Management Accounting Report: Cost Analysis & Planning Tools

VerifiedAdded on 2022/12/28

|17

|4535

|91

Report

AI Summary

This report provides a comprehensive overview of management accounting principles and their practical application within Prime Furniture, a London-based private limited company. The report delves into the core requirements of management accounting, differentiating it from financial accounting and highlighting the importance of various systems, including cost accounting, inventory management, job costing, and price optimization. It explores different methods for management accounting reporting, emphasizing the significance of understandable information. The report then proceeds to demonstrate cost calculations using absorption and marginal costing techniques, preparing income statements for both methods and providing reconciliation. Furthermore, it elaborates on planning tools utilized in management accounting, particularly budgeting, including capital and operating budgets. Finally, the report compares how organizations adapt management accounting systems to address financial problems, offering valuable insights for decision-making and financial strategy.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1: Management Accounting with its essential Requirement and types:....................................1

P2. Methods for management accounting reporting....................................................................3

TASK 2............................................................................................................................................4

P3: Calculations of cost by utilising appropriates techniques for cost analysis for preparing

income statement by using absorption as well as marginal costs:...............................................4

TASK 3............................................................................................................................................7

P4: Explanation of planning tools which is utilised in management accounting:.......................7

TASK 4..........................................................................................................................................11

P5: Comparison of ways in which organizations adapt management accounting system as a

response to financial problems:.................................................................................................11

CONCLUSION.............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1: Management Accounting with its essential Requirement and types:....................................1

P2. Methods for management accounting reporting....................................................................3

TASK 2............................................................................................................................................4

P3: Calculations of cost by utilising appropriates techniques for cost analysis for preparing

income statement by using absorption as well as marginal costs:...............................................4

TASK 3............................................................................................................................................7

P4: Explanation of planning tools which is utilised in management accounting:.......................7

TASK 4..........................................................................................................................................11

P5: Comparison of ways in which organizations adapt management accounting system as a

response to financial problems:.................................................................................................11

CONCLUSION.............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION

Management accounting can be elaborated as a procedure of identification, measurement,

analysis, interpretation and communication of financial information or data to managers of an

organization for the purpose of pursuing goals of business. Purpose of applying management

accounting is to assist internal users of a firm for making decisions that are well-informed.

Hence, it encompasses all financial information which is assessed by internal users of a company

(Agrawal, 2018). This report is based on analysis of management accounting in Prime Furniture.

Entity is based in London. It is a private limited company which was started in the year 2019.

This report covers demonstration of management accounting systems and reports.

Further, techniques of management accounting are applied. Apart from it, different planning

tools that are utilised in management accounting are applied. And lastly, comparative ways in

which business management accounting as a respond for financial problems.

TASK 1

P1: Management Accounting with its essential Requirement and types:

Management Accounting:

Management accounting is the process of measuring, assessing and communicating the

information to the manager. Prime furniture use management accounting for the purpose of

getting information about their organization, for better decision making and for planning,

controlling organizational activity (Aouni, McGillis and Abdulkarim, 2017).

Management Accounting System:

Management accounting system is the process of implementing management accounting

in organization is called Management Accounting. This helps the manger for the assessment of

organization purpose and help them to ensure better control over the financial activity. There are

different type of management accounting system which are used by Prime Furniture to carry out

operations for goal attainment.

Origin, role and principles of management accounting:

Management accounting was originated in early 1800s with the objective of use the

information in policy formulation and decision making. Role of management accounting in

1

Management accounting can be elaborated as a procedure of identification, measurement,

analysis, interpretation and communication of financial information or data to managers of an

organization for the purpose of pursuing goals of business. Purpose of applying management

accounting is to assist internal users of a firm for making decisions that are well-informed.

Hence, it encompasses all financial information which is assessed by internal users of a company

(Agrawal, 2018). This report is based on analysis of management accounting in Prime Furniture.

Entity is based in London. It is a private limited company which was started in the year 2019.

This report covers demonstration of management accounting systems and reports.

Further, techniques of management accounting are applied. Apart from it, different planning

tools that are utilised in management accounting are applied. And lastly, comparative ways in

which business management accounting as a respond for financial problems.

TASK 1

P1: Management Accounting with its essential Requirement and types:

Management Accounting:

Management accounting is the process of measuring, assessing and communicating the

information to the manager. Prime furniture use management accounting for the purpose of

getting information about their organization, for better decision making and for planning,

controlling organizational activity (Aouni, McGillis and Abdulkarim, 2017).

Management Accounting System:

Management accounting system is the process of implementing management accounting

in organization is called Management Accounting. This helps the manger for the assessment of

organization purpose and help them to ensure better control over the financial activity. There are

different type of management accounting system which are used by Prime Furniture to carry out

operations for goal attainment.

