Management Accounting in Oshodi PLC: Unit 5 Report Analysis

VerifiedAdded on 2021/02/20

|16

|5239

|65

Report

AI Summary

This report provides a detailed analysis of management accounting systems and their application within Oshodi PLC, a manufacturing company producing JOJO fruit juice. The report covers various aspects of management accounting, including different systems like price optimization, inventory management, cost accounting, and job costing, along with their essential requirements. It explores different methodologies utilized in management accounting reporting, such as performance reports, budget reports, and inventory management reports, evaluating their benefits and applications in an organizational context. Furthermore, the report computes costs using marginal and absorption costing techniques to prepare financial income statements, demonstrating the application of management accounting techniques in producing appropriate financial reporting documents. It also examines the advantages and disadvantages of various planning tools utilized for budgetary control, and analyzes how management accounting systems contribute towards sustainable organizational success and how companies adapt to management systems in the face of financial issues, with a focus on resolving financial problems through accounting planning tools.

UNIT 5 –

MANAGEMENT

ACCOUNTING L-4

MANAGEMENT

ACCOUNTING L-4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1. Various Management Accounting Systems and their essential requirements .................1

P2. Different Methodologies utilised in Management Accounting Reporting ......................3

M1. Evaluating benefits of Management Accounting Systems and their application in

organisational context.............................................................................................................5

TASK 2............................................................................................................................................5

P3. Computing Costs through Marginal and Absorption Costing to prepare financial income

statements...............................................................................................................................5

M2. Application of management accounting techniques to produce appropriate financial

reporting documents...............................................................................................................7

TASK 3............................................................................................................................................8

P4. Advantages and Disadvantages of various planning tools utilised to exercise budgetary

control.....................................................................................................................................8

M3. Analysing use of different planning tools and their application for developing and

forecasting budgets...............................................................................................................10

TASK 4..........................................................................................................................................10

P5. Examining how companies adapt to management systems in the face of financial issues10

M4. Analysing how management accounting systems contribute towards sustainable

organisational success..........................................................................................................12

D3. Evaluating how accounting planning tools help in resolving financial problems.........12

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1. Various Management Accounting Systems and their essential requirements .................1

P2. Different Methodologies utilised in Management Accounting Reporting ......................3

M1. Evaluating benefits of Management Accounting Systems and their application in

organisational context.............................................................................................................5

TASK 2............................................................................................................................................5

P3. Computing Costs through Marginal and Absorption Costing to prepare financial income

statements...............................................................................................................................5

M2. Application of management accounting techniques to produce appropriate financial

reporting documents...............................................................................................................7

TASK 3............................................................................................................................................8

P4. Advantages and Disadvantages of various planning tools utilised to exercise budgetary

control.....................................................................................................................................8

M3. Analysing use of different planning tools and their application for developing and

forecasting budgets...............................................................................................................10

TASK 4..........................................................................................................................................10

P5. Examining how companies adapt to management systems in the face of financial issues10

M4. Analysing how management accounting systems contribute towards sustainable

organisational success..........................................................................................................12

D3. Evaluating how accounting planning tools help in resolving financial problems.........12

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION

The concept of 'Management Accounting' is related to the processes and systems adopted

by the organisations in order to ensure smooth functioning of their internal operations. Hence, it

includes the procedures that recognise, measure, evaluate, interpret and convey important

information regarding the business activities to the managers across all levels. This helps them to

undertake informed decisions as well as facilitate the successful fulfilment of organisational

goals within a stipulated time-frame (Achleitner and others, 2014) .

This project report aims to provide an insight into how the management accounting

systems and techniques contribute towards the successful and smooth operation of a business

entity. For this purpose, Oshodi PLC has been taken into account which is a manufacturing

enterprise that produces JOJO fruit juice across all age bracket. Using this information, an

income statement has been produced under Marginal and Absorption Costing. Additionally, this

report also explains the merits and demerits of different planning tools that are utilised for

budgetary control as well as compares how different organisations adopt such systems to respond

to financial problems.

TASK 1

P1. Various Management Accounting Systems and their essential requirements

Management Accounting can be defined as a system that facilitates the analysis of

various business activities so as to enable the business managers to make better decisions from a

short-term and long-term perspective. Due to this reason, it is essential for a manager to analyse

their internal as well as external business environment in order to translate raw data into

meaningful information. This, then, helps the enterprise in achieving a comparative advantage

for the company as a whole. In the context of given case scenario, Oshodi PLC is a

manufacturing business which produces JOJO fruit juice that is consumed across all

demographics. In order to ensure that the business is able to perform well and control its costs in

an effective manner, the following management accounting systems can be employed by it:

Price Optimisation System: This can be referred to as a method that facilitates the

determination of optimum price levels for a company's products or services under

alternative scenarios (Zvezdov and Schaltegger, 2015). Thus, enabling the management

to better achieve their goals in a sustainable manner as well as meet customer acquisition

1

The concept of 'Management Accounting' is related to the processes and systems adopted

by the organisations in order to ensure smooth functioning of their internal operations. Hence, it

includes the procedures that recognise, measure, evaluate, interpret and convey important

information regarding the business activities to the managers across all levels. This helps them to

undertake informed decisions as well as facilitate the successful fulfilment of organisational

goals within a stipulated time-frame (Achleitner and others, 2014) .

This project report aims to provide an insight into how the management accounting

systems and techniques contribute towards the successful and smooth operation of a business

entity. For this purpose, Oshodi PLC has been taken into account which is a manufacturing

enterprise that produces JOJO fruit juice across all age bracket. Using this information, an

income statement has been produced under Marginal and Absorption Costing. Additionally, this

report also explains the merits and demerits of different planning tools that are utilised for

budgetary control as well as compares how different organisations adopt such systems to respond

to financial problems.

