Management Accounting Report: Cost Analysis and Tools

VerifiedAdded on 2023/01/06

|12

|3256

|36

Report

AI Summary

This report, prepared for Prime Furniture, a developing furniture company, delves into management accounting principles. It begins with an introduction to management accounting and its role in strategic planning and financial control. The main body of the report includes detailed cost analysis, differentiating between direct and indirect costs, and fixed and variable costs, with a focus on inventory costs. It examines marginal and absorption costing methods, providing income statements and a reconciliation statement to illustrate their differences. The report further explores various management accounting tools, such as cash budgets, sales budgets, and capital budgeting, highlighting their advantages and disadvantages. Finally, it addresses financial problems like sales decline and rising raw material costs, suggesting solutions through financial governance, benchmarking, key performance indicators, and budgetary targets. The report emphasizes the importance of management accounting in making informed decisions and formulating effective strategies for business growth and financial stability.

Management Accounting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

TASK 1............................................................................................................................................3

TASK 2............................................................................................................................................3

P3 Cost Analysis.....................................................................................................................3

TASK 3............................................................................................................................................6

P4 Management accounting tools...........................................................................................6

TASK 4............................................................................................................................................8

P5 Usefulness of Management Accounting system in solving financial problems................8

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................12

2

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

TASK 1............................................................................................................................................3

TASK 2............................................................................................................................................3

P3 Cost Analysis.....................................................................................................................3

TASK 3............................................................................................................................................6

P4 Management accounting tools...........................................................................................6

TASK 4............................................................................................................................................8

P5 Usefulness of Management Accounting system in solving financial problems................8

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................12

2

INTRODUCTION

Management accounting is a branch of knowledge of Accounting. This consists of

various inspection tools and techniques that help in assisting management to plan for future

course of actions (Biddle, Ma and Song, 2020). This branch of accounting helps in monitoring

and control of finance within organization. Management accounting helps in analysing results of

financial accounting so that a detailed statement which consists useful information can be

prepared so that management of organization can take suitable decisions. In this report, main

focus is on operations of prime furniture, which is dealing in all types of furniture for homes and

offices. It is a developing East London based company. Therefore, in its development phase, it is

important that it formulate effective strategies, so that they can succeed in future. This report is

prepared by the junior management accountant of company keeping focus on topics like

management accounting systems, management accounting reporting methods, link between

MAS and organizational operations.

MAIN BODY

TASK 1

(covered in PPT)

TASK 2

P3 Cost Analysis

Cost is the value incurred to the company in order to produce its products and services.

Cost is the value without mark up. Accounting with the purpose of ascertaining cost and its

relationship with profit is called cost-accounting (Bobryshev and et.al., 2015). In cost-

accounting, cost is classified into various types such as direct and indirect cost, fixed and

variable cost, operating and opportunity cost, controllable and uncontrollable cost, sunk cost, etc.

Most important classifications are direct and indirect cost and fixed and variable cost.

Inventory Cost

Inventory cost is the cost that is incurred to a company for managing its inventory. It can be

broken down to three categories:

3

Management accounting is a branch of knowledge of Accounting. This consists of

various inspection tools and techniques that help in assisting management to plan for future

course of actions (Biddle, Ma and Song, 2020). This branch of accounting helps in monitoring

and control of finance within organization. Management accounting helps in analysing results of

financial accounting so that a detailed statement which consists useful information can be

prepared so that management of organization can take suitable decisions. In this report, main

focus is on operations of prime furniture, which is dealing in all types of furniture for homes and

offices. It is a developing East London based company. Therefore, in its development phase, it is

important that it formulate effective strategies, so that they can succeed in future. This report is

prepared by the junior management accountant of company keeping focus on topics like

management accounting systems, management accounting reporting methods, link between

MAS and organizational operations.

MAIN BODY

TASK 1

(covered in PPT)

TASK 2

P3 Cost Analysis

Cost is the value incurred to the company in order to produce its products and services.

Cost is the value without mark up. Accounting with the purpose of ascertaining cost and its

relationship with profit is called cost-accounting (Bobryshev and et.al., 2015). In cost-

accounting, cost is classified into various types such as direct and indirect cost, fixed and

variable cost, operating and opportunity cost, controllable and uncontrollable cost, sunk cost, etc.

Most important classifications are direct and indirect cost and fixed and variable cost.

Inventory Cost

Inventory cost is the cost that is incurred to a company for managing its inventory. It can be

broken down to three categories:

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Ordering cost – It is the cost that is incurred to business for preparing and purchasing

