Management Accounting: Methods, Benefits, and Integration Analysis

VerifiedAdded on 2023/01/12

|17

|4333

|22

Report

AI Summary

This report provides a comprehensive overview of management accounting, detailing its role in managerial decision-making and its distinction from financial accounting. Section 1 explains management accounting, its essential systems, and reporting methods, including inventory management, job costing, price optimization, and cost accounting systems. It evaluates the benefits of these systems and their integration. Section 2 compares absorption and marginal costing, presenting cost cards and interpretations. Section 3 and 4 delve into further aspects of management accounting, including the evaluation of the benefits of MA systems and their application. The report emphasizes how management accounting contributes to organizational goal achievement and enhances efficiency. The report also highlights the role of different MA systems in the smooth functioning of an organization.

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION...........................................................................................................................4

SECTION 1.....................................................................................................................................4

1.1 Explaining management accounting with essential requirements of its several systems......4

1.2 Explaining different methods that are used for reporting under management accounting....5

1.3 Evaluating benefits of the MA systems and its application...................................................6

1.4 Critically evaluating integrating between systems and reporting under management

accounting....................................................................................................................................8

SECTION 2.....................................................................................................................................8

2.1................................................................................................................................................8

2.2..............................................................................................................................................10

2.3..............................................................................................................................................10

SECTION3....................................................................................................................................12

3.1..............................................................................................................................................12

SECTION 4...................................................................................................................................13

4.1..............................................................................................................................................13

4.2..............................................................................................................................................14

4.3..............................................................................................................................................15

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

SECTION 1.....................................................................................................................................4

1.1 Explaining management accounting with essential requirements of its several systems......4

1.2 Explaining different methods that are used for reporting under management accounting....5

1.3 Evaluating benefits of the MA systems and its application...................................................6

1.4 Critically evaluating integrating between systems and reporting under management

accounting....................................................................................................................................8

SECTION 2.....................................................................................................................................8

2.1................................................................................................................................................8

2.2..............................................................................................................................................10

2.3..............................................................................................................................................10

SECTION3....................................................................................................................................12

3.1..............................................................................................................................................12

SECTION 4...................................................................................................................................13

4.1..............................................................................................................................................13

4.2..............................................................................................................................................14

4.3..............................................................................................................................................15

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION

Management accounting is a branch of accounting that helps a business in taking

managerial decisions by optimum utilization of resources. Management accounting is only used

by the internal management of an organization which distinguishes it from financial accounting.

It is essential for every business as it not only helps in adequate decision making but also

increases the profitability of the company in long run. Furthermore, it acts as a bridge between

the finance function and other parts of business. The current study will focus on the overall

concept and advantages of management accounting and how it can contribute towards

achievement of goals and objectives of an organization effectively and efficiently.

SECTION 1

1.1 Explaining management accounting with essential requirements of its several systems

Management accounting referred as the practice that facilitates financial resources and

information for the managers in the process of decisions making. In other words, it is called as

managerial accounting or the cost accounting. It is the process of assessing the costs and the

operations of business for preparing an internal financial report, account and records that helps

the managers in achieving the business effectively and efficiently (Ghasemi and et.al., 2016). It

is an act of the costing and the financial data by translating data into meaningful information for

the officers and the management within an enterprise. MA is counted as one of the essential units

of the company as it helps in formulating financial reports internally, accounts and records for

helping the managers in an organization to make suitable decisions in order to achieve long and

short term goals of the business. There are several aspects in which MA a system plays a crucial

role that are as follows-

Determining aim- Based on the information available, MA systems helps in determining

the goals and tries in finding out route by which it could reach the business or set goals.

Helps in preparing plan- It helps in formulation of the plan in accordance to needs and

the preferences of consumers. It helps the managers in studying and assessing future and present

prospects of business.

Better customer service- MA systems assist in reducing the cost incurred in

manufacturing the product by making use of cost accounting systems. It helps in defining the

quality standards in producing the product which in turn helps in providing better services to the

customer.

Management accounting is a branch of accounting that helps a business in taking

managerial decisions by optimum utilization of resources. Management accounting is only used

by the internal management of an organization which distinguishes it from financial accounting.

It is essential for every business as it not only helps in adequate decision making but also

increases the profitability of the company in long run. Furthermore, it acts as a bridge between

the finance function and other parts of business. The current study will focus on the overall

concept and advantages of management accounting and how it can contribute towards

achievement of goals and objectives of an organization effectively and efficiently.

SECTION 1

1.1 Explaining management accounting with essential requirements of its several systems

Management accounting referred as the practice that facilitates financial resources and

information for the managers in the process of decisions making. In other words, it is called as

managerial accounting or the cost accounting. It is the process of assessing the costs and the

operations of business for preparing an internal financial report, account and records that helps

the managers in achieving the business effectively and efficiently (Ghasemi and et.al., 2016). It

is an act of the costing and the financial data by translating data into meaningful information for

the officers and the management within an enterprise. MA is counted as one of the essential units

of the company as it helps in formulating financial reports internally, accounts and records for

helping the managers in an organization to make suitable decisions in order to achieve long and

short term goals of the business. There are several aspects in which MA a system plays a crucial

role that are as follows-

Determining aim- Based on the information available, MA systems helps in determining

the goals and tries in finding out route by which it could reach the business or set goals.

Helps in preparing plan- It helps in formulation of the plan in accordance to needs and

the preferences of consumers. It helps the managers in studying and assessing future and present

prospects of business.

Better customer service- MA systems assist in reducing the cost incurred in

manufacturing the product by making use of cost accounting systems. It helps in defining the

quality standards in producing the product which in turn helps in providing better services to the

customer.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Increases efficiency- MA helps in enhancing efficiency of the processes as the targets of

the different department of an enterprise are been determined or identified in advance and

achieving such goals is been taken as the tool in measuring an efficiency.

Measuring performance- The planning tool under MA helps in measuring the

performance of an organization by way of determining the variance between the standard and an

actual cost.

Easy in taking judgment- Before determining any plan or the policy, an organization

uses MA systems so that best or the most suitable policy can be chosen.

1.2 Explaining different methods that are used for reporting under management accounting

Inventory management system- It is the system that manages an inventory and the stock

items of the business, keeping track of the areas where an asset of the business are present and its

worth. It also assesses an inventory need of the business and could automate the ordering. This

system of management accounting helps in reporting the level of inventory flowing within the

premises and also helps in keeping the business more organized. It presents information

regarding the need of an inventory and the amount of unused inventory at the workplace. It is the

system which is used for reporting and managing an optimum level of inventory so that wastage

can be avoided and more productivity can be achieved. It includes information relating to hourly

labor cost, per unit cost of overhead and inventory wastage. It also helps in comparing the

different assembly lines present within the business organization for the purpose of highlighting

areas for an improvement and offers bonuses to the departments that are best performing.

