Management Accounting Systems and Financial Reporting: Nisa Retail

VerifiedAdded on 2020/02/03

|16

|5628

|86

Report

AI Summary

This report provides a comprehensive analysis of management accounting practices within Nisa Retail, a UK-based retail store. It begins by defining management accounting and outlining its essential requirements, exploring different types of management accounting systems such as ABC costing, FIFO, LIFO, inventory accounting, and weighted average methods. The report then delves into various management accounting reporting methods, including payroll reports, accounts receivable reports, budget reports, job cost reports, and manufacturing reports. Furthermore, it examines cost analysis techniques, specifically marginal and absorption costing, and demonstrates their application in preparing income statements. The report also discusses the advantages and disadvantages of different planning tools used for budgetary control. Finally, it investigates how Nisa Retail adapts management accounting systems to respond to financial challenges, providing a complete overview of the company's financial management strategies.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting and essential requirements of different types of management

accounting systems.................................................................................................................1

P2 Different methods used for management accounting reporting........................................2

TASK 2............................................................................................................................................4

P3. Calculating costs using techniques of cost analysis to prepare an income statement using

marginal and absorption costs................................................................................................4

TASK 3............................................................................................................................................7

P4. Advantages and disadvantages of different types of planning tools used for budgetary

control.....................................................................................................................................7

TASK 4............................................................................................................................................9

P5. Comparing ways through which Nisa retail store is adapting management accounting

systems to respond to financial...............................................................................................9

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

APPENDIX 1.................................................................................................................................14

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting and essential requirements of different types of management

accounting systems.................................................................................................................1

P2 Different methods used for management accounting reporting........................................2

TASK 2............................................................................................................................................4

P3. Calculating costs using techniques of cost analysis to prepare an income statement using

marginal and absorption costs................................................................................................4

TASK 3............................................................................................................................................7

P4. Advantages and disadvantages of different types of planning tools used for budgetary

control.....................................................................................................................................7

TASK 4............................................................................................................................................9

P5. Comparing ways through which Nisa retail store is adapting management accounting

systems to respond to financial...............................................................................................9

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

APPENDIX 1.................................................................................................................................14

INTRODUCTION

Management accounting can be determined as a process that involves partnering of

devising planning, performance management system and decision making. For all the different

set of activities that are being set by the firm needs money so that the plan can be enacted in an

effective manner (Bennett, Schaltegger and Zvezdov, 2013). In this context, it is important for

the organization to have management of accounting. There are different type of process that are

helpful enough to manage resources related to finance. Present report is on Nisa retail store that

is headquartered in UK and they make sure to deliver their customers with high quality services.

This report covers different type of management accounting that are being used within the

organization. Further, it covers advantages and disadvantages of different tools that is used for

budgetary control. Lastly, it also includes different ways with the help of which firms adopt

management accounting system in order to report the financial.

TASK 1

P1 Management accounting and essential requirements of different types of management

accounting systems

Management accounting can be defined as the process with the help of which

organizations get to record financial transaction, accounts and different financial statement

(Macintosh and Quattrone, 2010). For example, it includes cash flow statement, balance sheet,

income statement, etc. selected company gets benefited as they are able to provide clear data

regarding finance and accounts. When management of the firm have proper information related

with their financial position, then it helpful enough to make decision for the future. Further, there

are different set of decision that are taken by the firm which can be long term or short term. For

all these aspects it requires effective financial support. Moreover, purchase decision are taken up

by financial support. When the rate of financial support is high, then it becomes favourable for

the firm to manage and control resources related to finance in effective manner. There are

various type of approaches and system that can be used by Nisa in order to manage their business

operations. In this context, below given are few of the different management accounting:

ABC costing: This is a type of method that is helpful to determine expenses and cost for

every day to day operations. In order to perform daily business efficiently, it requires

1

Management accounting can be determined as a process that involves partnering of

devising planning, performance management system and decision making. For all the different

set of activities that are being set by the firm needs money so that the plan can be enacted in an

effective manner (Bennett, Schaltegger and Zvezdov, 2013). In this context, it is important for

the organization to have management of accounting. There are different type of process that are

helpful enough to manage resources related to finance. Present report is on Nisa retail store that

is headquartered in UK and they make sure to deliver their customers with high quality services.

This report covers different type of management accounting that are being used within the

organization. Further, it covers advantages and disadvantages of different tools that is used for

budgetary control. Lastly, it also includes different ways with the help of which firms adopt

management accounting system in order to report the financial.

TASK 1

P1 Management accounting and essential requirements of different types of management

accounting systems

Management accounting can be defined as the process with the help of which

organizations get to record financial transaction, accounts and different financial statement

(Macintosh and Quattrone, 2010). For example, it includes cash flow statement, balance sheet,

income statement, etc. selected company gets benefited as they are able to provide clear data

regarding finance and accounts. When management of the firm have proper information related

with their financial position, then it helpful enough to make decision for the future. Further, there

are different set of decision that are taken by the firm which can be long term or short term. For

all these aspects it requires effective financial support. Moreover, purchase decision are taken up

by financial support. When the rate of financial support is high, then it becomes favourable for

the firm to manage and control resources related to finance in effective manner. There are

various type of approaches and system that can be used by Nisa in order to manage their business

operations. In this context, below given are few of the different management accounting:

ABC costing: This is a type of method that is helpful to determine expenses and cost for

every day to day operations. In order to perform daily business efficiently, it requires

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

management to identify the expense that they will need in order to perform the business activities

(van der Meer-Kooistra and Vosselman, 2012).

FIFO (first in first out): It is type of stock evaluation method as per this process the stock

and inventory that are used for the first time will be sent off. This method is generally used by

most of the companies in order to valuing the level of inventory. It helps to determine the level

of overall stock in accurate manner.

LIFO (last in first out): This is another type of stock evaluation method. In this process

management is able to sell their stock and manage the operations of business efficiently (Siegel

and et.al., 2010). As per this method, all the inventory that is bought by Nisa at last will be sold

at first place. This method is not much used by companies as it is less effective when compared

with FIFO.

Inventory accounting: This can be determined as a system or method that manages the

stock or inventory of the organization. This is managed in order to generate sales for the firm.

With the help of inventory accounting, Nisa is able to make use of terms that are helpful enough

to produce services and products (Chenhall and Moers, 2015). In case the level of inventory is

high, then it affects the profitability of the organization. With the help of accounting process, it

supports Nisa retail to make proper control over stock and inventory. There is a limit that has to

be maintained by the firm in relation with the stock that they are willing to use for production but

when the rate of stock is high, then there are negative impact over the firm.

Weighted average: As per this method, it enables to know the average value of LIFO and

FIFO. This way firm is able to determine the difference that they are getting when both FIFO and

LIFO is applied (Chiwamit, Modell and Yang, 2014). In addition to this, overall evaluation can

be identified from the available stock or inventory.

