Management Accounting Principles: Analysis of Cost and Budgeting

VerifiedAdded on 2023/01/05

|12

|3273

|38

Report

AI Summary

This report provides a comprehensive overview of management accounting principles, exploring their significance in business decision-making. It delves into the principles of management accounting, emphasizing their role in improving business functions and outcomes. The report analyzes various cost analysis techniques, including marginal and absorption costing, and presents income statements under both methods. Furthermore, it examines different planning tools used for budgetary control, such as activity-based budgeting and zero-based budgeting, comparing their advantages and disadvantages. The report also evaluates how organizations adapt management accounting systems to address financial challenges, offering insights into effective financial planning and control. Overall, the report offers valuable insights into the practical application of management accounting concepts.

Management

Accounting Principles

1

Accounting Principles

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

TASK ONE......................................................................................................................................3

PART -A..........................................................................................................................................3

Explanation associated with the principles of management accounting.....................................3

Evaluating the use of techniques as well as methods used in management accounting..............4

Evaluation of the way management account is integrated within organisation...........................5

PART-B...........................................................................................................................................6

Application of different cost analysis techniques........................................................................6

TASK TWO.....................................................................................................................................7

PART -A..........................................................................................................................................7

Comparison and contrast between different types of planning tool used for budgetary control

with their respective advantages and disadvantages....................................................................7

PART -B..........................................................................................................................................9

The way different organisation are adapting management accounting system in response to

financial problem.........................................................................................................................9

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

2

INTRODUCTION...........................................................................................................................3

TASK ONE......................................................................................................................................3

PART -A..........................................................................................................................................3

Explanation associated with the principles of management accounting.....................................3

Evaluating the use of techniques as well as methods used in management accounting..............4

Evaluation of the way management account is integrated within organisation...........................5

PART-B...........................................................................................................................................6

Application of different cost analysis techniques........................................................................6

TASK TWO.....................................................................................................................................7

PART -A..........................................................................................................................................7

Comparison and contrast between different types of planning tool used for budgetary control

with their respective advantages and disadvantages....................................................................7

PART -B..........................................................................................................................................9

The way different organisation are adapting management accounting system in response to

financial problem.........................................................................................................................9

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

2

INTRODUCTION

Management accounting is considered to be as the key process which is useful in

preparing the reports associated with the business (Borker, 2016). It is considered to be

prominent for the managers of the company to take long term as well as short term decision

making. This study will focus on developing understanding on the principles of management

accounting. Furthermore, the study also demonstrates the use of techniques and methods used in

management accounting. This study also calculates the cost to use appropriate techniques linked

with the cost analysis by the use of aboriginal and marginal cost. Also, the present study also

determine the advantages and disadvantages of the different planning tools which has been used

within the budgetary control. Lastly, the report will compare and also evaluate ways through

which the management accounting responds to the key financial problems.

TASK ONE

PART -A

Explanation associated with the principles of management accounting.

Management accounting is a key process which is useful in preparing the reports

associated with the business. It is relevant to measure, interpret and analyse the relevant

information to the managers. It is prominent for the managers of the company to take long term

as well as short term decision making. The key principles linked with the management

accounting is considered to be prominent in improving the business functions and helps in taking

prominent set of decision and improve the business results and outcomes.

Influence: The key significant principle linked with the management accounting is that,

it mainly focuses on effectively communicating the key relevant information. It is useful to

effectively strengthen the key process of the decision making (Borker, 2016). The access to the

information must be only with the key relevant professionals within the company.

Relevance: This is another prominent principle which states that the information is

considered to be highly valuable and is considered to be highly useful in the better decision

making. It is relevant to effectively interpret the financial as well as the non- financial details in a

significant and prominent manner.

3

Management accounting is considered to be as the key process which is useful in

preparing the reports associated with the business (Borker, 2016). It is considered to be

prominent for the managers of the company to take long term as well as short term decision

making. This study will focus on developing understanding on the principles of management

accounting. Furthermore, the study also demonstrates the use of techniques and methods used in

management accounting. This study also calculates the cost to use appropriate techniques linked

with the cost analysis by the use of aboriginal and marginal cost. Also, the present study also

determine the advantages and disadvantages of the different planning tools which has been used

within the budgetary control. Lastly, the report will compare and also evaluate ways through

which the management accounting responds to the key financial problems.

TASK ONE

PART -A

Explanation associated with the principles of management accounting.

Management accounting is a key process which is useful in preparing the reports

associated with the business. It is relevant to measure, interpret and analyse the relevant

information to the managers. It is prominent for the managers of the company to take long term

as well as short term decision making. The key principles linked with the management

accounting is considered to be prominent in improving the business functions and helps in taking

prominent set of decision and improve the business results and outcomes.

