Management Accounting Problem: Turramurra Furniture Company

VerifiedAdded on 2020/06/06

|7

|1472

|41

Report

AI Summary

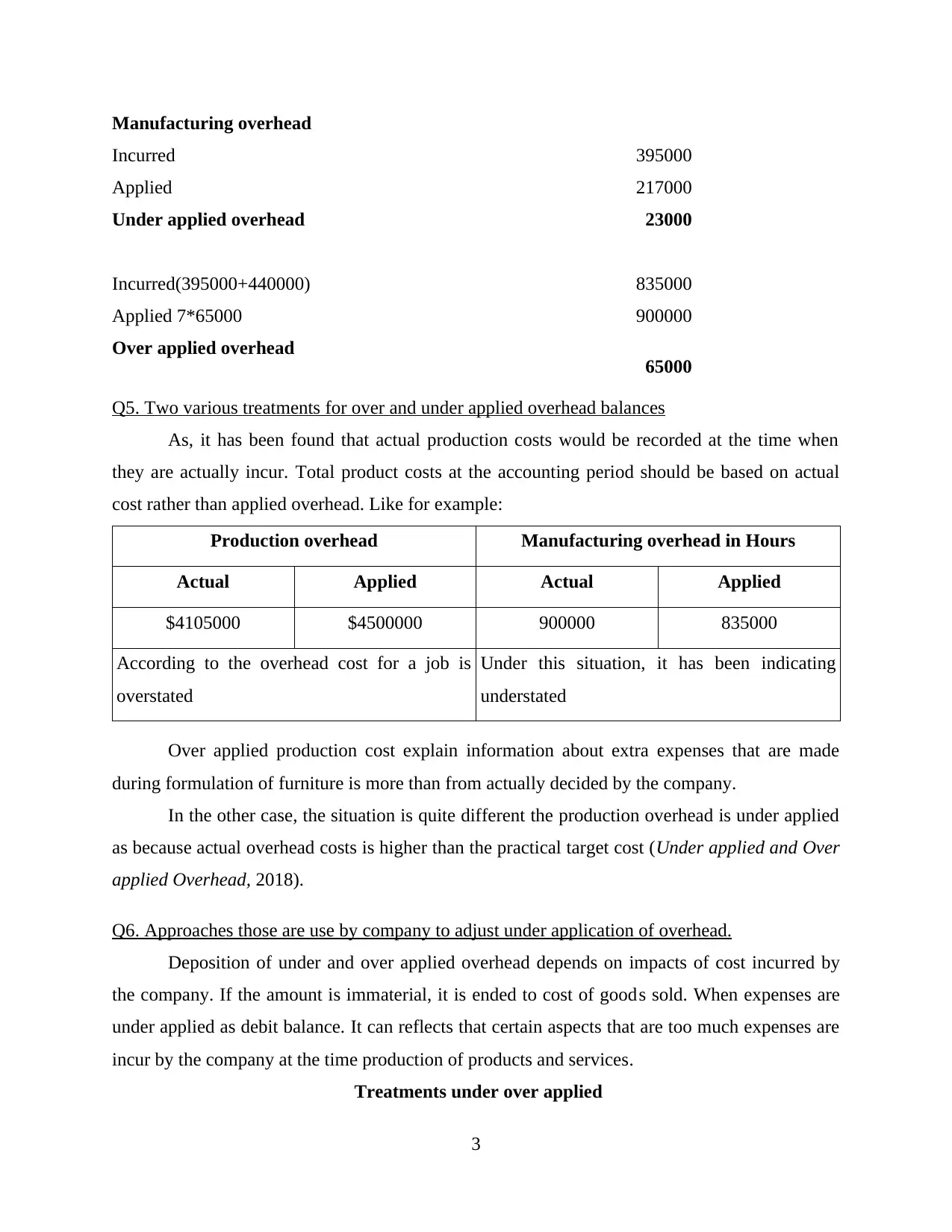

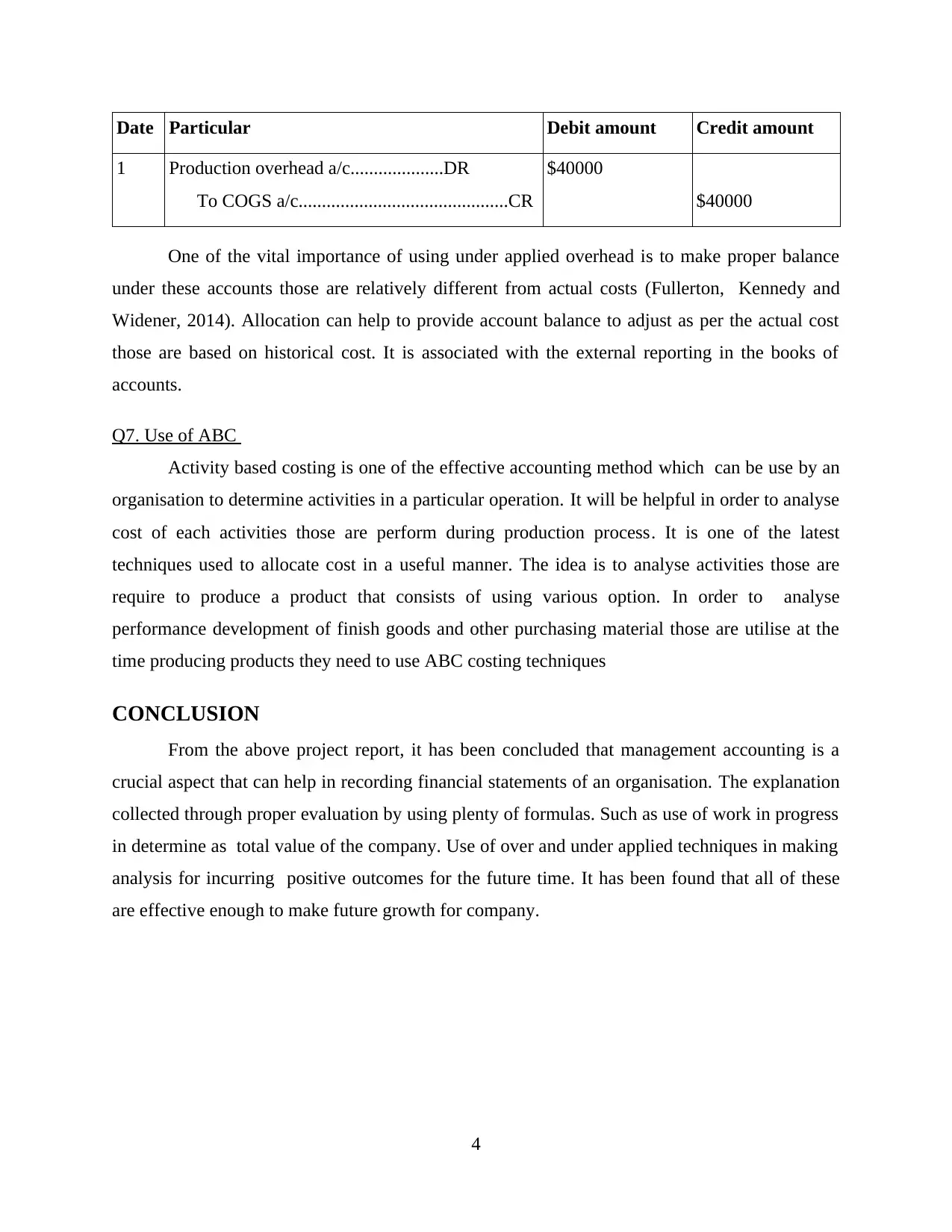

This report analyzes the financial records of the Turramurra Furniture company, addressing key management accounting concepts. It begins by explaining the circumstances in which job costing can be used, then proceeds to calculate Work-in-Progress (WIP). The report also calculates the cost of chairs in finished goods inventory and determines over and under applied overhead. It explains different treatments for over and under applied overhead balances and discusses approaches to adjust under application of overhead. The report concludes with the use of Activity-Based Costing (ABC) to determine activities in a particular operation. The analysis uses formulas and evaluations to provide insights into the company's financial performance and growth potential.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.