MA_A2.1: Use of Planning Tools & Management Accounting Response

VerifiedAdded on 2021/10/04

|18

|4208

|386

Homework Assignment

AI Summary

This report analyzes the use of planning tools and management accounting techniques to address financial problems, focusing on Coffeegreen Ltd. The assignment is divided into two parts: the first part examines the strengths and weaknesses of planning tools like standard costing, standard prices, budgets, and balanced scorecards, including cost calculations and revenue maximization strategies. The second part focuses on ethical considerations and proposes methods for dealing with financial problems in both Coffeegreen Ltd. and Galaxy Hotel. The report includes SWOT, PEST, and balanced scorecard analyses to assess the company's performance and strategic position, along with detailed monthly budgets and an examination of budget variances. The student provides insights into how these tools can be used to improve financial performance and decision-making.

MA_A2.1: Use of planning tools and management accounting to respond to

financial problems techniques

(Assessment 2 of 2, Individual assignment)

Unit Assessors: Nguyen Thi Phuong Hoa/ Le Quang Dung

Student’s name: Nguyen Ngoc Quang

Student’s ID: 10200189

Table of Content

financial problems techniques

(Assessment 2 of 2, Individual assignment)

Unit Assessors: Nguyen Thi Phuong Hoa/ Le Quang Dung

Student’s name: Nguyen Ngoc Quang

Student’s ID: 10200189

Table of Content

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

I. INTRODUCTION........................................................................................................................3

II. PART A: SCENARIO 1:............................................................................................................4

1. Strengths and weaknesses of different planning tools.............................................................4

1.1. Standard cost.....................................................................................................................4

1.2. Standard prices..................................................................................................................5

1.3. Budgets.............................................................................................................................5

1.4. Balanced Scorecard..........................................................................................................6

2. Cost calculation.......................................................................................................................7

2.1. Task 2................................................................................................................................7

2.2. Task 3 :.............................................................................................................................7

2.3. Task 4................................................................................................................................9

3. SWOT, PEST and balanced scorecard analysis of Coffeegreen Ltd.....................................10

3.1. Balanced Scorecard........................................................................................................10

3.2 PEST....................................................................................................................................11

3.2.1. Political........................................................................................................................11

3.2.2. Economic.....................................................................................................................11

3.2.3. Social...........................................................................................................................12

3.2.4. Technology..................................................................................................................12

3.3 SWOT..................................................................................................................................13

III. Part B: SCENERIO 2...............................................................................................................14

1. Task 1.....................................................................................................................................14

1. A strong ethical sense................................................................................................................15

2. Task 2.....................................................................................................................................15

3. Task 3.....................................................................................................................................16

IV. CONCLUSION.......................................................................................................................17

VII. REFERENCE LIST...............................................................................................................18

II. PART A: SCENARIO 1:............................................................................................................4

1. Strengths and weaknesses of different planning tools.............................................................4

1.1. Standard cost.....................................................................................................................4

1.2. Standard prices..................................................................................................................5

1.3. Budgets.............................................................................................................................5

1.4. Balanced Scorecard..........................................................................................................6

2. Cost calculation.......................................................................................................................7

2.1. Task 2................................................................................................................................7

2.2. Task 3 :.............................................................................................................................7

2.3. Task 4................................................................................................................................9

3. SWOT, PEST and balanced scorecard analysis of Coffeegreen Ltd.....................................10

3.1. Balanced Scorecard........................................................................................................10

3.2 PEST....................................................................................................................................11

3.2.1. Political........................................................................................................................11

3.2.2. Economic.....................................................................................................................11

3.2.3. Social...........................................................................................................................12

3.2.4. Technology..................................................................................................................12

3.3 SWOT..................................................................................................................................13

III. Part B: SCENERIO 2...............................................................................................................14

1. Task 1.....................................................................................................................................14

1. A strong ethical sense................................................................................................................15

2. Task 2.....................................................................................................................................15

3. Task 3.....................................................................................................................................16

IV. CONCLUSION.......................................................................................................................17

VII. REFERENCE LIST...............................................................................................................18

I. INTRODUCTION

For the majority of accountants, a key role is giving the manager a clear picture consists of the

information gathered, processed, and interpreted. The organization might employ several

approaches and planning tools to finish the work. This report will be divided into 2 parts. The

first part is dedicated to the use of planning tools in management accounting of Coffeegreen Ltd

and the other part is about suggesting different methods for both Galaxy Hotel and Coffeegreen

