Management Accounting Report: Oshodi PLC, Costing and Reporting

VerifiedAdded on 2021/02/19

|18

|5729

|36

Report

AI Summary

This report provides a comprehensive overview of management accounting (MA) and its application within Oshodi PLC, a company specializing in JOJO fruit products. It begins by defining MA, its essential requirements, and contrasting it with financial accounting. The report then delves into various MA systems, including job costing, price optimization, inventory management, and cost accounting, detailing their advantages and disadvantages. Furthermore, it explores different methods used in MA reporting, such as budget reports, accounts receivable aging, cost managerial accounting reports, and performance reports. The report also addresses costing and income statements using marginal and absorption costing. Overall, the report provides a detailed analysis of MA tools, methods, and their application in addressing financial issues within an organization, offering valuable insights for decision-making and strategic planning.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION

Management accounting (MA) is application of different skills and knowledge in a way for

preparing accounting data which assist management to formulate policies, and to plan and in

controlling of operations. In other words profession of management accounting involves part in

planning, decision making, performance management, providing financial reports and controls

for assisting management in formulating and implementing of cost budgets and strategies.

(Kaplan and Atkinson, 2015). It facilitates management pertaining to various aspects namely

strategic, performance and risk factors. In contrast, with the financial accounting, MA is

concerned about providing the relevant data and report to internal users like entrepreneurs and

managers. This report is based on Oshodi PLC which is specialised in JOJO fruit across all age

brackets. This report will include MA and its necessary requirement of various accounting

systems. The report also highlights various methods that are used in MA reporting. It will also

develop understanding about costing system that can be used for preparing profitability statement

namely marginal and absorption. It also entails benefits and disadvantages associated with

different tools of planning which could be used for budgeting control. Further, reports provides

deeper insight about how organisations can use MA systems for responding to financial issues.

LO 1

P1 Explaining management accounting and its essential requirement within organizational

context.

Management accounting: - The tool is used in business to analyse business and its

activities. MA is “ Application of different skills and knowledge in way to prepare accounting

information that enables management in formulating policies and to plan & control the

operations of organisations” (Otley, 2016). It also includes methods and concept that are

essential for efficient planning to choose the best alternative among the available alternatives in

business for acting and controlling by evaluating and interpreting data. MA helps in planning,

decision making, identifying the early signs of the problem, strategic management. It analyses

the financing and non-financing informations and conclude results through information.