Origin, role and principles of management accounting:

Management accounting was originated in early 1800s with the objective of use the

information in policy formulation and decision making. Role of management accounting in

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Prime furniture is to provide essential information to the manager that help the manager in

management of strategy and risk (Endenich, Trapp, and Brandau, 2017). Principle of

management accounting is as follows:

Principle of Causality: Principle of causality defines the relationship between input and

output resources contributed in the process of production. Strong causality relationship helps

business such as Prime Furniture to achieve its goals where weaker causality relationship

increase the cost of the firm.

Principle of Analogy: Principle of analogy states how the user of accounting information

apply the learning and knowledge to the operation to utilize the resources.

Distinction between management and financial accounting

Financial accounting Management accounting

Financial accounting is the practice of

recording, reporting transaction of business in

the financial statement like balance sheet, cash

flow etc.

Management accounting refers to identifying,

assessing and communicating financial

information to the company in order to attain

organizational goal.

In prime furniture, it is prepared for the

external users of the company like shareholder,

customer, regulatory authority etc.

It is prepared for the internal users like

manager of the company.

Financial accounting is mandatory for the

company.

It is optional for the company.

Essential requirements of management accounting systems

Cost-accounting system: Cost accounting is a system used to approximate the cost of

product by evaluating fixed and variable cost to identify the profitability and cost control

of the firm (Guinea,2016). Company like Prime furniture require cost accounting to

estimate the cost of the product.

Inventory Management System: Inventory management is the procedure to track the

goods of company start from purchase to the sale of the goods. Essential requirement of

the system in Prime Furniture is to guide managers in managing situations of over stock

and under stock.

2

management of strategy and risk (Endenich, Trapp, and Brandau, 2017). Principle of

management accounting is as follows:

Principle of Causality: Principle of causality defines the relationship between input and

output resources contributed in the process of production. Strong causality relationship helps

business such as Prime Furniture to achieve its goals where weaker causality relationship

increase the cost of the firm.

Principle of Analogy: Principle of analogy states how the user of accounting information

apply the learning and knowledge to the operation to utilize the resources.

Distinction between management and financial accounting

Financial accounting Management accounting

Financial accounting is the practice of

recording, reporting transaction of business in

the financial statement like balance sheet, cash

flow etc.

Management accounting refers to identifying,

assessing and communicating financial

information to the company in order to attain

organizational goal.

In prime furniture, it is prepared for the

external users of the company like shareholder,

customer, regulatory authority etc.

It is prepared for the internal users like

manager of the company.

Financial accounting is mandatory for the

company.

It is optional for the company.

Essential requirements of management accounting systems

Cost-accounting system: Cost accounting is a system used to approximate the cost of

product by evaluating fixed and variable cost to identify the profitability and cost control

of the firm (Guinea,2016). Company like Prime furniture require cost accounting to

estimate the cost of the product.

Inventory Management System: Inventory management is the procedure to track the

goods of company start from purchase to the sale of the goods. Essential requirement of

the system in Prime Furniture is to guide managers in managing situations of over stock

and under stock.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Job-Costing System: Job costing is a process of estimating the cost of particular job in

the context of customer specification. Job Costing is essential for Prime furniture as it

track the cost of material, labour and overhead related to particular job.

Price-Optimising System: The price optimising system is the process of estimating the

fluctuation of demand at different price level in order to recommand best price for the

product which provide profit to the business.

Benefits of Management Accounting System:

Cost-Accounting System Manager of Prime Furniture use this system to estimate the

cost of product in order to gain profit.

Inventory Management System This system helps manager of Prime furniture in tracking

inventory so that firm produce estimated inventory.

Job-Costing System It helps to provide estimation of cost of a particular job to

the manager of Prime furniture.

Price-Optimising System It help the management team of Prime furniture to set the

best price of the product.

P2. Methods for management accounting reporting

Importance of Information Presented in Understandable way:

Information presented in Management accounting should be in understandable way as it

helps the manager to understand each activity of organization and it also saves the time of

manager to understand the problem (Kumarasiri,2017). If the information is presented in

understandable way it will help the manager to timely identify the problem and make solution for

the same in order to attain organizational goals.

Types of Managerial Accounting Reports:

Budget Report: It include critical analysis of company's performance in order to cut the

overall cost of business. Prime furniture need budget report to guide manager to cut cost and

offer better incentive to the staff.

3

the context of customer specification. Job Costing is essential for Prime furniture as it

track the cost of material, labour and overhead related to particular job.

Price-Optimising System: The price optimising system is the process of estimating the

fluctuation of demand at different price level in order to recommand best price for the

product which provide profit to the business.

Benefits of Management Accounting System:

Cost-Accounting System Manager of Prime Furniture use this system to estimate the

cost of product in order to gain profit.

Inventory Management System This system helps manager of Prime furniture in tracking

inventory so that firm produce estimated inventory.

Job-Costing System It helps to provide estimation of cost of a particular job to

the manager of Prime furniture.

Price-Optimising System It help the management team of Prime furniture to set the

best price of the product.

P2. Methods for management accounting reporting

Importance of Information Presented in Understandable way:

Information presented in Management accounting should be in understandable way as it

helps the manager to understand each activity of organization and it also saves the time of

manager to understand the problem (Kumarasiri,2017). If the information is presented in

understandable way it will help the manager to timely identify the problem and make solution for

the same in order to attain organizational goals.