Ltd to help them deal with financial problems

For the majority of accountants, a key role is giving the manager a clear picture consists of the

information gathered, processed, and interpreted. The organization might employ several

approaches and planning tools to finish the work. This report will be divided into 2 parts. The

first part is dedicated to the use of planning tools in management accounting of Coffeegreen Ltd

and the other part is about suggesting different methods for both Galaxy Hotel and Coffeegreen

Ltd to help them deal with financial problems

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

II. PART A: SCENARIO 1:

1. Strengths and weaknesses of different planning tools

1.1. Standard cost

Standard costing is a method of allocating costs to a product based on an analysis of the

resources used to create it and the related costs. This is a common method that has been used by

many suppliers to see the differences between the estimated cost of the products manufactured

and the cost of the estimated goods sold (Standard costing - What is standard costing? n.d.).

According to Mr. Kieso and his partners wrote in “Intermediate accounting” in 2019, there are

several advantages and disadvantages for this method,

Advantage:

- Firms could enhance their cost management by setting higher targets for the expanding

type of spending.

- Helps the firm to be able to calculate the cost of the product precisely to make better

preparations.

- Assist in simplifying the process of predicting inventories, which is easier compared to

actual costing systems.

- Manages to help managers keep the cost down to maximize the profit

Disadvantage:

- It is difficult for managers to calculate the cost precisely since it requires them to analyze

a lot of data to assess cost performance.

- Due to the enormous amount of date needed to do analysis, it can put more pressure on

workers, which can lead to the reduce in productivity

- If the firm does not update the statistics regularly while preparing financial statements,

the actual expenses may fluctuate.

1.2. Standard prices

Standard price is a pre-determined standardized pricing for a good or service based on its current

value, cost of replacement, or an assessment of its strategic significance in the industry

(BusinessDictionary.com, 2020).

1. Strengths and weaknesses of different planning tools

1.1. Standard cost

Standard costing is a method of allocating costs to a product based on an analysis of the

resources used to create it and the related costs. This is a common method that has been used by

many suppliers to see the differences between the estimated cost of the products manufactured

and the cost of the estimated goods sold (Standard costing - What is standard costing? n.d.).

According to Mr. Kieso and his partners wrote in “Intermediate accounting” in 2019, there are

several advantages and disadvantages for this method,

Advantage:

- Firms could enhance their cost management by setting higher targets for the expanding

type of spending.

- Helps the firm to be able to calculate the cost of the product precisely to make better

preparations.

- Assist in simplifying the process of predicting inventories, which is easier compared to

actual costing systems.

- Manages to help managers keep the cost down to maximize the profit

Disadvantage:

- It is difficult for managers to calculate the cost precisely since it requires them to analyze

a lot of data to assess cost performance.

- Due to the enormous amount of date needed to do analysis, it can put more pressure on

workers, which can lead to the reduce in productivity

- If the firm does not update the statistics regularly while preparing financial statements,

the actual expenses may fluctuate.

1.2. Standard prices

Standard price is a pre-determined standardized pricing for a good or service based on its current

value, cost of replacement, or an assessment of its strategic significance in the industry

(BusinessDictionary.com, 2020).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

According to Mr. Blocher and his partners wrote in “Cost management: A strategic emphasis” in

2010, there are several notiocable advantages and disadvantages about standard prices.

Advantage

- It can increase the firm’s revenue by decreasing the input costs

- Allowing the organization to make the selection of the perfectly suited provider

- Helping managers work more effietly by providing data about price-fixing

- Provide further information about generating an emergency reserve money.

Disadvantage

- Similar to one biggest drawback of standard cost, it takes a lot of time and effort from

employees to analyse precisely.

1.3. Budgets

Budgets are organized lists of predicted sales and expenditure that are focused on the probable

objectives that the company expects to achieve. It is therefore a kind of management's wish-list,

which are prepared as a document to use as a template for the company's expected future year

expenditures based on the organization's objectives (My Accounting Course, 2019).

According to Mr. Drury wrote in “Management and cost accounting” in 1980, there are several

notiocable advantages and disadvantages about this planning tool.