Job costing system- It is the method that records cost for producing or manufacturing the

job instead of the processes. Along with this system, manager could keep a track of cost for each

and every job, maintaining the data that is seen as more relevant to operations of business. This

system reports an expense for the particular project that is financed by the small business

(Amran, 2020). Such expenses are usually matched with an estimate of the revenue so that

profitability of the job can be evaluated in an appropriate manner. It helps in determining the

areas that provides higher earnings so that company could focus or put additional efforts in

developing those areas rather than in wasting money and the time on the low profitable areas.

This system reports analysis of disbursements at the time when project is at progressing stage so

that it could correct the areas of the waste before cost spiral is seen as out of control.

Price optimization system- This system means use of the mathematical tools by a firm for

determining response of the customers towards different price level in relation to its products and

the services. The data or information used in this system includes operating cost, survey data,

historic prices, inventories and the sales (Taylor and Scapens, 2016). It reports for the most

suitable price that the company should set up for the purpose of gaining large customers and

market share. This helps in producing the goods as per the specifications and the preferences of

the different department of an enterprise are been determined or identified in advance and

achieving such goals is been taken as the tool in measuring an efficiency.

Measuring performance- The planning tool under MA helps in measuring the

performance of an organization by way of determining the variance between the standard and an

actual cost.

Easy in taking judgment- Before determining any plan or the policy, an organization

uses MA systems so that best or the most suitable policy can be chosen.

1.2 Explaining different methods that are used for reporting under management accounting

Inventory management system- It is the system that manages an inventory and the stock

items of the business, keeping track of the areas where an asset of the business are present and its

worth. It also assesses an inventory need of the business and could automate the ordering. This

system of management accounting helps in reporting the level of inventory flowing within the

premises and also helps in keeping the business more organized. It presents information

regarding the need of an inventory and the amount of unused inventory at the workplace. It is the

system which is used for reporting and managing an optimum level of inventory so that wastage

can be avoided and more productivity can be achieved. It includes information relating to hourly

labor cost, per unit cost of overhead and inventory wastage. It also helps in comparing the

different assembly lines present within the business organization for the purpose of highlighting

areas for an improvement and offers bonuses to the departments that are best performing.

Job costing system- It is the method that records cost for producing or manufacturing the

job instead of the processes. Along with this system, manager could keep a track of cost for each

and every job, maintaining the data that is seen as more relevant to operations of business. This

system reports an expense for the particular project that is financed by the small business

(Amran, 2020). Such expenses are usually matched with an estimate of the revenue so that

profitability of the job can be evaluated in an appropriate manner. It helps in determining the

areas that provides higher earnings so that company could focus or put additional efforts in

developing those areas rather than in wasting money and the time on the low profitable areas.

This system reports analysis of disbursements at the time when project is at progressing stage so

that it could correct the areas of the waste before cost spiral is seen as out of control.

Price optimization system- This system means use of the mathematical tools by a firm for

determining response of the customers towards different price level in relation to its products and

the services. The data or information used in this system includes operating cost, survey data,

historic prices, inventories and the sales (Taylor and Scapens, 2016). It reports for the most

suitable price that the company should set up for the purpose of gaining large customers and

market share. This helps in producing the goods as per the specifications and the preferences of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the customers with setting up of the affordable prices so that large market could be captured by

an enterprise.

Cost accounting system- It refers to the framework which is been used by an entity for

estimating cost of their respective products for the profitability assessment, controlling cost and

valuing inventory. It presents reporting of accurate product cost which is critical for profitable

operations. It includes information regarding all the raw material costs, labor, overhead and

added cost that is taken into account. It is the report that offers summary of all such information

and also offers the managers a capacity in realizing cost price of an item over its selling prices

(Shevelev, Sheveleva and Gvozdev, 2017). The profit margins are been estimated and monitored

by using such reports and provides a clear picture of all the cost that incurred in procurement and

production of article. It provides an exact or clear understanding of the expenses that are

essential for gaining optimization of the resources among all the departments.

