Management Accounting: Analysis of Prime Furniture Private Ltd

VerifiedAdded on 2022/12/14

|16

|4616

|78

Report

AI Summary

This report analyzes the management accounting practices at Prime Furniture Private Ltd, a UK-based furniture retail company. It covers various aspects of management accounting, including understanding management accounting systems such as cost accounting, lean accounting, throughput accounting, and transfer pricing, and different methods used for management accounting reporting like budget reports, performance reports, and account receivables aging reports. The report also discusses the benefits of applying a management accounting system, techniques of cost analysis to prepare income statements using marginal and absorption costing, and management accounting techniques to produce appropriate financial reporting documents. Furthermore, it examines the advantages and disadvantages of various planning tools used for budgetary control, such as variance analysis and financial budgets, and ways in which organizations can use management accounting to address financial problems. This comprehensive analysis provides insights into how management accounting can enhance operational efficiency and financial decision-making within the organization.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Contents

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

LO1 Understanding of management accounting system............................................................1

LO2 Application of management techniques..............................................................................4

LO3 Planning tools used in management accounting.................................................................6

LO4 Ways in which organisations could use management accounting to address financial

problems....................................................................................................................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................13

Contents

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

LO1 Understanding of management accounting system............................................................1

LO2 Application of management techniques..............................................................................4

LO3 Planning tools used in management accounting.................................................................6

LO4 Ways in which organisations could use management accounting to address financial

problems....................................................................................................................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................13

INTRODUCTION

Management accounting or managerial accounting is a tool which is used by management

of organisation to take long and short term and decisions regarding organisations operational

activities. To increase operational efficiency of an organisation with help of using provisions of

accounting information systems is management accounting. Prime furniture private ltd is a UK

based furniture retail sale company and this report is conducted in context of this company.

Accounting management, accounting management systems, accounting methods, financial

reporting, planning tools used for budgetary control and use of management accounting systems

for financial problems are explained in organisation’s context.

MAIN BODY

LO1 Understanding of management accounting system

P1 Management accounting and management accounting systems

Management Accounting: This also known as cost accounting, management accounting

is a process of interpreting, analysing and identifying information relevant to operational

activities of firm and provide it to managers so that, they can achieve business goals. Internal

management accounting systems are used in providing critical information to management to

make decisions regarding operational activities of business (Agrawal, 2018). These systems can

be valuable for costing and managing different operational processes. Following are different

management accounting systems which are used by management of company.

Cost Accounting: This is a traditional accounting system which is used in measuring

cost by using job order costing or process costing. Allocation of cost is also done on basis of cost

accounting such as direct labour, direct material, manufacturing overhead etc. this traditional

accounting system measures a single overhead rate and that rate is applied to each job or

department. Job order costing is used in accumulation of manufacturing cost distinctly for every

job whereas process costing accumulates manufacturing cost for each process. Activity rate and

application of overhead is measured with help of activity-based costing on basis of activity

usage.

Lean Accounting: This management accounting system is used by lean organisations,

this system is used for gathering all financial and non-financial information to perform lean

strategies of organisation and attain financial growth. Lean accounting system not only focuses

1

Management accounting or managerial accounting is a tool which is used by management

of organisation to take long and short term and decisions regarding organisations operational

activities. To increase operational efficiency of an organisation with help of using provisions of

accounting information systems is management accounting. Prime furniture private ltd is a UK

based furniture retail sale company and this report is conducted in context of this company.

Accounting management, accounting management systems, accounting methods, financial

reporting, planning tools used for budgetary control and use of management accounting systems

for financial problems are explained in organisation’s context.

MAIN BODY

LO1 Understanding of management accounting system

P1 Management accounting and management accounting systems

Management Accounting: This also known as cost accounting, management accounting

is a process of interpreting, analysing and identifying information relevant to operational

activities of firm and provide it to managers so that, they can achieve business goals. Internal

management accounting systems are used in providing critical information to management to

make decisions regarding operational activities of business (Agrawal, 2018). These systems can

be valuable for costing and managing different operational processes. Following are different

management accounting systems which are used by management of company.

Cost Accounting: This is a traditional accounting system which is used in measuring

cost by using job order costing or process costing. Allocation of cost is also done on basis of cost

accounting such as direct labour, direct material, manufacturing overhead etc. this traditional

accounting system measures a single overhead rate and that rate is applied to each job or

department. Job order costing is used in accumulation of manufacturing cost distinctly for every

job whereas process costing accumulates manufacturing cost for each process. Activity rate and

application of overhead is measured with help of activity-based costing on basis of activity

usage.

Lean Accounting: This management accounting system is used by lean organisations,

this system is used for gathering all financial and non-financial information to perform lean

strategies of organisation and attain financial growth. Lean accounting system not only focuses

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

over cost but it helps in reducing cost and eliminating waste by providing efficient strategies

(Alawattage, and Wickramasinghe, 2018). Financial information is gathered on basis of these

strategies with help of that information accountants can take immediate decisions and excess cost

which a waste can be cut down. Implementation of various lean accounting principles and effect

of these principles on business is also measured with help of lean management accounting

systems.

