Management Accounting Report: Business Analysis of OAK Cash and Carry

VerifiedAdded on 2020/12/09

|18

|5490

|134

Report

AI Summary

This report provides a comprehensive analysis of management accounting practices within OAK Cash and Carry, a UK-based retail company. It begins with an introduction to management accounting, detailing its role in decision-making and financial reporting, and then explores various accounting systems, including cost accounting, inventory management, job costing, and price optimization systems, highlighting their advantages and applications within the company. The report then examines different management accounting reporting methods, such as budgeting, cost, and performance reports, and evaluates their integration within OAK Cash and Carry's organizational processes. Furthermore, it delves into cost analysis techniques, specifically marginal and absorption costing, to prepare income statements. The report also discusses the advantages and disadvantages of planning tools used for budgetary control and concludes with a comparison of how organizations adapt management accounting systems to address financial challenges.

MANAGEMENT

ACCOUNTANTING

ACCOUNTANTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting and requirements of different kinds of accounting systems..........1

P2 Methods used for management accounting reporting............................................................3

TASK 2............................................................................................................................................5

P3 Techniques of cost analysis to prepare an income statement using marginal and absorption

costs.............................................................................................................................................5

TASK 3............................................................................................................................................8

P4 Advantages and disadvantages of different planning tools used for budgetary control........8

TASK 4 .........................................................................................................................................11

P5 Comparison on how organisations are adapting management accounting systems............11

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting and requirements of different kinds of accounting systems..........1

P2 Methods used for management accounting reporting............................................................3

TASK 2............................................................................................................................................5

P3 Techniques of cost analysis to prepare an income statement using marginal and absorption

costs.............................................................................................................................................5

TASK 3............................................................................................................................................8

P4 Advantages and disadvantages of different planning tools used for budgetary control........8

TASK 4 .........................................................................................................................................11

P5 Comparison on how organisations are adapting management accounting systems............11

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION

Management accounting is a process that assist firms in developing and keeping

managerial records as it will further assist company in taking appropriate decision for its

business operations. Books under which all data and records are kept are further used by

companies in gaining trust of stakeholders, investors, creditors etc. OAK Cash and Carry is one

of the leading company in United Kingdom which has less than 50 number of employee. Present

report includes demonstration and understanding of management accounting system. Other than

this, calculation of cost with the help of appropriate techniques related to cost analysis is

included in this in order to prepare an income statement with the help of marginal and absorption

costs (DRURY, 2013). Different type of tools and management accounting system for

responding financial problems is also discussed in further part which help in analysing position

of business at marketplace.

Management accounting is a process that assist firms in developing and keeping

managerial records as it will further assist company in taking appropriate decision for its

business operations. Books under which all data and records are kept are further used by

companies in gaining trust of stakeholders, investors, creditors etc. OAK Cash and Carry is one

of the leading company in United Kingdom which has less than 50 number of employee. Present

report includes demonstration and understanding of management accounting system. Other than

this, calculation of cost with the help of appropriate techniques related to cost analysis is

included in this in order to prepare an income statement with the help of marginal and absorption

costs (DRURY, 2013). Different type of tools and management accounting system for

responding financial problems is also discussed in further part which help in analysing position

of business at marketplace.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 1

P1 Management accounting and requirements of different kinds of accounting systems

Management accounting can be defined as a process of preparing accounts and reports

which give financial and statistical information in an accurate manner. It includes information

about day-to-day transactions and short term decisions. Along with this, it can also stated as

representation of accounting information by which managers of a company can formulate

policies and strategies for conducting activities as well as take decisions on regular manner.

Moreover, it is based on financial and cost accounting with main objectives are measuring

performance, assessing risks, allocating resources and more.

OAK Cash and Carry deals in retail market and deliver groceries as well as home utility

products to customers of UK on affordable price rates (Springer.Arroyo, 2012) on affordable

price rates (Springer.Arroyo, 2012). This organisation use management accounting systems in

order to take important decision related to utilise financial resources for day-to-day operations.

Types of accounting systems and their needs:

System of management and accounting helps a firm in organising and controlling overall

activities of business by determining different costs of the same. It also varies as per application

and assist in making proper decisions (Tools of management and accounting, 2018). There are

various managing accounting systems are available like inventory management, price

optimisation, job costing system and more. Some of them are stated as below:

Cost accounting system: It is considered as framework which applied by management

of a company for inventory valuation by approximating costs of products. In this

system, allocation of cost is generally based either on activity or traditional costing.

Managers of OAK Cash and Carry use this system to capture production cost by

weighing input and fixed costs such as capital equipment depreciation. Along with this,

costs accounting system helps in discovering all costs related with distributing,

marketing, production, selling and more through which employers can assume future

profitability ratio. As OAK Cash and Carry is engaged with many functions like

manufacturing and delivering best quality of products which includes much expenses.

Therefore, with the help of cost accounting system, its managers can control all

expenses. Along with this, it also includes two types of cost accounting that are Job

Costing and Process Costing. In job costings, managers can track actual cost of product

P1 Management accounting and requirements of different kinds of accounting systems

Management accounting can be defined as a process of preparing accounts and reports

which give financial and statistical information in an accurate manner. It includes information

about day-to-day transactions and short term decisions. Along with this, it can also stated as

representation of accounting information by which managers of a company can formulate

policies and strategies for conducting activities as well as take decisions on regular manner.

Moreover, it is based on financial and cost accounting with main objectives are measuring

performance, assessing risks, allocating resources and more.

