Management Accounting Report: Nisa Retail's Decision-Making Strategies

VerifiedAdded on 2020/01/07

|16

|5785

|59

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles and their application within Nisa Retail, a small grocery wholesaler. The report begins with an introduction to management accounting, differentiating it from financial accounting and emphasizing its role in internal decision-making. Task 1 focuses on explaining management accounting systems, including cost accounting, job costing, inventory management, and price optimization, along with their essential requirements. It presents distinctive methods for managerial accounting reporting, such as job cost reports, inventory management reports, and departmental reports. The report evaluates the benefits of management accounting systems, highlighting how they aid in integrating operational reports, streamlining business activities, and facilitating informed decision-making. Task 2 delves into cost calculation, comparing marginal and absorption costing methods and their impact on income statements. The report also explores the application of management accounting techniques in producing financial reporting documents, including the preparation of income statements using marginal and absorption costing. The report further investigates the integration of management accounting systems and reporting within Nisa's processes, emphasizing the importance of integration for effective operational management. The report then examines planning tools and their advantages and disadvantages, analyzing their use in forecasting and budgeting. The report concludes by evaluating planning tools that could be used for solving financial problems and how Nisa can adopt management accounting systems to respond to financial problems and achieve sustainable success.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION................................................................................................................................3

TASK 1.................................................................................................................................................3

LO1.......................................................................................................................................................3

P1 Explaining the management accounting & give the essential requirement of different MA

system..............................................................................................................................................3

Essential requirement of different MA system................................................................................4

P2 Presenting distinctive methods for the managerial accounting reporting...................................5

M1 Evaluating the benefits of Management accounting systems and their applications in Nisa

Retail store.......................................................................................................................................6

D1 Critically examine how MA systems and MA reporting can be integrated with Nisa’s

processes..........................................................................................................................................6

TASK 2.................................................................................................................................................7

LO2.......................................................................................................................................................7

P3 Cost calculation to prepare an income statement under marginal and absorption costing.........7

M2. Apply a range of management accounting technique & produce financial reporting

document..........................................................................................................................................9

D2 Producing financial reports to apply and interpret data for different activities.......................10

TASK 3...............................................................................................................................................10

LO3.....................................................................................................................................................10

P4 advantage and disadvantage of different types of planning tools.............................................11

M2 Analysis of use of planning tools and application for forecasting budget..............................12

D3 Evaluation of planning tools that could be used for solving financial problem......................12

LO4.....................................................................................................................................................13

P5 Compare how Nisa can adopt MA systems to respond financial problems.............................13

M4 Analysing how MA can lead to resolve financial problems and attain sustainable success. . .14

CONCLUSION..................................................................................................................................14

REFERENCES...................................................................................................................................15

INTRODUCTION................................................................................................................................3

TASK 1.................................................................................................................................................3

LO1.......................................................................................................................................................3

P1 Explaining the management accounting & give the essential requirement of different MA

system..............................................................................................................................................3

Essential requirement of different MA system................................................................................4

P2 Presenting distinctive methods for the managerial accounting reporting...................................5

M1 Evaluating the benefits of Management accounting systems and their applications in Nisa

Retail store.......................................................................................................................................6

D1 Critically examine how MA systems and MA reporting can be integrated with Nisa’s

processes..........................................................................................................................................6

TASK 2.................................................................................................................................................7

LO2.......................................................................................................................................................7

P3 Cost calculation to prepare an income statement under marginal and absorption costing.........7

M2. Apply a range of management accounting technique & produce financial reporting

document..........................................................................................................................................9

D2 Producing financial reports to apply and interpret data for different activities.......................10

TASK 3...............................................................................................................................................10

LO3.....................................................................................................................................................10

P4 advantage and disadvantage of different types of planning tools.............................................11

M2 Analysis of use of planning tools and application for forecasting budget..............................12

D3 Evaluation of planning tools that could be used for solving financial problem......................12

LO4.....................................................................................................................................................13

P5 Compare how Nisa can adopt MA systems to respond financial problems.............................13

M4 Analysing how MA can lead to resolve financial problems and attain sustainable success. . .14

CONCLUSION..................................................................................................................................14

REFERENCES...................................................................................................................................15

INTRODUCTION

Managerial accounting is the procedure of measuring, examining and interpreting the

performance of an organization which aimed at assisting top executives within the firm to make

right decisions. It is different from the financial accounting which purpose is to produce financial

reports like income statement, balance sheet and cash flow statement to measure the profitability,

financial health and cash position. However, MA can be defined as a process of managing business

operational metric and covers various aspects such as cost determination, examining managerial

reports, forecasting through budgets, variance analysis by finding deviations of actual results with

the targets and many others for making on-time decisions to arrive the defined target goals. The

present project report focuses Nisa Retail Limited which is small grocery wholesaler located in UK.

It is a private limited organization whose aim is to deliver best quality of retail services and

competitive food at affordable charges. The proposed assignment will critically examine the role of

managerial accounting information as a decision-making tool for Nisa’s success. Moreover, the

report will also present an in-depth evaluation of MA systems with the advantages and

disadvantages and cost determination through marginal and absorption costing for reaching for the

qualitative decisions.

TASK 1

LO1

P1 Explaining the management accounting & give the essential requirement of different MA system

To: General Manager, Nisa Retail Store Ltd

From: Management Accounting officer

Date: 7th April 2017

Subject: Management accounting (MA) and Management Accounting system (MAS)

Introduction

This report will introduce the management accounting role and importance for the Nisa retail

stores along with the various types of MAS that it can use for the objective of making goal-oriented

decisions.

Management accounting: It consists of preparation, delivering and analysis of the financial

& statistical information to the executives, managers and directors, so that, they can handle short-

term managerial decisions, devise planning & manage business performance. In Nisa retail store, it

is the accountability of the managers to administrate, supervise, monitor and control their

departmental functioning (Bhimani and et.al, 2013). MA provides them relevant or needed

Managerial accounting is the procedure of measuring, examining and interpreting the

performance of an organization which aimed at assisting top executives within the firm to make

right decisions. It is different from the financial accounting which purpose is to produce financial

reports like income statement, balance sheet and cash flow statement to measure the profitability,

financial health and cash position. However, MA can be defined as a process of managing business

operational metric and covers various aspects such as cost determination, examining managerial

reports, forecasting through budgets, variance analysis by finding deviations of actual results with

the targets and many others for making on-time decisions to arrive the defined target goals. The

present project report focuses Nisa Retail Limited which is small grocery wholesaler located in UK.

It is a private limited organization whose aim is to deliver best quality of retail services and

competitive food at affordable charges. The proposed assignment will critically examine the role of

managerial accounting information as a decision-making tool for Nisa’s success. Moreover, the

report will also present an in-depth evaluation of MA systems with the advantages and

disadvantages and cost determination through marginal and absorption costing for reaching for the

qualitative decisions.