Throughput Accounting: This accounting system is used in improving profitability of

company with principle-based and simplified management accounting approach. Throughput

refers to number of units which go through a process in a particular period of time. All revenues

which are generated by process and minus all expenses which are incurred during that particular

process presents throughput. In this process all constrains revenant to production system of

organisation are identified. These constrains include inadequate levels of production capacity,

labour and materials of company. Cost of individual products can be reduced and production

volume can be increased by putting more throughputs and reducing constraints.

Transfer Pricing: This is a pricing accounting system; it is used when one department of

organisation sells or provides its manufactured goods to another department of same

organisation. So at what price particular department will provide products to other department is

decided with help of transfer pricing accounting management system (Almasan and et. al. 2019).

Transfer pricing common management accounting system under this method, goods are costed

when they move through different departments. Common cost of product is added with transfer

price, opportunity cost and variable cost. Opportunity cost refers to price which company would

have to pay otherwise if company outsources production.

P2 Different methods used for management accounting reporting

Management accounting reporting: This reporting purposes at informing managers

various aspects of business so that, mangers can make better decisions. Data is collected and

tacked from different departments of company through key performance indicators (Ammar,

2017). Financial and operational information of a specific period is disclosed, on basis of that

worth of business is measured. These reports are used in decision making, regulating, planning

and measuring performance. Various methods of management accounting reporting are

explained below.

2

(Alawattage, and Wickramasinghe, 2018). Financial information is gathered on basis of these

strategies with help of that information accountants can take immediate decisions and excess cost

which a waste can be cut down. Implementation of various lean accounting principles and effect

of these principles on business is also measured with help of lean management accounting

systems.

Throughput Accounting: This accounting system is used in improving profitability of

company with principle-based and simplified management accounting approach. Throughput

refers to number of units which go through a process in a particular period of time. All revenues

which are generated by process and minus all expenses which are incurred during that particular

process presents throughput. In this process all constrains revenant to production system of

organisation are identified. These constrains include inadequate levels of production capacity,

labour and materials of company. Cost of individual products can be reduced and production

volume can be increased by putting more throughputs and reducing constraints.

Transfer Pricing: This is a pricing accounting system; it is used when one department of

organisation sells or provides its manufactured goods to another department of same

organisation. So at what price particular department will provide products to other department is

decided with help of transfer pricing accounting management system (Almasan and et. al. 2019).

Transfer pricing common management accounting system under this method, goods are costed

when they move through different departments. Common cost of product is added with transfer

price, opportunity cost and variable cost. Opportunity cost refers to price which company would

have to pay otherwise if company outsources production.

P2 Different methods used for management accounting reporting

Management accounting reporting: This reporting purposes at informing managers

various aspects of business so that, mangers can make better decisions. Data is collected and

tacked from different departments of company through key performance indicators (Ammar,

2017). Financial and operational information of a specific period is disclosed, on basis of that

worth of business is measured. These reports are used in decision making, regulating, planning

and measuring performance. Various methods of management accounting reporting are

explained below.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Budget reports: These reports are generated department-wise for large organisations and

for small businesses these are generated for whole organisation. This is very critical in measuring

company’s performance; however, every company creates budget for specific time or period

according to their requirements. A well prepared budget can cater to unpredicted situations that

may arise in future. A good budget report is made on basis of past experiences and it includes all

estimated expenses and earnings of company. Company should work in its budgeted amount so

that it can effectively achieve its organisational goals in minimum expenses.

Performance Report: Such reports are created or generated by companies on the end of

a particular period or term which shows performance of organisation as a whole and for each

individual employee as well. In large organisations departmental performance reports are also

generated, all these performance reports play a vital role in making strategic decisions for future

of organisation (Bisogno, and Vaia, 2017). According to performance outputs individuals are

rewarded for their good performance and employees with not satisfied performance are also dealt

with accordingly. These reports present company’s growth, success and position in market. On

basis of performance reports, management of company can make strategies for future operations

of organisation.

Account receivables aging report: If a company runs its business on extending credits,

then company must have knowledge about all its creditors and this report is very essential for

such business. Management can divide creditors in specific time periods of according to their

debt and categories by this company can identify defaulters easily and collection process of

company can work well (Burger, and Middelberg, 2018). If report shows that there are so many

defaulters, then company should transform its credit policies and tighter credit rules should be

applied because cash flow is vital for smooth running of any organisation. Bad debts can be

identified and written off with help of this report.

M1 Benefits of applying management accounting system

Prime furniture private ltd uses management accounting system in its business and it is

very beneficial for company. Following are benefits of applying management accounting system.

Planning: For proper planning management of Prime furniture can prepare various

functional budgets and accounting information which can be arranged in organisation for better

operation of organisational activities

3

for small businesses these are generated for whole organisation. This is very critical in measuring

company’s performance; however, every company creates budget for specific time or period

according to their requirements. A well prepared budget can cater to unpredicted situations that

may arise in future. A good budget report is made on basis of past experiences and it includes all

estimated expenses and earnings of company. Company should work in its budgeted amount so

that it can effectively achieve its organisational goals in minimum expenses.