P2 Different methods used for management accounting reporting

There are different type of financial accounting that has to be prepared b y Nisa or any

other organization. In this context it includes balance sheet, cash flow statement, profit and loss

account, etc. (Cullen, Tsamenyi and Gorst, 2013). All the data that involves the expenses that are

incurred by the firm are recorded in these financial statement and they are helpful to get proper

information for where they stand. It is also helpful to determine the position of firm in context of

2

(van der Meer-Kooistra and Vosselman, 2012).

FIFO (first in first out): It is type of stock evaluation method as per this process the stock

and inventory that are used for the first time will be sent off. This method is generally used by

most of the companies in order to valuing the level of inventory. It helps to determine the level

of overall stock in accurate manner.

LIFO (last in first out): This is another type of stock evaluation method. In this process

management is able to sell their stock and manage the operations of business efficiently (Siegel

and et.al., 2010). As per this method, all the inventory that is bought by Nisa at last will be sold

at first place. This method is not much used by companies as it is less effective when compared

with FIFO.

Inventory accounting: This can be determined as a system or method that manages the

stock or inventory of the organization. This is managed in order to generate sales for the firm.

With the help of inventory accounting, Nisa is able to make use of terms that are helpful enough

to produce services and products (Chenhall and Moers, 2015). In case the level of inventory is

high, then it affects the profitability of the organization. With the help of accounting process, it

supports Nisa retail to make proper control over stock and inventory. There is a limit that has to

be maintained by the firm in relation with the stock that they are willing to use for production but

when the rate of stock is high, then there are negative impact over the firm.

Weighted average: As per this method, it enables to know the average value of LIFO and

FIFO. This way firm is able to determine the difference that they are getting when both FIFO and

LIFO is applied (Chiwamit, Modell and Yang, 2014). In addition to this, overall evaluation can

be identified from the available stock or inventory.

P2 Different methods used for management accounting reporting

There are different type of financial accounting that has to be prepared b y Nisa or any

other organization. In this context it includes balance sheet, cash flow statement, profit and loss

account, etc. (Cullen, Tsamenyi and Gorst, 2013). All the data that involves the expenses that are

incurred by the firm are recorded in these financial statement and they are helpful to get proper

information for where they stand. It is also helpful to determine the position of firm in context of

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

financial position. Below give are the different type of reports that are used by cited firm that is

Nisa retail store with the help of which they are able to assess financial performance:

Payroll report: There are different type of departments that are involved in the

organization and for each of them roles and responsibilities are divided among workers. Further,

each of them is given with certain pay. Payroll report is helpful to make proper report of the pay

that is provided to each employee (Figge and Hahn, 2013). It consists of the expenditure that is

incurred by workers are included. More specifically, it includes salary, wages, incentives,

monitory motivation, compensation, etc. This way it supports the cited firm to know the total

amount of expenses that they have made on employees is evaluated.

Report of account receivables: As per this report, Nisa retail is able to identify the total

amount of money that is to be received. In this context, it can be stated that more the amount to

be received the more will be profit margin (Bennett Schaltegger and Zvezdov, 2013). On the

other hand, if the amount that is to be received is low, then the rate of profit will also differ.

Budget report: This reports shows information of fiscal year and financial data. This

report enables to make plan for the future as they get to know the total amount that will be

required by the firm. Each and every year, it requires proper use of money that has to be spend

for each and every operations (Macintosh and Quattrone, 2010). In this context, budget reports

enables to develop plan with the help of which plans for business can be made for the future.

With time, there are many changes that take place and it is important for the firm to understand

them and develop plan. For each of the plan made, it requires financial support and the

requirement is determined through the budget report prepared.

Job cost reports: In accordance with this report, it is important to identify and to make

proper record of financial transaction (van der Meer-Kooistra and Vosselman, 2012). As per this

report, managers get to understand how much the cost will be incurred for the activities planned.

There are long and short term goals that are set by the firm. In order to achieve them, it is

important to develop activities and tasks and for each of them it requires proper support of

materials, resources, etc. This way cost is incurred and this report enables to determine the total

cost that has to be spend by the firm.

Manufacturing report: It is a type of report that determine the total cost that is incurred

by the process of manufacturing for services and products that is delivered by the organization

(Siegel and et.al., 2010). Further, Nisa retail get benefited with this report as they get to

3

Nisa retail store with the help of which they are able to assess financial performance:

Payroll report: There are different type of departments that are involved in the

organization and for each of them roles and responsibilities are divided among workers. Further,

each of them is given with certain pay. Payroll report is helpful to make proper report of the pay

that is provided to each employee (Figge and Hahn, 2013). It consists of the expenditure that is

incurred by workers are included. More specifically, it includes salary, wages, incentives,

monitory motivation, compensation, etc. This way it supports the cited firm to know the total

amount of expenses that they have made on employees is evaluated.

Report of account receivables: As per this report, Nisa retail is able to identify the total

amount of money that is to be received. In this context, it can be stated that more the amount to

be received the more will be profit margin (Bennett Schaltegger and Zvezdov, 2013). On the

other hand, if the amount that is to be received is low, then the rate of profit will also differ.

Budget report: This reports shows information of fiscal year and financial data. This

report enables to make plan for the future as they get to know the total amount that will be

required by the firm. Each and every year, it requires proper use of money that has to be spend

for each and every operations (Macintosh and Quattrone, 2010). In this context, budget reports

enables to develop plan with the help of which plans for business can be made for the future.

With time, there are many changes that take place and it is important for the firm to understand

them and develop plan. For each of the plan made, it requires financial support and the

requirement is determined through the budget report prepared.

Job cost reports: In accordance with this report, it is important to identify and to make

proper record of financial transaction (van der Meer-Kooistra and Vosselman, 2012). As per this

report, managers get to understand how much the cost will be incurred for the activities planned.

There are long and short term goals that are set by the firm. In order to achieve them, it is

important to develop activities and tasks and for each of them it requires proper support of

materials, resources, etc. This way cost is incurred and this report enables to determine the total

cost that has to be spend by the firm.

Manufacturing report: It is a type of report that determine the total cost that is incurred

by the process of manufacturing for services and products that is delivered by the organization

(Siegel and et.al., 2010). Further, Nisa retail get benefited with this report as they get to

3

understand the number of units that they have to produce so that demand can be met. There are

different type of manufacturing expenses that are involved. With this respect, it includes cost

related to technology, labour charges, raw materials, etc. (Chenhall and Moers, 2015). All the

cost incurred is added and the cost is then recorded in profit and loss account and they are

recorded in the name of cost of production.

