Evaluation of Management Accounting System for Pavestone

VerifiedAdded on 2020/12/29

|19

|5488

|134

Report

AI Summary

This report delves into the realm of management accounting, focusing on the application of various systems and techniques within the context of Pavestone, a UK-based building materials supplier. The report initiates with an overview of management accounting, its types, and its significance in facilitating internal decision-making. It then explores diverse reporting methods, including budget reports, job cost reports, and accounts receivable aging reports, highlighting their advantages and integration within organizational processes. The core of the report examines costing methods, specifically marginal and absorption costing, providing detailed calculations and income statements. Furthermore, the report analyzes budgetary control, planning tools, and their role in preparing and forecasting budgets. Finally, it addresses how management accounting systems respond to financial problems, concluding that these systems lead to sustainable success. The report includes tables, calculations, and critical evaluations to support its arguments.

MANAGEMENT

ACCOUNTING SYSTEM

ACCOUNTING SYSTEM

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting and its types..............................................................................1

P2 Different methods of management accounting reporting..................................................2

M1 Advantage of applications of management accounting system.......................................3

D1 Critical evaluation on how management accounting system and its reporting can be

integrated within organisational process................................................................................4

TASK 2............................................................................................................................................4

P3 Calculation of costing........................................................................................................4

M2 Different types of accounting techniques.......................................................................8

D2 Data interpretation............................................................................................................8

TASK 3............................................................................................................................................9

P4 Budgetary control and different types of planning tool and their advantages and

disadvantages used in budgetary control................................................................................9

M3 Uses and applications of planning tools for preparing and forecasting budgets............10

TASK 4..........................................................................................................................................11

P5: Responses of management accounting system to deal with financial problems............11

M4: Management accounting can lead organisation to sustainable success in responding to

financial problems................................................................................................................13

D3: Planning tools respond appropriately to resolve financial problems.............................13

CONCLUSION..............................................................................................................................13

REFERENCE ................................................................................................................................15

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting and its types..............................................................................1

P2 Different methods of management accounting reporting..................................................2

M1 Advantage of applications of management accounting system.......................................3

D1 Critical evaluation on how management accounting system and its reporting can be

integrated within organisational process................................................................................4

TASK 2............................................................................................................................................4

P3 Calculation of costing........................................................................................................4

M2 Different types of accounting techniques.......................................................................8

D2 Data interpretation............................................................................................................8

TASK 3............................................................................................................................................9

P4 Budgetary control and different types of planning tool and their advantages and

disadvantages used in budgetary control................................................................................9

M3 Uses and applications of planning tools for preparing and forecasting budgets............10

TASK 4..........................................................................................................................................11

P5: Responses of management accounting system to deal with financial problems............11

M4: Management accounting can lead organisation to sustainable success in responding to

financial problems................................................................................................................13

D3: Planning tools respond appropriately to resolve financial problems.............................13

CONCLUSION..............................................................................................................................13

REFERENCE ................................................................................................................................15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management accounting refers to a process of preparing reports and accounts which

gives accurate information about internal state of a company. It helps managers of a firm in

making decisions related to short-term and day-to-day operation. The present assignment is made

on Pavestone of UK which deals in small sector. This firm supplies building materials to

construction companies on reasonable and affordable price rates (Hilton and Platt, 2013). This

report includes a critical discussion of different types of management accounting systems and its

methods of reporting. It includes a preparation of income statement of this company on the basis

of marginal and absorption costing. Along with this, various types of planning tool used in

budgetary control also discusses with some of its advantages and disadvantages. In order to

resolve financial problems, a comparison is made to show how management accounting helps in

dealing with such issues.

TASK 1

P1 Management accounting and its types

Management accounting is a process of analysing cost and operations of business which

helps in preparing internal report and account. It is also termed as cost or managerial accounting

through which managers of a company can make decisions related to achievement of business

goals (Otley and Emmanuel, 2013). Therefore, it is an important concept in business which

enhance efficiency of operations. In context with Pavestone, which deals in manufacturing

sector, through management accounting, managers can plan, control and manage entire activities

in systematic manner.

Managers of Pavestone can compare actual performance of business with expected

outcome. It sets out some major deviations on which essential steps can be taken as well as

implemented. In this regard, some important methods of management accounting are

explained as below:-

Cost accounting system – This method helps a company in estimating its product cost

for analysing organisational profitability and inventories valuation. Since the accurate cost of

goods is critical for small companies therefore, in context with Pavestone, it is required to

analyse which product will be profitable. This firm manufactures a wide variety of pre-cast

concrete walling and paving products. Thus, to serve goods to landscapers and other companies

1

Management accounting refers to a process of preparing reports and accounts which

gives accurate information about internal state of a company. It helps managers of a firm in

making decisions related to short-term and day-to-day operation. The present assignment is made

on Pavestone of UK which deals in small sector. This firm supplies building materials to

construction companies on reasonable and affordable price rates (Hilton and Platt, 2013). This

report includes a critical discussion of different types of management accounting systems and its

methods of reporting. It includes a preparation of income statement of this company on the basis

of marginal and absorption costing. Along with this, various types of planning tool used in

budgetary control also discusses with some of its advantages and disadvantages. In order to

resolve financial problems, a comparison is made to show how management accounting helps in

dealing with such issues.