TASK 1

LO1

P1 Explaining the management accounting & give the essential requirement of different MA system

To: General Manager, Nisa Retail Store Ltd

From: Management Accounting officer

Date: 7th April 2017

Subject: Management accounting (MA) and Management Accounting system (MAS)

Introduction

This report will introduce the management accounting role and importance for the Nisa retail

stores along with the various types of MAS that it can use for the objective of making goal-oriented

decisions.

Management accounting: It consists of preparation, delivering and analysis of the financial

& statistical information to the executives, managers and directors, so that, they can handle short-

term managerial decisions, devise planning & manage business performance. In Nisa retail store, it

is the accountability of the managers to administrate, supervise, monitor and control their

departmental functioning (Bhimani and et.al, 2013). MA provides them relevant or needed

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

accounting information which assist them in strategy formulation & implementation as well. Now-

a-days, in the competitive challenging world, many-times, managers have to make big decisions

promptly, which cause difficulty for them in analysing and interpreting the data, therefore, they use

MAS to get the required data quickly and examine it for making suitable decisions for the growth.

Cost accounting system: It is essential for the company to estimate their product and

services cost accurately (Saladrigues and Tena, 2017). As its name, the system enables Nisa retail’s

managers to identify the right cost of their retail goods, identifying its trend, inventory &

profitability analysis and making decisions for the cost-control.

Job costing system: It refers to the process of accumulating various cost information that

belonged to a particular job (Fullerton, Kennedy and Widener, 2013). It is mainly helpful to provide

cost information to the consumers for their order placed. It allows Nisa retail store to quote their

goods prices after adding a reasonable return.

Inventory management system: This software enable corporation to track their inventory

levels for the ordering and delivering purpose to satisfy their consumer base. With the help of

managing stock to a right level, Nisa can place order on-time for having adequate inventories in the

warehouse to maintain their stock level.

Price optimisation: This MA system helps retailers to identify that how their clients will

respond at distinctive prices of the goods and services, so that, managers can set right prices to

maximize their operational return (Quattrone, 2016). More importantly, in retail sector, it seems

essential for the marketers to figure out the impact of change in their goods prices on the market

demand in order to fix an optimum price.

Essential requirement of different MA system

Relevant information: Every departmental manager of Nisa retail store i.e. finance,

purchase, sales, marketing, production need relevant information about their cost, revenues and

operational efficiency for performance measurement and interpretation and thereby make

rationalized plans and decisions (Romano, 2015).

Reliability and accurate information: CAS, IAS, JCS and other management accounting

systems must provide reliable & accurate data to the managers. It is because; manipulated data may

mislead the decisions and bring serious harm.

Time-updated: MA systems must render up-to-date information so that comparative

analysis can be made over the years to devise better policies and plans for the organizational

progress.

a-days, in the competitive challenging world, many-times, managers have to make big decisions

promptly, which cause difficulty for them in analysing and interpreting the data, therefore, they use

MAS to get the required data quickly and examine it for making suitable decisions for the growth.

Cost accounting system: It is essential for the company to estimate their product and

services cost accurately (Saladrigues and Tena, 2017). As its name, the system enables Nisa retail’s

managers to identify the right cost of their retail goods, identifying its trend, inventory &

profitability analysis and making decisions for the cost-control.

Job costing system: It refers to the process of accumulating various cost information that

belonged to a particular job (Fullerton, Kennedy and Widener, 2013). It is mainly helpful to provide

cost information to the consumers for their order placed. It allows Nisa retail store to quote their

goods prices after adding a reasonable return.

Inventory management system: This software enable corporation to track their inventory

levels for the ordering and delivering purpose to satisfy their consumer base. With the help of

managing stock to a right level, Nisa can place order on-time for having adequate inventories in the

warehouse to maintain their stock level.

Price optimisation: This MA system helps retailers to identify that how their clients will

respond at distinctive prices of the goods and services, so that, managers can set right prices to

maximize their operational return (Quattrone, 2016). More importantly, in retail sector, it seems

essential for the marketers to figure out the impact of change in their goods prices on the market

demand in order to fix an optimum price.

Essential requirement of different MA system

Relevant information: Every departmental manager of Nisa retail store i.e. finance,

purchase, sales, marketing, production need relevant information about their cost, revenues and

operational efficiency for performance measurement and interpretation and thereby make

rationalized plans and decisions (Romano, 2015).

Reliability and accurate information: CAS, IAS, JCS and other management accounting

systems must provide reliable & accurate data to the managers. It is because; manipulated data may

mislead the decisions and bring serious harm.

Time-updated: MA systems must render up-to-date information so that comparative

analysis can be made over the years to devise better policies and plans for the organizational

