Management Accounting Report: Oshodi Plc Analysis and Solutions

VerifiedAdded on 2021/02/20

|15

|5187

|19

Report

AI Summary

This report delves into the realm of management accounting, focusing on Oshodi Plc, a manufacturing company. It begins by defining management accounting and its systems, including price optimization, cost accounting, inventory management, and job costing. The report then explores management accounting reporting, detailing various reports such as performance reports, accounts receivable aging reports, budget reports, and trend analysis reports. It highlights the benefits of these systems in enhancing efficiency, profitability, and decision-making. Furthermore, the report demonstrates the application of marginal and absorption costing techniques, providing calculations and interpretations. It also examines planning tools for budgetary control and analyzes how management accounting techniques can identify and resolve financial problems, leading to sustainable success. The report concludes with a comprehensive overview of the integration of these elements within organizational processes. This report is a valuable resource for students studying finance and management accounting on Desklib.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management Accounting & Its Systems:...............................................................................1

P2 Management Accounting Reporting:......................................................................................3

M1 Benefits of Management Accounting Systems:....................................................................4

D1 Integration of management accounting system and management accounting reporting in

organizational processes:.............................................................................................................5

TASK 2............................................................................................................................................5

P3 Calculation of cost using management accounting techniques:.............................................5

M2 Applying a range of management accounting techniques:....................................................6

D2 Interpretation of profit as calculated by different costing techniques:...................................7

TASK 3............................................................................................................................................7

P4 Different types of planning tools used for budgetary control:................................................7

M3 Use of planning tools and their application in forecasting budgets:.....................................9

TASK 4..........................................................................................................................................10

P5 Management accounting techniques used to identify financial problems:...........................10

M4 Analysis of how financial problems can lead an organisation to sustainable success:.......11

D3 Planning tools respond appropriately to solving financial problems to lead organisations to

sustainable success:....................................................................................................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

1

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management Accounting & Its Systems:...............................................................................1

P2 Management Accounting Reporting:......................................................................................3

M1 Benefits of Management Accounting Systems:....................................................................4

D1 Integration of management accounting system and management accounting reporting in

organizational processes:.............................................................................................................5

TASK 2............................................................................................................................................5

P3 Calculation of cost using management accounting techniques:.............................................5

M2 Applying a range of management accounting techniques:....................................................6

D2 Interpretation of profit as calculated by different costing techniques:...................................7

TASK 3............................................................................................................................................7

P4 Different types of planning tools used for budgetary control:................................................7

M3 Use of planning tools and their application in forecasting budgets:.....................................9

TASK 4..........................................................................................................................................10

P5 Management accounting techniques used to identify financial problems:...........................10

M4 Analysis of how financial problems can lead an organisation to sustainable success:.......11

D3 Planning tools respond appropriately to solving financial problems to lead organisations to

sustainable success:....................................................................................................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

1

INTRODUCTION

At the beginning of nineteenth century, the huge private business owners felt the need of

such system or structure that can help the internal stakeholder to control over the internal

environmental factors of the business so that organization can survive. For that purpose, an

accounting system has been created that is called management accounting which is different

from traditional financial accounting in so many aspects (Ahmad, Ismail and Anantharaman,

2015).

For optimistic knowledge of management accounting term, the new trainee managerial

accountant of Oshodi Plc, which is a manufacturing company involved in production and

distribution business of JOJO fruit juice products for all age brackets, is presenting a repost that

covers definition of management accounting, management accounting system and reporting and

planning tools and budgetary control process (Management accounting, 2019). It also includes

solution of financial problems by the help of financial governance techniques and critical

evaluation of entire repost in different parts.

TASK 1

P1 Management Accounting & Its Systems:

Management accounting: Management accounting which is also known as managerial

accounting is a professional method to represent all financial and non-financial data in such a

skilful manner that internal stakeholders such as managers and directors can use this information

in organizational planning and decision making in order to achieve organizational goals

(Angelakis and et.al., 2015). This accounting method is not mandatory to be adopted hence it

does not follow any specific formate which make it easy, adaptable and convenient for the

company.

Management Accounting System: The further step in process of managerial accounting,

is to create management accounting system. This system is formed to collect, record, prepare and

present different accounts and estimations for inside stakeholders such as managers. It records

and presents a whole approximation prospect of operations and transactions which may take

place in particular time. These systematic statements also provides assistance in preparation of

financial accounts and documents of Oshodi Plc at the end of financial year. The establishment

follows various types of management accounting systems which are:

At the beginning of nineteenth century, the huge private business owners felt the need of

such system or structure that can help the internal stakeholder to control over the internal

environmental factors of the business so that organization can survive. For that purpose, an

accounting system has been created that is called management accounting which is different

from traditional financial accounting in so many aspects (Ahmad, Ismail and Anantharaman,

2015).