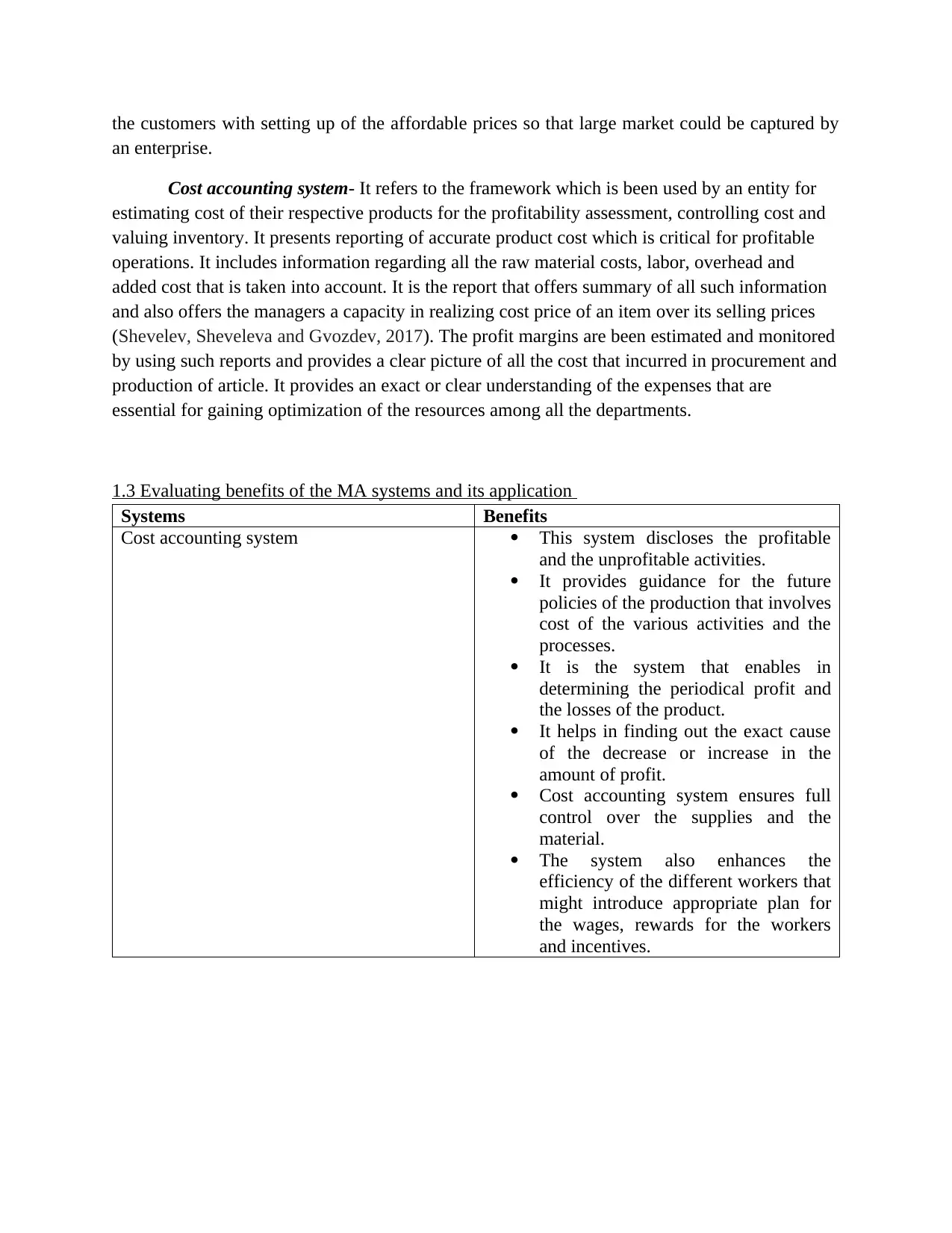

1.3 Evaluating benefits of the MA systems and its application

Systems Benefits

Cost accounting system This system discloses the profitable

and the unprofitable activities.

It provides guidance for the future

policies of the production that involves

cost of the various activities and the

processes.

It is the system that enables in

determining the periodical profit and

the losses of the product.

It helps in finding out the exact cause

of the decrease or increase in the

amount of profit.

Cost accounting system ensures full

control over the supplies and the

material.

The system also enhances the

efficiency of the different workers that

might introduce appropriate plan for

the wages, rewards for the workers

and incentives.

an enterprise.

Cost accounting system- It refers to the framework which is been used by an entity for

estimating cost of their respective products for the profitability assessment, controlling cost and

valuing inventory. It presents reporting of accurate product cost which is critical for profitable

operations. It includes information regarding all the raw material costs, labor, overhead and

added cost that is taken into account. It is the report that offers summary of all such information

and also offers the managers a capacity in realizing cost price of an item over its selling prices

(Shevelev, Sheveleva and Gvozdev, 2017). The profit margins are been estimated and monitored

by using such reports and provides a clear picture of all the cost that incurred in procurement and

production of article. It provides an exact or clear understanding of the expenses that are

essential for gaining optimization of the resources among all the departments.

1.3 Evaluating benefits of the MA systems and its application

Systems Benefits

Cost accounting system This system discloses the profitable

and the unprofitable activities.

It provides guidance for the future

policies of the production that involves

cost of the various activities and the

processes.

It is the system that enables in

determining the periodical profit and

the losses of the product.

It helps in finding out the exact cause

of the decrease or increase in the

amount of profit.

Cost accounting system ensures full

control over the supplies and the

material.

The system also enhances the

efficiency of the different workers that

might introduce appropriate plan for

the wages, rewards for the workers

and incentives.

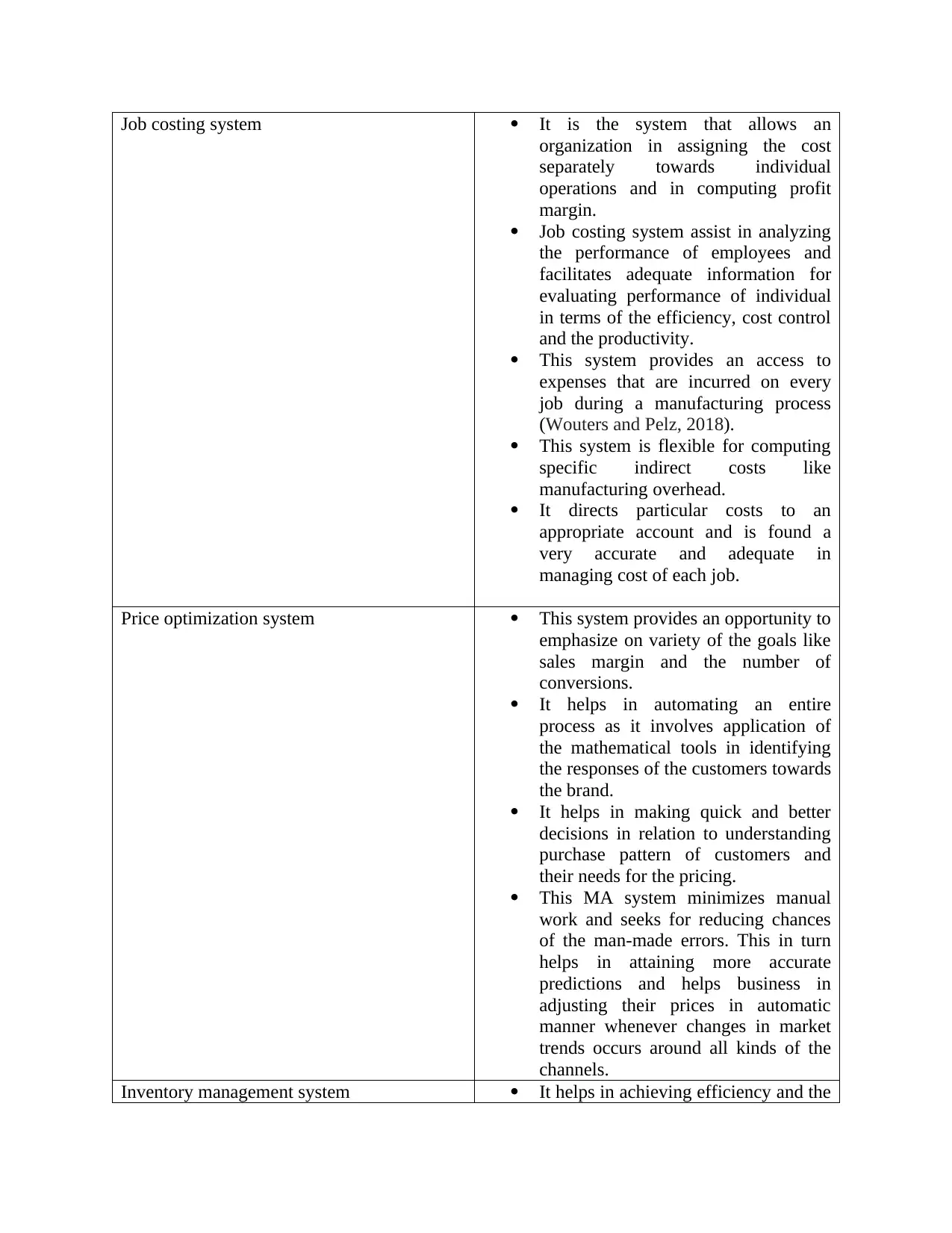

Job costing system It is the system that allows an

organization in assigning the cost

separately towards individual

operations and in computing profit

margin.

