Management Accounting Systems: Financial Analysis & Planning Tools

VerifiedAdded on 2024/05/20

|17

|3879

|217

Report

AI Summary

This report provides a comprehensive overview of management accounting systems, including their definition, types, and reporting methods. It evaluates the benefits of these systems within an organizational context and explores their integration into organizational processes. The report also delves into income statements under marginal and absorption costing, explaining the differences and their impact on financial reporting. Furthermore, it discusses the use of planning tools in management accounting, focusing on budgetary control, and analyzes how organizations adapt management accounting systems to respond to financial problems, ultimately aiming for sustainable success. The document includes practical examples and reconciliations to illustrate key concepts.

Management Accounting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Introduction:..............................................................................................................................3

LO1: Demonstrate an understanding of management accounting systems..................4

P1: Explain management accounting and give the essential requirements of

different types of management accounting.....................................................................4

P2: Explain different methods used for management accounting reporting..............6

M1: Evaluate the benefits of management accounting systems and their

application within an organizational context................................................................7

D1: how management accounting systems and management accounting

reporting are integrated within organizational processes.........................................8

LO2: Income statement under marginal and absorption costing.....................................9

LO3: Explain the use of planning tools used in management accounting...................12

P4 Explain the advantages and disadvantages of different types of planning tools

used in the budgetary control..........................................................................................12

M3 Analyse the use of different planning tools and their application for preparing

and forecasting budgets...................................................................................................13

LO4: Compare ways in which organizations could use management accounting to

respond to financial problems.............................................................................................14

P5 Compare how organizations are adapting management accounting systems to

respond to financial problems.........................................................................................14

M4 Analyze how, in responding to financial problems, management accounting

can lead organizations to sustainable success............................................................14

References.............................................................................................................................17

2

Introduction:..............................................................................................................................3

LO1: Demonstrate an understanding of management accounting systems..................4

P1: Explain management accounting and give the essential requirements of

different types of management accounting.....................................................................4

P2: Explain different methods used for management accounting reporting..............6

M1: Evaluate the benefits of management accounting systems and their

application within an organizational context................................................................7

D1: how management accounting systems and management accounting

reporting are integrated within organizational processes.........................................8

LO2: Income statement under marginal and absorption costing.....................................9

LO3: Explain the use of planning tools used in management accounting...................12

P4 Explain the advantages and disadvantages of different types of planning tools

used in the budgetary control..........................................................................................12

M3 Analyse the use of different planning tools and their application for preparing

and forecasting budgets...................................................................................................13

LO4: Compare ways in which organizations could use management accounting to

respond to financial problems.............................................................................................14

P5 Compare how organizations are adapting management accounting systems to

respond to financial problems.........................................................................................14

M4 Analyze how, in responding to financial problems, management accounting

can lead organizations to sustainable success............................................................14

References.............................................................................................................................17

2

Introduction:

Management accounting is a tool for the effective management of business

enterprises. Present assignment describes the same. This assignment incorporates

definition and different types of management accounting system. Methods of

management accounting reporting are also discussed in this assignment. In this

assignment various gains of management accounting system and how management

accounting is beneficial for enterprises, is discussed in detail. With the study of this

assignment user can understand the techniques of cost accounting system. User

also enables to understand the Income statement under cost accounting techniques

like marginal and absorption costing. Budgetary control system also explained in this

report. Report describes how planning tolls of management accounting is helpful for

budgeting. various problems which are faced by business in day to day work and

how business organisations are using management tools for solving them is also

defined in this report. In addition, report defines relation of planning tools with the

sustainable success of business briefly.

3

Management accounting is a tool for the effective management of business

enterprises. Present assignment describes the same. This assignment incorporates

definition and different types of management accounting system. Methods of

management accounting reporting are also discussed in this assignment. In this

assignment various gains of management accounting system and how management

accounting is beneficial for enterprises, is discussed in detail. With the study of this

assignment user can understand the techniques of cost accounting system. User

also enables to understand the Income statement under cost accounting techniques

like marginal and absorption costing. Budgetary control system also explained in this

report. Report describes how planning tolls of management accounting is helpful for

budgeting. various problems which are faced by business in day to day work and

how business organisations are using management tools for solving them is also

defined in this report. In addition, report defines relation of planning tools with the

sustainable success of business briefly.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

LO1: Demonstrate an understanding of management accounting

systems.

P1: Explain management accounting and give the essential requirements of

different types of management accounting.

Management accounting: management accounting is a system of examination,

inspection, and broadcasting of financial and non-financial data collected with the

use of cost and finance accounting for the policy planning of an organisation.