Types of Managerial Accounting Reports:

Budget Report: It include critical analysis of company's performance in order to cut the

overall cost of business. Prime furniture need budget report to guide manager to cut cost and

offer better incentive to the staff.

3

Account Receivable Report: Account receivable reports help those company who

extend credit in order to manage their cash flows. It help managers of Prime furniture to find out

defaulter and also guide the company to change their collection policy.

Performance Report: Performance report helps to analyse the performance of the

company and its employees. Manager of Prime furniture use this report to make strategic

decision related to the company.

TASK 2

P3: Calculations of cost by utilising appropriates techniques for cost analysis for preparing

income statement by using absorption as well as marginal costs:

Cost refers to a monetary value that is spend by an organization for functioning its

operations (Libby and Salterio, 2019). Costs are of basically three types, i.e., fixed, variable and

semi-variable. These costs are further explained below:

Fixed costs: This type of cost does not vary with variations in level of output produced in

a firm. Fixed cost of Prime Furniture involves rent, insurance, legal charges etc.

Variable costs: It is depended on number of output produced in an enterprise. Hence, it

can be noted that variable cost is directly proportional to level of produced units.

Different types of variable costs that incurs in Prime Furniture are direct labour, raw

materials, etc.

Semi variable costs: It refers to a mixture of fixed as well as variable components. An

example of semi-variable costs is payment of commissions (Ostaev and Khosiev, 2018).

Cost analysis can be defined as a measure of relationship between cost and output. In

other words, approach of cost analysis helps in defining optimum production level.

Absorption costing: This method of costing captures all costs which is associated with

manufacturing of a product. Absorption costing considers both variable as well as fixed cost for

each produced unit.

Marginal costing: This method of costing indicates charging of variable costs to units

produced and fixed cost that is attributable for specific period of time.

