Management Accounting: Techniques and Cost Reporting - Palmer & Harvey

VerifiedAdded on 2023/03/24

|18

|4949

|80

Report

AI Summary

This report provides a detailed analysis of management accounting within the context of Palmer and Harvey, focusing on various management accounting techniques, optimal cost reporting systems, and key drivers influencing the management accounting process. It begins by outlining the significance of management accounting, differentiating between lean, traditional, throughput, and transfer pricing systems, and highlighting their potential applications within the organization. The report further explores the benefits of management accounting, including enhanced cash flow management, improved decision-making, performance analysis, cost reduction, and increased profitability. It also discusses various management accounting methods such as financial planning, financial statement analysis, and standard costing, emphasizing their role in achieving organizational goals and maintaining a competitive edge. The report aims to provide the General Manager with a critical understanding of the functions of a management accountant and the strategic importance of effective management accounting practices.

MANAGEMENT ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of contents

Introduction......................................................................................................................................2

Task 1...............................................................................................................................................2

Task 2...............................................................................................................................................8

Task 3.............................................................................................................................................13

Conclusion:....................................................................................................................................15

Reference list.................................................................................................................................16

Page 1 of 18

Introduction......................................................................................................................................2

Task 1...............................................................................................................................................2

Task 2...............................................................................................................................................8

Task 3.............................................................................................................................................13

Conclusion:....................................................................................................................................15

Reference list.................................................................................................................................16

Page 1 of 18

Introduction

In this study, attempts has been made to illustrate on the various aspect of a management

accountant in an business organization. Efforts have been made in the study to present a detailed

discussion in the form of a report. The report is to be presented to the General Manager of the

organization so that he is able to critically analyze the functions of the management accountant.

In order to provide a precise understanding about the research subject, an organization Palmer

and Harvey has been selected. This study primarily deals with various management accounting

techniques that are applied in an organization, the cost reporting system that is best suited for the

organization and also show a relation between the traditional cost accounting system. In addition

to that, attempts have been made in the study to discuss on the factors that acts as drivers to the

management accounting process of an organization.

Task 1

Introduction

It is evident that with the advent of globalization, the complexity in the business process has

tended to increase to a significant level. Subsequently, it has raised the level of competition in

the market. In this regards, organizations especially those catering to the manufacturing sector

faces several challenges in proper maintenance of records related to the production process. This

has necessitated organizations to adopt management accounting process. It not only helps

the ,management of the organization in guiding at each step of the process but also provide them

with facts and evidences based on which, effective decisions are taken. In addition to that, it

enhances the level of efficiency of the management. In this part of the study, efforts have been

made to discuss on the various aspect of management accounting system to an organization

including its significance and importance.

Management accounting: Its significance and types

The management accounting process unlike the financial accounting system caters to the internal

control of an organization. It is a process of identification of the organizational goals and

objectives, make a critical analysis of the same and communication about the findings to the

Page 2 of 18

In this study, attempts has been made to illustrate on the various aspect of a management

accountant in an business organization. Efforts have been made in the study to present a detailed

discussion in the form of a report. The report is to be presented to the General Manager of the

organization so that he is able to critically analyze the functions of the management accountant.

In order to provide a precise understanding about the research subject, an organization Palmer

and Harvey has been selected. This study primarily deals with various management accounting

techniques that are applied in an organization, the cost reporting system that is best suited for the

organization and also show a relation between the traditional cost accounting system. In addition

to that, attempts have been made in the study to discuss on the factors that acts as drivers to the

management accounting process of an organization.

Task 1

Introduction

It is evident that with the advent of globalization, the complexity in the business process has

tended to increase to a significant level. Subsequently, it has raised the level of competition in

the market. In this regards, organizations especially those catering to the manufacturing sector

faces several challenges in proper maintenance of records related to the production process. This

has necessitated organizations to adopt management accounting process. It not only helps

the ,management of the organization in guiding at each step of the process but also provide them

with facts and evidences based on which, effective decisions are taken. In addition to that, it

enhances the level of efficiency of the management. In this part of the study, efforts have been

made to discuss on the various aspect of management accounting system to an organization

including its significance and importance.

Management accounting: Its significance and types

The management accounting process unlike the financial accounting system caters to the internal

control of an organization. It is a process of identification of the organizational goals and

objectives, make a critical analysis of the same and communication about the findings to the

Page 2 of 18

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

management such that they are able to make effective decision. Earliest this branch of

accounting was known as cost accounting method. Usually, it is seen that the management

accounting process tends to involve use of various information related to the cost implications

incurred internally by the organization. The information aids the managers to critically analyze

the key areas of an organization and accordingly formulate action plan for future operations of

the organization (Bodie, 2013).