Job costing system assist in analyzing

the performance of employees and

facilitates adequate information for

evaluating performance of individual

in terms of the efficiency, cost control

and the productivity.

This system provides an access to

expenses that are incurred on every

job during a manufacturing process

(Wouters and Pelz, 2018).

This system is flexible for computing

specific indirect costs like

manufacturing overhead.

It directs particular costs to an

appropriate account and is found a

very accurate and adequate in

managing cost of each job.

Price optimization system This system provides an opportunity to

emphasize on variety of the goals like

sales margin and the number of

conversions.

It helps in automating an entire

process as it involves application of

the mathematical tools in identifying

the responses of the customers towards

the brand.

It helps in making quick and better

decisions in relation to understanding

purchase pattern of customers and

their needs for the pricing.

This MA system minimizes manual

work and seeks for reducing chances

of the man-made errors. This in turn

helps in attaining more accurate

predictions and helps business in

adjusting their prices in automatic

manner whenever changes in market

trends occurs around all kinds of the

channels.

Inventory management system It helps in achieving efficiency and the

organization in assigning the cost

separately towards individual

operations and in computing profit

margin.

Job costing system assist in analyzing

the performance of employees and

facilitates adequate information for

evaluating performance of individual

in terms of the efficiency, cost control

and the productivity.

This system provides an access to

expenses that are incurred on every

job during a manufacturing process

(Wouters and Pelz, 2018).

This system is flexible for computing

specific indirect costs like

manufacturing overhead.

It directs particular costs to an

appropriate account and is found a

very accurate and adequate in

managing cost of each job.

Price optimization system This system provides an opportunity to

emphasize on variety of the goals like

sales margin and the number of

conversions.

It helps in automating an entire

process as it involves application of

the mathematical tools in identifying

the responses of the customers towards

the brand.

It helps in making quick and better

decisions in relation to understanding

purchase pattern of customers and

their needs for the pricing.

This MA system minimizes manual

work and seeks for reducing chances

of the man-made errors. This in turn

helps in attaining more accurate

predictions and helps business in

adjusting their prices in automatic

manner whenever changes in market

trends occurs around all kinds of the

channels.

Inventory management system It helps in achieving efficiency and the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

productivity in an operation.

This system minimizes an inventory

cost and maximizes the profits and the

sales.

It helps in integrating an entire

business along with automation of the

manual tasks.

Inventory system enables in

maintaining the happiness of the

customers by delivering or supplying

the product within a time frame.

1.4 Critically evaluating integrating between systems and reporting under management

accounting

The different systems of MA plays an important role in smooth functioning of an

organization as cost accounting system plays a major role in reporting the cost or ascertaining

cost incurred with keeping control over it. This helps an organization in gaining higher profits

with low cost and higher margin. Inventory management software helps in managing the

inventory optimally in order to avoid wastage and misuse of the resources.

SECTION 2

2.1

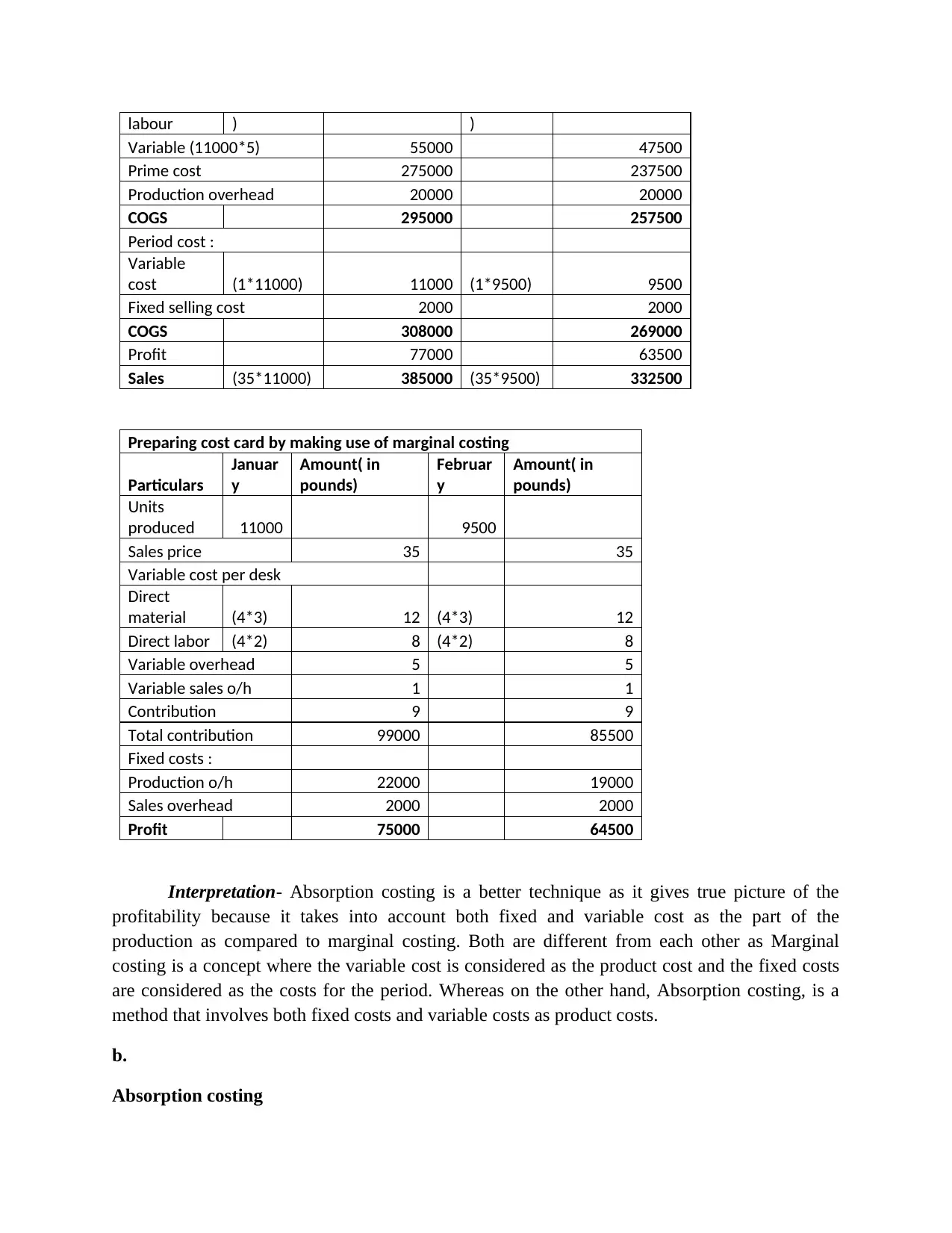

a.