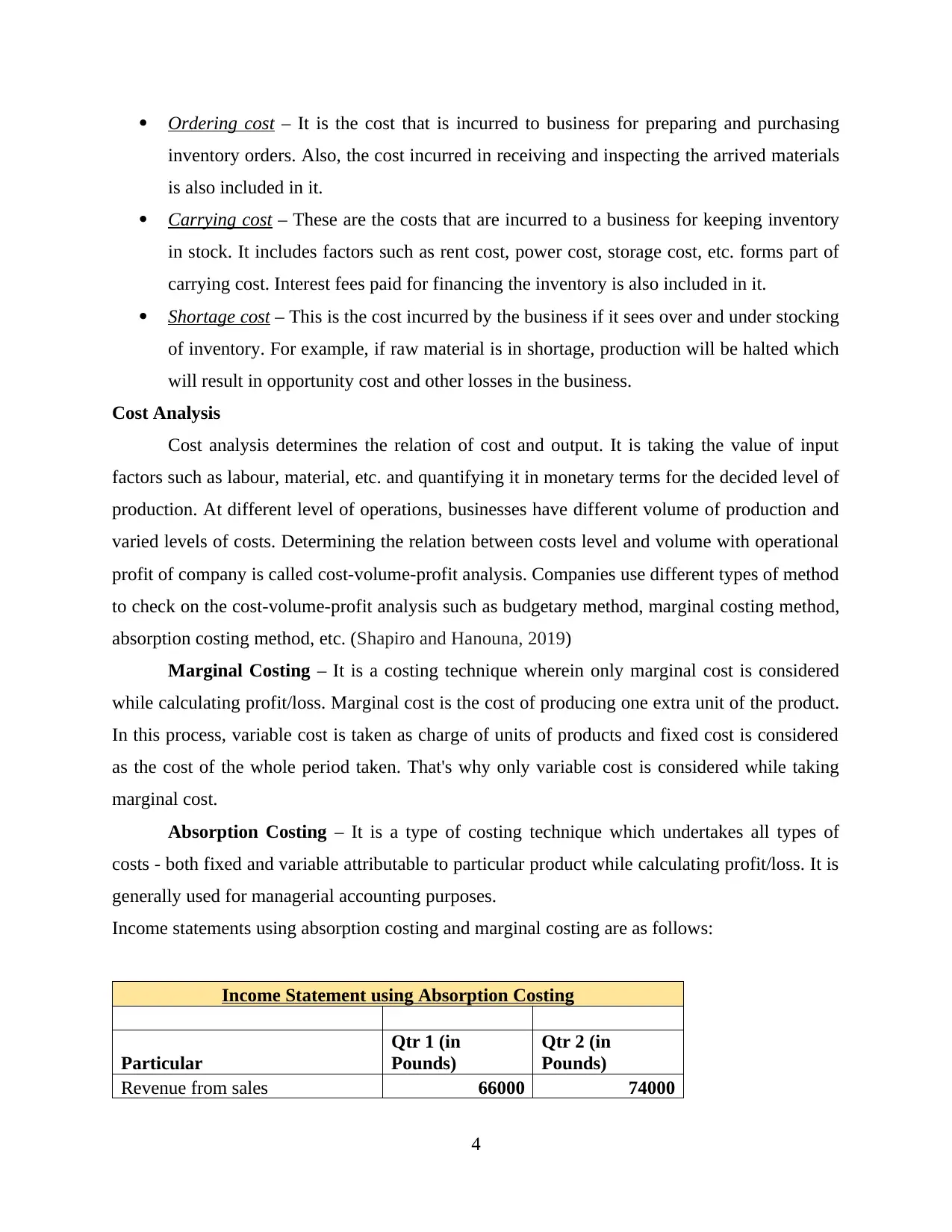

inventory orders. Also, the cost incurred in receiving and inspecting the arrived materials

is also included in it.

Carrying cost – These are the costs that are incurred to a business for keeping inventory

in stock. It includes factors such as rent cost, power cost, storage cost, etc. forms part of

carrying cost. Interest fees paid for financing the inventory is also included in it.

Shortage cost – This is the cost incurred by the business if it sees over and under stocking

of inventory. For example, if raw material is in shortage, production will be halted which

will result in opportunity cost and other losses in the business.

Cost Analysis

Cost analysis determines the relation of cost and output. It is taking the value of input

factors such as labour, material, etc. and quantifying it in monetary terms for the decided level of

production. At different level of operations, businesses have different volume of production and

varied levels of costs. Determining the relation between costs level and volume with operational

profit of company is called cost-volume-profit analysis. Companies use different types of method

to check on the cost-volume-profit analysis such as budgetary method, marginal costing method,

absorption costing method, etc. (Shapiro and Hanouna, 2019)

Marginal Costing – It is a costing technique wherein only marginal cost is considered

while calculating profit/loss. Marginal cost is the cost of producing one extra unit of the product.

In this process, variable cost is taken as charge of units of products and fixed cost is considered

as the cost of the whole period taken. That's why only variable cost is considered while taking

marginal cost.

Absorption Costing – It is a type of costing technique which undertakes all types of

costs - both fixed and variable attributable to particular product while calculating profit/loss. It is

generally used for managerial accounting purposes.

Income statements using absorption costing and marginal costing are as follows:

Income Statement using Absorption Costing

Particular

Qtr 1 (in

Pounds)

Qtr 2 (in

Pounds)

Revenue from sales 66000 74000

4

inventory orders. Also, the cost incurred in receiving and inspecting the arrived materials

is also included in it.

Carrying cost – These are the costs that are incurred to a business for keeping inventory

in stock. It includes factors such as rent cost, power cost, storage cost, etc. forms part of

carrying cost. Interest fees paid for financing the inventory is also included in it.

Shortage cost – This is the cost incurred by the business if it sees over and under stocking

of inventory. For example, if raw material is in shortage, production will be halted which

will result in opportunity cost and other losses in the business.

Cost Analysis

Cost analysis determines the relation of cost and output. It is taking the value of input

factors such as labour, material, etc. and quantifying it in monetary terms for the decided level of

production. At different level of operations, businesses have different volume of production and

varied levels of costs. Determining the relation between costs level and volume with operational

profit of company is called cost-volume-profit analysis. Companies use different types of method

to check on the cost-volume-profit analysis such as budgetary method, marginal costing method,

absorption costing method, etc. (Shapiro and Hanouna, 2019)

Marginal Costing – It is a costing technique wherein only marginal cost is considered

while calculating profit/loss. Marginal cost is the cost of producing one extra unit of the product.

In this process, variable cost is taken as charge of units of products and fixed cost is considered

as the cost of the whole period taken. That's why only variable cost is considered while taking

marginal cost.

Absorption Costing – It is a type of costing technique which undertakes all types of

costs - both fixed and variable attributable to particular product while calculating profit/loss. It is

generally used for managerial accounting purposes.

