Management Accounting Report: O'Keefe Construction Analysis

VerifiedAdded on 2021/01/02

|18

|4661

|421

Report

AI Summary

This report provides a comprehensive overview of management accounting, focusing on its crucial role in organizational decision-making, particularly within the construction industry. It begins with an introduction to management accounting, emphasizing its importance in analyzing financial data for internal decisions, and then selects O'Keefe Construction Limited as a case study. The report explores various management accounting systems, including inventory management and price optimization, detailing their applications and benefits within the context of the construction firm. It also examines different reporting methods such as budgetary reports, cost managerial accounting reports, and inventory cost reports. Furthermore, the report analyzes the integration of management accounting systems and reporting within organizational processes. The report includes practical examples using marginal costing and absorption costing methods, along with calculations for overhead absorption using labor hour and activity-based costing (ABC) approaches. This report serves as a valuable resource for understanding and applying management accounting principles to real-world business scenarios.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

ACTIVITY 1....................................................................................................................................1

PART (A)...............................................................................................................................1

PART(B).................................................................................................................................4

ACTIVITY 2....................................................................................................................................8

PART (A)...............................................................................................................................8

PART(B)...............................................................................................................................12

CONCLUSION..............................................................................................................................14

.......................................................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION...........................................................................................................................1

ACTIVITY 1....................................................................................................................................1

PART (A)...............................................................................................................................1

PART(B).................................................................................................................................4

ACTIVITY 2....................................................................................................................................8

PART (A)...............................................................................................................................8

PART(B)...............................................................................................................................12

CONCLUSION..............................................................................................................................14

.......................................................................................................................................................14

REFERENCES..............................................................................................................................15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management accounting is an accounting system which is commonly related with

analysing, monitoring and interpreting all the financial data in order to take internal decisions. It

is one of the most important accounting system for the overall organisations because it includes

all required information related to financial data which becomes the basis of future planning and

policies. In addition to this, it includes both type of data monetary as well as non- monetary

information. It includes various other accounting system (Bennett and James, 2017). In this

report, O'Keefe construction limited is chosen as the base company in this report. It is the

company which is located in the United Kingdom which provides construction as well as ground

work services and so on. This report includes different type of management accounting along

with their advantages. In addition to this, the present report includes various methods of

budgetary control along with the role of management accounting techniques while solving

different financial issues.

ACTIVITY 1.

PART (A)

Management accounting and essential requirement of different accounting method.

Management accounting system is related to the accounting system which help in providing

required information to the manager of organisation which required within decision making

process. Within organisation, management accounting system is important but not mandatory

part of an organisation because not framed according to the accounting concepts and rules.

Moreover, uses of management accounting system is increasing day by day because there are

several approaches as well as techniques involves within it which have own importance within

working of organisation. In addition to this, within wide term there are several accounting

systems included within management accounting system and used by companies within their

working (Bromwich and Scapens, 2016). In relation of the O' Keefe construction company wide

range of accounting system will be implemented that are needed within several civil engineering

project. Explanation of these are as follows: -

Inventory system management – It is type of accounting management system which

help organisation in accurately managing raw material as well as finished products. Generally,

inventory management system keep focus on the movement of raw material and finished

1

Management accounting is an accounting system which is commonly related with

analysing, monitoring and interpreting all the financial data in order to take internal decisions. It

is one of the most important accounting system for the overall organisations because it includes

all required information related to financial data which becomes the basis of future planning and

policies. In addition to this, it includes both type of data monetary as well as non- monetary

information. It includes various other accounting system (Bennett and James, 2017). In this

report, O'Keefe construction limited is chosen as the base company in this report. It is the

company which is located in the United Kingdom which provides construction as well as ground

work services and so on. This report includes different type of management accounting along

with their advantages. In addition to this, the present report includes various methods of

budgetary control along with the role of management accounting techniques while solving

different financial issues.

ACTIVITY 1.

PART (A)

Management accounting and essential requirement of different accounting method.

Management accounting system is related to the accounting system which help in providing

required information to the manager of organisation which required within decision making

process. Within organisation, management accounting system is important but not mandatory

part of an organisation because not framed according to the accounting concepts and rules.

Moreover, uses of management accounting system is increasing day by day because there are

several approaches as well as techniques involves within it which have own importance within

working of organisation. In addition to this, within wide term there are several accounting

systems included within management accounting system and used by companies within their

working (Bromwich and Scapens, 2016). In relation of the O' Keefe construction company wide

range of accounting system will be implemented that are needed within several civil engineering

project. Explanation of these are as follows: -

Inventory system management – It is type of accounting management system which

help organisation in accurately managing raw material as well as finished products. Generally,

inventory management system keep focus on the movement of raw material and finished

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

products within organisation within overall supply chain management. In addition to this,

respective inventory stage-management system has their importance within organisation in

evaluating stock availability as well as raw material within warehouses. Because of this,

inventory manager within organisation assist in managing and purchasing goods and services

within business firm. Along with this, respective accounting system is needed in company for

managing raw material and prepared goods (Chenhall and Moers, 2015). So that, companies can

make purchase of new material according to the needs. In the context of O'Keefe construction

limited company, they can implement inventory management system for proper management of

available raw material related to civil projects. Along with this, they will get aware about the

quantity of raw material available within stock.

