Management Accounting Report: Methods, Analysis, and Planning

VerifiedAdded on 2020/11/23

|14

|3875

|329

Report

AI Summary

This report delves into the realm of management accounting, providing a comprehensive overview of its systems, applications, and benefits. It begins by defining management accounting and its role in assisting strategic decision-making within organizations, using Aldi as a case study. The report explores various management accounting systems, including cost control, job costing, price optimization, and inventory management, highlighting their essential requirements and advantages. It then presents different methods of management accounting reporting, such as cost reports, performance reports, budget reports, accounts receivable reports, and inventory/manufacturing reports. Furthermore, the report includes a detailed analysis and calculation using both marginal and absorption costing techniques, exemplified by Conway Ltd. The advantages and disadvantages of different planning tools for budgetary control are also discussed. Finally, the report examines the adoption of management accounting systems for responding to financial problems and achieving sustainable success, concluding with a synthesis of the key concepts and their practical implications.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting and its system with their essential requirements...........................1

P2 Presenting different methods of Management Accounting reporting....................................3

TASK 2............................................................................................................................................4

P3 Presenting the calculation of on basis of Marginal and Absorption costing..........................4

TASK 3............................................................................................................................................6

P4 Explaining advantages and disadvantages of different types of planning tools for budgetary

control.........................................................................................................................................6

TASK 4............................................................................................................................................8

P5 Adoption of management accounting system for responding to financial problems and

leading to sustainable success.....................................................................................................8

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting and its system with their essential requirements...........................1

P2 Presenting different methods of Management Accounting reporting....................................3

TASK 2............................................................................................................................................4

P3 Presenting the calculation of on basis of Marginal and Absorption costing..........................4

TASK 3............................................................................................................................................6

P4 Explaining advantages and disadvantages of different types of planning tools for budgetary

control.........................................................................................................................................6

TASK 4............................................................................................................................................8

P5 Adoption of management accounting system for responding to financial problems and

leading to sustainable success.....................................................................................................8

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................11

INTRODUCTION

Accounting is the language of a business as it defines the performance and financial

position of the organisation. The accounting mainly includes mainly two parts that is financial

and management. Financial one deals with the monetary transaction of firm while the scope of

management accounting is vast as it includes both financial and statistical data of the entity to

assist the management of the company in strategic decision-making process. In the present report

a detailed discussion about the management accounting system. Their application in business and

benefits are presented. Moreover, calculation using marginal and abortion method of costing is

carried out use and application of planning tools for budgetary control is presented. Application

of management accounting for responding financial problems is also carried out.

TASK 1

P1 Management accounting and its system with their essential requirements

Management Accounting: This can be defined as that process which analyse the cost of

business and its operation for preparation of internal financial reports, records and accounts

which assist the management in the decision-making process to achieve the business objectives

(Kenno and Free, 2018). This is an act making the financial and costing data sensible and

translating the same into useful information for the management and offices in the organisation

to use the same in effective decision making.

The institute of management accounting defines it as “it is a profession involving

partnership with decision making, making plans, performance management system, with

providing expertise in the financial reporting and controlling to assist management in

formulation and implementation of the strategy of the business”

Different types of management accounting system and their requirements, benefits and

application in Aldi:

Cost control system: This system is used by Aldi to involve a practice of identification

and reduction of the expenses and cost of business with enhancing the profits of the business.

This starts with preparation of the budgetary system (Hiebl, 2018). The managers of Aldi

compare actual cost and revenue with the budgeted ones, if the actual cost is Hight than planned,

controlling actions are taken to reach the expected level.

Benefits:

It assists in improvement of profitability and competitiveness of the firm.

1

Accounting is the language of a business as it defines the performance and financial

position of the organisation. The accounting mainly includes mainly two parts that is financial

and management. Financial one deals with the monetary transaction of firm while the scope of

management accounting is vast as it includes both financial and statistical data of the entity to

assist the management of the company in strategic decision-making process. In the present report

a detailed discussion about the management accounting system. Their application in business and

benefits are presented. Moreover, calculation using marginal and abortion method of costing is

carried out use and application of planning tools for budgetary control is presented. Application

of management accounting for responding financial problems is also carried out.

TASK 1

P1 Management accounting and its system with their essential requirements

Management Accounting: This can be defined as that process which analyse the cost of

business and its operation for preparation of internal financial reports, records and accounts

which assist the management in the decision-making process to achieve the business objectives

(Kenno and Free, 2018). This is an act making the financial and costing data sensible and

translating the same into useful information for the management and offices in the organisation

to use the same in effective decision making.

