Management Accounting Systems: Techniques, Analysis, and Performance

VerifiedAdded on 2024/05/17

|35

|4974

|452

Report

AI Summary

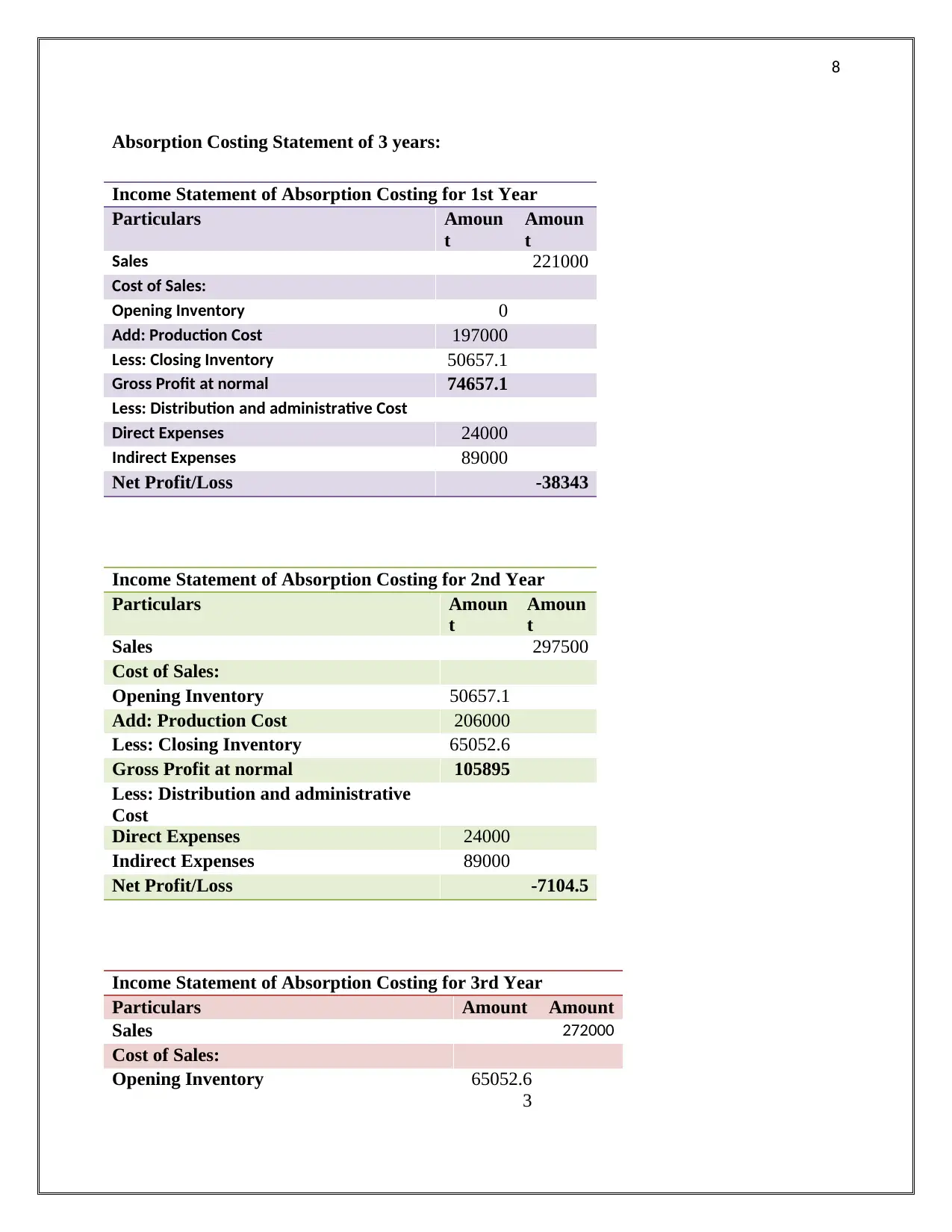

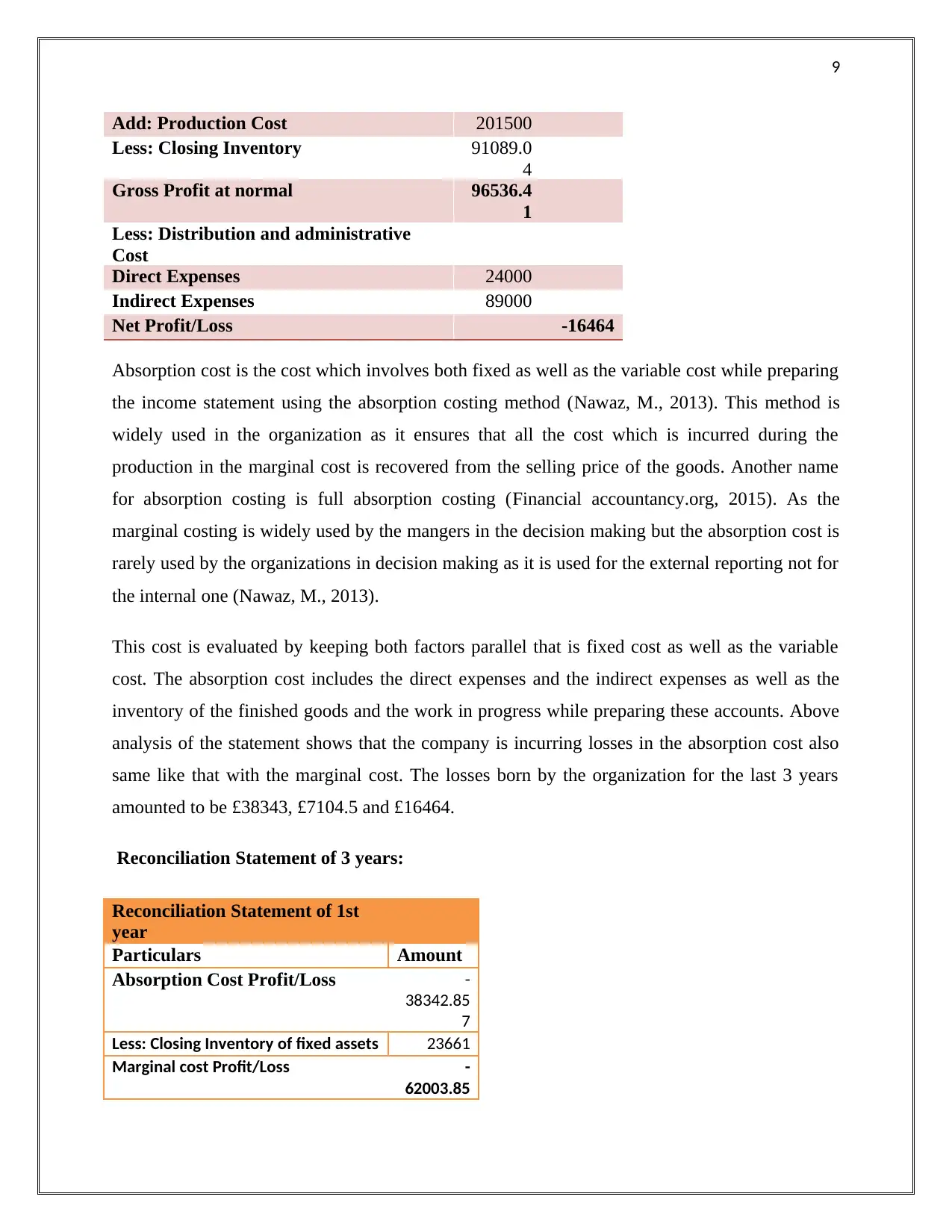

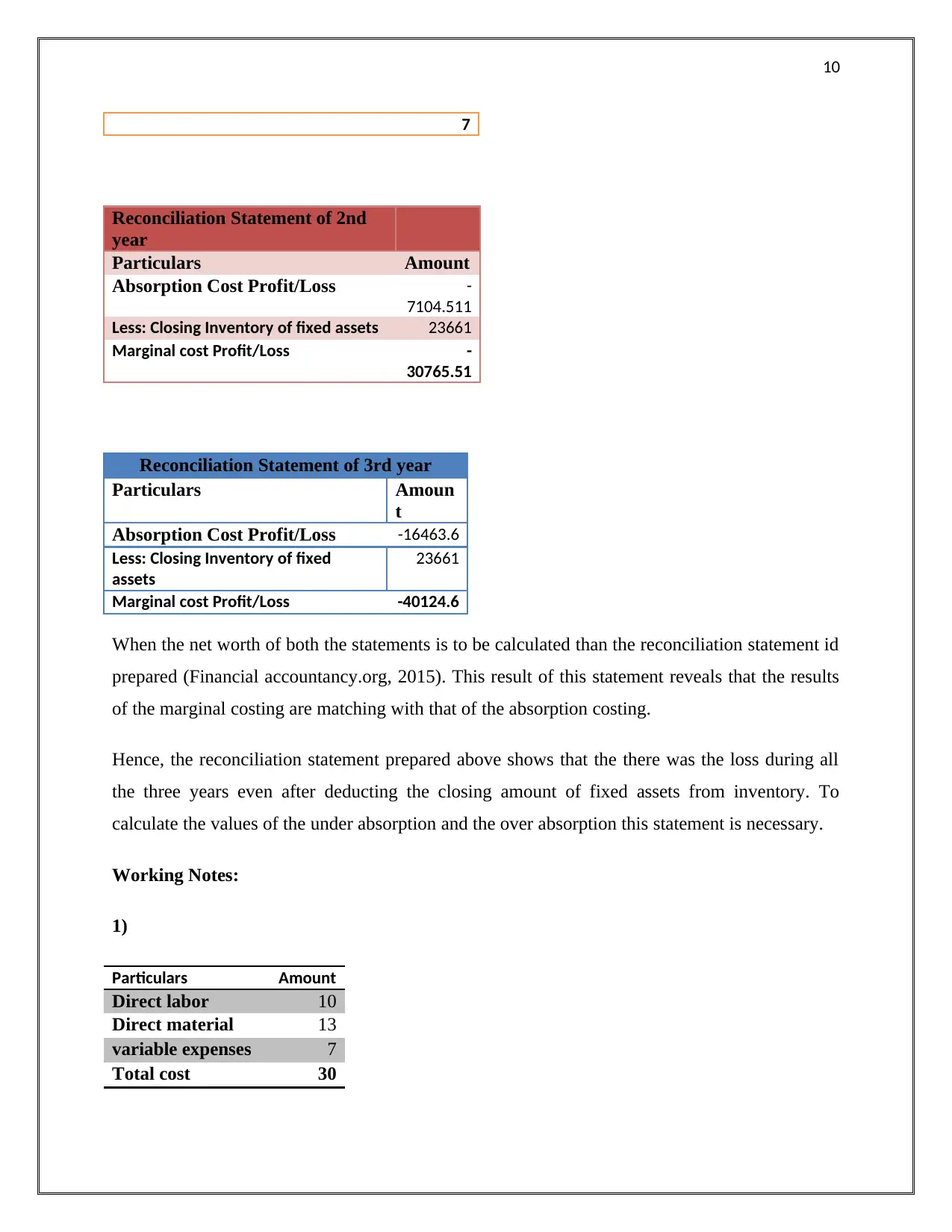

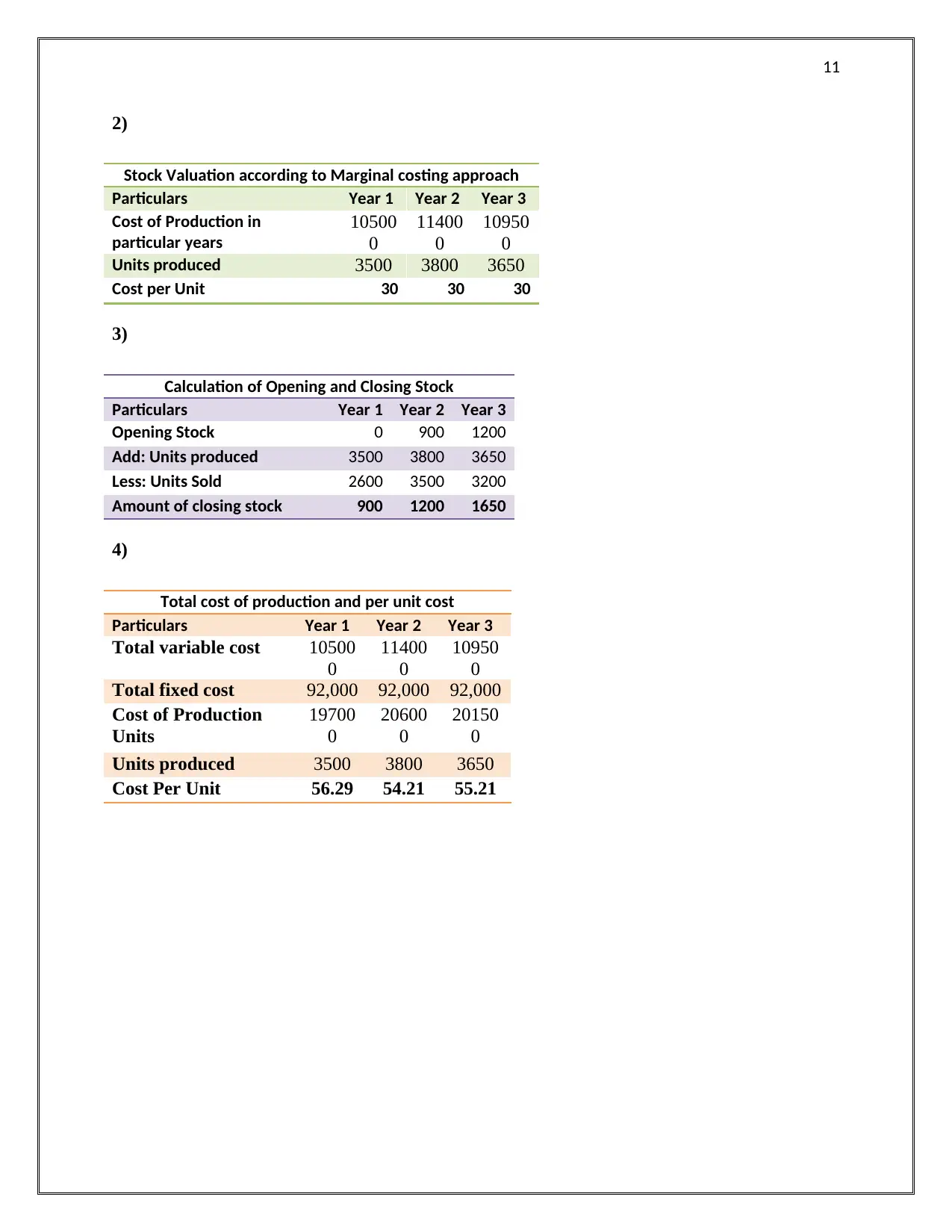

This report explores various management accounting systems used to analyze a company's performance, identifying cost analysis techniques and their application in financial reporting. It explains the benefits of management accounting systems within an organizational context, highlighting the use of planning tools to address financial problems and ensure sustainability. The report includes a marginal costing statement and an absorption costing statement for three years, along with a reconciliation statement to compare the results. It discusses the principles of management accounting, such as profit calculation considering inflation, utility, return on business, and resource utilization. The report also touches on fund flow statement analysis, standard costing, marginal costing techniques, and budgetary control. It concludes that management accounting is crucial for preparing and managing reports, while various accounting systems are responsible for evaluating organizational performance in the external market.

1 out of 35

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.