Usually, it is noted that, the management accounting process are classified into four different

types. They include Lean accounting system, Traditional accounting system, Throughput

accounting system and Transfer pricing. The explanation of the various types of management

accounting system is given as follows:

● Lean accounting system: It is seen that this accounting method is used in lean

organization and forms an integral part of the managerial system. It helps the managers in

bringing out the full capacity as well as helps in maintaining a consistent level of

performance metrics within the organization. Usually, this form of accounting is used in

organizations in order to tackle many extreme situations that may include issues related

to market strategies or increasing cost implications in the production process. In context

to Palmer and Harvey, it can be stated that, this form of accounting is suited and may be

applied in accordance with the convenience of the management (Fullerton et al. 2014).

● Traditional accounting system: Traditional method of accounting or as popularly known

as the cost accounting system is one of the oldest form of accounting system. Notably,

this system of accounting catered to the internal cost incurred by an organization.

However, it is seen that this form of accounting was entirely based on assumptions and

sometimes gave wrong information to the management. In addition to that, it involved

allocation of the indirect cost although it does not reflect any changes in the consumption

of resources. In context to Palmer and Harvey, it is noted that, the management of the

organization tends to face certain difficulty in adapting to the new managerial system. In

this context, it can be said that the management of the organization may opt for

traditional cost accounting methods in the initial phases in order to mitigate the identified

issues (DRURY, 2013).

● Throughput accounting system: Notably, this form, of accounting system is used by

organization in order to get a fuller utilization of the allocated resources and put them to

Page 3 of 18

accounting was known as cost accounting method. Usually, it is seen that the management

accounting process tends to involve use of various information related to the cost implications

incurred internally by the organization. The information aids the managers to critically analyze

the key areas of an organization and accordingly formulate action plan for future operations of

the organization (Bodie, 2013).

Usually, it is noted that, the management accounting process are classified into four different

types. They include Lean accounting system, Traditional accounting system, Throughput

accounting system and Transfer pricing. The explanation of the various types of management

accounting system is given as follows:

● Lean accounting system: It is seen that this accounting method is used in lean

organization and forms an integral part of the managerial system. It helps the managers in

bringing out the full capacity as well as helps in maintaining a consistent level of

performance metrics within the organization. Usually, this form of accounting is used in

organizations in order to tackle many extreme situations that may include issues related

to market strategies or increasing cost implications in the production process. In context

to Palmer and Harvey, it can be stated that, this form of accounting is suited and may be

applied in accordance with the convenience of the management (Fullerton et al. 2014).

● Traditional accounting system: Traditional method of accounting or as popularly known

as the cost accounting system is one of the oldest form of accounting system. Notably,

this system of accounting catered to the internal cost incurred by an organization.

However, it is seen that this form of accounting was entirely based on assumptions and

sometimes gave wrong information to the management. In addition to that, it involved

allocation of the indirect cost although it does not reflect any changes in the consumption

of resources. In context to Palmer and Harvey, it is noted that, the management of the

organization tends to face certain difficulty in adapting to the new managerial system. In

this context, it can be said that the management of the organization may opt for

traditional cost accounting methods in the initial phases in order to mitigate the identified

issues (DRURY, 2013).

● Throughput accounting system: Notably, this form, of accounting system is used by

organization in order to get a fuller utilization of the allocated resources and put them to

Page 3 of 18

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the organizational advantage. It is seen that, this form of accounting helps the

management to get precise information related to the organizational operational and its

corresponding performance. Subsequently, it helps the management to use the findings

and use them to make effective decisions regarding the future operation of the

organization. This form of accounting system is based upon the basic principles of

management accounting system and thus, can be applied to any organizational situations.

In context to Palmer and Harvey, it can be apprehended that, in case of any

organizational issues, the management may at their own discretion adopt this form of

accounting in order to mitigate them (Cohen et al. 2017).

● Transfer pricing: This form of accounting mainly caters to the taxation aspect of an

organization. In addition to that, a single owner or entity can apply this form of

accounting on organizations that are owned. It helps the management of the organization

to get a clear knowledge about the factors involved in the taxation process, identify any

key issues in the process and accordingly devise policies for rectification of the same. In

context to Palmer and Harvey, this system of accounting can be applied in order to

effectively deal with the prevalent taxation system within the organization (Cooper et al.

2017).

Significance of Management accounting system:

● Proper estimation and enhancement of the cash flow system: It is noted that the

management accounting process tends to effectively administer the cash balance of the

organization. In addition to that, it helps the management of the organization to ensure

that a standard level of liquidity is maintained within the organization for setting the

organizational operations (Bebbington et al. 2014). It helps the managers in preparation

of budget and thereby, get a precise estimation of the cash requirements and the

corresponding cash generation of the organization. Subsequently, it helps the managers in

proper allocation of the organizational resources, monitoring the usage of cash in various

activities, identifying any deviations and accordingly in formulation of policies in order

to avoid any future contingencies. Hence, it helps the management of the organization in

effective cash management (Zhou, 2017).