Price optimisation system – This is a management accounting method which utilise

within organisation for allotting right or accurate level of price for product and services. In

addition to this, price optimisation system provides a framework which help in reviewing

reaction of customers within different price level. Respective system is not only beneficial for

organisation but also for customer too. This is best way which help organisation is deciding

accurate price of their product and services which will be suitable for organisation as well as

their customers. Within absence of this, it will become difficult for respective construction

company to determine right offering price of their product and services. Along with this, it

results in conflict within occurring cost of offering and their price. In simple words, price

optimisation system is needed within organisation for fixing price of goods and services at every

level which will be beneficial for both company and their customers (Maas, Schaltegger and

Crutzen, 2016). For instance, the O'Keefe construction limited organisation implements

respective method of price optimisation help in analysing as well as determining the price of

different civil projects within business firm. Along with this, by the assistance of this system

company will be able to satisfy their customers’ needs in relation of price within effective

manner.

Different methods of management accounting reporting:

Management accounting reporting refers to the process of formulating reports on the

basis of data given by management accounting systems. There are various types of reports that

are being developed with the support of management accounting. In context of O'Keefe

2

respective inventory stage-management system has their importance within organisation in

evaluating stock availability as well as raw material within warehouses. Because of this,

inventory manager within organisation assist in managing and purchasing goods and services

within business firm. Along with this, respective accounting system is needed in company for

managing raw material and prepared goods (Chenhall and Moers, 2015). So that, companies can

make purchase of new material according to the needs. In the context of O'Keefe construction

limited company, they can implement inventory management system for proper management of

available raw material related to civil projects. Along with this, they will get aware about the

quantity of raw material available within stock.

Price optimisation system – This is a management accounting method which utilise

within organisation for allotting right or accurate level of price for product and services. In

addition to this, price optimisation system provides a framework which help in reviewing

reaction of customers within different price level. Respective system is not only beneficial for

organisation but also for customer too. This is best way which help organisation is deciding

accurate price of their product and services which will be suitable for organisation as well as

their customers. Within absence of this, it will become difficult for respective construction

company to determine right offering price of their product and services. Along with this, it

results in conflict within occurring cost of offering and their price. In simple words, price

optimisation system is needed within organisation for fixing price of goods and services at every

level which will be beneficial for both company and their customers (Maas, Schaltegger and

Crutzen, 2016). For instance, the O'Keefe construction limited organisation implements

respective method of price optimisation help in analysing as well as determining the price of

different civil projects within business firm. Along with this, by the assistance of this system

company will be able to satisfy their customers’ needs in relation of price within effective

manner.

Different methods of management accounting reporting:

Management accounting reporting refers to the process of formulating reports on the

basis of data given by management accounting systems. There are various types of reports that

are being developed with the support of management accounting. In context of O'Keefe

2

construction limited company, it has been analysed that the company is making various kind of

reports. Some main of them are described as follows:

Budgetary reports- Budgetary reports are seen as those reports which have been created

for measuring actual action or performance company by comparison of actual outcome with the

estimated outcomes. It is seen as internal report which is useful for the performance evaluation

and its analysis of its issues. these reports also helps manager in taking essential decisions at

workplace (Bennett and James, 2017). With reference to O'Keefe construction limited company,

it can be said that its managers prepares these kind of reports to identify the actual financial

performance of company.

Cost managerial accounting reports- It is a kind of accounting report which includes

all relevant information about cost which occurs in the procedure of service or product offering.

This kind of accounting report includes several information such as direct cost , material

cost,labour overhead, etc. With the helps of this report company check out whole information in

order to find out which department is consuming high cost. With reference to O'Keefe

construction limited company, the top management team of the company prepares cost reports

for measuring cost of various projects activities. With the helps of these reports, they can

enhance their knowledge regarding cost in construction.

Inventory cost report- Inventory cost reports includes data about the availability of raw

material and other related stocks in the warehouses of company. With the support of this report,

the manager is able to analyse that how much quantity is available in their company and what

additional is required for executing business activities ion effective manner. Apart from this, this

type of report that is inventory cost report also contains information related to the carrying cost,

ordering and storage (Bromwich and Scapens, 2016). With reference to O'Keefe construction

limited company, the top management team of the company develops this report for effective

management of raw material used in construction as well as for evaluating the different cost of

inventory management.

Benefits of management accounting systems and their application in organisational context.

Management accounting systems include different kind of systems like inventory

management system cost accounting systems and price optimisation system. It can be said that

all of these systems are valuable for the company. With reference to O'Keefe construction

3

reports. Some main of them are described as follows:

Budgetary reports- Budgetary reports are seen as those reports which have been created

for measuring actual action or performance company by comparison of actual outcome with the

estimated outcomes. It is seen as internal report which is useful for the performance evaluation

and its analysis of its issues. these reports also helps manager in taking essential decisions at

workplace (Bennett and James, 2017). With reference to O'Keefe construction limited company,

it can be said that its managers prepares these kind of reports to identify the actual financial

performance of company.