The institute of management accounting defines it as “it is a profession involving

partnership with decision making, making plans, performance management system, with

providing expertise in the financial reporting and controlling to assist management in

formulation and implementation of the strategy of the business”

Different types of management accounting system and their requirements, benefits and

application in Aldi:

Cost control system: This system is used by Aldi to involve a practice of identification

and reduction of the expenses and cost of business with enhancing the profits of the business.

This starts with preparation of the budgetary system (Hiebl, 2018). The managers of Aldi

compare actual cost and revenue with the budgeted ones, if the actual cost is Hight than planned,

controlling actions are taken to reach the expected level.

Benefits:

It assists in improvement of profitability and competitiveness of the firm.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It helps in reduction of the cost of production and thus reducing the sale prices.

The prices are kept stable hence maintaining the higher level of sales which ensure

regular profits generation.

Job costing system: This system is used by the management of the Aldi for assigning

and accumulating the manufacturing cost to individual units, departments or job. This is used as

various items are produces which are significantly different from each other and their cost of

production changes too (Usenko and et.al., 2018). The job cost record reports each item's direct

materials and direct labour that are actually used and an assigned amount of manufacturing

overhead.

Price optimization:

This technique is emphasised on analysing and comparing the prices of products and

services which have been offered by Aldi in different segmentation. It demonstrates how people

respond to the different prices at the same products and services (Azudin and Mansor, 2018). It

benefits the managerial professionals in analysing demand and developing best pricing strategies

for better profitability. This strategy will benefit the managerial professionals in decision making

and analysing the outcomes as per effective requirements.

Inventory management:

This is the method presented for managing inventories of the organisation. Therefore, there

are several elements which have been presented in the database that defines effective supply

chain management. It funnels the managerial professionals in analysing the demand and

producing the products as per the required (Anand, Balakrishnan and Labro, 2018). Therefore,

the chances of having wastage and inappropriate management of products will be controlled.

Additionally, it will help Aldi in securing the costs utilised in products and distribution of

products by effective execution over inflows and outflows of stock.

However, by implicating these techniques in the business operations will be effective in

terms of improving the creditability. Thus, it will be beneficial in terms of presenting accurate

and reliable information among the accountant of Aldi which in turn helpful in drafting the final

disclosure and decision making in the business. Additionally, such information will be effective

for organisation for having strong financial control.

2

The prices are kept stable hence maintaining the higher level of sales which ensure

regular profits generation.

Job costing system: This system is used by the management of the Aldi for assigning

and accumulating the manufacturing cost to individual units, departments or job. This is used as

various items are produces which are significantly different from each other and their cost of

production changes too (Usenko and et.al., 2018). The job cost record reports each item's direct

materials and direct labour that are actually used and an assigned amount of manufacturing

overhead.

Price optimization:

This technique is emphasised on analysing and comparing the prices of products and

services which have been offered by Aldi in different segmentation. It demonstrates how people

respond to the different prices at the same products and services (Azudin and Mansor, 2018). It

benefits the managerial professionals in analysing demand and developing best pricing strategies

for better profitability. This strategy will benefit the managerial professionals in decision making

and analysing the outcomes as per effective requirements.

Inventory management:

This is the method presented for managing inventories of the organisation. Therefore, there

are several elements which have been presented in the database that defines effective supply

chain management. It funnels the managerial professionals in analysing the demand and

producing the products as per the required (Anand, Balakrishnan and Labro, 2018). Therefore,

the chances of having wastage and inappropriate management of products will be controlled.

Additionally, it will help Aldi in securing the costs utilised in products and distribution of

products by effective execution over inflows and outflows of stock.

However, by implicating these techniques in the business operations will be effective in

terms of improving the creditability. Thus, it will be beneficial in terms of presenting accurate

and reliable information among the accountant of Aldi which in turn helpful in drafting the final

disclosure and decision making in the business. Additionally, such information will be effective

for organisation for having strong financial control.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

P2 Presenting different methods of Management Accounting reporting

Management accounting report: These reports are essential requirement of the

business of Aldi an organisation the retail sector of UK. Theses report provides the business

with the required information to trim the cost, giving reward to high performing employees, to

cut out the not profiting product line, and make investment in goods which are offering

significant financial returns for the business of Aldi. These reports can be generated quarterly,

monthly, weekly or even daily (Bodleand and et.al., 2018). Beneath are the different types of

management accounting report used in Aldi:

Cost report: The cost report defined the cost related with specific project, department,

job and even the per unit cost of production of Aldi. This aids in identification of the areas with

higher earning and area not generating any profits in Aldi (Habidin and et.al., 2018). Thus, assist

the management of the business in allocation of the resources as more allocation to profit making

activities and to cut the resources for those jobs with no or less profits.