● Helps in making effective managerial decisions: One of the primary aspect of the

management accounting system is that it aids the managers of the organization in making

Page 4 of 18

management to get precise information related to the organizational operational and its

corresponding performance. Subsequently, it helps the management to use the findings

and use them to make effective decisions regarding the future operation of the

organization. This form of accounting system is based upon the basic principles of

management accounting system and thus, can be applied to any organizational situations.

In context to Palmer and Harvey, it can be apprehended that, in case of any

organizational issues, the management may at their own discretion adopt this form of

accounting in order to mitigate them (Cohen et al. 2017).

● Transfer pricing: This form of accounting mainly caters to the taxation aspect of an

organization. In addition to that, a single owner or entity can apply this form of

accounting on organizations that are owned. It helps the management of the organization

to get a clear knowledge about the factors involved in the taxation process, identify any

key issues in the process and accordingly devise policies for rectification of the same. In

context to Palmer and Harvey, this system of accounting can be applied in order to

effectively deal with the prevalent taxation system within the organization (Cooper et al.

2017).

Significance of Management accounting system:

● Proper estimation and enhancement of the cash flow system: It is noted that the

management accounting process tends to effectively administer the cash balance of the

organization. In addition to that, it helps the management of the organization to ensure

that a standard level of liquidity is maintained within the organization for setting the

organizational operations (Bebbington et al. 2014). It helps the managers in preparation

of budget and thereby, get a precise estimation of the cash requirements and the

corresponding cash generation of the organization. Subsequently, it helps the managers in

proper allocation of the organizational resources, monitoring the usage of cash in various

activities, identifying any deviations and accordingly in formulation of policies in order

to avoid any future contingencies. Hence, it helps the management of the organization in

effective cash management (Zhou, 2017).

● Helps in making effective managerial decisions: One of the primary aspect of the

management accounting system is that it aids the managers of the organization in making

Page 4 of 18

effective decisions. Usually, it is seen that, unlike financial accounting system,

management accounting system tends to include both qualitative as well as quantitative

aspect and thereby aids the managers in effective and efficient decision-making. It is seen

that, the managers of an organization tends to use information that are based on certain

assumptions and there lies a probability of taking wrong decisions. The management

accounting system acts as a bridge in mitigating such gaps and thereby helps in effective

decisions (Bouten and Hoozée, 2013).

● Analysis of the overall performance of the organization: the management accounting

process helps the managers of the organization to identify any kinds of downturn or

shortcomings in the organizational operations and helps to formulate control measures for

mitigating the same. It is evident to hate the management accounting process caters to the

internal operations of the organization. It helps in proper identification of the issues or

any kind of deviations related to the organizational operations, monitor the allocation of

the organizational resources and accordingly devise control measures for mitigation of

the identified issues. It helps in enhancing the efficiency of the organization and thereby,

its performance in the market (Bouten and Hoozée, 2013).

● Reduction of the cost implications related to the organisational operations: Another major

function of the management accounting system is effective management of the cost

implications. It helps the management of the organization to efficiently monitor the

overall costs implications as well as put control measures in case of excess expenses

(Cohen et al. 2017). Additionally, it helps the management to get a precise estimation of

the costs to be incurred for various activities of the organization, identify the potential

sources to procure the financial resources and accordingly devise strategies. In addition to

that, the management accounting process helps the managers to make forecasts about

future contingencies and take necessary control measures in order to mitigate them.

Moreover, it helps in effective cash management related to the production process

(Bouten and Hoozée, 2013).

● Enhancing the productivity as well as the profitability of the organization: It is seen that

management accounting process if applied to an organization facilitates the managers

with several benefits. They include reductions in the internal cost implications, effective

decision making, enhancing efficiency in cash flow and thereby, in enhancing the

Page 5 of 18

management accounting system tends to include both qualitative as well as quantitative

aspect and thereby aids the managers in effective and efficient decision-making. It is seen

that, the managers of an organization tends to use information that are based on certain

assumptions and there lies a probability of taking wrong decisions. The management

accounting system acts as a bridge in mitigating such gaps and thereby helps in effective

decisions (Bouten and Hoozée, 2013).

● Analysis of the overall performance of the organization: the management accounting

process helps the managers of the organization to identify any kinds of downturn or

shortcomings in the organizational operations and helps to formulate control measures for

mitigating the same. It is evident to hate the management accounting process caters to the

internal operations of the organization. It helps in proper identification of the issues or

any kind of deviations related to the organizational operations, monitor the allocation of

the organizational resources and accordingly devise control measures for mitigation of

the identified issues. It helps in enhancing the efficiency of the organization and thereby,

its performance in the market (Bouten and Hoozée, 2013).