progress.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

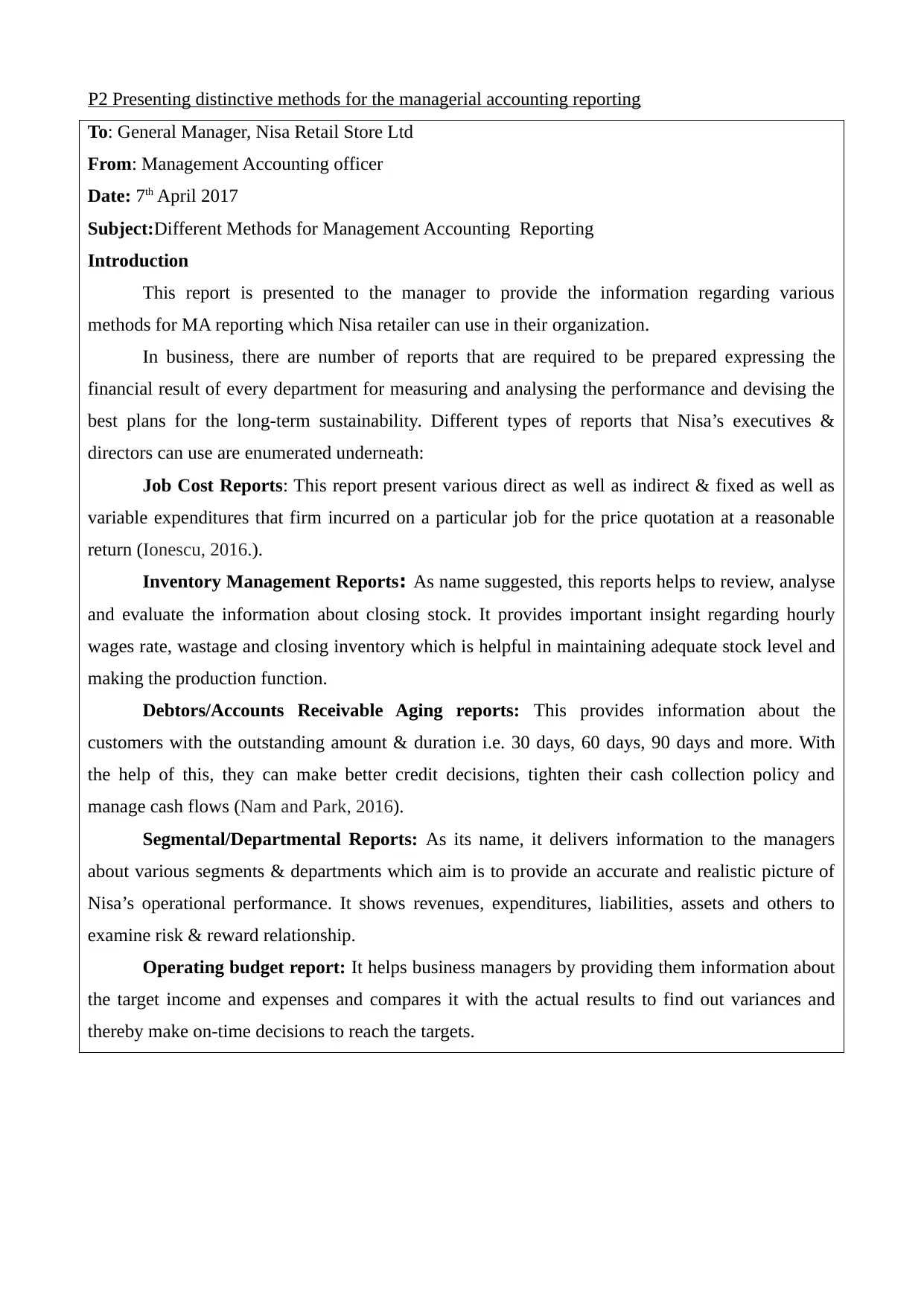

P2 Presenting distinctive methods for the managerial accounting reporting

To: General Manager, Nisa Retail Store Ltd

From: Management Accounting officer

Date: 7th April 2017

Subject:Different Methods for Management Accounting Reporting

Introduction

This report is presented to the manager to provide the information regarding various

methods for MA reporting which Nisa retailer can use in their organization.

In business, there are number of reports that are required to be prepared expressing the

financial result of every department for measuring and analysing the performance and devising the

best plans for the long-term sustainability. Different types of reports that Nisa’s executives &

directors can use are enumerated underneath:

Job Cost Reports: This report present various direct as well as indirect & fixed as well as

variable expenditures that firm incurred on a particular job for the price quotation at a reasonable

return (Ionescu, 2016.).

Inventory Management Reports: As name suggested, this reports helps to review, analyse

and evaluate the information about closing stock. It provides important insight regarding hourly

wages rate, wastage and closing inventory which is helpful in maintaining adequate stock level and

making the production function.

Debtors/Accounts Receivable Aging reports: This provides information about the

customers with the outstanding amount & duration i.e. 30 days, 60 days, 90 days and more. With

the help of this, they can make better credit decisions, tighten their cash collection policy and

manage cash flows (Nam and Park, 2016).

Segmental/Departmental Reports: As its name, it delivers information to the managers

about various segments & departments which aim is to provide an accurate and realistic picture of

Nisa’s operational performance. It shows revenues, expenditures, liabilities, assets and others to

examine risk & reward relationship.

Operating budget report: It helps business managers by providing them information about

the target income and expenses and compares it with the actual results to find out variances and

thereby make on-time decisions to reach the targets.

To: General Manager, Nisa Retail Store Ltd

From: Management Accounting officer

Date: 7th April 2017

Subject:Different Methods for Management Accounting Reporting

Introduction

This report is presented to the manager to provide the information regarding various

methods for MA reporting which Nisa retailer can use in their organization.

In business, there are number of reports that are required to be prepared expressing the

financial result of every department for measuring and analysing the performance and devising the

best plans for the long-term sustainability. Different types of reports that Nisa’s executives &

directors can use are enumerated underneath:

Job Cost Reports: This report present various direct as well as indirect & fixed as well as

variable expenditures that firm incurred on a particular job for the price quotation at a reasonable

return (Ionescu, 2016.).

Inventory Management Reports: As name suggested, this reports helps to review, analyse

and evaluate the information about closing stock. It provides important insight regarding hourly

wages rate, wastage and closing inventory which is helpful in maintaining adequate stock level and

making the production function.

Debtors/Accounts Receivable Aging reports: This provides information about the

customers with the outstanding amount & duration i.e. 30 days, 60 days, 90 days and more. With

the help of this, they can make better credit decisions, tighten their cash collection policy and

manage cash flows (Nam and Park, 2016).

Segmental/Departmental Reports: As its name, it delivers information to the managers

about various segments & departments which aim is to provide an accurate and realistic picture of

Nisa’s operational performance. It shows revenues, expenditures, liabilities, assets and others to

examine risk & reward relationship.

Operating budget report: It helps business managers by providing them information about

the target income and expenses and compares it with the actual results to find out variances and

thereby make on-time decisions to reach the targets.