For optimistic knowledge of management accounting term, the new trainee managerial

accountant of Oshodi Plc, which is a manufacturing company involved in production and

distribution business of JOJO fruit juice products for all age brackets, is presenting a repost that

covers definition of management accounting, management accounting system and reporting and

planning tools and budgetary control process (Management accounting, 2019). It also includes

solution of financial problems by the help of financial governance techniques and critical

evaluation of entire repost in different parts.

TASK 1

P1 Management Accounting & Its Systems:

Management accounting: Management accounting which is also known as managerial

accounting is a professional method to represent all financial and non-financial data in such a

skilful manner that internal stakeholders such as managers and directors can use this information

in organizational planning and decision making in order to achieve organizational goals

(Angelakis and et.al., 2015). This accounting method is not mandatory to be adopted hence it

does not follow any specific formate which make it easy, adaptable and convenient for the

company.

Management Accounting System: The further step in process of managerial accounting,

is to create management accounting system. This system is formed to collect, record, prepare and

present different accounts and estimations for inside stakeholders such as managers. It records

and presents a whole approximation prospect of operations and transactions which may take

place in particular time. These systematic statements also provides assistance in preparation of

financial accounts and documents of Oshodi Plc at the end of financial year. The establishment

follows various types of management accounting systems which are:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Price Optimisation System: Price optimisation system is a mathematical tool that

studied about the customer behaviour towards different pricing policies of various products. This

system is used to decide and control the prices of different products at the same time. It examines

the flow of demand with the fluctuation in price at different levels so that the best price for the

product can be opt out in accordance with customer needs (Berry, Broadbent and Otley, 2016). It

also consider the effective life cycle of the product, competitors' pricing policy, profit margin

goals, etc. The Oshodi Plc uses price optimisation system in tailoring the prices of its fruit juices

for various customer segments by evaluating their responses to the pricing policy. The

administration of the company also take the help of this system in deciding pricing structure for

initial pricing, promotional pricing and discounted pricing.

Cost Accounting System: Cost accounting system is a part of managerial accounting that

revolves around the cost calculation, cost analysis and cost reduction. This system is a structure

that assists the manufacturers of Oshodi Plc to record the stream of assorted costs in order to

manufacture of each product. This accounting system consists approximation of different fixed

costs as well as variable overheads, allocation of cost centres and absorption of costs. The

essential for a good cost accounting system is to be flexible and easy. With the help of flexible

cost accounting system, respective firm is capable to calculate appropriate cost and ascertain the

profitability of the company.

Inventory Management System: This management accounting system is related with

management and supervision of inventory and non-capitalized assets of the enterprises. It helps

the managers in keeping a view over the flow and movement of inventory available within the

firm for the sale. This assists the management in advanced operation and cost calculation for

carrying and selling the products. The line manager of selected firm is capable to track goods

through the entire production and distribution process or the portion of it a business operates in.

this system includes each and everything from warehousing to dispatching for sale, production

to retailing and all the movements of stock and parts between.

Job Costing System: Job costing method is used by the companies when every

manufactured unit or batch of product has specific significations from each other in terms of

quality, quantity, measurements, etc. Job costing systems determine manufacturing costs

systematically by dividing them in overhead, direct labour and direct material costs and

estimating them at their actual value (Bhattacharya, 2014). The goods produced on customised

2

studied about the customer behaviour towards different pricing policies of various products. This

system is used to decide and control the prices of different products at the same time. It examines

the flow of demand with the fluctuation in price at different levels so that the best price for the

product can be opt out in accordance with customer needs (Berry, Broadbent and Otley, 2016). It

also consider the effective life cycle of the product, competitors' pricing policy, profit margin

goals, etc. The Oshodi Plc uses price optimisation system in tailoring the prices of its fruit juices

for various customer segments by evaluating their responses to the pricing policy. The

administration of the company also take the help of this system in deciding pricing structure for

initial pricing, promotional pricing and discounted pricing.

Cost Accounting System: Cost accounting system is a part of managerial accounting that

revolves around the cost calculation, cost analysis and cost reduction. This system is a structure

that assists the manufacturers of Oshodi Plc to record the stream of assorted costs in order to

manufacture of each product. This accounting system consists approximation of different fixed

costs as well as variable overheads, allocation of cost centres and absorption of costs. The

essential for a good cost accounting system is to be flexible and easy. With the help of flexible

cost accounting system, respective firm is capable to calculate appropriate cost and ascertain the

profitability of the company.

Inventory Management System: This management accounting system is related with

management and supervision of inventory and non-capitalized assets of the enterprises. It helps

the managers in keeping a view over the flow and movement of inventory available within the

firm for the sale. This assists the management in advanced operation and cost calculation for

carrying and selling the products. The line manager of selected firm is capable to track goods

through the entire production and distribution process or the portion of it a business operates in.

this system includes each and everything from warehousing to dispatching for sale, production

to retailing and all the movements of stock and parts between.