Cost managerial accounting reports- It is a kind of accounting report which includes

all relevant information about cost which occurs in the procedure of service or product offering.

This kind of accounting report includes several information such as direct cost , material

cost,labour overhead, etc. With the helps of this report company check out whole information in

order to find out which department is consuming high cost. With reference to O'Keefe

construction limited company, the top management team of the company prepares cost reports

for measuring cost of various projects activities. With the helps of these reports, they can

enhance their knowledge regarding cost in construction.

Inventory cost report- Inventory cost reports includes data about the availability of raw

material and other related stocks in the warehouses of company. With the support of this report,

the manager is able to analyse that how much quantity is available in their company and what

additional is required for executing business activities ion effective manner. Apart from this, this

type of report that is inventory cost report also contains information related to the carrying cost,

ordering and storage (Bromwich and Scapens, 2016). With reference to O'Keefe construction

limited company, the top management team of the company develops this report for effective

management of raw material used in construction as well as for evaluating the different cost of

inventory management.

Benefits of management accounting systems and their application in organisational context.

Management accounting systems include different kind of systems like inventory

management system cost accounting systems and price optimisation system. It can be said that

all of these systems are valuable for the company. With reference to O'Keefe construction

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

limited company, it can be said that benefits of these systems for the company are stated as

below:

Benefits of inventory management system- It can be said that this accounting system is

helpful for tracking the movement finish goods as well as raw material in whole supply chain

process (Chenhall and Moers, 2015). With reference to O'Keefe construction limited company,

the system helps its top management team in checking out accessibility of raw material like iron

and cement concrete in the outlets.

Benefits of price optimisation system- With reference to O'Keefe construction limited

company, it can be said that the system is helpful in determining actual price of products and

services. Along with this, it also guides top management team about finalising prices of the

actual products and services.

Benefits of cost accounting system- This system is aid in providing various information

which are related to the various cost which occurs in various processes. As per the above

mentioned company i.e., engineering company, cost accounting system is helpful for them to

check the overall cost of various engineering projects.

Management accounting system and reporting are integrated within the organisational process.

Management accounting system is valuable for the companies as it helps preparing

management accounting reporting. This is because, different management accounting reports like

budgetary, inventory cost report etc. are developed with the support of data which is provided by

the various accounting systems. All of these systems are interrelated to each other along with the

organisational process (Maas, Schaltegger and Crutzen, 2016). With reference to O'Keefe

construction limited company, the top management team of the company formulates different

reports with the support of various accounting systems such as cost accounting systems,

inventory management system etc. It can be said that in the absence of combination of

accounting systems with the management accounting reporting it might be difficult for them to

prepare effective report. This shows that both of them are interrelated with each other within

process of company.

PART(B)

ANNEX(A)

4

below:

Benefits of inventory management system- It can be said that this accounting system is

helpful for tracking the movement finish goods as well as raw material in whole supply chain

process (Chenhall and Moers, 2015). With reference to O'Keefe construction limited company,

the system helps its top management team in checking out accessibility of raw material like iron

and cement concrete in the outlets.

Benefits of price optimisation system- With reference to O'Keefe construction limited

company, it can be said that the system is helpful in determining actual price of products and

services. Along with this, it also guides top management team about finalising prices of the

actual products and services.

Benefits of cost accounting system- This system is aid in providing various information

which are related to the various cost which occurs in various processes. As per the above

mentioned company i.e., engineering company, cost accounting system is helpful for them to

check the overall cost of various engineering projects.

Management accounting system and reporting are integrated within the organisational process.

Management accounting system is valuable for the companies as it helps preparing

management accounting reporting. This is because, different management accounting reports like

budgetary, inventory cost report etc. are developed with the support of data which is provided by

the various accounting systems. All of these systems are interrelated to each other along with the

organisational process (Maas, Schaltegger and Crutzen, 2016). With reference to O'Keefe

construction limited company, the top management team of the company formulates different

reports with the support of various accounting systems such as cost accounting systems,

inventory management system etc. It can be said that in the absence of combination of

accounting systems with the management accounting reporting it might be difficult for them to

prepare effective report. This shows that both of them are interrelated with each other within

process of company.

PART(B)

ANNEX(A)