Performance Report: Such reports are created or generated by companies on the end of

a particular period or term which shows performance of organisation as a whole and for each

individual employee as well. In large organisations departmental performance reports are also

generated, all these performance reports play a vital role in making strategic decisions for future

of organisation (Bisogno, and Vaia, 2017). According to performance outputs individuals are

rewarded for their good performance and employees with not satisfied performance are also dealt

with accordingly. These reports present company’s growth, success and position in market. On

basis of performance reports, management of company can make strategies for future operations

of organisation.

Account receivables aging report: If a company runs its business on extending credits,

then company must have knowledge about all its creditors and this report is very essential for

such business. Management can divide creditors in specific time periods of according to their

debt and categories by this company can identify defaulters easily and collection process of

company can work well (Burger, and Middelberg, 2018). If report shows that there are so many

defaulters, then company should transform its credit policies and tighter credit rules should be

applied because cash flow is vital for smooth running of any organisation. Bad debts can be

identified and written off with help of this report.

M1 Benefits of applying management accounting system

Prime furniture private ltd uses management accounting system in its business and it is

very beneficial for company. Following are benefits of applying management accounting system.

Planning: For proper planning management of Prime furniture can prepare various

functional budgets and accounting information which can be arranged in organisation for better

operation of organisational activities

3

Controlling: Performance of Prime furniture is measured and compared with key

performance indicators. Performance of individuals and whole organisation can be evaluated and

controlled. Standard costing and budgetary control both helps in management of company.

D1 Integration of management accounting systems and management accounting reporting

Management accounting system provides qualitative and quantitative on operational and

financial performance of organisation. Whereas management accounting report is created on

basis of management accounting systems and it focuses on external use of this information for

assessment of creditors and other performance measures (Chiwamit, Modell, and Scapens,

2017). Financial and non-financial decisions are taken on basis of management accounting

systems and management accounting reports. Management accounting systems are used in

various processes such as operational and financial processes of organisation and management

accounting report is prepared on basis of these systems.

LO2 Application of management techniques

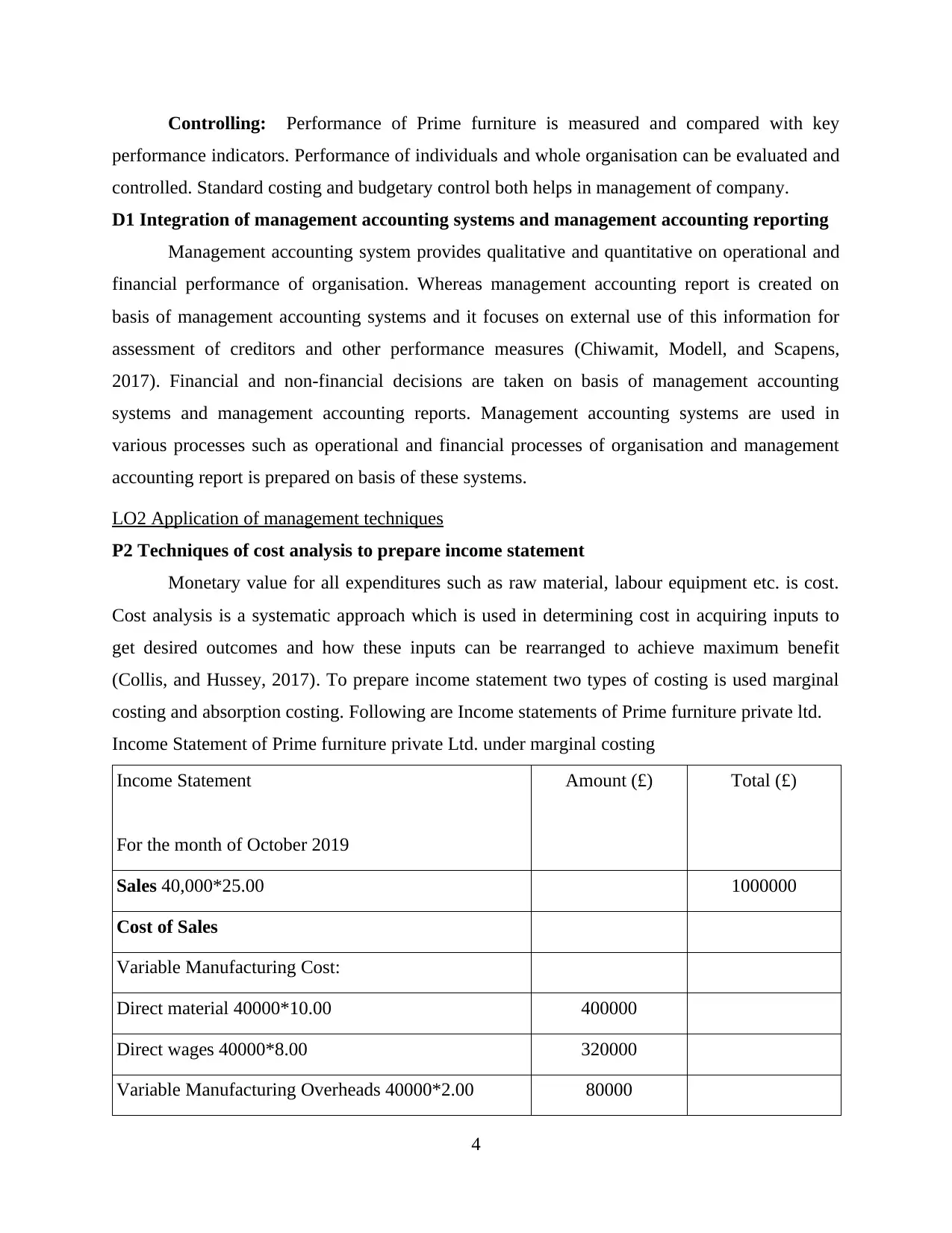

P2 Techniques of cost analysis to prepare income statement

Monetary value for all expenditures such as raw material, labour equipment etc. is cost.