TASK 1

P1 Management accounting and its types

Management accounting is a process of analysing cost and operations of business which

helps in preparing internal report and account. It is also termed as cost or managerial accounting

through which managers of a company can make decisions related to achievement of business

goals (Otley and Emmanuel, 2013). Therefore, it is an important concept in business which

enhance efficiency of operations. In context with Pavestone, which deals in manufacturing

sector, through management accounting, managers can plan, control and manage entire activities

in systematic manner.

Managers of Pavestone can compare actual performance of business with expected

outcome. It sets out some major deviations on which essential steps can be taken as well as

implemented. In this regard, some important methods of management accounting are

explained as below:-

Cost accounting system – This method helps a company in estimating its product cost

for analysing organisational profitability and inventories valuation. Since the accurate cost of

goods is critical for small companies therefore, in context with Pavestone, it is required to

analyse which product will be profitable. This firm manufactures a wide variety of pre-cast

concrete walling and paving products. Thus, to serve goods to landscapers and other companies

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

in profitable manner, this company use two methods of accounting system that are job order and

process costing. Job order costing accumulates cost of manufacturing separately for each job.

While process costing accumulates the same for each process. Therefore, both methods help in

getting participation and cooperation of executives required by different departments.

Price Optimisation system – Using this system, Pavestone can determine how demand

of goods will fluctuate with different price rates and formulate strategies accordingly. As this

system of accounting consider various factors like category goals, competitors price strategy and

product life cycle (Christ and Burritt, 2013). Therefore, it is used in controlling the price of

different resources of a company, a firm can decide price of multiple products in a single time

period. Along with this, it also aid in deciding price structure for initial and promotional pricing

strategies.

Inventory management system – This type of accounting system is concerned with

management and supervision of stock. It also helps in tracking availability of company's stock

and non-capitalised assets. Henceforth, integrating this system with organisational process,

Pavestone can achieve effective and efficient flow of inventory. Inventory management system

includes many methods like– FIFO, LIFO and weighted average. This firm follows FIFO

inventory management system under which valuation is done by selling those products which are

manufactured first. Along with this, management of inventory in both monetarily and physical

manner, gives various advantages like cost reduction. All these processes help in forecasting and

replenishing strategies which aids Pavestone in advance management and planning of cost

requirement.

P2 Different methods of management accounting reporting

Accounting report is considered as crucial part of organisations which depicts a complete

picture how business is performing. As in small and medium sized companies every pound is

counted therefore, keeping an eye on bottom line is essential for review process (Banerjee,

2012). In this regard, managerial accounting report provide the information related to trim cost.

There are several methods of management accounting reports which assist Pavestone to develop

on regular basis as stated below:-

Budget Report: This report assist small companies like Pavestone in analysing

performance of business, different departments and controlling costs as well. Managers can also

use this budget report in providing incentives to workers on the basis of performance. As

2

process costing. Job order costing accumulates cost of manufacturing separately for each job.

While process costing accumulates the same for each process. Therefore, both methods help in

getting participation and cooperation of executives required by different departments.

Price Optimisation system – Using this system, Pavestone can determine how demand

of goods will fluctuate with different price rates and formulate strategies accordingly. As this

system of accounting consider various factors like category goals, competitors price strategy and

product life cycle (Christ and Burritt, 2013). Therefore, it is used in controlling the price of

different resources of a company, a firm can decide price of multiple products in a single time

period. Along with this, it also aid in deciding price structure for initial and promotional pricing

strategies.

Inventory management system – This type of accounting system is concerned with

management and supervision of stock. It also helps in tracking availability of company's stock

and non-capitalised assets. Henceforth, integrating this system with organisational process,

Pavestone can achieve effective and efficient flow of inventory. Inventory management system

includes many methods like– FIFO, LIFO and weighted average. This firm follows FIFO

inventory management system under which valuation is done by selling those products which are

manufactured first. Along with this, management of inventory in both monetarily and physical

manner, gives various advantages like cost reduction. All these processes help in forecasting and

replenishing strategies which aids Pavestone in advance management and planning of cost

requirement.

P2 Different methods of management accounting reporting

Accounting report is considered as crucial part of organisations which depicts a complete

picture how business is performing. As in small and medium sized companies every pound is

counted therefore, keeping an eye on bottom line is essential for review process (Banerjee,

2012). In this regard, managerial accounting report provide the information related to trim cost.

There are several methods of management accounting reports which assist Pavestone to develop

on regular basis as stated below:-

Budget Report: This report assist small companies like Pavestone in analysing

performance of business, different departments and controlling costs as well. Managers can also

use this budget report in providing incentives to workers on the basis of performance. As

2

estimated budget for a particular period is mostly based on actual performance of past record.

Therefore, if budget goes over and Pavestone is not in condition to trim cost then future budget

also not increases in order to meet specific goals. Thus, in such case it is necessary for

management to control cost of products.

Job Cost Report: This report shows expenses for a particular product which is financed

by small companies. Through this information, managers of Pavestone can evaluate profitability

of certain type of jobs as well as optimise operations also. Since this firm deals in manufacturing

sector which supply a range of materials such as stones and concrete to other construction

companies (Nahar and Yaacob, 2011). Therefore, this kind of report helps in controlling extra

expenses and reducing wastage of production also.

Accounts Receivable Aging Report: It is a critical tool used for managing business of a

company and estimating potential bad debts. Information regarding to bad debts generally used

to revise adjustment for doubtful accounts also. Thus, using this report, managers of Pavestone

can evaluate a list of customer invoices or which invoices are overdue for payment. Along with

this, credit department of this firm use aging report to analyse the current payment status related

to outstanding invoices. It will aid in determining if credit limit of customers are required to be

changed or not.