OAK Cash and Carry deals in retail market and deliver groceries as well as home utility

products to customers of UK on affordable price rates (Springer.Arroyo, 2012) on affordable

price rates (Springer.Arroyo, 2012). This organisation use management accounting systems in

order to take important decision related to utilise financial resources for day-to-day operations.

Types of accounting systems and their needs:

System of management and accounting helps a firm in organising and controlling overall

activities of business by determining different costs of the same. It also varies as per application

and assist in making proper decisions (Tools of management and accounting, 2018). There are

various managing accounting systems are available like inventory management, price

optimisation, job costing system and more. Some of them are stated as below:

Cost accounting system: It is considered as framework which applied by management

of a company for inventory valuation by approximating costs of products. In this

system, allocation of cost is generally based either on activity or traditional costing.

Managers of OAK Cash and Carry use this system to capture production cost by

weighing input and fixed costs such as capital equipment depreciation. Along with this,

costs accounting system helps in discovering all costs related with distributing,

marketing, production, selling and more through which employers can assume future

profitability ratio. As OAK Cash and Carry is engaged with many functions like

manufacturing and delivering best quality of products which includes much expenses.

Therefore, with the help of cost accounting system, its managers can control all

expenses. Along with this, it also includes two types of cost accounting that are Job

Costing and Process Costing. In job costings, managers can track actual cost of product

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

by summing up materials and overhead expensed of manufacturing process. Since,

OAK Cash and Carry produces different type of products or services so, process

costing helps in specifying costs to each.

Inventory management system: This system belongs to method of controlling as well

as overseeing the usage and storage of components that management of a company

applies in production of goods which are ready for sale. It combines various

applications such as desktop software, mobile devices, barcode scanner and printers.

All these applications helps in streamlining the inventory management like goods,

stocks, consumables and suppliers. Managers of OAK Cash and Carry use this system

for minimising overstock situations and track record of inventories across different

level. It gives various benefits like improving bottom line of business, increasing

accuracy of inventory as well as developing workflow of company. In inventory

management, LIFO and FIFO are some accounting methods which helps in handling

operations of business. In this regard, FIFO i.e. First In First Out states a firm in

getting rid for old inventories first. While LIFO- Last In First Out assist in leaving last

inventories first.

Job costing system: It is generally used for allocating costs of manufacturing products

if process of goods are different from each other. Moreover, this system includes

various practices of compiling data on the costs belongs to particular services or job

(Bodie, 2013). Company which deals in customised goods like OAK Cash and Carry

use this system to provide information to customers for submit cost data as per contract

under which costs are refunded as well. Thus, it will help in assuming cost which can

be utilised in decisions-making process related to material procurement and need of

labours. It includes three main components that are- Direct Materials, Direct Labour

and Overhead. Under this, job costing helps in tracking cost of materials and other

resources used in manufacturing. It also assists managers of this company in

determining what employees charge for doing a specific job. While overhead costs

include depreciation on equipment of production and building rent etc. as cost pools.

Price optimisation system: It belongs to application of different mathematical analysis

to business corporation for determining the response of customers with different price

rates of products. Thus, price optimising refers to a process of determining rates by

OAK Cash and Carry produces different type of products or services so, process

costing helps in specifying costs to each.

Inventory management system: This system belongs to method of controlling as well

as overseeing the usage and storage of components that management of a company

applies in production of goods which are ready for sale. It combines various

applications such as desktop software, mobile devices, barcode scanner and printers.

All these applications helps in streamlining the inventory management like goods,

stocks, consumables and suppliers. Managers of OAK Cash and Carry use this system

for minimising overstock situations and track record of inventories across different

level. It gives various benefits like improving bottom line of business, increasing

accuracy of inventory as well as developing workflow of company. In inventory

management, LIFO and FIFO are some accounting methods which helps in handling

operations of business. In this regard, FIFO i.e. First In First Out states a firm in

getting rid for old inventories first. While LIFO- Last In First Out assist in leaving last

inventories first.

Job costing system: It is generally used for allocating costs of manufacturing products

if process of goods are different from each other. Moreover, this system includes

various practices of compiling data on the costs belongs to particular services or job

(Bodie, 2013). Company which deals in customised goods like OAK Cash and Carry

use this system to provide information to customers for submit cost data as per contract

under which costs are refunded as well. Thus, it will help in assuming cost which can

be utilised in decisions-making process related to material procurement and need of

labours. It includes three main components that are- Direct Materials, Direct Labour

and Overhead. Under this, job costing helps in tracking cost of materials and other

resources used in manufacturing. It also assists managers of this company in

determining what employees charge for doing a specific job. While overhead costs

include depreciation on equipment of production and building rent etc. as cost pools.