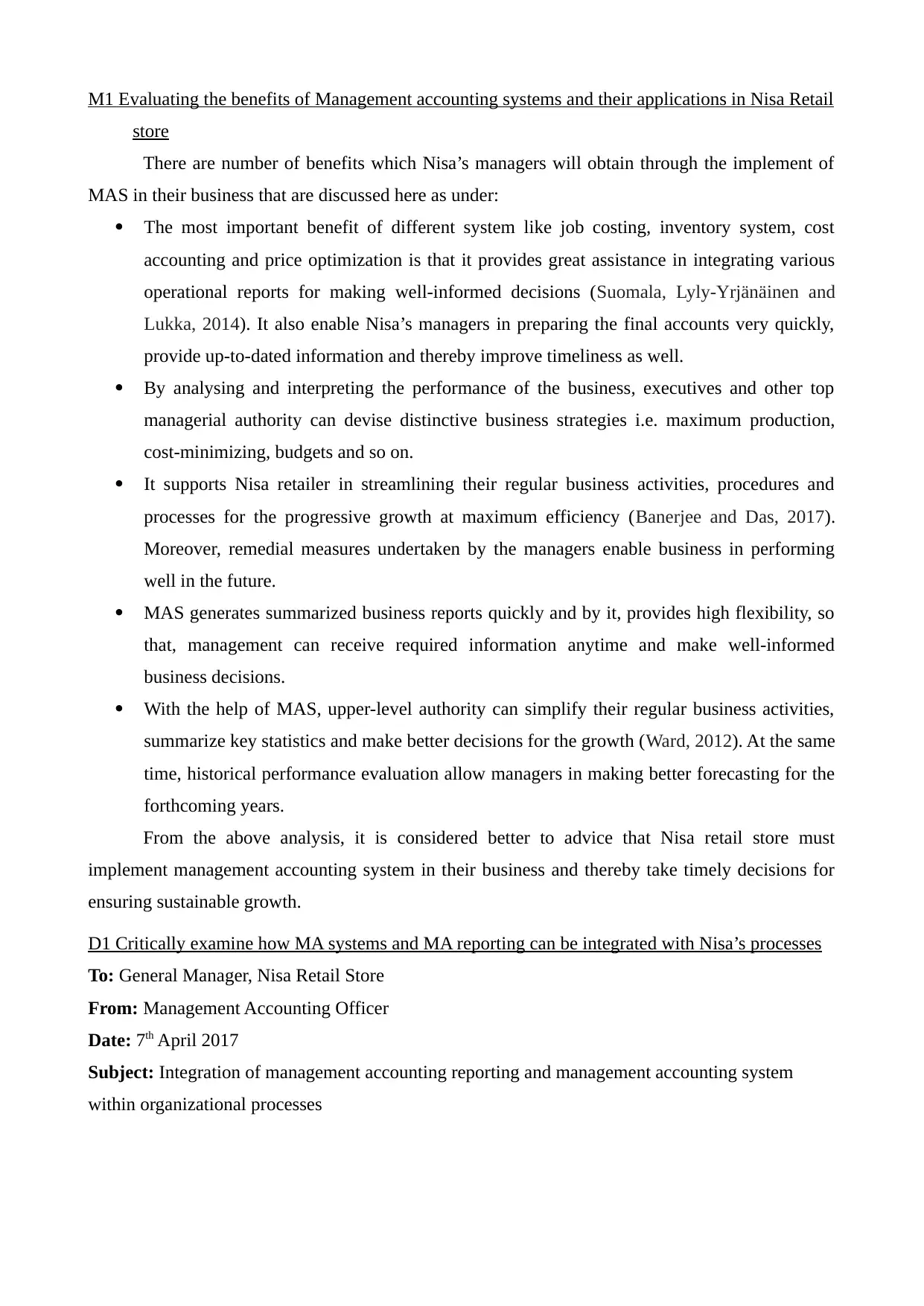

M1 Evaluating the benefits of Management accounting systems and their applications in Nisa Retail

store

There are number of benefits which Nisa’s managers will obtain through the implement of

MAS in their business that are discussed here as under:

The most important benefit of different system like job costing, inventory system, cost

accounting and price optimization is that it provides great assistance in integrating various

operational reports for making well-informed decisions (Suomala, Lyly-Yrjänäinen and

Lukka, 2014). It also enable Nisa’s managers in preparing the final accounts very quickly,

provide up-to-dated information and thereby improve timeliness as well.

By analysing and interpreting the performance of the business, executives and other top

managerial authority can devise distinctive business strategies i.e. maximum production,

cost-minimizing, budgets and so on.

It supports Nisa retailer in streamlining their regular business activities, procedures and

processes for the progressive growth at maximum efficiency (Banerjee and Das, 2017).

Moreover, remedial measures undertaken by the managers enable business in performing

well in the future.

MAS generates summarized business reports quickly and by it, provides high flexibility, so

that, management can receive required information anytime and make well-informed

business decisions.

With the help of MAS, upper-level authority can simplify their regular business activities,

summarize key statistics and make better decisions for the growth (Ward, 2012). At the same

time, historical performance evaluation allow managers in making better forecasting for the

forthcoming years.

From the above analysis, it is considered better to advice that Nisa retail store must

implement management accounting system in their business and thereby take timely decisions for

ensuring sustainable growth.

D1 Critically examine how MA systems and MA reporting can be integrated with Nisa’s processes

To: General Manager, Nisa Retail Store

From: Management Accounting Officer

Date: 7th April 2017

Subject: Integration of management accounting reporting and management accounting system

within organizational processes

store

There are number of benefits which Nisa’s managers will obtain through the implement of

MAS in their business that are discussed here as under:

The most important benefit of different system like job costing, inventory system, cost

accounting and price optimization is that it provides great assistance in integrating various

operational reports for making well-informed decisions (Suomala, Lyly-Yrjänäinen and

Lukka, 2014). It also enable Nisa’s managers in preparing the final accounts very quickly,

provide up-to-dated information and thereby improve timeliness as well.

By analysing and interpreting the performance of the business, executives and other top

managerial authority can devise distinctive business strategies i.e. maximum production,

cost-minimizing, budgets and so on.

It supports Nisa retailer in streamlining their regular business activities, procedures and

processes for the progressive growth at maximum efficiency (Banerjee and Das, 2017).

Moreover, remedial measures undertaken by the managers enable business in performing

well in the future.

MAS generates summarized business reports quickly and by it, provides high flexibility, so

that, management can receive required information anytime and make well-informed

business decisions.

With the help of MAS, upper-level authority can simplify their regular business activities,

summarize key statistics and make better decisions for the growth (Ward, 2012). At the same

time, historical performance evaluation allow managers in making better forecasting for the

forthcoming years.

From the above analysis, it is considered better to advice that Nisa retail store must

implement management accounting system in their business and thereby take timely decisions for

ensuring sustainable growth.

D1 Critically examine how MA systems and MA reporting can be integrated with Nisa’s processes

To: General Manager, Nisa Retail Store

From: Management Accounting Officer

Date: 7th April 2017

Subject: Integration of management accounting reporting and management accounting system

within organizational processes

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Management accounting system and MA reporting needs to be integrated with each other for

the effective and efficient operational management. With the help of this, business executives and

managers can generate confidential reports like inventory, sales, job costing and others and detect

the main hurdles for the firm and make timely decisions to get rid of it. Various departments i.e.

HR, Finance, Sales, Purchase, production, marketing, credit collection etc. can get summarized

reports from the system like costing, inventory, accounting, receivables and others and make timely

decisions for the success. Such integrated system can be used as a key decision-making tool to drive

long-run success into the business (Ahmed and Manab, 2016). Managers and director of the retail

store will not have to waste time in making reports manually, they just have to input data accurately

into the system and thereafter, reports can be generated automatically which saves time, cost plus

energy. By such facilities, Nisa’s management can make right plans and create strategies for the

high progress and growth in the future years at strong competitiveness.

TASK 2

LO2

P3 Cost calculation to prepare an income statement under marginal and absorption costing

Identifying an accurate cost per unit is one of the most significant area upon which pricing

decisions are based. Finding an inaccurate cost may leads to take misleading pricing decisions and

cause failure whereas right price fixation can bring success to the business by generating high

demand at a reasonable charges. There are various methods of cost identification i.e. marginal as

well as absorption which have been analysed here as under:

Absorption costing: This method absorbs all the payments incurred in the manufacturing

functions such as fixed as well as variable expenditures to the production for finding out the total

cost per unit, therefore, it is also known as full costing method (Malmi, 2016).