Advantage

- With regards to the budget management in the implementation stage, the primary job is to

provide an outlet for resources and to produce business activities.

- Itoisousedoasoanoinnovativeostrategyothatoletsofirmsocontrolocapitaloandoaccomplisho

targets.

Disadvantage

- The budget cannot support organizational strategies only if the financial strategy is

precise, accurate and practicable.

- It will be difficult for the firm to focus on its long-term goals if the managers don’t put

much effort into tracking, monitoring its present activities and operations.

2010, there are several notiocable advantages and disadvantages about standard prices.

Advantage

- It can increase the firm’s revenue by decreasing the input costs

- Allowing the organization to make the selection of the perfectly suited provider

- Helping managers work more effietly by providing data about price-fixing

- Provide further information about generating an emergency reserve money.

Disadvantage

- Similar to one biggest drawback of standard cost, it takes a lot of time and effort from

employees to analyse precisely.

1.3. Budgets

Budgets are organized lists of predicted sales and expenditure that are focused on the probable

objectives that the company expects to achieve. It is therefore a kind of management's wish-list,

which are prepared as a document to use as a template for the company's expected future year

expenditures based on the organization's objectives (My Accounting Course, 2019).

According to Mr. Drury wrote in “Management and cost accounting” in 1980, there are several

notiocable advantages and disadvantages about this planning tool.

Advantage

- With regards to the budget management in the implementation stage, the primary job is to

provide an outlet for resources and to produce business activities.

- Itoisousedoasoanoinnovativeostrategyothatoletsofirmsocontrolocapitaloandoaccomplisho

targets.

Disadvantage

- The budget cannot support organizational strategies only if the financial strategy is

precise, accurate and practicable.

- It will be difficult for the firm to focus on its long-term goals if the managers don’t put

much effort into tracking, monitoring its present activities and operations.

1.4. Balanced Scorecard

A phrase known as balanced scorecard (BSC) denotes a management strategy that is utilized to

identify and advance various business operations while also measuring and optimizing various

company outcomes and effects on external businesses (Tarver, 2020).

According to Mr. Ayres’s article “4 Pros and Cons of Balanced Scorecard”, there are several

notiocable advantages and disadvantages about this planning tool.

Advantage:

- Creating a specific illustration that offers companies the opportunity to succinctly convey

their strategies both within and outside their organizations.

- Creating a collaborative working environment for the employees from different divisions

within the company.

- Offer a clear strategy foundation and communication system

- Help the firm’s customers and shareholders have more insight knowledge about the

organization.

Disadvantage:

- The company-wide action plan focus mainly on the overall performance of the business,

and it will not focus on personal achievement or work satisfaction.

- Collaboration across several divisions is required, which is further compounded by

integration with other programs, such as KPI (key performance indicator) tracking.

2. Cost calculation

2.1. Task 2

The standard cost of 1kg of processed coffee :

Direct material + Direct Labour + Overhead

= 1.4 x 2 + 0.6 x 5 + 100% x (0.6 x 5)

= 8.8 ($)

The cost of contract No. 348 :

- Overhead Allocate :

Overhead Rate (150%) x Quantity ( 24000 x 0.6 ) = 21600 ( < 70000)

A phrase known as balanced scorecard (BSC) denotes a management strategy that is utilized to

identify and advance various business operations while also measuring and optimizing various

company outcomes and effects on external businesses (Tarver, 2020).

According to Mr. Ayres’s article “4 Pros and Cons of Balanced Scorecard”, there are several

notiocable advantages and disadvantages about this planning tool.

Advantage:

- Creating a specific illustration that offers companies the opportunity to succinctly convey

their strategies both within and outside their organizations.

- Creating a collaborative working environment for the employees from different divisions

within the company.

- Offer a clear strategy foundation and communication system

- Help the firm’s customers and shareholders have more insight knowledge about the

organization.

Disadvantage:

- The company-wide action plan focus mainly on the overall performance of the business,

and it will not focus on personal achievement or work satisfaction.

- Collaboration across several divisions is required, which is further compounded by

integration with other programs, such as KPI (key performance indicator) tracking.