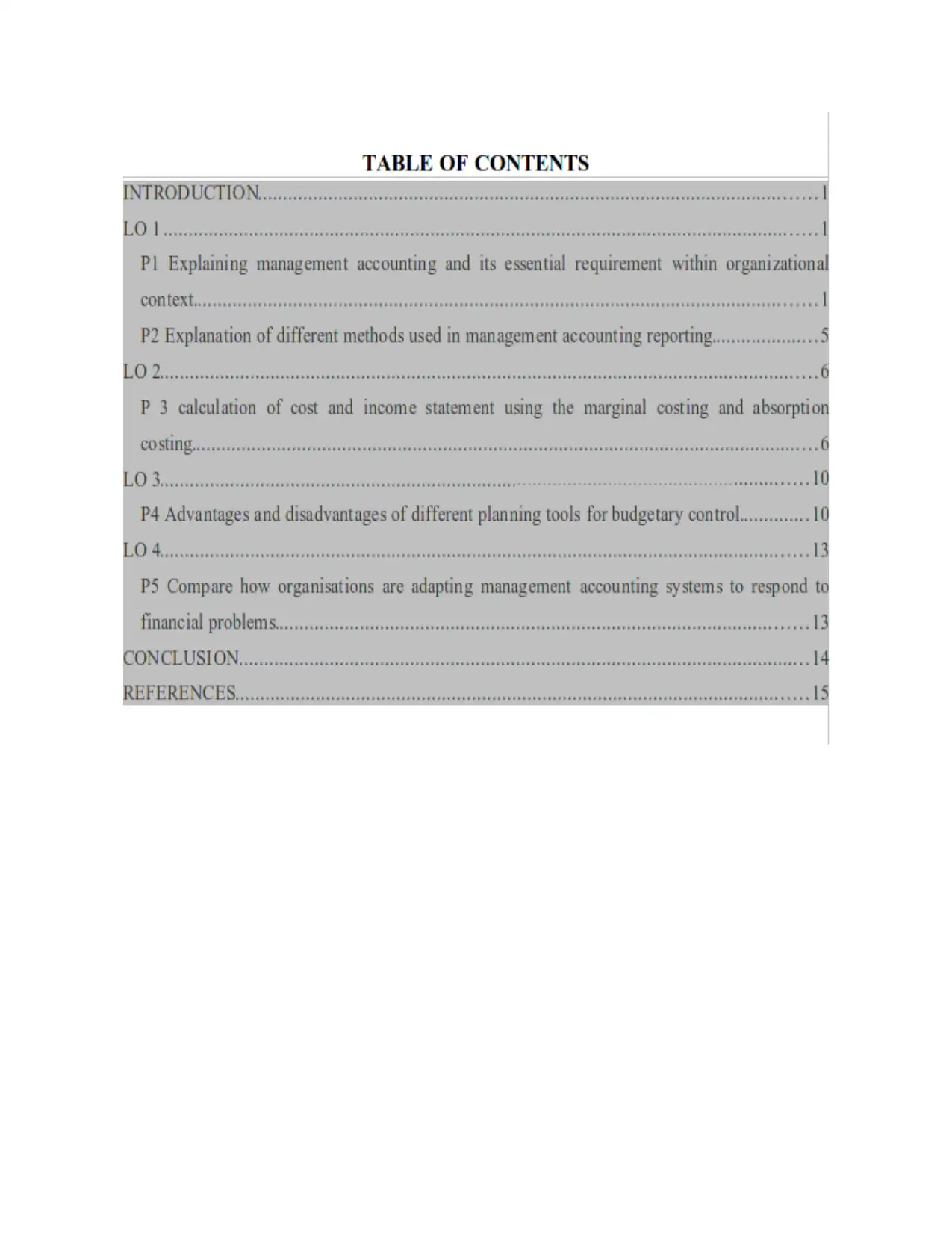

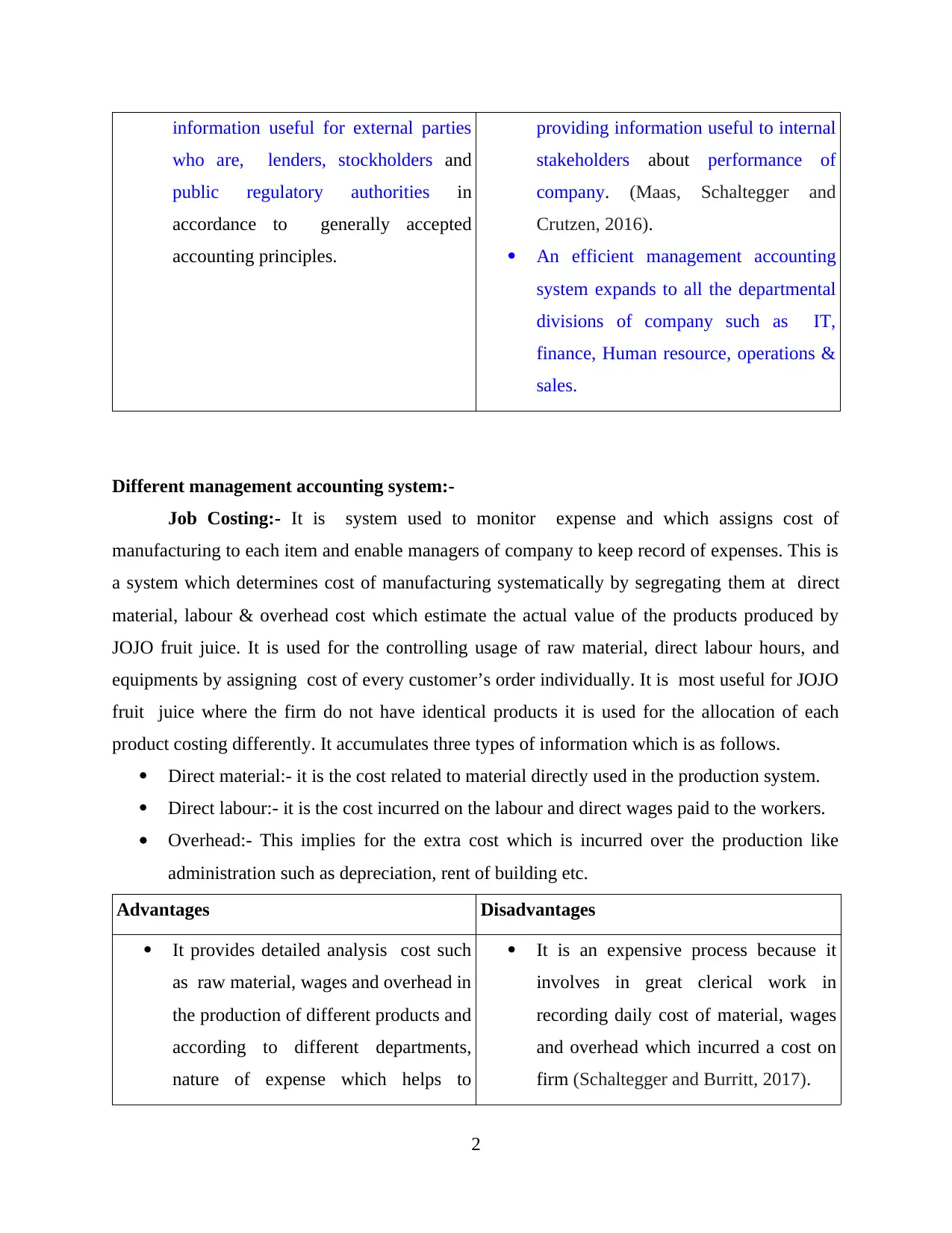

Management v/s financial accounting system

Financial Accounting Management Accounting

FA has focus on the preparation of On other side, managerial accounting is

1

Management accounting (MA) is application of different skills and knowledge in a way for

preparing accounting data which assist management to formulate policies, and to plan and in

controlling of operations. In other words profession of management accounting involves part in

planning, decision making, performance management, providing financial reports and controls

for assisting management in formulating and implementing of cost budgets and strategies.

(Kaplan and Atkinson, 2015). It facilitates management pertaining to various aspects namely

strategic, performance and risk factors. In contrast, with the financial accounting, MA is

concerned about providing the relevant data and report to internal users like entrepreneurs and

managers. This report is based on Oshodi PLC which is specialised in JOJO fruit across all age

brackets. This report will include MA and its necessary requirement of various accounting

systems. The report also highlights various methods that are used in MA reporting. It will also

develop understanding about costing system that can be used for preparing profitability statement

namely marginal and absorption. It also entails benefits and disadvantages associated with

different tools of planning which could be used for budgeting control. Further, reports provides

deeper insight about how organisations can use MA systems for responding to financial issues.

LO 1

P1 Explaining management accounting and its essential requirement within organizational

context.

Management accounting: - The tool is used in business to analyse business and its

activities. MA is “ Application of different skills and knowledge in way to prepare accounting

information that enables management in formulating policies and to plan & control the

operations of organisations” (Otley, 2016). It also includes methods and concept that are

essential for efficient planning to choose the best alternative among the available alternatives in

business for acting and controlling by evaluating and interpreting data. MA helps in planning,

decision making, identifying the early signs of the problem, strategic management. It analyses

the financing and non-financing informations and conclude results through information.

Management v/s financial accounting system

Financial Accounting Management Accounting

FA has focus on the preparation of On other side, managerial accounting is

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

information useful for external parties

who are, lenders, stockholders and

public regulatory authorities in

accordance to generally accepted

accounting principles.

providing information useful to internal

stakeholders about performance of

company. (Maas, Schaltegger and

Crutzen, 2016).

An efficient management accounting

system expands to all the departmental

divisions of company such as IT,

finance, Human resource, operations &

sales.

Different management accounting system:-

Job Costing:- It is system used to monitor expense and which assigns cost of

manufacturing to each item and enable managers of company to keep record of expenses. This is

a system which determines cost of manufacturing systematically by segregating them at direct

material, labour & overhead cost which estimate the actual value of the products produced by

JOJO fruit juice. It is used for the controlling usage of raw material, direct labour hours, and

equipments by assigning cost of every customer’s order individually. It is most useful for JOJO

fruit juice where the firm do not have identical products it is used for the allocation of each

product costing differently. It accumulates three types of information which is as follows.

Direct material:- it is the cost related to material directly used in the production system.

Direct labour:- it is the cost incurred on the labour and direct wages paid to the workers.

Overhead:- This implies for the extra cost which is incurred over the production like

administration such as depreciation, rent of building etc.

Advantages Disadvantages

It provides detailed analysis cost such

as raw material, wages and overhead in

the production of different products and

according to different departments,

nature of expense which helps to

It is an expensive process because it

involves in great clerical work in

recording daily cost of material, wages

and overhead which incurred a cost on

firm (Schaltegger and Burritt, 2017).

2

who are, lenders, stockholders and

public regulatory authorities in

accordance to generally accepted

accounting principles.

providing information useful to internal

stakeholders about performance of

company. (Maas, Schaltegger and

Crutzen, 2016).

An efficient management accounting

system expands to all the departmental

divisions of company such as IT,

finance, Human resource, operations &

sales.

Different management accounting system:-

Job Costing:- It is system used to monitor expense and which assigns cost of

manufacturing to each item and enable managers of company to keep record of expenses. This is

a system which determines cost of manufacturing systematically by segregating them at direct

material, labour & overhead cost which estimate the actual value of the products produced by

JOJO fruit juice. It is used for the controlling usage of raw material, direct labour hours, and

equipments by assigning cost of every customer’s order individually. It is most useful for JOJO

fruit juice where the firm do not have identical products it is used for the allocation of each

product costing differently. It accumulates three types of information which is as follows.

Direct material:- it is the cost related to material directly used in the production system.

Direct labour:- it is the cost incurred on the labour and direct wages paid to the workers.