TASK 2

P3. Calculating costs using techniques of cost analysis to prepare an income statement using

marginal and absorption costs

With the help of business process, net profit is calculated. Main aim of any firm is to gain

maximum profit. This is can be identified when the net profit of the firm is raising (Chiwamit,

Modell and Yang, 2014). There are different type of methods that can be applied by Nisa retail in

order to calculate their expenses. When net profit is calculated, then it becomes helpful to know

where the financial position of the firm lies. Both marginal and absorption cost are effective for

the firm in order to make analysis of cost. Below given are the calculation done with the help of

Absorption cost:

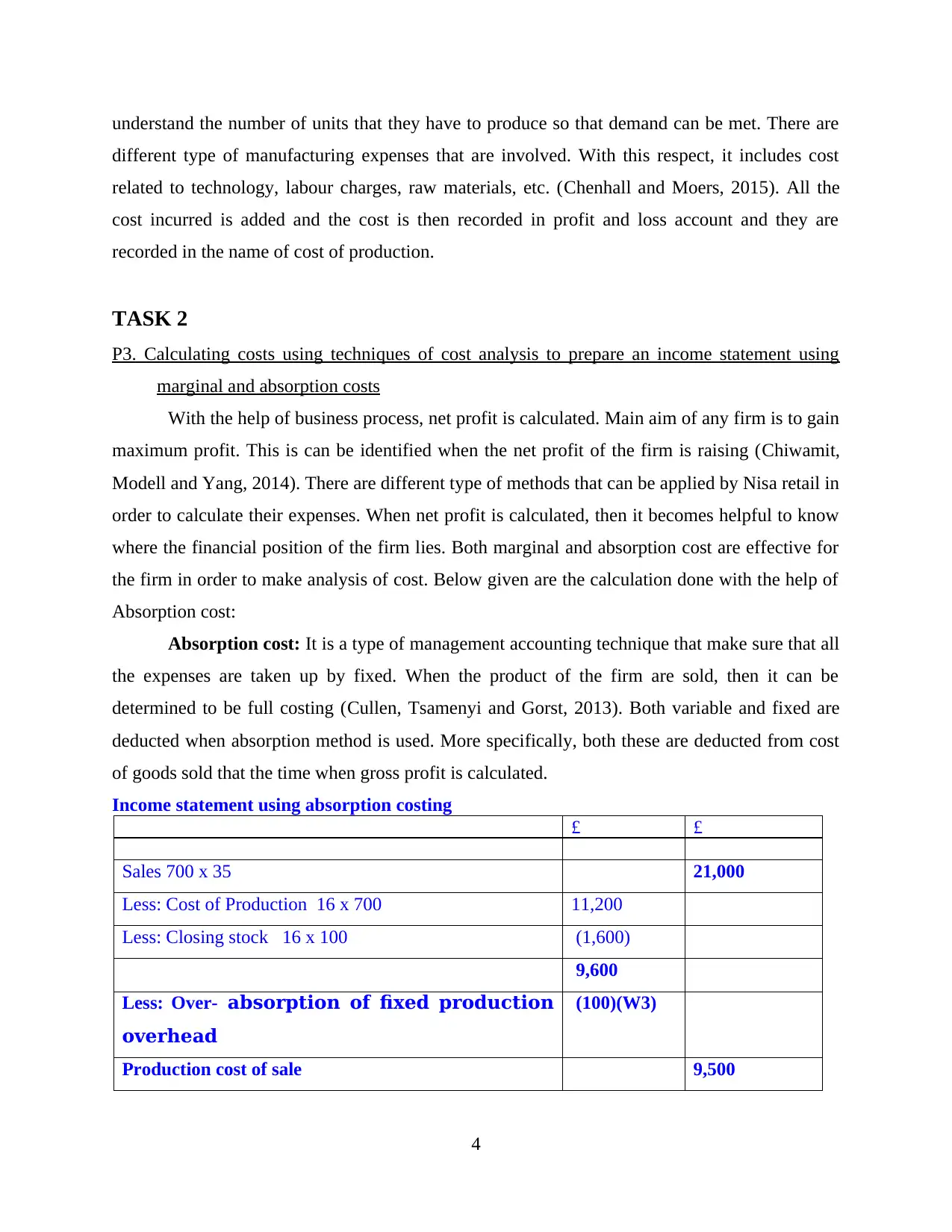

Absorption cost: It is a type of management accounting technique that make sure that all

the expenses are taken up by fixed. When the product of the firm are sold, then it can be

determined to be full costing (Cullen, Tsamenyi and Gorst, 2013). Both variable and fixed are

deducted when absorption method is used. More specifically, both these are deducted from cost

of goods sold that the time when gross profit is calculated.

Income statement using absorption costing

£ £

Sales 700 x 35 21,000

Less: Cost of Production 16 x 700 11,200

Less: Closing stock 16 x 100 (1,600)

9,600

Less: Over- absorption of fixed production

overhead

(100)(W3)

Production cost of sale 9,500

4

different type of manufacturing expenses that are involved. With this respect, it includes cost

related to technology, labour charges, raw materials, etc. (Chenhall and Moers, 2015). All the

cost incurred is added and the cost is then recorded in profit and loss account and they are

recorded in the name of cost of production.

TASK 2

P3. Calculating costs using techniques of cost analysis to prepare an income statement using

marginal and absorption costs

With the help of business process, net profit is calculated. Main aim of any firm is to gain

maximum profit. This is can be identified when the net profit of the firm is raising (Chiwamit,

Modell and Yang, 2014). There are different type of methods that can be applied by Nisa retail in

order to calculate their expenses. When net profit is calculated, then it becomes helpful to know

where the financial position of the firm lies. Both marginal and absorption cost are effective for

the firm in order to make analysis of cost. Below given are the calculation done with the help of

Absorption cost:

Absorption cost: It is a type of management accounting technique that make sure that all

the expenses are taken up by fixed. When the product of the firm are sold, then it can be

determined to be full costing (Cullen, Tsamenyi and Gorst, 2013). Both variable and fixed are

deducted when absorption method is used. More specifically, both these are deducted from cost

of goods sold that the time when gross profit is calculated.

Income statement using absorption costing

£ £

Sales 700 x 35 21,000

Less: Cost of Production 16 x 700 11,200

Less: Closing stock 16 x 100 (1,600)

9,600

Less: Over- absorption of fixed production

overhead

(100)(W3)