Price optimisation system: It belongs to application of different mathematical analysis

to business corporation for determining the response of customers with different price

rates of products. Thus, price optimising refers to a process of determining rates by

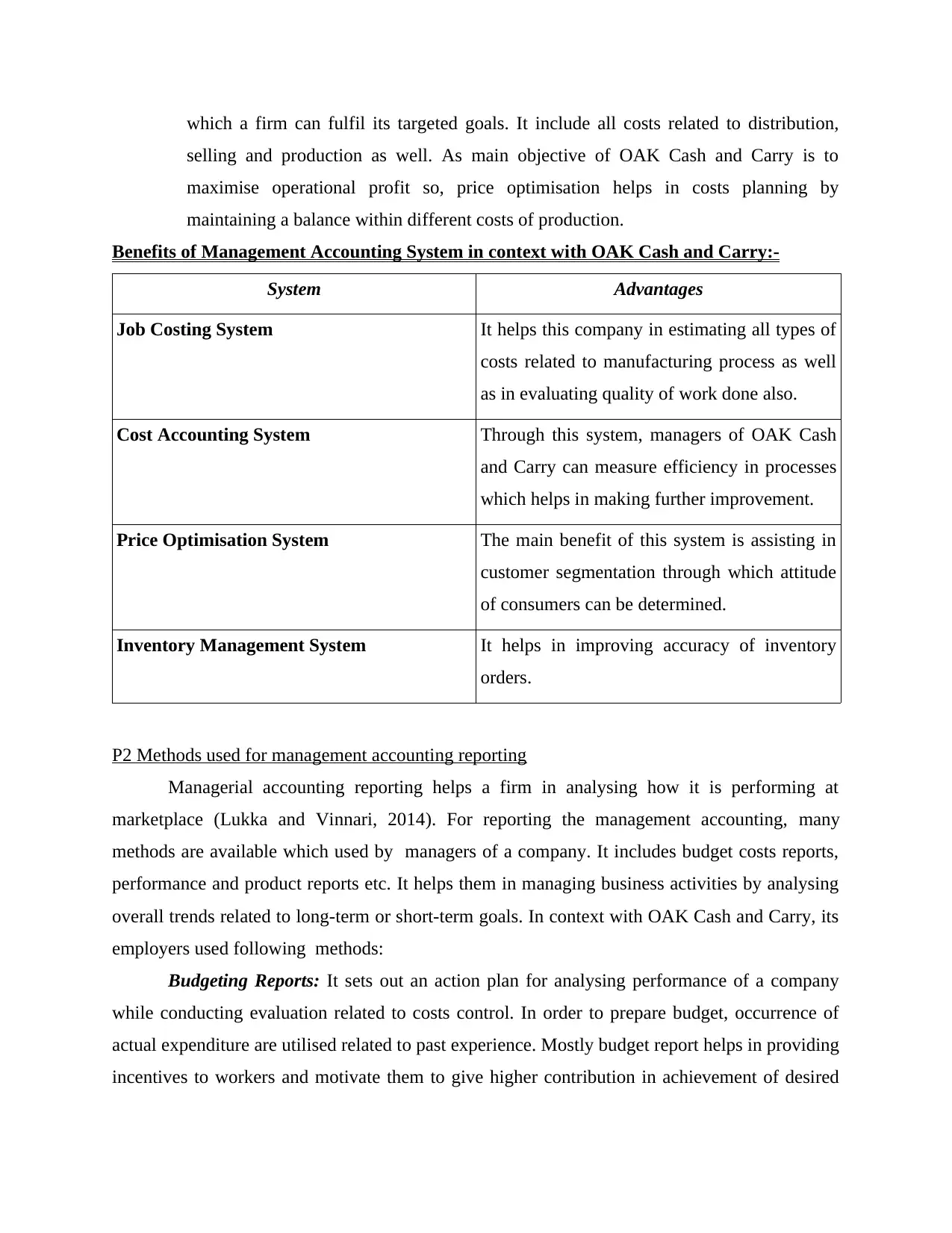

which a firm can fulfil its targeted goals. It include all costs related to distribution,

selling and production as well. As main objective of OAK Cash and Carry is to

maximise operational profit so, price optimisation helps in costs planning by

maintaining a balance within different costs of production.

Benefits of Management Accounting System in context with OAK Cash and Carry:-

System Advantages

Job Costing System It helps this company in estimating all types of

costs related to manufacturing process as well

as in evaluating quality of work done also.

Cost Accounting System Through this system, managers of OAK Cash

and Carry can measure efficiency in processes

which helps in making further improvement.

Price Optimisation System The main benefit of this system is assisting in

customer segmentation through which attitude

of consumers can be determined.

Inventory Management System It helps in improving accuracy of inventory

orders.

P2 Methods used for management accounting reporting

Managerial accounting reporting helps a firm in analysing how it is performing at

marketplace (Lukka and Vinnari, 2014). For reporting the management accounting, many

methods are available which used by managers of a company. It includes budget costs reports,

performance and product reports etc. It helps them in managing business activities by analysing

overall trends related to long-term or short-term goals. In context with OAK Cash and Carry, its

employers used following methods:

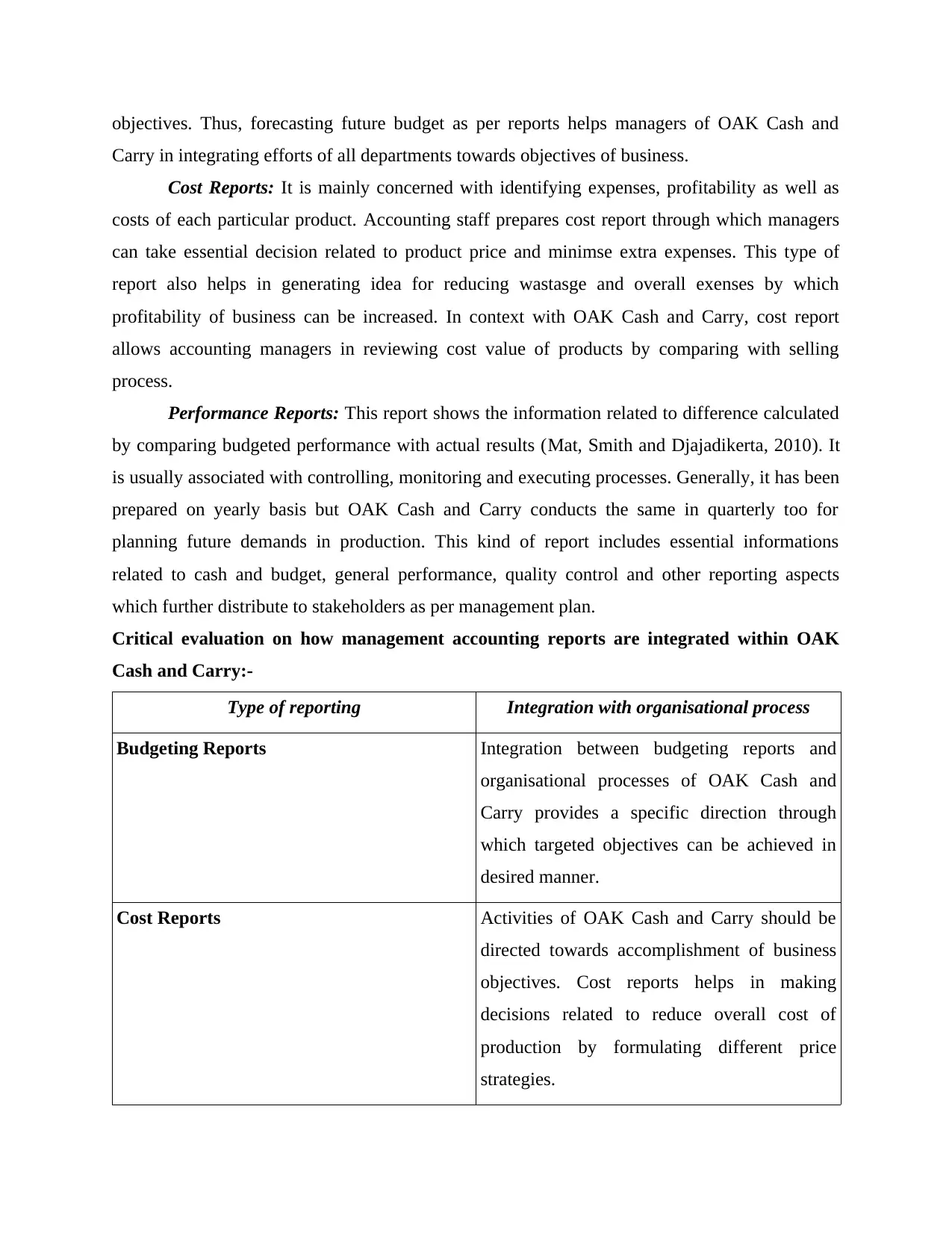

Budgeting Reports: It sets out an action plan for analysing performance of a company

while conducting evaluation related to costs control. In order to prepare budget, occurrence of

actual expenditure are utilised related to past experience. Mostly budget report helps in providing

incentives to workers and motivate them to give higher contribution in achievement of desired

selling and production as well. As main objective of OAK Cash and Carry is to

maximise operational profit so, price optimisation helps in costs planning by

maintaining a balance within different costs of production.

Benefits of Management Accounting System in context with OAK Cash and Carry:-

System Advantages

Job Costing System It helps this company in estimating all types of

costs related to manufacturing process as well

as in evaluating quality of work done also.

Cost Accounting System Through this system, managers of OAK Cash

and Carry can measure efficiency in processes

which helps in making further improvement.

Price Optimisation System The main benefit of this system is assisting in

customer segmentation through which attitude

of consumers can be determined.

Inventory Management System It helps in improving accuracy of inventory

orders.

P2 Methods used for management accounting reporting

Managerial accounting reporting helps a firm in analysing how it is performing at

marketplace (Lukka and Vinnari, 2014). For reporting the management accounting, many

methods are available which used by managers of a company. It includes budget costs reports,

performance and product reports etc. It helps them in managing business activities by analysing

overall trends related to long-term or short-term goals. In context with OAK Cash and Carry, its

employers used following methods:

Budgeting Reports: It sets out an action plan for analysing performance of a company

while conducting evaluation related to costs control. In order to prepare budget, occurrence of

actual expenditure are utilised related to past experience. Mostly budget report helps in providing

incentives to workers and motivate them to give higher contribution in achievement of desired

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

objectives. Thus, forecasting future budget as per reports helps managers of OAK Cash and

Carry in integrating efforts of all departments towards objectives of business.

Cost Reports: It is mainly concerned with identifying expenses, profitability as well as

costs of each particular product. Accounting staff prepares cost report through which managers

can take essential decision related to product price and minimse extra expenses. This type of

report also helps in generating idea for reducing wastasge and overall exenses by which

profitability of business can be increased. In context with OAK Cash and Carry, cost report

allows accounting managers in reviewing cost value of products by comparing with selling

process.

Performance Reports: This report shows the information related to difference calculated

by comparing budgeted performance with actual results (Mat, Smith and Djajadikerta, 2010). It

is usually associated with controlling, monitoring and executing processes. Generally, it has been

prepared on yearly basis but OAK Cash and Carry conducts the same in quarterly too for

planning future demands in production. This kind of report includes essential informations

related to cash and budget, general performance, quality control and other reporting aspects

which further distribute to stakeholders as per management plan.