M1 Advantage of applications of management accounting system

System Advantages

Cost Accounting System This method management and accounting helps

Pavestone in meeting requirement of customers

as well as gives various techniques for

ascertaining the cost of products.

Price Optimisation System This system assists Pavestone in determining

price strategy of products at different level.

Inventory Management System Integrating this accounting system, Pavestone

can achieve appropriate inventory

management.

3

Therefore, if budget goes over and Pavestone is not in condition to trim cost then future budget

also not increases in order to meet specific goals. Thus, in such case it is necessary for

management to control cost of products.

Job Cost Report: This report shows expenses for a particular product which is financed

by small companies. Through this information, managers of Pavestone can evaluate profitability

of certain type of jobs as well as optimise operations also. Since this firm deals in manufacturing

sector which supply a range of materials such as stones and concrete to other construction

companies (Nahar and Yaacob, 2011). Therefore, this kind of report helps in controlling extra

expenses and reducing wastage of production also.

Accounts Receivable Aging Report: It is a critical tool used for managing business of a

company and estimating potential bad debts. Information regarding to bad debts generally used

to revise adjustment for doubtful accounts also. Thus, using this report, managers of Pavestone

can evaluate a list of customer invoices or which invoices are overdue for payment. Along with

this, credit department of this firm use aging report to analyse the current payment status related

to outstanding invoices. It will aid in determining if credit limit of customers are required to be

changed or not.

M1 Advantage of applications of management accounting system

System Advantages

Cost Accounting System This method management and accounting helps

Pavestone in meeting requirement of customers

as well as gives various techniques for

ascertaining the cost of products.

Price Optimisation System This system assists Pavestone in determining

price strategy of products at different level.

Inventory Management System Integrating this accounting system, Pavestone

can achieve appropriate inventory

management.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

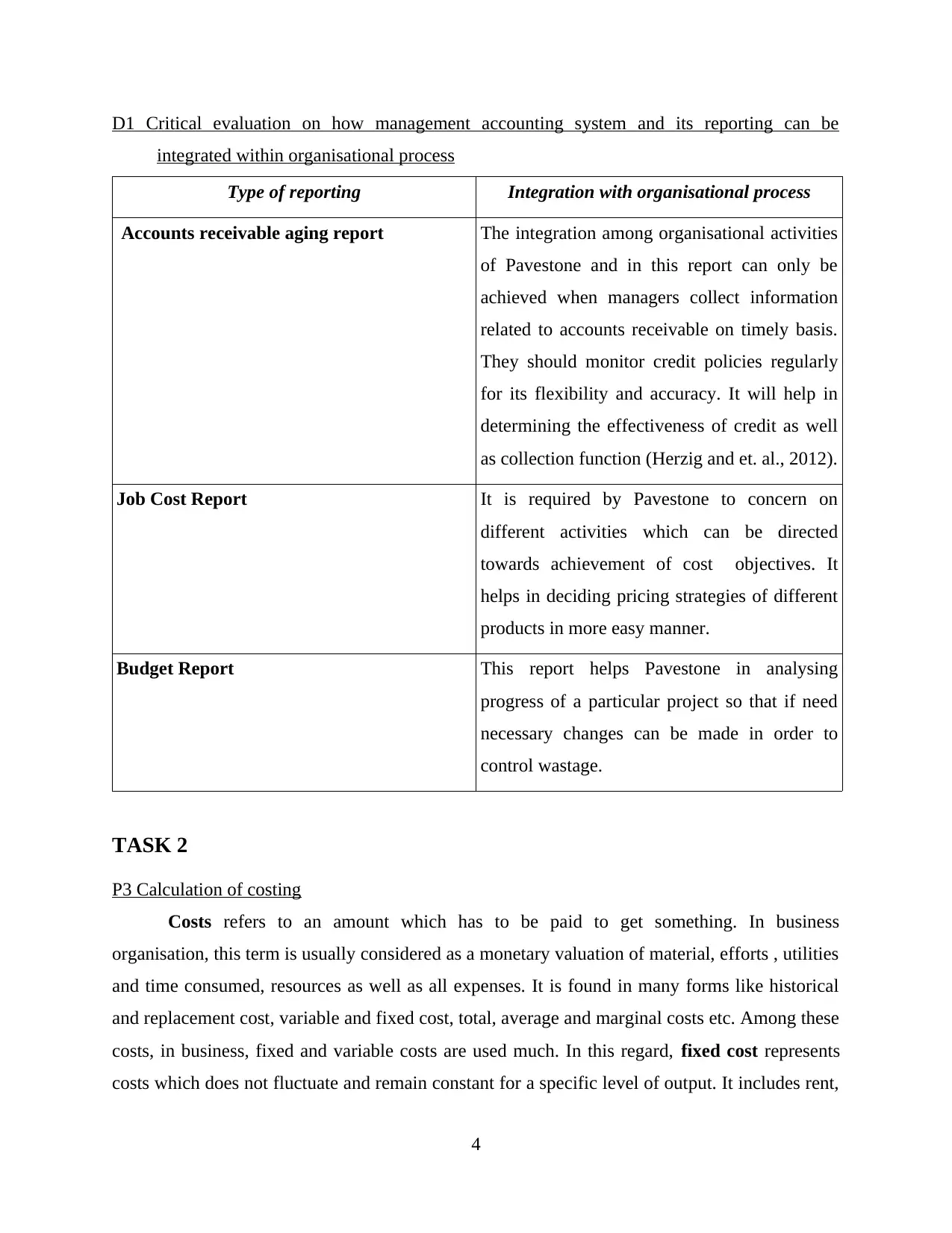

D1 Critical evaluation on how management accounting system and its reporting can be

integrated within organisational process

Type of reporting Integration with organisational process

Accounts receivable aging report The integration among organisational activities

of Pavestone and in this report can only be

achieved when managers collect information

related to accounts receivable on timely basis.