Influence: The key significant principle linked with the management accounting is that,

it mainly focuses on effectively communicating the key relevant information. It is useful to

effectively strengthen the key process of the decision making (Borker, 2016). The access to the

information must be only with the key relevant professionals within the company.

Relevance: This is another prominent principle which states that the information is

considered to be highly valuable and is considered to be highly useful in the better decision

making. It is relevant to effectively interpret the financial as well as the non- financial details in a

significant and prominent manner.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Value: This is another prominent principle which helps in estimating the value of the

business and also determines the business operations in an accurate and relevant manner

(Abdusalomova, 2020).

Credibility: This principle tends to effectively demonstrate that, stewardship tends to

form credibility. Scrutiny as well as the credibility is prominent for the better decision making. It

is considered to be useful for the near term interest and must ensure business operations are

carried out in an ethical and reliable manner.

Determining the role of management accounting as well as the management accounting

systems.

The key significant role of the management accounting is that it is useful in the better

decision making activities. It is prominent to effectively determine the existing set of expenses

and is considered to be relevant for the evidence based decision in a significant and reliable

manner. It is considered to be highly significant in analysing the budget and suggesting the

funding and allocation. Management accounting system is relevant to effectively evaluate the

process for the management of internal process within the company (Oyewo, 2020). The key

benefit of the management accounting system is that, it must focus on effectively planning as

well as controlling the key operations of the business in a significant and relevant manner. It is

considered to be relevant in improving the business operations with high degree of accuracy and

key relevance.

Evaluating the use of techniques as well as methods used in management accounting.

Management accounting system is useful in effectively planning as well as controlling

the key operations of the business. It is useful in taking internal decision of the company and

leads to better decision making and improved business operations.

Cost accounting system: This is the significant framework which has been used by the

company to effectively evaluate and also estimate the cost of the products which is useful

for the analysis of the profitability. It is useful for the disclosure of the unprofitable and

profitable set of activities (Lebedev, 2019). It is significant for the periodical

determination of the profit and losses of the company.

Benefits of Cost accounting system

4

business and also determines the business operations in an accurate and relevant manner

(Abdusalomova, 2020).

Credibility: This principle tends to effectively demonstrate that, stewardship tends to

form credibility. Scrutiny as well as the credibility is prominent for the better decision making. It

is considered to be useful for the near term interest and must ensure business operations are

carried out in an ethical and reliable manner.

Determining the role of management accounting as well as the management accounting

systems.

The key significant role of the management accounting is that it is useful in the better

decision making activities. It is prominent to effectively determine the existing set of expenses

and is considered to be relevant for the evidence based decision in a significant and reliable

manner. It is considered to be highly significant in analysing the budget and suggesting the

funding and allocation. Management accounting system is relevant to effectively evaluate the

process for the management of internal process within the company (Oyewo, 2020). The key

benefit of the management accounting system is that, it must focus on effectively planning as

well as controlling the key operations of the business in a significant and relevant manner. It is

considered to be relevant in improving the business operations with high degree of accuracy and

key relevance.

Evaluating the use of techniques as well as methods used in management accounting.

Management accounting system is useful in effectively planning as well as controlling

the key operations of the business. It is useful in taking internal decision of the company and

leads to better decision making and improved business operations.

Cost accounting system: This is the significant framework which has been used by the

company to effectively evaluate and also estimate the cost of the products which is useful

for the analysis of the profitability. It is useful for the disclosure of the unprofitable and

profitable set of activities (Lebedev, 2019). It is significant for the periodical

determination of the profit and losses of the company.

Benefits of Cost accounting system

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

This system is prominent to effectively disclose the profitable as well as unprofitable

activities within the company. It is useful in controlling the cost linked with the material and

supplies. It is useful for the reliable set of comparison and periodical degree of determination

associated with the profit and loss of the company.

Inventory management system: It is considered to be as the key significant procedure

which is relevant to track the key goods which is useful in effectively tracking the goods

effectively throughout the entire supply chain which mainly starts from the production to

the end of sales.

Benefits of Inventory management system

Inventory management system is significant in avoiding the excess stock or the stock

outs. It helps in maintaining optimum level of stock for the specific period. It is relevant in

reducing the risk of overselling and simplifying the inventory management.

Job costing system: It is mainly involved as the key procedure which is considered to be

prominent in accumulating the key relevant information related with the cost which is

mainly linked with the specific job (What Is a Management Accounting System?, 2018).

It is relevant in submitting the cost information and also helps in determining from where

the cost has been reimbursed.

Benefits of Job costing system

This management accounting system is useful in accurately determining the key

profitability associated with the individual operations linked with the specific job. It i9s also

useful in the prediction of the employee performance benchmark and is relevant to measure the

indirect cost (Borker, 2016). This system is prominent in effectively monitoring the cost linked

with the manufacturing process.