Management accounting tools provides support for manage the business activities

according to the goals of company (Kristandl, et. al., 2014). In addition, Management

accounting includes the finance accounting and cost system.

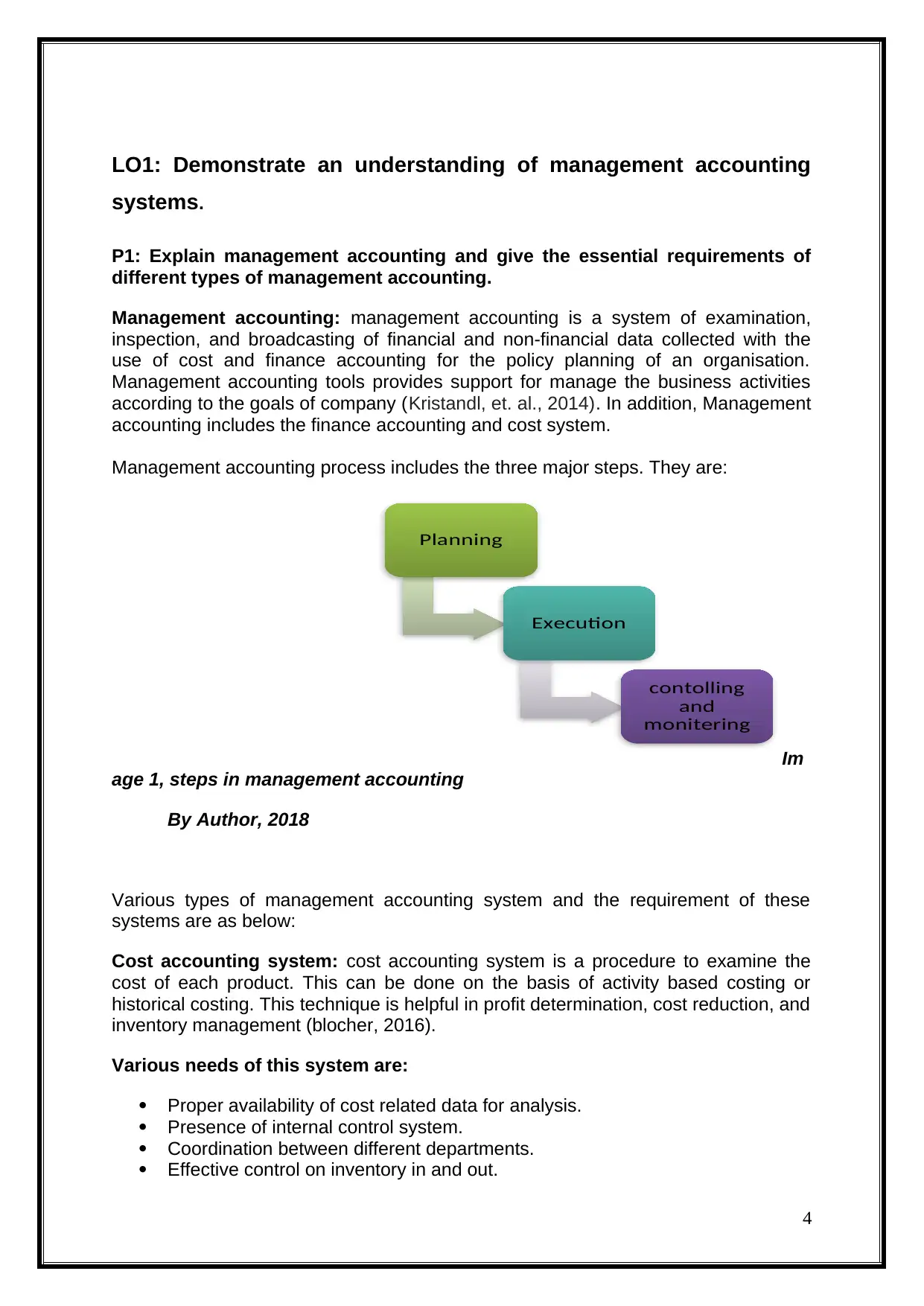

Management accounting process includes the three major steps. They are:

Im

age 1, steps in management accounting

By Author, 2018

Various types of management accounting system and the requirement of these

systems are as below:

Cost accounting system: cost accounting system is a procedure to examine the

cost of each product. This can be done on the basis of activity based costing or

historical costing. This technique is helpful in profit determination, cost reduction, and

inventory management (blocher, 2016).

Various needs of this system are:

Proper availability of cost related data for analysis.

Presence of internal control system.

