Management Accounting Report: Financial Analysis for Pearson Education

VerifiedAdded on 2021/02/18

|14

|4557

|397

Report

AI Summary

This report provides a comprehensive overview of management accounting, focusing on techniques, financial analysis, and practical applications within Pearson Education. It begins with an introduction to management accounting, outlining its core functions and benefits, followed by an in-depth exploration of various management accounting systems, including inventory management, cost accounting, and price optimization. The report then delves into the presentation of financial information, detailing methods such as balance sheets, income statements, and cash flow statements, along with different types of management accounting reporting. Furthermore, it examines microeconomic techniques like cost analysis, cost variances, marginal costing, and absorption costing. Through detailed financial data and analysis, the report illustrates how these techniques can be applied to assess performance, make informed decisions, and address financial challenges. The conclusion summarizes the key findings, highlighting the importance of management accounting in achieving business goals and objectives. This report is designed to provide students with a solid understanding of management accounting principles and their practical application in a real-world business context.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

LO1 Understanding of management accounting systems ..............................................................1

Evaluate the range of management accounting techniques.........................................................1

Presenting financial information..................................................................................................2

LO2 Range of management accounting techniques .......................................................................4

Microeconomic techniques..........................................................................................................4

Product costing.............................................................................................................................8

Cost of inventory..........................................................................................................................8

LO3 Explain the use of planning tools in management accounting ...............................................8

Use of budget for planning & controlling....................................................................................8

Pricing Strategies.........................................................................................................................9

Common costing systems............................................................................................................9

LO4 Compare how organization respond to their financial problems by using management

accounting systems ......................................................................................................................10

Identify financial problems........................................................................................................10

CONCLUSION .............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

LO1 Understanding of management accounting systems ..............................................................1

Evaluate the range of management accounting techniques.........................................................1

Presenting financial information..................................................................................................2

LO2 Range of management accounting techniques .......................................................................4

Microeconomic techniques..........................................................................................................4

Product costing.............................................................................................................................8

Cost of inventory..........................................................................................................................8

LO3 Explain the use of planning tools in management accounting ...............................................8

Use of budget for planning & controlling....................................................................................8

Pricing Strategies.........................................................................................................................9

Common costing systems............................................................................................................9

LO4 Compare how organization respond to their financial problems by using management

accounting systems ......................................................................................................................10

Identify financial problems........................................................................................................10

CONCLUSION .............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION

Management accounting is the process of managing business operations and all the

relevant activities as well. It include various functions which helps the manager to gather

information and used in producing financial statement that used by stakeholders for further

decision making process (Bebbington, Unerman and , 2014). For the better understanding of this

concept, this report based on Pearson Education which is world's leading company over 40,000

employees and it operated more than 70 countries. This report cover various topics such as

concept of management accounting, its benefits and essential requirement in the organization to

achieve business goals & objectives.

Different methods of accounting reporting and it further used to produce budget for

budgetary control. In addition, it include costing methods which helps in calculating net profit of

the year. Along with this, identify financial problem which impact production as well as

profitability and analyse how accounting systems helps in resolving these issues.

MAIN BODY

LO1 Understanding of management accounting systems

Evaluate the range of management accounting techniques

Management accounting: It is also called managerial accounting which helps the

business through providing financial information and other resources in order to make decisions

(Boučková, 2015). It is used for internal analysis which make it different from financial

accounting and its main objectives is to take accurate decision and control over the business

activities.

Different types of management accounting systems:

Inventory management system: It is an combination of technology (software as well as

hardware) where it helps the manager to monitor or control inventory level. In order to

manufacture products of manage clients information they have to use this system which provide

them accurate information. It will be beneficial for decision making process and there are three

types of inventory management system such as LIFO, FIFO or AVCO. Pearson use FIFO system

to manage their inventory. It is essentially required by the company to minimise their workload

because it is very complex to physically manage all data and regular monitoring as well.

1

Management accounting is the process of managing business operations and all the

relevant activities as well. It include various functions which helps the manager to gather

information and used in producing financial statement that used by stakeholders for further

decision making process (Bebbington, Unerman and , 2014). For the better understanding of this

concept, this report based on Pearson Education which is world's leading company over 40,000

employees and it operated more than 70 countries. This report cover various topics such as

concept of management accounting, its benefits and essential requirement in the organization to

achieve business goals & objectives.

Different methods of accounting reporting and it further used to produce budget for

budgetary control. In addition, it include costing methods which helps in calculating net profit of

the year. Along with this, identify financial problem which impact production as well as

profitability and analyse how accounting systems helps in resolving these issues.

MAIN BODY

LO1 Understanding of management accounting systems

Evaluate the range of management accounting techniques

Management accounting: It is also called managerial accounting which helps the

business through providing financial information and other resources in order to make decisions

(Boučková, 2015). It is used for internal analysis which make it different from financial

accounting and its main objectives is to take accurate decision and control over the business

activities.

Different types of management accounting systems:

Inventory management system: It is an combination of technology (software as well as

hardware) where it helps the manager to monitor or control inventory level. In order to

manufacture products of manage clients information they have to use this system which provide

them accurate information. It will be beneficial for decision making process and there are three

types of inventory management system such as LIFO, FIFO or AVCO. Pearson use FIFO system

to manage their inventory. It is essentially required by the company to minimise their workload

because it is very complex to physically manage all data and regular monitoring as well.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cost accounting system: This framework used by organization to estimate overall

product cost and it further beneficial in inventory valuation, cost control or profit analysis. It is

essentially required to identify which product are profitable which one is not. There two main

costing systems such as job order costing and process costing. Pearson can use any one costing

system to estimate their product cost which further help manager to formulate strategies in

respect of organization.

Price optimising system: This system help the manager to determine that how demand

will impact the price level of product. It is used to set price for the different segment of

customers (Carlsson-Wall, Kraus and Lind, 2015). It help the manager of Pearson to measure

customer behaviour regarding their price policy. They try to minimise product cost which

increase profit margin and helps in achieving business gaols & objectives. It required for develop

price, promotion strategy, forecast demand etc.

Benefits of management accounting systems:

Accounting systems Benefits

Inventory management

system

This software provide centralised database facility which helps

the manager of Pearson to access information anytime and

make effective decision accordingly. It will enhance

transparency, reduce labour or carrying cost, improve cash flow

etc.