Critical evaluation on how management accounting reports are integrated within OAK

Cash and Carry:-

Type of reporting Integration with organisational process

Budgeting Reports Integration between budgeting reports and

organisational processes of OAK Cash and

Carry provides a specific direction through

which targeted objectives can be achieved in

desired manner.

Cost Reports Activities of OAK Cash and Carry should be

directed towards accomplishment of business

objectives. Cost reports helps in making

decisions related to reduce overall cost of

production by formulating different price

strategies.

Carry in integrating efforts of all departments towards objectives of business.

Cost Reports: It is mainly concerned with identifying expenses, profitability as well as

costs of each particular product. Accounting staff prepares cost report through which managers

can take essential decision related to product price and minimse extra expenses. This type of

report also helps in generating idea for reducing wastasge and overall exenses by which

profitability of business can be increased. In context with OAK Cash and Carry, cost report

allows accounting managers in reviewing cost value of products by comparing with selling

process.

Performance Reports: This report shows the information related to difference calculated

by comparing budgeted performance with actual results (Mat, Smith and Djajadikerta, 2010). It

is usually associated with controlling, monitoring and executing processes. Generally, it has been

prepared on yearly basis but OAK Cash and Carry conducts the same in quarterly too for

planning future demands in production. This kind of report includes essential informations

related to cash and budget, general performance, quality control and other reporting aspects

which further distribute to stakeholders as per management plan.

Critical evaluation on how management accounting reports are integrated within OAK

Cash and Carry:-

Type of reporting Integration with organisational process

Budgeting Reports Integration between budgeting reports and

organisational processes of OAK Cash and

Carry provides a specific direction through

which targeted objectives can be achieved in

desired manner.

Cost Reports Activities of OAK Cash and Carry should be

directed towards accomplishment of business

objectives. Cost reports helps in making

decisions related to reduce overall cost of

production by formulating different price

strategies.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Performance Reports Integration among performance reports and

process of OAK Cash and Carry help managers

in planning for future production.

TASK 2

P3 Techniques of cost analysis to prepare an income statement using marginal and absorption

costs

Costs is generally referred to value of money and used for producing and representing

monitory evaluation of resources, materials, efforts, risk incurred and more (Harris and Durden,

2012). The costs which remains constant for a certain level of output as well as does not get

fluctuated with variation is termed as fixed costs. But, per unit fixed cost of goods will get

decrease when there is an increase in production. It includes depreciation, rents and more. While

costs that varies with variation is considered as variable costs which has direct relationship with

production. As when there is increase in production then variable costs also enhance and vice

versa like labour, raw materials and more. For preparing an income statement, managers of OAK

Cash and Carry use absorption and marginal cost whose concept can be explained in following

manner:

Marginal costing- It can be described as the accounting system under which variable

costs are allocated to different costs units. While fixed costs is written off for a specific period to

the aggregate contribution (Managerial Accounting. 2017). Therefore, it is considered as relevant

source for purpose of decisions-making. As it is simple technique for cost information analysis

where managers give their efforts in identifying changes in production level which effect ratio of

profitability.

Absorption costing – This concept of accounting system treat overall cost of production

as product costs by taking under consideration all expenses and resources related to the same. It

includes labour, material as well as both variable and fixed overhead cost (Tsafe and Rahman,

2014). This identification of costs helps managers of OAK Cash and Carry in utilising

information for decision-making process.

As per present case study, the cost card of OAK Cash and Carry is given as below:-

£

process of OAK Cash and Carry help managers

in planning for future production.

TASK 2

P3 Techniques of cost analysis to prepare an income statement using marginal and absorption

costs

Costs is generally referred to value of money and used for producing and representing

monitory evaluation of resources, materials, efforts, risk incurred and more (Harris and Durden,

2012). The costs which remains constant for a certain level of output as well as does not get

fluctuated with variation is termed as fixed costs. But, per unit fixed cost of goods will get

decrease when there is an increase in production. It includes depreciation, rents and more. While

costs that varies with variation is considered as variable costs which has direct relationship with

production. As when there is increase in production then variable costs also enhance and vice

versa like labour, raw materials and more. For preparing an income statement, managers of OAK

Cash and Carry use absorption and marginal cost whose concept can be explained in following

manner:

Marginal costing- It can be described as the accounting system under which variable

costs are allocated to different costs units. While fixed costs is written off for a specific period to

the aggregate contribution (Managerial Accounting. 2017). Therefore, it is considered as relevant

source for purpose of decisions-making. As it is simple technique for cost information analysis

where managers give their efforts in identifying changes in production level which effect ratio of

profitability.

Absorption costing – This concept of accounting system treat overall cost of production

as product costs by taking under consideration all expenses and resources related to the same. It

includes labour, material as well as both variable and fixed overhead cost (Tsafe and Rahman,

2014). This identification of costs helps managers of OAK Cash and Carry in utilising

information for decision-making process.