Evaluation of the way management account is integrated within organisation

Management accounting provide key insight to top executive of JMrunsa to take

appropriate decision for growth and success of business by maintain record of financial

information. Integration of management accounting will also contribute manager in taking

correct decision regarding areas that need to be providing more attention as compared to others.

Therefore integration of management account is necessary so JMrunsa manager complete the

5

activities within the company. It is useful in controlling the cost linked with the material and

supplies. It is useful for the reliable set of comparison and periodical degree of determination

associated with the profit and loss of the company.

Inventory management system: It is considered to be as the key significant procedure

which is relevant to track the key goods which is useful in effectively tracking the goods

effectively throughout the entire supply chain which mainly starts from the production to

the end of sales.

Benefits of Inventory management system

Inventory management system is significant in avoiding the excess stock or the stock

outs. It helps in maintaining optimum level of stock for the specific period. It is relevant in

reducing the risk of overselling and simplifying the inventory management.

Job costing system: It is mainly involved as the key procedure which is considered to be

prominent in accumulating the key relevant information related with the cost which is

mainly linked with the specific job (What Is a Management Accounting System?, 2018).

It is relevant in submitting the cost information and also helps in determining from where

the cost has been reimbursed.

Benefits of Job costing system

This management accounting system is useful in accurately determining the key

profitability associated with the individual operations linked with the specific job. It i9s also

useful in the prediction of the employee performance benchmark and is relevant to measure the

indirect cost (Borker, 2016). This system is prominent in effectively monitoring the cost linked

with the manufacturing process.

Evaluation of the way management account is integrated within organisation

Management accounting provide key insight to top executive of JMrunsa to take

appropriate decision for growth and success of business by maintain record of financial

information. Integration of management accounting will also contribute manager in taking

correct decision regarding areas that need to be providing more attention as compared to others.

Therefore integration of management account is necessary so JMrunsa manager complete the

5

process by maintaining records of data, facts and figure in document thereby they can be used as

and when required for achievement of end goals. Regular reporting, collecting fact and figure

also helped in integrating crucial information or management accounting within organisation.