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

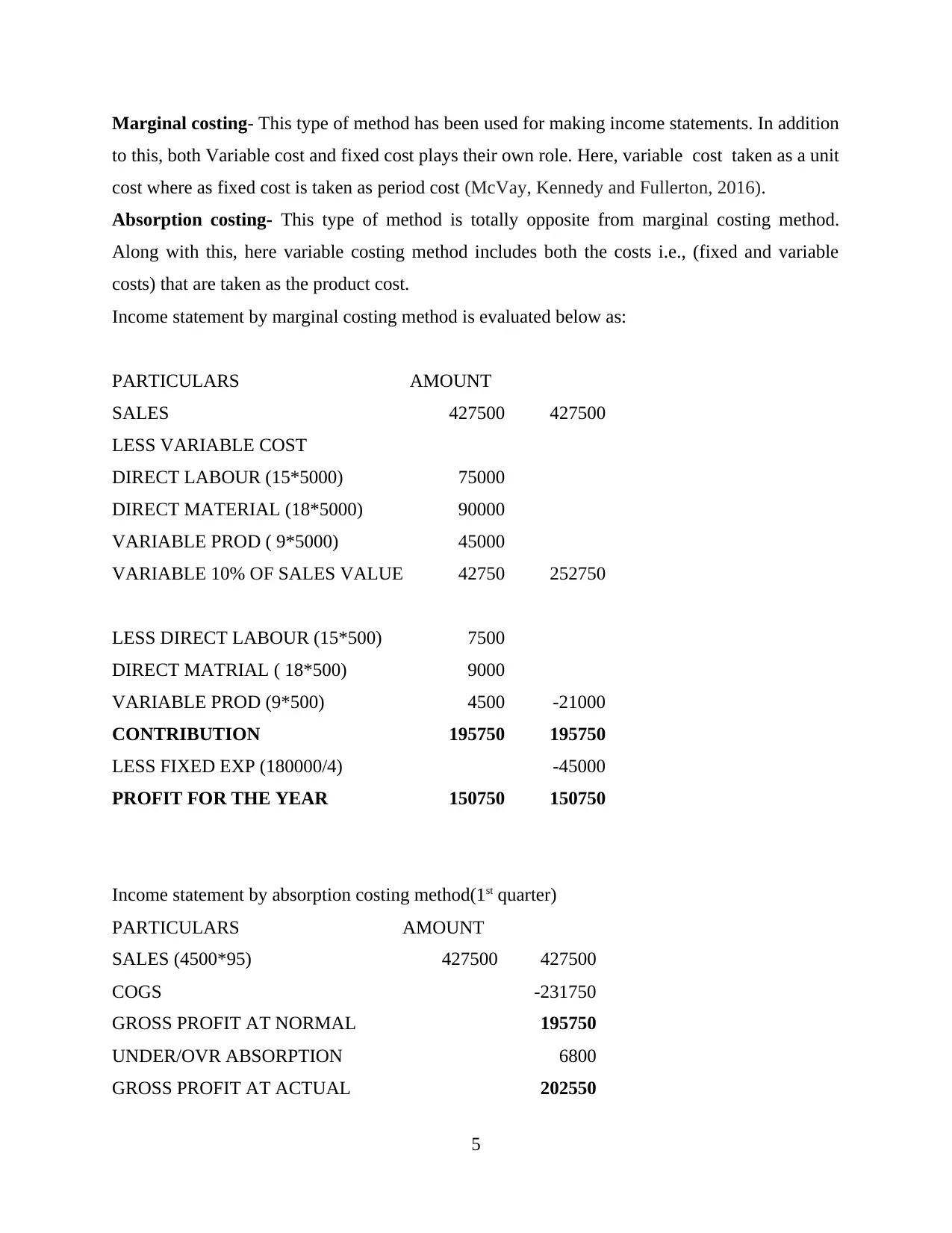

Marginal costing- This type of method has been used for making income statements. In addition

to this, both Variable cost and fixed cost plays their own role. Here, variable cost taken as a unit

cost where as fixed cost is taken as period cost (McVay, Kennedy and Fullerton, 2016).

Absorption costing- This type of method is totally opposite from marginal costing method.

Along with this, here variable costing method includes both the costs i.e., (fixed and variable

costs) that are taken as the product cost.

Income statement by marginal costing method is evaluated below as:

PARTICULARS AMOUNT

SALES 427500 427500

LESS VARIABLE COST

DIRECT LABOUR (15*5000) 75000

DIRECT MATERIAL (18*5000) 90000

VARIABLE PROD ( 9*5000) 45000

VARIABLE 10% OF SALES VALUE 42750 252750

LESS DIRECT LABOUR (15*500) 7500

DIRECT MATRIAL ( 18*500) 9000

VARIABLE PROD (9*500) 4500 -21000

CONTRIBUTION 195750 195750

LESS FIXED EXP (180000/4) -45000

PROFIT FOR THE YEAR 150750 150750

Income statement by absorption costing method(1st quarter)

PARTICULARS AMOUNT

SALES (4500*95) 427500 427500

COGS -231750

GROSS PROFIT AT NORMAL 195750

UNDER/OVR ABSORPTION 6800

GROSS PROFIT AT ACTUAL 202550

5

to this, both Variable cost and fixed cost plays their own role. Here, variable cost taken as a unit

cost where as fixed cost is taken as period cost (McVay, Kennedy and Fullerton, 2016).

Absorption costing- This type of method is totally opposite from marginal costing method.

Along with this, here variable costing method includes both the costs i.e., (fixed and variable

costs) that are taken as the product cost.