Price optimization system In context of Pearson, this system help business to analyse

customer behaviour on different price range of products

(Chenhall and Moers, 2015). It help the manager to focus on

key areas such as margin of sales.

Cost accounting system It helps the manager of Pearson to estimate their product cost

and further they try to minimise their cost through regular

review. It helps in fixing product price, improve efficiency,

control over material etc.

Presenting financial information

Explain the methods which used in presenting financial information:

2

product cost and it further beneficial in inventory valuation, cost control or profit analysis. It is

essentially required to identify which product are profitable which one is not. There two main

costing systems such as job order costing and process costing. Pearson can use any one costing

system to estimate their product cost which further help manager to formulate strategies in

respect of organization.

Price optimising system: This system help the manager to determine that how demand

will impact the price level of product. It is used to set price for the different segment of

customers (Carlsson-Wall, Kraus and Lind, 2015). It help the manager of Pearson to measure

customer behaviour regarding their price policy. They try to minimise product cost which

increase profit margin and helps in achieving business gaols & objectives. It required for develop

price, promotion strategy, forecast demand etc.

Benefits of management accounting systems:

Accounting systems Benefits

Inventory management

system

This software provide centralised database facility which helps

the manager of Pearson to access information anytime and

make effective decision accordingly. It will enhance

transparency, reduce labour or carrying cost, improve cash flow

etc.

Price optimization system In context of Pearson, this system help business to analyse

customer behaviour on different price range of products

(Chenhall and Moers, 2015). It help the manager to focus on

key areas such as margin of sales.

Cost accounting system It helps the manager of Pearson to estimate their product cost

and further they try to minimise their cost through regular

review. It helps in fixing product price, improve efficiency,

control over material etc.

Presenting financial information

Explain the methods which used in presenting financial information:

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

There are various methods which helps the organization to present financial information

for stakeholder analysis. Some of it discussed below:

Balance sheet: In this statement, assets and liabilities of the company recorded and make

sure that it will be balanced. With the help of it, organization able to identify financial

position of company and liquidity as well.

Income statement: This statement include all the expenditures or revenues which related

to the business operations. It help the manager to analyse that operations are profit

making or not.

Cash flow statement: In this statement, accountant record inflow or outflow of cash

from various activities such as operating, financial or inventing. It helps in categorising

inflow or outflow according to the task which further helps the manager to formulate

strategies.

Different types of management accounting reporting:

Performance reports: This report used to review performance of individual as well as

entire organization. With the help of departmental report, manager able to analyse their

performance and compare with others in order to measure improvement (Hiebl, 2014). Manager

of Pearson use this report for strategic decisions for the future. It further help in providing

reward or other incentives to the employees as per their performance.

Budget reports: Under this report manager produce policies and schemes which going to

follow at the time of performing individual task. Every organization develop overall budget

which specify the overall expenses for each task & activity. Manager of Pearson have to make

sure that, employees follow it properly try to perform under budget in order to maximise

productivity and profitability.

Cost managerial accounting reports: This report include all types of cost such as

material, labour, overheads etc. Cost report provide overall summary of expenses at the time of

performing business operations. In context of Pearson, with the help of this report manager

analyse the figures and build strategy to control cost over the production period.

Above mention reports used by the manager of Pearson in order to make effective

decision which helps in maximising profit through reducing cost and further helps in achieving

business goals & objectives.

3

for stakeholder analysis. Some of it discussed below:

Balance sheet: In this statement, assets and liabilities of the company recorded and make

sure that it will be balanced. With the help of it, organization able to identify financial

position of company and liquidity as well.

Income statement: This statement include all the expenditures or revenues which related

to the business operations. It help the manager to analyse that operations are profit

making or not.

Cash flow statement: In this statement, accountant record inflow or outflow of cash

from various activities such as operating, financial or inventing. It helps in categorising

inflow or outflow according to the task which further helps the manager to formulate

strategies.

Different types of management accounting reporting:

Performance reports: This report used to review performance of individual as well as

entire organization. With the help of departmental report, manager able to analyse their

performance and compare with others in order to measure improvement (Hiebl, 2014). Manager

of Pearson use this report for strategic decisions for the future. It further help in providing

reward or other incentives to the employees as per their performance.

Budget reports: Under this report manager produce policies and schemes which going to

follow at the time of performing individual task. Every organization develop overall budget

which specify the overall expenses for each task & activity. Manager of Pearson have to make

sure that, employees follow it properly try to perform under budget in order to maximise

productivity and profitability.

Cost managerial accounting reports: This report include all types of cost such as

material, labour, overheads etc. Cost report provide overall summary of expenses at the time of

performing business operations. In context of Pearson, with the help of this report manager

analyse the figures and build strategy to control cost over the production period.

Above mention reports used by the manager of Pearson in order to make effective

decision which helps in maximising profit through reducing cost and further helps in achieving

business goals & objectives.