Job Costing System: Job costing method is used by the companies when every

manufactured unit or batch of product has specific significations from each other in terms of

quality, quantity, measurements, etc. Job costing systems determine manufacturing costs

systematically by dividing them in overhead, direct labour and direct material costs and

estimating them at their actual value (Bhattacharya, 2014). The goods produced on customised

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

specifications is sent to the clients straight away and can not be included in cost accounting or

inventory management system, therefore the administration generates this costing system for job

costing. The management also measures efficiency and performance of the employees in order to

achieve their set goals by using the information provided by job costing method.

P2 Management Accounting Reporting:

Management Accounting Reports: The process of management accounting reporting

assists the management in preparation of appropriate managerial accounting reports which

contain estimations, forecasts and actual effective outcomes related to different activities and

operations. These managerial reports provides accurate financial and statistical data and

information to the managers for making critical business decisions and planning strategies for

success of business objectives. There are so many types of accounting reports generated by the

managerial accountant of Oshodi Plc which are elaborated as below:

Performance Report: Performance report is basically a type of report card provided to

any person or task regarding their efficiency and effectiveness in context with achieving the

goals. This report reviews the performance of each employee as well as entire organization

(Charifzadeh and Taschner, 2017). Top management uses this report to make key strategies for

the future operations and reward the personnels when they perform as they commit while laid off

them who are under performers or dealt with them accordingly. This report also suggests points

towards flaw with the setup. The managers of respective firm prepare performance report for

every employee so that a deep insight can be seen regarding employee performance and

effectiveness.

Accounts Receivable Aging Report: When a business relies hugely on credit terms, an

accounts receivable ageing report is vital for the organization. This report contains all the

essential and material information about debtors and amount that has to be recovered from

customers. This report helps in breaking down the leftover balances of clients into particular time

periods and permits managers to determine the defaulters as well as discover issues in the

company's debtor turnover procedures and policies. Oshodi Plc instructed its managers to

generate this kind of report on a regular basis so that it can indicate the management team to

collect receipts from debtors on time, reduce the ratio of bad debts and liquidity of the firm can

be maintained properly.

3

inventory management system, therefore the administration generates this costing system for job

costing. The management also measures efficiency and performance of the employees in order to

achieve their set goals by using the information provided by job costing method.

P2 Management Accounting Reporting:

Management Accounting Reports: The process of management accounting reporting

assists the management in preparation of appropriate managerial accounting reports which

contain estimations, forecasts and actual effective outcomes related to different activities and

operations. These managerial reports provides accurate financial and statistical data and

information to the managers for making critical business decisions and planning strategies for

success of business objectives. There are so many types of accounting reports generated by the

managerial accountant of Oshodi Plc which are elaborated as below:

Performance Report: Performance report is basically a type of report card provided to

any person or task regarding their efficiency and effectiveness in context with achieving the

goals. This report reviews the performance of each employee as well as entire organization

(Charifzadeh and Taschner, 2017). Top management uses this report to make key strategies for

the future operations and reward the personnels when they perform as they commit while laid off

them who are under performers or dealt with them accordingly. This report also suggests points

towards flaw with the setup. The managers of respective firm prepare performance report for

every employee so that a deep insight can be seen regarding employee performance and

effectiveness.

Accounts Receivable Aging Report: When a business relies hugely on credit terms, an

accounts receivable ageing report is vital for the organization. This report contains all the

essential and material information about debtors and amount that has to be recovered from

customers. This report helps in breaking down the leftover balances of clients into particular time

periods and permits managers to determine the defaulters as well as discover issues in the

company's debtor turnover procedures and policies. Oshodi Plc instructed its managers to

generate this kind of report on a regular basis so that it can indicate the management team to

collect receipts from debtors on time, reduce the ratio of bad debts and liquidity of the firm can

be maintained properly.

3

Budget Report: Budgets reports are very crucial in analysing company performance and

are generated for whole enterprise as well as various departments. A budget report is created

with the help of previous budgets, forecasted budget for current period and data available

regarding actual results (Englund and Gerdin, 2018). This report assists the management in

finding out the variances between standard estimations and real time outcomes and reasons

behind these variances so that remedial or favourable actions can be taken and performance and

productivity of the firm can be improved. Directors of the selected firm uses these budget reports

to cut off the costs, offer better employee rewards and incentives and their terms and conditions

with suppliers and vendors.

Trend Analysis and Forecasting Reports: These trend reports basically comprise the

information about market patterns and trends of product costs, qualities and prices as well as the

deviation between actual and predicted estimations. This report also determines the reasons

behind these variances. These reports provides the assistance to the management of the company

to analyse and examine market trends and utilize these informations in order to prepare budgets,

improving product quality according to the customer requirements and dividing the costs.

Management of Oshodi Plc creates this report to analyse competitive strategies, enhance the use

of technology and betterment of its fruit juice products regarding health of its consumers.