They should monitor credit policies regularly

for its flexibility and accuracy. It will help in

determining the effectiveness of credit as well

as collection function (Herzig and et. al., 2012).

Job Cost Report It is required by Pavestone to concern on

different activities which can be directed

towards achievement of cost objectives. It

helps in deciding pricing strategies of different

products in more easy manner.

Budget Report This report helps Pavestone in analysing

progress of a particular project so that if need

necessary changes can be made in order to

control wastage.

TASK 2

P3 Calculation of costing

Costs refers to an amount which has to be paid to get something. In business

organisation, this term is usually considered as a monetary valuation of material, efforts , utilities

and time consumed, resources as well as all expenses. It is found in many forms like historical

and replacement cost, variable and fixed cost, total, average and marginal costs etc. Among these

costs, in business, fixed and variable costs are used much. In this regard, fixed cost represents

costs which does not fluctuate and remain constant for a specific level of output. It includes rent,

4

integrated within organisational process

Type of reporting Integration with organisational process

Accounts receivable aging report The integration among organisational activities

of Pavestone and in this report can only be

achieved when managers collect information

related to accounts receivable on timely basis.

They should monitor credit policies regularly

for its flexibility and accuracy. It will help in

determining the effectiveness of credit as well

as collection function (Herzig and et. al., 2012).

Job Cost Report It is required by Pavestone to concern on

different activities which can be directed

towards achievement of cost objectives. It

helps in deciding pricing strategies of different

products in more easy manner.

Budget Report This report helps Pavestone in analysing

progress of a particular project so that if need

necessary changes can be made in order to

control wastage.