Income statement by marginal costing method is evaluated below as:

PARTICULARS AMOUNT

SALES 427500 427500

LESS VARIABLE COST

DIRECT LABOUR (15*5000) 75000

DIRECT MATERIAL (18*5000) 90000

VARIABLE PROD ( 9*5000) 45000

VARIABLE 10% OF SALES VALUE 42750 252750

LESS DIRECT LABOUR (15*500) 7500

DIRECT MATRIAL ( 18*500) 9000

VARIABLE PROD (9*500) 4500 -21000

CONTRIBUTION 195750 195750

LESS FIXED EXP (180000/4) -45000

PROFIT FOR THE YEAR 150750 150750

Income statement by absorption costing method(1st quarter)

PARTICULARS AMOUNT

SALES (4500*95) 427500 427500

COGS -231750

GROSS PROFIT AT NORMAL 195750

UNDER/OVR ABSORPTION 6800

GROSS PROFIT AT ACTUAL 202550

5

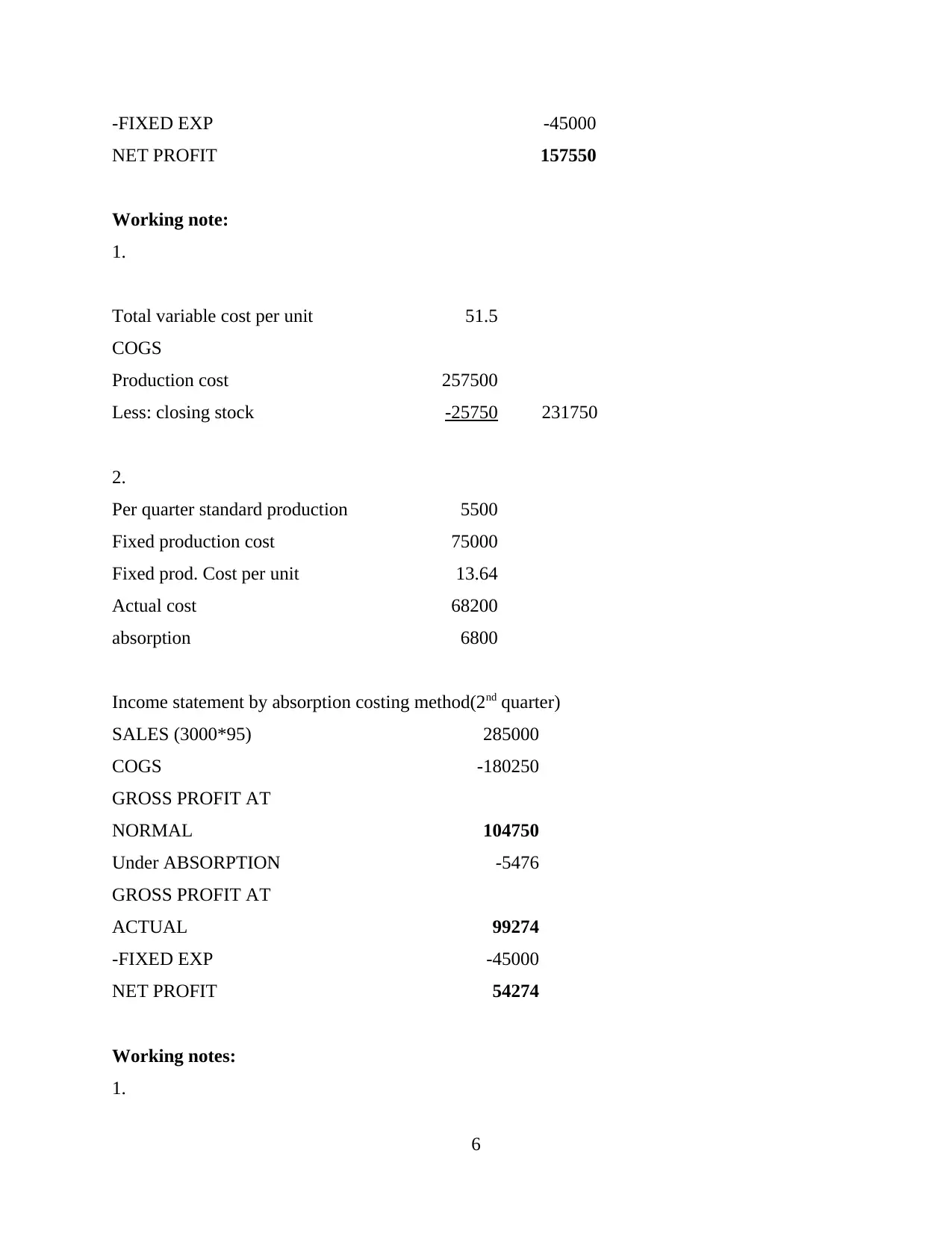

-FIXED EXP -45000

NET PROFIT 157550

Working note:

1.

Total variable cost per unit 51.5

COGS

Production cost 257500

Less: closing stock -25750 231750

2.

Per quarter standard production 5500

Fixed production cost 75000

Fixed prod. Cost per unit 13.64

Actual cost 68200

absorption 6800

Income statement by absorption costing method(2nd quarter)

SALES (3000*95) 285000

COGS -180250

GROSS PROFIT AT

NORMAL 104750

Under ABSORPTION -5476

GROSS PROFIT AT

ACTUAL 99274

-FIXED EXP -45000

NET PROFIT 54274

Working notes:

1.

6

NET PROFIT 157550

Working note:

1.

Total variable cost per unit 51.5

COGS

Production cost 257500

Less: closing stock -25750 231750

2.