Coordination between different departments.

Effective control on inventory in and out.

4

Planning

Execution

contolling

and

monitering

systems.

P1: Explain management accounting and give the essential requirements of

different types of management accounting.

Management accounting: management accounting is a system of examination,

inspection, and broadcasting of financial and non-financial data collected with the

use of cost and finance accounting for the policy planning of an organisation.

Management accounting tools provides support for manage the business activities

according to the goals of company (Kristandl, et. al., 2014). In addition, Management

accounting includes the finance accounting and cost system.

Management accounting process includes the three major steps. They are:

Im

age 1, steps in management accounting

By Author, 2018

Various types of management accounting system and the requirement of these

systems are as below:

Cost accounting system: cost accounting system is a procedure to examine the

cost of each product. This can be done on the basis of activity based costing or

historical costing. This technique is helpful in profit determination, cost reduction, and

inventory management (blocher, 2016).

Various needs of this system are:

Proper availability of cost related data for analysis.

Presence of internal control system.

Coordination between different departments.

Effective control on inventory in and out.

4

Planning

Execution

contolling

and

monitering

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Regular inventory physical examination.

Price optimisation method: POM is an approach of analysis to investigate the

customer reaction on different price levels for products and services. This approach

is used to identify the best price of product so company can achieve the desired

targets of high sales and profit and eliminate the undesired targets. (Drury, 2015)

Different needs of this system are:

Previous sales, price and cost related information

Regular monitoring of prices and expenses by upper level management

Effective communication between sales department, production department

and management.

Inventory management system: Inventory management system assists the

management of inventory. It refers the monitoring and controlling of raw inventory,

work-in-progress and finished inventory. This system includes the process of

ordering, receiving, storing, use for production and sales (Drury, 2015).

Proper valuation of stock according to the guided methods like LIFO, FIFO

etc.

Physical monitoring and control on inventory storage.

Internal control system like internal audit of inventory is necessary for this

system.

Proper selling system of waste or deficit inventory.

Job costing: job costing is used to determinate the price of each job. Job represents

the group of products which are different from each other.

Each job is identified with unique identity.

Direct cost charged to product and fix cost as per standard.

Necessary in cost plus contracts (Drury, 2015).

5

Price optimisation method: POM is an approach of analysis to investigate the

customer reaction on different price levels for products and services. This approach

is used to identify the best price of product so company can achieve the desired

targets of high sales and profit and eliminate the undesired targets. (Drury, 2015)

Different needs of this system are:

Previous sales, price and cost related information

Regular monitoring of prices and expenses by upper level management

Effective communication between sales department, production department

and management.

Inventory management system: Inventory management system assists the

management of inventory. It refers the monitoring and controlling of raw inventory,

work-in-progress and finished inventory. This system includes the process of

ordering, receiving, storing, use for production and sales (Drury, 2015).

Proper valuation of stock according to the guided methods like LIFO, FIFO

etc.

Physical monitoring and control on inventory storage.

Internal control system like internal audit of inventory is necessary for this

system.

Proper selling system of waste or deficit inventory.

Job costing: job costing is used to determinate the price of each job. Job represents

the group of products which are different from each other.

Each job is identified with unique identity.

Direct cost charged to product and fix cost as per standard.

Necessary in cost plus contracts (Drury, 2015).

5

P2: Explain different methods used for management accounting reporting.

Cost report: cost report defines the cost of production. This report contains data

about the cost elements like material labour and overheads. This report enables the

manager to define and control the cost and to maintain profit margins for company

(Harris and Durden, 2012).

Budget: budget reports are prepaid to assist the decision making process by

providing useful information about the business. These reports include the detailed

information about future expenses and incomes. Budget helps to manage the

company growth (Accounting tools, 2018).

Performance reports: performance reports are prepared for the purpose of analysis

of performance. Manager can prepare various performance reports to determinate

the efficiency of employees and take step for eliminate the deficiency (Harris and

Durden, 2012).

Revenue reports: various revenue analysis reports are prepared for the purpose of

reporting under management accounting. Manager can determinate the sales figures

of company and take suitable action for adverse change.

6

Cost report: cost report defines the cost of production. This report contains data

about the cost elements like material labour and overheads. This report enables the

manager to define and control the cost and to maintain profit margins for company

(Harris and Durden, 2012).

Budget: budget reports are prepaid to assist the decision making process by

providing useful information about the business. These reports include the detailed

information about future expenses and incomes. Budget helps to manage the

company growth (Accounting tools, 2018).