Absorption costing- Absorption costing includes all of the manufacturing costs that have

been assigned to (or absorbed by) the units produced. It is concerned with the cost of a finished

product that will include the costs of: direct materials, direct labor, variable manufacturing

overhead.

Marginal costing- Marginal costing is a part of Management accounting where the fixed

cost is completely written off and variable cost is charged off to the units of cost. It is basically

concerned with the cost of producing one additional good. It takes into account all the costs that

vary with the level of production.

Preparing cost card by making use of absorption costing

Particulars January

Amount( in

pounds) February

Amount( in

pounds)

Units

produced 11000 9500

Direct

material

(4*3*11000

) 132000

(4*3*9500

) 114000

Direct (4*2*11000 88000 (4*2*9500 76000

This system minimizes an inventory

cost and maximizes the profits and the

sales.

It helps in integrating an entire

business along with automation of the

manual tasks.

Inventory system enables in

maintaining the happiness of the

customers by delivering or supplying

the product within a time frame.

1.4 Critically evaluating integrating between systems and reporting under management

accounting

The different systems of MA plays an important role in smooth functioning of an

organization as cost accounting system plays a major role in reporting the cost or ascertaining

cost incurred with keeping control over it. This helps an organization in gaining higher profits

with low cost and higher margin. Inventory management software helps in managing the

inventory optimally in order to avoid wastage and misuse of the resources.

SECTION 2

2.1

a.

Absorption costing- Absorption costing includes all of the manufacturing costs that have

been assigned to (or absorbed by) the units produced. It is concerned with the cost of a finished

product that will include the costs of: direct materials, direct labor, variable manufacturing

overhead.

Marginal costing- Marginal costing is a part of Management accounting where the fixed

cost is completely written off and variable cost is charged off to the units of cost. It is basically

concerned with the cost of producing one additional good. It takes into account all the costs that

vary with the level of production.

Preparing cost card by making use of absorption costing

Particulars January

Amount( in

pounds) February

Amount( in

pounds)

Units

produced 11000 9500

Direct

material

(4*3*11000

) 132000

(4*3*9500

) 114000

Direct (4*2*11000 88000 (4*2*9500 76000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

labour ) )

Variable (11000*5) 55000 47500

Prime cost 275000 237500

Production overhead 20000 20000

COGS 295000 257500

Period cost :

Variable

cost (1*11000) 11000 (1*9500) 9500

Fixed selling cost 2000 2000

COGS 308000 269000

Profit 77000 63500

Sales (35*11000) 385000 (35*9500) 332500

Preparing cost card by making use of marginal costing

Particulars

Januar

y

Amount( in

pounds)

Februar

y

Amount( in

pounds)

Units

produced 11000 9500

Sales price 35 35

Variable cost per desk

Direct

material (4*3) 12 (4*3) 12

Direct labor (4*2) 8 (4*2) 8

Variable overhead 5 5

Variable sales o/h 1 1

Contribution 9 9

Total contribution 99000 85500

Fixed costs :

Production o/h 22000 19000

Sales overhead 2000 2000

Profit 75000 64500

Interpretation- Absorption costing is a better technique as it gives true picture of the

profitability because it takes into account both fixed and variable cost as the part of the

production as compared to marginal costing. Both are different from each other as Marginal

costing is a concept where the variable cost is considered as the product cost and the fixed costs

are considered as the costs for the period. Whereas on the other hand, Absorption costing, is a

method that involves both fixed costs and variable costs as product costs.

b.

Absorption costing

Variable (11000*5) 55000 47500

Prime cost 275000 237500

Production overhead 20000 20000

COGS 295000 257500

Period cost :

Variable

cost (1*11000) 11000 (1*9500) 9500

Fixed selling cost 2000 2000

COGS 308000 269000

Profit 77000 63500

Sales (35*11000) 385000 (35*9500) 332500

Preparing cost card by making use of marginal costing

Particulars

Januar

y

Amount( in

pounds)

Februar

y

Amount( in

pounds)

Units

produced 11000 9500

Sales price 35 35

Variable cost per desk

Direct

material (4*3) 12 (4*3) 12

Direct labor (4*2) 8 (4*2) 8

Variable overhead 5 5

Variable sales o/h 1 1

Contribution 9 9

Total contribution 99000 85500

Fixed costs :

Production o/h 22000 19000

Sales overhead 2000 2000

Profit 75000 64500

Interpretation- Absorption costing is a better technique as it gives true picture of the

profitability because it takes into account both fixed and variable cost as the part of the

production as compared to marginal costing. Both are different from each other as Marginal

costing is a concept where the variable cost is considered as the product cost and the fixed costs

are considered as the costs for the period. Whereas on the other hand, Absorption costing, is a

method that involves both fixed costs and variable costs as product costs.

b.