Per quarter standard production 5500

Fixed production cost 75000

Fixed prod. Cost per unit 13.64

Actual cost 68200

absorption 6800

Income statement by absorption costing method(2nd quarter)

SALES (3000*95) 285000

COGS -180250

GROSS PROFIT AT

NORMAL 104750

Under ABSORPTION -5476

GROSS PROFIT AT

ACTUAL 99274

-FIXED EXP -45000

NET PROFIT 54274

Working notes:

1.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

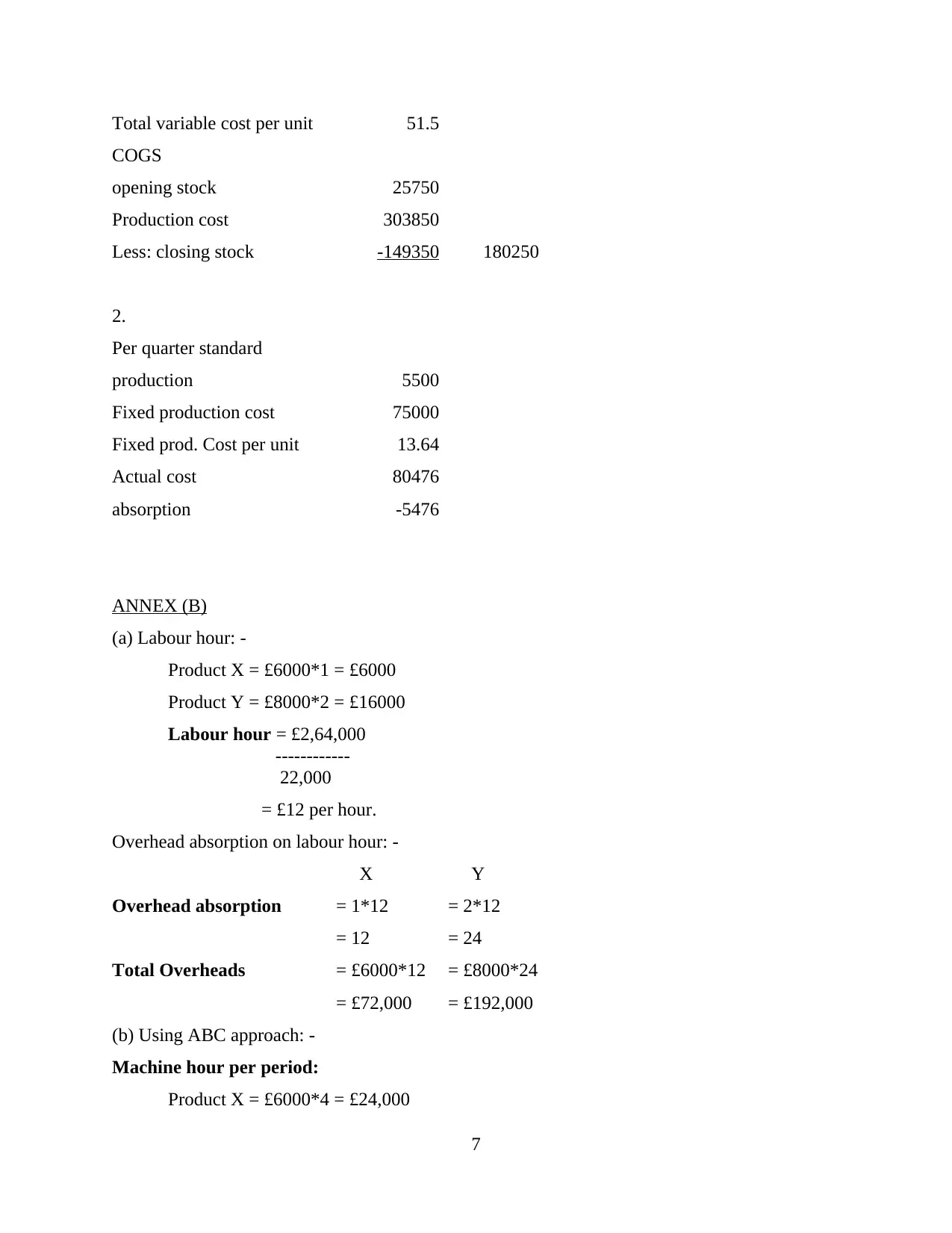

Total variable cost per unit 51.5

COGS

opening stock 25750

Production cost 303850

Less: closing stock -149350 180250

2.

Per quarter standard

production 5500

Fixed production cost 75000

Fixed prod. Cost per unit 13.64

Actual cost 80476

absorption -5476

ANNEX (B)