As per present case study, the cost card of OAK Cash and Carry is given as below:-

£

Direct Labour 6

Direct Material 7

Variable Production Overhead 2

Fixed Production Overhead 1

Fixed Production Overhead incurred

actually

£6000

Variable selling & distribution expenses 30% of sales value

Selling Price 55

Sales 20000

Working Notes:

Formula of marginal costing:

sales revenue – marginal cost of goods sold = contribution – fixed cost = net income

Particulars Amount

Sales revenue = (selling price * no. of goods sold = 55 * 600) 33000

Marginal Cost of goods sold: 9600

Production = (units produced * marginal cost per unit = 800 * 16) 12800

closing stock = (closing stock units * marginal cost per unit = 200 *

16) 3200

Contribution 23400

Fixed cost ( 3200+1200+1500 ) 5900

Net profit 17500

Formula of absorption costing:

Direct Material 7

Variable Production Overhead 2

Fixed Production Overhead 1

Fixed Production Overhead incurred

actually

£6000

Variable selling & distribution expenses 30% of sales value

Selling Price 55

Sales 20000

Working Notes:

Formula of marginal costing:

sales revenue – marginal cost of goods sold = contribution – fixed cost = net income

Particulars Amount

Sales revenue = (selling price * no. of goods sold = 55 * 600) 33000

Marginal Cost of goods sold: 9600

Production = (units produced * marginal cost per unit = 800 * 16) 12800

closing stock = (closing stock units * marginal cost per unit = 200 *

16) 3200

Contribution 23400

Fixed cost ( 3200+1200+1500 ) 5900

Net profit 17500

Formula of absorption costing:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

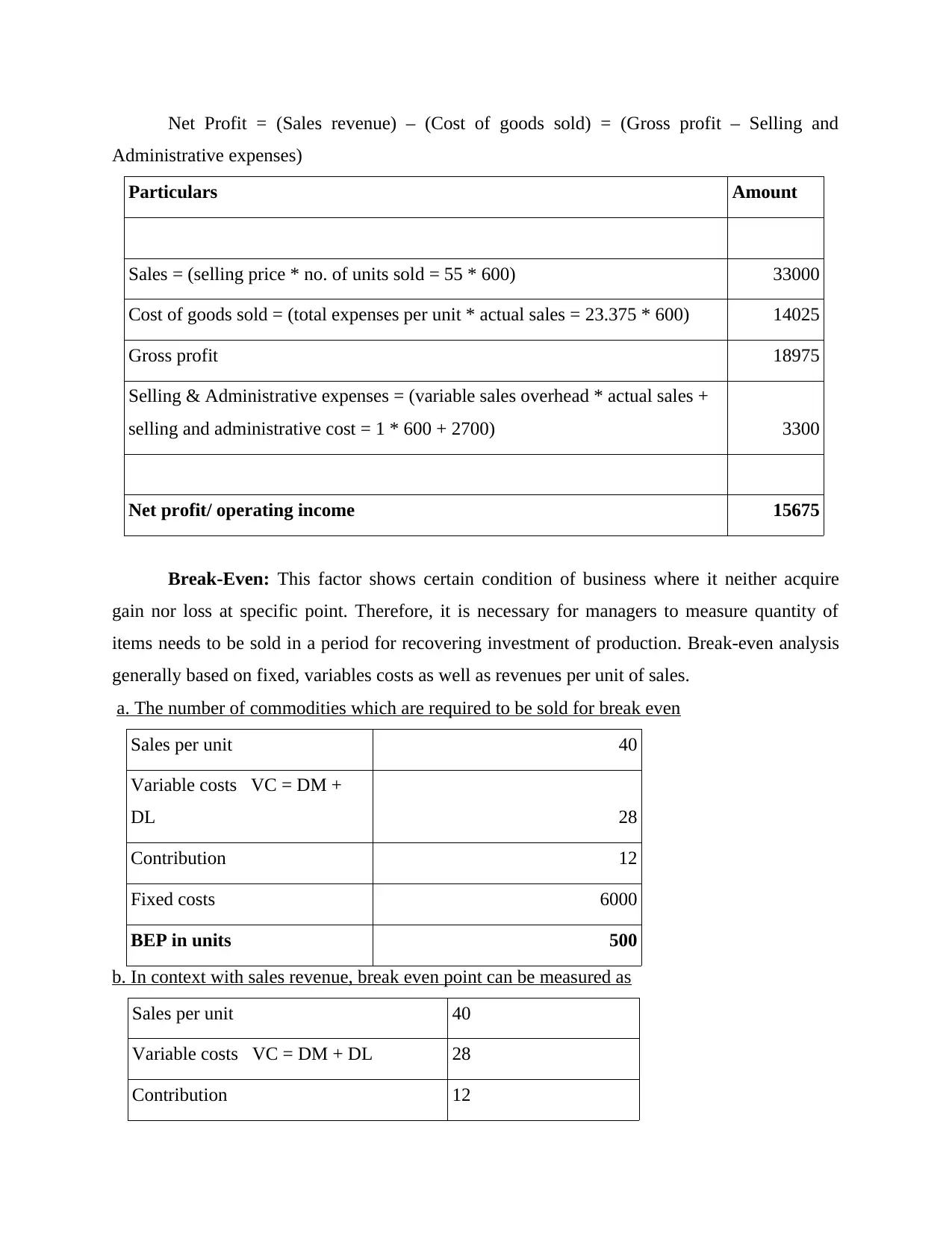

Net Profit = (Sales revenue) – (Cost of goods sold) = (Gross profit – Selling and

Administrative expenses)

Particulars Amount

Sales = (selling price * no. of units sold = 55 * 600) 33000

Cost of goods sold = (total expenses per unit * actual sales = 23.375 * 600) 14025