TASK 2

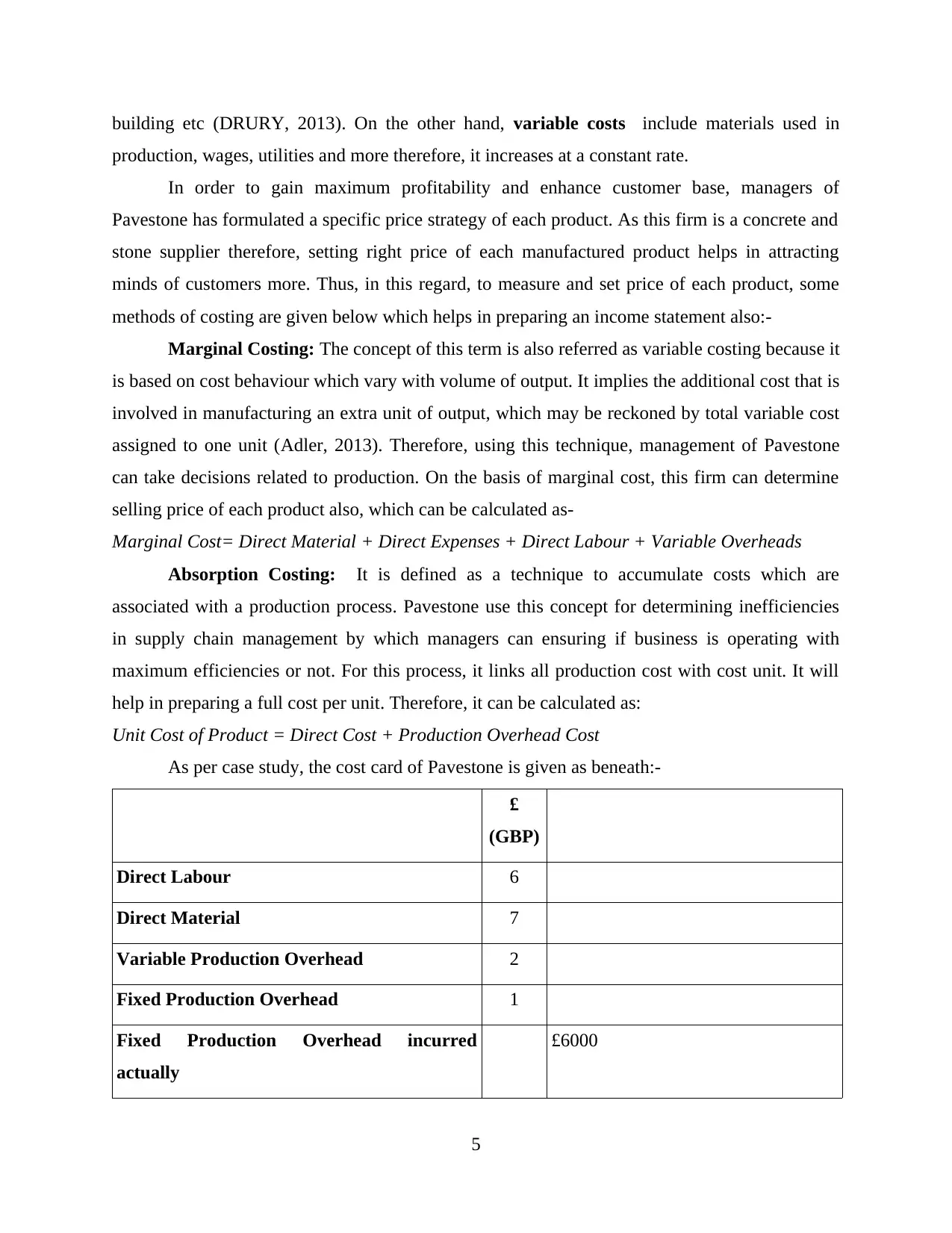

P3 Calculation of costing

Costs refers to an amount which has to be paid to get something. In business

organisation, this term is usually considered as a monetary valuation of material, efforts , utilities

and time consumed, resources as well as all expenses. It is found in many forms like historical

and replacement cost, variable and fixed cost, total, average and marginal costs etc. Among these

costs, in business, fixed and variable costs are used much. In this regard, fixed cost represents

costs which does not fluctuate and remain constant for a specific level of output. It includes rent,

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

building etc (DRURY, 2013). On the other hand, variable costs include materials used in

production, wages, utilities and more therefore, it increases at a constant rate.

In order to gain maximum profitability and enhance customer base, managers of

Pavestone has formulated a specific price strategy of each product. As this firm is a concrete and

stone supplier therefore, setting right price of each manufactured product helps in attracting

minds of customers more. Thus, in this regard, to measure and set price of each product, some

methods of costing are given below which helps in preparing an income statement also:-

Marginal Costing: The concept of this term is also referred as variable costing because it

is based on cost behaviour which vary with volume of output. It implies the additional cost that is

involved in manufacturing an extra unit of output, which may be reckoned by total variable cost

assigned to one unit (Adler, 2013). Therefore, using this technique, management of Pavestone

can take decisions related to production. On the basis of marginal cost, this firm can determine

selling price of each product also, which can be calculated as-

Marginal Cost= Direct Material + Direct Expenses + Direct Labour + Variable Overheads

Absorption Costing: It is defined as a technique to accumulate costs which are

associated with a production process. Pavestone use this concept for determining inefficiencies

in supply chain management by which managers can ensuring if business is operating with

maximum efficiencies or not. For this process, it links all production cost with cost unit. It will

help in preparing a full cost per unit. Therefore, it can be calculated as:

Unit Cost of Product = Direct Cost + Production Overhead Cost

As per case study, the cost card of Pavestone is given as beneath:-

£

(GBP)

Direct Labour 6

Direct Material 7

Variable Production Overhead 2

Fixed Production Overhead 1

Fixed Production Overhead incurred

actually

£6000

5

production, wages, utilities and more therefore, it increases at a constant rate.

In order to gain maximum profitability and enhance customer base, managers of

Pavestone has formulated a specific price strategy of each product. As this firm is a concrete and

stone supplier therefore, setting right price of each manufactured product helps in attracting

minds of customers more. Thus, in this regard, to measure and set price of each product, some

methods of costing are given below which helps in preparing an income statement also:-

Marginal Costing: The concept of this term is also referred as variable costing because it

is based on cost behaviour which vary with volume of output. It implies the additional cost that is

involved in manufacturing an extra unit of output, which may be reckoned by total variable cost

assigned to one unit (Adler, 2013). Therefore, using this technique, management of Pavestone

can take decisions related to production. On the basis of marginal cost, this firm can determine

selling price of each product also, which can be calculated as-

Marginal Cost= Direct Material + Direct Expenses + Direct Labour + Variable Overheads

Absorption Costing: It is defined as a technique to accumulate costs which are

associated with a production process. Pavestone use this concept for determining inefficiencies

in supply chain management by which managers can ensuring if business is operating with

maximum efficiencies or not. For this process, it links all production cost with cost unit. It will

help in preparing a full cost per unit. Therefore, it can be calculated as:

Unit Cost of Product = Direct Cost + Production Overhead Cost

As per case study, the cost card of Pavestone is given as beneath:-

£

(GBP)

Direct Labour 6

Direct Material 7

Variable Production Overhead 2

Fixed Production Overhead 1

Fixed Production Overhead incurred

actually

£6000

5

Variable selling & distribution expenses 30% of sales value

Selling Price 55

Sales 20000

Working Notes:

Formula of marginal costing:

sales revenue – marginal cost of goods sold = contribution – fixed cost = net income

Particulars Amount

Sales revenue = (selling price * no. of goods sold = 55 * 600) 33000

Marginal Cost of goods sold: 9600

Production = (units produced * marginal cost per unit = 800 * 16) 12800

closing stock = (closing stock units * marginal cost per unit = 200 *

16) 3200

Contribution 23400

Fixed cost ( 3200+1200+1500 ) 5900

Net profit 17500

Formula of absorption costing:

Net Profit = (Sales revenue) – (Cost of goods sold) = (Gross profit – Selling and

Administrative expenses)

Particulars Amount

Sales = (selling price * no. of units sold = 55 * 600) 33000

Cost of goods sold = (total expenses per unit * actual sales = 23.375 * 600) 14025

6

Selling Price 55

Sales 20000

Working Notes:

Formula of marginal costing:

sales revenue – marginal cost of goods sold = contribution – fixed cost = net income

Particulars Amount

Sales revenue = (selling price * no. of goods sold = 55 * 600) 33000

Marginal Cost of goods sold: 9600

Production = (units produced * marginal cost per unit = 800 * 16) 12800

closing stock = (closing stock units * marginal cost per unit = 200 *

16) 3200

Contribution 23400

Fixed cost ( 3200+1200+1500 ) 5900

Net profit 17500

Formula of absorption costing:

Net Profit = (Sales revenue) – (Cost of goods sold) = (Gross profit – Selling and

Administrative expenses)

Particulars Amount

Sales = (selling price * no. of units sold = 55 * 600) 33000

Cost of goods sold = (total expenses per unit * actual sales = 23.375 * 600) 14025

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Gross profit 18975

Selling & Administrative expenses = (variable sales overhead * actual sales +

selling and administrative cost = 1 * 600 + 2700) 3300

Net profit/ operating income 15675

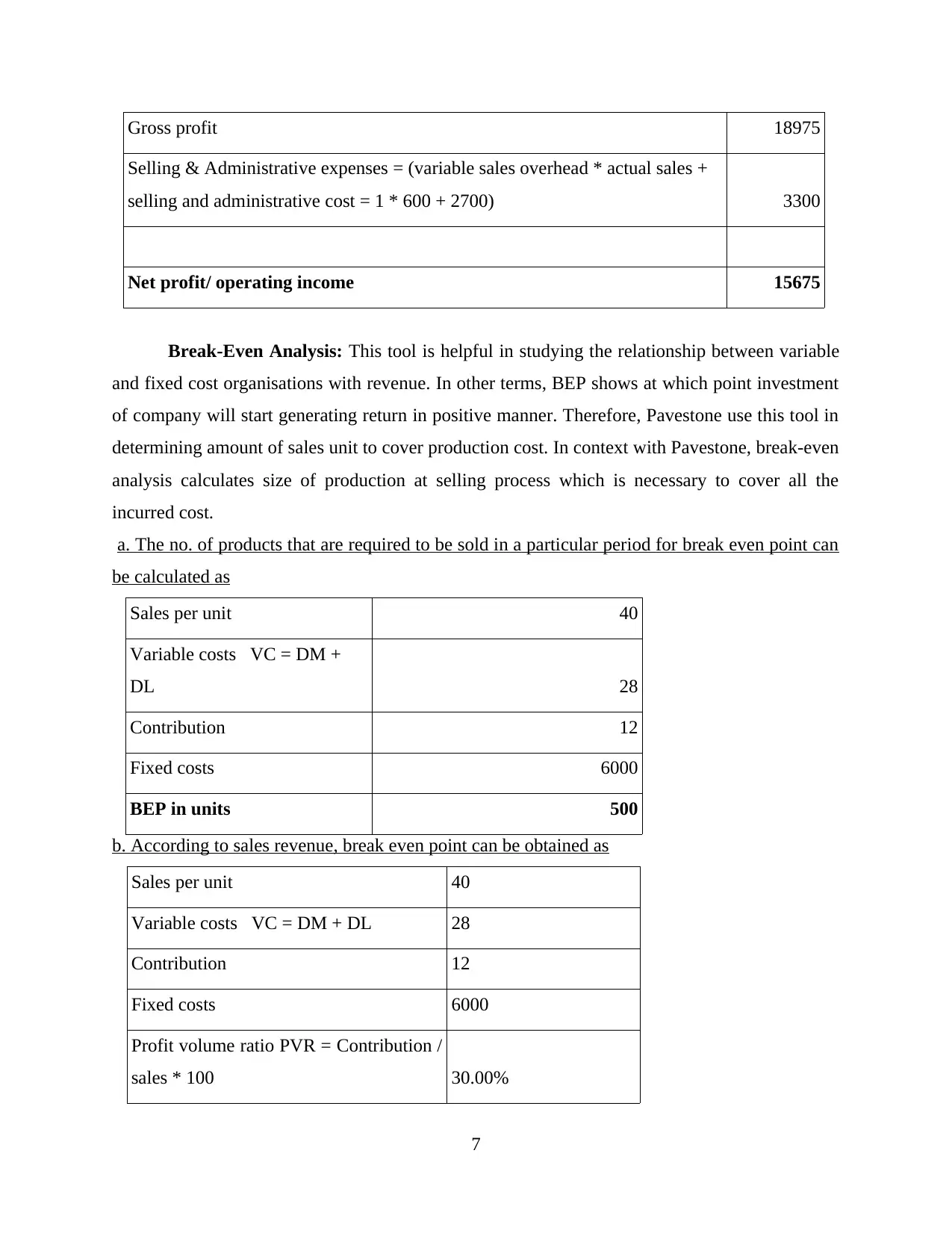

Break-Even Analysis: This tool is helpful in studying the relationship between variable

and fixed cost organisations with revenue. In other terms, BEP shows at which point investment

of company will start generating return in positive manner. Therefore, Pavestone use this tool in

determining amount of sales unit to cover production cost. In context with Pavestone, break-even

analysis calculates size of production at selling process which is necessary to cover all the

incurred cost.