Absorption costing

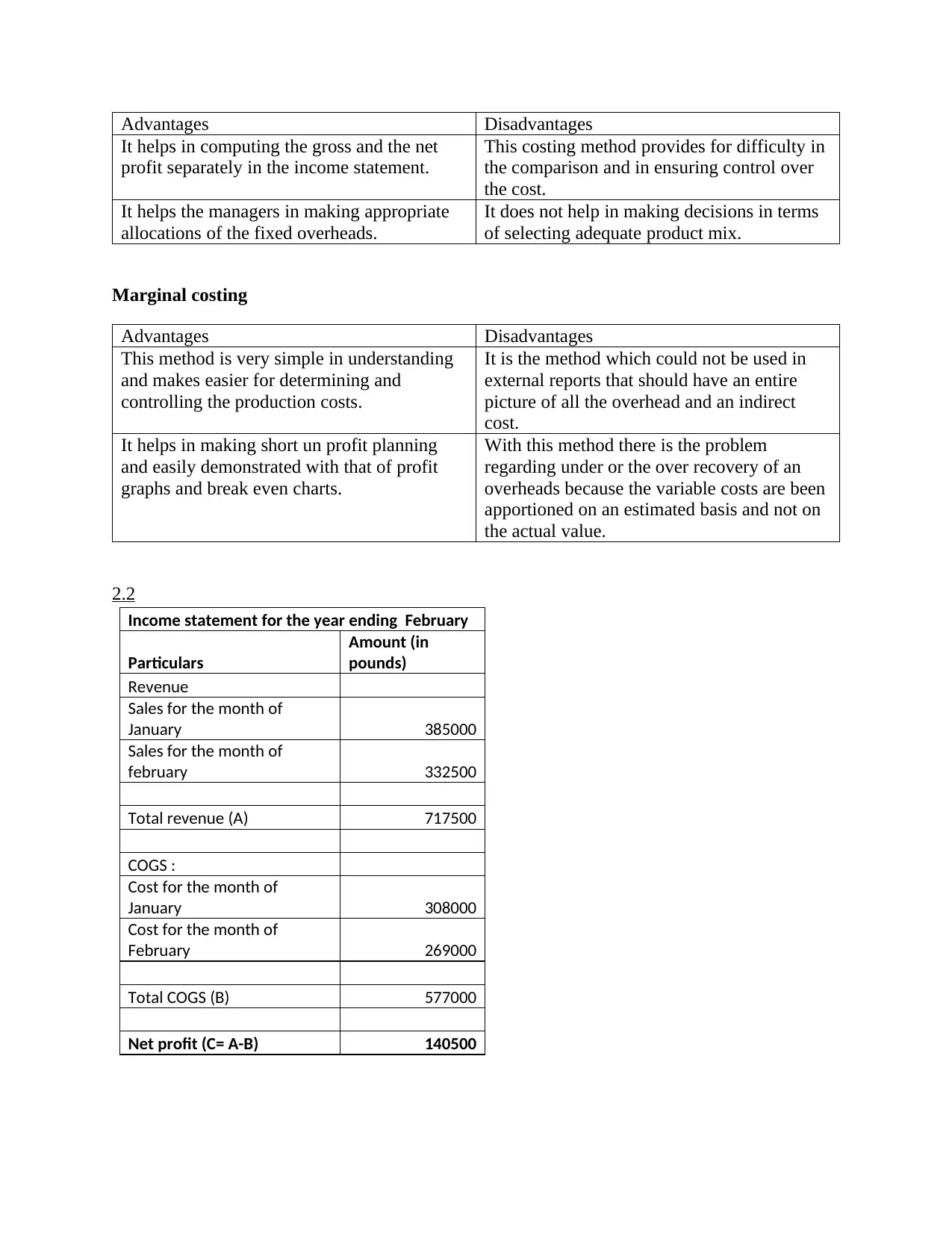

Advantages Disadvantages

It helps in computing the gross and the net

profit separately in the income statement.

This costing method provides for difficulty in

the comparison and in ensuring control over

the cost.

It helps the managers in making appropriate

allocations of the fixed overheads.

It does not help in making decisions in terms

of selecting adequate product mix.

Marginal costing

Advantages Disadvantages

This method is very simple in understanding

and makes easier for determining and

controlling the production costs.

It is the method which could not be used in

external reports that should have an entire

picture of all the overhead and an indirect

cost.

It helps in making short un profit planning

and easily demonstrated with that of profit

graphs and break even charts.

With this method there is the problem

regarding under or the over recovery of an

overheads because the variable costs are been

apportioned on an estimated basis and not on

the actual value.

2.2

Income statement for the year ending February

Particulars

Amount (in

pounds)

Revenue

Sales for the month of

January 385000

Sales for the month of

february 332500

Total revenue (A) 717500

COGS :

Cost for the month of

January 308000

Cost for the month of

February 269000

Total COGS (B) 577000

Net profit (C= A-B) 140500

It helps in computing the gross and the net

profit separately in the income statement.

This costing method provides for difficulty in

the comparison and in ensuring control over

the cost.

It helps the managers in making appropriate

allocations of the fixed overheads.

It does not help in making decisions in terms

of selecting adequate product mix.

Marginal costing

Advantages Disadvantages

This method is very simple in understanding

and makes easier for determining and

controlling the production costs.

It is the method which could not be used in

external reports that should have an entire

picture of all the overhead and an indirect

cost.

It helps in making short un profit planning

and easily demonstrated with that of profit

graphs and break even charts.

With this method there is the problem

regarding under or the over recovery of an

overheads because the variable costs are been

apportioned on an estimated basis and not on

the actual value.

2.2

Income statement for the year ending February

Particulars

Amount (in

pounds)

Revenue

Sales for the month of

January 385000

Sales for the month of

february 332500

Total revenue (A) 717500

COGS :

Cost for the month of

January 308000

Cost for the month of

February 269000

Total COGS (B) 577000

Net profit (C= A-B) 140500

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

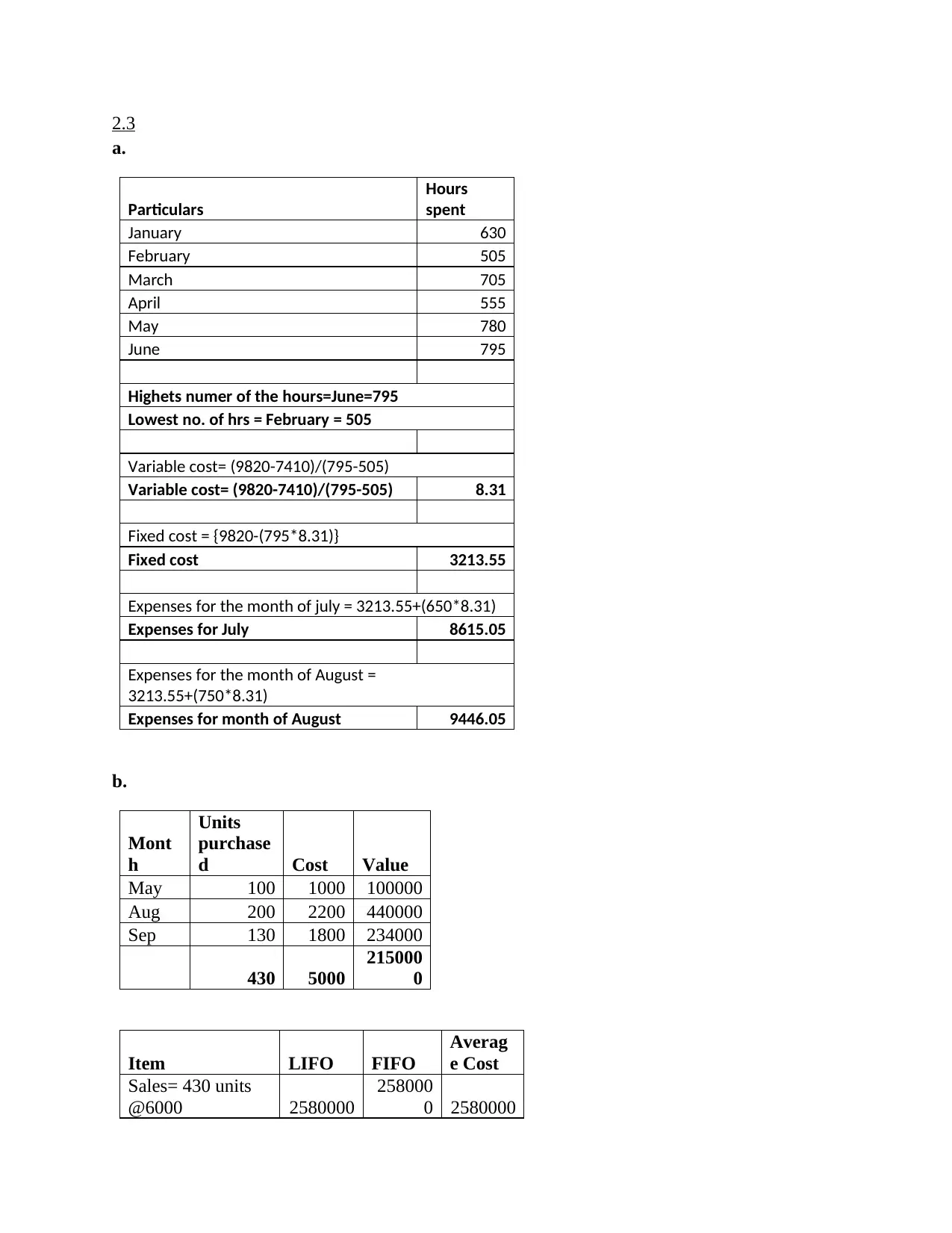

2.3

a.