TASK 1

P1. Various Management Accounting Systems and their essential requirements

Management Accounting can be defined as a system that facilitates the analysis of

various business activities so as to enable the business managers to make better decisions from a

short-term and long-term perspective. Due to this reason, it is essential for a manager to analyse

their internal as well as external business environment in order to translate raw data into

meaningful information. This, then, helps the enterprise in achieving a comparative advantage

for the company as a whole. In the context of given case scenario, Oshodi PLC is a

manufacturing business which produces JOJO fruit juice that is consumed across all

demographics. In order to ensure that the business is able to perform well and control its costs in

an effective manner, the following management accounting systems can be employed by it:

Price Optimisation System: This can be referred to as a method that facilitates the

determination of optimum price levels for a company's products or services under

alternative scenarios (Zvezdov and Schaltegger, 2015). Thus, enabling the management

to better achieve their goals in a sustainable manner as well as meet customer acquisition

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

targets within stipulated time periods. As price is a driving factor in determining the

bottom-line sales for any organisation, it is important for the management to know its

ideal level of price, strategies and structure (Aouni, McGillis and Abdulkarim, 2017) .

This would not only help in maintaining competitiveness within the market but also

create comparative advantage for the company, thus, enhancing their overall market

share. For its implementation, it is required by Osholdi Plc to consider its current pricing

strategy as well as value of the product to both buyer and itself. Based on this, the most

suitable pricing optimisation system can be identified and utilised by the business.

Inventory management System: Stock-keeping is one of the crucial practices of any

organisation. Each and every manufacturing business enterprise holds inventory in the

form of finished goods, work-in-progress and raw material. Thus, it becomes paramount

for the management to know that the inventory management system implemented by it is

suitable for the organisation to full extent. For Osholdi, most of the inventory is in the

form of fruit-juice bottles or packs. In order to ensure that no abnormal wastage or

shortage of material takes place, its inventory systems must be fully suitable to its

operational requirements. Thus, the essential requirements of an ideal inventory

management system include location, storage needs, types of the products included in the

inventory are some of the key factors that determine what policies and systems related to

inventory management need to be adopted by the business.

Cost Accounting System: Another important accounting system of management, Cost

Accounting Systems include different activities which facilitate the business manager to

determine whether or not the available resources are being utilised optimally. Being a

manufacturing company, Osholdi's cost-based system is of paramount importance as it

helps in deciding the overall pricing strategies for the company (Waters, 2015) . Thus,

one can say that the essential requirements of this management system is to be

informative, simple, accurate, authentic, uniform, adaptive and flexible enough to be

integrated with other managerial functions such as finance, taxation, operations and

marketing among others.

Job Costing System: This involves the process of accumulating information regarding

costs that are specific to the production and deliverance of a particular job. For Osholdi

2

bottom-line sales for any organisation, it is important for the management to know its

ideal level of price, strategies and structure (Aouni, McGillis and Abdulkarim, 2017) .

This would not only help in maintaining competitiveness within the market but also

create comparative advantage for the company, thus, enhancing their overall market

share. For its implementation, it is required by Osholdi Plc to consider its current pricing

strategy as well as value of the product to both buyer and itself. Based on this, the most

suitable pricing optimisation system can be identified and utilised by the business.

Inventory management System: Stock-keeping is one of the crucial practices of any

organisation. Each and every manufacturing business enterprise holds inventory in the

form of finished goods, work-in-progress and raw material. Thus, it becomes paramount

for the management to know that the inventory management system implemented by it is

suitable for the organisation to full extent. For Osholdi, most of the inventory is in the

form of fruit-juice bottles or packs. In order to ensure that no abnormal wastage or

shortage of material takes place, its inventory systems must be fully suitable to its

operational requirements. Thus, the essential requirements of an ideal inventory

management system include location, storage needs, types of the products included in the

inventory are some of the key factors that determine what policies and systems related to

inventory management need to be adopted by the business.

Cost Accounting System: Another important accounting system of management, Cost

Accounting Systems include different activities which facilitate the business manager to

determine whether or not the available resources are being utilised optimally. Being a

manufacturing company, Osholdi's cost-based system is of paramount importance as it

helps in deciding the overall pricing strategies for the company (Waters, 2015) . Thus,

one can say that the essential requirements of this management system is to be

informative, simple, accurate, authentic, uniform, adaptive and flexible enough to be

integrated with other managerial functions such as finance, taxation, operations and

marketing among others.

Job Costing System: This involves the process of accumulating information regarding

costs that are specific to the production and deliverance of a particular job. For Osholdi

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

PLC, this type of management accounting system requires three types of information viz.

Direct Materials, Direct Labour and Overheads. These have been discussed as under:

▪ Direct Material: For an optimal job costing system, traceability of direct material

must be easy, especially those that are used or scrapped during the course of the

job. Thus, enabling the business manager to match costs efficiently with their

relevant jobs (Datar and Rajan, 2014) .

▪ Direct Labour: Typically, this may be identified through the time-cards allotted

to the workers and linked to the software. Thus, facilitating the identification of

job in an easier manner as well as implementation of costs to the jobs correctly.

▪ Overheads: Another important piece of information required for this system is

Overheads. These may be either assigned to one or more cost pools in the form of

depreciation or any other cost which may be bifurcated among various jobs at the

end of an accounting period.

Thus, for the job costing system to be efficient enough, it is crucial for the business managers to

be aware of the needs and requirements of their products.

P2. Different Methodologies utilised in Management Accounting Reporting

Management Accounting Reporting can be defined as a business practice which

includes a comprehensive process of planning, controlling, decision-making and measuring

corporate performance using a variety of customized reports. Two characteristics of a good

management accounting report is their reliability and accuracy in communicating important

financial information to the internal management in a concise and unambiguous manner. One of

the main features of this practice is that the preparation of such reports is not a static but a

dynamic process. Thus, they are continuously being prepared by the organisations, including

Osholdi, to serve different purpose all around the world. Mainly, these reports can be classified

on the basis of different methodologies that have been described as under:

Performance Report: It is important to determine overall corporate as well as internal

performance across all organisational levels. This is due to the fact that regular review of

this component helps in the identification of any deviations or shortcomings occurring in

a given department or group of employees. For Osholdi, this report holds an important

status, mainly because manufacturing processes as well as employee activities are

required to be in synchronization (Ge and Kim, 2014) . Otherwise, the company can incur

3

Direct Materials, Direct Labour and Overheads. These have been discussed as under:

▪ Direct Material: For an optimal job costing system, traceability of direct material

must be easy, especially those that are used or scrapped during the course of the

job. Thus, enabling the business manager to match costs efficiently with their

relevant jobs (Datar and Rajan, 2014) .