2. Cost calculation

2.1. Task 2

The standard cost of 1kg of processed coffee :

Direct material + Direct Labour + Overhead

= 1.4 x 2 + 0.6 x 5 + 100% x (0.6 x 5)

= 8.8 ($)

The cost of contract No. 348 :

- Overhead Allocate :

Overhead Rate (150%) x Quantity ( 24000 x 0.6 ) = 21600 ( < 70000)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

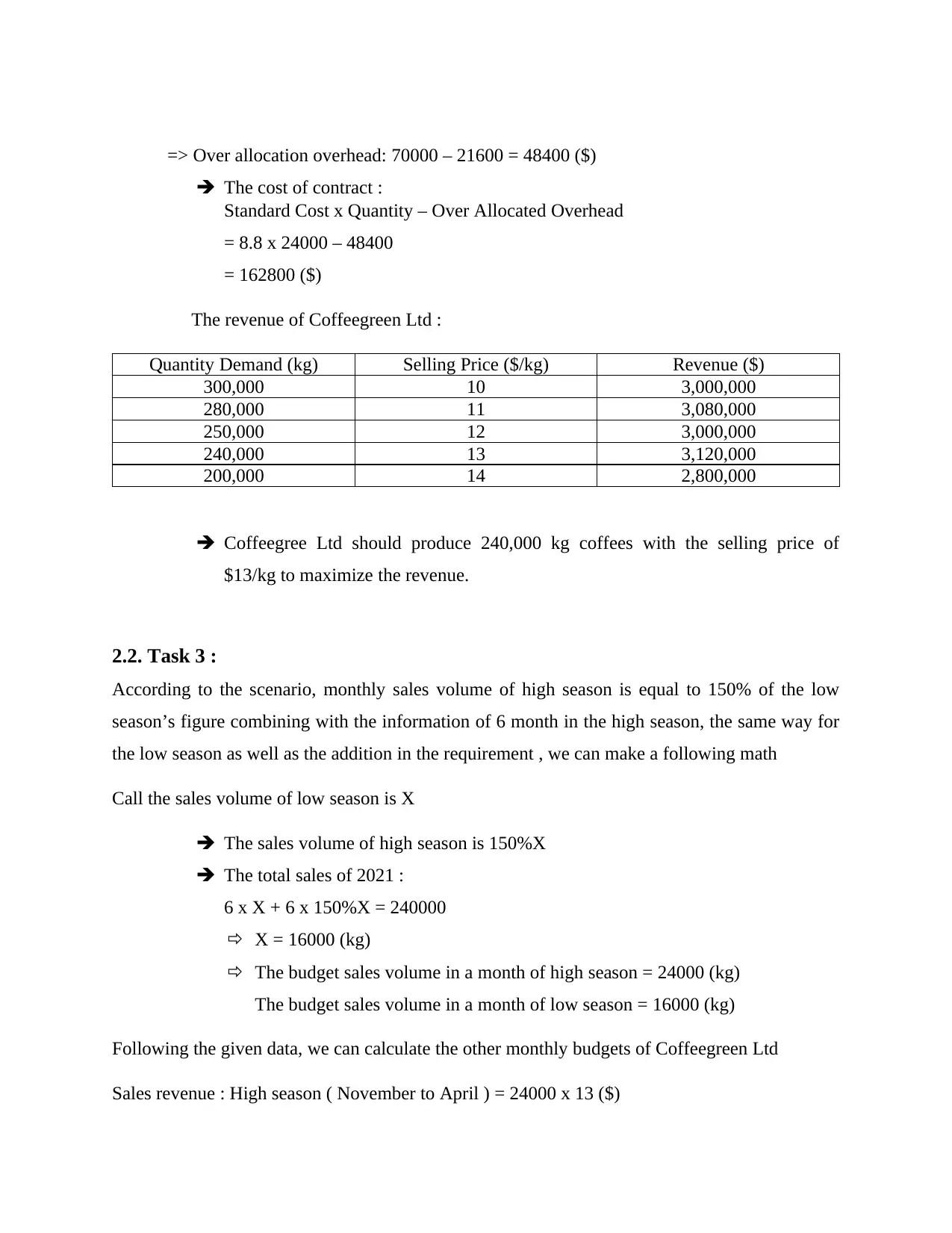

=> Over allocation overhead: 70000 – 21600 = 48400 ($)

The cost of contract :

Standard Cost x Quantity – Over Allocated Overhead

= 8.8 x 24000 – 48400

= 162800 ($)

The revenue of Coffeegreen Ltd :

Quantity Demand (kg) Selling Price ($/kg) Revenue ($)

300,000 10 3,000,000

280,000 11 3,080,000

250,000 12 3,000,000

240,000 13 3,120,000

200,000 14 2,800,000

Coffeegree Ltd should produce 240,000 kg coffees with the selling price of

$13/kg to maximize the revenue.