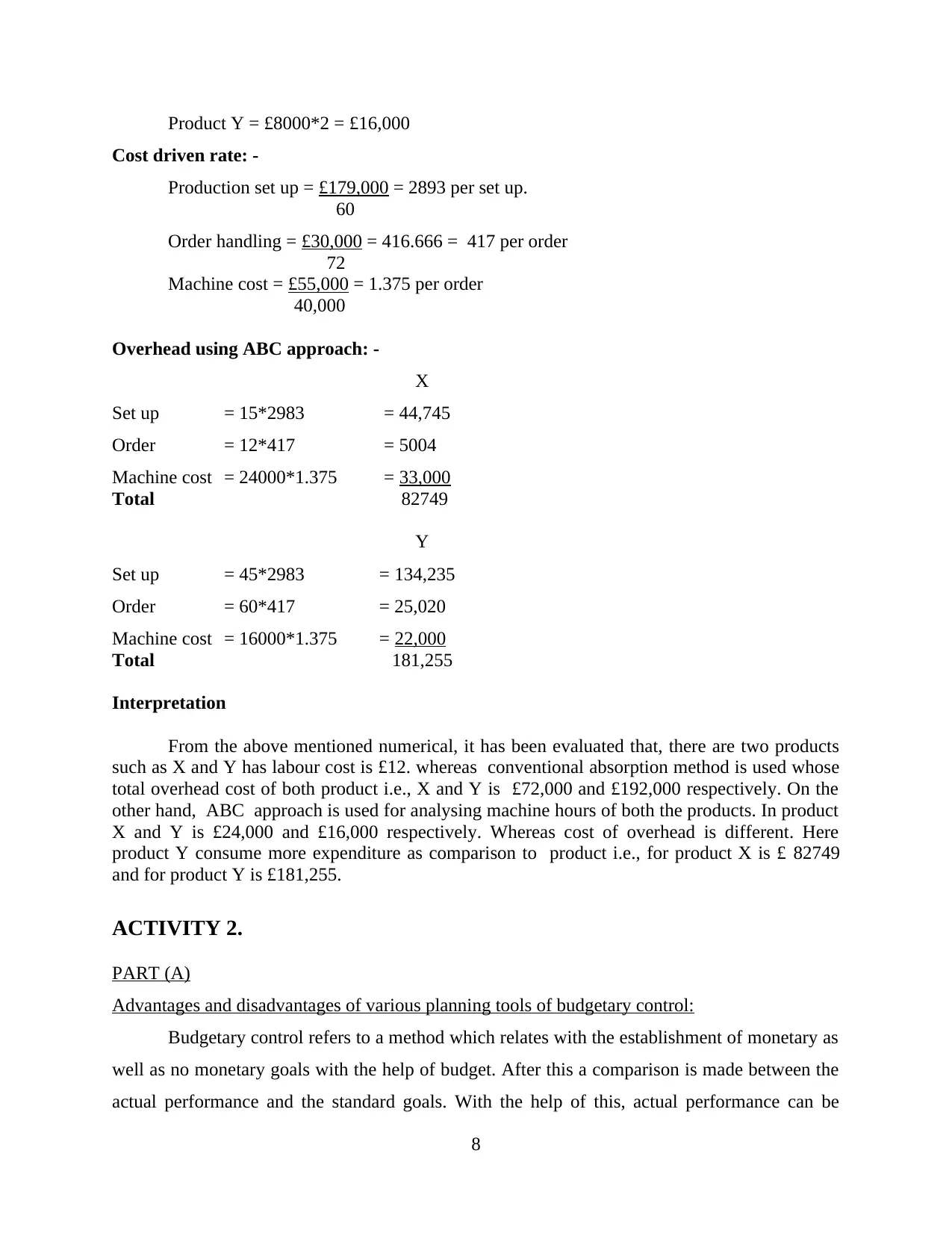

(a) Labour hour: -

Product X = £6000*1 = £6000

Product Y = £8000*2 = £16000

Labour hour = £2,64,000

------------

22,000

= £12 per hour.

Overhead absorption on labour hour: -

X Y

Overhead absorption = 1*12 = 2*12

= 12 = 24

Total Overheads = £6000*12 = £8000*24

= £72,000 = £192,000

(b) Using ABC approach: -

Machine hour per period:

Product X = £6000*4 = £24,000

7

COGS

opening stock 25750

Production cost 303850

Less: closing stock -149350 180250

2.

Per quarter standard

production 5500

Fixed production cost 75000

Fixed prod. Cost per unit 13.64

Actual cost 80476

absorption -5476

ANNEX (B)

(a) Labour hour: -

Product X = £6000*1 = £6000

Product Y = £8000*2 = £16000

Labour hour = £2,64,000

------------

22,000

= £12 per hour.

Overhead absorption on labour hour: -

X Y

Overhead absorption = 1*12 = 2*12

= 12 = 24

Total Overheads = £6000*12 = £8000*24

= £72,000 = £192,000

(b) Using ABC approach: -

Machine hour per period:

Product X = £6000*4 = £24,000

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Product Y = £8000*2 = £16,000

Cost driven rate: -

Production set up = £179,000 = 2893 per set up.

60

Order handling = £30,000 = 416.666 = 417 per order

72

Machine cost = £55,000 = 1.375 per order

40,000

Overhead using ABC approach: -

X

Set up = 15*2983 = 44,745

Order = 12*417 = 5004

Machine cost = 24000*1.375 = 33,000

Total 82749

Y

Set up = 45*2983 = 134,235

Order = 60*417 = 25,020

Machine cost = 16000*1.375 = 22,000

Total 181,255

Interpretation

From the above mentioned numerical, it has been evaluated that, there are two products

such as X and Y has labour cost is £12. whereas conventional absorption method is used whose

total overhead cost of both product i.e., X and Y is £72,000 and £192,000 respectively. On the

other hand, ABC approach is used for analysing machine hours of both the products. In product

X and Y is £24,000 and £16,000 respectively. Whereas cost of overhead is different. Here

product Y consume more expenditure as comparison to product i.e., for product X is £ 82749

and for product Y is £181,255.