Income statements using absorption costing and marginal costing are as follows:

Income Statement using Absorption Costing

Particular

Qtr 1 (in

Pounds)

Qtr 2 (in

Pounds)

Revenue from sales 66000 74000

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

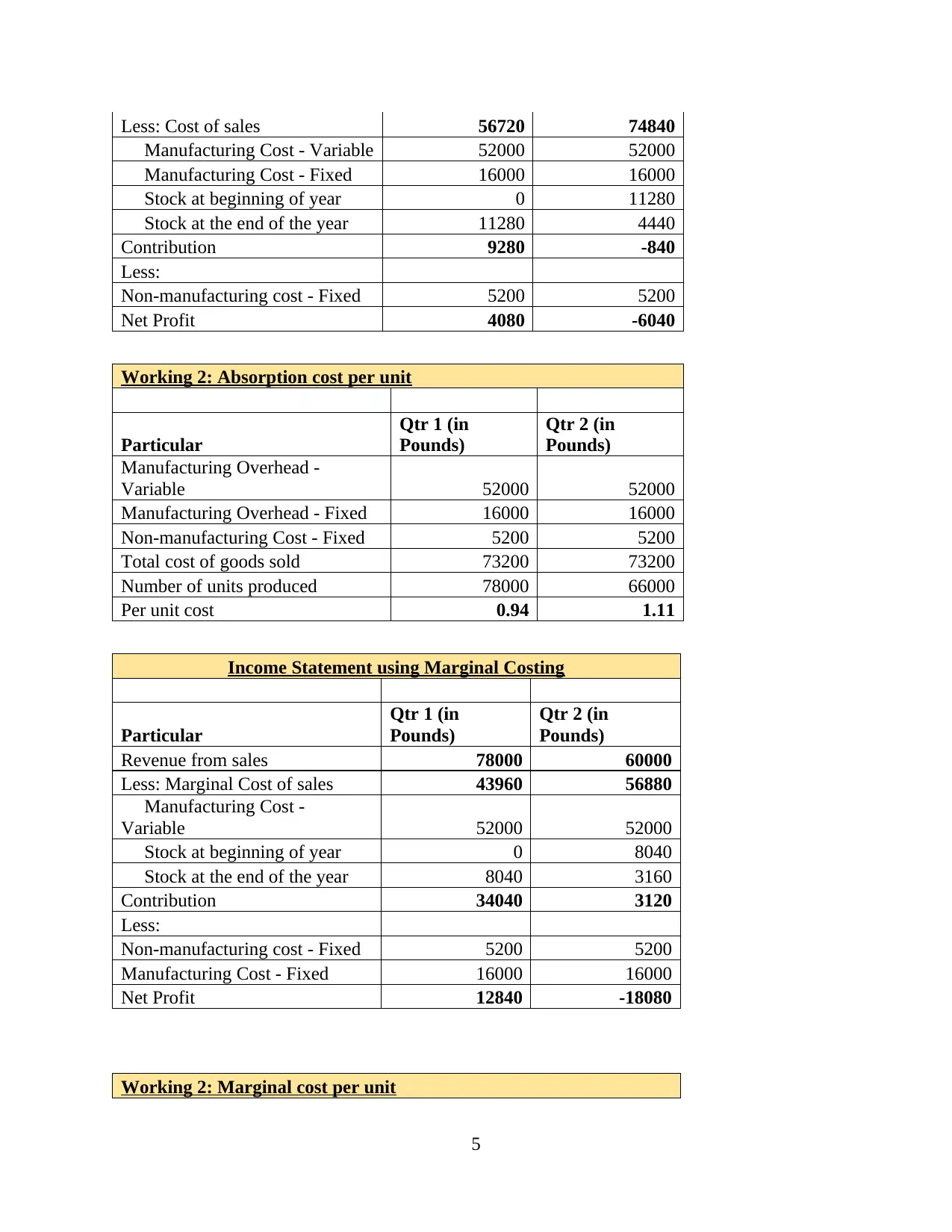

Less: Cost of sales 56720 74840

Manufacturing Cost - Variable 52000 52000

Manufacturing Cost - Fixed 16000 16000

Stock at beginning of year 0 11280

Stock at the end of the year 11280 4440

Contribution 9280 -840

Less:

Non-manufacturing cost - Fixed 5200 5200

Net Profit 4080 -6040

Working 2: Absorption cost per unit

Particular

Qtr 1 (in

Pounds)

Qtr 2 (in

Pounds)

Manufacturing Overhead -

Variable 52000 52000

Manufacturing Overhead - Fixed 16000 16000

Non-manufacturing Cost - Fixed 5200 5200

Total cost of goods sold 73200 73200

Number of units produced 78000 66000

Per unit cost 0.94 1.11

Income Statement using Marginal Costing

Particular

Qtr 1 (in

Pounds)

Qtr 2 (in

Pounds)

Revenue from sales 78000 60000

Less: Marginal Cost of sales 43960 56880

Manufacturing Cost -

Variable 52000 52000

Stock at beginning of year 0 8040

Stock at the end of the year 8040 3160

Contribution 34040 3120

Less:

Non-manufacturing cost - Fixed 5200 5200

Manufacturing Cost - Fixed 16000 16000

Net Profit 12840 -18080

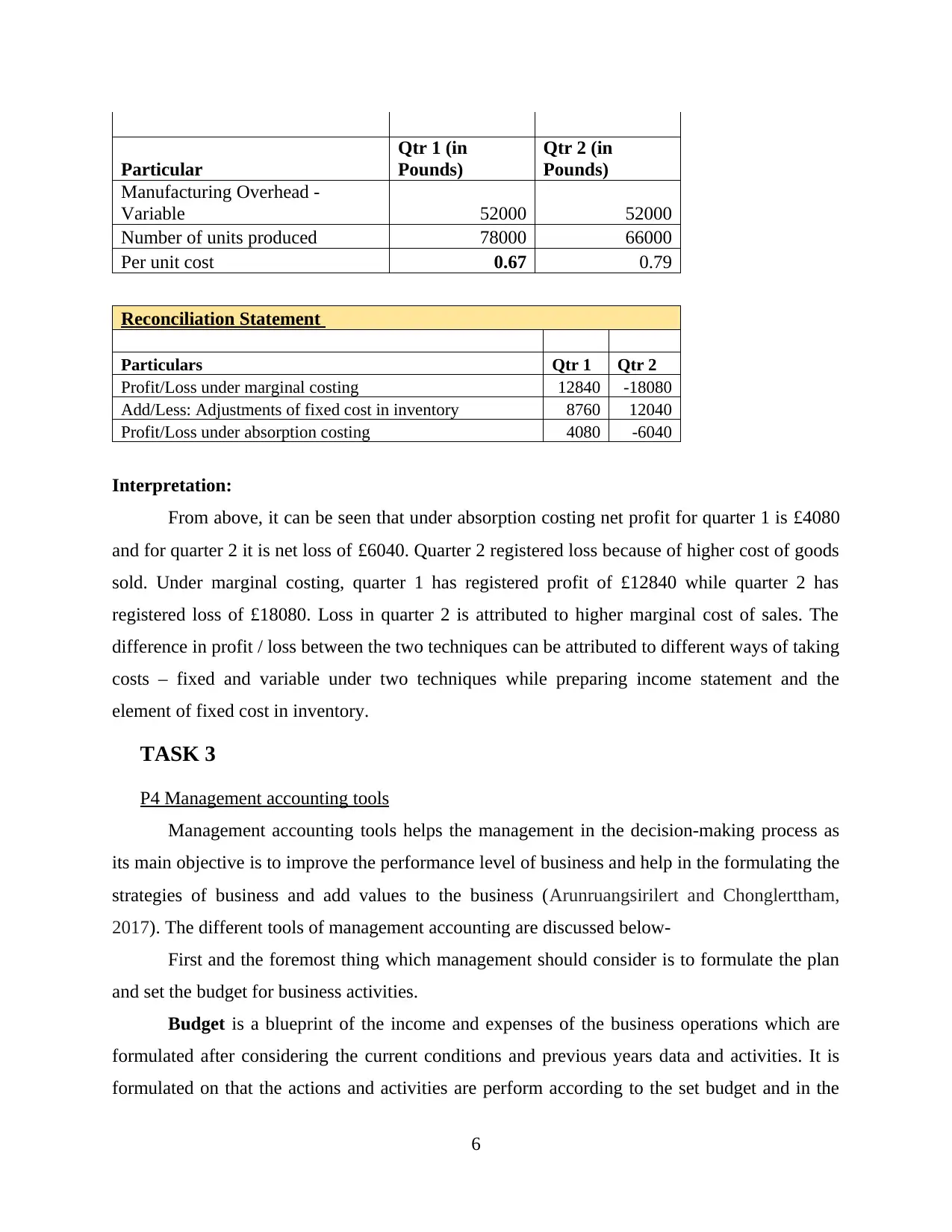

Working 2: Marginal cost per unit

5

Manufacturing Cost - Variable 52000 52000

Manufacturing Cost - Fixed 16000 16000

Stock at beginning of year 0 11280

Stock at the end of the year 11280 4440

Contribution 9280 -840

Less:

Non-manufacturing cost - Fixed 5200 5200

Net Profit 4080 -6040

Working 2: Absorption cost per unit

Particular

Qtr 1 (in

Pounds)

Qtr 2 (in

Pounds)

Manufacturing Overhead -

Variable 52000 52000

Manufacturing Overhead - Fixed 16000 16000

Non-manufacturing Cost - Fixed 5200 5200

Total cost of goods sold 73200 73200

Number of units produced 78000 66000

Per unit cost 0.94 1.11

Income Statement using Marginal Costing

Particular

Qtr 1 (in

Pounds)

Qtr 2 (in

Pounds)

Revenue from sales 78000 60000

Less: Marginal Cost of sales 43960 56880

Manufacturing Cost -

Variable 52000 52000

Stock at beginning of year 0 8040

Stock at the end of the year 8040 3160

Contribution 34040 3120

Less:

Non-manufacturing cost - Fixed 5200 5200

Manufacturing Cost - Fixed 16000 16000

Net Profit 12840 -18080

Working 2: Marginal cost per unit

5

Particular

Qtr 1 (in

Pounds)

Qtr 2 (in

Pounds)

Manufacturing Overhead -

Variable 52000 52000

Number of units produced 78000 66000

Per unit cost 0.67 0.79

Reconciliation Statement

Particulars Qtr 1 Qtr 2

Profit/Loss under marginal costing 12840 -18080

Add/Less: Adjustments of fixed cost in inventory 8760 12040

Profit/Loss under absorption costing 4080 -6040

Interpretation:

From above, it can be seen that under absorption costing net profit for quarter 1 is £4080

and for quarter 2 it is net loss of £6040. Quarter 2 registered loss because of higher cost of goods

sold. Under marginal costing, quarter 1 has registered profit of £12840 while quarter 2 has

registered loss of £18080. Loss in quarter 2 is attributed to higher marginal cost of sales. The

difference in profit / loss between the two techniques can be attributed to different ways of taking

costs – fixed and variable under two techniques while preparing income statement and the

element of fixed cost in inventory.

TASK 3

P4 Management accounting tools

Management accounting tools helps the management in the decision-making process as

its main objective is to improve the performance level of business and help in the formulating the

strategies of business and add values to the business (Arunruangsirilert and Chonglerttham,

2017). The different tools of management accounting are discussed below-

First and the foremost thing which management should consider is to formulate the plan

and set the budget for business activities.