Production cost of sale 9,500

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

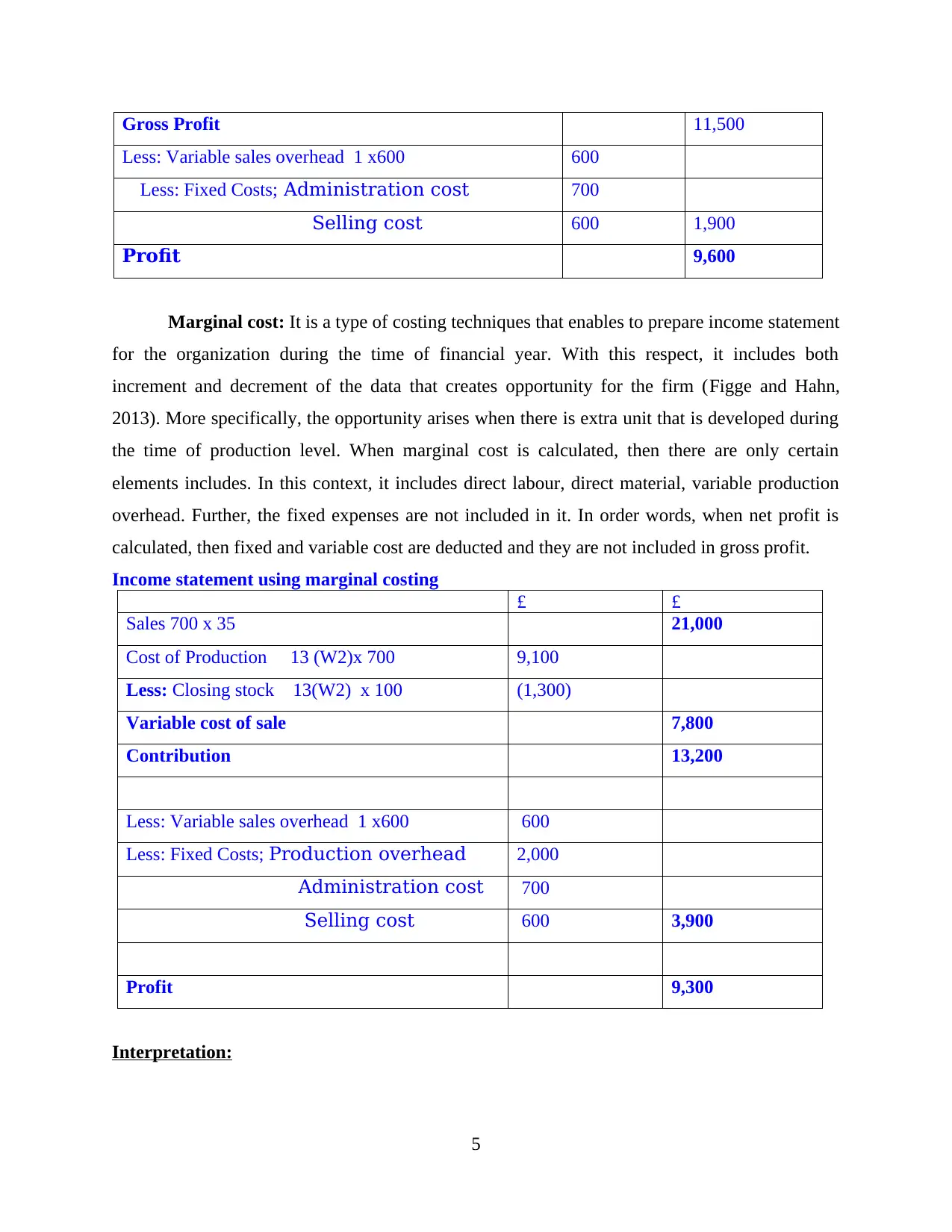

Gross Profit 11,500

Less: Variable sales overhead 1 x600 600

Less: Fixed Costs; Administration cost 700

Selling cost 600 1,900

Profit 9,600

Marginal cost: It is a type of costing techniques that enables to prepare income statement

for the organization during the time of financial year. With this respect, it includes both

increment and decrement of the data that creates opportunity for the firm (Figge and Hahn,

2013). More specifically, the opportunity arises when there is extra unit that is developed during

the time of production level. When marginal cost is calculated, then there are only certain

elements includes. In this context, it includes direct labour, direct material, variable production

overhead. Further, the fixed expenses are not included in it. In order words, when net profit is

calculated, then fixed and variable cost are deducted and they are not included in gross profit.

Income statement using marginal costing

£ £

Sales 700 x 35 21,000

Cost of Production 13 (W2)x 700 9,100

Less: Closing stock 13(W2) x 100 (1,300)

Variable cost of sale 7,800

Contribution 13,200

Less: Variable sales overhead 1 x600 600

Less: Fixed Costs; Production overhead 2,000

Administration cost 700

Selling cost 600 3,900

Profit 9,300

Interpretation:

5

Less: Variable sales overhead 1 x600 600

Less: Fixed Costs; Administration cost 700

Selling cost 600 1,900

Profit 9,600

Marginal cost: It is a type of costing techniques that enables to prepare income statement

for the organization during the time of financial year. With this respect, it includes both

increment and decrement of the data that creates opportunity for the firm (Figge and Hahn,

2013). More specifically, the opportunity arises when there is extra unit that is developed during

the time of production level. When marginal cost is calculated, then there are only certain

elements includes. In this context, it includes direct labour, direct material, variable production

overhead. Further, the fixed expenses are not included in it. In order words, when net profit is

calculated, then fixed and variable cost are deducted and they are not included in gross profit.

Income statement using marginal costing

£ £

Sales 700 x 35 21,000

Cost of Production 13 (W2)x 700 9,100

Less: Closing stock 13(W2) x 100 (1,300)

Variable cost of sale 7,800

Contribution 13,200

Less: Variable sales overhead 1 x600 600

Less: Fixed Costs; Production overhead 2,000

Administration cost 700

Selling cost 600 3,900

Profit 9,300

Interpretation:

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Aforementioned calculation show that in income statement final income of Nisa retail company

is different. Further, in variable method costing the net yield is higher while in the present

method it is only 9100 GBP. Hence, it shows that the variable approach is the system and it is

taken in consideration that only expenses which can be directly incurred in organization which

can be fluctuated by the level of output. Furthermore, second approach that is absorption costing

approach show less profit of Nisa retail company which lead to reduce the profitability. It

impacts the position of Nisa organization in market and also lead to impact the reputation in

retail industry. It is so because amount of net yield is find out that is 5800 GBP when absorption

method.

There are different type of organization who use absorption costing method instead of using

marginal approach of costing for measuring the financial performance. The main reason behind

choosing absorption system by Nisa retail company is that it support in determine the actual

profit which comes after deducting all expenditures of business activities.

Marginal cost Differences Absorption cost

The method of costing in

which only direct as well as

variable types of costs are to

be included to determine level

of net profit at the year ending

is known as marginal costing.

Due to considering only

variable expenses it called as a

variable method of costing

also

On the basis of meaning While Another costing

approach of derive net yield is

absorption in which direct and

indirect, fixed and variable etc.

all kinds of expenditures

included which comes into

consideration at the workplace

of Nisa store.

Direct material

Direct wages

On the basis of type of costs Cost of direct raw

materials

6

is different. Further, in variable method costing the net yield is higher while in the present

method it is only 9100 GBP. Hence, it shows that the variable approach is the system and it is

taken in consideration that only expenses which can be directly incurred in organization which

can be fluctuated by the level of output. Furthermore, second approach that is absorption costing

approach show less profit of Nisa retail company which lead to reduce the profitability. It

impacts the position of Nisa organization in market and also lead to impact the reputation in

retail industry. It is so because amount of net yield is find out that is 5800 GBP when absorption

method.

There are different type of organization who use absorption costing method instead of using

marginal approach of costing for measuring the financial performance. The main reason behind

choosing absorption system by Nisa retail company is that it support in determine the actual

profit which comes after deducting all expenditures of business activities.

Marginal cost Differences Absorption cost

The method of costing in

which only direct as well as

variable types of costs are to

be included to determine level

of net profit at the year ending

is known as marginal costing.

Due to considering only

variable expenses it called as a

variable method of costing

also

On the basis of meaning While Another costing

approach of derive net yield is

absorption in which direct and

indirect, fixed and variable etc.

all kinds of expenditures

included which comes into

consideration at the workplace

of Nisa store.