Cost analysis is a systematic approach which is used in determining cost in acquiring inputs to

get desired outcomes and how these inputs can be rearranged to achieve maximum benefit

(Collis, and Hussey, 2017). To prepare income statement two types of costing is used marginal

costing and absorption costing. Following are Income statements of Prime furniture private ltd.

Income Statement of Prime furniture private Ltd. under marginal costing

Income Statement

For the month of October 2019

Amount (£) Total (£)

Sales 40,000*25.00 1000000

Cost of Sales

Variable Manufacturing Cost:

Direct material 40000*10.00 400000

Direct wages 40000*8.00 320000

Variable Manufacturing Overheads 40000*2.00 80000

4

performance indicators. Performance of individuals and whole organisation can be evaluated and

controlled. Standard costing and budgetary control both helps in management of company.

D1 Integration of management accounting systems and management accounting reporting

Management accounting system provides qualitative and quantitative on operational and

financial performance of organisation. Whereas management accounting report is created on

basis of management accounting systems and it focuses on external use of this information for

assessment of creditors and other performance measures (Chiwamit, Modell, and Scapens,

2017). Financial and non-financial decisions are taken on basis of management accounting

systems and management accounting reports. Management accounting systems are used in

various processes such as operational and financial processes of organisation and management

accounting report is prepared on basis of these systems.

LO2 Application of management techniques

P2 Techniques of cost analysis to prepare income statement

Monetary value for all expenditures such as raw material, labour equipment etc. is cost.

Cost analysis is a systematic approach which is used in determining cost in acquiring inputs to

get desired outcomes and how these inputs can be rearranged to achieve maximum benefit

(Collis, and Hussey, 2017). To prepare income statement two types of costing is used marginal

costing and absorption costing. Following are Income statements of Prime furniture private ltd.

Income Statement of Prime furniture private Ltd. under marginal costing

Income Statement

For the month of October 2019

Amount (£) Total (£)

Sales 40,000*25.00 1000000

Cost of Sales

Variable Manufacturing Cost:

Direct material 40000*10.00 400000

Direct wages 40000*8.00 320000

Variable Manufacturing Overheads 40000*2.00 80000

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

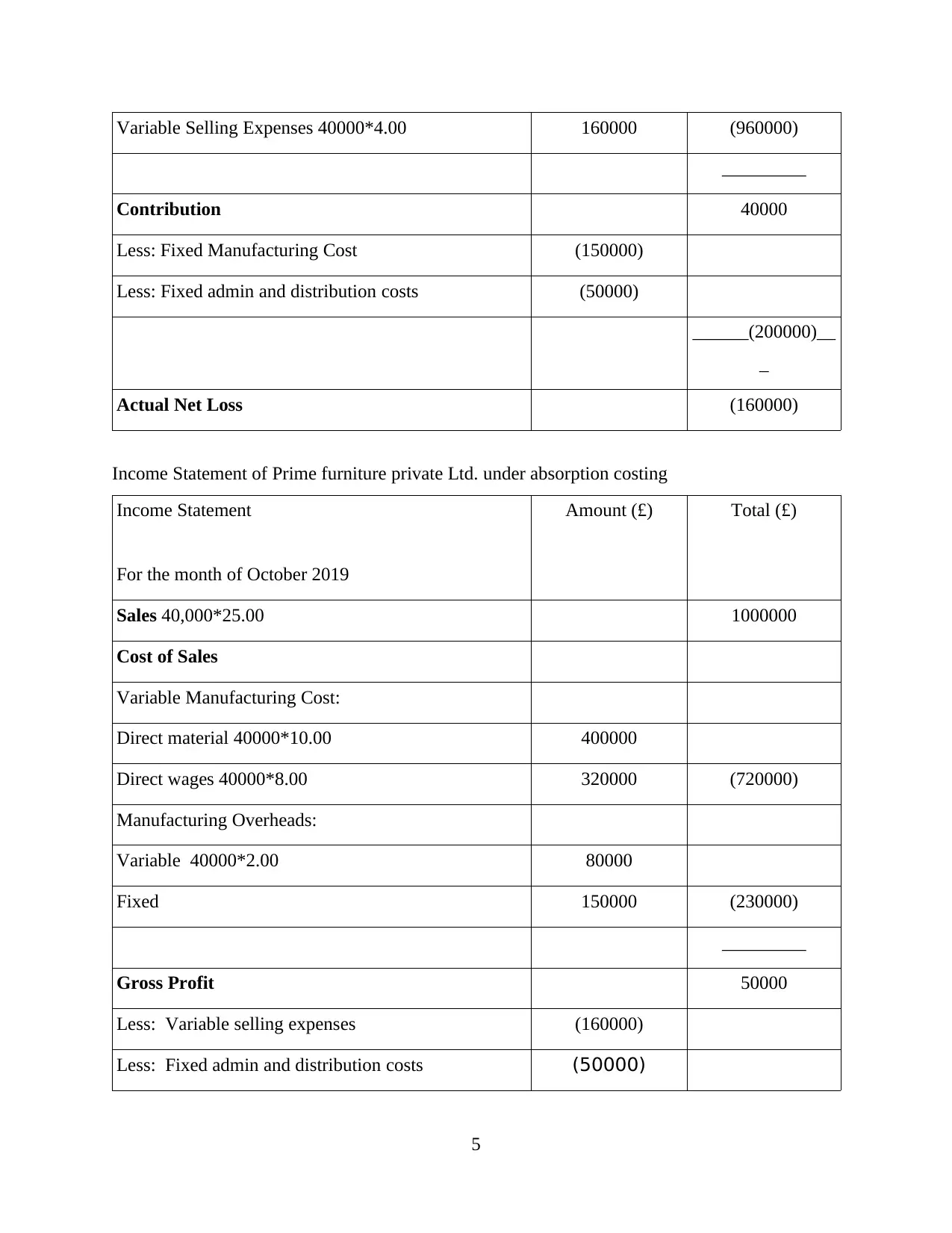

Variable Selling Expenses 40000*4.00 160000 (960000)

_________

Contribution 40000

Less: Fixed Manufacturing Cost (150000)

Less: Fixed admin and distribution costs (50000)

______(200000)__

_

Actual Net Loss (160000)

Income Statement of Prime furniture private Ltd. under absorption costing

Income Statement

For the month of October 2019

Amount (£) Total (£)

Sales 40,000*25.00 1000000

Cost of Sales

Variable Manufacturing Cost:

Direct material 40000*10.00 400000

Direct wages 40000*8.00 320000 (720000)

Manufacturing Overheads:

Variable 40000*2.00 80000

Fixed 150000 (230000)

_________

Gross Profit 50000

Less: Variable selling expenses (160000)

Less: Fixed admin and distribution costs (50000)

5

_________

Contribution 40000

Less: Fixed Manufacturing Cost (150000)

Less: Fixed admin and distribution costs (50000)

______(200000)__

_

Actual Net Loss (160000)

Income Statement of Prime furniture private Ltd. under absorption costing

Income Statement

For the month of October 2019

Amount (£) Total (£)

Sales 40,000*25.00 1000000

Cost of Sales

Variable Manufacturing Cost:

Direct material 40000*10.00 400000

Direct wages 40000*8.00 320000 (720000)

Manufacturing Overheads:

Variable 40000*2.00 80000

Fixed 150000 (230000)

_________

Gross Profit 50000

Less: Variable selling expenses (160000)

Less: Fixed admin and distribution costs (50000)

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

_____(210000)___

_

Actual Net Loss (160000)

M2 Management accounting techniques to produce appropriate financial reporting

documents

Income statement: This is also known as revenue and expenditure statement; this is a

financial statement which represents financial performance of a company for a specific time

period. Net income or loss = (Total revenue + gains)- (total expenses +losses) this is formula of

calculating net income or loss with help of income statement.

D2 Financial reports to apply and interpret data

Income statement or profit and loss statement can be prepared on basis of marginal

costing or absorption costing these are explained below.

Marginal costing: This is a technique of costing which identifies marginal cost by

dividing fixed cost and variable cost. Fixed cost is charged from profit and loss account whereas

variable costs are charged from operation.

Absorption costing: This is a method of costing to calculate cost of product or

organisation by taking direct expenses and all costs. These costs include direct and indirect cost.

LO3 Planning tools used in management accounting

P4 Advantages and disadvantages of various planning tools used for budgetary control

Budgetary control refers to control over operational and financial activities with help of

budget. Budget is a tool which helps in forecasting future income and expenses and on basis of

that company frames plan of action or strategy. Basically it’s an estimated financial plan which is

prepared for a specific period of time (Curry, 2019). Budget can be diversified in 3 categories;

surplus budget, balance budget, and deficit budget. In budgetary control numerous tools and

techniques are used for future financial planning of organisation. On the basis of measurement

financial requirements of business are arranged in orderly basis so that these can be fulfilled for

achievement of business goals. Budgetary control is useful in controlling financial activities and

decisions of organisation to move company towards attainment of desired objectives. Budgetary

control is a process in which estimated budget of a specific period is compared with actual

outcomes which company achieved in that particular time. On basis of outcomes of that

6

_

Actual Net Loss (160000)

M2 Management accounting techniques to produce appropriate financial reporting

documents

Income statement: This is also known as revenue and expenditure statement; this is a

financial statement which represents financial performance of a company for a specific time

period. Net income or loss = (Total revenue + gains)- (total expenses +losses) this is formula of

calculating net income or loss with help of income statement.

D2 Financial reports to apply and interpret data

Income statement or profit and loss statement can be prepared on basis of marginal

costing or absorption costing these are explained below.

Marginal costing: This is a technique of costing which identifies marginal cost by

dividing fixed cost and variable cost. Fixed cost is charged from profit and loss account whereas

variable costs are charged from operation.