PART-B

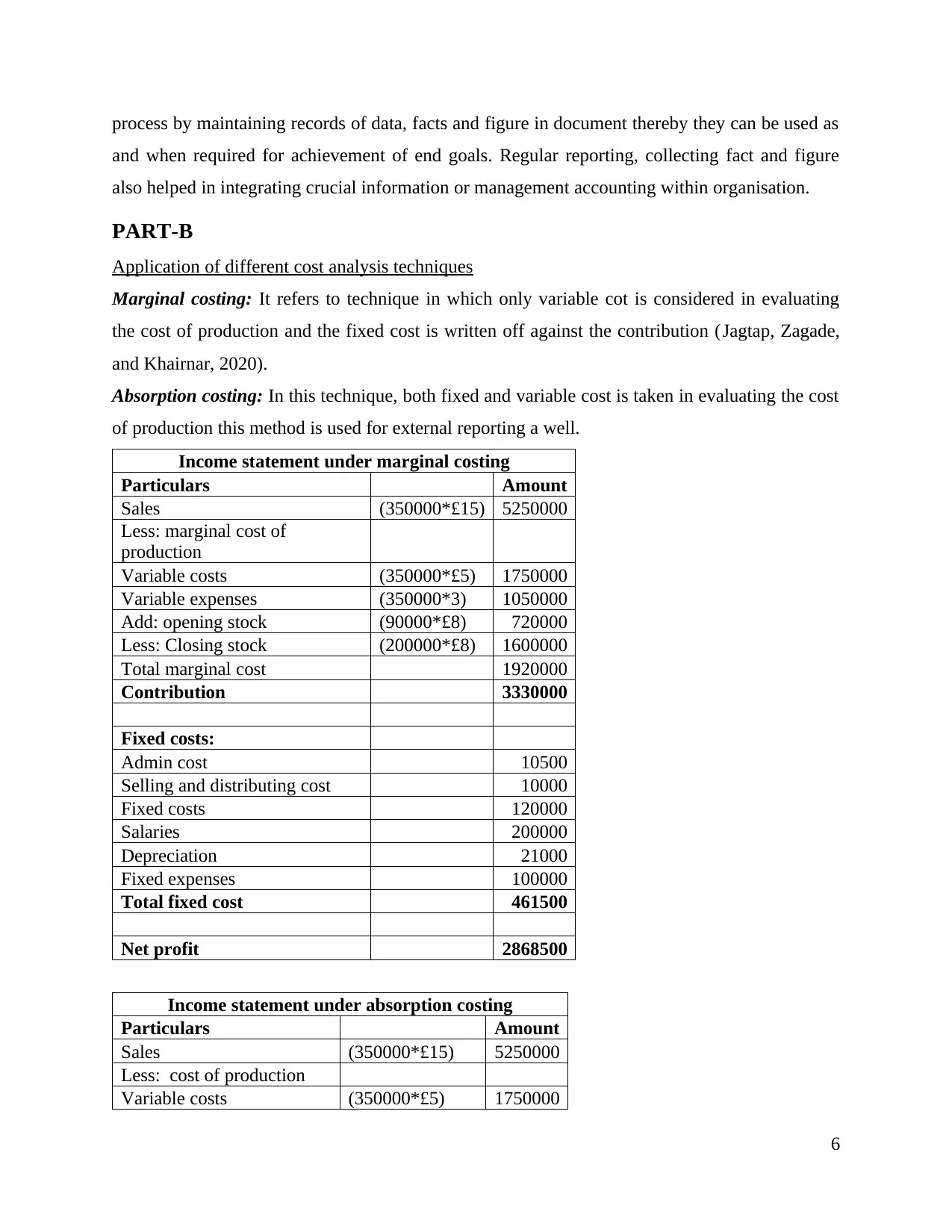

Application of different cost analysis techniques

Marginal costing: It refers to technique in which only variable cot is considered in evaluating

the cost of production and the fixed cost is written off against the contribution (Jagtap, Zagade,

and Khairnar, 2020).

Absorption costing: In this technique, both fixed and variable cost is taken in evaluating the cost

of production this method is used for external reporting a well.

Income statement under marginal costing

Particulars Amount

Sales (350000*£15) 5250000

Less: marginal cost of

production

Variable costs (350000*£5) 1750000

Variable expenses (350000*3) 1050000

Add: opening stock (90000*£8) 720000

Less: Closing stock (200000*£8) 1600000

Total marginal cost 1920000

Contribution 3330000

Fixed costs:

Admin cost 10500

Selling and distributing cost 10000

Fixed costs 120000

Salaries 200000

Depreciation 21000

Fixed expenses 100000

Total fixed cost 461500

Net profit 2868500

Income statement under absorption costing

Particulars Amount

Sales (350000*£15) 5250000

Less: cost of production

Variable costs (350000*£5) 1750000

6

and when required for achievement of end goals. Regular reporting, collecting fact and figure

also helped in integrating crucial information or management accounting within organisation.

PART-B

Application of different cost analysis techniques

Marginal costing: It refers to technique in which only variable cot is considered in evaluating

the cost of production and the fixed cost is written off against the contribution (Jagtap, Zagade,

and Khairnar, 2020).

Absorption costing: In this technique, both fixed and variable cost is taken in evaluating the cost

of production this method is used for external reporting a well.

Income statement under marginal costing

Particulars Amount

Sales (350000*£15) 5250000

Less: marginal cost of

production

Variable costs (350000*£5) 1750000

Variable expenses (350000*3) 1050000

Add: opening stock (90000*£8) 720000

Less: Closing stock (200000*£8) 1600000

Total marginal cost 1920000

Contribution 3330000

Fixed costs:

Admin cost 10500

Selling and distributing cost 10000

Fixed costs 120000

Salaries 200000

Depreciation 21000

Fixed expenses 100000

Total fixed cost 461500

Net profit 2868500

Income statement under absorption costing

Particulars Amount

Sales (350000*£15) 5250000

Less: cost of production

Variable costs (350000*£5) 1750000

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

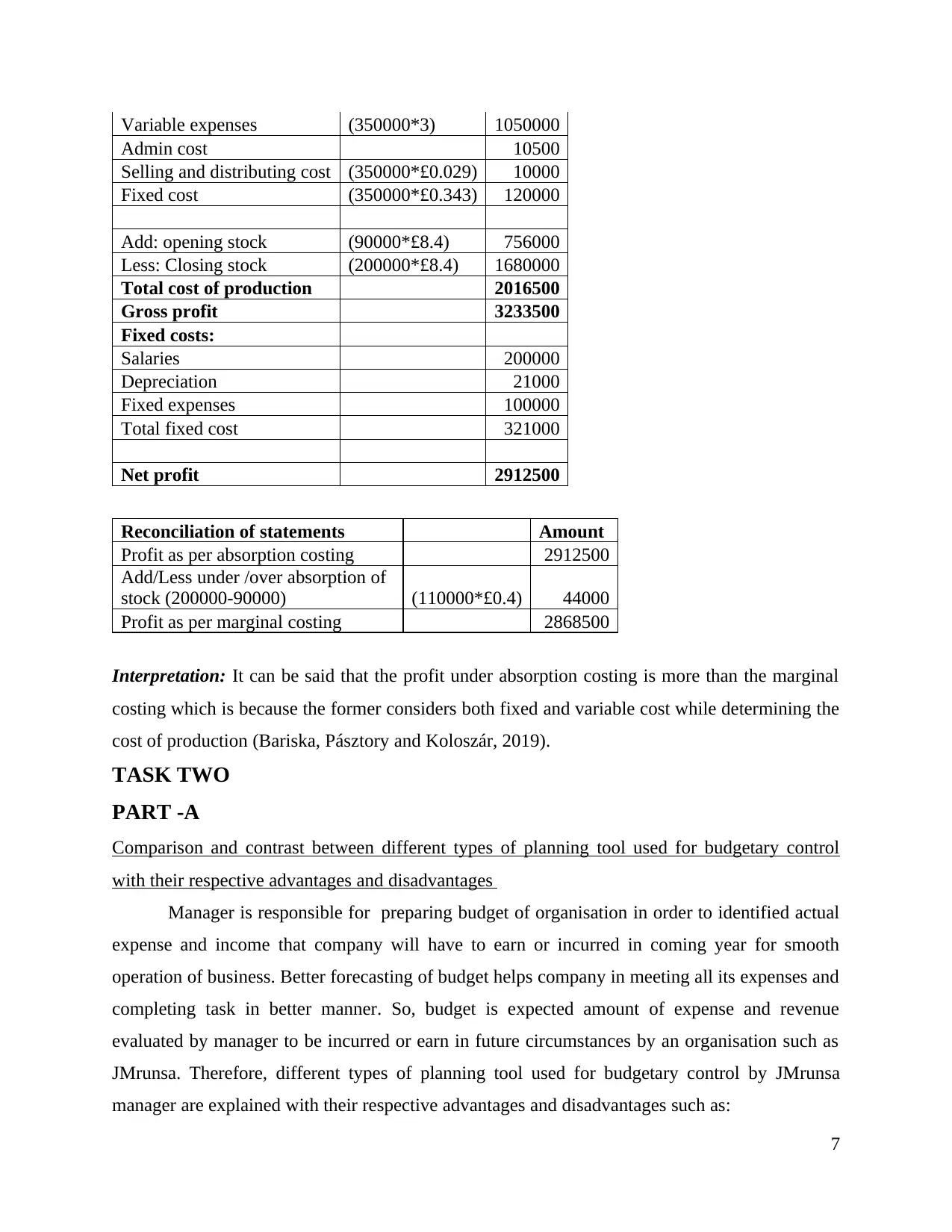

Variable expenses (350000*3) 1050000

Admin cost 10500

Selling and distributing cost (350000*£0.029) 10000

Fixed cost (350000*£0.343) 120000

Add: opening stock (90000*£8.4) 756000

Less: Closing stock (200000*£8.4) 1680000

Total cost of production 2016500

Gross profit 3233500

Fixed costs:

Salaries 200000

Depreciation 21000

Fixed expenses 100000

Total fixed cost 321000

Net profit 2912500

Reconciliation of statements Amount

Profit as per absorption costing 2912500

Add/Less under /over absorption of

stock (200000-90000) (110000*£0.4) 44000

Profit as per marginal costing 2868500

Interpretation: It can be said that the profit under absorption costing is more than the marginal

costing which is because the former considers both fixed and variable cost while determining the

cost of production (Bariska, Pásztory and Koloszár, 2019).

TASK TWO

PART -A

Comparison and contrast between different types of planning tool used for budgetary control

with their respective advantages and disadvantages

Manager is responsible for preparing budget of organisation in order to identified actual

expense and income that company will have to earn or incurred in coming year for smooth

operation of business. Better forecasting of budget helps company in meeting all its expenses and

completing task in better manner. So, budget is expected amount of expense and revenue

evaluated by manager to be incurred or earn in future circumstances by an organisation such as

JMrunsa. Therefore, different types of planning tool used for budgetary control by JMrunsa

manager are explained with their respective advantages and disadvantages such as:

7

Admin cost 10500

Selling and distributing cost (350000*£0.029) 10000

Fixed cost (350000*£0.343) 120000

Add: opening stock (90000*£8.4) 756000

Less: Closing stock (200000*£8.4) 1680000

Total cost of production 2016500

Gross profit 3233500

Fixed costs:

Salaries 200000

Depreciation 21000

Fixed expenses 100000

Total fixed cost 321000

Net profit 2912500

Reconciliation of statements Amount

Profit as per absorption costing 2912500

Add/Less under /over absorption of

stock (200000-90000) (110000*£0.4) 44000

Profit as per marginal costing 2868500

Interpretation: It can be said that the profit under absorption costing is more than the marginal

costing which is because the former considers both fixed and variable cost while determining the

cost of production (Bariska, Pásztory and Koloszár, 2019).