M1 Benefits of Management Accounting Systems:

According to the applications of different management accounting systems in various

situations presented above, benefits of these systems can be defined as below:

Managerial Accounting

Systems

Benefits

Price Optimisation System The management of Oshodi Plc is able to analyse the

behaviour of the customers regarding different prices.

It is helpful in maximisation of profit margin with the help

of customer segmentation.

Cost Accounting System This system can measure the efficiency in production

procedures and aid in improving the quality of the product.

Respective firm is capable to reduce and fix its product

prices with the use of this costing system.

4

are generated for whole enterprise as well as various departments. A budget report is created

with the help of previous budgets, forecasted budget for current period and data available

regarding actual results (Englund and Gerdin, 2018). This report assists the management in

finding out the variances between standard estimations and real time outcomes and reasons

behind these variances so that remedial or favourable actions can be taken and performance and

productivity of the firm can be improved. Directors of the selected firm uses these budget reports

to cut off the costs, offer better employee rewards and incentives and their terms and conditions

with suppliers and vendors.

Trend Analysis and Forecasting Reports: These trend reports basically comprise the

information about market patterns and trends of product costs, qualities and prices as well as the

deviation between actual and predicted estimations. This report also determines the reasons

behind these variances. These reports provides the assistance to the management of the company

to analyse and examine market trends and utilize these informations in order to prepare budgets,

improving product quality according to the customer requirements and dividing the costs.

Management of Oshodi Plc creates this report to analyse competitive strategies, enhance the use

of technology and betterment of its fruit juice products regarding health of its consumers.

M1 Benefits of Management Accounting Systems:

According to the applications of different management accounting systems in various

situations presented above, benefits of these systems can be defined as below:

Managerial Accounting

Systems

Benefits

Price Optimisation System The management of Oshodi Plc is able to analyse the

behaviour of the customers regarding different prices.

It is helpful in maximisation of profit margin with the help

of customer segmentation.

Cost Accounting System This system can measure the efficiency in production

procedures and aid in improving the quality of the product.

Respective firm is capable to reduce and fix its product

prices with the use of this costing system.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Inventory Management

System

This system helps in improving efficiency and productivity

by saving valuable funds, space and time.

The management can eliminate the shortage of inventory

situation and create a satisfy customer base.

Job Costing System It helps the management of selected firm in evaluating all

type of costs in manufacturing process.

This system also helps in evaluation of quality of work

done and employees as well.

D1 Integration of management accounting system and management accounting reporting in

organizational processes:

For the improvement and growth of an establishment, management accounting, its

systems and reporting plays an important role. Different management accounting systems helps

in creating a solid structure for the estimations and forecasting of organizational objective and

aims while reporting system and various reports provides data and information regarding

effectiveness and performance of the whole enterprise as well as every employee and activity

which eventually helps in making futuristic plans, strategies, policies and decisions. Survival of

the Oshodi Plc may be in danger without the help of these accounting and reporting systems.

TASK 2

P3 Calculation of cost using management accounting techniques:

Marginal Costing: Marginal costing is a method which proposed that all variable cost

related to production are allocated to cost units while all fixed overheads for the period are fully

written off against the contribution (Broccardo, 2014).

Marginal costing:

Particulars November (£) December (£)

Sales 500000 600000

Less: Cost of sales

Direct Material Costs -180000 -216000

Direct Labour costs -40000 -48000

Variable Production Overheads -30000 -36000

5

System

This system helps in improving efficiency and productivity

by saving valuable funds, space and time.

The management can eliminate the shortage of inventory

situation and create a satisfy customer base.

Job Costing System It helps the management of selected firm in evaluating all

type of costs in manufacturing process.

This system also helps in evaluation of quality of work

done and employees as well.

D1 Integration of management accounting system and management accounting reporting in

organizational processes:

For the improvement and growth of an establishment, management accounting, its

systems and reporting plays an important role. Different management accounting systems helps

in creating a solid structure for the estimations and forecasting of organizational objective and

aims while reporting system and various reports provides data and information regarding

effectiveness and performance of the whole enterprise as well as every employee and activity

which eventually helps in making futuristic plans, strategies, policies and decisions. Survival of

the Oshodi Plc may be in danger without the help of these accounting and reporting systems.

TASK 2

P3 Calculation of cost using management accounting techniques:

Marginal Costing: Marginal costing is a method which proposed that all variable cost

related to production are allocated to cost units while all fixed overheads for the period are fully

written off against the contribution (Broccardo, 2014).