Benefits:

1. This technique is considered appropriate because it takes into account all the payments made

by Nisa on their production function and provides an accurate insight towards net profit.

2. It also make necessary adjustments regarding over as well as under-absorption of the

overheads to minimize cost.

3. It values inventory at cost per unit which is measured after considering fixed & variable

production expense (Tucker and Lowe, 2014).

Drawbacks:

the effective and efficient operational management. With the help of this, business executives and

managers can generate confidential reports like inventory, sales, job costing and others and detect

the main hurdles for the firm and make timely decisions to get rid of it. Various departments i.e.

HR, Finance, Sales, Purchase, production, marketing, credit collection etc. can get summarized

reports from the system like costing, inventory, accounting, receivables and others and make timely

decisions for the success. Such integrated system can be used as a key decision-making tool to drive

long-run success into the business (Ahmed and Manab, 2016). Managers and director of the retail

store will not have to waste time in making reports manually, they just have to input data accurately

into the system and thereafter, reports can be generated automatically which saves time, cost plus

energy. By such facilities, Nisa’s management can make right plans and create strategies for the

high progress and growth in the future years at strong competitiveness.

TASK 2

LO2

P3 Cost calculation to prepare an income statement under marginal and absorption costing

Identifying an accurate cost per unit is one of the most significant area upon which pricing

decisions are based. Finding an inaccurate cost may leads to take misleading pricing decisions and

cause failure whereas right price fixation can bring success to the business by generating high

demand at a reasonable charges. There are various methods of cost identification i.e. marginal as

well as absorption which have been analysed here as under:

Absorption costing: This method absorbs all the payments incurred in the manufacturing

functions such as fixed as well as variable expenditures to the production for finding out the total

cost per unit, therefore, it is also known as full costing method (Malmi, 2016).

Benefits:

1. This technique is considered appropriate because it takes into account all the payments made

by Nisa on their production function and provides an accurate insight towards net profit.

2. It also make necessary adjustments regarding over as well as under-absorption of the

overheads to minimize cost.

3. It values inventory at cost per unit which is measured after considering fixed & variable

production expense (Tucker and Lowe, 2014).

Drawbacks:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

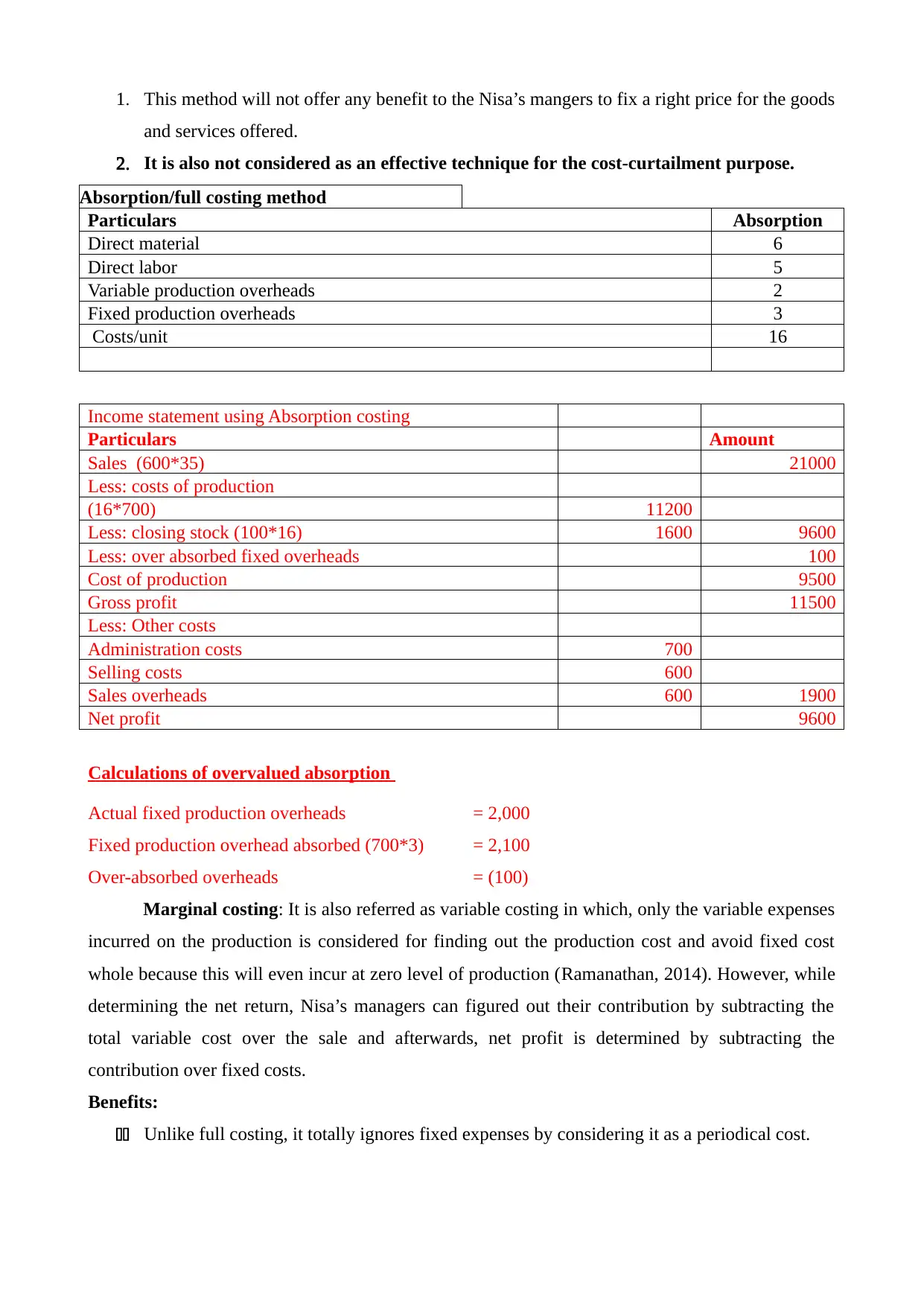

1. This method will not offer any benefit to the Nisa’s mangers to fix a right price for the goods

and services offered.