Performance report: These reports are generated in Aldi to review the performances of

company as a whole as well as each employee and department in the organisation (Aziz and

Ahmad, 2018). These reports are used by the manager of the Aldi to make the key strategic

3

MANAGEMENT ACCOUNTING REPORT

Cost Report

Budget

Report

Performance

Report

Account

Receivable

Report

Inventory and

Manufacturing

Report

Management accounting report: These reports are essential requirement of the

business of Aldi an organisation the retail sector of UK. Theses report provides the business

with the required information to trim the cost, giving reward to high performing employees, to

cut out the not profiting product line, and make investment in goods which are offering

significant financial returns for the business of Aldi. These reports can be generated quarterly,

monthly, weekly or even daily (Bodleand and et.al., 2018). Beneath are the different types of

management accounting report used in Aldi:

Cost report: The cost report defined the cost related with specific project, department,

job and even the per unit cost of production of Aldi. This aids in identification of the areas with

higher earning and area not generating any profits in Aldi (Habidin and et.al., 2018). Thus, assist

the management of the business in allocation of the resources as more allocation to profit making

activities and to cut the resources for those jobs with no or less profits.

Performance report: These reports are generated in Aldi to review the performances of

company as a whole as well as each employee and department in the organisation (Aziz and

Ahmad, 2018). These reports are used by the manager of the Aldi to make the key strategic

3

MANAGEMENT ACCOUNTING REPORT

Cost Report

Budget

Report

Performance

Report

Account

Receivable

Report

Inventory and

Manufacturing

Report

decisions regarding future of the firm. The higher performers are given rewards and for under

performer controlling and monitoring strategies are made.

Budget report: This report assists them in analysis the business performance by the

owners and evaluating the department wise performance by manager of Aldi. The forecasted

budgeted are prepared for a specific time period and are based on the actual expense and revenue

of previous years (Bebbington and Unerman, 2018). This budget helps the management of Aldi

in cutting the cost and to decide upon the bonus and incentives to the employees. This report is

also crucial in the context of decision making as it need preciseness and accuracy in determining

the level of outcomes that can be achieved, with the available resource with the business.

Account receivable report: For the business relying on extending credits this report is of

essential need. It is necessary to prepare to break down the remaining balance due form the

consumers for a time period allowing the manager of the Aldi to identity the defaulters as well

the problems in the collection process of the organisation (Kenno and Free, 2018). There is

always some bad debt that needs to be written off, which can be done with the help of this report

which makes is easy to find the defining parties who will not make payments.

Inventory and manufacturing report: This management accounting report is used to

maintain the inventory level of the organisation. This reporting makes the manufacturing process

more efficient. In this reports' thing which generally includes are, inventory waste, hourly labour

costs, per unit overhead cost (Hiebl, 2018). A comparison of the cost of different assembly line

within the business is done with a view to highlight the areas for the improvement or offering

business best performing department.

TASK 2

P3 Presenting the calculation of on basis of Marginal and Absorption costing

Conway Ltd has been presented several accounting issues on which outcomes has been

determined by the managerial professionals (Usenko and et.al., 2018). However, these

accounting problems will be resolved as per implicating two methods such as Marginal and

Absorption costing techniques.

Income statement through Marginal costing techniques:

In marginal costing technique there will be consideration of the variable cost which will

be charged in the Unit of costs (Azudin and Mansor, 2018). Similarly, the fixed cost of the

4

performer controlling and monitoring strategies are made.

Budget report: This report assists them in analysis the business performance by the

owners and evaluating the department wise performance by manager of Aldi. The forecasted

budgeted are prepared for a specific time period and are based on the actual expense and revenue

of previous years (Bebbington and Unerman, 2018). This budget helps the management of Aldi

in cutting the cost and to decide upon the bonus and incentives to the employees. This report is

also crucial in the context of decision making as it need preciseness and accuracy in determining

the level of outcomes that can be achieved, with the available resource with the business.