TASK TWO

PART -A

Comparison and contrast between different types of planning tool used for budgetary control

with their respective advantages and disadvantages

Manager is responsible for preparing budget of organisation in order to identified actual

expense and income that company will have to earn or incurred in coming year for smooth

operation of business. Better forecasting of budget helps company in meeting all its expenses and

completing task in better manner. So, budget is expected amount of expense and revenue

evaluated by manager to be incurred or earn in future circumstances by an organisation such as

JMrunsa. Therefore, different types of planning tool used for budgetary control by JMrunsa

manager are explained with their respective advantages and disadvantages such as:

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACTIVITY BASED BUDGETING

It is planning tool of budgetary control in which activities that will lead in incurring cost

to firm are recorded and analysed. This method is mostly useful for new enterprise that has

initially started their business operation. At the same time, this method does not undertake past

year budget while making current budget thus cost are deeply research, identified and analysed.

So, manager of JMrunsa in order to find actual cost that company need to incurred in future

scrutinised activities and its potential cost that helps it in preparing accurate budget for

organisation.

Advantages

Evaluation: The biggest advantages of using activity based budgeting is that it helps in

evaluating and analyzing each cost driver as manager while preparing budget undertake each

step involved in the activity (Mazikana, 2019). Thus manager of JMrunsa has eliminated

unnecessary activities or steps so that maximum outcome can be gained at minimum input or

budget thereby easily gains competitive advantages.

Disadvantages

Required understanding: It can be stated that manager for making use of activity based

budgeting must have deep understanding of several activities or function that has to be complete

by organisation in order to attain its objectives.

ZERO BASED BUDGETING

It is budgeting technique in which zero bases in taken in order to prepare budget for

financial year or in another word, manager justified for all expenses for every new period.

Therefore, manager of JMrunsa in order to make use of zero based budgeting techniques needs to

restart planning of all expense that company will make in future circumstances to attain end

goals.

Advantages

Justification of all operating expense: The benefit of using zero based budgeting planning tool

is that manager need to justified for each dollar company will spend in particular task to attain its

goals. Thus, it will contribute in minimising unnecessary expense as clear justification is given

about where and whom much capital will be required to complete the task (Popova-Yosifova,

2020).

Disadvantages

8

It is planning tool of budgetary control in which activities that will lead in incurring cost

to firm are recorded and analysed. This method is mostly useful for new enterprise that has

initially started their business operation. At the same time, this method does not undertake past

year budget while making current budget thus cost are deeply research, identified and analysed.

So, manager of JMrunsa in order to find actual cost that company need to incurred in future

scrutinised activities and its potential cost that helps it in preparing accurate budget for

organisation.

Advantages

Evaluation: The biggest advantages of using activity based budgeting is that it helps in

evaluating and analyzing each cost driver as manager while preparing budget undertake each

step involved in the activity (Mazikana, 2019). Thus manager of JMrunsa has eliminated

unnecessary activities or steps so that maximum outcome can be gained at minimum input or

budget thereby easily gains competitive advantages.

Disadvantages

Required understanding: It can be stated that manager for making use of activity based

budgeting must have deep understanding of several activities or function that has to be complete

by organisation in order to attain its objectives.

ZERO BASED BUDGETING

It is budgeting technique in which zero bases in taken in order to prepare budget for

financial year or in another word, manager justified for all expenses for every new period.

Therefore, manager of JMrunsa in order to make use of zero based budgeting techniques needs to

restart planning of all expense that company will make in future circumstances to attain end

goals.

Advantages

Justification of all operating expense: The benefit of using zero based budgeting planning tool

is that manager need to justified for each dollar company will spend in particular task to attain its

goals. Thus, it will contribute in minimising unnecessary expense as clear justification is given

about where and whom much capital will be required to complete the task (Popova-Yosifova,

2020).

Disadvantages

8

Resource intensive: The biggest disadvantages or limitation of zero based budgeting is that it

involves more resources, time in order to closely review and analysis actual cost that company

need to incur in order to achieve its desired goals.

OPERATION BUDGETING

It state overall operating expense and revenue that company will received or spend

during particular accounting period in order to promote its business operation. Manager by

planning in advance or making an report about expect fixed and variable cost is future can

prepare operating budget for the company.

Advantages

Provide assistance to manager: Manager by making use of previous budget can easily and

timely prepare budget for the company so that several activities can be completed and goals can

be achieved. Therefore, manager of JMrunsa can easily make best utilisation of resources by

investing them in different fields for growth and expansion of firm.

Disadvantages

Use of previous year budget: On the other hand disadvantages of using operation budgeting is

that it may use of last year financial budgeting which may not resulted in taking accurate

decision for business.

PART -B

The way different organisation are adapting management accounting system in response

to financial problem

There are different method which has been used by enterprise in order to response to their

financial problem such as they are trying to adapt to management accounting system in order to

promote their growth. Key strategies that are used by organisation in order to resolve financial

problem can be illustrated as follows:

Key performance indicator: Company through this process is able to evaluate its performance

with other competitors that are operating in similar industry to earn maximum profit margin.

JMrunsa manager through improving its financial or non financial key performance indicators

can helped company in gaining competitive advantages.