Budget is a blueprint of the income and expenses of the business operations which are

formulated after considering the current conditions and previous years data and activities. It is

formulated on that the actions and activities are perform according to the set budget and in the

6

Qtr 1 (in

Pounds)

Qtr 2 (in

Pounds)

Manufacturing Overhead -

Variable 52000 52000

Number of units produced 78000 66000

Per unit cost 0.67 0.79

Reconciliation Statement

Particulars Qtr 1 Qtr 2

Profit/Loss under marginal costing 12840 -18080

Add/Less: Adjustments of fixed cost in inventory 8760 12040

Profit/Loss under absorption costing 4080 -6040

Interpretation:

From above, it can be seen that under absorption costing net profit for quarter 1 is £4080

and for quarter 2 it is net loss of £6040. Quarter 2 registered loss because of higher cost of goods

sold. Under marginal costing, quarter 1 has registered profit of £12840 while quarter 2 has

registered loss of £18080. Loss in quarter 2 is attributed to higher marginal cost of sales. The

difference in profit / loss between the two techniques can be attributed to different ways of taking

costs – fixed and variable under two techniques while preparing income statement and the

element of fixed cost in inventory.

TASK 3

P4 Management accounting tools

Management accounting tools helps the management in the decision-making process as

its main objective is to improve the performance level of business and help in the formulating the

strategies of business and add values to the business (Arunruangsirilert and Chonglerttham,

2017). The different tools of management accounting are discussed below-

First and the foremost thing which management should consider is to formulate the plan

and set the budget for business activities.

Budget is a blueprint of the income and expenses of the business operations which are

formulated after considering the current conditions and previous years data and activities. It is

formulated on that the actions and activities are perform according to the set budget and in the

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

last the obtain results are measured with the desired results. Here is different type of budgets

which the management of Prime Furniture can use in its operational activities.

Cash Budget

Cash budget is the blueprint of all the cash related activities that is it contains the inflow

and outflow of cash and cash equivalents. In context of Prime Furniture, the managers with the

use of cash budget identifies the cash availability and allocation of cash in the business activities.

Advantages- It provide support to the company in handling the situations of liquidations

that is under or over liquidation problems.

Disadvantages- Cash budgets are the estimations that is don't outline the exact budget

that is ups and downs can take place according to environment and lead to rigidity.

Sales Budgets

The tool is used in determining and forecasting the sales activities of the particular year.

In context of Prime Furniture, the management use this method in organizing and scheduling its

production activities (Carlsson-Wall, Kraus and Lind, 2015).

Advantages- It helps in the formulation of master budget as sales budget is one of the

important aspects which determines the overall profitability of business for that

particular year.

Disadvantages- One of the major disadvantages is that market is uncertain that is

changes in the market trends are frequent so there are chances of formulation of

inaccurate sales forecasts.

Capital Budgeting

It is the process with the help of which company identifies and analysis the various

options that are available for financing the new investment and business expansion projects. In

context of Prime Furniture, the management use this option to analyse the various available

options and select the most desirable and beneficial option (Chenhall and Moers, 2015). When a

firm is presented with a capital budgeting decision, one of its first tasks is to determine whether

or not the project will prove to be profitable. The payback period (PB), internal rate of return

(IRR) and net present value (NPV) methods are the most common approaches to project

selection.

Although an ideal capital budgeting solution is such that all three metrics will indicate the

same decision, these approaches will often produce contradictory results. Depending on

7

which the management of Prime Furniture can use in its operational activities.

Cash Budget

Cash budget is the blueprint of all the cash related activities that is it contains the inflow

and outflow of cash and cash equivalents. In context of Prime Furniture, the managers with the

use of cash budget identifies the cash availability and allocation of cash in the business activities.

Advantages- It provide support to the company in handling the situations of liquidations

that is under or over liquidation problems.

Disadvantages- Cash budgets are the estimations that is don't outline the exact budget

that is ups and downs can take place according to environment and lead to rigidity.

Sales Budgets

The tool is used in determining and forecasting the sales activities of the particular year.

In context of Prime Furniture, the management use this method in organizing and scheduling its

production activities (Carlsson-Wall, Kraus and Lind, 2015).

Advantages- It helps in the formulation of master budget as sales budget is one of the

important aspects which determines the overall profitability of business for that

particular year.

Disadvantages- One of the major disadvantages is that market is uncertain that is

changes in the market trends are frequent so there are chances of formulation of

inaccurate sales forecasts.

Capital Budgeting

It is the process with the help of which company identifies and analysis the various

options that are available for financing the new investment and business expansion projects. In

context of Prime Furniture, the management use this option to analyse the various available

options and select the most desirable and beneficial option (Chenhall and Moers, 2015). When a

firm is presented with a capital budgeting decision, one of its first tasks is to determine whether

or not the project will prove to be profitable. The payback period (PB), internal rate of return

(IRR) and net present value (NPV) methods are the most common approaches to project

selection.

Although an ideal capital budgeting solution is such that all three metrics will indicate the

same decision, these approaches will often produce contradictory results. Depending on

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

management's preferences and selection criteria, more emphasis will be put on one approach

over another. Nonetheless, there are common advantages and disadvantages associated with

these widely used valuation methods.

Advantages- The capital budgeting tools helps in choosing the right direction and helps

in minimising the risk of wrong investment.

Disadvantages- It is based on the predictions so any wrong prediction can lead to

problems and business need to suffer due to wrong decisions.

TASK 4

P5 Usefulness of Management Accounting system in solving financial problems

Financial problems: Every business is facing various problems and risks while working

in a business environment. In case when management fails to foresee problems and predicting

possible solutions to these issues, company is confronted by several problems like reduction in

sales, increased expenses, downfall in growth opportunities, etc. Two major problems are

discussed below:

Sales downfall: Every product undergoes a cycle which includes four stages,

introduction, growth, maturity and decline. These four stages have different sales volume of

product. If proper strategies are not adopted, then product can be confronted with a decline in

sales volume. This downfall can have various possible reasons like better marketing policies of

competitors, harsh business environment, uncertainties in trade laws, dynamic taste and

preferences of customers, etc. Decline is sales volume puts a direct impact on revenue and

growth of company.