Overhead:- This implies for the extra cost which is incurred over the production like

administration such as depreciation, rent of building etc.

Advantages Disadvantages

It provides detailed analysis cost such

as raw material, wages and overhead in

the production of different products and

according to different departments,

nature of expense which helps to

It is an expensive process because it

involves in great clerical work in

recording daily cost of material, wages

and overhead which incurred a cost on

firm (Schaltegger and Burritt, 2017).

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

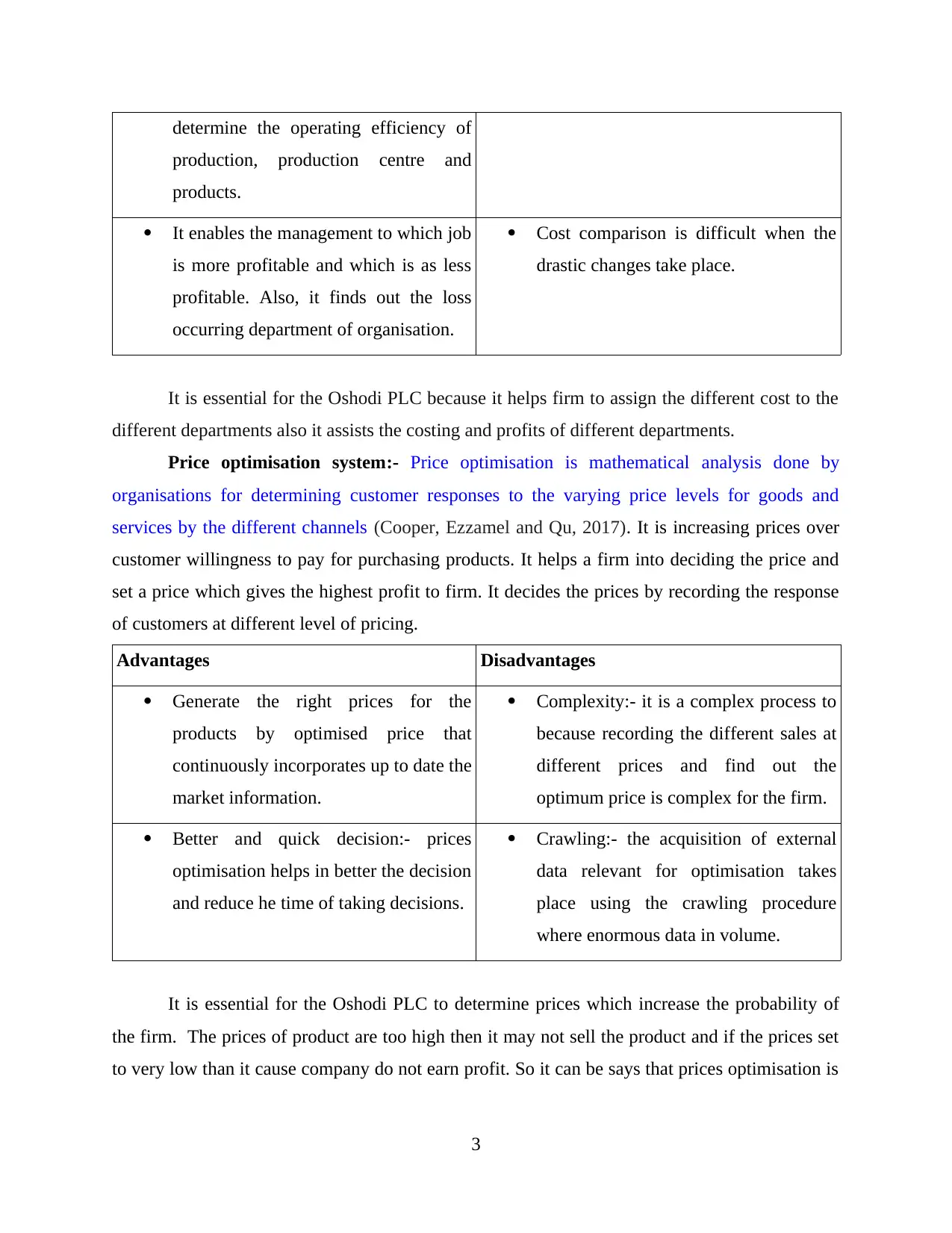

determine the operating efficiency of

production, production centre and

products.

It enables the management to which job

is more profitable and which is as less

profitable. Also, it finds out the loss

occurring department of organisation.

Cost comparison is difficult when the

drastic changes take place.

It is essential for the Oshodi PLC because it helps firm to assign the different cost to the

different departments also it assists the costing and profits of different departments.

Price optimisation system:- Price optimisation is mathematical analysis done by

organisations for determining customer responses to the varying price levels for goods and

services by the different channels (Cooper, Ezzamel and Qu, 2017). It is increasing prices over

customer willingness to pay for purchasing products. It helps a firm into deciding the price and

set a price which gives the highest profit to firm. It decides the prices by recording the response

of customers at different level of pricing.

Advantages Disadvantages

Generate the right prices for the

products by optimised price that

continuously incorporates up to date the

market information.

Complexity:- it is a complex process to

because recording the different sales at

different prices and find out the

optimum price is complex for the firm.

Better and quick decision:- prices

optimisation helps in better the decision

and reduce he time of taking decisions.

Crawling:- the acquisition of external

data relevant for optimisation takes

place using the crawling procedure

where enormous data in volume.

It is essential for the Oshodi PLC to determine prices which increase the probability of

the firm. The prices of product are too high then it may not sell the product and if the prices set

to very low than it cause company do not earn profit. So it can be says that prices optimisation is

3

production, production centre and

products.

It enables the management to which job

is more profitable and which is as less

profitable. Also, it finds out the loss

occurring department of organisation.

Cost comparison is difficult when the

drastic changes take place.

It is essential for the Oshodi PLC because it helps firm to assign the different cost to the

different departments also it assists the costing and profits of different departments.

Price optimisation system:- Price optimisation is mathematical analysis done by

organisations for determining customer responses to the varying price levels for goods and

services by the different channels (Cooper, Ezzamel and Qu, 2017). It is increasing prices over

customer willingness to pay for purchasing products. It helps a firm into deciding the price and

set a price which gives the highest profit to firm. It decides the prices by recording the response

of customers at different level of pricing.

Advantages Disadvantages

Generate the right prices for the

products by optimised price that

continuously incorporates up to date the

market information.

Complexity:- it is a complex process to

because recording the different sales at

different prices and find out the

optimum price is complex for the firm.

Better and quick decision:- prices

optimisation helps in better the decision

and reduce he time of taking decisions.

Crawling:- the acquisition of external

data relevant for optimisation takes

place using the crawling procedure

where enormous data in volume.