Benchmarking: It is another approach in which enterprise set a bench mark in respect to its

competitors that helps manager in identifying variation or error, mistake in the process so that

9

involves more resources, time in order to closely review and analysis actual cost that company

need to incur in order to achieve its desired goals.

OPERATION BUDGETING

It state overall operating expense and revenue that company will received or spend

during particular accounting period in order to promote its business operation. Manager by

planning in advance or making an report about expect fixed and variable cost is future can

prepare operating budget for the company.

Advantages

Provide assistance to manager: Manager by making use of previous budget can easily and

timely prepare budget for the company so that several activities can be completed and goals can

be achieved. Therefore, manager of JMrunsa can easily make best utilisation of resources by

investing them in different fields for growth and expansion of firm.

Disadvantages

Use of previous year budget: On the other hand disadvantages of using operation budgeting is

that it may use of last year financial budgeting which may not resulted in taking accurate

decision for business.

PART -B

The way different organisation are adapting management accounting system in response

to financial problem

There are different method which has been used by enterprise in order to response to their

financial problem such as they are trying to adapt to management accounting system in order to

promote their growth. Key strategies that are used by organisation in order to resolve financial

problem can be illustrated as follows:

Key performance indicator: Company through this process is able to evaluate its performance

with other competitors that are operating in similar industry to earn maximum profit margin.

JMrunsa manager through improving its financial or non financial key performance indicators

can helped company in gaining competitive advantages.

Benchmarking: It is another approach in which enterprise set a bench mark in respect to its

competitors that helps manager in identifying variation or error, mistake in the process so that

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

corrective action can be taken for better outcome. Therefore, benchmarking helps company in

understanding key areas in which it lack thereby helping in formulating key strategies that can be

fruitful for organisation.

Budgetary target: In this method companies set different budget to complete specific task that

helps in comparing whether one firm has effectively utilised its fund or not as compared to other

organisation in external environment (Vatslavskyi, 2016). Thus, necessary steps can be taken by

manager in order to make optimum utilisation of resources so that end goals of firm can be

achieved.

Comparison between two firm regarding the way they have adapted to management accounting

for resolving their financial issue

Walmart has made use of cost account system

in order to make record of all expense or cost

of production that are incurred by company to

complete its specific task. Cost management

accounting system has contributed in

eliminating unnecessary cost thus resolving

some of the financial issue of firm.

On the other hand it can be stated that Coca

Cola is company that has make use of job

costing system in order to resolve financial

problem. Manager through job costing is able

to identified actual cost company need to incur

in order to complete the job or task. Thus, it

helps manager in taking decision to remove

addition cost or unnecessary expense on job

that are not profitable for organisation.

It can be analysis from above comparison that both organisations by adapting to different

management accounting system is able to contributed in growth and success of firm by resolving

key financial issue. Like cost accounting system has helped in maintaining records of several

cost or expense that company incurred in order to achieve their respective objectives (Nielsen

and Pontoppidan, 2019). While, job costing helps in understanding actual expenses incurred to

complete particular task thus contributed in resolving key financial issue.

10

understanding key areas in which it lack thereby helping in formulating key strategies that can be

fruitful for organisation.

Budgetary target: In this method companies set different budget to complete specific task that

helps in comparing whether one firm has effectively utilised its fund or not as compared to other

organisation in external environment (Vatslavskyi, 2016). Thus, necessary steps can be taken by

manager in order to make optimum utilisation of resources so that end goals of firm can be

achieved.

Comparison between two firm regarding the way they have adapted to management accounting

for resolving their financial issue

Walmart has made use of cost account system

in order to make record of all expense or cost

of production that are incurred by company to

complete its specific task. Cost management

accounting system has contributed in

eliminating unnecessary cost thus resolving

some of the financial issue of firm.

On the other hand it can be stated that Coca

Cola is company that has make use of job

costing system in order to resolve financial

problem. Manager through job costing is able

to identified actual cost company need to incur

in order to complete the job or task. Thus, it

helps manager in taking decision to remove

addition cost or unnecessary expense on job

that are not profitable for organisation.

It can be analysis from above comparison that both organisations by adapting to different

management accounting system is able to contributed in growth and success of firm by resolving

key financial issue. Like cost accounting system has helped in maintaining records of several

cost or expense that company incurred in order to achieve their respective objectives (Nielsen

and Pontoppidan, 2019). While, job costing helps in understanding actual expenses incurred to

complete particular task thus contributed in resolving key financial issue.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONCLUSION

From the above report it can be concluded that accounting management is process in

which manager ensure that all financial records and reports are kept safe and secure so that it can

be used by interested people or stakeholders. It has also been learnt that there are different

method of preparing management accounting report that is used by JMrunsa to present its

financial information. At last it can be concluded from above discussion that companies in order

to overcome financial problem are adapting to management accounting which has contributed in

growth and success of firm.