Performance reports: performance reports are prepared for the purpose of analysis

of performance. Manager can prepare various performance reports to determinate

the efficiency of employees and take step for eliminate the deficiency (Harris and

Durden, 2012).

Revenue reports: various revenue analysis reports are prepared for the purpose of

reporting under management accounting. Manager can determinate the sales figures

of company and take suitable action for adverse change.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

M1: Evaluate the benefits of management accounting systems and their

application within an organizational context.

Increase flow of funds: management accounting determinates the fund needs. It

also provides the detailed knowledge about the fund comes and goes. Manager can

use this detail for the effective management of funds.

Control on expenses: management accounting gives a strong base to solve the

expenses related problem. It explains the need of every expense. Manager can

analysis the cost of every business activity and take step to eliminate useless

expenditure (Legaspi, 2014).

Performance: management accounting techniques examines the efficiency of each

work unit. Management can identify the short performance and try to solve it with the

help of training and other steps.

Profitability: management accounting tools are used to eliminate the extra

expenditure of every business activity. This increases the profit level indirectly

(Legaspi, 2014).

Two way information system: information is a big resource in today’s business

environment. Management accounting tool gives accurate information about the

business. This information is helpful in strategy planning.

Support in decision making: management tools provide various information

reports about business. Manager can use these reports for the strategy planning,

controlling and decision making.

Fund management: various funding choices are available in market for business.

With the help of management tools manager can analyse all the options and choose

best suitable options. In this way management tools assist the fund management

(Legaspi, 2014).

D1: how management accounting systems and management accounting

reporting are integrated within organizational processes.

Sales reports: sales reports give the details of sales. Manager can determinate the

demand of product at various sales levels. This will helps the manager to set the

best strategies for future (Legaspi, 2014).

Cost reports: cost is very important factor for every business enterprises. A cost

report provides complete and analysed information about every expense. This

information can be used in future for effective management of costs.

Integration of production reports: various production reports explain the problems

of production process. Manager can take action on these problems and create

accuracy in production process (Legaspi, 2014).

7

application within an organizational context.

Increase flow of funds: management accounting determinates the fund needs. It

also provides the detailed knowledge about the fund comes and goes. Manager can

use this detail for the effective management of funds.

Control on expenses: management accounting gives a strong base to solve the

expenses related problem. It explains the need of every expense. Manager can

analysis the cost of every business activity and take step to eliminate useless

expenditure (Legaspi, 2014).

Performance: management accounting techniques examines the efficiency of each

work unit. Management can identify the short performance and try to solve it with the

help of training and other steps.

Profitability: management accounting tools are used to eliminate the extra

expenditure of every business activity. This increases the profit level indirectly

(Legaspi, 2014).

Two way information system: information is a big resource in today’s business

environment. Management accounting tool gives accurate information about the

business. This information is helpful in strategy planning.

Support in decision making: management tools provide various information

reports about business. Manager can use these reports for the strategy planning,

controlling and decision making.

Fund management: various funding choices are available in market for business.

With the help of management tools manager can analyse all the options and choose

best suitable options. In this way management tools assist the fund management

(Legaspi, 2014).

D1: how management accounting systems and management accounting

reporting are integrated within organizational processes.

Sales reports: sales reports give the details of sales. Manager can determinate the

demand of product at various sales levels. This will helps the manager to set the

best strategies for future (Legaspi, 2014).

Cost reports: cost is very important factor for every business enterprises. A cost

report provides complete and analysed information about every expense. This

information can be used in future for effective management of costs.

Integration of production reports: various production reports explain the problems

of production process. Manager can take action on these problems and create

accuracy in production process (Legaspi, 2014).