Absorption costing: This is a method of costing to calculate cost of product or

organisation by taking direct expenses and all costs. These costs include direct and indirect cost.

LO3 Planning tools used in management accounting

P4 Advantages and disadvantages of various planning tools used for budgetary control

Budgetary control refers to control over operational and financial activities with help of

budget. Budget is a tool which helps in forecasting future income and expenses and on basis of

that company frames plan of action or strategy. Basically it’s an estimated financial plan which is

prepared for a specific period of time (Curry, 2019). Budget can be diversified in 3 categories;

surplus budget, balance budget, and deficit budget. In budgetary control numerous tools and

techniques are used for future financial planning of organisation. On the basis of measurement

financial requirements of business are arranged in orderly basis so that these can be fulfilled for

achievement of business goals. Budgetary control is useful in controlling financial activities and

decisions of organisation to move company towards attainment of desired objectives. Budgetary

control is a process in which estimated budget of a specific period is compared with actual

outcomes which company achieved in that particular time. On basis of outcomes of that

6

compression strategies and policies are changed or modified to achieve organisational goals with

less cost and maximum profit. This budgetary control can be very useful in optimising and

controlling financial performance of company. Following are tools or techniques of budgetary

control.

Variance analysis: In process of this analysis budgets are created for each department

for specific period after completion of period estimated budgets are compared with actual

accounting results. Difference between estimated budget and actual accounting results of period

is deemed as variance (Dahal, 2018). Variances are diversified in two categories favourable and

unfavourable variances. For example, difference between estimated distribution expenses and

actual distribution expenses is distribution expenses variance. This variance can be useful in

reducing cost.

Financial budgets: These budgets determine company’s cash flow, from where company

is going to receive cash and in which activity or operation that cash will be used or spend.

Business can receive cash mainly from sales revenues, loan, stock issue or by selling any asset of

company. Whereas company can use its cash or revenue in purchasing new asset for company,

expansion of business, dividend payment to shareholders, repaying debts of business, and

settling all expenses of company. Financial budgets are used by company to manage its cash

flow, assets, income and expense following are various types of financial budget.

Capital expenditure budget: This budget is created by firm for purchase of fixed assets

such as plants and machinery, equipment required for new joiners, construction of new buildings

or upgrading existing assets of company (Diab, 2020). Any organisation weather small or large

needs to focus on this budget because this shows capital expenditure of company which a big and

long term investment. Most probably such expenditures are generated through long term

borrowing through issuance of securities or bonds.

Cash budget: This is a process of comparing estimated cash receipts and disbursements

of company with actual inflow and outflow of cash for a specific time period such as weekly,

monthly, quarterly or yearly. Business uses cash budget to identify weather company have

sufficient cash for all its operational activities or not. Organisation can have better control over

its cash resources and allocation of cash can also be done on basis of cash budget. Since cash

budgets can be prepared for any specific time period company can easily identify its current

obligations to meet. Cash budget also presents excess available cash in the business thus

7

less cost and maximum profit. This budgetary control can be very useful in optimising and

controlling financial performance of company. Following are tools or techniques of budgetary

control.

Variance analysis: In process of this analysis budgets are created for each department

for specific period after completion of period estimated budgets are compared with actual

accounting results. Difference between estimated budget and actual accounting results of period

is deemed as variance (Dahal, 2018). Variances are diversified in two categories favourable and

unfavourable variances. For example, difference between estimated distribution expenses and

actual distribution expenses is distribution expenses variance. This variance can be useful in

reducing cost.

Financial budgets: These budgets determine company’s cash flow, from where company

is going to receive cash and in which activity or operation that cash will be used or spend.

Business can receive cash mainly from sales revenues, loan, stock issue or by selling any asset of

company. Whereas company can use its cash or revenue in purchasing new asset for company,

expansion of business, dividend payment to shareholders, repaying debts of business, and

settling all expenses of company. Financial budgets are used by company to manage its cash

flow, assets, income and expense following are various types of financial budget.

Capital expenditure budget: This budget is created by firm for purchase of fixed assets

such as plants and machinery, equipment required for new joiners, construction of new buildings

or upgrading existing assets of company (Diab, 2020). Any organisation weather small or large

needs to focus on this budget because this shows capital expenditure of company which a big and

long term investment. Most probably such expenditures are generated through long term

borrowing through issuance of securities or bonds.

Cash budget: This is a process of comparing estimated cash receipts and disbursements

of company with actual inflow and outflow of cash for a specific time period such as weekly,

monthly, quarterly or yearly. Business uses cash budget to identify weather company have

sufficient cash for all its operational activities or not. Organisation can have better control over

its cash resources and allocation of cash can also be done on basis of cash budget. Since cash

budgets can be prepared for any specific time period company can easily identify its current

obligations to meet. Cash budget also presents excess available cash in the business thus

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

businessman can easily make investment of surplus. With help of this budget company can

manage its sales and expenses in certain way so that optimal cash flow level can be maintained

in business. Company can determine if it has sufficient budget to meet cash requirement for

operational activities of a specific time period with help of cash budget.