Direct material

Direct wages

On the basis of type of costs Cost of direct raw

materials

6

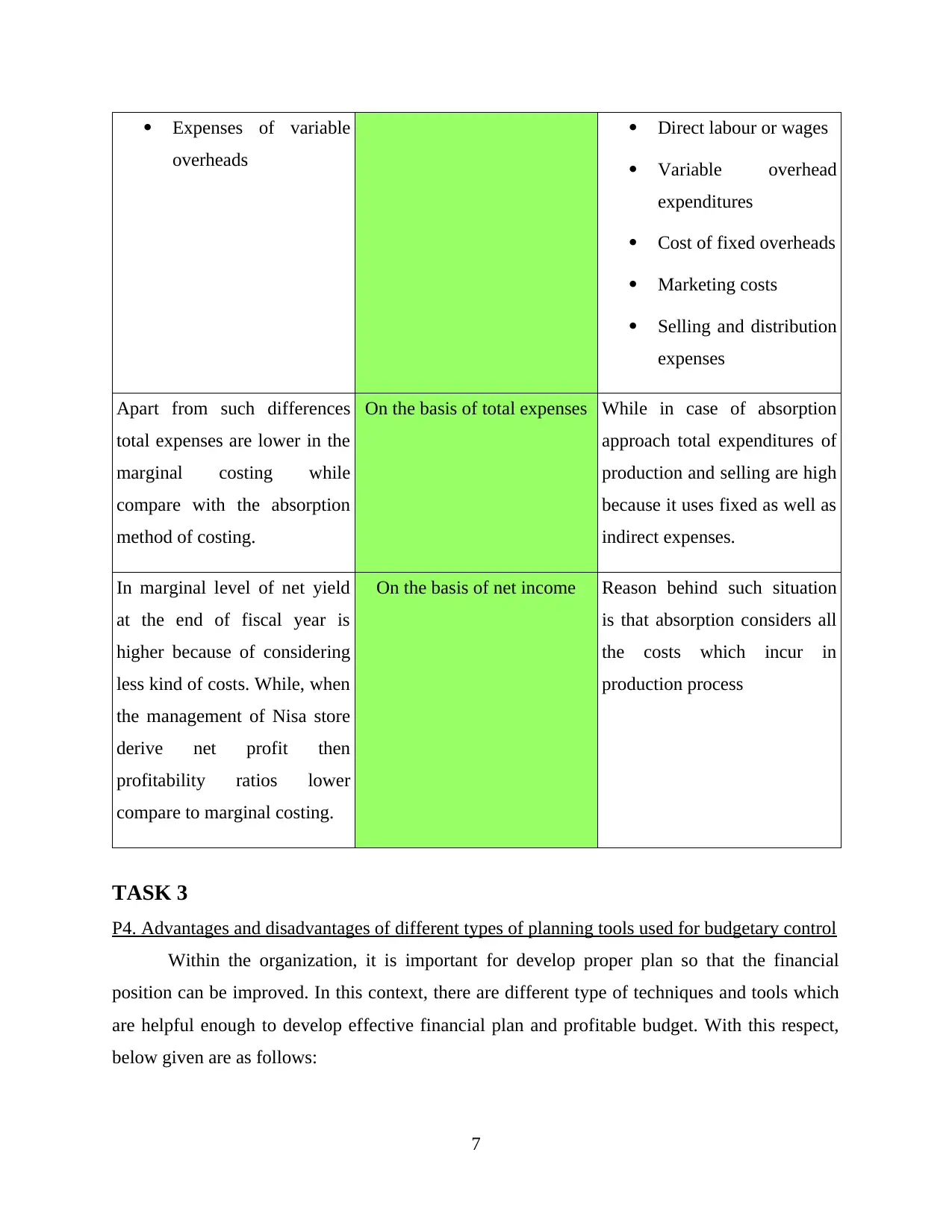

Expenses of variable

overheads

Direct labour or wages

Variable overhead

expenditures

Cost of fixed overheads

Marketing costs

Selling and distribution

expenses

Apart from such differences

total expenses are lower in the

marginal costing while

compare with the absorption

method of costing.

On the basis of total expenses While in case of absorption

approach total expenditures of

production and selling are high

because it uses fixed as well as

indirect expenses.

In marginal level of net yield

at the end of fiscal year is

higher because of considering

less kind of costs. While, when

the management of Nisa store

derive net profit then

profitability ratios lower

compare to marginal costing.

On the basis of net income Reason behind such situation

is that absorption considers all

the costs which incur in

production process

TASK 3

P4. Advantages and disadvantages of different types of planning tools used for budgetary control

Within the organization, it is important for develop proper plan so that the financial

position can be improved. In this context, there are different type of techniques and tools which

are helpful enough to develop effective financial plan and profitable budget. With this respect,

below given are as follows:

7

overheads

Direct labour or wages

Variable overhead

expenditures

Cost of fixed overheads

Marketing costs

Selling and distribution

expenses

Apart from such differences

total expenses are lower in the

marginal costing while

compare with the absorption

method of costing.

On the basis of total expenses While in case of absorption

approach total expenditures of

production and selling are high

because it uses fixed as well as

indirect expenses.

In marginal level of net yield

at the end of fiscal year is

higher because of considering

less kind of costs. While, when

the management of Nisa store

derive net profit then

profitability ratios lower

compare to marginal costing.

On the basis of net income Reason behind such situation

is that absorption considers all

the costs which incur in

production process

TASK 3

P4. Advantages and disadvantages of different types of planning tools used for budgetary control

Within the organization, it is important for develop proper plan so that the financial

position can be improved. In this context, there are different type of techniques and tools which

are helpful enough to develop effective financial plan and profitable budget. With this respect,

below given are as follows:

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

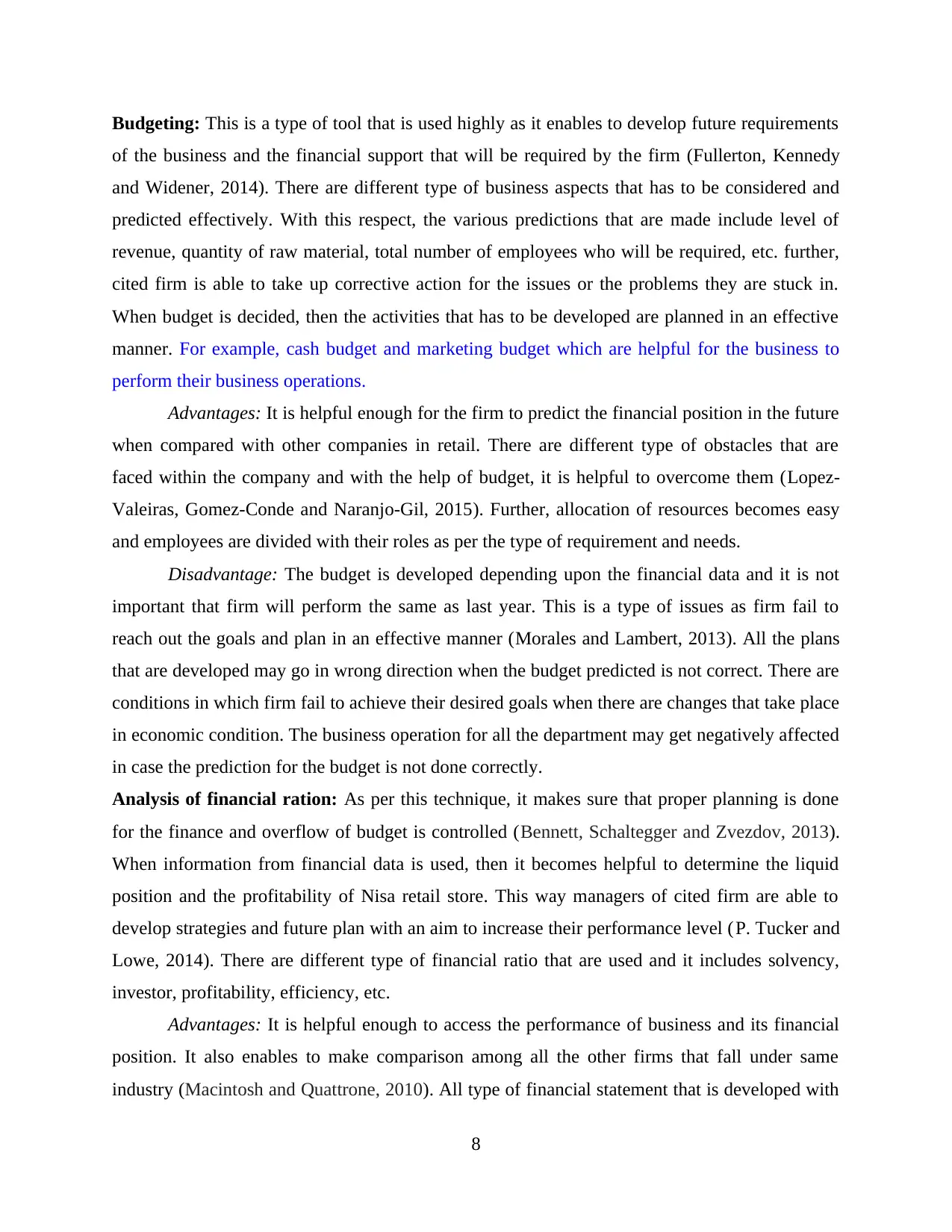

Budgeting: This is a type of tool that is used highly as it enables to develop future requirements

of the business and the financial support that will be required by the firm (Fullerton, Kennedy

and Widener, 2014). There are different type of business aspects that has to be considered and

predicted effectively. With this respect, the various predictions that are made include level of

revenue, quantity of raw material, total number of employees who will be required, etc. further,

cited firm is able to take up corrective action for the issues or the problems they are stuck in.

When budget is decided, then the activities that has to be developed are planned in an effective

manner. For example, cash budget and marketing budget which are helpful for the business to

perform their business operations.

Advantages: It is helpful enough for the firm to predict the financial position in the future

when compared with other companies in retail. There are different type of obstacles that are

faced within the company and with the help of budget, it is helpful to overcome them (Lopez-

Valeiras, Gomez-Conde and Naranjo-Gil, 2015). Further, allocation of resources becomes easy

and employees are divided with their roles as per the type of requirement and needs.

Disadvantage: The budget is developed depending upon the financial data and it is not

important that firm will perform the same as last year. This is a type of issues as firm fail to

reach out the goals and plan in an effective manner (Morales and Lambert, 2013). All the plans

that are developed may go in wrong direction when the budget predicted is not correct. There are

conditions in which firm fail to achieve their desired goals when there are changes that take place

in economic condition. The business operation for all the department may get negatively affected

in case the prediction for the budget is not done correctly.

Analysis of financial ration: As per this technique, it makes sure that proper planning is done

for the finance and overflow of budget is controlled (Bennett, Schaltegger and Zvezdov, 2013).

When information from financial data is used, then it becomes helpful to determine the liquid

position and the profitability of Nisa retail store. This way managers of cited firm are able to

develop strategies and future plan with an aim to increase their performance level (P. Tucker and

Lowe, 2014). There are different type of financial ratio that are used and it includes solvency,

investor, profitability, efficiency, etc.

Advantages: It is helpful enough to access the performance of business and its financial

position. It also enables to make comparison among all the other firms that fall under same

industry (Macintosh and Quattrone, 2010). All type of financial statement that is developed with

8

of the business and the financial support that will be required by the firm (Fullerton, Kennedy

and Widener, 2014). There are different type of business aspects that has to be considered and

predicted effectively. With this respect, the various predictions that are made include level of

revenue, quantity of raw material, total number of employees who will be required, etc. further,

cited firm is able to take up corrective action for the issues or the problems they are stuck in.

When budget is decided, then the activities that has to be developed are planned in an effective

manner. For example, cash budget and marketing budget which are helpful for the business to

perform their business operations.

Advantages: It is helpful enough for the firm to predict the financial position in the future

when compared with other companies in retail. There are different type of obstacles that are

faced within the company and with the help of budget, it is helpful to overcome them (Lopez-

Valeiras, Gomez-Conde and Naranjo-Gil, 2015). Further, allocation of resources becomes easy

and employees are divided with their roles as per the type of requirement and needs.

Disadvantage: The budget is developed depending upon the financial data and it is not

important that firm will perform the same as last year. This is a type of issues as firm fail to

reach out the goals and plan in an effective manner (Morales and Lambert, 2013). All the plans

that are developed may go in wrong direction when the budget predicted is not correct. There are

conditions in which firm fail to achieve their desired goals when there are changes that take place

in economic condition. The business operation for all the department may get negatively affected

in case the prediction for the budget is not done correctly.

Analysis of financial ration: As per this technique, it makes sure that proper planning is done

for the finance and overflow of budget is controlled (Bennett, Schaltegger and Zvezdov, 2013).

When information from financial data is used, then it becomes helpful to determine the liquid

position and the profitability of Nisa retail store. This way managers of cited firm are able to

develop strategies and future plan with an aim to increase their performance level (P. Tucker and

Lowe, 2014). There are different type of financial ratio that are used and it includes solvency,

investor, profitability, efficiency, etc.