Marginal costing:

Particulars November (£) December (£)

Sales 500000 600000

Less: Cost of sales

Direct Material Costs -180000 -216000

Direct Labour costs -40000 -48000

Variable Production Overheads -30000 -36000

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

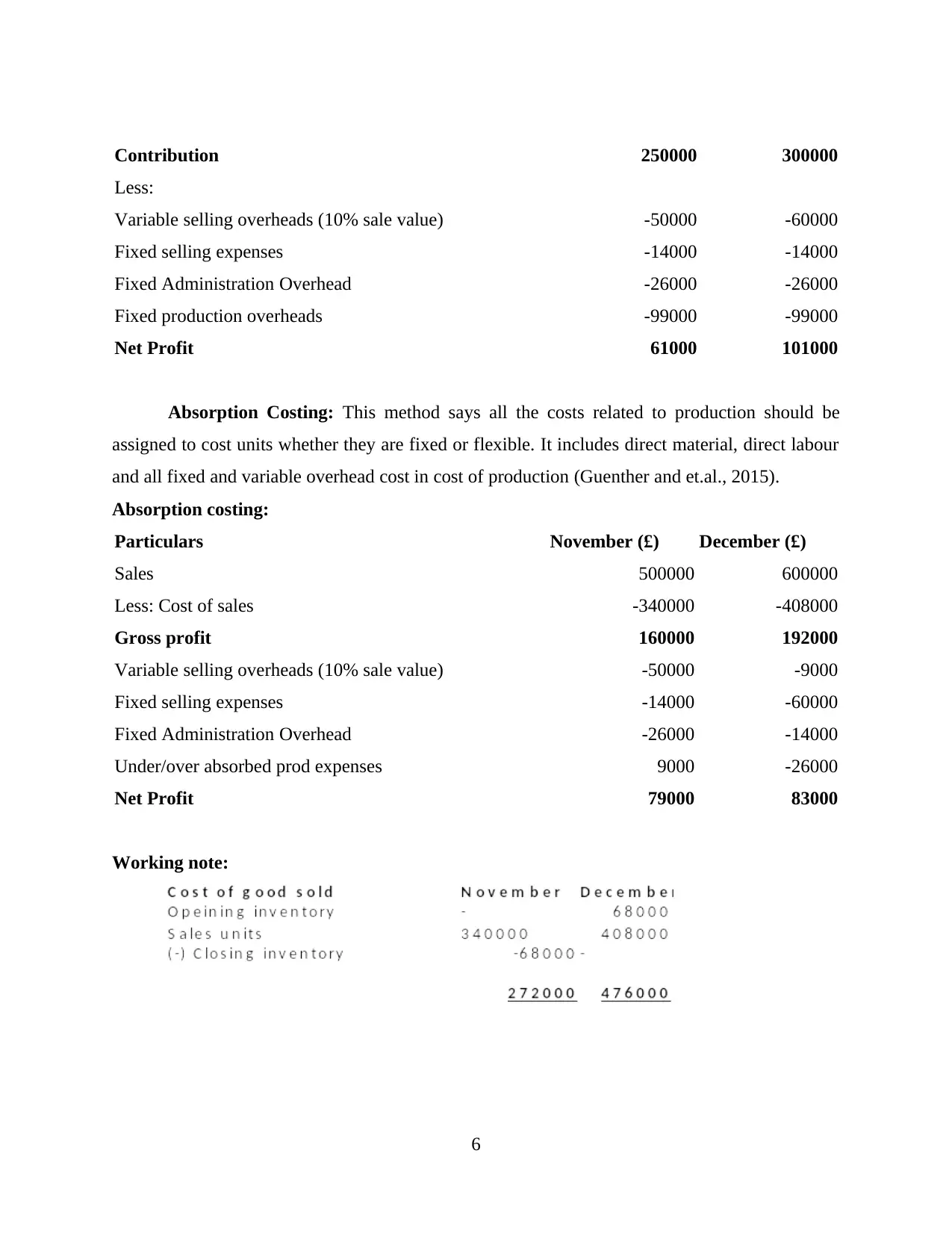

Contribution 250000 300000

Less:

Variable selling overheads (10% sale value) -50000 -60000

Fixed selling expenses -14000 -14000

Fixed Administration Overhead -26000 -26000

Fixed production overheads -99000 -99000

Net Profit 61000 101000

Absorption Costing: This method says all the costs related to production should be

assigned to cost units whether they are fixed or flexible. It includes direct material, direct labour

and all fixed and variable overhead cost in cost of production (Guenther and et.al., 2015).

Absorption costing:

Particulars November (£) December (£)

Sales 500000 600000

Less: Cost of sales -340000 -408000

Gross profit 160000 192000

Variable selling overheads (10% sale value) -50000 -9000

Fixed selling expenses -14000 -60000

Fixed Administration Overhead -26000 -14000

Under/over absorbed prod expenses 9000 -26000

Net Profit 79000 83000

Working note:

6

Less:

Variable selling overheads (10% sale value) -50000 -60000

Fixed selling expenses -14000 -14000

Fixed Administration Overhead -26000 -26000

Fixed production overheads -99000 -99000

Net Profit 61000 101000

Absorption Costing: This method says all the costs related to production should be

assigned to cost units whether they are fixed or flexible. It includes direct material, direct labour

and all fixed and variable overhead cost in cost of production (Guenther and et.al., 2015).