It is essential for the Oshodi PLC to determine prices which increase the probability of

the firm. The prices of product are too high then it may not sell the product and if the prices set

to very low than it cause company do not earn profit. So it can be says that prices optimisation is

3

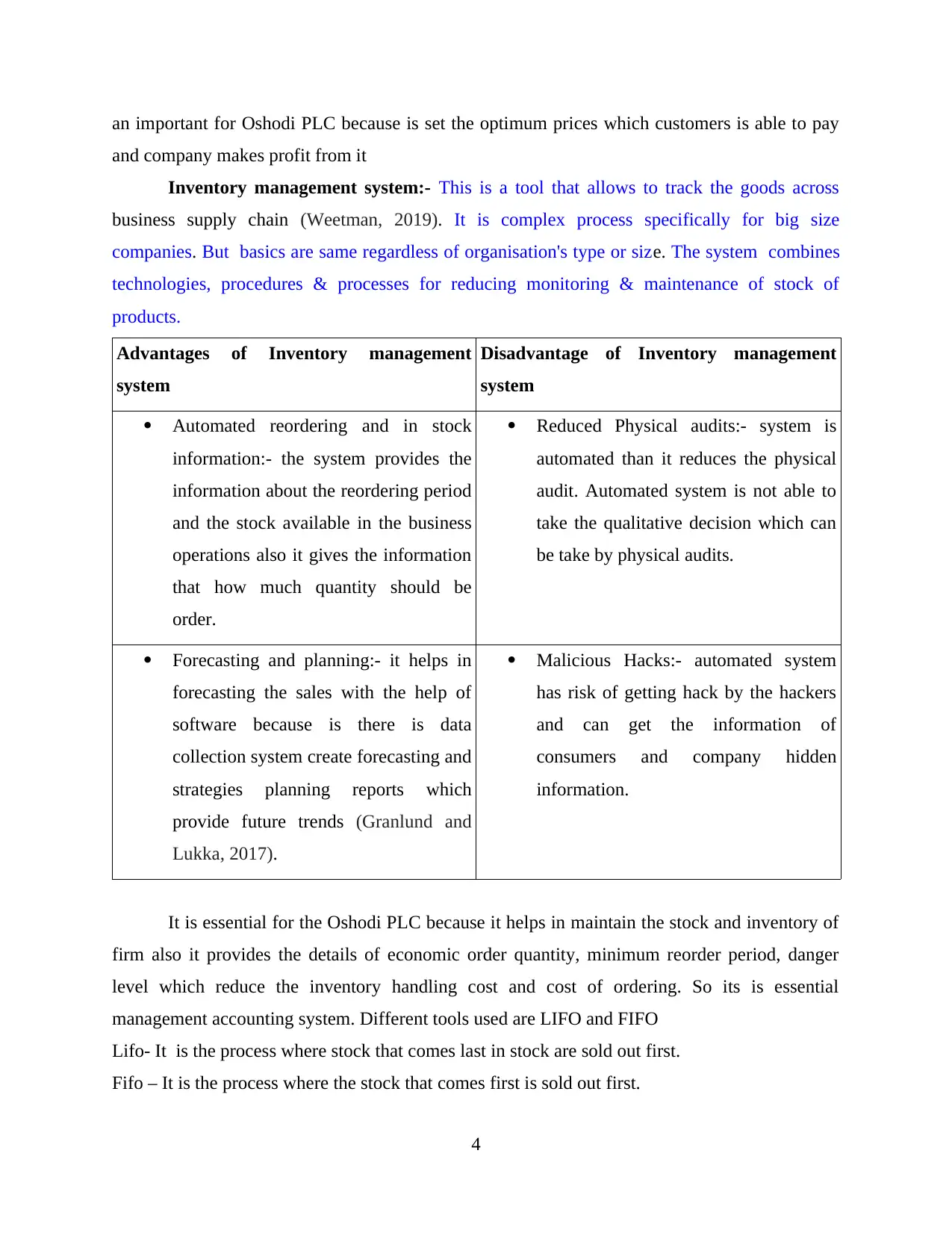

an important for Oshodi PLC because is set the optimum prices which customers is able to pay

and company makes profit from it

Inventory management system:- This is a tool that allows to track the goods across

business supply chain (Weetman, 2019). It is complex process specifically for big size

companies. But basics are same regardless of organisation's type or size. The system combines

technologies, procedures & processes for reducing monitoring & maintenance of stock of

products.

Advantages of Inventory management

system

Disadvantage of Inventory management

system

Automated reordering and in stock

information:- the system provides the

information about the reordering period

and the stock available in the business

operations also it gives the information

that how much quantity should be

order.

Reduced Physical audits:- system is

automated than it reduces the physical

audit. Automated system is not able to

take the qualitative decision which can

be take by physical audits.

Forecasting and planning:- it helps in

forecasting the sales with the help of

software because is there is data

collection system create forecasting and

strategies planning reports which

provide future trends (Granlund and

Lukka, 2017).

Malicious Hacks:- automated system

has risk of getting hack by the hackers

and can get the information of

consumers and company hidden

information.

It is essential for the Oshodi PLC because it helps in maintain the stock and inventory of

firm also it provides the details of economic order quantity, minimum reorder period, danger

level which reduce the inventory handling cost and cost of ordering. So its is essential

management accounting system. Different tools used are LIFO and FIFO

Lifo- It is the process where stock that comes last in stock are sold out first.

Fifo – It is the process where the stock that comes first is sold out first.

4

and company makes profit from it

Inventory management system:- This is a tool that allows to track the goods across

business supply chain (Weetman, 2019). It is complex process specifically for big size

companies. But basics are same regardless of organisation's type or size. The system combines

technologies, procedures & processes for reducing monitoring & maintenance of stock of

products.

Advantages of Inventory management

system

Disadvantage of Inventory management

system

Automated reordering and in stock

information:- the system provides the

information about the reordering period

and the stock available in the business

operations also it gives the information

that how much quantity should be

order.

Reduced Physical audits:- system is

automated than it reduces the physical

audit. Automated system is not able to

take the qualitative decision which can

be take by physical audits.

Forecasting and planning:- it helps in

forecasting the sales with the help of

software because is there is data

collection system create forecasting and

strategies planning reports which

provide future trends (Granlund and

Lukka, 2017).

Malicious Hacks:- automated system

has risk of getting hack by the hackers

and can get the information of

consumers and company hidden

information.

It is essential for the Oshodi PLC because it helps in maintain the stock and inventory of

firm also it provides the details of economic order quantity, minimum reorder period, danger

level which reduce the inventory handling cost and cost of ordering. So its is essential

management accounting system. Different tools used are LIFO and FIFO

Lifo- It is the process where stock that comes last in stock are sold out first.