Increasing costs of raw materials: This risk can be posed due to several factors like

increase in cost of transportation, increase in bargaining power of supplier, increase in tax rates,

etc. This will lead to increase in operating expenditures and hence, decreased profit margins.

This increase in cost will result into ultimate rise in final price and thus, can put a negative

impact on sales of company.

Financial governance: It refers to a systematic setup of monitoring and controlling financial

information of a company. The main motive of this process in to track financial transactions in

interest of all stakeholders. If any risk is identified earlier than they can devise suitable strategy

8

over another. Nonetheless, there are common advantages and disadvantages associated with

these widely used valuation methods.

Advantages- The capital budgeting tools helps in choosing the right direction and helps

in minimising the risk of wrong investment.

Disadvantages- It is based on the predictions so any wrong prediction can lead to

problems and business need to suffer due to wrong decisions.

TASK 4

P5 Usefulness of Management Accounting system in solving financial problems

Financial problems: Every business is facing various problems and risks while working

in a business environment. In case when management fails to foresee problems and predicting

possible solutions to these issues, company is confronted by several problems like reduction in

sales, increased expenses, downfall in growth opportunities, etc. Two major problems are

discussed below:

Sales downfall: Every product undergoes a cycle which includes four stages,

introduction, growth, maturity and decline. These four stages have different sales volume of

product. If proper strategies are not adopted, then product can be confronted with a decline in

sales volume. This downfall can have various possible reasons like better marketing policies of

competitors, harsh business environment, uncertainties in trade laws, dynamic taste and

preferences of customers, etc. Decline is sales volume puts a direct impact on revenue and

growth of company.

Increasing costs of raw materials: This risk can be posed due to several factors like

increase in cost of transportation, increase in bargaining power of supplier, increase in tax rates,

etc. This will lead to increase in operating expenditures and hence, decreased profit margins.

This increase in cost will result into ultimate rise in final price and thus, can put a negative

impact on sales of company.

Financial governance: It refers to a systematic setup of monitoring and controlling financial

information of a company. The main motive of this process in to track financial transactions in

interest of all stakeholders. If any risk is identified earlier than they can devise suitable strategy

8

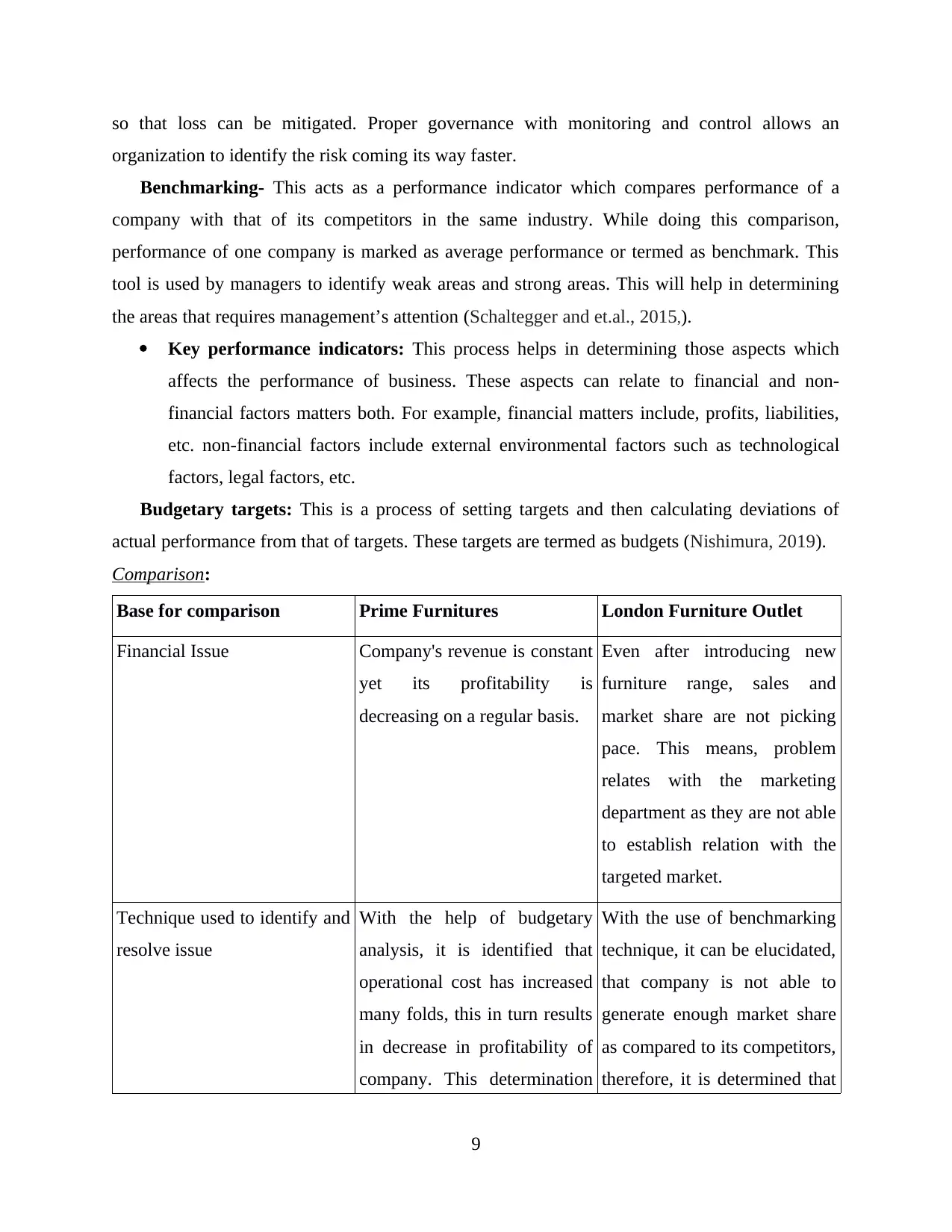

so that loss can be mitigated. Proper governance with monitoring and control allows an

organization to identify the risk coming its way faster.