2.2. Task 3 :

According to the scenario, monthly sales volume of high season is equal to 150% of the low

season’s figure combining with the information of 6 month in the high season, the same way for

the low season as well as the addition in the requirement , we can make a following math

Call the sales volume of low season is X

The sales volume of high season is 150%X

The total sales of 2021 :

6 x X + 6 x 150%X = 240000

X = 16000 (kg)

The budget sales volume in a month of high season = 24000 (kg)

The budget sales volume in a month of low season = 16000 (kg)

Following the given data, we can calculate the other monthly budgets of Coffeegreen Ltd

Sales revenue : High season ( November to April ) = 24000 x 13 ($)

The cost of contract :

Standard Cost x Quantity – Over Allocated Overhead

= 8.8 x 24000 – 48400

= 162800 ($)

The revenue of Coffeegreen Ltd :

Quantity Demand (kg) Selling Price ($/kg) Revenue ($)

300,000 10 3,000,000

280,000 11 3,080,000

250,000 12 3,000,000

240,000 13 3,120,000

200,000 14 2,800,000

Coffeegree Ltd should produce 240,000 kg coffees with the selling price of

$13/kg to maximize the revenue.

2.2. Task 3 :

According to the scenario, monthly sales volume of high season is equal to 150% of the low

season’s figure combining with the information of 6 month in the high season, the same way for

the low season as well as the addition in the requirement , we can make a following math

Call the sales volume of low season is X

The sales volume of high season is 150%X

The total sales of 2021 :

6 x X + 6 x 150%X = 240000

X = 16000 (kg)

The budget sales volume in a month of high season = 24000 (kg)

The budget sales volume in a month of low season = 16000 (kg)

Following the given data, we can calculate the other monthly budgets of Coffeegreen Ltd

Sales revenue : High season ( November to April ) = 24000 x 13 ($)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