Fifo – It is the process where the stock that comes first is sold out first.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

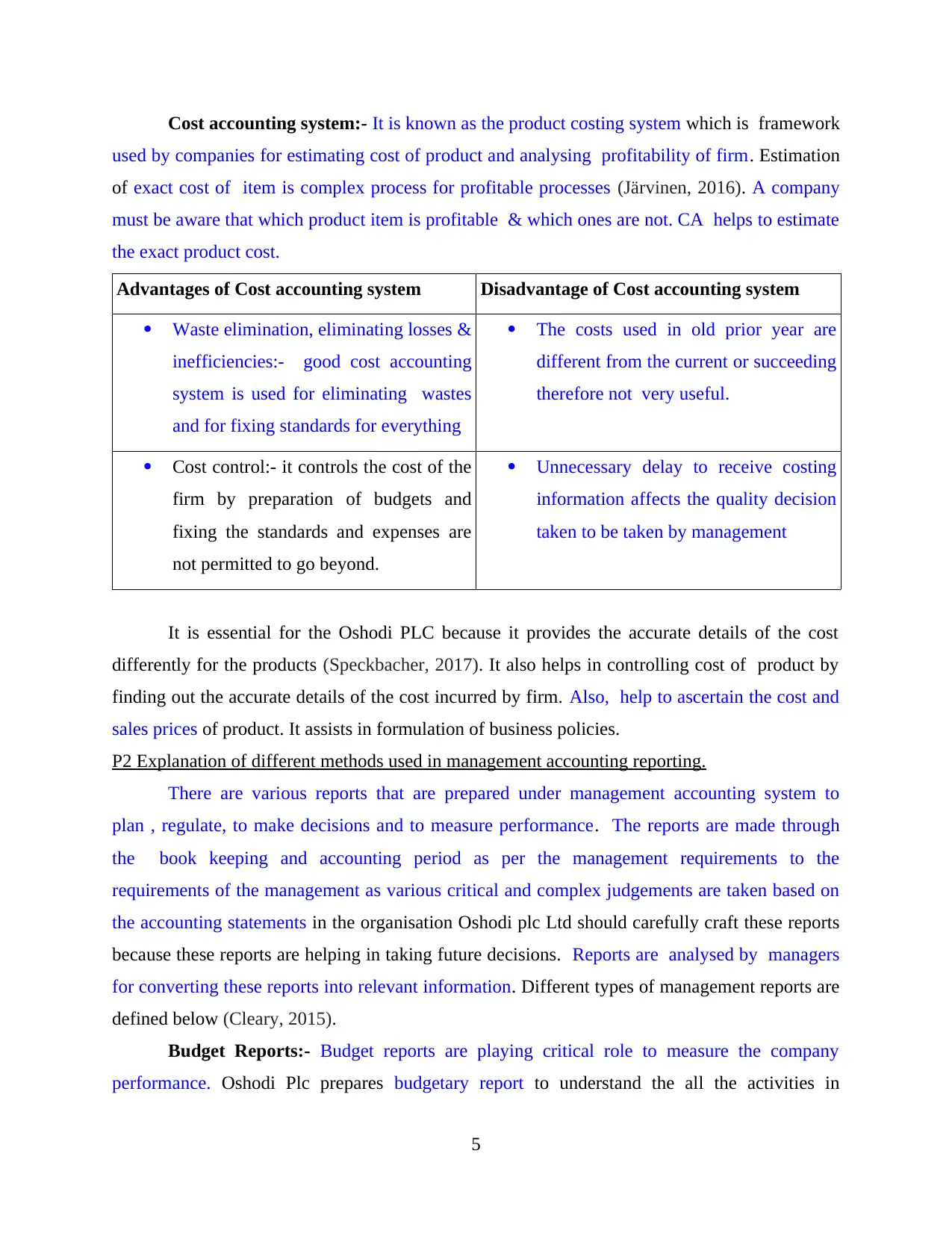

Cost accounting system:- It is known as the product costing system which is framework

used by companies for estimating cost of product and analysing profitability of firm. Estimation

of exact cost of item is complex process for profitable processes (Järvinen, 2016). A company

must be aware that which product item is profitable & which ones are not. CA helps to estimate

the exact product cost.

Advantages of Cost accounting system Disadvantage of Cost accounting system

Waste elimination, eliminating losses &

inefficiencies:- good cost accounting

system is used for eliminating wastes

and for fixing standards for everything

The costs used in old prior year are

different from the current or succeeding

therefore not very useful.

Cost control:- it controls the cost of the

firm by preparation of budgets and

fixing the standards and expenses are

not permitted to go beyond.

Unnecessary delay to receive costing

information affects the quality decision

taken to be taken by management

It is essential for the Oshodi PLC because it provides the accurate details of the cost

differently for the products (Speckbacher, 2017). It also helps in controlling cost of product by

finding out the accurate details of the cost incurred by firm. Also, help to ascertain the cost and

sales prices of product. It assists in formulation of business policies.

P2 Explanation of different methods used in management accounting reporting.

There are various reports that are prepared under management accounting system to

plan , regulate, to make decisions and to measure performance. The reports are made through

the book keeping and accounting period as per the management requirements to the

requirements of the management as various critical and complex judgements are taken based on

the accounting statements in the organisation Oshodi plc Ltd should carefully craft these reports

because these reports are helping in taking future decisions. Reports are analysed by managers

for converting these reports into relevant information. Different types of management reports are

defined below (Cleary, 2015).

Budget Reports:- Budget reports are playing critical role to measure the company

performance. Oshodi Plc prepares budgetary report to understand the all the activities in

5

used by companies for estimating cost of product and analysing profitability of firm. Estimation

of exact cost of item is complex process for profitable processes (Järvinen, 2016). A company

must be aware that which product item is profitable & which ones are not. CA helps to estimate

the exact product cost.

Advantages of Cost accounting system Disadvantage of Cost accounting system

Waste elimination, eliminating losses &

inefficiencies:- good cost accounting

system is used for eliminating wastes

and for fixing standards for everything

The costs used in old prior year are

different from the current or succeeding

therefore not very useful.

Cost control:- it controls the cost of the

firm by preparation of budgets and

fixing the standards and expenses are

not permitted to go beyond.

Unnecessary delay to receive costing

information affects the quality decision

taken to be taken by management

It is essential for the Oshodi PLC because it provides the accurate details of the cost

differently for the products (Speckbacher, 2017). It also helps in controlling cost of product by

finding out the accurate details of the cost incurred by firm. Also, help to ascertain the cost and

sales prices of product. It assists in formulation of business policies.

P2 Explanation of different methods used in management accounting reporting.

There are various reports that are prepared under management accounting system to

plan , regulate, to make decisions and to measure performance. The reports are made through

the book keeping and accounting period as per the management requirements to the

requirements of the management as various critical and complex judgements are taken based on

the accounting statements in the organisation Oshodi plc Ltd should carefully craft these reports

because these reports are helping in taking future decisions. Reports are analysed by managers

for converting these reports into relevant information. Different types of management reports are

defined below (Cleary, 2015).

Budget Reports:- Budget reports are playing critical role to measure the company

performance. Oshodi Plc prepares budgetary report to understand the all the activities in

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

organisation. It assists the business owner or managers to define and control the cost. Managers

also create this reports for the employees' performance and provide incentives. The budget is

decided on the basis of previous year actual expenses and sales. It is important as it helps

company to analyse an d costs and overspendings.

Accounts Receivable Aging:- The report is used for enlisting the unpaid consumer

invoices and credit memos which are not used by dates. The report help the managers to

determine the unpaid overdue invoices so that collection can be made. Management uses this

report for determining level of effectiveness in credit collection functions.. A manager of Oshodi

uses aging report for finding out issues faced by company in collection processes. If significant

number of consumers are not able to repay the balance than managers can tight the credit policy.

It helps to determine the defaulters and not payers.