2. It is also not considered as an effective technique for the cost-curtailment purpose.

Absorption/full costing method

Particulars Absorption

Direct material 6

Direct labor 5

Variable production overheads 2

Fixed production overheads 3

Costs/unit 16

Income statement using Absorption costing

Particulars Amount

Sales (600*35) 21000

Less: costs of production

(16*700) 11200

Less: closing stock (100*16) 1600 9600

Less: over absorbed fixed overheads 100

Cost of production 9500

Gross profit 11500

Less: Other costs

Administration costs 700

Selling costs 600

Sales overheads 600 1900

Net profit 9600

Calculations of overvalued absorption

Actual fixed production overheads = 2,000

Fixed production overhead absorbed (700*3) = 2,100

Over-absorbed overheads = (100)

Marginal costing: It is also referred as variable costing in which, only the variable expenses

incurred on the production is considered for finding out the production cost and avoid fixed cost

whole because this will even incur at zero level of production (Ramanathan, 2014). However, while

determining the net return, Nisa’s managers can figured out their contribution by subtracting the

total variable cost over the sale and afterwards, net profit is determined by subtracting the

contribution over fixed costs.

Benefits:

11 Unlike full costing, it totally ignores fixed expenses by considering it as a periodical cost.

and services offered.

2. It is also not considered as an effective technique for the cost-curtailment purpose.

Absorption/full costing method

Particulars Absorption

Direct material 6

Direct labor 5

Variable production overheads 2

Fixed production overheads 3

Costs/unit 16

Income statement using Absorption costing

Particulars Amount

Sales (600*35) 21000

Less: costs of production

(16*700) 11200

Less: closing stock (100*16) 1600 9600

Less: over absorbed fixed overheads 100

Cost of production 9500

Gross profit 11500

Less: Other costs

Administration costs 700

Selling costs 600

Sales overheads 600 1900

Net profit 9600

Calculations of overvalued absorption

Actual fixed production overheads = 2,000

Fixed production overhead absorbed (700*3) = 2,100

Over-absorbed overheads = (100)

Marginal costing: It is also referred as variable costing in which, only the variable expenses

incurred on the production is considered for finding out the production cost and avoid fixed cost

whole because this will even incur at zero level of production (Ramanathan, 2014). However, while

determining the net return, Nisa’s managers can figured out their contribution by subtracting the

total variable cost over the sale and afterwards, net profit is determined by subtracting the

contribution over fixed costs.

Benefits:

11 Unlike full costing, it totally ignores fixed expenses by considering it as a periodical cost.

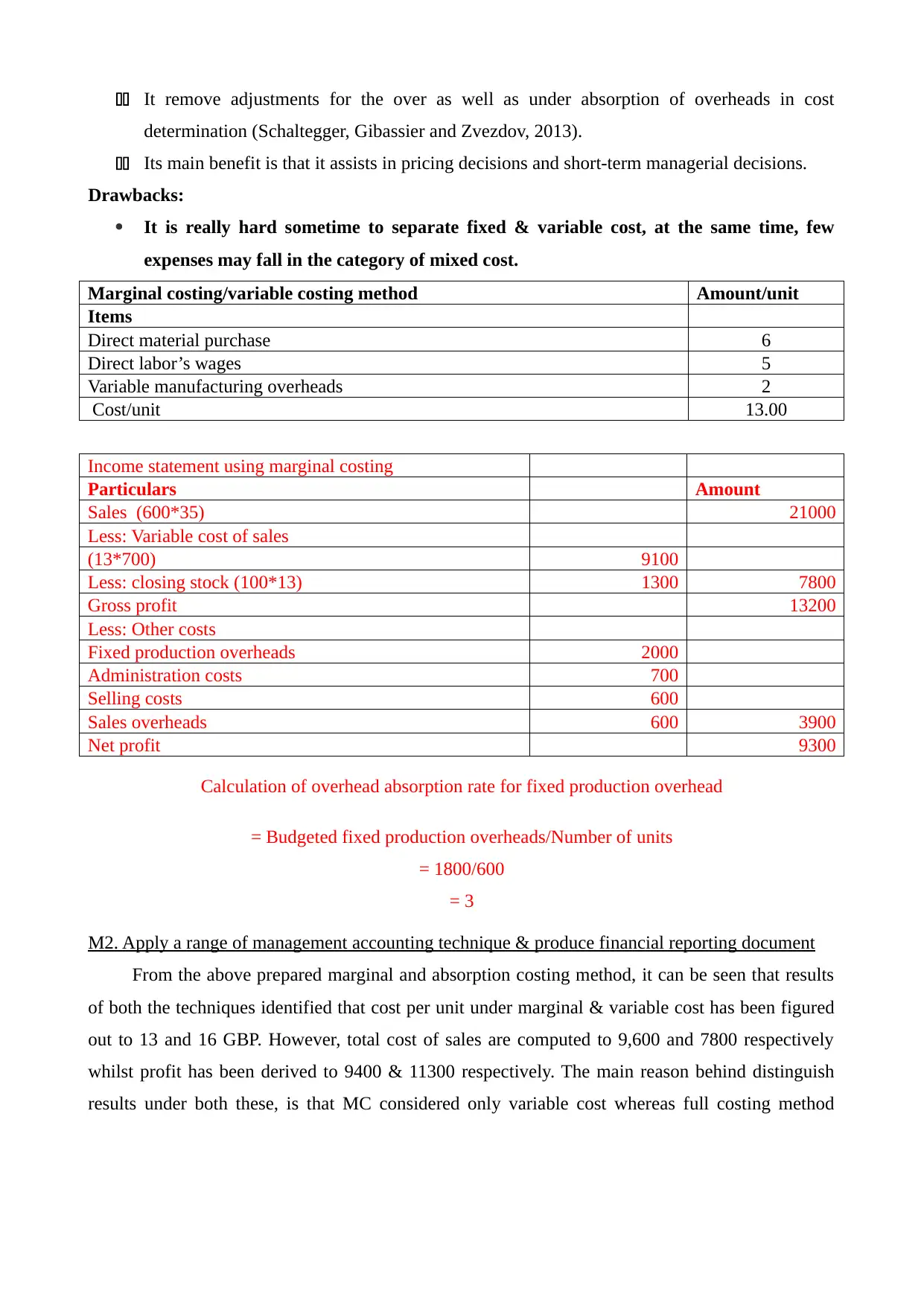

11 It remove adjustments for the over as well as under absorption of overheads in cost

determination (Schaltegger, Gibassier and Zvezdov, 2013).

11 Its main benefit is that it assists in pricing decisions and short-term managerial decisions.

Drawbacks:

It is really hard sometime to separate fixed & variable cost, at the same time, few

expenses may fall in the category of mixed cost.