Benchmarking- This acts as a performance indicator which compares performance of a

company with that of its competitors in the same industry. While doing this comparison,

performance of one company is marked as average performance or termed as benchmark. This

tool is used by managers to identify weak areas and strong areas. This will help in determining

the areas that requires management’s attention (Schaltegger and et.al., 2015,).

Key performance indicators: This process helps in determining those aspects which

affects the performance of business. These aspects can relate to financial and non-

financial factors matters both. For example, financial matters include, profits, liabilities,

etc. non-financial factors include external environmental factors such as technological

factors, legal factors, etc.

Budgetary targets: This is a process of setting targets and then calculating deviations of

actual performance from that of targets. These targets are termed as budgets (Nishimura, 2019).

Comparison:

Base for comparison Prime Furnitures London Furniture Outlet

Financial Issue Company's revenue is constant

yet its profitability is

decreasing on a regular basis.

Even after introducing new

furniture range, sales and

market share are not picking

pace. This means, problem

relates with the marketing

department as they are not able

to establish relation with the

targeted market.

Technique used to identify and

resolve issue

With the help of budgetary

analysis, it is identified that

operational cost has increased

many folds, this in turn results

in decrease in profitability of

company. This determination

With the use of benchmarking

technique, it can be elucidated,

that company is not able to

generate enough market share

as compared to its competitors,

therefore, it is determined that

9

organization to identify the risk coming its way faster.

Benchmarking- This acts as a performance indicator which compares performance of a

company with that of its competitors in the same industry. While doing this comparison,

performance of one company is marked as average performance or termed as benchmark. This

tool is used by managers to identify weak areas and strong areas. This will help in determining

the areas that requires management’s attention (Schaltegger and et.al., 2015,).

Key performance indicators: This process helps in determining those aspects which

affects the performance of business. These aspects can relate to financial and non-

financial factors matters both. For example, financial matters include, profits, liabilities,

etc. non-financial factors include external environmental factors such as technological

factors, legal factors, etc.

Budgetary targets: This is a process of setting targets and then calculating deviations of

actual performance from that of targets. These targets are termed as budgets (Nishimura, 2019).

Comparison:

Base for comparison Prime Furnitures London Furniture Outlet

Financial Issue Company's revenue is constant

yet its profitability is

decreasing on a regular basis.

Even after introducing new

furniture range, sales and

market share are not picking

pace. This means, problem

relates with the marketing

department as they are not able

to establish relation with the

targeted market.

Technique used to identify and

resolve issue

With the help of budgetary

analysis, it is identified that

operational cost has increased

many folds, this in turn results

in decrease in profitability of

company. This determination

With the use of benchmarking

technique, it can be elucidated,

that company is not able to

generate enough market share

as compared to its competitors,

therefore, it is determined that

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

is done by comparing actual

performance of company with

budgeted one. Budgeted cost

and actual cost differed.

management need to focus

more upon their marketing

strategies so that they can

reach to a wider market area.

MAS Cost accounting system – this

is a system which is applied to

analyse the cost which is

already occurred. Under this

system, those areas are

identified which have cost

occurred more than what is

actually needed. Therefore,

now company can take

required corrective measures

to control and monitor costs

(Hsu and Lin, 2016).

Differential pricing system – in

this system, company now

properly determines the

targeted market and do proper

segmenting within the target

market. This segmentation

helps in setting prices

according to the affordability

of each segment.

Management accounting system to solve financial problems

Management accountants help senior management in planning and decision-making

tasks. They possess the combination of leadership and managerial expertise. They use techniques

like absorption costing, break even analysis etc. to identify significant factors affecting financial

health of the organization. Then, using various techniques of MAS, senior management prepares

strategies and policies to improve business of organization. above table shows how different

management accounting systems helps in solving financial problems in time so that maximum

profitability can be generated (Ponisciakova, Gogolova, and Ivankova, 2015). The report

proposes many ways in which management accountants may guide their company’s towards the

sustainable success of the business:

Identify the social and environmental trends which will impact on the organization’s

capability to build value over the time.

Liking sustainable corporate challenges to the strategy of the company, performance

outlook, business model and license to function.

10

performance of company with

budgeted one. Budgeted cost

and actual cost differed.

management need to focus

more upon their marketing

strategies so that they can

reach to a wider market area.

MAS Cost accounting system – this

is a system which is applied to

analyse the cost which is

already occurred. Under this

system, those areas are

identified which have cost

occurred more than what is

actually needed. Therefore,

now company can take

required corrective measures

to control and monitor costs

(Hsu and Lin, 2016).

Differential pricing system – in

this system, company now

properly determines the

targeted market and do proper

segmenting within the target

market. This segmentation

helps in setting prices

according to the affordability

of each segment.

Management accounting system to solve financial problems

Management accountants help senior management in planning and decision-making

tasks. They possess the combination of leadership and managerial expertise. They use techniques

like absorption costing, break even analysis etc. to identify significant factors affecting financial

health of the organization. Then, using various techniques of MAS, senior management prepares

strategies and policies to improve business of organization. above table shows how different

management accounting systems helps in solving financial problems in time so that maximum

profitability can be generated (Ponisciakova, Gogolova, and Ivankova, 2015). The report

proposes many ways in which management accountants may guide their company’s towards the

sustainable success of the business:

Identify the social and environmental trends which will impact on the organization’s

capability to build value over the time.

Liking sustainable corporate challenges to the strategy of the company, performance

outlook, business model and license to function.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Describe the impact of the sustainability issues in strong business terms comprising of

how and when they would affect the company.