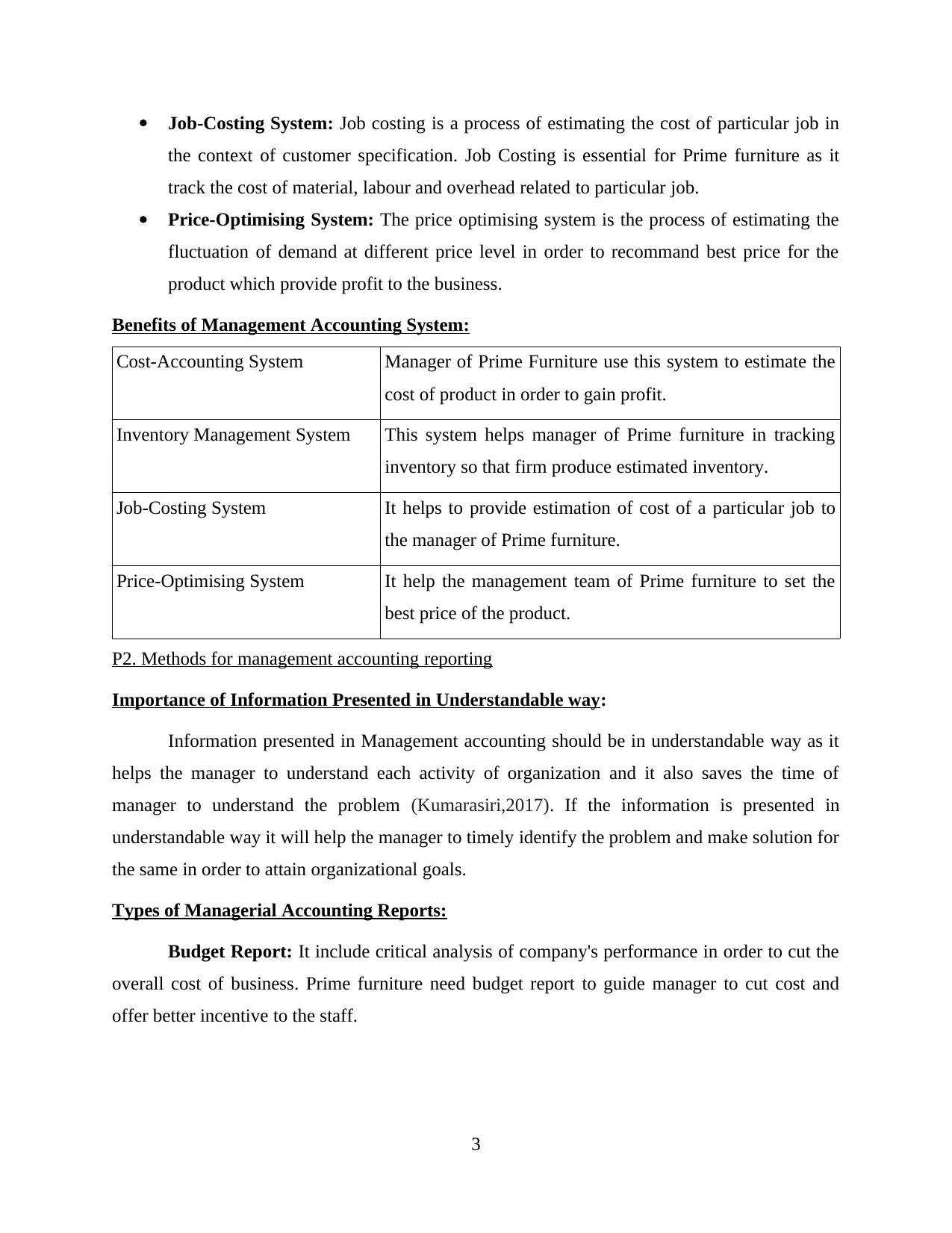

Statement of marginal costing for first quarter

(£) Amount

4

extend credit in order to manage their cash flows. It help managers of Prime furniture to find out

defaulter and also guide the company to change their collection policy.

Performance Report: Performance report helps to analyse the performance of the

company and its employees. Manager of Prime furniture use this report to make strategic

decision related to the company.

TASK 2

P3: Calculations of cost by utilising appropriates techniques for cost analysis for preparing

income statement by using absorption as well as marginal costs:

Cost refers to a monetary value that is spend by an organization for functioning its

operations (Libby and Salterio, 2019). Costs are of basically three types, i.e., fixed, variable and

semi-variable. These costs are further explained below:

Fixed costs: This type of cost does not vary with variations in level of output produced in

a firm. Fixed cost of Prime Furniture involves rent, insurance, legal charges etc.

Variable costs: It is depended on number of output produced in an enterprise. Hence, it

can be noted that variable cost is directly proportional to level of produced units.

Different types of variable costs that incurs in Prime Furniture are direct labour, raw

materials, etc.

Semi variable costs: It refers to a mixture of fixed as well as variable components. An

example of semi-variable costs is payment of commissions (Ostaev and Khosiev, 2018).

Cost analysis can be defined as a measure of relationship between cost and output. In

other words, approach of cost analysis helps in defining optimum production level.

Absorption costing: This method of costing captures all costs which is associated with

manufacturing of a product. Absorption costing considers both variable as well as fixed cost for

each produced unit.

Marginal costing: This method of costing indicates charging of variable costs to units

produced and fixed cost that is attributable for specific period of time.

Statement of marginal costing for first quarter

(£) Amount

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Sales 66, 000

Cost of Sales:

Opening Inventory - - -

Variable cost (78,000 * 0.65) 50, 700

________

50, 700

Less: Closing

Inventory

( 12,000 * 0.65 ) 7800

________

-42, 900

________

Contribution 23, 100

Less: Fixed cost -16, 000

Less: Fixed selling and

administration cost

-5, 200

________

Actual net profit 1, 900

Statement of marginal costing for second quarter

Workings(£)

Sales 74, 000

Cost of Sales

Opening inventory 12,000 * 0.65 7, 800 -

Variable 66,000 * 0.65 42, 900

________

5

Cost of Sales:

Opening Inventory - - -

Variable cost (78,000 * 0.65) 50, 700

________

50, 700

Less: Closing

Inventory

( 12,000 * 0.65 ) 7800

________

-42, 900

________

Contribution 23, 100

Less: Fixed cost -16, 000

Less: Fixed selling and

administration cost

-5, 200

________

Actual net profit 1, 900

Statement of marginal costing for second quarter

Workings(£)