3

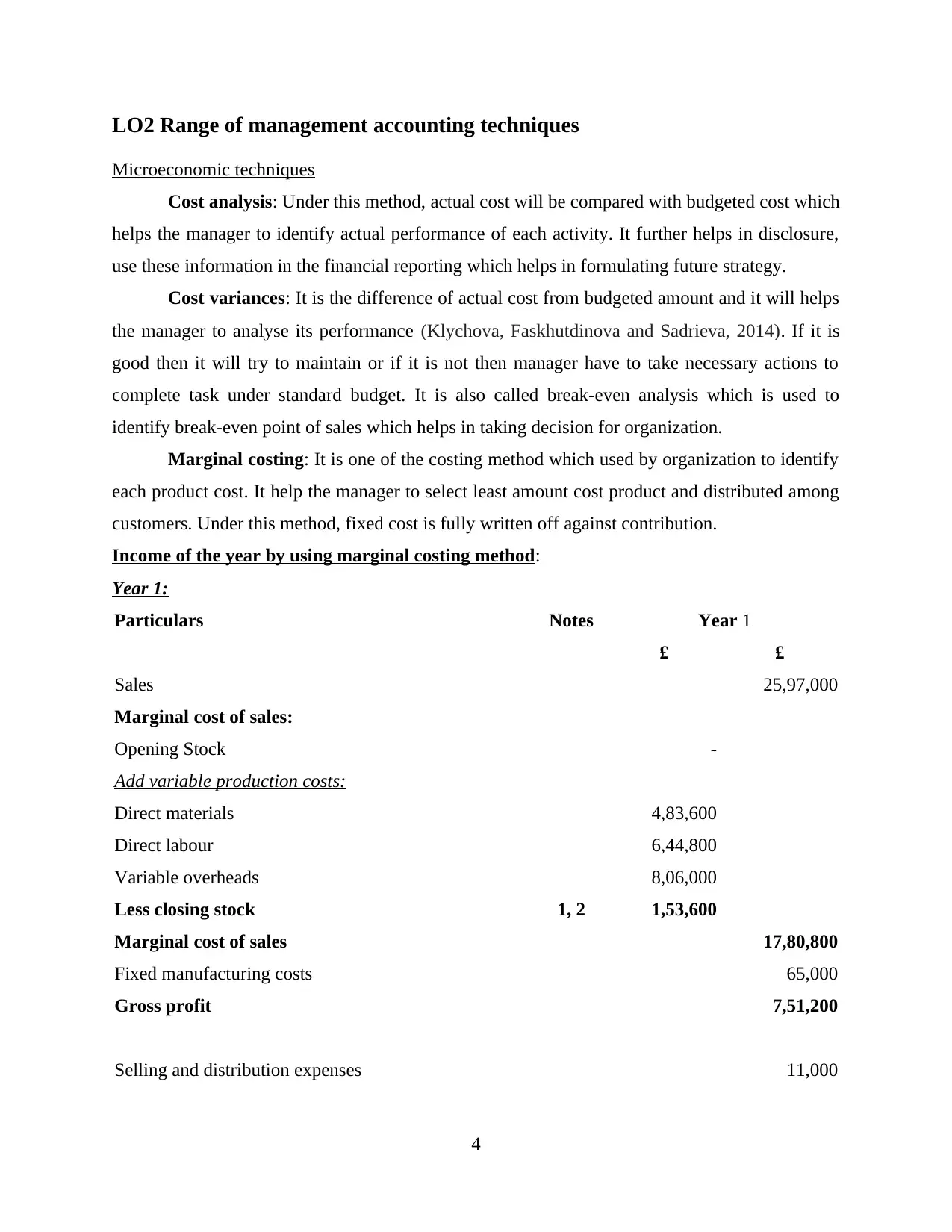

LO2 Range of management accounting techniques

Microeconomic techniques

Cost analysis: Under this method, actual cost will be compared with budgeted cost which

helps the manager to identify actual performance of each activity. It further helps in disclosure,

use these information in the financial reporting which helps in formulating future strategy.

Cost variances: It is the difference of actual cost from budgeted amount and it will helps

the manager to analyse its performance (Klychova, Faskhutdinova and Sadrieva, 2014). If it is

good then it will try to maintain or if it is not then manager have to take necessary actions to

complete task under standard budget. It is also called break-even analysis which is used to

identify break-even point of sales which helps in taking decision for organization.

Marginal costing: It is one of the costing method which used by organization to identify

each product cost. It help the manager to select least amount cost product and distributed among

customers. Under this method, fixed cost is fully written off against contribution.

Income of the year by using marginal costing method:

Year 1:

Particulars Notes Year 1

£ £

Sales 25,97,000

Marginal cost of sales:

Opening Stock -

Add variable production costs:

Direct materials 4,83,600

Direct labour 6,44,800

Variable overheads 8,06,000

Less closing stock 1, 2 1,53,600

Marginal cost of sales 17,80,800

Fixed manufacturing costs 65,000

Gross profit 7,51,200

Selling and distribution expenses 11,000

4

Microeconomic techniques

Cost analysis: Under this method, actual cost will be compared with budgeted cost which

helps the manager to identify actual performance of each activity. It further helps in disclosure,

use these information in the financial reporting which helps in formulating future strategy.

Cost variances: It is the difference of actual cost from budgeted amount and it will helps

the manager to analyse its performance (Klychova, Faskhutdinova and Sadrieva, 2014). If it is

good then it will try to maintain or if it is not then manager have to take necessary actions to

complete task under standard budget. It is also called break-even analysis which is used to

identify break-even point of sales which helps in taking decision for organization.

Marginal costing: It is one of the costing method which used by organization to identify

each product cost. It help the manager to select least amount cost product and distributed among

customers. Under this method, fixed cost is fully written off against contribution.

Income of the year by using marginal costing method:

Year 1:

Particulars Notes Year 1

£ £

Sales 25,97,000

Marginal cost of sales:

Opening Stock -

Add variable production costs:

Direct materials 4,83,600

Direct labour 6,44,800

Variable overheads 8,06,000

Less closing stock 1, 2 1,53,600

Marginal cost of sales 17,80,800

Fixed manufacturing costs 65,000

Gross profit 7,51,200

Selling and distribution expenses 11,000

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

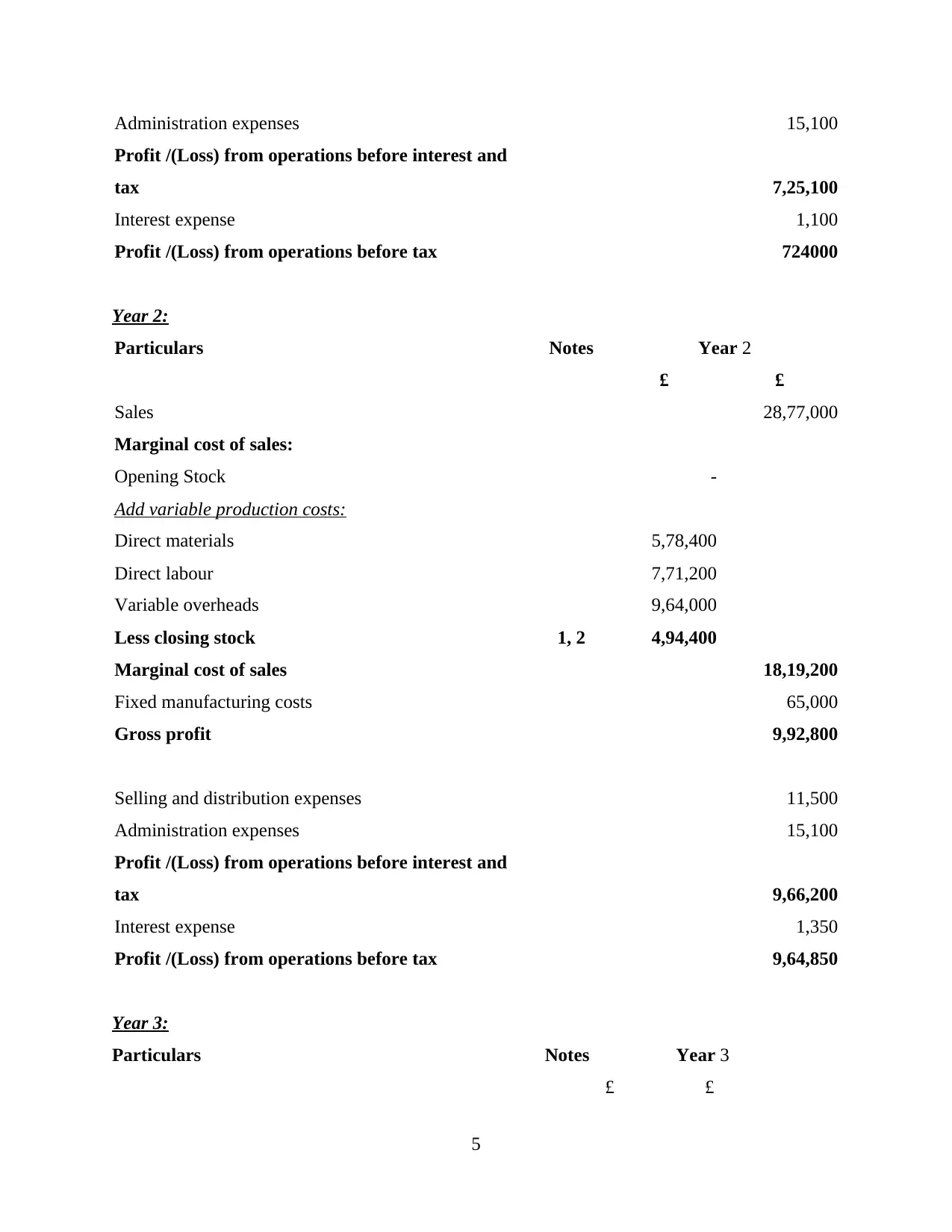

Administration expenses 15,100

Profit /(Loss) from operations before interest and

tax 7,25,100

Interest expense 1,100

Profit /(Loss) from operations before tax 724000

Year 2:

Particulars Notes Year 2

£ £

Sales 28,77,000

Marginal cost of sales:

Opening Stock -

Add variable production costs:

Direct materials 5,78,400

Direct labour 7,71,200

Variable overheads 9,64,000

Less closing stock 1, 2 4,94,400

Marginal cost of sales 18,19,200

Fixed manufacturing costs 65,000

Gross profit 9,92,800

Selling and distribution expenses 11,500

Administration expenses 15,100

Profit /(Loss) from operations before interest and

tax 9,66,200

Interest expense 1,350

Profit /(Loss) from operations before tax 9,64,850

Year 3:

Particulars Notes Year 3

£ £

5

Profit /(Loss) from operations before interest and

tax 7,25,100

Interest expense 1,100

Profit /(Loss) from operations before tax 724000

Year 2:

Particulars Notes Year 2

£ £

Sales 28,77,000

Marginal cost of sales:

Opening Stock -

Add variable production costs:

Direct materials 5,78,400

Direct labour 7,71,200

Variable overheads 9,64,000

Less closing stock 1, 2 4,94,400

Marginal cost of sales 18,19,200

Fixed manufacturing costs 65,000

Gross profit 9,92,800

Selling and distribution expenses 11,500

Administration expenses 15,100

Profit /(Loss) from operations before interest and

tax 9,66,200

Interest expense 1,350

Profit /(Loss) from operations before tax 9,64,850

Year 3:

Particulars Notes Year 3

£ £

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

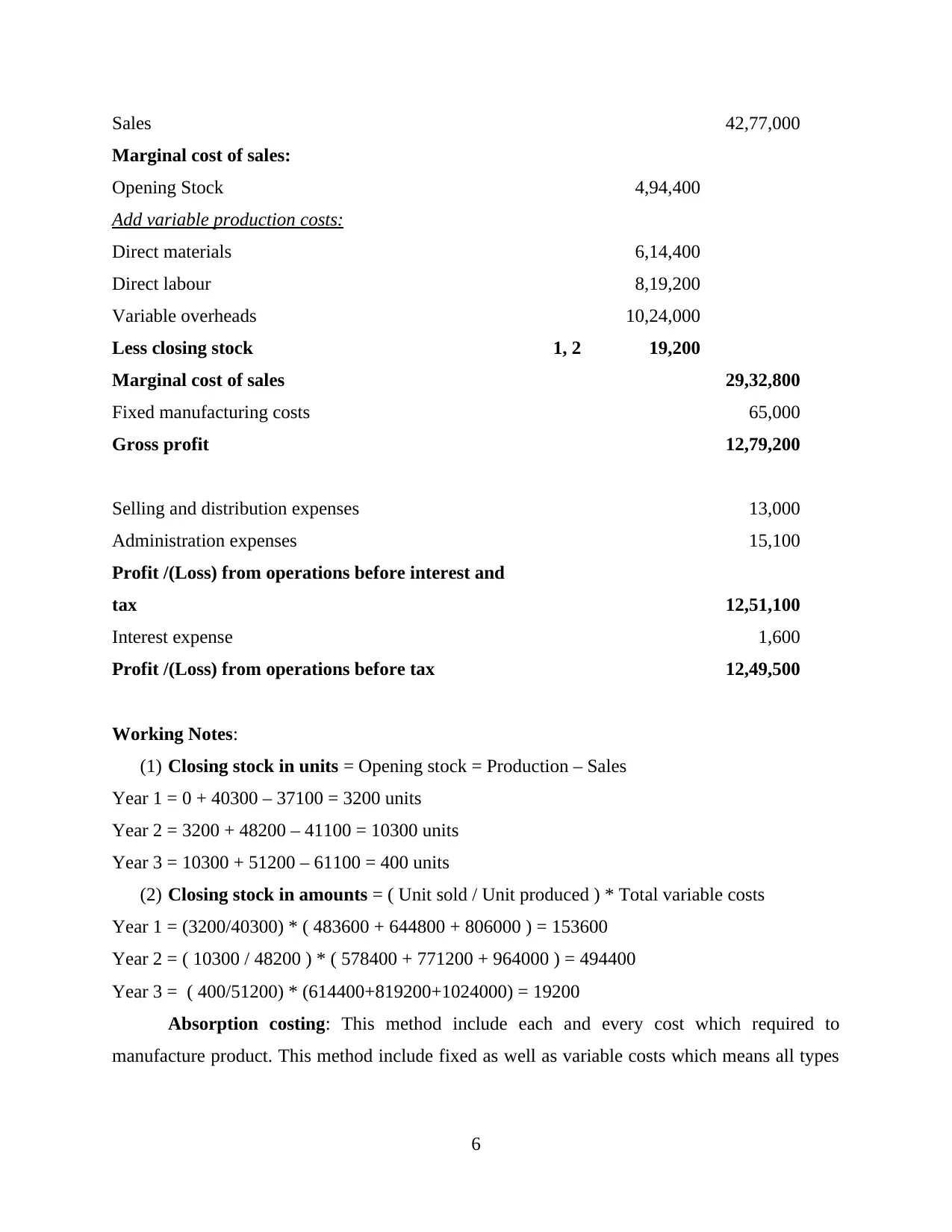

Sales 42,77,000

Marginal cost of sales:

Opening Stock 4,94,400

Add variable production costs:

Direct materials 6,14,400

Direct labour 8,19,200

Variable overheads 10,24,000

Less closing stock 1, 2 19,200

Marginal cost of sales 29,32,800

Fixed manufacturing costs 65,000

Gross profit 12,79,200

Selling and distribution expenses 13,000

Administration expenses 15,100

Profit /(Loss) from operations before interest and

tax 12,51,100

Interest expense 1,600

Profit /(Loss) from operations before tax 12,49,500

Working Notes:

(1) Closing stock in units = Opening stock = Production – Sales

Year 1 = 0 + 40300 – 37100 = 3200 units

Year 2 = 3200 + 48200 – 41100 = 10300 units

Year 3 = 10300 + 51200 – 61100 = 400 units

(2) Closing stock in amounts = ( Unit sold / Unit produced ) * Total variable costs

Year 1 = (3200/40300) * ( 483600 + 644800 + 806000 ) = 153600

Year 2 = ( 10300 / 48200 ) * ( 578400 + 771200 + 964000 ) = 494400

Year 3 = ( 400/51200) * (614400+819200+1024000) = 19200

Absorption costing: This method include each and every cost which required to

manufacture product. This method include fixed as well as variable costs which means all types

6

Marginal cost of sales:

Opening Stock 4,94,400

Add variable production costs:

Direct materials 6,14,400

Direct labour 8,19,200

Variable overheads 10,24,000

Less closing stock 1, 2 19,200

Marginal cost of sales 29,32,800

Fixed manufacturing costs 65,000

Gross profit 12,79,200

Selling and distribution expenses 13,000

Administration expenses 15,100

Profit /(Loss) from operations before interest and

tax 12,51,100

Interest expense 1,600

Profit /(Loss) from operations before tax 12,49,500

Working Notes:

(1) Closing stock in units = Opening stock = Production – Sales

Year 1 = 0 + 40300 – 37100 = 3200 units

Year 2 = 3200 + 48200 – 41100 = 10300 units

Year 3 = 10300 + 51200 – 61100 = 400 units

(2) Closing stock in amounts = ( Unit sold / Unit produced ) * Total variable costs

Year 1 = (3200/40300) * ( 483600 + 644800 + 806000 ) = 153600

Year 2 = ( 10300 / 48200 ) * ( 578400 + 771200 + 964000 ) = 494400

Year 3 = ( 400/51200) * (614400+819200+1024000) = 19200

Absorption costing: This method include each and every cost which required to

manufacture product. This method include fixed as well as variable costs which means all types

6

of cost such as direct or indirect. It will provide more accuracy which helps the manager to