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

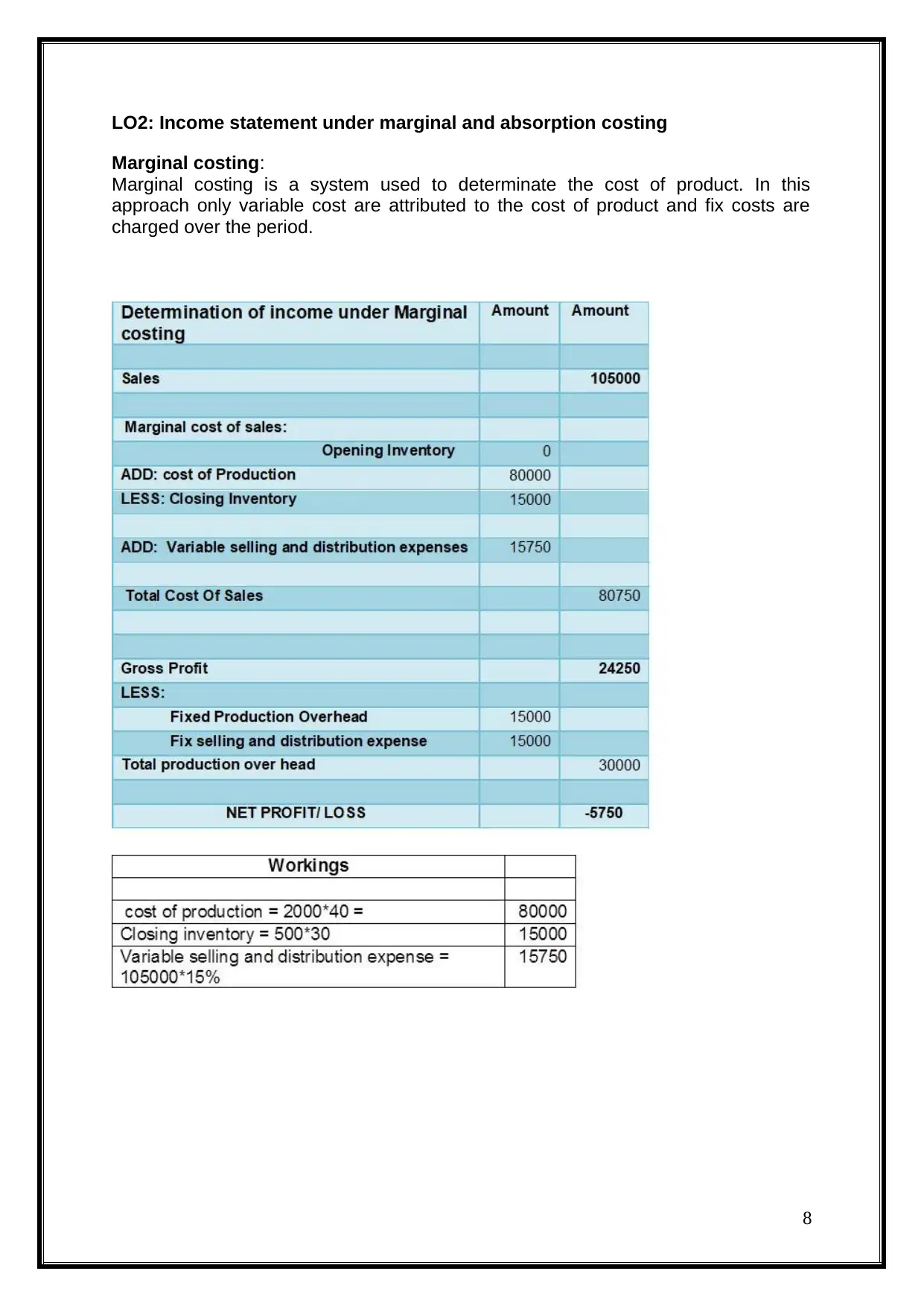

LO2: Income statement under marginal and absorption costing

Marginal costing:

Marginal costing is a system used to determinate the cost of product. In this

approach only variable cost are attributed to the cost of product and fix costs are

charged over the period.

8

Marginal costing:

Marginal costing is a system used to determinate the cost of product. In this

approach only variable cost are attributed to the cost of product and fix costs are

charged over the period.