Marginal costing/variable costing method Amount/unit

Items

Direct material purchase 6

Direct labor’s wages 5

Variable manufacturing overheads 2

Cost/unit 13.00

Income statement using marginal costing

Particulars Amount

Sales (600*35) 21000

Less: Variable cost of sales

(13*700) 9100

Less: closing stock (100*13) 1300 7800

Gross profit 13200

Less: Other costs

Fixed production overheads 2000

Administration costs 700

Selling costs 600

Sales overheads 600 3900

Net profit 9300

Calculation of overhead absorption rate for fixed production overhead

= Budgeted fixed production overheads/Number of units

= 1800/600

= 3

M2. Apply a range of management accounting technique & produce financial reporting document

From the above prepared marginal and absorption costing method, it can be seen that results

of both the techniques identified that cost per unit under marginal & variable cost has been figured

out to 13 and 16 GBP. However, total cost of sales are computed to 9,600 and 7800 respectively

whilst profit has been derived to 9400 & 11300 respectively. The main reason behind distinguish

results under both these, is that MC considered only variable cost whereas full costing method

determination (Schaltegger, Gibassier and Zvezdov, 2013).

11 Its main benefit is that it assists in pricing decisions and short-term managerial decisions.

Drawbacks:

It is really hard sometime to separate fixed & variable cost, at the same time, few

expenses may fall in the category of mixed cost.

Marginal costing/variable costing method Amount/unit

Items

Direct material purchase 6

Direct labor’s wages 5

Variable manufacturing overheads 2

Cost/unit 13.00

Income statement using marginal costing

Particulars Amount

Sales (600*35) 21000

Less: Variable cost of sales

(13*700) 9100

Less: closing stock (100*13) 1300 7800

Gross profit 13200

Less: Other costs

Fixed production overheads 2000

Administration costs 700

Selling costs 600

Sales overheads 600 3900

Net profit 9300

Calculation of overhead absorption rate for fixed production overhead

= Budgeted fixed production overheads/Number of units

= 1800/600

= 3

M2. Apply a range of management accounting technique & produce financial reporting document

From the above prepared marginal and absorption costing method, it can be seen that results

of both the techniques identified that cost per unit under marginal & variable cost has been figured

out to 13 and 16 GBP. However, total cost of sales are computed to 9,600 and 7800 respectively

whilst profit has been derived to 9400 & 11300 respectively. The main reason behind distinguish

results under both these, is that MC considered only variable cost whereas full costing method

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

utilized both the fixed and variable costs. Besides this, other managerial accounting techniques that

can be used are the break-even analysis, made below:

Breakeven point = Total fixed cost/selling cost-total variable costs

(2000+700+600)/(35-6-5-2-1)

3300/(22)

= 150 units

The results stated that at 150 units at a sale of (150*35) = 5,250 GBP, Nisa retail store can

get its break-even point which showcase maximum capacity utilization and before the point, firm

bear loss and beyond this, it drive positive return. Looking to the current sale, Nisa had sold 600

units which is above the BEP and drive return in both the cases to 9,400 & 11,300.

D2 Producing financial reports to apply and interpret data for different activities

To: General Manager, Nisa Retail Stores

From: Management Accounting Officer

Date: 7th April 2017

Subjects: Evaluating the performance and its reporting to the managers

The application of both the full & variable costing method provided different results to each

other, because of distinctive implications. It is comparatively greater in marginal costing to 11,300

because it had just considered variable cost which is measured at 13 GBP per unit, in despite of this,

full costing method used 16 GBP of unit cost because it took both the fixed & variable cost into

consideration. Due to this, inventory valuation also has been affected which had been computed at

1300 & 1600 greater in absorption costing. Besides this, variable costing did not considered under

absorbed fixed overheads of 100 GBP while determining the net profit, in contrast, full costing

method considered the same and declined the gross and net return to 11,300 & 9,400 respectively.

On the contrary side, there are no such kind of adjustments made in marginal costing method and as

a result, high yield has been shown to 11,300.

TASK 3

LO3

can be used are the break-even analysis, made below:

Breakeven point = Total fixed cost/selling cost-total variable costs

(2000+700+600)/(35-6-5-2-1)

3300/(22)

= 150 units

The results stated that at 150 units at a sale of (150*35) = 5,250 GBP, Nisa retail store can

get its break-even point which showcase maximum capacity utilization and before the point, firm

bear loss and beyond this, it drive positive return. Looking to the current sale, Nisa had sold 600

units which is above the BEP and drive return in both the cases to 9,400 & 11,300.

D2 Producing financial reports to apply and interpret data for different activities

To: General Manager, Nisa Retail Stores

From: Management Accounting Officer

Date: 7th April 2017

Subjects: Evaluating the performance and its reporting to the managers

The application of both the full & variable costing method provided different results to each

other, because of distinctive implications. It is comparatively greater in marginal costing to 11,300

because it had just considered variable cost which is measured at 13 GBP per unit, in despite of this,

full costing method used 16 GBP of unit cost because it took both the fixed & variable cost into

consideration. Due to this, inventory valuation also has been affected which had been computed at

1300 & 1600 greater in absorption costing. Besides this, variable costing did not considered under

absorbed fixed overheads of 100 GBP while determining the net profit, in contrast, full costing

method considered the same and declined the gross and net return to 11,300 & 9,400 respectively.

On the contrary side, there are no such kind of adjustments made in marginal costing method and as

a result, high yield has been shown to 11,300.

TASK 3

LO3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

P4 advantage and disadvantage of different types of planning tools

Budgetary control is a practice that is used in the company for making budget for the future

time period. It aids in comparing actual performance of the company with the budgetary figures.

Weak performing areas of the business can be identified and on the basis of that measures can be

taken for making improvements in existing performance of the business. Corrective actions can be

taken by business for making improvements in performance of the business (DRURY, 2013). There

are many methods that could be used by the company for accomplishing this objective. Methods

and their advantages and disadvantages are as described:-

Activity based budgeting: - This method is used by Nia Retail store for preparing budget

and every activity that is needed to be completed is mentioned while making use of this approach.

In this method income is allocated to activity's cost. This method has many advantageous and it

supports for allocating revenues that have been generated in the business. In addition to that this

technique focuses on regulating the overheads. On the other hand there are some disadvantageous

that are associated with this method and it requires managerial techniques to train managers so that

they can make use of this method.

Incremental budgeting:- This method makes use of changes that occurred in budget at

every year and on the basis of that incremental amount is added to the budget that has been prepared

in previous year. There are some advantages that are associated with this method and it is simple to

create budget and it aids in maintaining transparency among all the departments that are working in

the organization. However there are some disadvantages that are associated with this method and in

this no incentives are there for controlling the cost.

Cash budget: - It is a very good financial tool that can be used by management of Imda tech

for controlling their financial functions. Making use of this tool helps for finding cash balance that

has been sufficient for fulfilling the regular obligations. It aids for identifying the cash availability

of the organization and company can identify about requirement of cash in the company. It helps for

coordinating the activities and minimizing the cost and maximizing the profit.

Disadvantage of cash budget: - this budget is prepared on estimates that are subjective and

it might take a longer time for achieving the required financial objectives. Operating this budget

might proves expensive and productivity can be decreased if targets are not realistic.