● Reduction of the cost implications related to the organisational operations: Another major

function of the management accounting system is effective management of the cost

implications. It helps the management of the organization to efficiently monitor the

overall costs implications as well as put control measures in case of excess expenses

(Cohen et al. 2017). Additionally, it helps the management to get a precise estimation of

the costs to be incurred for various activities of the organization, identify the potential

sources to procure the financial resources and accordingly devise strategies. In addition to

that, the management accounting process helps the managers to make forecasts about

future contingencies and take necessary control measures in order to mitigate them.

Moreover, it helps in effective cash management related to the production process

(Bouten and Hoozée, 2013).

● Enhancing the productivity as well as the profitability of the organization: It is seen that

management accounting process if applied to an organization facilitates the managers

with several benefits. They include reductions in the internal cost implications, effective

decision making, enhancing efficiency in cash flow and thereby, in enhancing the

Page 5 of 18

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

productivity of the organization. It helps the managers to get a clear understanding of the

market factors and subsequently identify the requisites to deliver quality returns. In

addition to that, it helps the management of the organization to identify the strategies

adopted by the competitors in the market, analyzed their performance and thereby take

decisions for future operations of the organization (Cooper et al. 2017). Subsequently, it

helps the management of the organization to effectively manage the operations, monitor

the level of sales and production and accordingly boosts the profitability of the

organization. In addition to that, it is noted that, the management accounting process

helps to identify the degree of profitability in various business projects and thereby, make

effective investing decisions. In regards to this, it can be apprehended that the

management accounting process helps an organization to get a competitive edge in the

market and in enhancing the level of profitability as well. Moreover, this process acts as a

tool for the management of the organization to measure the overall performance, identify

any key issues, critically analyze them as well as formulate policies in order to mitigate.

It acts as effective instrument for the management to enhance the performance metrics of

the organization and accordingly increase the level of profitability (Zhou, 2017).

Different methods of management accounting system and its application in Palmer and

Harvey:

The various methods of management accounting system are listed as below:

● Financial Planning: Usually, it is noted that financial planning by the management tends

to include various activities like identification of the sources of finances, estimating the

financial requisites of the organization, etc. It helps the management of the organization

to set both short-term as well as long-term organizational goals and objectives (Cohen et

al. 2017).

● Analysis of the financial statements of the organization: The management accounting

system helps the managers in critical analysis of the financial report of van organization.

It provides the managers with an insight into the financial stability of the organization,

the different costs implications involved and the net earnings of the organization. It helps

to make a comparative analysis with that of the competitor in the market (Bodie, 2013).

● Standard costing: the standard costing method is one of the effective management

accounting system that helps in making a comparative analysis between the actual output

Page 6 of 18

market factors and subsequently identify the requisites to deliver quality returns. In

addition to that, it helps the management of the organization to identify the strategies

adopted by the competitors in the market, analyzed their performance and thereby take

decisions for future operations of the organization (Cooper et al. 2017). Subsequently, it

helps the management of the organization to effectively manage the operations, monitor

the level of sales and production and accordingly boosts the profitability of the

organization. In addition to that, it is noted that, the management accounting process

helps to identify the degree of profitability in various business projects and thereby, make

effective investing decisions. In regards to this, it can be apprehended that the

management accounting process helps an organization to get a competitive edge in the

market and in enhancing the level of profitability as well. Moreover, this process acts as a

tool for the management of the organization to measure the overall performance, identify

any key issues, critically analyze them as well as formulate policies in order to mitigate.

It acts as effective instrument for the management to enhance the performance metrics of

the organization and accordingly increase the level of profitability (Zhou, 2017).

Different methods of management accounting system and its application in Palmer and

Harvey:

The various methods of management accounting system are listed as below:

● Financial Planning: Usually, it is noted that financial planning by the management tends

to include various activities like identification of the sources of finances, estimating the

financial requisites of the organization, etc. It helps the management of the organization

to set both short-term as well as long-term organizational goals and objectives (Cohen et

al. 2017).

● Analysis of the financial statements of the organization: The management accounting

system helps the managers in critical analysis of the financial report of van organization.

It provides the managers with an insight into the financial stability of the organization,

the different costs implications involved and the net earnings of the organization. It helps

to make a comparative analysis with that of the competitor in the market (Bodie, 2013).

● Standard costing: the standard costing method is one of the effective management

accounting system that helps in making a comparative analysis between the actual output

Page 6 of 18

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

with that of the budgeted figures. It helps the management to identify any kind of

deviation from the estimated budget, analyze or evaluate the key areas that need

improvement and accordingly devise strategies in order to control the deviations. It helps

the management to analyze the variances and take relevant measures for the same (Zhou,

2017).

● Budgetary control:

This is been utilized as a part of request to controller diverse sort of costs that are acquired by the

business association, particularly the Palmer and Harvey. The different exercises are checked and

controlled so as to dispose of any sort of wastage of the assets of the association and along these

lines the expenses are kept up in such a request, with the goal that the organization can acquire

consistent measure of benefits.

● Marginal costing:

Marginal costing are done in order to gain the analytical results of the accounting valuations. It is

done in order to gain the overall financial information of the firm’s activities and performances.