8

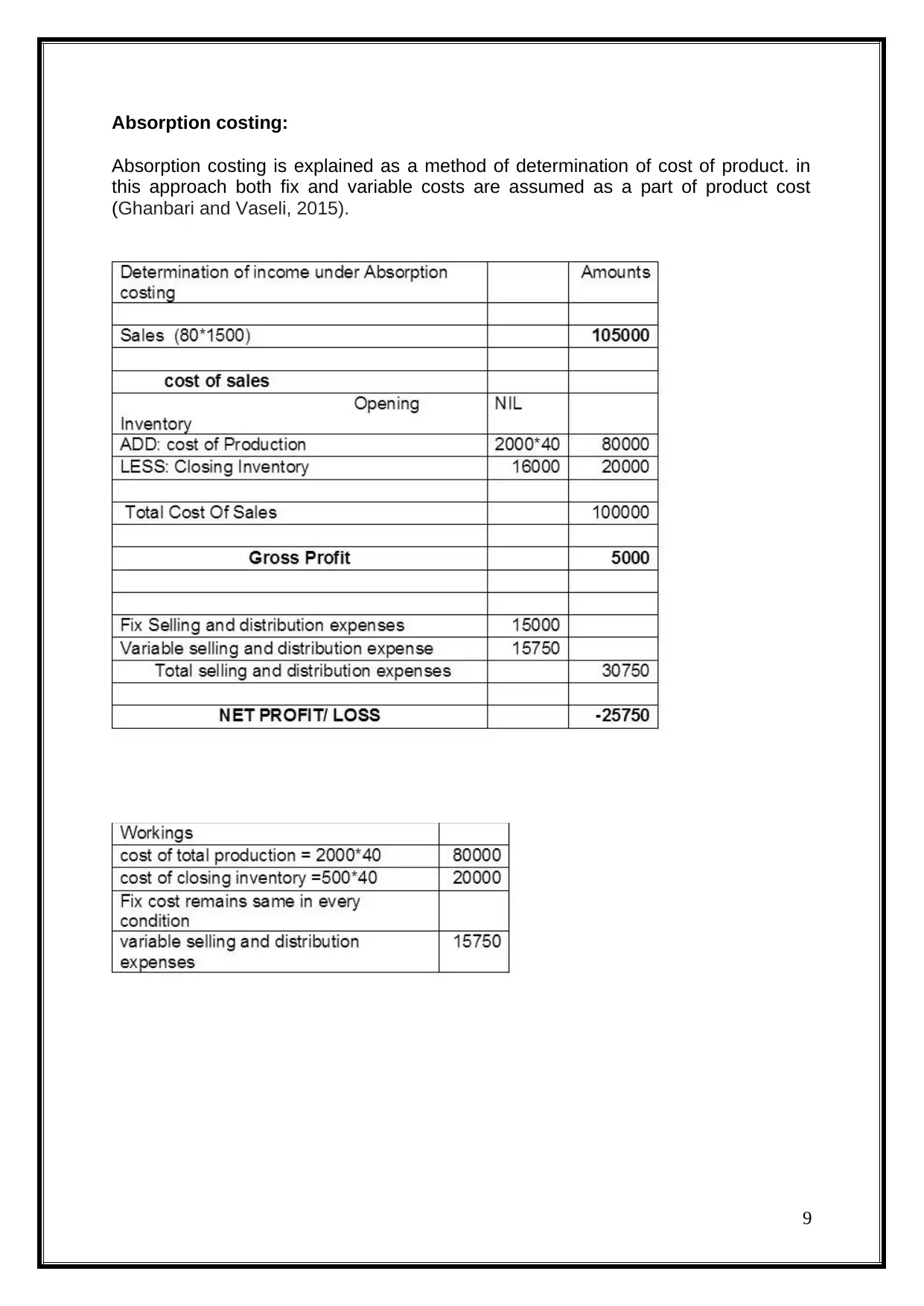

Absorption costing:

Absorption costing is explained as a method of determination of cost of product. in

this approach both fix and variable costs are assumed as a part of product cost

(Ghanbari and Vaseli, 2015).

9

Absorption costing is explained as a method of determination of cost of product. in

this approach both fix and variable costs are assumed as a part of product cost

(Ghanbari and Vaseli, 2015).