Absorption costing:

Particulars November (£) December (£)

Sales 500000 600000

Less: Cost of sales -340000 -408000

Gross profit 160000 192000

Variable selling overheads (10% sale value) -50000 -9000

Fixed selling expenses -14000 -60000

Fixed Administration Overhead -26000 -14000

Under/over absorbed prod expenses 9000 -26000

Net Profit 79000 83000

Working note:

6

M2 Applying a range of management accounting techniques:

Standard costing: It is a costing technique used by management to identify and calculate

variance between actual cost of the goods that were produced & cost that should have been

occurred. For a manufacturing company, this consists of predetermined material, direct labour,

overhead cost and is used to calculate COGS as well as value of inventory (Kedia, Koh and

Rajgopal, 2015).

Normal costing: It is defined as method of costing which is used to derive cost for

products & services. For a manufacturing company, this comprises of actual cost of materials,

direct labour & production overhead.

D2 Interpretation of profit as calculated by different costing techniques:

As seen in the marginal costing statement, there is a high rise in the net profit figure

calculated for both the months i.e. November and December. It is because this technique does

not consider fixed overheads or inventory in that manner. For the income statement prepared

according to absorption costing technique, the net profit figure for both the months i.e.

November & December have a minor rise. This is because of a huge downfall in the under/over

absorbed production overheads as compared with both the months.

TASK 3

P4 Different types of planning tools used for budgetary control:

Budget: It is defined as a process wherein organisations prepare estimates for the future

gains & losses during the forthcoming year. This includes providing an approximation of all the

budgeted expenses as well as income which can occur during an accounting year. For that

purpose, a company can analyse prior year's budget to get a brief idea of how much funds should

be allocated to each functional department like production, sales, manufacturing, branding,

R&D, packaging & labelling etc (King and Clarkson, 2015). of the organisation. It is required in

order to achieve profitability & liquidity. For the production of JOJO fruit juice, Oshodi PLC

assigns and allocates finances to each functional unit within the company so that the managers

are able to produce good quality juices with attractive packaging.

Budgetary control: It refers to a systematic procedure where different kinds of budget

are prepared by management in order to achieve growth & welfare of the firm. This involves

analysing various activities in an organisation and then allocating funds accordingly. It consists

7

Standard costing: It is a costing technique used by management to identify and calculate

variance between actual cost of the goods that were produced & cost that should have been

occurred. For a manufacturing company, this consists of predetermined material, direct labour,

overhead cost and is used to calculate COGS as well as value of inventory (Kedia, Koh and

Rajgopal, 2015).

Normal costing: It is defined as method of costing which is used to derive cost for

products & services. For a manufacturing company, this comprises of actual cost of materials,

direct labour & production overhead.

D2 Interpretation of profit as calculated by different costing techniques:

As seen in the marginal costing statement, there is a high rise in the net profit figure

calculated for both the months i.e. November and December. It is because this technique does

not consider fixed overheads or inventory in that manner. For the income statement prepared

according to absorption costing technique, the net profit figure for both the months i.e.

November & December have a minor rise. This is because of a huge downfall in the under/over

absorbed production overheads as compared with both the months.

TASK 3

P4 Different types of planning tools used for budgetary control:

Budget: It is defined as a process wherein organisations prepare estimates for the future

gains & losses during the forthcoming year. This includes providing an approximation of all the

budgeted expenses as well as income which can occur during an accounting year. For that

purpose, a company can analyse prior year's budget to get a brief idea of how much funds should

be allocated to each functional department like production, sales, manufacturing, branding,

R&D, packaging & labelling etc (King and Clarkson, 2015). of the organisation. It is required in

order to achieve profitability & liquidity. For the production of JOJO fruit juice, Oshodi PLC

assigns and allocates finances to each functional unit within the company so that the managers

are able to produce good quality juices with attractive packaging.

Budgetary control: It refers to a systematic procedure where different kinds of budget

are prepared by management in order to achieve growth & welfare of the firm. This involves

analysing various activities in an organisation and then allocating funds accordingly. It consists

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

of a variety of budgeted statements like capital, operational, cash, master, zero-based, fixed etc.

The managers are required to assess Oshodi PLC's performance and then allocate finances to

each functional unit so that they are utilised by putting efforts efficiently. In relation to this, the

manufacturing company prepares a budgetary control procedure wherein forecasts are prepared

for any future gains or losses. Some of them are explained below:

Capital budget: It refers to a process of evaluating investments and huge expenses in

order to obtain best return of investment. This is a way by which Oshodi PLC analyses how

much finance is required by the management in order to achieve goals & objectives of future

perspectives for the company (Vladu, Amat and Cuzdriorean, 2017). Usually, these budgets are

required by managers to identify any potential projects or long-term strategies so that the

company can attain high profit margin. Oshodi PLC selects an appropriate investment appraisal

technique i.e. NPV, IRR, ARR etc. due to which it is able to invest in long-term projects with

having an idea about own existing profitability situation with the help of capital budget. Some of

the pros and cons of using capital budgeting by the company are mentioned below:

Advantages:

It helps Oshodi PLC in choosing of appropriate investment appraisal techniques like

NPV, IRR, Payback period, ARR etc. for investing in future or current projects.