Marginal costing method consists of break even analysis that contains the financial breakdowns

of the year (Van, 2011).

● Decision making process:

The process is essential in order to gain different marketing strategies and plans in order to gain

the market revenues through financial activities (Scapens and Bromwich, 2010).

● Communication of information:

Communication skills are required to develop the financial activities of a firm. As the practices

and requirements of the essential elements of activities are gathered through communications.

Thus, the marketing and financial activities can be smoother and effective with better

communication and information processes.

● Graphical and statistical representation:

Management accounting helps in the development of different facts and understanding of the

information that are accessible within the workmanship hands. This assists the association to see

any essential information and make distinctive sort of strides in light of such sort of data (Renz,

2016).

Conclusion:

Page 7 of 18

deviation from the estimated budget, analyze or evaluate the key areas that need

improvement and accordingly devise strategies in order to control the deviations. It helps

the management to analyze the variances and take relevant measures for the same (Zhou,

2017).

● Budgetary control:

This is been utilized as a part of request to controller diverse sort of costs that are acquired by the

business association, particularly the Palmer and Harvey. The different exercises are checked and

controlled so as to dispose of any sort of wastage of the assets of the association and along these

lines the expenses are kept up in such a request, with the goal that the organization can acquire

consistent measure of benefits.

● Marginal costing:

Marginal costing are done in order to gain the analytical results of the accounting valuations. It is

done in order to gain the overall financial information of the firm’s activities and performances.

Marginal costing method consists of break even analysis that contains the financial breakdowns

of the year (Van, 2011).

● Decision making process:

The process is essential in order to gain different marketing strategies and plans in order to gain

the market revenues through financial activities (Scapens and Bromwich, 2010).

● Communication of information:

Communication skills are required to develop the financial activities of a firm. As the practices

and requirements of the essential elements of activities are gathered through communications.

Thus, the marketing and financial activities can be smoother and effective with better

communication and information processes.

● Graphical and statistical representation:

Management accounting helps in the development of different facts and understanding of the

information that are accessible within the workmanship hands. This assists the association to see

any essential information and make distinctive sort of strides in light of such sort of data (Renz,

2016).

Conclusion:

Page 7 of 18

This piece of the investigation has been done in view of the terms of clarification of

administration bookkeeping and giving the fundamental necessities of various sorts of

administration bookkeeping framework. Further, this part has additionally managed the

significance of administration Accounting and clarification of various techniques utilized for

administration bookkeeping detailing. Distinctive ideas identified with the part of administration

bookkeeping has been perceived and clarified in this investigation. Further, the centrality and

diverse sort of utilized of administration bookkeeping in various sort of business association

have likewise been distinguished and clarified in different parts of this examination.

Task 2

Introduction:

The study is mainly based on the assumptions and calculations that are required. The

accomplishment of the study depends on the calculations and analysis of the evaluation along

with the impact on the financial activated off the firm. It is also to be stated the calculations are

done based on financial figures that are researched and the calculation of costing methods are

done according to the given information. In this, the study costing methods are to be applied in

order to accomplish the calculation tasks. Absorption costing and Marginal costing are to be used

in the study. The study also requires the further extension of the calculation results ads the

researcher have to analyse and identify the deviations and other factors for costing valuations.

Calculation of the net profit using Absorption costing method:

Absorption costing

Year 1

Particulars Amount Units

Production 600

Sales volume 500

Page 8 of 18

administration bookkeeping and giving the fundamental necessities of various sorts of

administration bookkeeping framework. Further, this part has additionally managed the

significance of administration Accounting and clarification of various techniques utilized for

administration bookkeeping detailing. Distinctive ideas identified with the part of administration

bookkeeping has been perceived and clarified in this investigation. Further, the centrality and

diverse sort of utilized of administration bookkeeping in various sort of business association

have likewise been distinguished and clarified in different parts of this examination.

Task 2

Introduction:

The study is mainly based on the assumptions and calculations that are required. The

accomplishment of the study depends on the calculations and analysis of the evaluation along

with the impact on the financial activated off the firm. It is also to be stated the calculations are

done based on financial figures that are researched and the calculation of costing methods are

done according to the given information. In this, the study costing methods are to be applied in

order to accomplish the calculation tasks. Absorption costing and Marginal costing are to be used

in the study. The study also requires the further extension of the calculation results ads the

researcher have to analyse and identify the deviations and other factors for costing valuations.