11

From the above report it can be concluded that accounting management is process in

which manager ensure that all financial records and reports are kept safe and secure so that it can

be used by interested people or stakeholders. It has also been learnt that there are different

method of preparing management accounting report that is used by JMrunsa to present its

financial information. At last it can be concluded from above discussion that companies in order

to overcome financial problem are adapting to management accounting which has contributed in

growth and success of firm.

11

REFERENCES

Books and journals

Abdusalomova, N., 2020. Principles of ties of internal control and management accounting

systems at the enterprises of black metallurgy. Архив научных исследований, (2).

Borker, D.R., 2016. Gauging the impact of country-specific values on the acceptability of global

management accounting principles.

Lebedev, P., 2019. Management Accounting Practices in Mid-Sized Companies in Emerging

Economies: An Evidence from Russia. Knowledge–Economy–Society: Challenges for

Contemporary Economies–Global, Regional, Network and Organizational Perspective,

pp.93-103.

Mazikana, A. T., 2019. The Effect of Budgetary Controls on the Performance of an

Organization. Available at SSRN 3445247.

Nielsen, S. and Pontoppidan, I. C., 2019. Exploring the inclusion of risk in management

accounting and control. Management Research Review.

Oyewo, B.M., 2020. Outcomes of interaction between organizational characteristics and

management accounting practice on corporate sustainability: the global management

accounting principles (GMAP) approach. Journal of Sustainable Finance & Investment,

pp.1-35.

Popova-Yosifova, N., 2020. Opportunities For Improvementof The Financial Managementand

Control Systemin The Budgetary Organizations. Economic Science, education and the

real economy: Development and interactions in the digital age, (1). pp.519-528.

Saukkonen, N., Laine, T. and Suomala, P., 2018. Utilizing management accounting information

for decision-making. Qualitative Research in Accounting & Management.

Vatslavskyi, O., 2016. Question of improvement of budget control at the local level. Baltic

Journal of Economic Studies, 2(5).

Jagtap, P. K., Zagade, S. and Khairnar, S., 2020. Cost and Works Accounting (Paper III).

Diamond Publications.

Bariska, M., Pásztory, Z. and Koloszár, L., 2019. The Efficiency Based Costing Method–Using a

Sawmill as Example. EUROPEAN RESEARCH STUDIES: AN INTERNATIONAL

MULTIDISCIPLINARY JOURNAL WITH TOPICS IN EUROPEAN

INTEGRATION. 22(2). pp.229-243.

Online

What Is a Management Accounting System?. 2018. [Online]. Available through:

<https://bizfluent.com/facts-5460765-management-accounting-system.html>

12

Books and journals

Abdusalomova, N., 2020. Principles of ties of internal control and management accounting

systems at the enterprises of black metallurgy. Архив научных исследований, (2).

Borker, D.R., 2016. Gauging the impact of country-specific values on the acceptability of global

management accounting principles.

Lebedev, P., 2019. Management Accounting Practices in Mid-Sized Companies in Emerging

Economies: An Evidence from Russia. Knowledge–Economy–Society: Challenges for

Contemporary Economies–Global, Regional, Network and Organizational Perspective,

pp.93-103.

Mazikana, A. T., 2019. The Effect of Budgetary Controls on the Performance of an

Organization. Available at SSRN 3445247.

Nielsen, S. and Pontoppidan, I. C., 2019. Exploring the inclusion of risk in management

accounting and control. Management Research Review.

Oyewo, B.M., 2020. Outcomes of interaction between organizational characteristics and

management accounting practice on corporate sustainability: the global management

accounting principles (GMAP) approach. Journal of Sustainable Finance & Investment,

pp.1-35.

Popova-Yosifova, N., 2020. Opportunities For Improvementof The Financial Managementand

Control Systemin The Budgetary Organizations. Economic Science, education and the

real economy: Development and interactions in the digital age, (1). pp.519-528.

Saukkonen, N., Laine, T. and Suomala, P., 2018. Utilizing management accounting information

for decision-making. Qualitative Research in Accounting & Management.

Vatslavskyi, O., 2016. Question of improvement of budget control at the local level. Baltic

Journal of Economic Studies, 2(5).

Jagtap, P. K., Zagade, S. and Khairnar, S., 2020. Cost and Works Accounting (Paper III).

Diamond Publications.

Bariska, M., Pásztory, Z. and Koloszár, L., 2019. The Efficiency Based Costing Method–Using a

Sawmill as Example. EUROPEAN RESEARCH STUDIES: AN INTERNATIONAL

MULTIDISCIPLINARY JOURNAL WITH TOPICS IN EUROPEAN

INTEGRATION. 22(2). pp.229-243.

Online

What Is a Management Accounting System?. 2018. [Online]. Available through:

<https://bizfluent.com/facts-5460765-management-accounting-system.html>

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.