▪ Direct Labour: Typically, this may be identified through the time-cards allotted

to the workers and linked to the software. Thus, facilitating the identification of

job in an easier manner as well as implementation of costs to the jobs correctly.

▪ Overheads: Another important piece of information required for this system is

Overheads. These may be either assigned to one or more cost pools in the form of

depreciation or any other cost which may be bifurcated among various jobs at the

end of an accounting period.

Thus, for the job costing system to be efficient enough, it is crucial for the business managers to

be aware of the needs and requirements of their products.

P2. Different Methodologies utilised in Management Accounting Reporting

Management Accounting Reporting can be defined as a business practice which

includes a comprehensive process of planning, controlling, decision-making and measuring

corporate performance using a variety of customized reports. Two characteristics of a good

management accounting report is their reliability and accuracy in communicating important

financial information to the internal management in a concise and unambiguous manner. One of

the main features of this practice is that the preparation of such reports is not a static but a

dynamic process. Thus, they are continuously being prepared by the organisations, including

Osholdi, to serve different purpose all around the world. Mainly, these reports can be classified

on the basis of different methodologies that have been described as under:

Performance Report: It is important to determine overall corporate as well as internal

performance across all organisational levels. This is due to the fact that regular review of

this component helps in the identification of any deviations or shortcomings occurring in

a given department or group of employees. For Osholdi, this report holds an important

status, mainly because manufacturing processes as well as employee activities are

required to be in synchronization (Ge and Kim, 2014) . Otherwise, the company can incur

3

huge amount of losses so much so that its current level of economies of scale is

diminished. On the other hand, inclusion of such reports can also enable the management

to recognise and reward those who have been performing excellently within their

respective departments or field. Thus, acting as a motivator for others to follow suit.

Budget Report: Similar to Performance Report, this type of management accounting

report enables the business manager to ascertain the performance of various cost centres

as well as overall corporate performance. Usually, a master budget is prepared by the

companies so as to know the overall allocation of available resources in an effective

manner. Based on the level of complexity and nature of business, the number of budget

reports prepared across all organisational levels can vary. In the context of given case

scenario, Osholdi prepares this report to understand variances among actual and standard

costing figures. This enables the business managers to know weak as well as

opportunistic areas that can be improved and utilised to expand their overall profits and

performance.

Account Receivable Ageing Report: This report includes a detailed break-down of

account receivables based on the time and limits agreed upon between the company and

such parties. Thus, enabling the management to know about outstanding amounts,

upcoming deadlines to recover money as well as potential bad-debts for each provisions

can be made well in advance. As Osholdi is a manufacturing business, its sensible for it

to have a large amount of accounts payable as well as receivables. Thus, formulation of

such reports is crucial for the company to ensure that their current credit policies are

strong enough to be adhered to by the lending parties or not.

Inventory Management Report: Inventory Management is an important practice which

helps in the determination of economic quantity for the company, re-order or safety stock

levels as well as ensure their easy traceability. For Osholdi, this report helps in

maintaining record of materials utilised and overheads incurred in relation to them in a

comprehensive manner. It is helpful for the organisation as this report facilitates the

determination of current status of the warehouse, transit or delivered to clients in an

efficient manner (Guragai and others, 2015).

4

diminished. On the other hand, inclusion of such reports can also enable the management

to recognise and reward those who have been performing excellently within their

respective departments or field. Thus, acting as a motivator for others to follow suit.

Budget Report: Similar to Performance Report, this type of management accounting

report enables the business manager to ascertain the performance of various cost centres

as well as overall corporate performance. Usually, a master budget is prepared by the

companies so as to know the overall allocation of available resources in an effective

manner. Based on the level of complexity and nature of business, the number of budget

reports prepared across all organisational levels can vary. In the context of given case

scenario, Osholdi prepares this report to understand variances among actual and standard

costing figures. This enables the business managers to know weak as well as

opportunistic areas that can be improved and utilised to expand their overall profits and

performance.

Account Receivable Ageing Report: This report includes a detailed break-down of

account receivables based on the time and limits agreed upon between the company and

such parties. Thus, enabling the management to know about outstanding amounts,

upcoming deadlines to recover money as well as potential bad-debts for each provisions

can be made well in advance. As Osholdi is a manufacturing business, its sensible for it

to have a large amount of accounts payable as well as receivables. Thus, formulation of

such reports is crucial for the company to ensure that their current credit policies are

strong enough to be adhered to by the lending parties or not.

Inventory Management Report: Inventory Management is an important practice which

helps in the determination of economic quantity for the company, re-order or safety stock

levels as well as ensure their easy traceability. For Osholdi, this report helps in

maintaining record of materials utilised and overheads incurred in relation to them in a

comprehensive manner. It is helpful for the organisation as this report facilitates the

determination of current status of the warehouse, transit or delivered to clients in an

efficient manner (Guragai and others, 2015).