Advantages: It is helpful enough to access the performance of business and its financial

position. It also enables to make comparison among all the other firms that fall under same

industry (Macintosh and Quattrone, 2010). All type of financial statement that is developed with

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

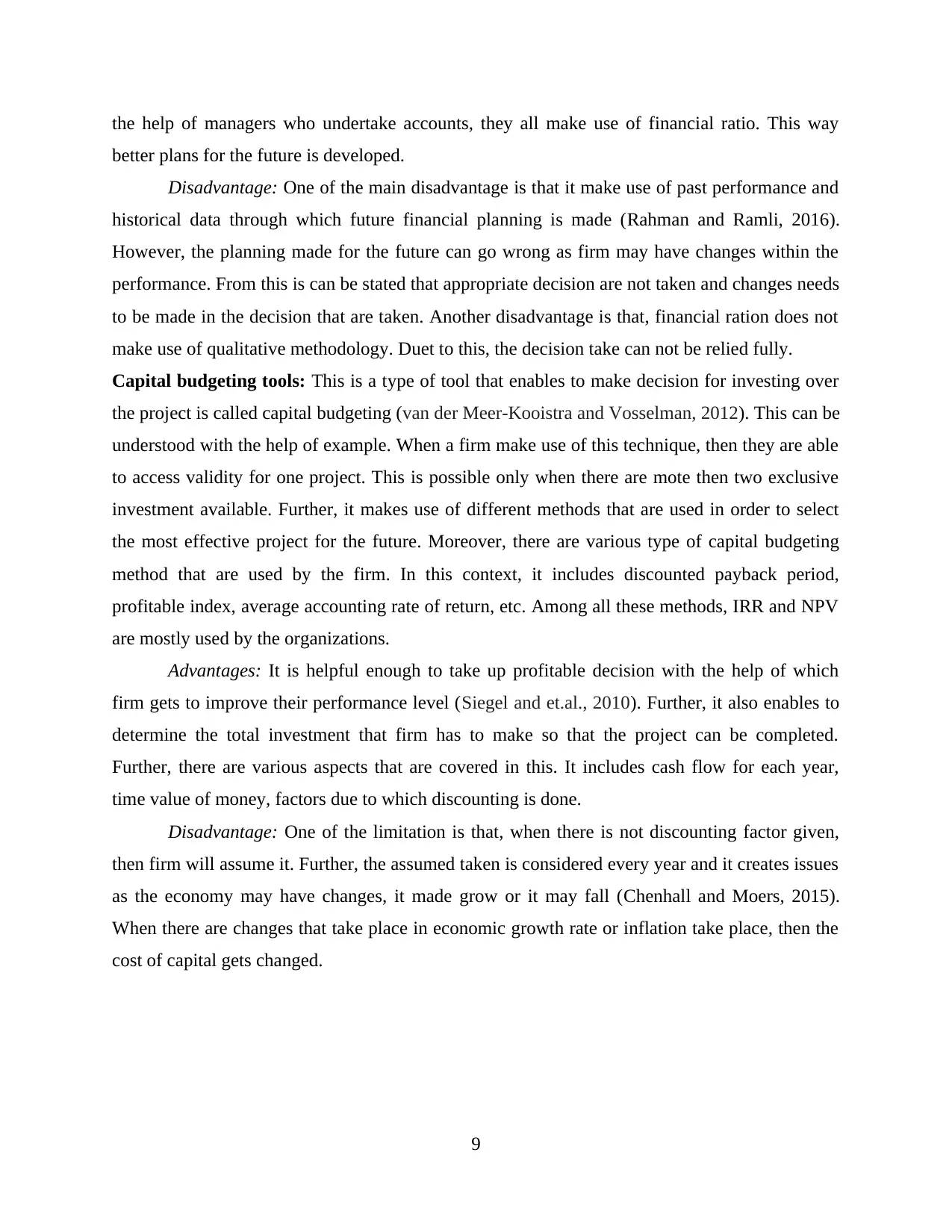

the help of managers who undertake accounts, they all make use of financial ratio. This way

better plans for the future is developed.

Disadvantage: One of the main disadvantage is that it make use of past performance and

historical data through which future financial planning is made (Rahman and Ramli, 2016).

However, the planning made for the future can go wrong as firm may have changes within the

performance. From this is can be stated that appropriate decision are not taken and changes needs

to be made in the decision that are taken. Another disadvantage is that, financial ration does not

make use of qualitative methodology. Duet to this, the decision take can not be relied fully.

Capital budgeting tools: This is a type of tool that enables to make decision for investing over

the project is called capital budgeting (van der Meer-Kooistra and Vosselman, 2012). This can be

understood with the help of example. When a firm make use of this technique, then they are able

to access validity for one project. This is possible only when there are mote then two exclusive

investment available. Further, it makes use of different methods that are used in order to select

the most effective project for the future. Moreover, there are various type of capital budgeting

method that are used by the firm. In this context, it includes discounted payback period,

profitable index, average accounting rate of return, etc. Among all these methods, IRR and NPV

are mostly used by the organizations.

Advantages: It is helpful enough to take up profitable decision with the help of which

firm gets to improve their performance level (Siegel and et.al., 2010). Further, it also enables to

determine the total investment that firm has to make so that the project can be completed.

Further, there are various aspects that are covered in this. It includes cash flow for each year,

time value of money, factors due to which discounting is done.

Disadvantage: One of the limitation is that, when there is not discounting factor given,

then firm will assume it. Further, the assumed taken is considered every year and it creates issues

as the economy may have changes, it made grow or it may fall (Chenhall and Moers, 2015).

When there are changes that take place in economic growth rate or inflation take place, then the

cost of capital gets changed.

9

better plans for the future is developed.

Disadvantage: One of the main disadvantage is that it make use of past performance and

historical data through which future financial planning is made (Rahman and Ramli, 2016).

However, the planning made for the future can go wrong as firm may have changes within the

performance. From this is can be stated that appropriate decision are not taken and changes needs

to be made in the decision that are taken. Another disadvantage is that, financial ration does not

make use of qualitative methodology. Duet to this, the decision take can not be relied fully.

Capital budgeting tools: This is a type of tool that enables to make decision for investing over

the project is called capital budgeting (van der Meer-Kooistra and Vosselman, 2012). This can be

understood with the help of example. When a firm make use of this technique, then they are able

to access validity for one project. This is possible only when there are mote then two exclusive

investment available. Further, it makes use of different methods that are used in order to select

the most effective project for the future. Moreover, there are various type of capital budgeting

method that are used by the firm. In this context, it includes discounted payback period,

profitable index, average accounting rate of return, etc. Among all these methods, IRR and NPV

are mostly used by the organizations.

Advantages: It is helpful enough to take up profitable decision with the help of which

firm gets to improve their performance level (Siegel and et.al., 2010). Further, it also enables to

determine the total investment that firm has to make so that the project can be completed.

Further, there are various aspects that are covered in this. It includes cash flow for each year,

time value of money, factors due to which discounting is done.

Disadvantage: One of the limitation is that, when there is not discounting factor given,

then firm will assume it. Further, the assumed taken is considered every year and it creates issues

as the economy may have changes, it made grow or it may fall (Chenhall and Moers, 2015).

When there are changes that take place in economic growth rate or inflation take place, then the

cost of capital gets changed.