Particulars

Hours

spent

January 630

February 505

March 705

April 555

May 780

June 795

Highets numer of the hours=June=795

Lowest no. of hrs = February = 505

Variable cost= (9820-7410)/(795-505)

Variable cost= (9820-7410)/(795-505) 8.31

Fixed cost = {9820-(795*8.31)}

Fixed cost 3213.55

Expenses for the month of july = 3213.55+(650*8.31)

Expenses for July 8615.05

Expenses for the month of August =

3213.55+(750*8.31)

Expenses for month of August 9446.05

b.

Mont

h

Units

purchase

d Cost Value

May 100 1000 100000

Aug 200 2200 440000

Sep 130 1800 234000

430 5000

215000

0

Item LIFO FIFO

Averag

e Cost

Sales= 430 units

@6000 2580000

258000

0 2580000

a.

Particulars

Hours

spent

January 630

February 505

March 705

April 555

May 780

June 795

Highets numer of the hours=June=795

Lowest no. of hrs = February = 505

Variable cost= (9820-7410)/(795-505)

Variable cost= (9820-7410)/(795-505) 8.31

Fixed cost = {9820-(795*8.31)}

Fixed cost 3213.55

Expenses for the month of july = 3213.55+(650*8.31)

Expenses for July 8615.05

Expenses for the month of August =

3213.55+(750*8.31)

Expenses for month of August 9446.05

b.

Mont

h

Units

purchase

d Cost Value

May 100 1000 100000

Aug 200 2200 440000

Sep 130 1800 234000

430 5000

215000

0

Item LIFO FIFO

Averag

e Cost

Sales= 430 units

@6000 2580000

258000

0 2580000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

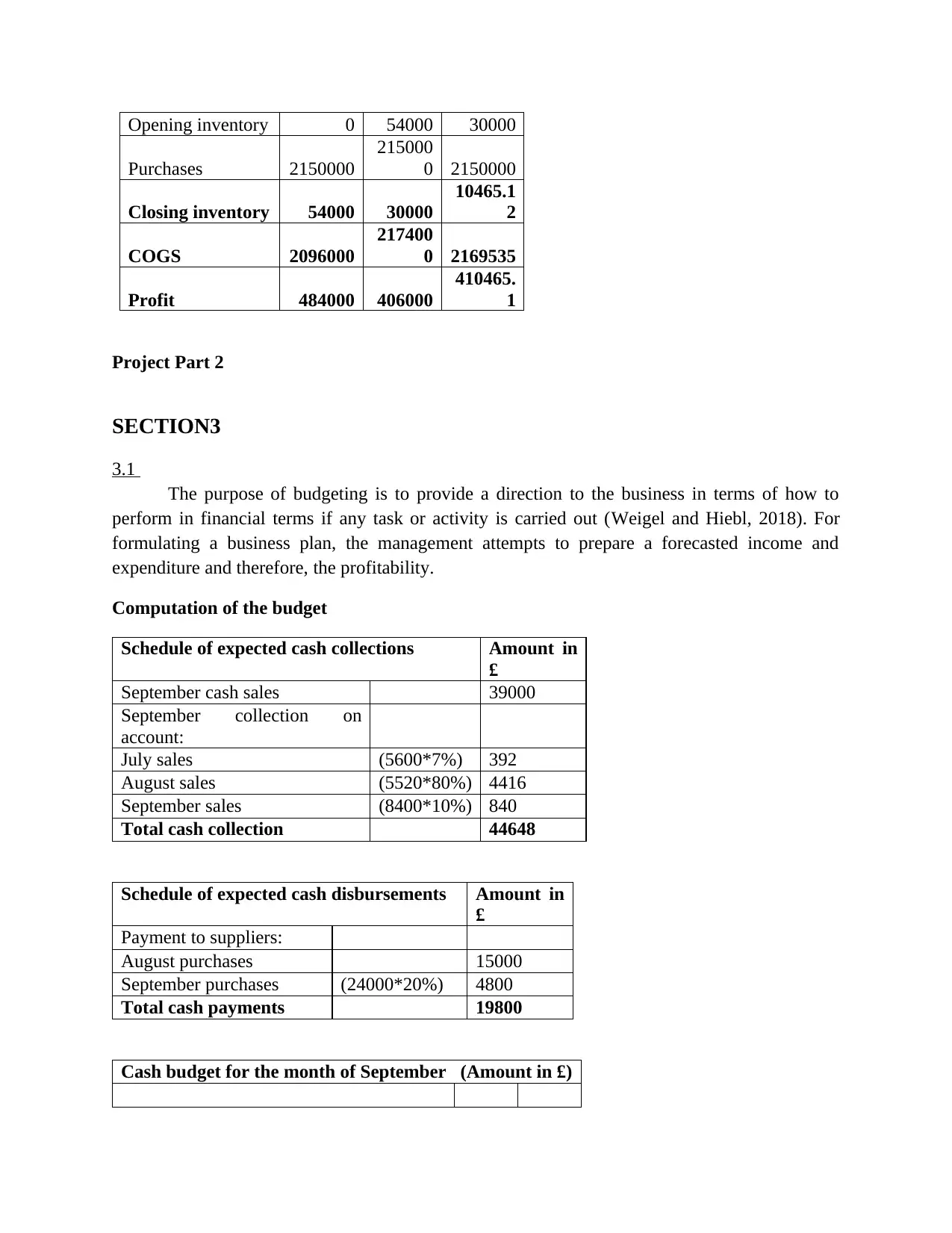

Opening inventory 0 54000 30000

Purchases 2150000

215000

0 2150000

Closing inventory 54000 30000

10465.1

2

COGS 2096000

217400

0 2169535

Profit 484000 406000

410465.