Cost plus pricing: - It is a very effective accounting tool that could be used by management

of Imda tech for regulating the financial performance of the business. It is a simple method that aid

for determining the price of the product. Reasons for increases in expenses can be identified and on

the basis of that corrective measures can be taken by the organization.

Budgetary control is a practice that is used in the company for making budget for the future

time period. It aids in comparing actual performance of the company with the budgetary figures.

Weak performing areas of the business can be identified and on the basis of that measures can be

taken for making improvements in existing performance of the business. Corrective actions can be

taken by business for making improvements in performance of the business (DRURY, 2013). There

are many methods that could be used by the company for accomplishing this objective. Methods

and their advantages and disadvantages are as described:-

Activity based budgeting: - This method is used by Nia Retail store for preparing budget

and every activity that is needed to be completed is mentioned while making use of this approach.

In this method income is allocated to activity's cost. This method has many advantageous and it

supports for allocating revenues that have been generated in the business. In addition to that this

technique focuses on regulating the overheads. On the other hand there are some disadvantageous

that are associated with this method and it requires managerial techniques to train managers so that

they can make use of this method.

Incremental budgeting:- This method makes use of changes that occurred in budget at

every year and on the basis of that incremental amount is added to the budget that has been prepared

in previous year. There are some advantages that are associated with this method and it is simple to

create budget and it aids in maintaining transparency among all the departments that are working in

the organization. However there are some disadvantages that are associated with this method and in

this no incentives are there for controlling the cost.

Cash budget: - It is a very good financial tool that can be used by management of Imda tech

for controlling their financial functions. Making use of this tool helps for finding cash balance that

has been sufficient for fulfilling the regular obligations. It aids for identifying the cash availability

of the organization and company can identify about requirement of cash in the company. It helps for

coordinating the activities and minimizing the cost and maximizing the profit.

Disadvantage of cash budget: - this budget is prepared on estimates that are subjective and

it might take a longer time for achieving the required financial objectives. Operating this budget

might proves expensive and productivity can be decreased if targets are not realistic.

Cost plus pricing: - It is a very effective accounting tool that could be used by management

of Imda tech for regulating the financial performance of the business. It is a simple method that aid

for determining the price of the product. Reasons for increases in expenses can be identified and on

the basis of that corrective measures can be taken by the organization.

Disadvantage of cost plus pricing: - Future demand for the project cannot be identified and

this method also does not considerations for competitor actions. Sometimes overestimations for

price of the products are made and due to that difficulty are faced in calculating the profit margins.

M2 Analysis of use of planning tools and application for forecasting budget

There are many tools that are available with the Nisa retail store that could be used by the

business for forecasting budget. Zero based budgeting and Activity based budgeting are some

important and effective tools that could be sued by the business. Company has option for making

use of Activity based budgeting method so that future forecasting can be made for the business.

This technique provides options for preparing budget for the enterprise (Ramanathan, 2014).

It is assertive that data and information should be collected from the authentic and reliable

sources so that budget can be prepared in appropriate manner. It is vital that budget must be

prepared in systematic and strategic manner so that required objectives of the company could be

achieved (Schaltegger, Gibassier and Zvezdov, 2013). Along with this it activity based budgeting

method provides an effective medium for allocating revenues to the related expenditure. Variance

analysis can be prepared by managers of the firm and it will support for taking corrective and

effective actions for making improvements in the performance of the business.

D3 Evaluation of planning tools that could be used for solving financial problem

It is assertive that effective financial tools should be used by the Nisa for solving the

financial problems that are faced by business. Some of the methods that can be used are as

described:-

RATIO ANALYSIS: - Financial ratios are compared under this method and it supports for

examining the performance of the business in effective manner. There are different ratios that are

compared under this and it includes profitability ratio, liquidity ratio, solvency ratio and some other

ratios (Malmi, 2016). Making use of this method helps for assessing the actual performance of the

business as compared to estimated performance. It will help for making effective strategies and

action plans for the Nisa’s growth. Growth and better financial performance of the business can be

ensured and it will aid for enhancing the profitability of the entity.

CAPITAL BUDGETING: - It is also an effective method that could be sued by the entity for

solving diverse range of financial problems that are faced in the business. In this method project

evaluation methods are used and it includes payback, accounting rate of return and Net Present

value and internal rate of return (Tucker and Lowe, 2014). This technique provides opportunity for

the retailer to identify investment opportunities.

VARIANCE ANALYSIS: - In this method comparison is made between the set standards

against the actual standards and it also helps for causes for unfavourable variance can be identified.

this method also does not considerations for competitor actions. Sometimes overestimations for

price of the products are made and due to that difficulty are faced in calculating the profit margins.

M2 Analysis of use of planning tools and application for forecasting budget

There are many tools that are available with the Nisa retail store that could be used by the

business for forecasting budget. Zero based budgeting and Activity based budgeting are some

important and effective tools that could be sued by the business. Company has option for making

use of Activity based budgeting method so that future forecasting can be made for the business.

This technique provides options for preparing budget for the enterprise (Ramanathan, 2014).

It is assertive that data and information should be collected from the authentic and reliable

sources so that budget can be prepared in appropriate manner. It is vital that budget must be

prepared in systematic and strategic manner so that required objectives of the company could be

achieved (Schaltegger, Gibassier and Zvezdov, 2013). Along with this it activity based budgeting

method provides an effective medium for allocating revenues to the related expenditure. Variance

analysis can be prepared by managers of the firm and it will support for taking corrective and

effective actions for making improvements in the performance of the business.

D3 Evaluation of planning tools that could be used for solving financial problem

It is assertive that effective financial tools should be used by the Nisa for solving the

financial problems that are faced by business. Some of the methods that can be used are as

described:-

RATIO ANALYSIS: - Financial ratios are compared under this method and it supports for

examining the performance of the business in effective manner. There are different ratios that are

compared under this and it includes profitability ratio, liquidity ratio, solvency ratio and some other

ratios (Malmi, 2016). Making use of this method helps for assessing the actual performance of the

business as compared to estimated performance. It will help for making effective strategies and

action plans for the Nisa’s growth. Growth and better financial performance of the business can be

ensured and it will aid for enhancing the profitability of the entity.

CAPITAL BUDGETING: - It is also an effective method that could be sued by the entity for

solving diverse range of financial problems that are faced in the business. In this method project

evaluation methods are used and it includes payback, accounting rate of return and Net Present

value and internal rate of return (Tucker and Lowe, 2014). This technique provides opportunity for

the retailer to identify investment opportunities.

VARIANCE ANALYSIS: - In this method comparison is made between the set standards

against the actual standards and it also helps for causes for unfavourable variance can be identified.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.