Capital budgeting technique helps in determining the risks involved in an investment

opportunity and states hoe these can affect returns of a company.

Disadvantages:

It requires an estimation of future cash inflows & outflows which is hard to determine as

any events in the future are uncertain.

This can affect long-term durability & profitability of Oshodi PLC in case a wrong

capital budgeting decision has been made.

Flexible budget: It is a type of budget which can flex or adjust itself with any change in

sales volume or activity. This is also known as a variable budget as it uses revenue & expenses

produced in the current year as a baseline to estimate how these will modify with changing level

of output (Vardon, Burnett and Dovers, 2016). These are beneficial for the management as they

can easily alter any amount of income or expense due to the nature of this forecast. Oshodi PLC

prepares flexible budget for the costs that vary with change in level of sales volume like

packaging & branding charges of JOJO fruit juice.

8

The managers are required to assess Oshodi PLC's performance and then allocate finances to

each functional unit so that they are utilised by putting efforts efficiently. In relation to this, the

manufacturing company prepares a budgetary control procedure wherein forecasts are prepared

for any future gains or losses. Some of them are explained below:

Capital budget: It refers to a process of evaluating investments and huge expenses in

order to obtain best return of investment. This is a way by which Oshodi PLC analyses how

much finance is required by the management in order to achieve goals & objectives of future

perspectives for the company (Vladu, Amat and Cuzdriorean, 2017). Usually, these budgets are

required by managers to identify any potential projects or long-term strategies so that the

company can attain high profit margin. Oshodi PLC selects an appropriate investment appraisal

technique i.e. NPV, IRR, ARR etc. due to which it is able to invest in long-term projects with

having an idea about own existing profitability situation with the help of capital budget. Some of

the pros and cons of using capital budgeting by the company are mentioned below:

Advantages:

It helps Oshodi PLC in choosing of appropriate investment appraisal techniques like

NPV, IRR, Payback period, ARR etc. for investing in future or current projects.

Capital budgeting technique helps in determining the risks involved in an investment

opportunity and states hoe these can affect returns of a company.

Disadvantages:

It requires an estimation of future cash inflows & outflows which is hard to determine as

any events in the future are uncertain.

This can affect long-term durability & profitability of Oshodi PLC in case a wrong

capital budgeting decision has been made.

Flexible budget: It is a type of budget which can flex or adjust itself with any change in

sales volume or activity. This is also known as a variable budget as it uses revenue & expenses

produced in the current year as a baseline to estimate how these will modify with changing level

of output (Vardon, Burnett and Dovers, 2016). These are beneficial for the management as they

can easily alter any amount of income or expense due to the nature of this forecast. Oshodi PLC

prepares flexible budget for the costs that vary with change in level of sales volume like

packaging & branding charges of JOJO fruit juice.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Advantages:

A flexible budget can update itself in diverse or adverse conditions by modifying with

each level of sales volume.

With the help of this budget, Oshodi PLC can change the price of JOJO fruit juice during

change of season. For example, in summers it can increase the cost due to high demand

whereas during winters the company can low down the value of its products.

Disadvantages:

It is subject to manipulation as the cost of products or services can change easily due to

its variable nature.

During peak season, it can be a time-consuming process for Oshodi PLC as they will

have to consider the price of each product & service with change in output.

Zero-based budget: It is a type of budget which is prepared from scratch without

considering any prior expenses or income. These are usually started from a zero-base by

analysing all the gains & losses that can arise during an accounting year (Masztalerz, 2014).

Mostly, this requires justification of each and every amount considered while preparing a

forecast for the future. Oshodi PLC analyses the customer's expectations as to what

diversification they would want in JOJO fruit juices. It can be a modification in price, increasing

the quantity of the product or making it available in tetra packs which can be used by the

consumer for travelling purpose.

Advantages:

It is easy to allocate resources as Oshodi PLC sell large carton of juices to suppliers

which makes it convenient for the company to efficiently distribute among different chain

of shops or stores.

This improves co-ordination and communication among staff members as it requires

decision-making at each step of preparing a forecast.

Disadvantages:

It requires well efficient staff who carry an understanding of all the line items used in

producing of budget since this is prepared from a zero-base.

Zero-based budget is easy to manipulate as it does not consider previous year's expenses

or income in preparation of the forecast.

9

A flexible budget can update itself in diverse or adverse conditions by modifying with

each level of sales volume.