Calculation of the net profit using Absorption costing method:

Absorption costing

Year 1

Particulars Amount Units

Production 600

Sales volume 500

Page 8 of 18

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

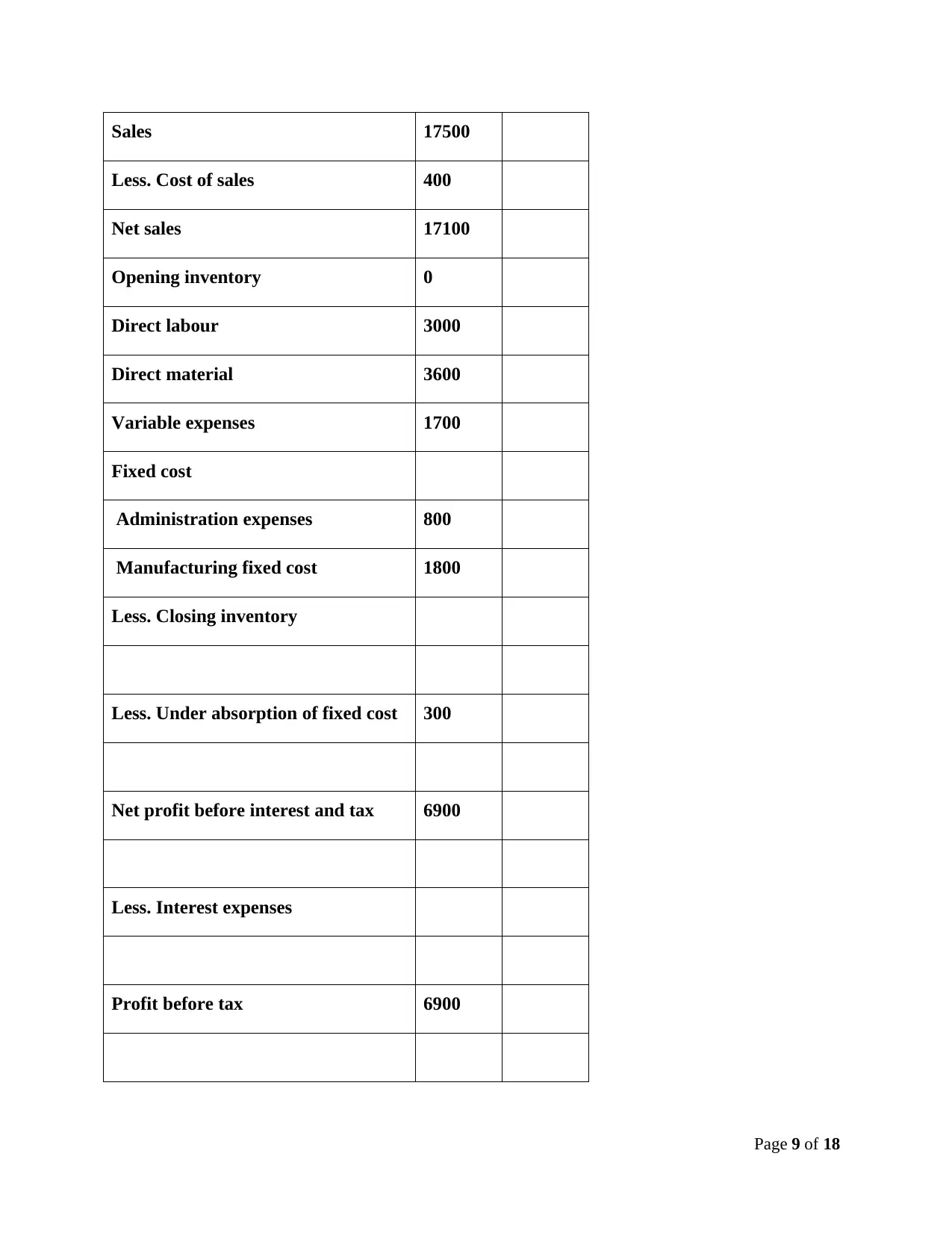

Sales 17500

Less. Cost of sales 400

Net sales 17100

Opening inventory 0

Direct labour 3000

Direct material 3600

Variable expenses 1700

Fixed cost

Administration expenses 800

Manufacturing fixed cost 1800

Less. Closing inventory

Less. Under absorption of fixed cost 300

Net profit before interest and tax 6900

Less. Interest expenses

Profit before tax 6900

Page 9 of 18

Less. Cost of sales 400

Net sales 17100

Opening inventory 0

Direct labour 3000

Direct material 3600

Variable expenses 1700

Fixed cost

Administration expenses 800