Establish KPIs which support sustainable and strategic goals.

Apply tools and techniques of management accounting like natural resource availability

scenario planning, carbon foot-printing and lifecycle costing to assist incorporate

sustainability issues into the process of decision-making.

Generate reports which include information on sustainability effects to inform pricing

and budgeting decisions, strategic planning and investment appraisals.

CONCLUSION

Management accounting system helps in assisting management to plan for future actions

and implement suitable controlling tools. These all activities are directed towards one objective

and that is to achieve maximum profitability. This objective can be achieved by using various

techniques like budgetary control, break – even analysis, etc. Management accounting reports

assist in providing complete details so that no vital information is omitted in course of planning.

One important conclusion of this report is that branch of management accounting along with

related tools and techniques helps managers to address financial issues and also aid in taking

corrective actions in time (Dimitropoulos, Leventis and Dedoulis, 2016).

11

how and when they would affect the company.

Establish KPIs which support sustainable and strategic goals.

Apply tools and techniques of management accounting like natural resource availability

scenario planning, carbon foot-printing and lifecycle costing to assist incorporate

sustainability issues into the process of decision-making.

Generate reports which include information on sustainability effects to inform pricing

and budgeting decisions, strategic planning and investment appraisals.

CONCLUSION

Management accounting system helps in assisting management to plan for future actions

and implement suitable controlling tools. These all activities are directed towards one objective

and that is to achieve maximum profitability. This objective can be achieved by using various

techniques like budgetary control, break – even analysis, etc. Management accounting reports

assist in providing complete details so that no vital information is omitted in course of planning.

One important conclusion of this report is that branch of management accounting along with

related tools and techniques helps managers to address financial issues and also aid in taking

corrective actions in time (Dimitropoulos, Leventis and Dedoulis, 2016).

11

REFERENCES

Books and Journals

Arunruangsirilert, T. and Chonglerttham, S., 2017. Effect of corporate governance

characteristics on strategic management accounting in Thailand. Asian Review of

Accounting.

Bobryshev, A.N. and et.al., 2015. The concept of management accounting in crisis conditions.

Journal of Advanced Research in Law and Economics. 6(3 (13)). p.520.

Carlsson-Wall, M., Kraus, K. and Lind, J., 2015. Strategic management accounting in close

inter-organisational relationships. Accounting and Business Research. 45(1). pp.27-54.

Chenhall, R.H. and Moers, F., 2015. The role of innovation in the evolution of management

accounting and its integration into management control. Accounting, organizations and

society. 47. pp.1-13.

Shapiro, A.C. and Hanouna, P., 2019. Multinational financial management. John Wiley & Sons.

Biddle, G.C., Ma, M.L. and Song, F.M., 2020. Accounting conservatism and bankruptcy

risk. Journal of Accounting, Auditing and Finance, Forthcoming.

Schaltegger, S and et.al., 2015. Management roles and sustainability information. Exploring

corporate practice. Australian Accounting Review.25(4) pp.328-345.

Nishimura, A., 2019. Comprehensive Opportunity and Lost Opportunity Control Model and

Enterprise Risk Management. In Management, Uncertainty, and Accounting (pp. 185-

213). Palgrave Macmillan, Singapore.

Hsu, P.H. and Lin, Y.R., 2016. Fair value accounting and Earnings Management. Eurasian

Journal of Business and Management. 4(2). pp.41-54.

Ponisciakova, O., Gogolova, M. and Ivankova, K., 2015. The use of accounting information

system for the management of business costs. Procedia Economics and Finance. 26.

pp.418-422.

Dimitropoulos, P., Leventis, S. and Dedoulis, E., 2016. Managing the European football

industry: UEFA’s regulatory intervention and the impact on accounting

quality. European Sport Management Quarterly. 16(4). pp.459-486.

12

Books and Journals

Arunruangsirilert, T. and Chonglerttham, S., 2017. Effect of corporate governance

characteristics on strategic management accounting in Thailand. Asian Review of

Accounting.

Bobryshev, A.N. and et.al., 2015. The concept of management accounting in crisis conditions.

Journal of Advanced Research in Law and Economics. 6(3 (13)). p.520.

Carlsson-Wall, M., Kraus, K. and Lind, J., 2015. Strategic management accounting in close

inter-organisational relationships. Accounting and Business Research. 45(1). pp.27-54.

Chenhall, R.H. and Moers, F., 2015. The role of innovation in the evolution of management

accounting and its integration into management control. Accounting, organizations and

society. 47. pp.1-13.

Shapiro, A.C. and Hanouna, P., 2019. Multinational financial management. John Wiley & Sons.

Biddle, G.C., Ma, M.L. and Song, F.M., 2020. Accounting conservatism and bankruptcy

risk. Journal of Accounting, Auditing and Finance, Forthcoming.

Schaltegger, S and et.al., 2015. Management roles and sustainability information. Exploring

corporate practice. Australian Accounting Review.25(4) pp.328-345.

Nishimura, A., 2019. Comprehensive Opportunity and Lost Opportunity Control Model and

Enterprise Risk Management. In Management, Uncertainty, and Accounting (pp. 185-

213). Palgrave Macmillan, Singapore.

Hsu, P.H. and Lin, Y.R., 2016. Fair value accounting and Earnings Management. Eurasian

Journal of Business and Management. 4(2). pp.41-54.

Ponisciakova, O., Gogolova, M. and Ivankova, K., 2015. The use of accounting information

system for the management of business costs. Procedia Economics and Finance. 26.

pp.418-422.

Dimitropoulos, P., Leventis, S. and Dedoulis, E., 2016. Managing the European football

industry: UEFA’s regulatory intervention and the impact on accounting

quality. European Sport Management Quarterly. 16(4). pp.459-486.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.