With the help of this budget, Oshodi PLC can change the price of JOJO fruit juice during

change of season. For example, in summers it can increase the cost due to high demand

whereas during winters the company can low down the value of its products.

Disadvantages:

It is subject to manipulation as the cost of products or services can change easily due to

its variable nature.

During peak season, it can be a time-consuming process for Oshodi PLC as they will

have to consider the price of each product & service with change in output.

Zero-based budget: It is a type of budget which is prepared from scratch without

considering any prior expenses or income. These are usually started from a zero-base by

analysing all the gains & losses that can arise during an accounting year (Masztalerz, 2014).

Mostly, this requires justification of each and every amount considered while preparing a

forecast for the future. Oshodi PLC analyses the customer's expectations as to what

diversification they would want in JOJO fruit juices. It can be a modification in price, increasing

the quantity of the product or making it available in tetra packs which can be used by the

consumer for travelling purpose.

Advantages:

It is easy to allocate resources as Oshodi PLC sell large carton of juices to suppliers

which makes it convenient for the company to efficiently distribute among different chain

of shops or stores.

This improves co-ordination and communication among staff members as it requires

decision-making at each step of preparing a forecast.

Disadvantages:

It requires well efficient staff who carry an understanding of all the line items used in

producing of budget since this is prepared from a zero-base.

Zero-based budget is easy to manipulate as it does not consider previous year's expenses

or income in preparation of the forecast.

9

M3 Use of planning tools and their application in forecasting budgets:

There is always a requirement of using different planning tools in preparation of budgets.

These tools are a useful asset for the company as it helps Oshodi PLC decide the price to be kept

for its different flavours of JOJO fruit juices. Different methods of budgeting also play a crucial

role in producing a forecast for future expenses & losses during the forthcoming year. They

include zero-based, fixed, flexible, capital, operational budget etc. These tools help the company

in producing a forecast from scratch without considering any prior year's estimate, analysing

various investment appraisal techniques by which an organisation can effectively invest in a

project.

TASK 4

P5 Management accounting techniques used to identify financial problems:

On a day-to-day basis, companies can face various financial problems which are

mentioned below:

Late payment from creditors: Most of the suppliers tend to sell their products on bulk

basis as this helps them in maintaining their client base and having good connections with the

customers. In the long-term, Oshodi PLC can face a downfall in profit margin if they continue to

give extended credit terms to the suppliers.

Sudden expenses: These expenses can arise in case of loss due to fire, loss of theft etc.

In such cases, the management team of Oshodi PLC is advised to take out some amount from

the reserves in order to use them if any unforeseen expense arises.

Improper money management: This can arise if Oshodi PLC appoints those people

who do not have the knowledge of managing funds for different activities in an organisation. For

that purpose, the company should hire supervisors for each individua Oshodi PLC l department

and then allocate funds to them so that proper management of finances is carried out.

In order to identify and resolve financial problems in a company, following measures

should be considered:

Key performance indicators: These are the indicators which measure performance of

organisational activities. This can be further categorised into financial as well as non-financial

which analyse the profitability as well as liquidity position of a company. It is an indicator by

which a critical success factor can be achieved (Mihăilă, 2014). This is required by managers to

10

There is always a requirement of using different planning tools in preparation of budgets.

These tools are a useful asset for the company as it helps Oshodi PLC decide the price to be kept

for its different flavours of JOJO fruit juices. Different methods of budgeting also play a crucial

role in producing a forecast for future expenses & losses during the forthcoming year. They

include zero-based, fixed, flexible, capital, operational budget etc. These tools help the company

in producing a forecast from scratch without considering any prior year's estimate, analysing

various investment appraisal techniques by which an organisation can effectively invest in a

project.

TASK 4

P5 Management accounting techniques used to identify financial problems:

On a day-to-day basis, companies can face various financial problems which are

mentioned below:

Late payment from creditors: Most of the suppliers tend to sell their products on bulk

basis as this helps them in maintaining their client base and having good connections with the

customers. In the long-term, Oshodi PLC can face a downfall in profit margin if they continue to

give extended credit terms to the suppliers.

Sudden expenses: These expenses can arise in case of loss due to fire, loss of theft etc.

In such cases, the management team of Oshodi PLC is advised to take out some amount from

the reserves in order to use them if any unforeseen expense arises.

Improper money management: This can arise if Oshodi PLC appoints those people

who do not have the knowledge of managing funds for different activities in an organisation. For

that purpose, the company should hire supervisors for each individua Oshodi PLC l department

and then allocate funds to them so that proper management of finances is carried out.

In order to identify and resolve financial problems in a company, following measures

should be considered:

Key performance indicators: These are the indicators which measure performance of

organisational activities. This can be further categorised into financial as well as non-financial

which analyse the profitability as well as liquidity position of a company. It is an indicator by

which a critical success factor can be achieved (Mihăilă, 2014). This is required by managers to

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.