Manufacturing fixed cost 1800

Less. Closing inventory

Less. Under absorption of fixed cost 300

Net profit before interest and tax 6900

Less. Interest expenses

Profit before tax 6900

Page 9 of 18

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Less. Tax 2070

Profit after tax 4830

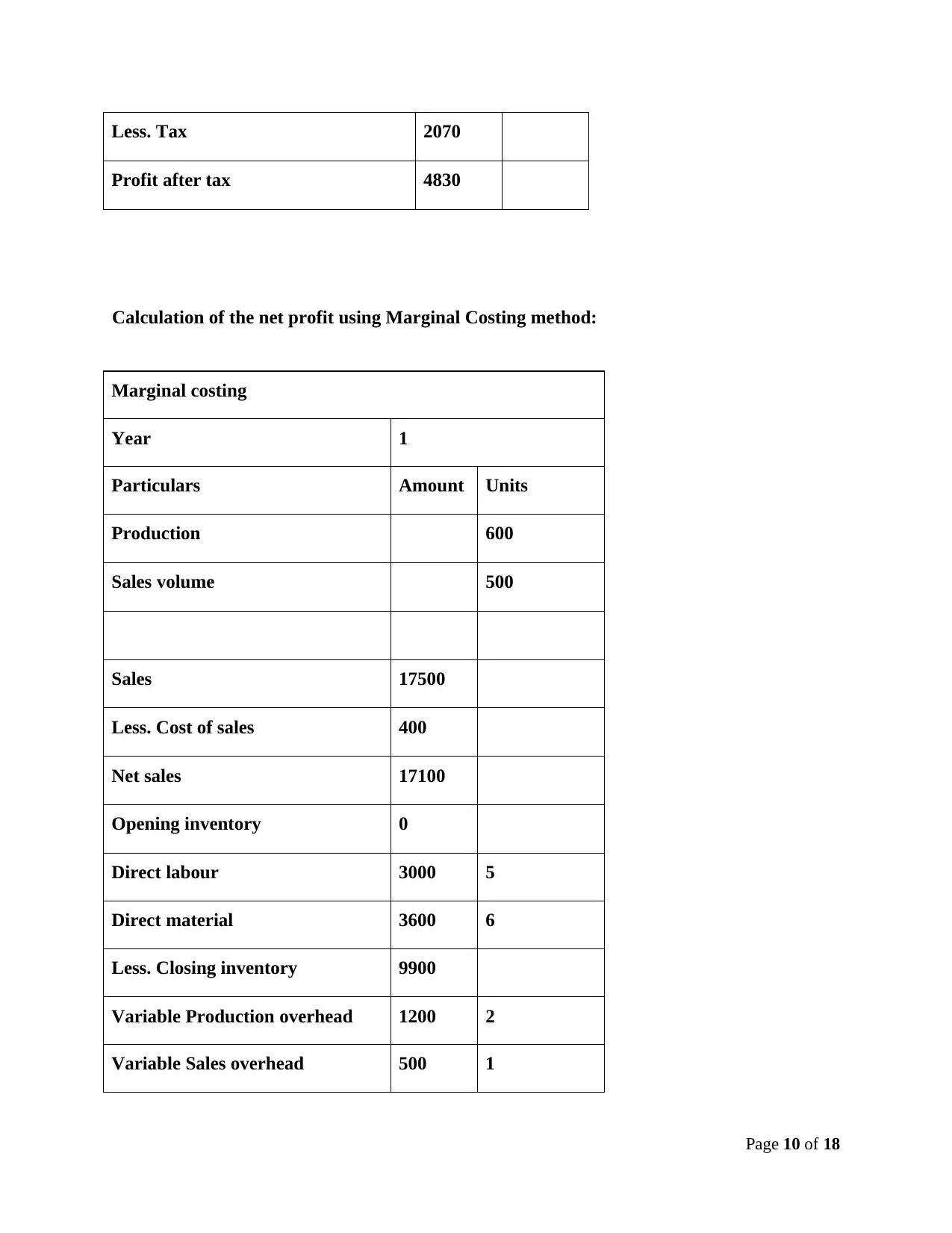

Calculation of the net profit using Marginal Costing method:

Marginal costing

Year 1

Particulars Amount Units

Production 600

Sales volume 500

Sales 17500

Less. Cost of sales 400

Net sales 17100

Opening inventory 0

Direct labour 3000 5

Direct material 3600 6

Less. Closing inventory 9900

Variable Production overhead 1200 2

Variable Sales overhead 500 1

Page 10 of 18

Profit after tax 4830

Calculation of the net profit using Marginal Costing method:

Marginal costing

Year 1

Particulars Amount Units

Production 600

Sales volume 500

Sales 17500

Less. Cost of sales 400

Net sales 17100

Opening inventory 0

Direct labour 3000 5

Direct material 3600 6

Less. Closing inventory 9900

Variable Production overhead 1200 2

Variable Sales overhead 500 1

Page 10 of 18

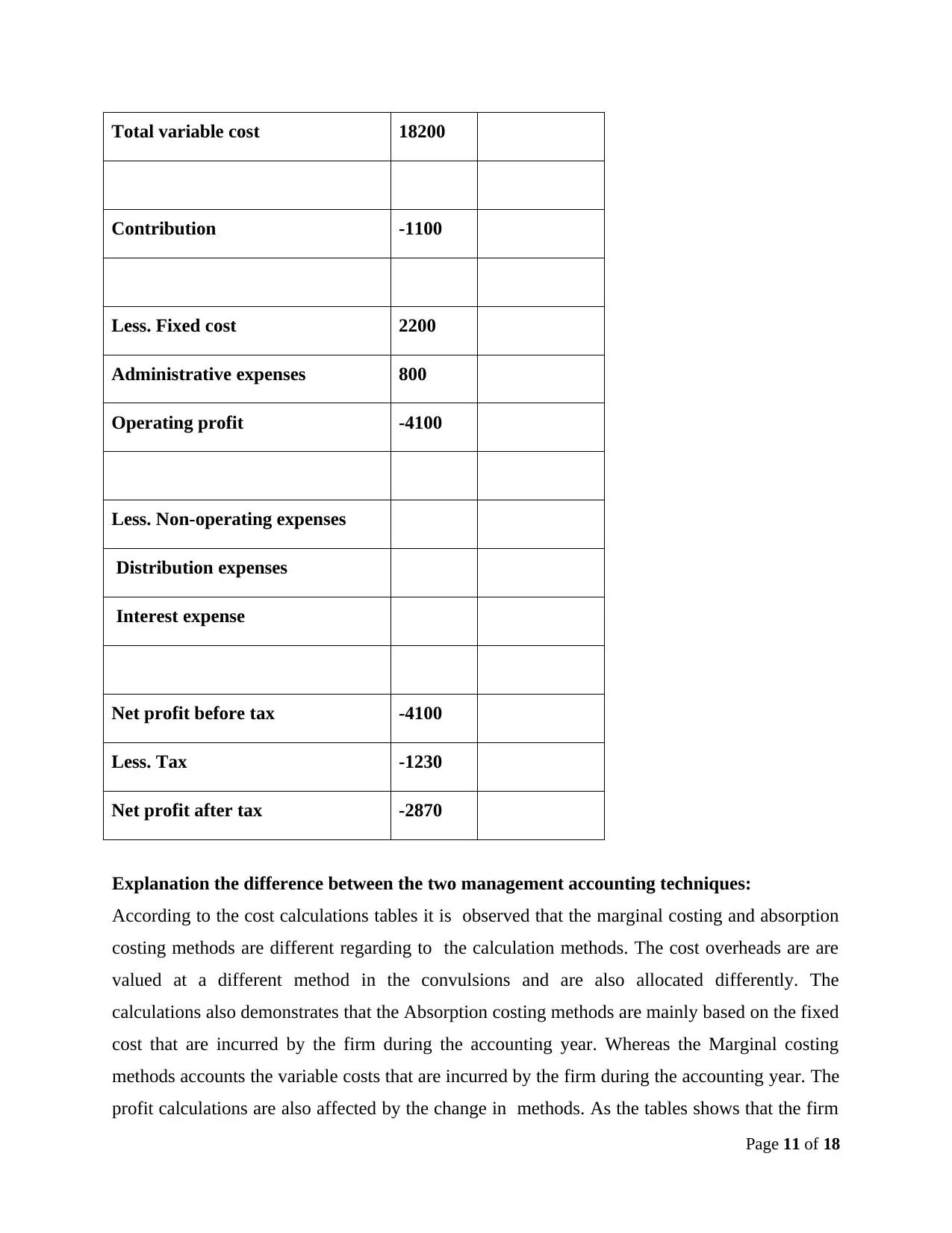

Total variable cost 18200

Contribution -1100

Less. Fixed cost 2200

Administrative expenses 800

Operating profit -4100

Less. Non-operating expenses

Distribution expenses

Interest expense

Net profit before tax -4100

Less. Tax -1230

Net profit after tax -2870

Explanation the difference between the two management accounting techniques:

According to the cost calculations tables it is observed that the marginal costing and absorption

costing methods are different regarding to the calculation methods. The cost overheads are are

valued at a different method in the convulsions and are also allocated differently. The

calculations also demonstrates that the Absorption costing methods are mainly based on the fixed

cost that are incurred by the firm during the accounting year. Whereas the Marginal costing

methods accounts the variable costs that are incurred by the firm during the accounting year. The

profit calculations are also affected by the change in methods. As the tables shows that the firm

Page 11 of 18

Contribution -1100

Less. Fixed cost 2200

Administrative expenses 800

Operating profit -4100

Less. Non-operating expenses

Distribution expenses

Interest expense

Net profit before tax -4100

Less. Tax -1230

Net profit after tax -2870

Explanation the difference between the two management accounting techniques:

According to the cost calculations tables it is observed that the marginal costing and absorption

costing methods are different regarding to the calculation methods. The cost overheads are are

valued at a different method in the convulsions and are also allocated differently. The

calculations also demonstrates that the Absorption costing methods are mainly based on the fixed

cost that are incurred by the firm during the accounting year. Whereas the Marginal costing

methods accounts the variable costs that are incurred by the firm during the accounting year. The

profit calculations are also affected by the change in methods. As the tables shows that the firm

Page 11 of 18

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.