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

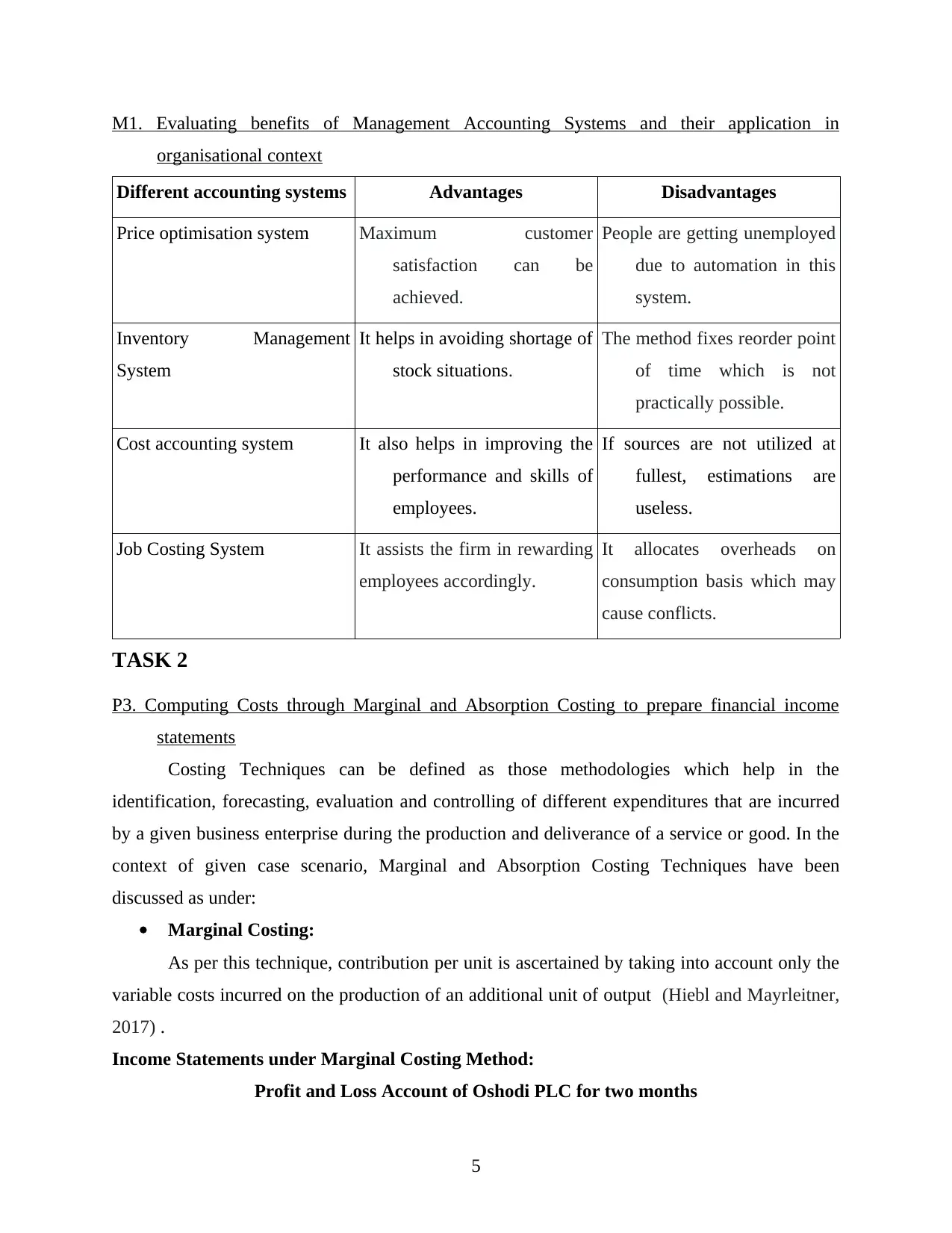

M1. Evaluating benefits of Management Accounting Systems and their application in

organisational context

Different accounting systems Advantages Disadvantages

Price optimisation system Maximum customer

satisfaction can be

achieved.

People are getting unemployed

due to automation in this

system.

Inventory Management

System

It helps in avoiding shortage of

stock situations.

The method fixes reorder point

of time which is not

practically possible.

Cost accounting system It also helps in improving the

performance and skills of

employees.

If sources are not utilized at

fullest, estimations are

useless.

Job Costing System It assists the firm in rewarding

employees accordingly.

It allocates overheads on

consumption basis which may

cause conflicts.