1

Project Part 2

SECTION3

3.1

The purpose of budgeting is to provide a direction to the business in terms of how to

perform in financial terms if any task or activity is carried out (Weigel and Hiebl, 2018). For

formulating a business plan, the management attempts to prepare a forecasted income and

expenditure and therefore, the profitability.

Computation of the budget

Schedule of expected cash collections Amount in

£

September cash sales 39000

September collection on

account:

July sales (5600*7%) 392

August sales (5520*80%) 4416

September sales (8400*10%) 840

Total cash collection 44648

Schedule of expected cash disbursements Amount in

£

Payment to suppliers:

August purchases 15000

September purchases (24000*20%) 4800

Total cash payments 19800

Cash budget for the month of September (Amount in £)

Purchases 2150000

215000

0 2150000

Closing inventory 54000 30000

10465.1

2

COGS 2096000

217400

0 2169535

Profit 484000 406000

410465.

1

Project Part 2

SECTION3

3.1

The purpose of budgeting is to provide a direction to the business in terms of how to

perform in financial terms if any task or activity is carried out (Weigel and Hiebl, 2018). For

formulating a business plan, the management attempts to prepare a forecasted income and

expenditure and therefore, the profitability.

Computation of the budget

Schedule of expected cash collections Amount in

£

September cash sales 39000

September collection on

account:

July sales (5600*7%) 392

August sales (5520*80%) 4416

September sales (8400*10%) 840

Total cash collection 44648

Schedule of expected cash disbursements Amount in

£

Payment to suppliers:

August purchases 15000

September purchases (24000*20%) 4800

Total cash payments 19800

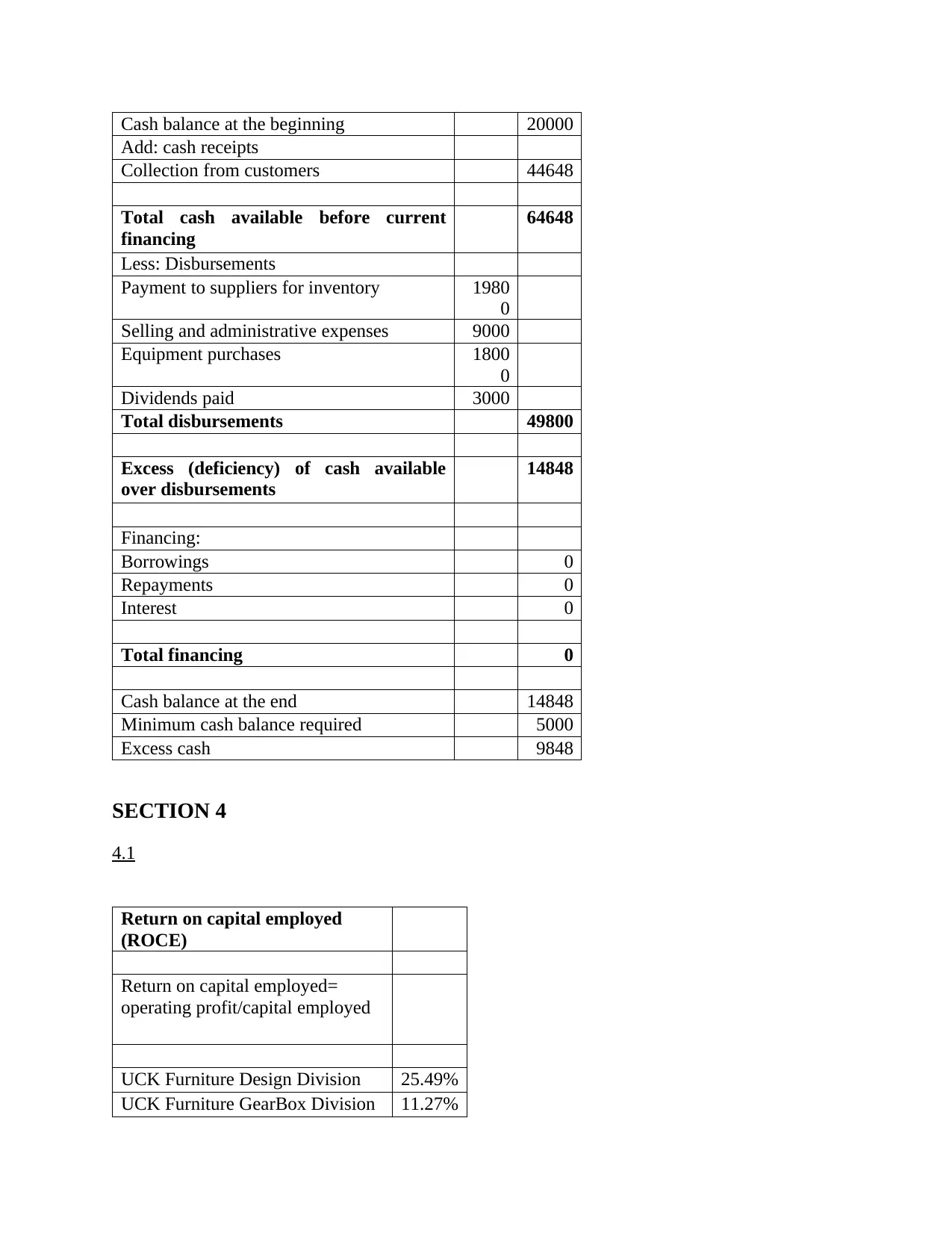

Cash budget for the month of September (Amount in £)

Cash balance at the beginning 20000

Add: cash receipts

Collection from customers 44648

Total cash available before current

financing

64648

Less: Disbursements

Payment to suppliers for inventory 1980

0

Selling and administrative expenses 9000

Equipment purchases 1800

0

Dividends paid 3000

Total disbursements 49800

Excess (deficiency) of cash available

over disbursements

14848

Financing:

Borrowings 0

Repayments 0

Interest 0

Total financing 0

Cash balance at the end 14848

Minimum cash balance required 5000

Excess cash 9848

SECTION 4

4.1

Return on capital employed

(ROCE)

Return on capital employed=

operating profit/capital employed

UCK Furniture Design Division 25.49%

UCK Furniture GearBox Division 11.27%

Add: cash receipts

Collection from customers 44648

Total cash available before current

financing

64648

Less: Disbursements

Payment to suppliers for inventory 1980

0

Selling and administrative expenses 9000

Equipment purchases 1800

0

Dividends paid 3000

Total disbursements 49800

Excess (deficiency) of cash available

over disbursements

14848

Financing:

Borrowings 0

Repayments 0

Interest 0

Total financing 0

Cash balance at the end 14848

Minimum cash balance required 5000

Excess cash 9848

SECTION 4

4.1

Return on capital employed

(ROCE)

Return on capital employed=

operating profit/capital employed

UCK Furniture Design Division 25.49%

UCK Furniture GearBox Division 11.27%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.