Cost managerial accounting report:- Work of managerial accounting is to compute the

cost of outputs which are produced by Oshodi. All the cost such as cost of raw material,

overhead cost, labour cost are deliberated by management. Division of total cost by total no.

products are produces which gives the per unit costing of the products. Cost report are offering

the summary information of every cost occurred for producing the product. These reports helps

the managers of Oshodi PLC to cost prices and sale price of output. It helps managers in

estimating profit margins of organisations.

Performance Reports:- This report is generated for reviewing the company performance

and its different departments also the employees working in organisation. Managers of Oshodi

PLC use these reports for framing the key strategic decisions related to future trends in

organisation. Employees are often awarded for their contribution in firm which is also analysed

by the performance report.

LO 2

P 3 Calculation of Cost and Income Statement using the Marginal Costing and Absorption

Costing.

Costing can be referred as system which is used for assigning costs to different elements

of business. It used for developing costs for various users and producers. There are different

techniques used in management accounting.

Different techniques of cost calculations

i ) Marginal Costing

6

also create this reports for the employees' performance and provide incentives. The budget is

decided on the basis of previous year actual expenses and sales. It is important as it helps

company to analyse an d costs and overspendings.

Accounts Receivable Aging:- The report is used for enlisting the unpaid consumer

invoices and credit memos which are not used by dates. The report help the managers to

determine the unpaid overdue invoices so that collection can be made. Management uses this

report for determining level of effectiveness in credit collection functions.. A manager of Oshodi

uses aging report for finding out issues faced by company in collection processes. If significant

number of consumers are not able to repay the balance than managers can tight the credit policy.

It helps to determine the defaulters and not payers.

Cost managerial accounting report:- Work of managerial accounting is to compute the

cost of outputs which are produced by Oshodi. All the cost such as cost of raw material,

overhead cost, labour cost are deliberated by management. Division of total cost by total no.

products are produces which gives the per unit costing of the products. Cost report are offering

the summary information of every cost occurred for producing the product. These reports helps

the managers of Oshodi PLC to cost prices and sale price of output. It helps managers in

estimating profit margins of organisations.

Performance Reports:- This report is generated for reviewing the company performance

and its different departments also the employees working in organisation. Managers of Oshodi

PLC use these reports for framing the key strategic decisions related to future trends in

organisation. Employees are often awarded for their contribution in firm which is also analysed

by the performance report.

LO 2

P 3 Calculation of Cost and Income Statement using the Marginal Costing and Absorption

Costing.

Costing can be referred as system which is used for assigning costs to different elements

of business. It used for developing costs for various users and producers. There are different

techniques used in management accounting.

Different techniques of cost calculations

i ) Marginal Costing

6

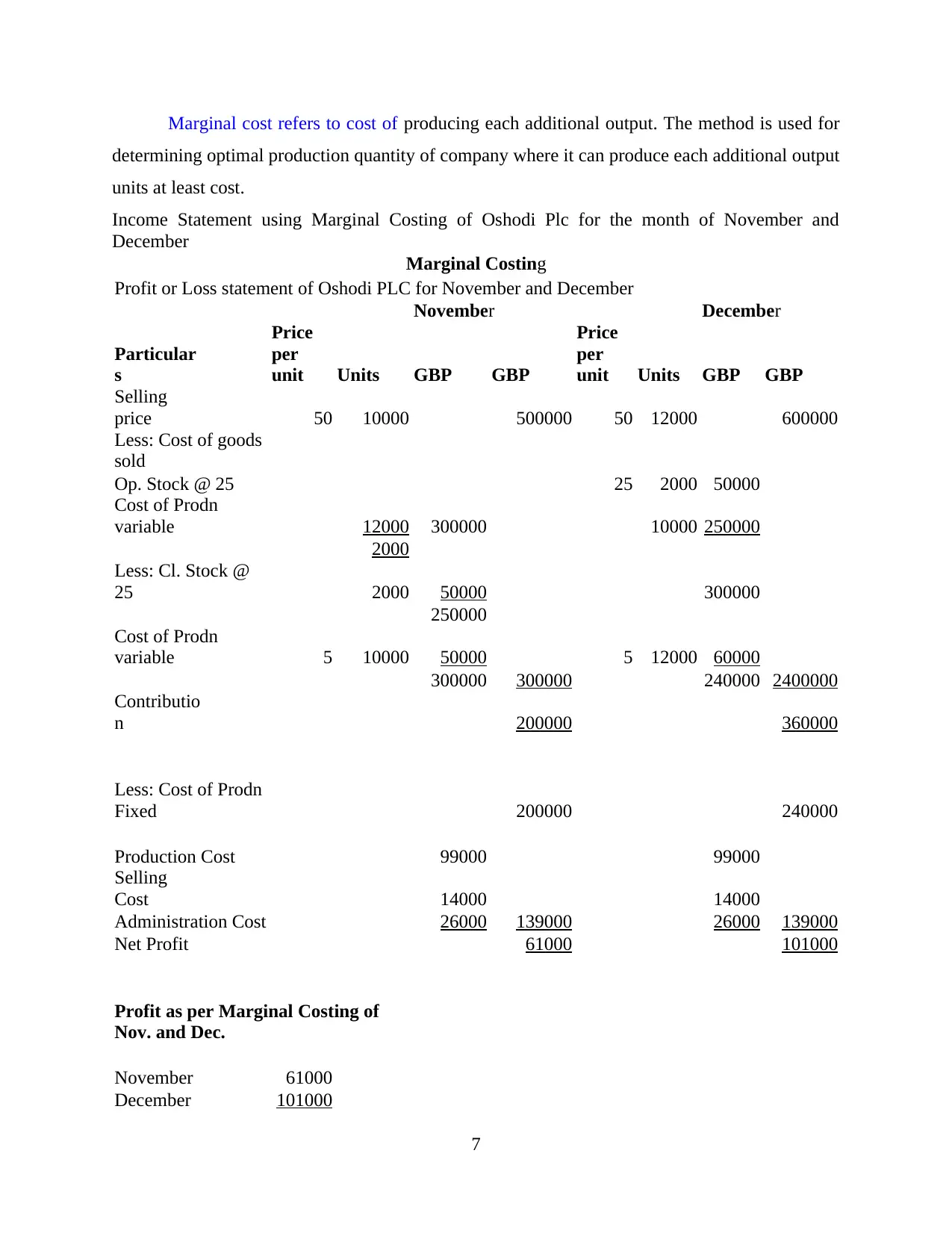

Marginal cost refers to cost of producing each additional output. The method is used for

determining optimal production quantity of company where it can produce each additional output

units at least cost.

Income Statement using Marginal Costing of Oshodi Plc for the month of November and

December

Marginal Costing

Profit or Loss statement of Oshodi PLC for November and December

November December

Particular

s

Price

per

unit Units GBP GBP

Price

per

unit Units GBP GBP

Selling

price 50 10000 500000 50 12000 600000

Less: Cost of goods

sold

Op. Stock @ 25 25 2000 50000

Cost of Prodn

variable 12000 300000 10000 250000

2000

Less: Cl. Stock @

25 2000 50000 300000

250000

Cost of Prodn

variable 5 10000 50000 5 12000 60000

300000 300000 240000 2400000

Contributio

n 200000 360000

Less: Cost of Prodn

Fixed 200000 240000

Production Cost 99000 99000

Selling

Cost 14000 14000

Administration Cost 26000 139000 26000 139000

Net Profit 61000 101000

Profit as per Marginal Costing of

Nov. and Dec.