TASK 2

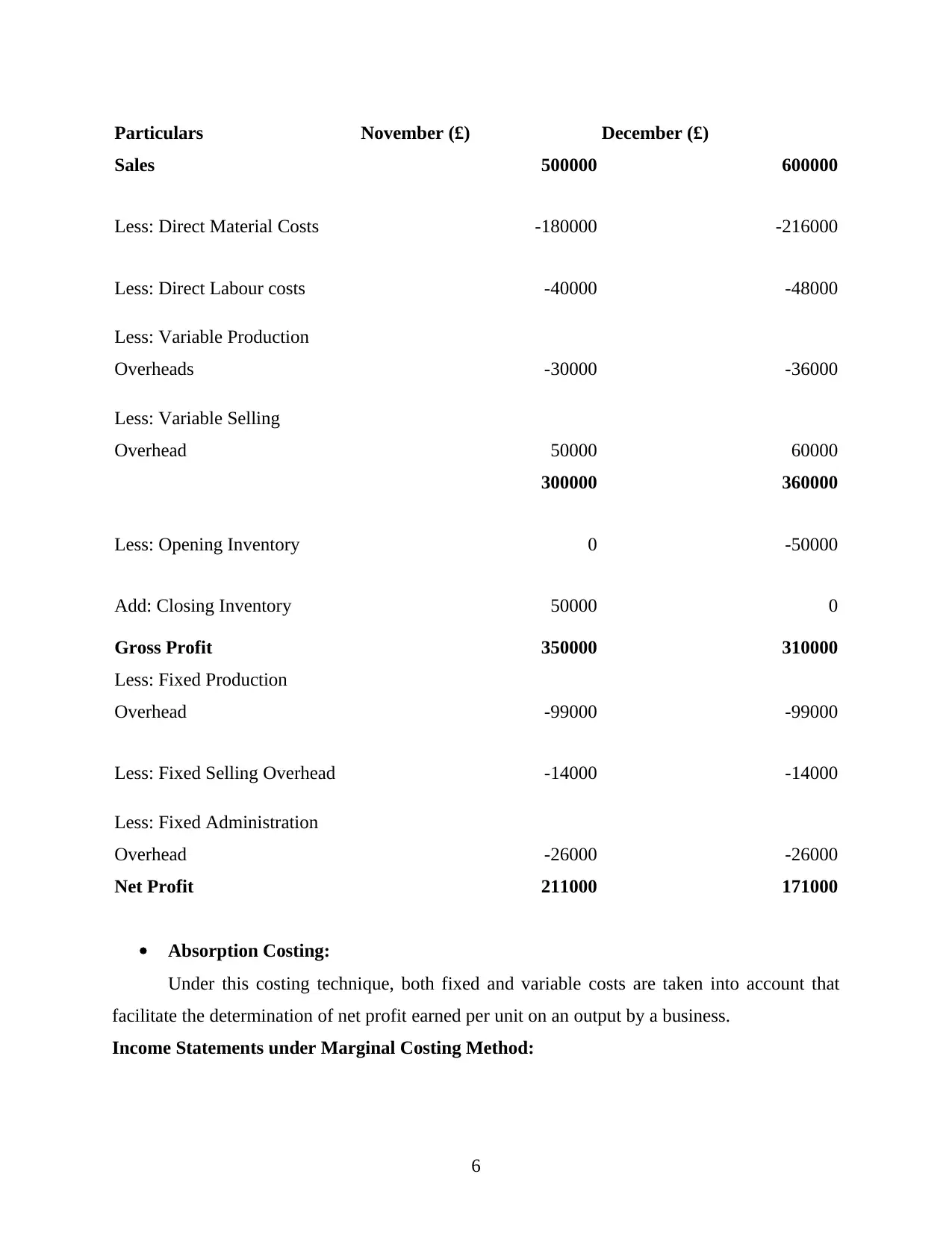

P3. Computing Costs through Marginal and Absorption Costing to prepare financial income

statements

Costing Techniques can be defined as those methodologies which help in the

identification, forecasting, evaluation and controlling of different expenditures that are incurred

by a given business enterprise during the production and deliverance of a service or good. In the

context of given case scenario, Marginal and Absorption Costing Techniques have been

discussed as under:

Marginal Costing:

As per this technique, contribution per unit is ascertained by taking into account only the

variable costs incurred on the production of an additional unit of output (Hiebl and Mayrleitner,

2017) .

Income Statements under Marginal Costing Method:

Profit and Loss Account of Oshodi PLC for two months

5

organisational context

Different accounting systems Advantages Disadvantages

Price optimisation system Maximum customer

satisfaction can be

achieved.

People are getting unemployed

due to automation in this

system.

Inventory Management

System

It helps in avoiding shortage of

stock situations.

The method fixes reorder point

of time which is not

practically possible.

Cost accounting system It also helps in improving the

performance and skills of

employees.

If sources are not utilized at

fullest, estimations are

useless.

Job Costing System It assists the firm in rewarding

employees accordingly.

It allocates overheads on

consumption basis which may

cause conflicts.

TASK 2

P3. Computing Costs through Marginal and Absorption Costing to prepare financial income

statements

Costing Techniques can be defined as those methodologies which help in the

identification, forecasting, evaluation and controlling of different expenditures that are incurred

by a given business enterprise during the production and deliverance of a service or good. In the

context of given case scenario, Marginal and Absorption Costing Techniques have been

discussed as under:

Marginal Costing:

As per this technique, contribution per unit is ascertained by taking into account only the

variable costs incurred on the production of an additional unit of output (Hiebl and Mayrleitner,

2017) .

Income Statements under Marginal Costing Method:

Profit and Loss Account of Oshodi PLC for two months

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Particulars November (£) December (£)

Sales 500000 600000

Less: Direct Material Costs -180000 -216000

Less: Direct Labour costs -40000 -48000

Less: Variable Production

Overheads -30000 -36000

Less: Variable Selling

Overhead 50000 60000

300000 360000

Less: Opening Inventory 0 -50000

Add: Closing Inventory 50000 0

Gross Profit 350000 310000

Less: Fixed Production

Overhead -99000 -99000

Less: Fixed Selling Overhead -14000 -14000

Less: Fixed Administration

Overhead -26000 -26000

Net Profit 211000 171000

Absorption Costing:

Under this costing technique, both fixed and variable costs are taken into account that

facilitate the determination of net profit earned per unit on an output by a business.

Income Statements under Marginal Costing Method:

6

Sales 500000 600000

Less: Direct Material Costs -180000 -216000

Less: Direct Labour costs -40000 -48000

Less: Variable Production

Overheads -30000 -36000

Less: Variable Selling

Overhead 50000 60000

300000 360000

Less: Opening Inventory 0 -50000

Add: Closing Inventory 50000 0

Gross Profit 350000 310000

Less: Fixed Production

Overhead -99000 -99000

Less: Fixed Selling Overhead -14000 -14000

Less: Fixed Administration

Overhead -26000 -26000

Net Profit 211000 171000

Absorption Costing:

Under this costing technique, both fixed and variable costs are taken into account that

facilitate the determination of net profit earned per unit on an output by a business.

Income Statements under Marginal Costing Method:

6

Particulars November (£) December (£)

Sales 500000 600000

Less: Direct Material Costs -180000 -216000

Less: Direct Labour costs -40000 -48000

Less: Variable Production Overheads -30000 -36000

Less: Fixed Production Overhead -99000 -99000

151000 201000

Less: Opening Inventory 0 -66500

Add: Closing Inventory 66500 0

Gross Profit 217500 134500

Less: Variable Selling Overhead -50000 -60000

Less: Fixed Selling Overhead -14000 -14000

Less: Fixed Administration Overhead -26000 -26000

Net Profit 127500 34500

Over/Under Absorption of Fixed Production Overheads:

Particulars November (£) December (£)

Actual Production Expenses 99000 99000

Standard Production Overheads 90750 108900

Over/Under Absorption 8250 -9900

M2. Application of management accounting techniques to produce appropriate financial

reporting documents

Under Marginal and Absorption Costing techniques, there is a variation in the Net profit

figures. One can observe that the Marginal Costing method generates a higher profit of £211,000

and £171,000 for November and December respectively in comparison to Absorption costing

