed by the activities. In comparison to the conventional costing,

indirect costs are assigned to direct cost in this method (Fullerton, Kennedy and Widener, 2013).

8

controlling the cost of products in the organisation.

Accounts receivable ageing report is the most crucial tool for the management. This

report is generally prepared in the organisations where credit is provided to the

customers.

Job costing report identifies the relationship between actual cost of a specific product and

revenue yielded from the same product.

Inventory and manufacturing report is prepared by the management for the verification of

physical inventory. This makes their manufacturing process more efficient (DRURY,

2013).

M2. Techniques and methods used in management accounting:

Following are the techniques that are used by Nisa Retail in management accounting:

Standard costing: standard costing records the variances between expected and actual cost by

substituting expected cost for actual cost in the reports. This system maintains large amount of

information about historical cost for the items that are held in stock. This system involves

creating of standard cost for the various activities of the organisation.

Activity Based costing: activity based costing system helps in assigning the manufacturing

overhead cost to the various products of the organisation. The assignment of cost is based on the

level of resources that are absorbed by the activities. In comparison to the conventional costing,

indirect costs are assigned to direct cost in this method (Fullerton, Kennedy and Widener, 2013).

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 2: ASSIGNMENT 2

PART C

P4 Comparing and contrasting three planning tools which are used under management

accounting

In the workplace of each and every organisation, there are different systems of

management accounting are applied on the workplace. Further, when any kind of financial plan

is required to prepare and implement in the business environment then various tools and

techniques are taken into account. In the present case scenario, Nisa retail enterprise is used

which has presence in the retail industry of UK. Further, it is one kind of small business due to

which operates in the UK only rather than international level. From various planning tools it

considers mainly three which are related to the budget. It is a statement through which financial

information forecasted for the upcoming year which include cost, cash, incomes, expenditures,

material purchase, production etc. Nisa retail store uses cash, sales and production budgets under

the management accounting which are stated below:

Cash budget

The tool in which cash incomes and payments for the next year ending are analysed in

proper way is known as cash budget. Apart from this, it reflects about the cash availability in the

upcoming accounting period which helps to make highly fruitful financial plan. If the

management of Nisa retail store founds that cash is available in adequate or enough proportion

then will increase expenses in the financial plan. On the other hand side, if position of cash is in

inverse condition or low then not make huge expenses in the firm. It helps to the management for

allocating financial resources in adequate way among each and every business function like

marketing, HR, IT, R&D, production etc (Merits and Demerits of Cash Budget, 2016). Further,

decisions related to fund raising and source of finance is also properly taken out using cash

budget. However, time taken for implementation and accomplish the target of cash budget is

huge which is key issue associated with this tool.

Sales budget

Second planning tool used by Nisa retail store is sales budget which provides amount

which must be earned by the firm for next financial year. Further, it provides one kind of revenue

9

PART C

P4 Comparing and contrasting three planning tools which are used under management

accounting

In the workplace of each and every organisation, there are different systems of

management accounting are applied on the workplace. Further, when any kind of financial plan

is required to prepare and implement in the business environment then various tools and

techniques are taken into account. In the present case scenario, Nisa retail enterprise is used

which has presence in the retail industry of UK. Further, it is one kind of small business due to

which operates in the UK only rather than international level. From various planning tools it

considers mainly three which are related to the budget. It is a statement through which financial

information forecasted for the upcoming year which include cost, cash, incomes, expenditures,

material purchase, production etc. Nisa retail store uses cash, sales and production budgets under

the management accounting which are stated below:

Cash budget

The tool in which cash incomes and payments for the next year ending are analysed in

proper way is known as cash budget. Apart from this, it reflects about the cash availability in the

upcoming accounting period which helps to make highly fruitful financial plan. If the

management of Nisa retail store founds that cash is available in adequate or enough proportion

then will increase expenses in the financial plan. On the other hand side, if position of cash is in

inverse condition or low then not make huge expenses in the firm. It helps to the management for

allocating financial resources in adequate way among each and every business function like

marketing, HR, IT, R&D, production etc (Merits and Demerits of Cash Budget, 2016). Further,

decisions related to fund raising and source of finance is also properly taken out using cash

budget. However, time taken for implementation and accomplish the target of cash budget is

huge which is key issue associated with this tool.