November 61000

December 101000

7

determining optimal production quantity of company where it can produce each additional output

units at least cost.

Income Statement using Marginal Costing of Oshodi Plc for the month of November and

December

Marginal Costing

Profit or Loss statement of Oshodi PLC for November and December

November December

Particular

s

Price

per

unit Units GBP GBP

Price

per

unit Units GBP GBP

Selling

price 50 10000 500000 50 12000 600000

Less: Cost of goods

sold

Op. Stock @ 25 25 2000 50000

Cost of Prodn

variable 12000 300000 10000 250000

2000

Less: Cl. Stock @

25 2000 50000 300000

250000

Cost of Prodn

variable 5 10000 50000 5 12000 60000

300000 300000 240000 2400000

Contributio

n 200000 360000

Less: Cost of Prodn

Fixed 200000 240000

Production Cost 99000 99000

Selling

Cost 14000 14000

Administration Cost 26000 139000 26000 139000

Net Profit 61000 101000

Profit as per Marginal Costing of

Nov. and Dec.

November 61000

December 101000

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

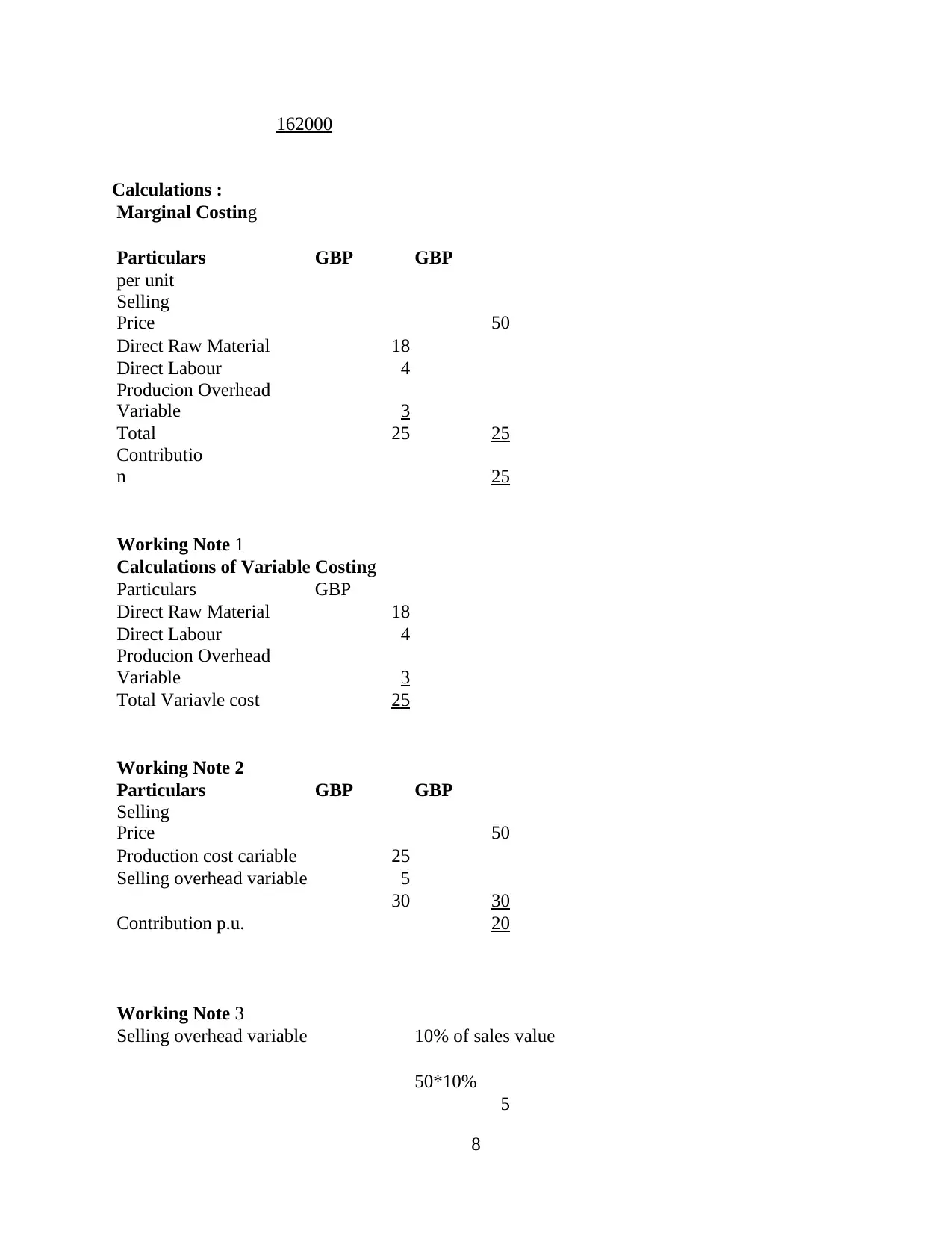

162000

Calculations :

Marginal Costing

Particulars GBP GBP

per unit

Selling

Price 50

Direct Raw Material 18

Direct Labour 4

Producion Overhead

Variable 3

Total 25 25

Contributio

n 25

Working Note 1

Calculations of Variable Costing

Particulars GBP

Direct Raw Material 18

Direct Labour 4

Producion Overhead

Variable 3

Total Variavle cost 25

Working Note 2

Particulars GBP GBP

Selling

Price 50

Production cost cariable 25

Selling overhead variable 5

30 30

Contribution p.u. 20

Working Note 3

Selling overhead variable 10% of sales value

50*10%

5

8

Calculations :