The balance sheet budget: This refers to estimated budgeted balance sheet of company

which forecasts assets, liabilities and equity available for company for particular accounting

period. Management of company uses this for taking various financial decisions (Horvat, and

Mojzer, 2019). For preparing and finalizing master budget this budgeted balance sheet is final

and very essential step. At the end of specific period actual account figures are compared with

budgeted balance sheet this represents current equity, assets and liabilities of company which

determines financial position of organisation.

Operating budget: This budget contains estimated income and expenses generated from

daily operations or activities of business. Operating budget includes operating expenses, cost of

goods sold (COGS) and income or revenue generated from operational activities (Nielsen, and

Pontoppidan2019).This budget concludes planned operations of an organisation for a particular

time period. Following are different types of operating budgets.

The expenses budget: Expenses are disbursements which are not a part of direct cost

such as rent and payroll. This budget estimates and presents anticipated expenses for a particular

time period. This budget also anticipates upcoming expenses which can be helpful for managers

because they can prepare or manage those expenses accordingly.

The project budget: This budget is prepared for estimation of total cost of a project by

project managers. Project budget is helpful in estimation of cost which is going to be incurred in

completion of individual project for a specific time period. This budget gets updated

continuously as project completes its levels (Rachmawati, and et. al. 2019). This project budget

focuses on differences between sales and revenue expenses. Sales budget can be increased and

expenses budget can be reduced if estimated profit figure is not adequate.

Sales or revenue budget: This budget forecasts selling expenses and sales revenue and

capital expenditures. Basically it focuses over estimated income which company may receive

from normal activities or operations of organisation. This budget includes sales revenue,

operational expense, capital expense, and number of units sold. This budget plays a vital role in

helping managers identifying and forecasting future financial position of organisation.

8

manage its sales and expenses in certain way so that optimal cash flow level can be maintained

in business. Company can determine if it has sufficient budget to meet cash requirement for

operational activities of a specific time period with help of cash budget.

The balance sheet budget: This refers to estimated budgeted balance sheet of company

which forecasts assets, liabilities and equity available for company for particular accounting

period. Management of company uses this for taking various financial decisions (Horvat, and

Mojzer, 2019). For preparing and finalizing master budget this budgeted balance sheet is final

and very essential step. At the end of specific period actual account figures are compared with

budgeted balance sheet this represents current equity, assets and liabilities of company which

determines financial position of organisation.

Operating budget: This budget contains estimated income and expenses generated from

daily operations or activities of business. Operating budget includes operating expenses, cost of

goods sold (COGS) and income or revenue generated from operational activities (Nielsen, and

Pontoppidan2019).This budget concludes planned operations of an organisation for a particular

time period. Following are different types of operating budgets.

The expenses budget: Expenses are disbursements which are not a part of direct cost

such as rent and payroll. This budget estimates and presents anticipated expenses for a particular

time period. This budget also anticipates upcoming expenses which can be helpful for managers

because they can prepare or manage those expenses accordingly.

The project budget: This budget is prepared for estimation of total cost of a project by

project managers. Project budget is helpful in estimation of cost which is going to be incurred in

completion of individual project for a specific time period. This budget gets updated

continuously as project completes its levels (Rachmawati, and et. al. 2019). This project budget

focuses on differences between sales and revenue expenses. Sales budget can be increased and

expenses budget can be reduced if estimated profit figure is not adequate.

Sales or revenue budget: This budget forecasts selling expenses and sales revenue and

capital expenditures. Basically it focuses over estimated income which company may receive

from normal activities or operations of organisation. This budget includes sales revenue,

operational expense, capital expense, and number of units sold. This budget plays a vital role in

helping managers identifying and forecasting future financial position of organisation.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Non-monetary budgets: Such budgets are expressed in non-financial terms for example

how much quantities will be required, direct machine hours or direct labour hours for different

operational activities. Labour budget is an example of non-monetary budget.

M3 Use and application of planning tools in preparing budget and forecasting

Planning tools are those devices or instruments which are used in implementation of an

initiative, intervention, or programme in an organisation. There are various planning tools which

are used in management accounting which are explained below.

Fund flow analysis: This analysis shows inflow and outflow cash within business of a

specific time period. This presents difference between last year and current year’s balance sheet

that how well or not cash resources are used by company in current year in comparison of last

year. Sources of fund and applications of fund are shown for a particular period with help of fund

flow statement. Fund from operations is identified with fund flow analysis and working capital

also changes because of movement from one period to another period.

Budgetary control: This is a financial tool which is used for estimating and forecasting

income and expenses of company. Actual revenue or expenditures are compared with estimated

or budgeted revenue or expenditures to identify if strategy or plan of business are working

properly. Budgetary control can be very useful in taking financial decisions of company for

achievement of financial goals of company. It helps in identifying weather policies and strategies

of business need to get modified or changed to achieve desired success. Thus budgetary control

is a very effective planning tool.

Financial planning: Every organisation wants maximum profit in minimum possible

investment. Financial planning is a very crucial tool for achieving business objectives with

maximum profit This is a process of framing policies, budgets and strategies for financial

operations and activities of organisation. Proper or sound financial planning can be helpful in

many ways such as determining capital requirements, framing financial policies, determining

capital structure etc. adequate funds can also be ensured with help of financial planning for

attainment of desired business objectives.