Sales 74, 000

Cost of Sales

Opening inventory 12,000 * 0.65 7, 800 -

Variable 66,000 * 0.65 42, 900

________

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

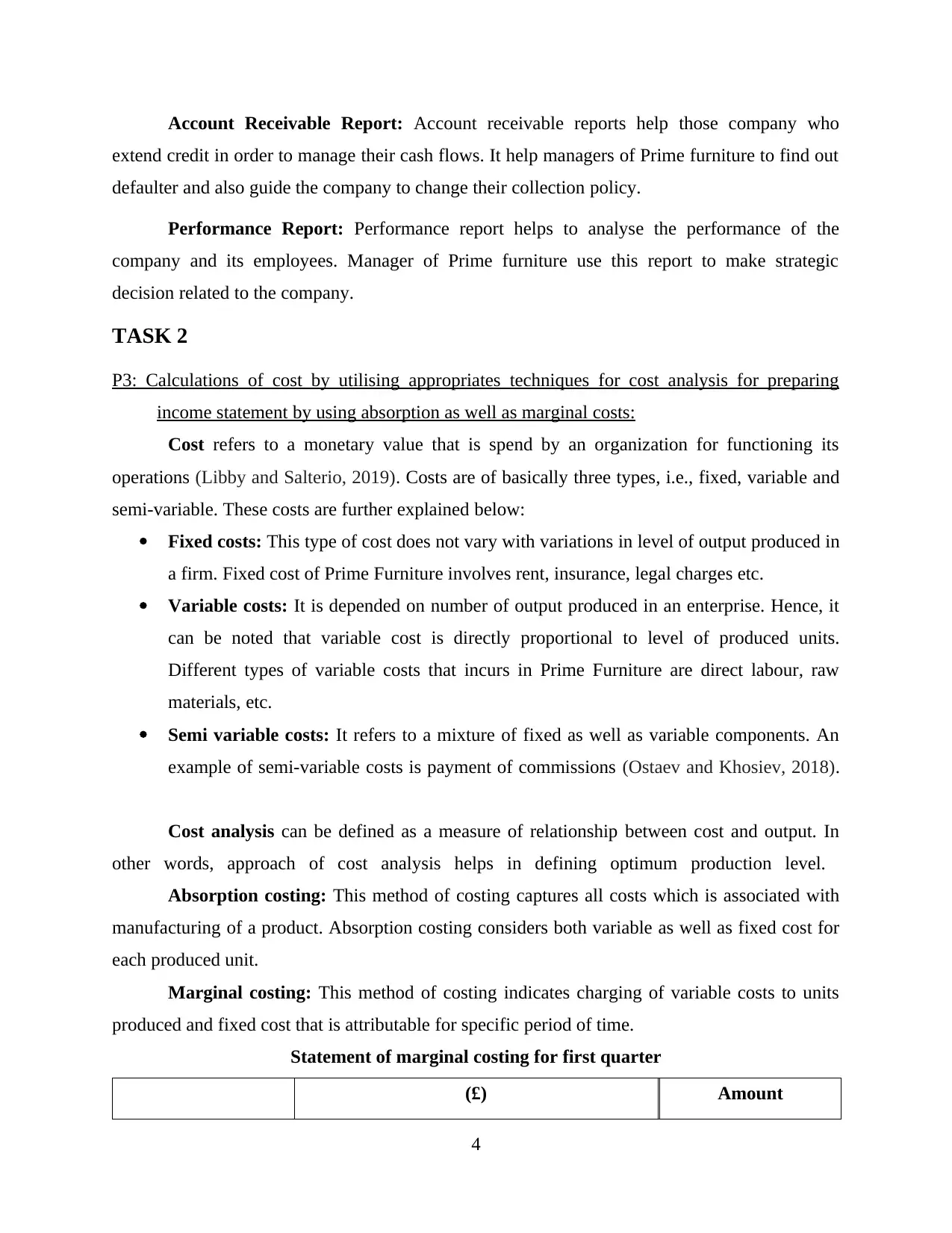

50, 700

Less: Closing

inventory

4,000 * 0.65 -2, 600

________

-48, 100

________

Contribution 25, 900

Less: Fixed Cost -16, 000

Less: Fixed selling and

administration cost

-5, 200

________

Net Profit 4, 700

Statement of absorption costing for first quarter

(£) Amount

Sales 66, 000

Cost of Sales:

Opening inventory - - -

Finished goods 78,000 * 0.85 66, 300

Less: Closing

inventory

12,000 * 0.85 -10, 200

________

-56, 100

________

Actual Gross Profit 9, 900

6

Less: Closing

inventory

4,000 * 0.65 -2, 600

________

-48, 100

________

Contribution 25, 900

Less: Fixed Cost -16, 000

Less: Fixed selling and

administration cost

-5, 200

________

Net Profit 4, 700

Statement of absorption costing for first quarter

(£) Amount

Sales 66, 000

Cost of Sales:

Opening inventory - - -

Finished goods 78,000 * 0.85 66, 300

Less: Closing

inventory

12,000 * 0.85 -10, 200

________

-56, 100

________

Actual Gross Profit 9, 900

6

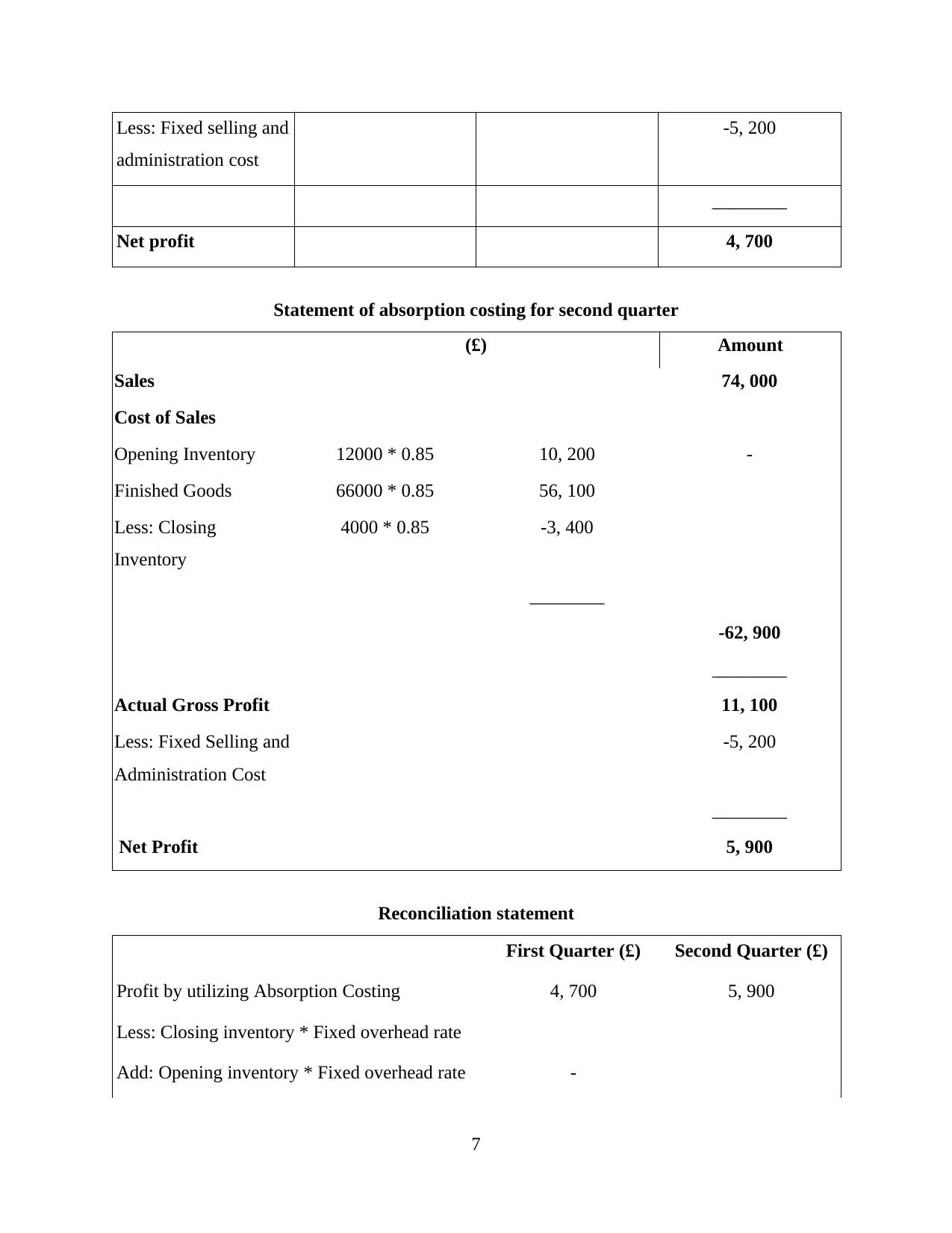

Less: Fixed selling and

administration cost

-5, 200

________

Net profit 4, 700

Statement of absorption costing for second quarter

(£) Amount

Sales 74, 000

Cost of Sales

Opening Inventory 12000 * 0.85 10, 200 -

Finished Goods 66000 * 0.85 56, 100

Less: Closing

Inventory

4000 * 0.85 -3, 400

________

-62, 900

________

Actual Gross Profit 11, 100

Less: Fixed Selling and

Administration Cost

-5, 200

________

Net Profit 5, 900

Reconciliation statement

First Quarter (£) Second Quarter (£)

Profit by utilizing Absorption Costing 4, 700 5, 900

Less: Closing inventory * Fixed overhead rate

Add: Opening inventory * Fixed overhead rate -

7

administration cost

-5, 200

________

Net profit 4, 700

Statement of absorption costing for second quarter

(£) Amount

Sales 74, 000

Cost of Sales

Opening Inventory 12000 * 0.85 10, 200 -

Finished Goods 66000 * 0.85 56, 100

Less: Closing

Inventory

4000 * 0.85 -3, 400

________

-62, 900

________

Actual Gross Profit 11, 100

Less: Fixed Selling and

Administration Cost

-5, 200

________

Net Profit 5, 900

Reconciliation statement

First Quarter (£) Second Quarter (£)

Profit by utilizing Absorption Costing 4, 700 5, 900

Less: Closing inventory * Fixed overhead rate

Add: Opening inventory * Fixed overhead rate -

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

________ ________

Profit by utilizing marginal costing 1, 900 4, 700

Inventory costs: It showcase expenses that is related with storing and managing of stock

in an organization. It involves costs associated with intangibles, such as, depreciation, lost

opportunity cost and warehousing cost of Prime Furniture. Different types of inventory costs is

stated below:

Ordering cost: It represents costs associated with replenishing of inventory. In other

words, ordering costs of Prime Furniture indicates expense which incurs in the process of

ordering (Prowle and Lucas, 2016).

Carrying cost: It involves capital cost, i.e., financing charges of stock, storage space

cost, inventory service cost as well as inventory risk cost.

Stock out cost: It indicates costs which by Prime Furniture bears in case of stock out.

TASK 3

P4: Explanation of planning tools which is utilised in management accounting:

Budget can be described as a an estimation for revenues and expenditures for a specific

period of time. It is usually re-evaluated or compiled on periodic basis (Renz, 2016). In context

to Prime Furniture, application of budgeting techniques ensures control and monitoring of

financial transactions. It facilitates achievement of organizational objectives by formulation of

effective strategies.