7

Sales 500000 600000

Less: Direct Material Costs -180000 -216000

Less: Direct Labour costs -40000 -48000

Less: Variable Production Overheads -30000 -36000

Less: Fixed Production Overhead -99000 -99000

151000 201000

Less: Opening Inventory 0 -66500

Add: Closing Inventory 66500 0

Gross Profit 217500 134500

Less: Variable Selling Overhead -50000 -60000

Less: Fixed Selling Overhead -14000 -14000

Less: Fixed Administration Overhead -26000 -26000

Net Profit 127500 34500

Over/Under Absorption of Fixed Production Overheads:

Particulars November (£) December (£)

Actual Production Expenses 99000 99000

Standard Production Overheads 90750 108900

Over/Under Absorption 8250 -9900

M2. Application of management accounting techniques to produce appropriate financial

reporting documents

Under Marginal and Absorption Costing techniques, there is a variation in the Net profit

figures. One can observe that the Marginal Costing method generates a higher profit of £211,000

and £171,000 for November and December respectively in comparison to Absorption costing

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

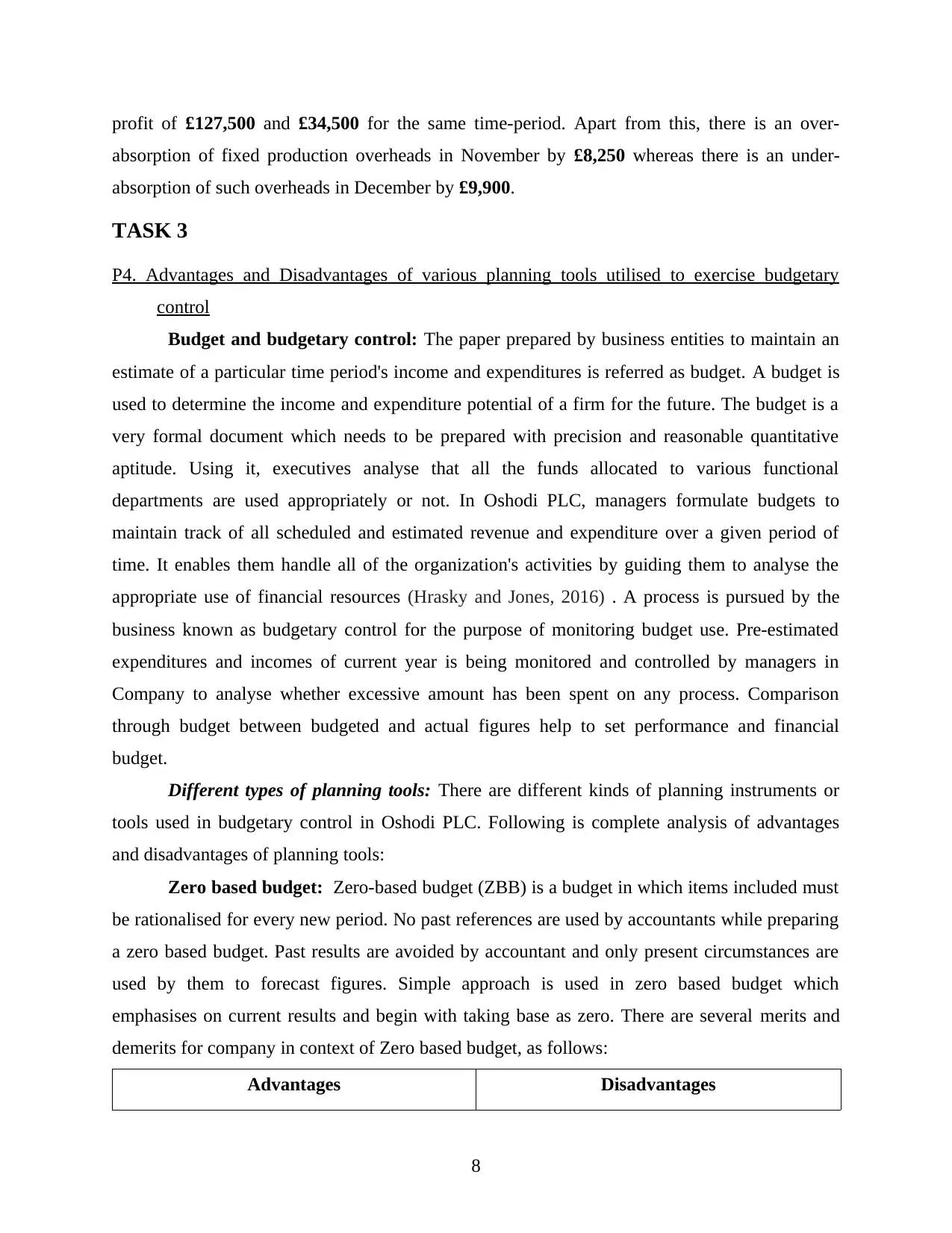

profit of £127,500 and £34,500 for the same time-period. Apart from this, there is an over-

absorption of fixed production overheads in November by £8,250 whereas there is an under-

absorption of such overheads in December by £9,900.

TASK 3

P4. Advantages and Disadvantages of various planning tools utilised to exercise budgetary

control

Budget and budgetary control: The paper prepared by business entities to maintain an

estimate of a particular time period's income and expenditures is referred as budget. A budget is

used to determine the income and expenditure potential of a firm for the future. The budget is a

very formal document which needs to be prepared with precision and reasonable quantitative

aptitude. Using it, executives analyse that all the funds allocated to various functional

departments are used appropriately or not. In Oshodi PLC, managers formulate budgets to

maintain track of all scheduled and estimated revenue and expenditure over a given period of

time. It enables them handle all of the organization's activities by guiding them to analyse the

appropriate use of financial resources (Hrasky and Jones, 2016) . A process is pursued by the

business known as budgetary control for the purpose of monitoring budget use. Pre-estimated

expenditures and incomes of current year is being monitored and controlled by managers in

Company to analyse whether excessive amount has been spent on any process. Comparison

through budget between budgeted and actual figures help to set performance and financial

budget.