Account receivable report: For the business relying on extending credits this report is of

essential need. It is necessary to prepare to break down the remaining balance due form the

consumers for a time period allowing the manager of the Aldi to identity the defaulters as well

the problems in the collection process of the organisation (Kenno and Free, 2018). There is

always some bad debt that needs to be written off, which can be done with the help of this report

which makes is easy to find the defining parties who will not make payments.

Inventory and manufacturing report: This management accounting report is used to

maintain the inventory level of the organisation. This reporting makes the manufacturing process

more efficient. In this reports' thing which generally includes are, inventory waste, hourly labour

costs, per unit overhead cost (Hiebl, 2018). A comparison of the cost of different assembly line

within the business is done with a view to highlight the areas for the improvement or offering

business best performing department.

TASK 2

P3 Presenting the calculation of on basis of Marginal and Absorption costing

Conway Ltd has been presented several accounting issues on which outcomes has been

determined by the managerial professionals (Usenko and et.al., 2018). However, these

accounting problems will be resolved as per implicating two methods such as Marginal and

Absorption costing techniques.

Income statement through Marginal costing techniques:

In marginal costing technique there will be consideration of the variable cost which will

be charged in the Unit of costs (Azudin and Mansor, 2018). Similarly, the fixed cost of the

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

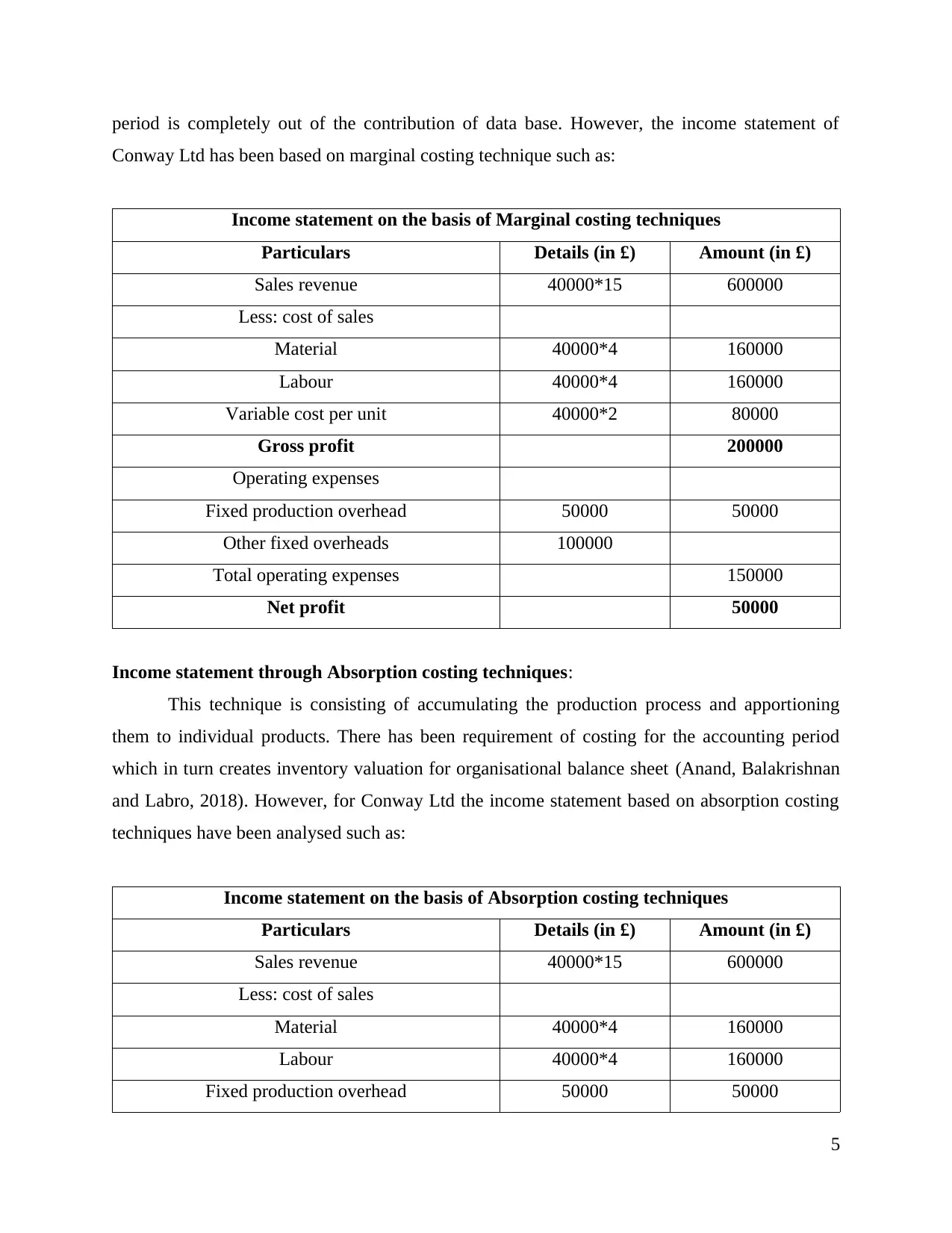

period is completely out of the contribution of data base. However, the income statement of