ACTIVITY 2.

PART (A)

Advantages and disadvantages of various planning tools of budgetary control:

Budgetary control refers to a method which relates with the establishment of monetary as

well as no monetary goals with the help of budget. After this a comparison is made between the

actual performance and the standard goals. With the help of this, actual performance can be

8

Cost driven rate: -

Production set up = £179,000 = 2893 per set up.

60

Order handling = £30,000 = 416.666 = 417 per order

72

Machine cost = £55,000 = 1.375 per order

40,000

Overhead using ABC approach: -

X

Set up = 15*2983 = 44,745

Order = 12*417 = 5004

Machine cost = 24000*1.375 = 33,000

Total 82749

Y

Set up = 45*2983 = 134,235

Order = 60*417 = 25,020

Machine cost = 16000*1.375 = 22,000

Total 181,255

Interpretation

From the above mentioned numerical, it has been evaluated that, there are two products

such as X and Y has labour cost is £12. whereas conventional absorption method is used whose

total overhead cost of both product i.e., X and Y is £72,000 and £192,000 respectively. On the

other hand, ABC approach is used for analysing machine hours of both the products. In product

X and Y is £24,000 and £16,000 respectively. Whereas cost of overhead is different. Here

product Y consume more expenditure as comparison to product i.e., for product X is £ 82749

and for product Y is £181,255.

ACTIVITY 2.

PART (A)

Advantages and disadvantages of various planning tools of budgetary control:

Budgetary control refers to a method which relates with the establishment of monetary as

well as no monetary goals with the help of budget. After this a comparison is made between the

actual performance and the standard goals. With the help of this, actual performance can be

8

analysed conducting while performing different activities. The main aim of this process to meet

the requirements as per the standards. Various types of planning tools are used by companies in

order to examine the actual result (Nilsson and Stockenstrand, 2015). The O'Keefe construction

limited, apply various budgetary control tool. Some of the tools are as follows:

Fixed budget- These are the budgets which are not flexible and also known as static

budget. Such budgets does not change according to the change in sales volume. So companies

formulate such type of policies for those activities which is not going to change in near future.

The above mentioned company select fixed budget in order to fulfil their small projects in less

time. There are some advantages and disadvantages of this budget:

Advantages-

It is the budget which does not need to update on a regular moth so it reduce the time of

managers. In O'Keefe construction limited, they only prepare fixed budget once and does

not change it.

One of the biggest advantage is that it is quite easy and quick to track the information

(Nørreklit, 2017). Reason behind this is that it remain same, so the managers of the

company easily track the performance.

Disadvantages-

Major disadvantage of this type of budget is that it remains same and create

confusion, as the sales and volumes changes continuously.

This budget remains same whether there is any kind of changes occur in the sales

or volume.

Flexible budget- It is a type of budget which changes continuously according to change

in volume and sale (Otley, 2016). Also, this budget is more comfortable in order to compare the

static budget. The O'Keefe construction limited, prepares such type of budget in order to fulfil

their long term project. Reason behind this is that in long term various changes occur in the

income and expenditure, so that all these changes can be updated in the budget. There are some

advantages and disadvantage which are explained as below:

Advantages-

This type of budget is less stressful as it helps in changing the estimated income

and expense. With the help of this, chosen engineering company can make change

according to their income in their budget.

9

the requirements as per the standards. Various types of planning tools are used by companies in

order to examine the actual result (Nilsson and Stockenstrand, 2015). The O'Keefe construction

limited, apply various budgetary control tool. Some of the tools are as follows:

Fixed budget- These are the budgets which are not flexible and also known as static

budget. Such budgets does not change according to the change in sales volume. So companies

formulate such type of policies for those activities which is not going to change in near future.

The above mentioned company select fixed budget in order to fulfil their small projects in less

time. There are some advantages and disadvantages of this budget:

Advantages-

It is the budget which does not need to update on a regular moth so it reduce the time of

managers. In O'Keefe construction limited, they only prepare fixed budget once and does

not change it.

One of the biggest advantage is that it is quite easy and quick to track the information

(Nørreklit, 2017). Reason behind this is that it remain same, so the managers of the

company easily track the performance.

Disadvantages-

Major disadvantage of this type of budget is that it remains same and create

confusion, as the sales and volumes changes continuously.

This budget remains same whether there is any kind of changes occur in the sales

or volume.

Flexible budget- It is a type of budget which changes continuously according to change

in volume and sale (Otley, 2016). Also, this budget is more comfortable in order to compare the

static budget. The O'Keefe construction limited, prepares such type of budget in order to fulfil

their long term project. Reason behind this is that in long term various changes occur in the

income and expenditure, so that all these changes can be updated in the budget. There are some

advantages and disadvantage which are explained as below:

Advantages-

This type of budget is less stressful as it helps in changing the estimated income

and expense. With the help of this, chosen engineering company can make change

according to their income in their budget.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.