Different types of planning tools: There are different kinds of planning instruments or

tools used in budgetary control in Oshodi PLC. Following is complete analysis of advantages

and disadvantages of planning tools:

Zero based budget: Zero-based budget (ZBB) is a budget in which items included must

be rationalised for every new period. No past references are used by accountants while preparing

a zero based budget. Past results are avoided by accountant and only present circumstances are

used by them to forecast figures. Simple approach is used in zero based budget which

emphasises on current results and begin with taking base as zero. There are several merits and

demerits for company in context of Zero based budget, as follows:

Advantages Disadvantages

8

absorption of fixed production overheads in November by £8,250 whereas there is an under-

absorption of such overheads in December by £9,900.

TASK 3

P4. Advantages and Disadvantages of various planning tools utilised to exercise budgetary

control

Budget and budgetary control: The paper prepared by business entities to maintain an

estimate of a particular time period's income and expenditures is referred as budget. A budget is

used to determine the income and expenditure potential of a firm for the future. The budget is a

very formal document which needs to be prepared with precision and reasonable quantitative

aptitude. Using it, executives analyse that all the funds allocated to various functional

departments are used appropriately or not. In Oshodi PLC, managers formulate budgets to

maintain track of all scheduled and estimated revenue and expenditure over a given period of

time. It enables them handle all of the organization's activities by guiding them to analyse the

appropriate use of financial resources (Hrasky and Jones, 2016) . A process is pursued by the

business known as budgetary control for the purpose of monitoring budget use. Pre-estimated

expenditures and incomes of current year is being monitored and controlled by managers in

Company to analyse whether excessive amount has been spent on any process. Comparison

through budget between budgeted and actual figures help to set performance and financial

budget.

Different types of planning tools: There are different kinds of planning instruments or

tools used in budgetary control in Oshodi PLC. Following is complete analysis of advantages

and disadvantages of planning tools:

Zero based budget: Zero-based budget (ZBB) is a budget in which items included must

be rationalised for every new period. No past references are used by accountants while preparing

a zero based budget. Past results are avoided by accountant and only present circumstances are

used by them to forecast figures. Simple approach is used in zero based budget which

emphasises on current results and begin with taking base as zero. There are several merits and

demerits for company in context of Zero based budget, as follows:

Advantages Disadvantages

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Due to zero base budget approach it provides

more effectiveness in assigning monetary and

fiscal resources.

Sometimes unrealistic facts and assumption

used in zero based budgets which affects

decision-making (Hu and others, 2015) .

It is very quick task for managers to prepare

zero based budget as no previous year data is

analysed.

It doest not provide comparative analysis using

previous performance and outcomes.

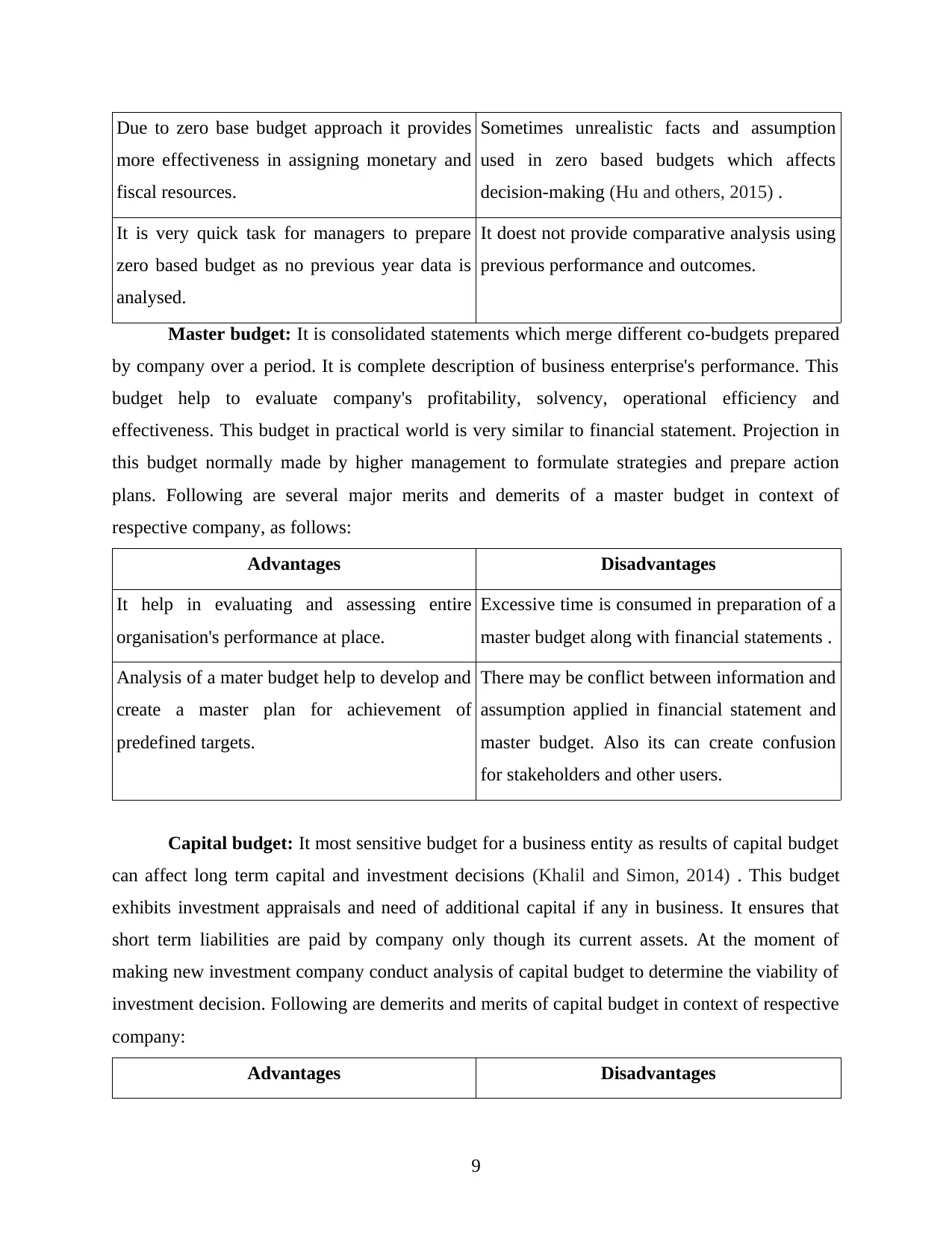

Master budget: It is consolidated statements which merge different co-budgets prepared

by company over a period. It is complete description of business enterprise's performance. This

budget help to evaluate company's profitability, solvency, operational efficiency and

effectiveness. This budget in practical world is very similar to financial statement. Projection in

this budget normally made by higher management to formulate strategies and prepare action

plans. Following are several major merits and demerits of a master budget in context of

respective company, as follows:

Advantages Disadvantages

It help in evaluating and assessing entire

organisation's performance at place.