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

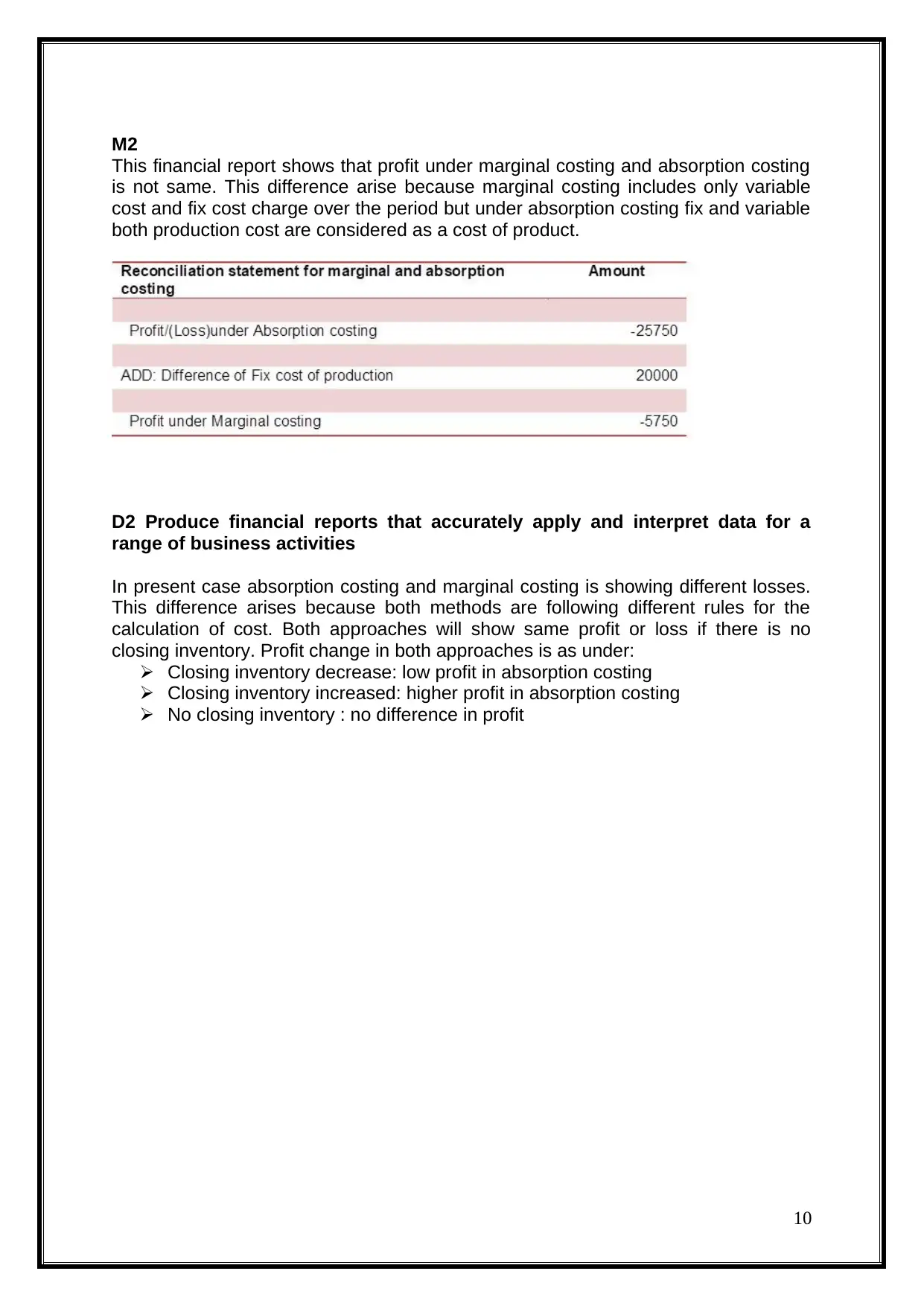

M2

This financial report shows that profit under marginal costing and absorption costing

is not same. This difference arise because marginal costing includes only variable

cost and fix cost charge over the period but under absorption costing fix and variable

both production cost are considered as a cost of product.

D2 Produce financial reports that accurately apply and interpret data for a

range of business activities

In present case absorption costing and marginal costing is showing different losses.

This difference arises because both methods are following different rules for the

calculation of cost. Both approaches will show same profit or loss if there is no

closing inventory. Profit change in both approaches is as under:

Closing inventory decrease: low profit in absorption costing

Closing inventory increased: higher profit in absorption costing

No closing inventory : no difference in profit

10

This financial report shows that profit under marginal costing and absorption costing

is not same. This difference arise because marginal costing includes only variable

cost and fix cost charge over the period but under absorption costing fix and variable

both production cost are considered as a cost of product.

D2 Produce financial reports that accurately apply and interpret data for a

range of business activities

In present case absorption costing and marginal costing is showing different losses.

This difference arises because both methods are following different rules for the

calculation of cost. Both approaches will show same profit or loss if there is no

closing inventory. Profit change in both approaches is as under:

Closing inventory decrease: low profit in absorption costing

Closing inventory increased: higher profit in absorption costing

No closing inventory : no difference in profit

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

LO3: Explain the use of planning tools used in management accounting.

P4 Explain the advantages and disadvantages of different types of planning

tools used in the budgetary control.

In Zylla, there are various changes which are taking place and therefore it is needed

that proper planning shall be done so that it will be possible to deal with all the

situations in a proper manner. Also, the expenses which will be incurred in that

process will be kept under control and this will be beneficial for the company ( De

Jong, et. al., 2012). Budgets are to be made in this situation which is of various

categories such as the financial or capital budget.

Merits of budgets:

The cost which company is required to spend will be identified and by that, it

will be possible to keep a check on them so that they can be controlled.

In various changes, it will be needed that proper process is undertaken so that

risk of errors is reduced and this will be possible with the help of budgets.

All the deviations which will be occurring will be determined and then they will

be taken into consideration in the business with the use of the budget as they

are included in making of it (De Jong, et. al., 2012).

Demerits of budgets:

The figures which are included in the budget are taken on the basis of

projections that are made and so there will be a certain risk which is involved

in this process.