Conway Ltd has been based on marginal costing technique such as:

Income statement on the basis of Marginal costing techniques

Particulars Details (in £) Amount (in £)

Sales revenue 40000*15 600000

Less: cost of sales

Material 40000*4 160000

Labour 40000*4 160000

Variable cost per unit 40000*2 80000

Gross profit 200000

Operating expenses

Fixed production overhead 50000 50000

Other fixed overheads 100000

Total operating expenses 150000

Net profit 50000

Income statement through Absorption costing techniques:

This technique is consisting of accumulating the production process and apportioning

them to individual products. There has been requirement of costing for the accounting period

which in turn creates inventory valuation for organisational balance sheet (Anand, Balakrishnan

and Labro, 2018). However, for Conway Ltd the income statement based on absorption costing

techniques have been analysed such as:

Income statement on the basis of Absorption costing techniques

Particulars Details (in £) Amount (in £)

Sales revenue 40000*15 600000

Less: cost of sales

Material 40000*4 160000

Labour 40000*4 160000

Fixed production overhead 50000 50000

5

Conway Ltd has been based on marginal costing technique such as:

Income statement on the basis of Marginal costing techniques

Particulars Details (in £) Amount (in £)

Sales revenue 40000*15 600000

Less: cost of sales

Material 40000*4 160000

Labour 40000*4 160000

Variable cost per unit 40000*2 80000

Gross profit 200000

Operating expenses

Fixed production overhead 50000 50000

Other fixed overheads 100000

Total operating expenses 150000

Net profit 50000

Income statement through Absorption costing techniques:

This technique is consisting of accumulating the production process and apportioning

them to individual products. There has been requirement of costing for the accounting period

which in turn creates inventory valuation for organisational balance sheet (Anand, Balakrishnan

and Labro, 2018). However, for Conway Ltd the income statement based on absorption costing

techniques have been analysed such as:

Income statement on the basis of Absorption costing techniques

Particulars Details (in £) Amount (in £)

Sales revenue 40000*15 600000

Less: cost of sales

Material 40000*4 160000

Labour 40000*4 160000

Fixed production overhead 50000 50000

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Gross profit 230000

Operating expenses

Other fixed overheads 100000

Total operating expenses 150000

Net profit 80000

Interpretation: On the basis of above analysed income statement through marginal and

absorption costing techniques for Conway Ltd. there have been huge differentiation in the

analysed data set by these methods. Sales revenue of business on the basis of produced units

which were 40000 on the selling price such as 15. The total amount of sales has been analysed as

600000. The gross profit of the data base as per marginal costing technique is analysed as

200000 and absorption costing GP as 230000. Similarly, in analysing the net profit of the

presented variables which have defined the outcomes or marginal costing as 50000 and for

absorption as 80000. Thus, as per such outcomes on which it can be said that, the absorption

costing techniques is comparatively profitable for the industry with reference to analyse the net

profit.

Basis Marginal costing Absorption costing

Cost application Variable cost of the inventory

is considered

Variable and fixed overheads

both are applied to inventory.

Profits Each individual sales shows

higher profits

The profitability appears

lower for each individual sale

Measurements Profits are calculated using

contribution margins

Gross margin which includes

applied overheads are used to

measure the profits

Cost consideration Variable cost is considered as

product cost and fixed one is

treated as period cost.

Considers both fixed and

variable cost as product cost.

6

Operating expenses

Other fixed overheads 100000

Total operating expenses 150000

Net profit 80000

Interpretation: On the basis of above analysed income statement through marginal and

absorption costing techniques for Conway Ltd. there have been huge differentiation in the

analysed data set by these methods. Sales revenue of business on the basis of produced units

which were 40000 on the selling price such as 15. The total amount of sales has been analysed as

600000. The gross profit of the data base as per marginal costing technique is analysed as

200000 and absorption costing GP as 230000. Similarly, in analysing the net profit of the

presented variables which have defined the outcomes or marginal costing as 50000 and for

absorption as 80000. Thus, as per such outcomes on which it can be said that, the absorption

costing techniques is comparatively profitable for the industry with reference to analyse the net

profit.