formulate their strategy accordingly

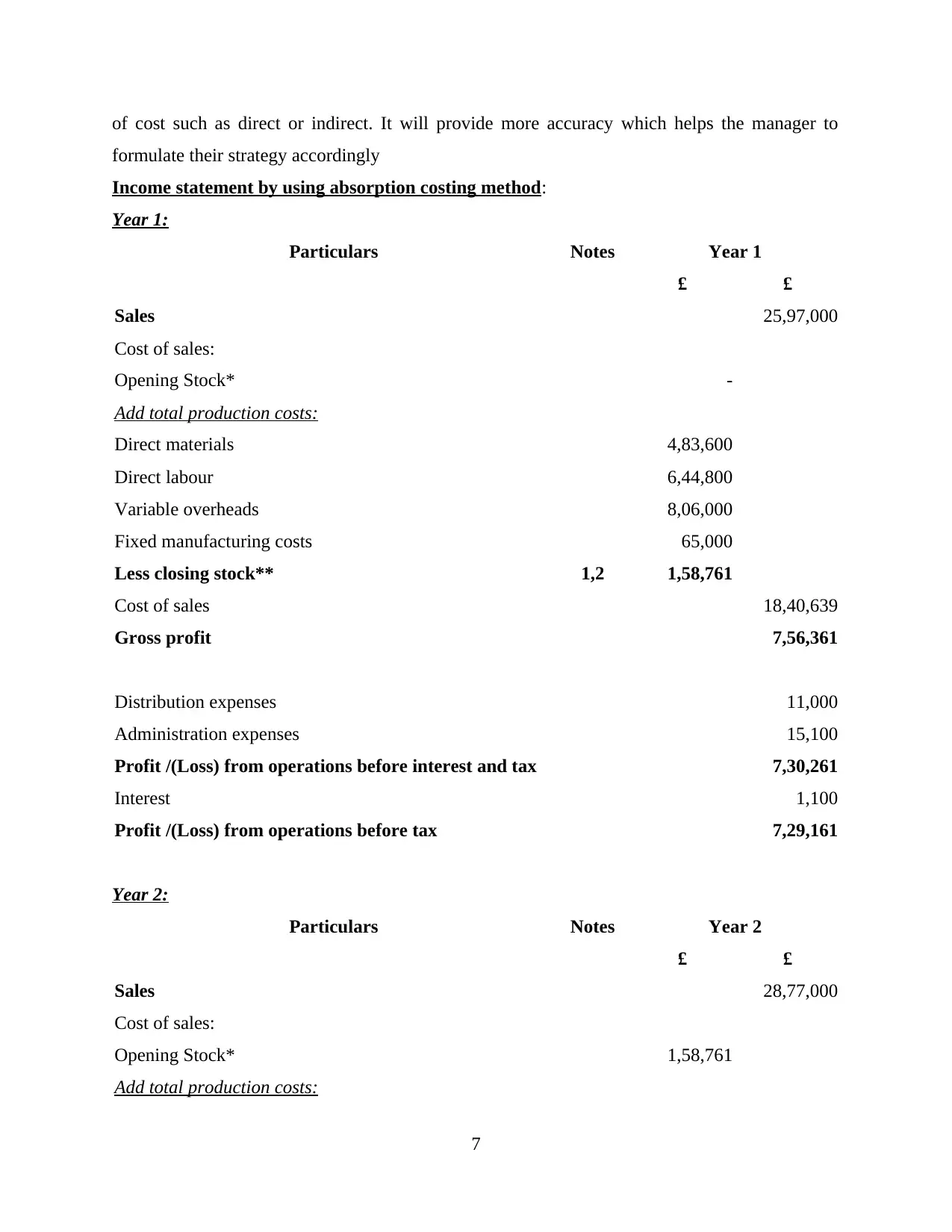

Income statement by using absorption costing method:

Year 1:

Particulars Notes Year 1

£ £

Sales 25,97,000

Cost of sales:

Opening Stock* -

Add total production costs:

Direct materials 4,83,600

Direct labour 6,44,800

Variable overheads 8,06,000

Fixed manufacturing costs 65,000

Less closing stock** 1,2 1,58,761

Cost of sales 18,40,639

Gross profit 7,56,361

Distribution expenses 11,000

Administration expenses 15,100

Profit /(Loss) from operations before interest and tax 7,30,261

Interest 1,100

Profit /(Loss) from operations before tax 7,29,161

Year 2:

Particulars Notes Year 2

£ £

Sales 28,77,000

Cost of sales:

Opening Stock* 1,58,761

Add total production costs:

7

formulate their strategy accordingly

Income statement by using absorption costing method:

Year 1:

Particulars Notes Year 1

£ £

Sales 25,97,000

Cost of sales:

Opening Stock* -

Add total production costs:

Direct materials 4,83,600

Direct labour 6,44,800

Variable overheads 8,06,000

Fixed manufacturing costs 65,000

Less closing stock** 1,2 1,58,761

Cost of sales 18,40,639

Gross profit 7,56,361

Distribution expenses 11,000

Administration expenses 15,100

Profit /(Loss) from operations before interest and tax 7,30,261

Interest 1,100

Profit /(Loss) from operations before tax 7,29,161

Year 2:

Particulars Notes Year 2

£ £

Sales 28,77,000

Cost of sales:

Opening Stock* 1,58,761

Add total production costs:

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

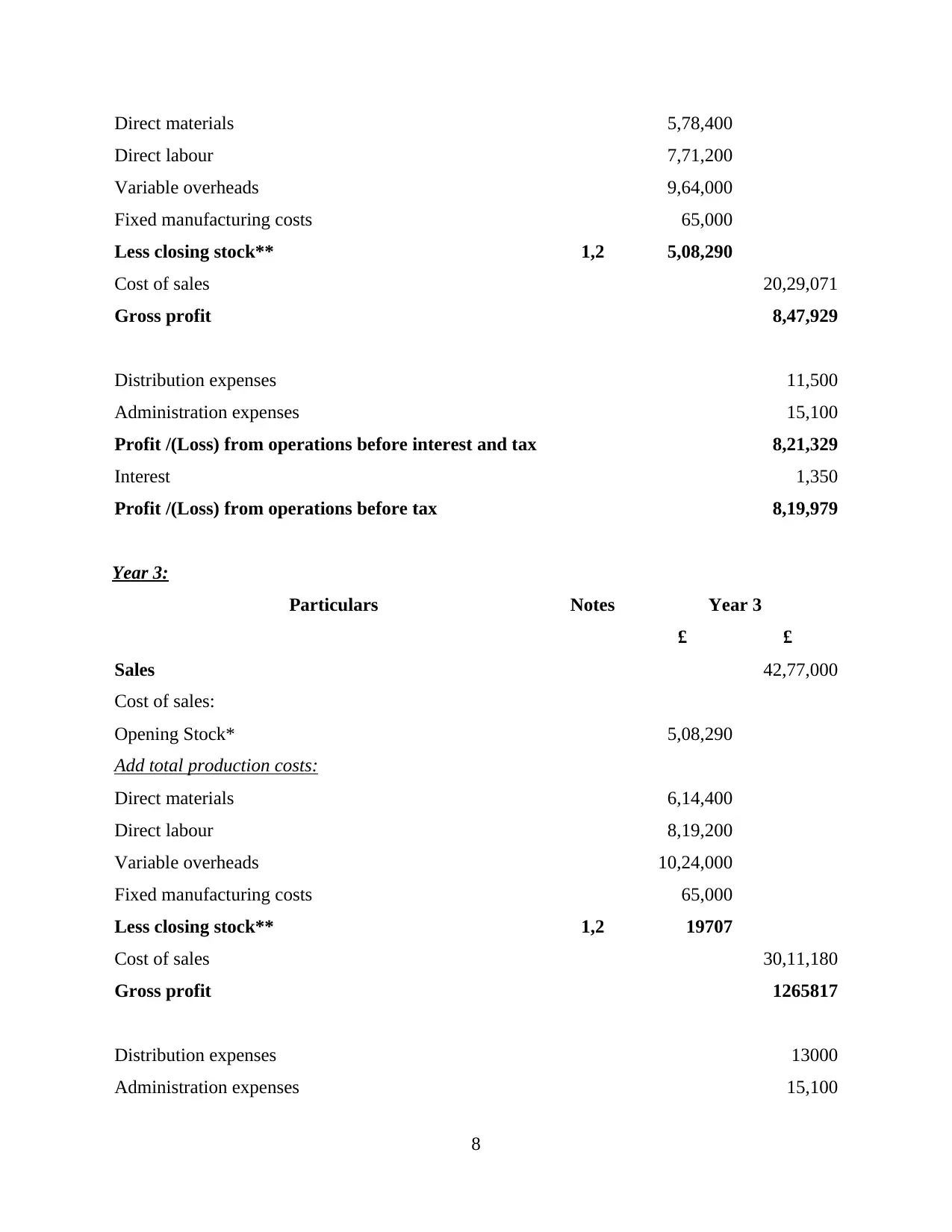

Direct materials 5,78,400

Direct labour 7,71,200

Variable overheads 9,64,000

Fixed manufacturing costs 65,000

Less closing stock** 1,2 5,08,290

Cost of sales 20,29,071

Gross profit 8,47,929

Distribution expenses 11,500

Administration expenses 15,100

Profit /(Loss) from operations before interest and tax 8,21,329

Interest 1,350

Profit /(Loss) from operations before tax 8,19,979

Year 3:

Particulars Notes Year 3

£ £

Sales 42,77,000

Cost of sales:

Opening Stock* 5,08,290

Add total production costs:

Direct materials 6,14,400

Direct labour 8,19,200

Variable overheads 10,24,000

Fixed manufacturing costs 65,000

Less closing stock** 1,2 19707

Cost of sales 30,11,180

Gross profit 1265817

Distribution expenses 13000

Administration expenses 15,100

8

Direct labour 7,71,200

Variable overheads 9,64,000

Fixed manufacturing costs 65,000

Less closing stock** 1,2 5,08,290

Cost of sales 20,29,071

Gross profit 8,47,929

Distribution expenses 11,500

Administration expenses 15,100

Profit /(Loss) from operations before interest and tax 8,21,329

Interest 1,350

Profit /(Loss) from operations before tax 8,19,979

Year 3:

Particulars Notes Year 3

£ £

Sales 42,77,000

Cost of sales:

Opening Stock* 5,08,290

Add total production costs:

Direct materials 6,14,400

Direct labour 8,19,200

Variable overheads 10,24,000

Fixed manufacturing costs 65,000

Less closing stock** 1,2 19707

Cost of sales 30,11,180

Gross profit 1265817

Distribution expenses 13000

Administration expenses 15,100

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

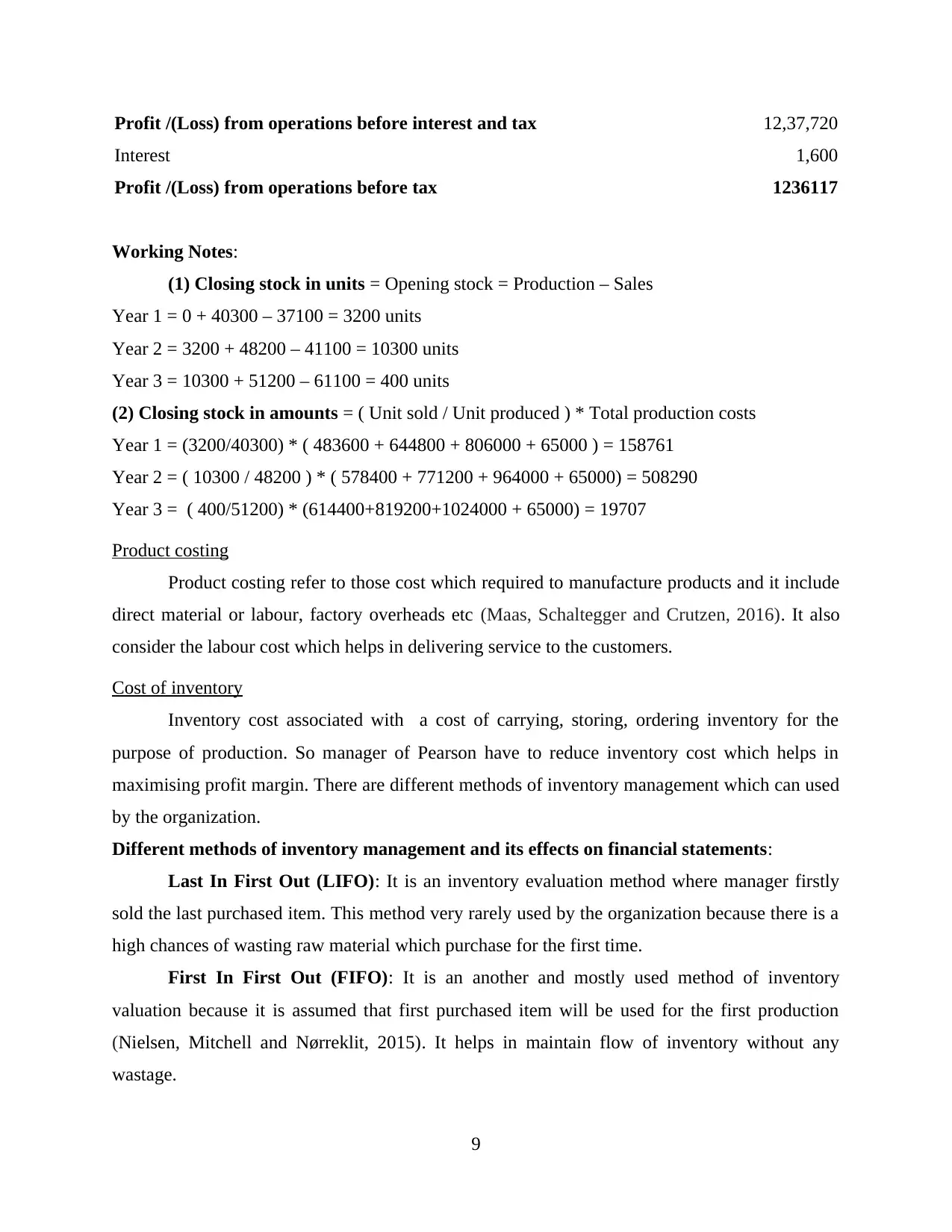

Profit /(Loss) from operations before interest and tax 12,37,720

Interest 1,600

Profit /(Loss) from operations before tax 1236117

Working Notes:

(1) Closing stock in units = Opening stock = Production – Sales

Year 1 = 0 + 40300 – 37100 = 3200 units

Year 2 = 3200 + 48200 – 41100 = 10300 units

Year 3 = 10300 + 51200 – 61100 = 400 units

(2) Closing stock in amounts = ( Unit sold / Unit produced ) * Total production costs

Year 1 = (3200/40300) * ( 483600 + 644800 + 806000 + 65000 ) = 158761

Year 2 = ( 10300 / 48200 ) * ( 578400 + 771200 + 964000 + 65000) = 508290

Year 3 = ( 400/51200) * (614400+819200+1024000 + 65000) = 19707

Product costing

Product costing refer to those cost which required to manufacture products and it include

direct material or labour, factory overheads etc (Maas, Schaltegger and Crutzen, 2016). It also

consider the labour cost which helps in delivering service to the customers.