The data which will be required is collected with the use of research and that

requires more time and cost which makes it expensive process and it cannot

be used by all due to this (De Jong, et. al., 2012).

11

P4 Explain the advantages and disadvantages of different types of planning

tools used in the budgetary control.

In Zylla, there are various changes which are taking place and therefore it is needed

that proper planning shall be done so that it will be possible to deal with all the

situations in a proper manner. Also, the expenses which will be incurred in that

process will be kept under control and this will be beneficial for the company ( De

Jong, et. al., 2012). Budgets are to be made in this situation which is of various

categories such as the financial or capital budget.

Merits of budgets:

The cost which company is required to spend will be identified and by that, it

will be possible to keep a check on them so that they can be controlled.

In various changes, it will be needed that proper process is undertaken so that

risk of errors is reduced and this will be possible with the help of budgets.

All the deviations which will be occurring will be determined and then they will

be taken into consideration in the business with the use of the budget as they

are included in making of it (De Jong, et. al., 2012).

Demerits of budgets:

The figures which are included in the budget are taken on the basis of

projections that are made and so there will be a certain risk which is involved

in this process.

The data which will be required is collected with the use of research and that

requires more time and cost which makes it expensive process and it cannot

be used by all due to this (De Jong, et. al., 2012).

11

Different types of budgets:

Incremental budgeting: The budget shall be such in which the increase which will

have to be made in expenses due to inflation will be taken into account and all the

values which will be included will be taken by making some addition in them. By this,

the problem of shortage will not be faced at the time of change (Egbide, and Agbude,

2014).

Master budget: All the departments will not be required to make separate budgets

and information in respect of all will be mentioned in the same budget. This reduces

the work of manager as all the data will be available in the same place. Saving of

time will also be possible with the help of this (Egbide, and Agbude, 2014).

Zero-based budgeting: In this type of budget all the values will be taken by making

the new findings. In this there will be the incorporation of all the new data and no

previous year’s information will be taken into account (Egbide and Agbude, 2014).

Due to the fact that it is started from the initial point, it is known as zero-based

budgeting in which there is no earlier base.

M3 Analyse the use of different planning tools and their application for

preparing and forecasting budgets.

It is required that the budgets shall be made in the proper manner and for that, it is

needed that all of the facts by which there will be the impact on the business shall be

taken into consideration under this. There will be the use of various tools so that this

can be made possible. The cost will be identified by the use of such strategy which

will provide accurate results and one of the techniques for this is activity-based

costing. Variance analysis is another tool which will be used in order to evaluate the

old budget by which deviations will be calculated and taken into account in the

making of the current budget. SWOT will also be used so that all the aspects of the

business are included (Ghanbari and Vaseli, 2015). In addition to all this, there are

certain factors which are external and for that proper analysis shall be made and this

will be carried with the use of Porter’s five forces or pestle analysis.

12

Incremental budgets

Master budgets

Zero based budgets

Incremental budgeting: The budget shall be such in which the increase which will

have to be made in expenses due to inflation will be taken into account and all the

values which will be included will be taken by making some addition in them. By this,

the problem of shortage will not be faced at the time of change (Egbide, and Agbude,

2014).

Master budget: All the departments will not be required to make separate budgets

and information in respect of all will be mentioned in the same budget. This reduces

the work of manager as all the data will be available in the same place. Saving of

time will also be possible with the help of this (Egbide, and Agbude, 2014).

Zero-based budgeting: In this type of budget all the values will be taken by making

the new findings. In this there will be the incorporation of all the new data and no

previous year’s information will be taken into account (Egbide and Agbude, 2014).

Due to the fact that it is started from the initial point, it is known as zero-based

budgeting in which there is no earlier base.

M3 Analyse the use of different planning tools and their application for

preparing and forecasting budgets.

It is required that the budgets shall be made in the proper manner and for that, it is

needed that all of the facts by which there will be the impact on the business shall be

taken into consideration under this. There will be the use of various tools so that this

can be made possible. The cost will be identified by the use of such strategy which

will provide accurate results and one of the techniques for this is activity-based

costing. Variance analysis is another tool which will be used in order to evaluate the

old budget by which deviations will be calculated and taken into account in the

making of the current budget. SWOT will also be used so that all the aspects of the

business are included (Ghanbari and Vaseli, 2015). In addition to all this, there are

certain factors which are external and for that proper analysis shall be made and this

will be carried with the use of Porter’s five forces or pestle analysis.

12

Incremental budgets

Master budgets

Zero based budgets

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.