Basis Marginal costing Absorption costing

Cost application Variable cost of the inventory

is considered

Variable and fixed overheads

both are applied to inventory.

Profits Each individual sales shows

higher profits

The profitability appears

lower for each individual sale

Measurements Profits are calculated using

contribution margins

Gross margin which includes

applied overheads are used to

measure the profits

Cost consideration Variable cost is considered as

product cost and fixed one is

treated as period cost.

Considers both fixed and

variable cost as product cost.

6

TASK 3

P4 Explaining advantages and disadvantages of different types of planning tools for budgetary

control

In relation with improving the efficiency of the business on which there will be use of

effective planning tools and budgetary control techniques. Preparing budgets will be beneficiary

methods on which managerial and accounting professionals will articulate the costs implied in

each activity as well as estimate it for the further period (Habidin and et.al., 2018). To analyse

the effectiveness of such tools there must be analysis on the advantages and disadvantages such

as:

Incremental budget: The concept behind this method is that managerial professionals

articulated costs and gains from the previous year and make slight changes in the preceding

period’s budget for Aldi (Incremental budgeting, 2017). It does not require much time for

formulating the budgets as they estimate the costs and profits on the basis of raising the actual

outcomes on a certain proportion.

Advantages:

This is the easiest way of formulating budget for upcoming period.

It does not require much time and efforts by professionals.

It brings stability in operations and funding

Disadvantages:

It is consisting of risks as there would not be proper analysis over cost implicated in the

activities.

There can be chances of manipulation by managers for satisfy their personal needs.

The allocation of costs in activities will not be accurate as some activities might have less

funds will the unnecessary activity have more than enough amount of funds.

Activity based budgeting: These are the budgets which were prepared on the basis of cost

implicates in each activity. Thus, on the basis of which professionals analyse the past results to

determine the costs implicated in each activity as well as revenue gains through them

(Advantages, Disadvantages and Limitations of Activity Based Costing (ABC) System, 2017).

These information helps them in drafting a valid conclusion to decide the future costs implicated

in such activities of Aldi.

Advantages

7

P4 Explaining advantages and disadvantages of different types of planning tools for budgetary

control

In relation with improving the efficiency of the business on which there will be use of

effective planning tools and budgetary control techniques. Preparing budgets will be beneficiary

methods on which managerial and accounting professionals will articulate the costs implied in

each activity as well as estimate it for the further period (Habidin and et.al., 2018). To analyse

the effectiveness of such tools there must be analysis on the advantages and disadvantages such

as:

Incremental budget: The concept behind this method is that managerial professionals

articulated costs and gains from the previous year and make slight changes in the preceding

period’s budget for Aldi (Incremental budgeting, 2017). It does not require much time for

formulating the budgets as they estimate the costs and profits on the basis of raising the actual

outcomes on a certain proportion.

Advantages:

This is the easiest way of formulating budget for upcoming period.

It does not require much time and efforts by professionals.

It brings stability in operations and funding

Disadvantages:

It is consisting of risks as there would not be proper analysis over cost implicated in the

activities.

There can be chances of manipulation by managers for satisfy their personal needs.

The allocation of costs in activities will not be accurate as some activities might have less

funds will the unnecessary activity have more than enough amount of funds.

Activity based budgeting: These are the budgets which were prepared on the basis of cost

implicates in each activity. Thus, on the basis of which professionals analyse the past results to

determine the costs implicated in each activity as well as revenue gains through them

(Advantages, Disadvantages and Limitations of Activity Based Costing (ABC) System, 2017).

These information helps them in drafting a valid conclusion to decide the future costs implicated

in such activities of Aldi.

Advantages

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

This is the most accurate and transparent technique in context with drafting budgets for

the activities.

Helpful in costing of process, value streams and supply chain management.

It considers the unit cost instead of total cost as well as integrates with six sigma

approach which enables the business in ongoing performance increment.

Disadvantages:

There will be requirement of appropriate information regarding the past transactions on

which it took much time and efforts.

Using this technique to generate reports is does not comply with principles of GAAP

(generally accepted accounting principles).