Different types of budget: Budgets are of various types which are stated below:

Capital budget: It is a tool of financial management which is utilised for the purpose of

measuring potential risk of a project and for analysing expected return on investment.

Implementation of planning tool of capital budgeting ensures well-informed decision making by

managers in relation to investments or projects which are pursued by an organization. In other

words, this budget facilitates analysis and measurement of value associated with a capital

investment.

Advantages: While considering advantages that is associated with preparation of capital

budget, it can be stated that capital budgeting enables understanding of risk which is involved

with an investment (Saeidi and Othman, 2017). Apart from it, this budgetary planning tool

evaluates affect of such risk on returns of an organization. In relevance to Prime Furniture,

8

Profit by utilizing marginal costing 1, 900 4, 700

Inventory costs: It showcase expenses that is related with storing and managing of stock

in an organization. It involves costs associated with intangibles, such as, depreciation, lost

opportunity cost and warehousing cost of Prime Furniture. Different types of inventory costs is

stated below:

Ordering cost: It represents costs associated with replenishing of inventory. In other

words, ordering costs of Prime Furniture indicates expense which incurs in the process of

ordering (Prowle and Lucas, 2016).

Carrying cost: It involves capital cost, i.e., financing charges of stock, storage space

cost, inventory service cost as well as inventory risk cost.

Stock out cost: It indicates costs which by Prime Furniture bears in case of stock out.

TASK 3

P4: Explanation of planning tools which is utilised in management accounting:

Budget can be described as a an estimation for revenues and expenditures for a specific

period of time. It is usually re-evaluated or compiled on periodic basis (Renz, 2016). In context

to Prime Furniture, application of budgeting techniques ensures control and monitoring of

financial transactions. It facilitates achievement of organizational objectives by formulation of

effective strategies.

Different types of budget: Budgets are of various types which are stated below:

Capital budget: It is a tool of financial management which is utilised for the purpose of

measuring potential risk of a project and for analysing expected return on investment.

Implementation of planning tool of capital budgeting ensures well-informed decision making by

managers in relation to investments or projects which are pursued by an organization. In other

words, this budget facilitates analysis and measurement of value associated with a capital

investment.

Advantages: While considering advantages that is associated with preparation of capital

budget, it can be stated that capital budgeting enables understanding of risk which is involved

with an investment (Saeidi and Othman, 2017). Apart from it, this budgetary planning tool

evaluates affect of such risk on returns of an organization. In relevance to Prime Furniture,

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

application of this tool enhances strategic investments of an enterprise for long term. It facilitates

adequate monitoring and management of investments and minimises the risk associated with it.

Disadvantages: Capital budget is irreversible in nature and it is based on future

estimations which do not remain certain. Hence, business cannot depend highly on this technique

of budgeting as it is not necessary that capital budget provides adequate interpretations for future

activities.

Operating budget: It showcase projected revenue as well as associated expenditures for

future period of time. This budgetary tools outlines funds that is required in a business for the

purpose of performing operational activities of an organization in a smooth and effective manner

(Taschner and Charifzadeh, 2016). In case of Prime furniture, preparation of operating budget

facilitates monitoring of revenues which are generated and expenses that are incurred in daily

operational activities of a firm.

Advantages: Operating budget facilitates management of operational expenses that incurs

in an organization. Hence, it enables reduction or elimination of unnecessary expenditures of

Prime Furniture which leads to enhancement of profitability of business. Further, computation of

operating budget ensures alignment of business activities with actual requirements of an

enterprise that fosters achievement of organizational goals.

Disadvantages: On consideration of disadvantages associated with operating budget, it is

noted that computation of this budget is a time-consuming activity. Apart from it, operating

budget is focused on allocation of fund for specific activities of an enterprise but, subjective

issues such as, quality of service which is provided to customers of Prime Furniture.

Alternative methods of budgeting:

Budgeting refers to a technique of estimating financial consequences as well as its

implementations on business (Tucker and Lawson, 2016). Computation of budgeting is crucial

for effective management of financial resources of Prime Furniture. Zero-based budgeting,

incremental budgeting, and activity based budgeting are some alternative methods of budgeting.

Zero based budgeting refers to an approach of formulating budget from the scratch, i.e., no prior

information is used for preparing this budget. Further, incremental budgeting involves utilization

of data of last year for estimating current year's information. Hence, while preparing incremental

budgeting, financial information of last year of Prime Furniture is added or subtracted. Activity

9

adequate monitoring and management of investments and minimises the risk associated with it.

Disadvantages: Capital budget is irreversible in nature and it is based on future

estimations which do not remain certain. Hence, business cannot depend highly on this technique

of budgeting as it is not necessary that capital budget provides adequate interpretations for future

activities.

Operating budget: It showcase projected revenue as well as associated expenditures for

future period of time. This budgetary tools outlines funds that is required in a business for the

purpose of performing operational activities of an organization in a smooth and effective manner

(Taschner and Charifzadeh, 2016). In case of Prime furniture, preparation of operating budget

facilitates monitoring of revenues which are generated and expenses that are incurred in daily

operational activities of a firm.