Sales budget

Second planning tool used by Nisa retail store is sales budget which provides amount

which must be earned by the firm for next financial year. Further, it provides one kind of revenue

9

target to the company which mandatory to meet in the upcoming period. Until and unless this

budgeted value is not achieved then it can be said that firm performs poor. Apart from this,

selling price is also determined with the help of sales budget of each and every unit produced or

sold in the workplace. It consists with basically three factors which are like selling price,

production units and closing stock. At the time of preparing plan about the sales generation then

market conditions are identified by the Nisa retail store.

Production budget

Apart from sales and cash, the third or last planning tool used by Nisa retail store is

production budget which gives target for manufacturing and selling specific units. On the basis

of this, the management clearly able to determine total units which must be produced in next

financial period (Nuhu and et.al., 2017). Under this combination of two values is considered

which is closing stock of finished products and sales or demand forecasted from market research.

When the cited firm apply this planning method in the workplace then able to reduce

unproductive expenses and utilise resources appropriately.

Comparison among cash, sales and production budget

When comparing to all the above stated planning techniques undertaken in management

accounting then all have nature of estimations for next year. With the help of these all the ways,

the Nisa retail store able to make targets for next financial year which will help to fulfil desired

objectives in adequate manner. Further, these are interrelated with each other because when these

combined and executed in workplace then support to meet the aims. Apart from this, to forecast

important financial information like cash availability, revenue and production units these are

highly supportive. Moreover, these all the tools have high degree similarity in specific aspect

which is forecast and estimate data for the next fiscal year.

Contrast between cash, sales and production budget

When considering to the contradiction then these all the planning tools differ with each

another. The cash budget shows about only cash position and availability of the liquidity in the

workplace of Nisa retail store. The second planning tool undertaken provide information about

the particular amount which required to generate by the firm in next year (Messner, 2016). These

both are totally different from each another and only one is not enough for preparing the

10

budgeted value is not achieved then it can be said that firm performs poor. Apart from this,

selling price is also determined with the help of sales budget of each and every unit produced or

sold in the workplace. It consists with basically three factors which are like selling price,

production units and closing stock. At the time of preparing plan about the sales generation then

market conditions are identified by the Nisa retail store.

Production budget

Apart from sales and cash, the third or last planning tool used by Nisa retail store is

production budget which gives target for manufacturing and selling specific units. On the basis

of this, the management clearly able to determine total units which must be produced in next

financial period (Nuhu and et.al., 2017). Under this combination of two values is considered

which is closing stock of finished products and sales or demand forecasted from market research.

When the cited firm apply this planning method in the workplace then able to reduce

unproductive expenses and utilise resources appropriately.

Comparison among cash, sales and production budget

When comparing to all the above stated planning techniques undertaken in management

accounting then all have nature of estimations for next year. With the help of these all the ways,

the Nisa retail store able to make targets for next financial year which will help to fulfil desired

objectives in adequate manner. Further, these are interrelated with each other because when these

combined and executed in workplace then support to meet the aims. Apart from this, to forecast

important financial information like cash availability, revenue and production units these are

highly supportive. Moreover, these all the tools have high degree similarity in specific aspect

which is forecast and estimate data for the next fiscal year.

Contrast between cash, sales and production budget

When considering to the contradiction then these all the planning tools differ with each

another. The cash budget shows about only cash position and availability of the liquidity in the

workplace of Nisa retail store. The second planning tool undertaken provide information about

the particular amount which required to generate by the firm in next year (Messner, 2016). These

both are totally different from each another and only one is not enough for preparing the

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.