Zero based budgeting: This budgetary technique is based on the concept of not considering

the previous year’s transactional details (Aziz and Ahmad, 2018). Thus, in which an accountant

decides the budgets to be start at the zero value. Each period activities have funds which is

relevant with the real time requirements.

Advantages

This is the systematic analysis over the costs of budgets as well as requires less time and

efforts from an accounting practitioner.

Each activity has enough amount of funds moreover, it is cost effective to business.

Disadvantages:

There will not be focus on cost centres as there are chances of having mis management of

costs implied in activities.

There will be huge manipulation and misinterpretation of funds in operations.

Cash flow budget: This method for planning and estimating the cost of operations and

revenue which will be generated through operations of firm (Bebbington and Unerman, 2018).

The cash flow statement has been prepared on the basis of inflows and out flows in a year

bounds manager in planning costs for proceeding period.

Advantages

It is the most accurate and simple way of determining the expenses and revenue from

operations of firm.

It entitles the managerial professionals in decision making and formulating the plans for

identifying alternatives that reduce costs.

8

the activities.

Helpful in costing of process, value streams and supply chain management.

It considers the unit cost instead of total cost as well as integrates with six sigma

approach which enables the business in ongoing performance increment.

Disadvantages:

There will be requirement of appropriate information regarding the past transactions on

which it took much time and efforts.

Using this technique to generate reports is does not comply with principles of GAAP

(generally accepted accounting principles).

Zero based budgeting: This budgetary technique is based on the concept of not considering

the previous year’s transactional details (Aziz and Ahmad, 2018). Thus, in which an accountant

decides the budgets to be start at the zero value. Each period activities have funds which is

relevant with the real time requirements.

Advantages

This is the systematic analysis over the costs of budgets as well as requires less time and

efforts from an accounting practitioner.

Each activity has enough amount of funds moreover, it is cost effective to business.

Disadvantages:

There will not be focus on cost centres as there are chances of having mis management of

costs implied in activities.

There will be huge manipulation and misinterpretation of funds in operations.

Cash flow budget: This method for planning and estimating the cost of operations and

revenue which will be generated through operations of firm (Bebbington and Unerman, 2018).

The cash flow statement has been prepared on the basis of inflows and out flows in a year

bounds manager in planning costs for proceeding period.

Advantages

It is the most accurate and simple way of determining the expenses and revenue from

operations of firm.

It entitles the managerial professionals in decision making and formulating the plans for

identifying alternatives that reduce costs.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Disadvantages:

It will require the past data and a good understanding of accounting terms which will help

in developing appropriate estimation.

TASK 4

P5 Adoption of management accounting system for responding to financial problems and leading

to sustainable success

Management accounting and financial problems:

The MAS can be defined as that systematic approach followed by an organisation to

measure and evaluate its internal performances so that the managements can be given with

significant information for decision making process. The financial problems faced by a business

can e outlined as inadequate cash flow, cost containment, credit and debt issues.

Advantages:

The MAS effective identify he financial problems and solve the same before time.

Assist in planning, decision making and directing the operation of the business.

Disadvantages:

This is time consuming process.

This requires key skills and detailed information to evaluate the performance.

For managing the operational performance of the organisation on which there will be

need of evaluating the objectives by implicating the several tools and techniques. Adaption of

management accounting system funnels the managerial professionals in decision making and

analysing the funds flow in entire business operations (Kenno and Free, 2018). It will be

effective in resolving the financial problems and have improved performance on long term.

Moreover, to respond the financial issues there must be implication of several management

accounting tools such as:

Variance analysis report:

This is the difference between actual and budgeted funds used in the business operations.

thus, such analysing represents positive and negative change, which enables accounting

practitioners in decisions making and resolving financial issues.

Pricing strategies:

It governs through implicating prices on products on a profit margin that cost of

manufacturing must be covered in a limited period (Hiebl, 2018). However, Aldi will be

9

It will require the past data and a good understanding of accounting terms which will help

in developing appropriate estimation.

TASK 4

P5 Adoption of management accounting system for responding to financial problems and leading

to sustainable success

Management accounting and financial problems:

The MAS can be defined as that systematic approach followed by an organisation to

measure and evaluate its internal performances so that the managements can be given with

significant information for decision making process. The financial problems faced by a business

can e outlined as inadequate cash flow, cost containment, credit and debt issues.

Advantages:

The MAS effective identify he financial problems and solve the same before time.

Assist in planning, decision making and directing the operation of the business.