Marginal Costing

Particulars GBP GBP

per unit

Selling

Price 50

Direct Raw Material 18

Direct Labour 4

Producion Overhead

Variable 3

Total 25 25

Contributio

n 25

Working Note 1

Calculations of Variable Costing

Particulars GBP

Direct Raw Material 18

Direct Labour 4

Producion Overhead

Variable 3

Total Variavle cost 25

Working Note 2

Particulars GBP GBP

Selling

Price 50

Production cost cariable 25

Selling overhead variable 5

30 30

Contribution p.u. 20

Working Note 3

Selling overhead variable 10% of sales value

50*10%

5

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

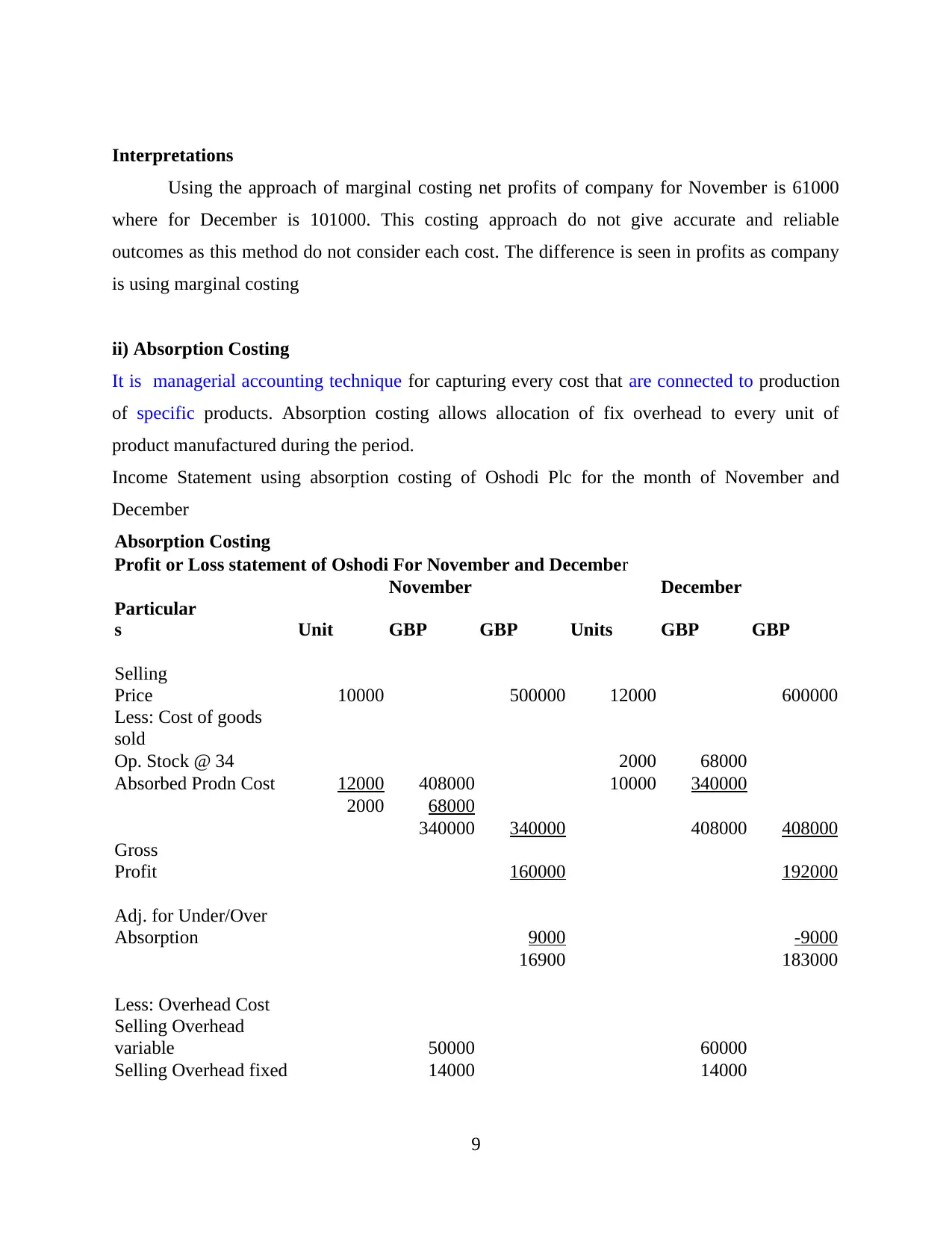

Interpretations

Using the approach of marginal costing net profits of company for November is 61000

where for December is 101000. This costing approach do not give accurate and reliable

outcomes as this method do not consider each cost. The difference is seen in profits as company

is using marginal costing

ii) Absorption Costing

It is managerial accounting technique for capturing every cost that are connected to production

of specific products. Absorption costing allows allocation of fix overhead to every unit of

product manufactured during the period.

Income Statement using absorption costing of Oshodi Plc for the month of November and

December

Absorption Costing

Profit or Loss statement of Oshodi For November and December

November December

Particular

s Unit GBP GBP Units GBP GBP

Selling

Price 10000 500000 12000 600000

Less: Cost of goods

sold

Op. Stock @ 34 2000 68000

Absorbed Prodn Cost 12000 408000 10000 340000

2000 68000

340000 340000 408000 408000

Gross

Profit 160000 192000

Adj. for Under/Over

Absorption 9000 -9000

16900 183000

Less: Overhead Cost

Selling Overhead

variable 50000 60000

Selling Overhead fixed 14000 14000

9

Using the approach of marginal costing net profits of company for November is 61000

where for December is 101000. This costing approach do not give accurate and reliable

outcomes as this method do not consider each cost. The difference is seen in profits as company

is using marginal costing

ii) Absorption Costing

It is managerial accounting technique for capturing every cost that are connected to production

of specific products. Absorption costing allows allocation of fix overhead to every unit of

product manufactured during the period.

Income Statement using absorption costing of Oshodi Plc for the month of November and

December

Absorption Costing

Profit or Loss statement of Oshodi For November and December

November December

Particular

s Unit GBP GBP Units GBP GBP

Selling

Price 10000 500000 12000 600000

Less: Cost of goods

sold

Op. Stock @ 34 2000 68000

Absorbed Prodn Cost 12000 408000 10000 340000

2000 68000

340000 340000 408000 408000

Gross

Profit 160000 192000

Adj. for Under/Over

Absorption 9000 -9000

16900 183000

Less: Overhead Cost

Selling Overhead

variable 50000 60000

Selling Overhead fixed 14000 14000

9

Admin overhead Fixed 26000 90000 26000 100000

Net profits 79000 83000

Calculation for Under/ Over Absorption for Oshodi PLC for November and

December

Month

Units of

Prodn.

O/H

absorbed

p.u.

Total

Absorptio

n

Actual

O/H

Under/ Over

Absorption

November 12000 9 108000 99000 9000

December 10000 9 90000 99000 -9000

Calculations

Working Note 1

Normal Production

Level 11000 units

Overhead cost Fixed 99000

Fixed O/H absorbed

99000/1100

0

GBP 9

Total

Prodn

Cost Variable Cost + Fixed O/H absorbed

Variable Cost 25

Fixed O/H absorbed 9

Total Prodn Cost 34 per unit

Interpretations

From the study of above it is identified that profit of company as per absorption costing

is 79000 for November and 83000 for the December which shows that results are more accurate

in comparison with marginal costing. Therefore, company has been suggested for adoption of

absorption costing for the company as it gives more accurate results on constant basis.

10

Net profits 79000 83000

Calculation for Under/ Over Absorption for Oshodi PLC for November and

December

Month

Units of

Prodn.

O/H

absorbed

p.u.

Total

Absorptio

n

Actual

O/H

Under/ Over

Absorption

November 12000 9 108000 99000 9000

December 10000 9 90000 99000 -9000

Calculations

Working Note 1

Normal Production

Level 11000 units

Overhead cost Fixed 99000

Fixed O/H absorbed

99000/1100

0

GBP 9

Total

Prodn

Cost Variable Cost + Fixed O/H absorbed

Variable Cost 25

Fixed O/H absorbed 9

Total Prodn Cost 34 per unit

Interpretations

From the study of above it is identified that profit of company as per absorption costing

is 79000 for November and 83000 for the December which shows that results are more accurate

in comparison with marginal costing. Therefore, company has been suggested for adoption of

absorption costing for the company as it gives more accurate results on constant basis.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.