Gross profit 18975

Selling & Administrative expenses = (variable sales overhead * actual sales +

selling and administrative cost = 1 * 600 + 2700) 3300

Net profit/ operating income 15675

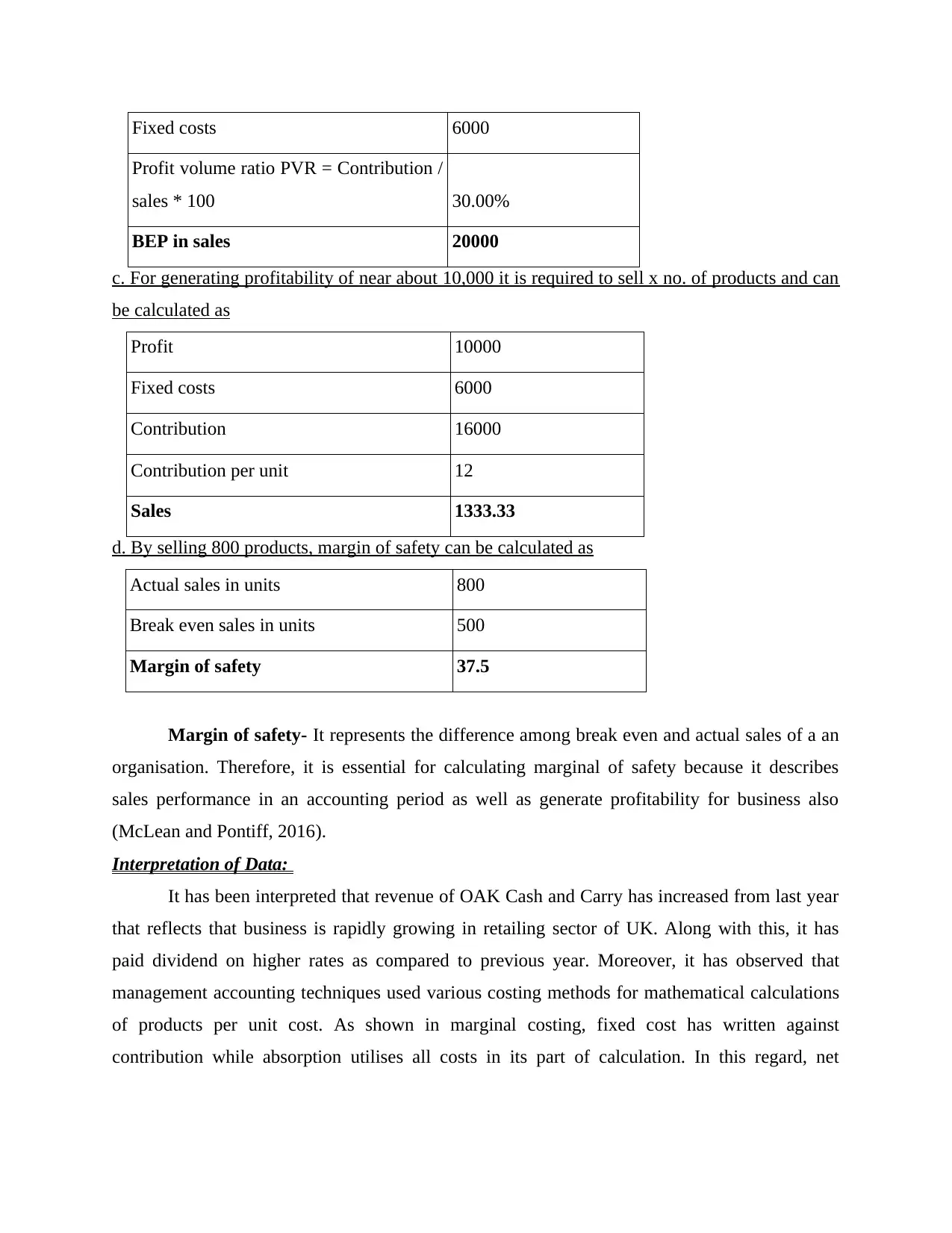

Break-Even: This factor shows certain condition of business where it neither acquire

gain nor loss at specific point. Therefore, it is necessary for managers to measure quantity of

items needs to be sold in a period for recovering investment of production. Break-even analysis

generally based on fixed, variables costs as well as revenues per unit of sales.

a. The number of commodities which are required to be sold for break even

Sales per unit 40

Variable costs VC = DM +

DL 28

Contribution 12

Fixed costs 6000

BEP in units 500

b. In context with sales revenue, break even point can be measured as

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Administrative expenses)

Particulars Amount

Sales = (selling price * no. of units sold = 55 * 600) 33000

Cost of goods sold = (total expenses per unit * actual sales = 23.375 * 600) 14025

Gross profit 18975

Selling & Administrative expenses = (variable sales overhead * actual sales +

selling and administrative cost = 1 * 600 + 2700) 3300

Net profit/ operating income 15675

Break-Even: This factor shows certain condition of business where it neither acquire

gain nor loss at specific point. Therefore, it is necessary for managers to measure quantity of

items needs to be sold in a period for recovering investment of production. Break-even analysis

generally based on fixed, variables costs as well as revenues per unit of sales.

a. The number of commodities which are required to be sold for break even

Sales per unit 40

Variable costs VC = DM +

DL 28

Contribution 12

Fixed costs 6000

BEP in units 500

b. In context with sales revenue, break even point can be measured as

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Fixed costs 6000

Profit volume ratio PVR = Contribution /

sales * 100 30.00%

BEP in sales 20000

c. For generating profitability of near about 10,000 it is required to sell x no. of products and can

be calculated as

Profit 10000

Fixed costs 6000

Contribution 16000

Contribution per unit 12

Sales 1333.33

d. By selling 800 products, margin of safety can be calculated as

Actual sales in units 800

Break even sales in units 500

Margin of safety 37.5

Margin of safety- It represents the difference among break even and actual sales of a an

organisation. Therefore, it is essential for calculating marginal of safety because it describes

sales performance in an accounting period as well as generate profitability for business also

(McLean and Pontiff, 2016).