9

TASK 4

P5. Comparing ways through which Nisa retail store is adapting management accounting

systems to respond to financial

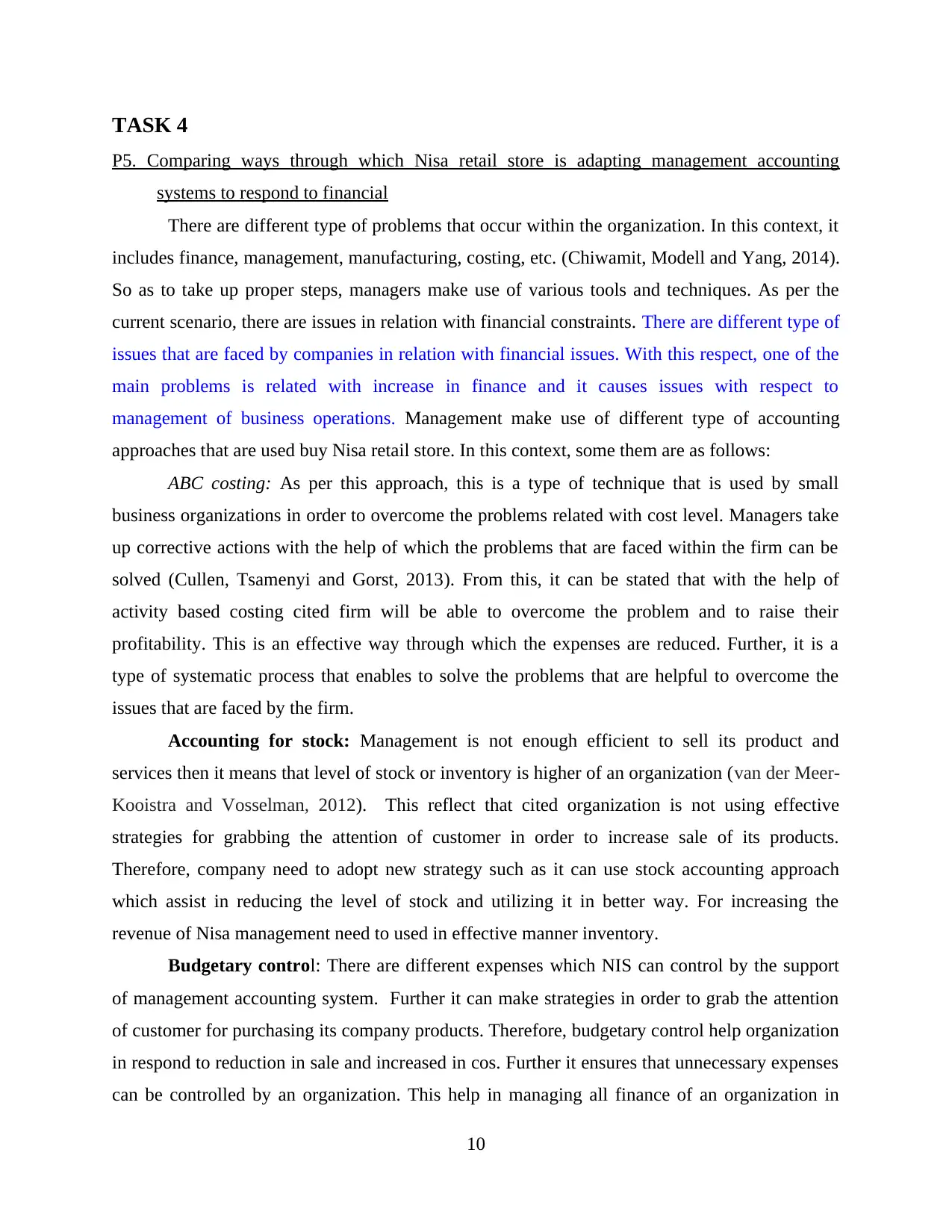

There are different type of problems that occur within the organization. In this context, it

includes finance, management, manufacturing, costing, etc. (Chiwamit, Modell and Yang, 2014).

So as to take up proper steps, managers make use of various tools and techniques. As per the

current scenario, there are issues in relation with financial constraints. There are different type of

issues that are faced by companies in relation with financial issues. With this respect, one of the

main problems is related with increase in finance and it causes issues with respect to

management of business operations. Management make use of different type of accounting

approaches that are used buy Nisa retail store. In this context, some them are as follows:

ABC costing: As per this approach, this is a type of technique that is used by small

business organizations in order to overcome the problems related with cost level. Managers take

up corrective actions with the help of which the problems that are faced within the firm can be

solved (Cullen, Tsamenyi and Gorst, 2013). From this, it can be stated that with the help of

activity based costing cited firm will be able to overcome the problem and to raise their

profitability. This is an effective way through which the expenses are reduced. Further, it is a

type of systematic process that enables to solve the problems that are helpful to overcome the

issues that are faced by the firm.

Accounting for stock: Management is not enough efficient to sell its product and

services then it means that level of stock or inventory is higher of an organization (van der Meer-

Kooistra and Vosselman, 2012). This reflect that cited organization is not using effective

strategies for grabbing the attention of customer in order to increase sale of its products.

Therefore, company need to adopt new strategy such as it can use stock accounting approach

which assist in reducing the level of stock and utilizing it in better way. For increasing the

revenue of Nisa management need to used in effective manner inventory.

Budgetary control: There are different expenses which NIS can control by the support

of management accounting system. Further it can make strategies in order to grab the attention

of customer for purchasing its company products. Therefore, budgetary control help organization

in respond to reduction in sale and increased in cos. Further it ensures that unnecessary expenses

can be controlled by an organization. This help in managing all finance of an organization in

10

P5. Comparing ways through which Nisa retail store is adapting management accounting

systems to respond to financial

There are different type of problems that occur within the organization. In this context, it

includes finance, management, manufacturing, costing, etc. (Chiwamit, Modell and Yang, 2014).

So as to take up proper steps, managers make use of various tools and techniques. As per the

current scenario, there are issues in relation with financial constraints. There are different type of

issues that are faced by companies in relation with financial issues. With this respect, one of the

main problems is related with increase in finance and it causes issues with respect to

management of business operations. Management make use of different type of accounting

approaches that are used buy Nisa retail store. In this context, some them are as follows:

ABC costing: As per this approach, this is a type of technique that is used by small

business organizations in order to overcome the problems related with cost level. Managers take

up corrective actions with the help of which the problems that are faced within the firm can be

solved (Cullen, Tsamenyi and Gorst, 2013). From this, it can be stated that with the help of

activity based costing cited firm will be able to overcome the problem and to raise their

profitability. This is an effective way through which the expenses are reduced. Further, it is a

type of systematic process that enables to solve the problems that are helpful to overcome the

issues that are faced by the firm.

Accounting for stock: Management is not enough efficient to sell its product and

services then it means that level of stock or inventory is higher of an organization (van der Meer-

Kooistra and Vosselman, 2012). This reflect that cited organization is not using effective

strategies for grabbing the attention of customer in order to increase sale of its products.

Therefore, company need to adopt new strategy such as it can use stock accounting approach

which assist in reducing the level of stock and utilizing it in better way. For increasing the

revenue of Nisa management need to used in effective manner inventory.

Budgetary control: There are different expenses which NIS can control by the support

of management accounting system. Further it can make strategies in order to grab the attention

of customer for purchasing its company products. Therefore, budgetary control help organization

in respond to reduction in sale and increased in cos. Further it ensures that unnecessary expenses

can be controlled by an organization. This help in managing all finance of an organization in

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.