Advantages: Operating budget facilitates management of operational expenses that incurs

in an organization. Hence, it enables reduction or elimination of unnecessary expenditures of

Prime Furniture which leads to enhancement of profitability of business. Further, computation of

operating budget ensures alignment of business activities with actual requirements of an

enterprise that fosters achievement of organizational goals.

Disadvantages: On consideration of disadvantages associated with operating budget, it is

noted that computation of this budget is a time-consuming activity. Apart from it, operating

budget is focused on allocation of fund for specific activities of an enterprise but, subjective

issues such as, quality of service which is provided to customers of Prime Furniture.

Alternative methods of budgeting:

Budgeting refers to a technique of estimating financial consequences as well as its

implementations on business (Tucker and Lawson, 2016). Computation of budgeting is crucial

for effective management of financial resources of Prime Furniture. Zero-based budgeting,

incremental budgeting, and activity based budgeting are some alternative methods of budgeting.

Zero based budgeting refers to an approach of formulating budget from the scratch, i.e., no prior

information is used for preparing this budget. Further, incremental budgeting involves utilization

of data of last year for estimating current year's information. Hence, while preparing incremental

budgeting, financial information of last year of Prime Furniture is added or subtracted. Activity

9

based budgeting signifies an approach of top-down budgeting which determines the amount of

input for supporting targets and outputs of Prime Furniture.

Behavioural implications of budget: Budgeting pertains positive behavioural

implications as it assists managers in planning as well as controlling of organizational resources

by providing appropriate financial information. In case of Prime Furniture, budgeting fosters

alignment of targets of management team with objectives of business.

Pricing strategies: It is an effective technique which is utilised for enhancing market

share of a company and expanding its profit margin. Competition based pricing strategy is used

by Prime Furniture which indicates that price of products offered by an organization is based on

price of its competitors. Application of this strategy of pricing enables firm to gain advantage

over its competitors which enhances sustainability and success of business in longer run. Further,

application of competitive pricing helps ion improving demand of customers as product is

supplied at reasonable rate as compared to competitors which provides competitive edge to an

enterprise.

Common costing system: It refers to a system which is designed for the purpose of

monitoring costs which incurs in a business. Costing system comprises set of processes, controls

as well as reports which management of revenue, costs as well as profitability. Actual costing,

normal costing and standard costing are three costing systems which is applied for deriving cost

of business products (Tucker and Leach, 2017). Job costing can be described as a specific

method of costing that is utilised when production work of Prime Furniture is carried in

accordance to customer requirements. Further, batch costing indicates production of products of

business in batches. It is applied in case of mass production. Process costing traces direct costs as

well as allocates all indirect costs that incurs in the process of manufacturing. Lastly, facilitates

tracking of expenses which is associated with specific contract.

Strategic Planning:

PEST analysis: It is a framework which is utilised for scanning of environmental

component in relevance to strategic management and its impact or influence on firm. Pest

analysis for Prime Furniture is computed below:

Political: This factor involves political stability, government policies, trade restrictions

etc. Political instability of a country pertains negative influence on Prime Furniture as its

hinders policy formulation for future period of time due to uncertainty.

10

input for supporting targets and outputs of Prime Furniture.

Behavioural implications of budget: Budgeting pertains positive behavioural

implications as it assists managers in planning as well as controlling of organizational resources

by providing appropriate financial information. In case of Prime Furniture, budgeting fosters

alignment of targets of management team with objectives of business.

Pricing strategies: It is an effective technique which is utilised for enhancing market

share of a company and expanding its profit margin. Competition based pricing strategy is used

by Prime Furniture which indicates that price of products offered by an organization is based on

price of its competitors. Application of this strategy of pricing enables firm to gain advantage

over its competitors which enhances sustainability and success of business in longer run. Further,

application of competitive pricing helps ion improving demand of customers as product is

supplied at reasonable rate as compared to competitors which provides competitive edge to an

enterprise.

Common costing system: It refers to a system which is designed for the purpose of

monitoring costs which incurs in a business. Costing system comprises set of processes, controls

as well as reports which management of revenue, costs as well as profitability. Actual costing,

normal costing and standard costing are three costing systems which is applied for deriving cost

of business products (Tucker and Leach, 2017). Job costing can be described as a specific

method of costing that is utilised when production work of Prime Furniture is carried in

accordance to customer requirements. Further, batch costing indicates production of products of

business in batches. It is applied in case of mass production. Process costing traces direct costs as

well as allocates all indirect costs that incurs in the process of manufacturing. Lastly, facilitates

tracking of expenses which is associated with specific contract.

Strategic Planning:

PEST analysis: It is a framework which is utilised for scanning of environmental

component in relevance to strategic management and its impact or influence on firm. Pest

analysis for Prime Furniture is computed below:

Political: This factor involves political stability, government policies, trade restrictions

etc. Political instability of a country pertains negative influence on Prime Furniture as its

hinders policy formulation for future period of time due to uncertainty.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.