a. The no. of products that are required to be sold in a particular period for break even point can

be calculated as

Sales per unit 40

Variable costs VC = DM +

DL 28

Contribution 12

Fixed costs 6000

BEP in units 500

b. According to sales revenue, break even point can be obtained as

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

Profit volume ratio PVR = Contribution /

sales * 100 30.00%

7

Selling & Administrative expenses = (variable sales overhead * actual sales +

selling and administrative cost = 1 * 600 + 2700) 3300

Net profit/ operating income 15675

Break-Even Analysis: This tool is helpful in studying the relationship between variable

and fixed cost organisations with revenue. In other terms, BEP shows at which point investment

of company will start generating return in positive manner. Therefore, Pavestone use this tool in

determining amount of sales unit to cover production cost. In context with Pavestone, break-even

analysis calculates size of production at selling process which is necessary to cover all the

incurred cost.

a. The no. of products that are required to be sold in a particular period for break even point can

be calculated as

Sales per unit 40

Variable costs VC = DM +

DL 28

Contribution 12

Fixed costs 6000

BEP in units 500

b. According to sales revenue, break even point can be obtained as

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

Profit volume ratio PVR = Contribution /

sales * 100 30.00%

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

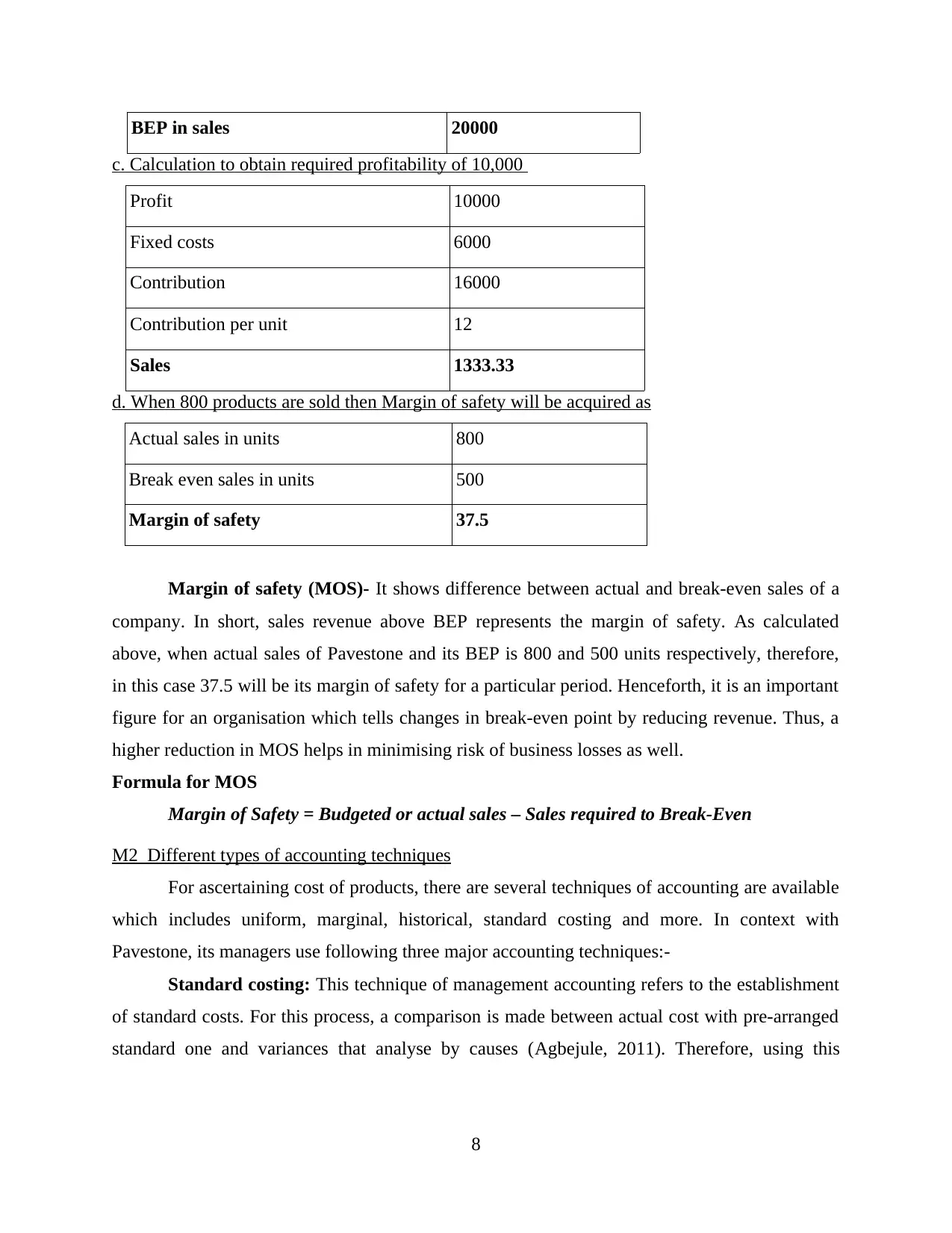

BEP in sales 20000

c. Calculation to obtain required profitability of 10,000

Profit 10000

Fixed costs 6000

Contribution 16000

Contribution per unit 12

Sales 1333.33

d. When 800 products are sold then Margin of safety will be acquired as

Actual sales in units 800

Break even sales in units 500

Margin of safety 37.5

Margin of safety (MOS)- It shows difference between actual and break-even sales of a

company. In short, sales revenue above BEP represents the margin of safety. As calculated

above, when actual sales of Pavestone and its BEP is 800 and 500 units respectively, therefore,

in this case 37.5 will be its margin of safety for a particular period. Henceforth, it is an important

figure for an organisation which tells changes in break-even point by reducing revenue. Thus, a

higher reduction in MOS helps in minimising risk of business losses as well.