Cost of inventory

Inventory cost associated with a cost of carrying, storing, ordering inventory for the

purpose of production. So manager of Pearson have to reduce inventory cost which helps in

maximising profit margin. There are different methods of inventory management which can used

by the organization.

Different methods of inventory management and its effects on financial statements:

Last In First Out (LIFO): It is an inventory evaluation method where manager firstly

sold the last purchased item. This method very rarely used by the organization because there is a

high chances of wasting raw material which purchase for the first time.

First In First Out (FIFO): It is an another and mostly used method of inventory

valuation because it is assumed that first purchased item will be used for the first production

(Nielsen, Mitchell and Nørreklit, 2015). It helps in maintain flow of inventory without any

wastage.

9

Interest 1,600

Profit /(Loss) from operations before tax 1236117

Working Notes:

(1) Closing stock in units = Opening stock = Production – Sales

Year 1 = 0 + 40300 – 37100 = 3200 units

Year 2 = 3200 + 48200 – 41100 = 10300 units

Year 3 = 10300 + 51200 – 61100 = 400 units

(2) Closing stock in amounts = ( Unit sold / Unit produced ) * Total production costs

Year 1 = (3200/40300) * ( 483600 + 644800 + 806000 + 65000 ) = 158761

Year 2 = ( 10300 / 48200 ) * ( 578400 + 771200 + 964000 + 65000) = 508290

Year 3 = ( 400/51200) * (614400+819200+1024000 + 65000) = 19707

Product costing

Product costing refer to those cost which required to manufacture products and it include

direct material or labour, factory overheads etc (Maas, Schaltegger and Crutzen, 2016). It also

consider the labour cost which helps in delivering service to the customers.

Cost of inventory

Inventory cost associated with a cost of carrying, storing, ordering inventory for the

purpose of production. So manager of Pearson have to reduce inventory cost which helps in

maximising profit margin. There are different methods of inventory management which can used

by the organization.

Different methods of inventory management and its effects on financial statements:

Last In First Out (LIFO): It is an inventory evaluation method where manager firstly

sold the last purchased item. This method very rarely used by the organization because there is a

high chances of wasting raw material which purchase for the first time.

First In First Out (FIFO): It is an another and mostly used method of inventory

valuation because it is assumed that first purchased item will be used for the first production

(Nielsen, Mitchell and Nørreklit, 2015). It helps in maintain flow of inventory without any

wastage.

9

Average Value of Cost (AVCO): It is an simple method where inventory stored in single

place and used in batched. There is no separation of inventory on the basis of purchasing order.

Company use stock as per the requirement on average basis.

Pearson company follow FIFO method for inventory valuation which helps in reducing

cost due to minimum wastage and further helps in maximising profit margin of the product.

LO3 Explain the use of planning tools in management accounting

Use of budget for planning & controlling

There are various planning tools which helps the organization to manage their operational

activity and try to minimise product. Some of the budget discussed below:

Master budget: This budget is the combination of different functional area and it will be

prepare on quarterly or monthly basis (Quattrone, 2016). With the help of this, manager able to

analyse performance of each department and compare with others. Further strategies will

develop on the basis of their departmental performance.

Zero based budget: Under this method, all the expenses will justify again for every new

period and all the estimation of cost will be start from the “Zero Base”. It is very time taken

process because manager does not use any previous information to build this budget. But it helps

the organization to provide accurate information regarding expenditure or revenue.

Capital budget: This budget prepare for the evaluation of investment in particular

project. At the time of inventing any new project, business produce capital budget for the

requirement of finance from various sources.

From the above mention budgets, manager of Pearson follow capital or master budget

which helps the organization to identify departmental performance as well as requirement of

finance for the further investments.

Pricing Strategies

There are various types of pricing used by the organization and it will be depend upon

customers (Pricing strategies, 2019). Some of them mentioned below:

Premium pricing: Under this pricing strategy, company select high price for their

products and it will be beneficial for the industrial segment where competition is very high.

Difficult for other organization to entered in this market.

10

place and used in batched. There is no separation of inventory on the basis of purchasing order.

Company use stock as per the requirement on average basis.

Pearson company follow FIFO method for inventory valuation which helps in reducing

cost due to minimum wastage and further helps in maximising profit margin of the product.

LO3 Explain the use of planning tools in management accounting

Use of budget for planning & controlling

There are various planning tools which helps the organization to manage their operational

activity and try to minimise product. Some of the budget discussed below:

Master budget: This budget is the combination of different functional area and it will be

prepare on quarterly or monthly basis (Quattrone, 2016). With the help of this, manager able to

analyse performance of each department and compare with others. Further strategies will

develop on the basis of their departmental performance.

Zero based budget: Under this method, all the expenses will justify again for every new

period and all the estimation of cost will be start from the “Zero Base”. It is very time taken

process because manager does not use any previous information to build this budget. But it helps

the organization to provide accurate information regarding expenditure or revenue.

Capital budget: This budget prepare for the evaluation of investment in particular

project. At the time of inventing any new project, business produce capital budget for the

requirement of finance from various sources.

From the above mention budgets, manager of Pearson follow capital or master budget

which helps the organization to identify departmental performance as well as requirement of

finance for the further investments.

Pricing Strategies

There are various types of pricing used by the organization and it will be depend upon

customers (Pricing strategies, 2019). Some of them mentioned below:

Premium pricing: Under this pricing strategy, company select high price for their

products and it will be beneficial for the industrial segment where competition is very high.

Difficult for other organization to entered in this market.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.