Excessive time is consumed in preparation of a

master budget along with financial statements .

Analysis of a mater budget help to develop and

create a master plan for achievement of

predefined targets.

There may be conflict between information and

assumption applied in financial statement and

master budget. Also its can create confusion

for stakeholders and other users.

Capital budget: It most sensitive budget for a business entity as results of capital budget

can affect long term capital and investment decisions (Khalil and Simon, 2014) . This budget

exhibits investment appraisals and need of additional capital if any in business. It ensures that

short term liabilities are paid by company only though its current assets. At the moment of

making new investment company conduct analysis of capital budget to determine the viability of

investment decision. Following are demerits and merits of capital budget in context of respective

company:

Advantages Disadvantages

9

more effectiveness in assigning monetary and

fiscal resources.

Sometimes unrealistic facts and assumption

used in zero based budgets which affects

decision-making (Hu and others, 2015) .

It is very quick task for managers to prepare

zero based budget as no previous year data is

analysed.

It doest not provide comparative analysis using

previous performance and outcomes.

Master budget: It is consolidated statements which merge different co-budgets prepared

by company over a period. It is complete description of business enterprise's performance. This

budget help to evaluate company's profitability, solvency, operational efficiency and

effectiveness. This budget in practical world is very similar to financial statement. Projection in

this budget normally made by higher management to formulate strategies and prepare action

plans. Following are several major merits and demerits of a master budget in context of

respective company, as follows:

Advantages Disadvantages

It help in evaluating and assessing entire

organisation's performance at place.

Excessive time is consumed in preparation of a

master budget along with financial statements .

Analysis of a mater budget help to develop and

create a master plan for achievement of

predefined targets.

There may be conflict between information and

assumption applied in financial statement and

master budget. Also its can create confusion

for stakeholders and other users.

Capital budget: It most sensitive budget for a business entity as results of capital budget

can affect long term capital and investment decisions (Khalil and Simon, 2014) . This budget

exhibits investment appraisals and need of additional capital if any in business. It ensures that

short term liabilities are paid by company only though its current assets. At the moment of

making new investment company conduct analysis of capital budget to determine the viability of

investment decision. Following are demerits and merits of capital budget in context of respective

company:

Advantages Disadvantages

9

It provide guidance to management in selecting

effective investment or project.

Some time a wrong prediction in capital budget

can even affect the organisation's survival and

performance in long run.

It identifies risks involved in any new project

and determine the effect on capital structure.

A capital budget prepared by unskilled and less

experienced employee can provide inaccurate

and unreliable data and results.

M3. Analysing use of different planning tools and their application for developing and

forecasting budgets

Various types of planning tools provide help in preparing budget which helps in planning

and decision making. These budgets also helps in providing standards for improving and

maintaining the performance of personnels as well as entire firm. The Oshodi Plc also includes

different budgets to forecast its costs and profitability. The administration prepares zero based

budget which helps in justifying each and every increment in cost where as generation of capital

budget assists in planning for investment in revenue generating assets and liabilities. At the end,

management creates master budget which provide an overall view of key objectives and

performance of the organization (Oler and others, 2015) .

TASK 4

P5. Examining how companies adapt to management systems in the face of financial issues

In present time ever firm face different types of financial problem which become reason

of mentally stress. It is required to be address in best possible way on the basis of accounting

principle or concepts. Every organisation wants to financial stability to conduct business

activities to run business for long time. They may face financial hurdles in opponent market.

Misuse of cash and credit may occur financial problems in business. At the present moment

Osholdi Plc is facing financial challenges that effects their production level and services of the

firm. There are discussed some financial problem of company -

Poor cash management – Management of Osholdi Plc has recognised problem of the

failure system of the organization. To conduct various business operations it is important to

understand the need of money in an organisation. The firm is not capable to arrange properly the

monetary resources so its financial business activities may influenced from it. The manager of

10

effective investment or project.

Some time a wrong prediction in capital budget

can even affect the organisation's survival and

performance in long run.

It identifies risks involved in any new project

and determine the effect on capital structure.

A capital budget prepared by unskilled and less

experienced employee can provide inaccurate

and unreliable data and results.

M3. Analysing use of different planning tools and their application for developing and

forecasting budgets

Various types of planning tools provide help in preparing budget which helps in planning

and decision making. These budgets also helps in providing standards for improving and

maintaining the performance of personnels as well as entire firm. The Oshodi Plc also includes

different budgets to forecast its costs and profitability. The administration prepares zero based

budget which helps in justifying each and every increment in cost where as generation of capital

budget assists in planning for investment in revenue generating assets and liabilities. At the end,

management creates master budget which provide an overall view of key objectives and

performance of the organization (Oler and others, 2015) .

TASK 4

P5. Examining how companies adapt to management systems in the face of financial issues

In present time ever firm face different types of financial problem which become reason

of mentally stress. It is required to be address in best possible way on the basis of accounting

principle or concepts. Every organisation wants to financial stability to conduct business

activities to run business for long time. They may face financial hurdles in opponent market.

Misuse of cash and credit may occur financial problems in business. At the present moment

Osholdi Plc is facing financial challenges that effects their production level and services of the

firm. There are discussed some financial problem of company -

Poor cash management – Management of Osholdi Plc has recognised problem of the

failure system of the organization. To conduct various business operations it is important to

understand the need of money in an organisation. The firm is not capable to arrange properly the

monetary resources so its financial business activities may influenced from it. The manager of

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.