Disadvantages:

This is time consuming process.

This requires key skills and detailed information to evaluate the performance.

For managing the operational performance of the organisation on which there will be

need of evaluating the objectives by implicating the several tools and techniques. Adaption of

management accounting system funnels the managerial professionals in decision making and

analysing the funds flow in entire business operations (Kenno and Free, 2018). It will be

effective in resolving the financial problems and have improved performance on long term.

Moreover, to respond the financial issues there must be implication of several management

accounting tools such as:

Variance analysis report:

This is the difference between actual and budgeted funds used in the business operations.

thus, such analysing represents positive and negative change, which enables accounting

practitioners in decisions making and resolving financial issues.

Pricing strategies:

It governs through implicating prices on products on a profit margin that cost of

manufacturing must be covered in a limited period (Hiebl, 2018). However, Aldi will be

9

beneficial as per setting prices on products with proper ascertainment of strategies. There are

several pricing techniques that will be helpful to the business such as price penetration, seasonal,

premium, economy and skimming pricing.

Financial governance:

Assigning the role and duties to the accounting professionals which is relevant with

controlling, monitoring and executing the operational transaction of business (Usenko and et.al.,

2018). Aldi will have profitable success as if the qualified and skilled auditor analyse the

performance of business and suggest effective changes to be done costing system.

Management accounting information system:

Communicating the reports regarding revenue and expenses incurred in each department or

unit of business with the top-level professionals (Azudin and Mansor, 2018). Thus, delivering the

accurate reports helps them in analysing the profitability of such department analysed as per their

cost of investment. It will be assistive to professionals of Aldi in making satisfactory changes in

the costing methods and funds invested in practices.

Key performance Indicators:

Setting up small targets, challenges and objectives leads a business to sustain growth and

profitability. KPI includes various techniques such as balance scorecard and benchmarking

which motivated workforce to make effective efforts in attaining business targets (Anand,

Balakrishnan and Labro, 2018). Thus, such motivation will be effective for Aldi in having better

growth and profitability through operational efforts by employees.

Benchmarking: with this an organisation sets a bar to reach a certain level of performance

with its owe performances or that of a competitors and by evaluating its current position with the

set bench mark it can identify the lag and facial problems.

CONCLUSION

On the basis of above report, it can be concluded that management accounting systems,

techniques, tools, reports and methods are effective for managing performance of business. Aldi

had been suggested methods and tools to be implicated in business operations which would lead

to attain sustainable success. Along with this, there had been use of two costing techniques such

as marginal and absorption for resolving accounting problems of Conway Ltd. Moreover, other

non-financial techniques had been suggested to overcome with the financial problems and

leading the business in retaining effective success for the upcoming period.

10

several pricing techniques that will be helpful to the business such as price penetration, seasonal,

premium, economy and skimming pricing.

Financial governance:

Assigning the role and duties to the accounting professionals which is relevant with

controlling, monitoring and executing the operational transaction of business (Usenko and et.al.,

2018). Aldi will have profitable success as if the qualified and skilled auditor analyse the

performance of business and suggest effective changes to be done costing system.

Management accounting information system:

Communicating the reports regarding revenue and expenses incurred in each department or

unit of business with the top-level professionals (Azudin and Mansor, 2018). Thus, delivering the

accurate reports helps them in analysing the profitability of such department analysed as per their

cost of investment. It will be assistive to professionals of Aldi in making satisfactory changes in

the costing methods and funds invested in practices.

Key performance Indicators:

Setting up small targets, challenges and objectives leads a business to sustain growth and

profitability. KPI includes various techniques such as balance scorecard and benchmarking

which motivated workforce to make effective efforts in attaining business targets (Anand,

Balakrishnan and Labro, 2018). Thus, such motivation will be effective for Aldi in having better

growth and profitability through operational efforts by employees.

Benchmarking: with this an organisation sets a bar to reach a certain level of performance

with its owe performances or that of a competitors and by evaluating its current position with the

set bench mark it can identify the lag and facial problems.

CONCLUSION

On the basis of above report, it can be concluded that management accounting systems,

techniques, tools, reports and methods are effective for managing performance of business. Aldi

had been suggested methods and tools to be implicated in business operations which would lead

to attain sustainable success. Along with this, there had been use of two costing techniques such

as marginal and absorption for resolving accounting problems of Conway Ltd. Moreover, other

non-financial techniques had been suggested to overcome with the financial problems and

leading the business in retaining effective success for the upcoming period.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.