Formula for MOS

Margin of Safety = Budgeted or actual sales – Sales required to Break-Even

M2 Different types of accounting techniques

For ascertaining cost of products, there are several techniques of accounting are available

which includes uniform, marginal, historical, standard costing and more. In context with

Pavestone, its managers use following three major accounting techniques:-

Standard costing: This technique of management accounting refers to the establishment

of standard costs. For this process, a comparison is made between actual cost with pre-arranged

standard one and variances that analyse by causes (Agbejule, 2011). Therefore, using this

8

c. Calculation to obtain required profitability of 10,000

Profit 10000

Fixed costs 6000

Contribution 16000

Contribution per unit 12

Sales 1333.33

d. When 800 products are sold then Margin of safety will be acquired as

Actual sales in units 800

Break even sales in units 500

Margin of safety 37.5

Margin of safety (MOS)- It shows difference between actual and break-even sales of a

company. In short, sales revenue above BEP represents the margin of safety. As calculated

above, when actual sales of Pavestone and its BEP is 800 and 500 units respectively, therefore,

in this case 37.5 will be its margin of safety for a particular period. Henceforth, it is an important

figure for an organisation which tells changes in break-even point by reducing revenue. Thus, a

higher reduction in MOS helps in minimising risk of business losses as well.

Formula for MOS

Margin of Safety = Budgeted or actual sales – Sales required to Break-Even

M2 Different types of accounting techniques

For ascertaining cost of products, there are several techniques of accounting are available

which includes uniform, marginal, historical, standard costing and more. In context with

Pavestone, its managers use following three major accounting techniques:-

Standard costing: This technique of management accounting refers to the establishment

of standard costs. For this process, a comparison is made between actual cost with pre-arranged

standard one and variances that analyse by causes (Agbejule, 2011). Therefore, using this

8

technique, Pavestone can investigate adverse reasons which causes variances and take remedial

actions accordingly so that such things will not happen again.

Marginal costing: It refers to ascertainment of marginal cost which analyse by

differentiating variable and fixed cost. Management accountant of Pavestone use this technique

of accounting for controlling cost and taking appropriate decisions related to production. It will

help in maximising profitability of business during a financial period.

D2 Data interpretation

Interpretation of Data:

It has interpreted from above data that both techniques of accounting management via

absorption and marginal costs, use different-different methods to calculate the estimated unit cost

of product. In this process, fixed cost has been totally written off in marginal costing to

contribution. While, all cost has been utilised properly in absorption costing. Therefore, for

Pavestone, net operating income as per marginal costing comes out to be £17500 whereas

absorption technique obtains £15675. This indicates that Pavestone has encountered with a

significant growth in terms of revenue. Along with this, by the technique of BEP analysis, it has

interpreted that in order to reach a break-even point which is 20,000, company requires to sell

500 units.

TASK 3

P4 Budgetary control and different types of planning tool and their advantages and disadvantages

used in budgetary control

Budgetary control refers to a financial process, which is used to manage income and

control expenditures. In this regard, management of Pavestone used various tools to plan manage

and forecast budget of company. Currently this enterprise wants to expand its business market in

another locations of UK. Therefore, preparation of budget in systematic manner help this firm in

achievement of its targeted objectives and goals in set period of time (Ramljak and Rogošić,

2012). For this process, its managers use online budgeting tools which provide many options for

managing budgets in an organised and streamlined way.

Types of planning tools for budgetary control:

One of the best advantage of use budgetary control is to gain opportunity by which a

company can move forward and keep business on track. It helps in getting success in business.

9

actions accordingly so that such things will not happen again.

Marginal costing: It refers to ascertainment of marginal cost which analyse by

differentiating variable and fixed cost. Management accountant of Pavestone use this technique

of accounting for controlling cost and taking appropriate decisions related to production. It will

help in maximising profitability of business during a financial period.

D2 Data interpretation

Interpretation of Data:

It has interpreted from above data that both techniques of accounting management via

absorption and marginal costs, use different-different methods to calculate the estimated unit cost

of product. In this process, fixed cost has been totally written off in marginal costing to

contribution. While, all cost has been utilised properly in absorption costing. Therefore, for

Pavestone, net operating income as per marginal costing comes out to be £17500 whereas

absorption technique obtains £15675. This indicates that Pavestone has encountered with a

significant growth in terms of revenue. Along with this, by the technique of BEP analysis, it has

interpreted that in order to reach a break-even point which is 20,000, company requires to sell

500 units.

TASK 3

P4 Budgetary control and different types of planning tool and their advantages and disadvantages

used in budgetary control

Budgetary control refers to a financial process, which is used to manage income and

control expenditures. In this regard, management of Pavestone used various tools to plan manage

and forecast budget of company. Currently this enterprise wants to expand its business market in

another locations of UK. Therefore, preparation of budget in systematic manner help this firm in

achievement of its targeted objectives and goals in set period of time (Ramljak and Rogošić,

2012). For this process, its managers use online budgeting tools which provide many options for

managing budgets in an organised and streamlined way.

Types of planning tools for budgetary control:

One of the best advantage of use budgetary control is to gain opportunity by which a

company can move forward and keep business on track. It helps in getting success in business.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.