Decision-making accounting: This tool is useful when there are various alternatives are

available and management have to choose best alternative out of them. Costs of these various

alternatives are compared and whichever alternatives consumes minimum cot gets selected. This

9

how much quantities will be required, direct machine hours or direct labour hours for different

operational activities. Labour budget is an example of non-monetary budget.

M3 Use and application of planning tools in preparing budget and forecasting

Planning tools are those devices or instruments which are used in implementation of an

initiative, intervention, or programme in an organisation. There are various planning tools which

are used in management accounting which are explained below.

Fund flow analysis: This analysis shows inflow and outflow cash within business of a

specific time period. This presents difference between last year and current year’s balance sheet

that how well or not cash resources are used by company in current year in comparison of last

year. Sources of fund and applications of fund are shown for a particular period with help of fund

flow statement. Fund from operations is identified with fund flow analysis and working capital

also changes because of movement from one period to another period.

Budgetary control: This is a financial tool which is used for estimating and forecasting

income and expenses of company. Actual revenue or expenditures are compared with estimated

or budgeted revenue or expenditures to identify if strategy or plan of business are working

properly. Budgetary control can be very useful in taking financial decisions of company for

achievement of financial goals of company. It helps in identifying weather policies and strategies

of business need to get modified or changed to achieve desired success. Thus budgetary control

is a very effective planning tool.

Financial planning: Every organisation wants maximum profit in minimum possible

investment. Financial planning is a very crucial tool for achieving business objectives with

maximum profit This is a process of framing policies, budgets and strategies for financial

operations and activities of organisation. Proper or sound financial planning can be helpful in

many ways such as determining capital requirements, framing financial policies, determining

capital structure etc. adequate funds can also be ensured with help of financial planning for

attainment of desired business objectives.

Decision-making accounting: This tool is useful when there are various alternatives are

available and management have to choose best alternative out of them. Costs of these various

alternatives are compared and whichever alternatives consumes minimum cot gets selected. This

9

method suggests option which will provide most revenue and lesser cost on basis of accounting.

Thus it is very useful tool in making important financial decisions of organisation.

Management information system: This system is used in business for effective

communication within organisation. Employees of organisation can use this information system

to understand and fulfil their duties. This system also concentrates over accounting and economic

aspects of organisation by identifying problems and resolving them.

LO4 Ways in which organisations could use management accounting to address financial

problems

P5 Adaptation of management accounting systems to resolve financial problems

Financial problem is a situation in which organisation cannot pay its debts or continue

business due to lack of financial resources or financial mismanagement. Organisations have to

face various financial problems these days such as problem of budgeting, poor cash flow

management, raising loans, unfavourable input-output ratio etc. without appropriate financial

planning (Sunarni, and Ambarriani, 2019. Management accounting systems are used by

managers of Prime furniture private ltd. to deal with such financial problems. Management

accounting system or managerial accounting systems are very useful in identifying and resolving

financial problems of an organisation. Adaptation of these management accounting systems in an

organisations according to current financial problems is explained below.

Company can identify its financial issues with help of management accounting systems

such as using various budgets and with help of those budgets company can identify

variance in actual financial position of company and estimated financial position.

Strategies and policies can be modified or changed on basis of that.

Several key performance indicators or benchmarking methods can be used in in finding

financial issues and problems of company. According to these methods standards of

performance of processes or operations are predetermined and actual outcomes are

compared with those standards to identify financial issues and resolve them.

Skills of a managerial accountant can be very useful for recognize financial issues of an

organisation and address those financial issues.

These systems can be useful for allocation of natural resources, appropriate use of these

resources can be ensured with help of managerial systems.

10

Thus it is very useful tool in making important financial decisions of organisation.

Management information system: This system is used in business for effective

communication within organisation. Employees of organisation can use this information system

to understand and fulfil their duties. This system also concentrates over accounting and economic

aspects of organisation by identifying problems and resolving them.

LO4 Ways in which organisations could use management accounting to address financial

problems

P5 Adaptation of management accounting systems to resolve financial problems

Financial problem is a situation in which organisation cannot pay its debts or continue

business due to lack of financial resources or financial mismanagement. Organisations have to

face various financial problems these days such as problem of budgeting, poor cash flow

management, raising loans, unfavourable input-output ratio etc. without appropriate financial

planning (Sunarni, and Ambarriani, 2019. Management accounting systems are used by

managers of Prime furniture private ltd. to deal with such financial problems. Management

accounting system or managerial accounting systems are very useful in identifying and resolving

financial problems of an organisation. Adaptation of these management accounting systems in an

organisations according to current financial problems is explained below.

Company can identify its financial issues with help of management accounting systems

such as using various budgets and with help of those budgets company can identify

variance in actual financial position of company and estimated financial position.

Strategies and policies can be modified or changed on basis of that.

Several key performance indicators or benchmarking methods can be used in in finding

financial issues and problems of company. According to these methods standards of

performance of processes or operations are predetermined and actual outcomes are

compared with those standards to identify financial issues and resolve them.

Skills of a managerial accountant can be very useful for recognize financial issues of an

organisation and address those financial issues.

These systems can be useful for allocation of natural resources, appropriate use of these

resources can be ensured with help of managerial systems.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.