Interpretation of Data:

It has been interpreted that revenue of OAK Cash and Carry has increased from last year

that reflects that business is rapidly growing in retailing sector of UK. Along with this, it has

paid dividend on higher rates as compared to previous year. Moreover, it has observed that

management accounting techniques used various costing methods for mathematical calculations

of products per unit cost. As shown in marginal costing, fixed cost has written against

contribution while absorption utilises all costs in its part of calculation. In this regard, net

Profit volume ratio PVR = Contribution /

sales * 100 30.00%

BEP in sales 20000

c. For generating profitability of near about 10,000 it is required to sell x no. of products and can

be calculated as

Profit 10000

Fixed costs 6000

Contribution 16000

Contribution per unit 12

Sales 1333.33

d. By selling 800 products, margin of safety can be calculated as

Actual sales in units 800

Break even sales in units 500

Margin of safety 37.5

Margin of safety- It represents the difference among break even and actual sales of a an

organisation. Therefore, it is essential for calculating marginal of safety because it describes

sales performance in an accounting period as well as generate profitability for business also

(McLean and Pontiff, 2016).

Interpretation of Data:

It has been interpreted that revenue of OAK Cash and Carry has increased from last year

that reflects that business is rapidly growing in retailing sector of UK. Along with this, it has

paid dividend on higher rates as compared to previous year. Moreover, it has observed that

management accounting techniques used various costing methods for mathematical calculations

of products per unit cost. As shown in marginal costing, fixed cost has written against

contribution while absorption utilises all costs in its part of calculation. In this regard, net

operating costs as per marginal as well as absorption has obtained as £17500 and £15675,

respectively.

TASK 3

P4 Advantages and disadvantages of different planning tools used for budgetary control

It is considered as the system which is used my manager of organisation in order to

control the irrelevant expenses at work place. In this, manager compares actual expenses and

income with the planned one. It emphasize on evaluating all the procedures and activities in

organisation for checking whether they are accomplishing in the given time frame. If

organisational activities are not meeting with the planned one then it is required by manager to

change it for maximising profitability (Hall, 2012). Budget of firm involves cost, sales,

production etc. Cash budget of organisation states financial position of the business in terms of

future prediction. Apart from this, sales budget is used by the every organisation to find out how

much sales is required to achieve the targeted profit.

Therefore, it is required by the top management of small business to formulate

appropriate budget which helps the business manager in decision making process related to

marketing and production activities. In addition to this, budgetary control techniques are

advantageous for organisation as it guides them to minimise extra expenses at work place. This

will reducing expenses and enhance profitability of business. Manager of OAK Cash and Carry

can compare its activities at workplace with their formulated budget. This will help enterprise in

taking required steps for reducing its expenses. addition to this, it has been evaluated that there

are numerous of which can be used by small business like OAK Cash and Carry in order to

control their activities. These tools are evaluated as below:

SCORO- It helps a firm in managing entire activities of company by combining different

features of budgeting with various tools and techniques (Cleary and Quinn, 2016). This type of

planning tool gives an integrated plan through which managers can manage overall expenses and

available resources of business while maintaining budgets.

Advantages: The main feature of this tool is planning and forecasting budgets which

provides an automated revenue stream. Along with this, by financial report, managers of

OAK Cash and Carry can evaluate budget targets as well.

respectively.

TASK 3

P4 Advantages and disadvantages of different planning tools used for budgetary control

It is considered as the system which is used my manager of organisation in order to

control the irrelevant expenses at work place. In this, manager compares actual expenses and

income with the planned one. It emphasize on evaluating all the procedures and activities in

organisation for checking whether they are accomplishing in the given time frame. If

organisational activities are not meeting with the planned one then it is required by manager to

change it for maximising profitability (Hall, 2012). Budget of firm involves cost, sales,

production etc. Cash budget of organisation states financial position of the business in terms of

future prediction. Apart from this, sales budget is used by the every organisation to find out how

much sales is required to achieve the targeted profit.

Therefore, it is required by the top management of small business to formulate

appropriate budget which helps the business manager in decision making process related to

marketing and production activities. In addition to this, budgetary control techniques are

advantageous for organisation as it guides them to minimise extra expenses at work place. This

will reducing expenses and enhance profitability of business. Manager of OAK Cash and Carry

can compare its activities at workplace with their formulated budget. This will help enterprise in

taking required steps for reducing its expenses. addition to this, it has been evaluated that there

are numerous of which can be used by small business like OAK Cash and Carry in order to

control their activities. These tools are evaluated as below:

SCORO- It helps a firm in managing entire activities of company by combining different

features of budgeting with various tools and techniques (Cleary and Quinn, 2016). This type of

planning tool gives an integrated plan through which managers can manage overall expenses and

available resources of business while maintaining budgets.

Advantages: The main feature of this tool is planning and forecasting budgets which

provides an automated revenue stream. Along with this, by financial report, managers of

OAK Cash and Carry can evaluate budget targets as well.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.