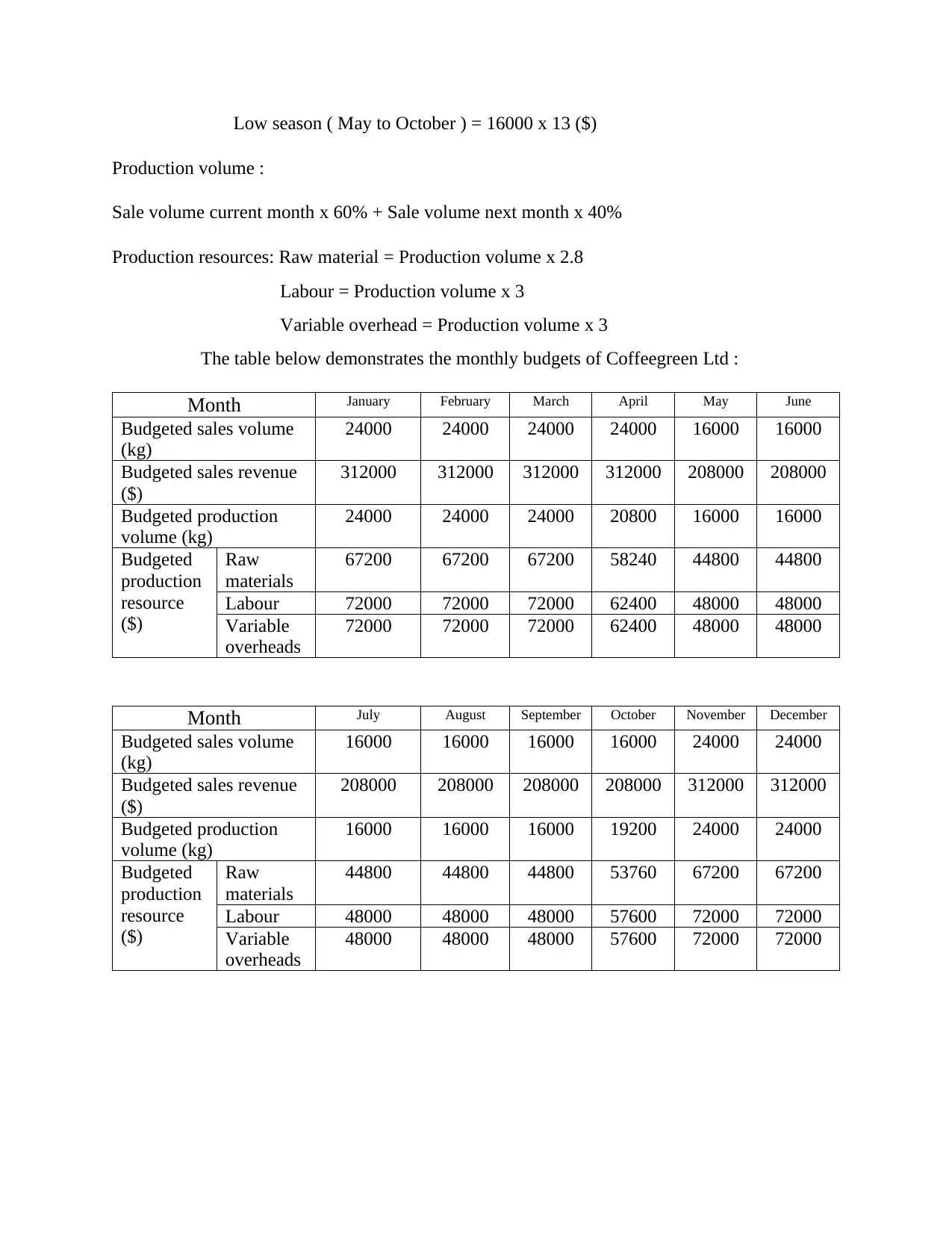

Low season ( May to October ) = 16000 x 13 ($)

Production volume :

Sale volume current month x 60% + Sale volume next month x 40%

Production resources: Raw material = Production volume x 2.8

Labour = Production volume x 3

Variable overhead = Production volume x 3

The table below demonstrates the monthly budgets of Coffeegreen Ltd :

Month January February March April May June

Budgeted sales volume

(kg)

24000 24000 24000 24000 16000 16000

Budgeted sales revenue

($)

312000 312000 312000 312000 208000 208000

Budgeted production

volume (kg)

24000 24000 24000 20800 16000 16000

Budgeted

production

resource

($)

Raw

materials

67200 67200 67200 58240 44800 44800

Labour 72000 72000 72000 62400 48000 48000

Variable

overheads

72000 72000 72000 62400 48000 48000

Month July August September October November December

Budgeted sales volume

(kg)

16000 16000 16000 16000 24000 24000

Budgeted sales revenue

($)

208000 208000 208000 208000 312000 312000

Budgeted production

volume (kg)

16000 16000 16000 19200 24000 24000

Budgeted

production

resource

($)

Raw

materials

44800 44800 44800 53760 67200 67200

Labour 48000 48000 48000 57600 72000 72000

Variable

overheads

48000 48000 48000 57600 72000 72000

Production volume :

Sale volume current month x 60% + Sale volume next month x 40%

Production resources: Raw material = Production volume x 2.8

Labour = Production volume x 3

Variable overhead = Production volume x 3

The table below demonstrates the monthly budgets of Coffeegreen Ltd :

Month January February March April May June

Budgeted sales volume

(kg)

24000 24000 24000 24000 16000 16000

Budgeted sales revenue

($)

312000 312000 312000 312000 208000 208000

Budgeted production

volume (kg)

24000 24000 24000 20800 16000 16000

Budgeted

production

resource

($)

Raw

materials

67200 67200 67200 58240 44800 44800

Labour 72000 72000 72000 62400 48000 48000

Variable

overheads

72000 72000 72000 62400 48000 48000

Month July August September October November December

Budgeted sales volume

(kg)

16000 16000 16000 16000 24000 24000

Budgeted sales revenue

($)

208000 208000 208000 208000 312000 312000

Budgeted production

volume (kg)

16000 16000 16000 19200 24000 24000

Budgeted

production

resource

($)

Raw

materials

44800 44800 44800 53760 67200 67200

Labour 48000 48000 48000 57600 72000 72000

Variable

overheads

48000 48000 48000 57600 72000 72000

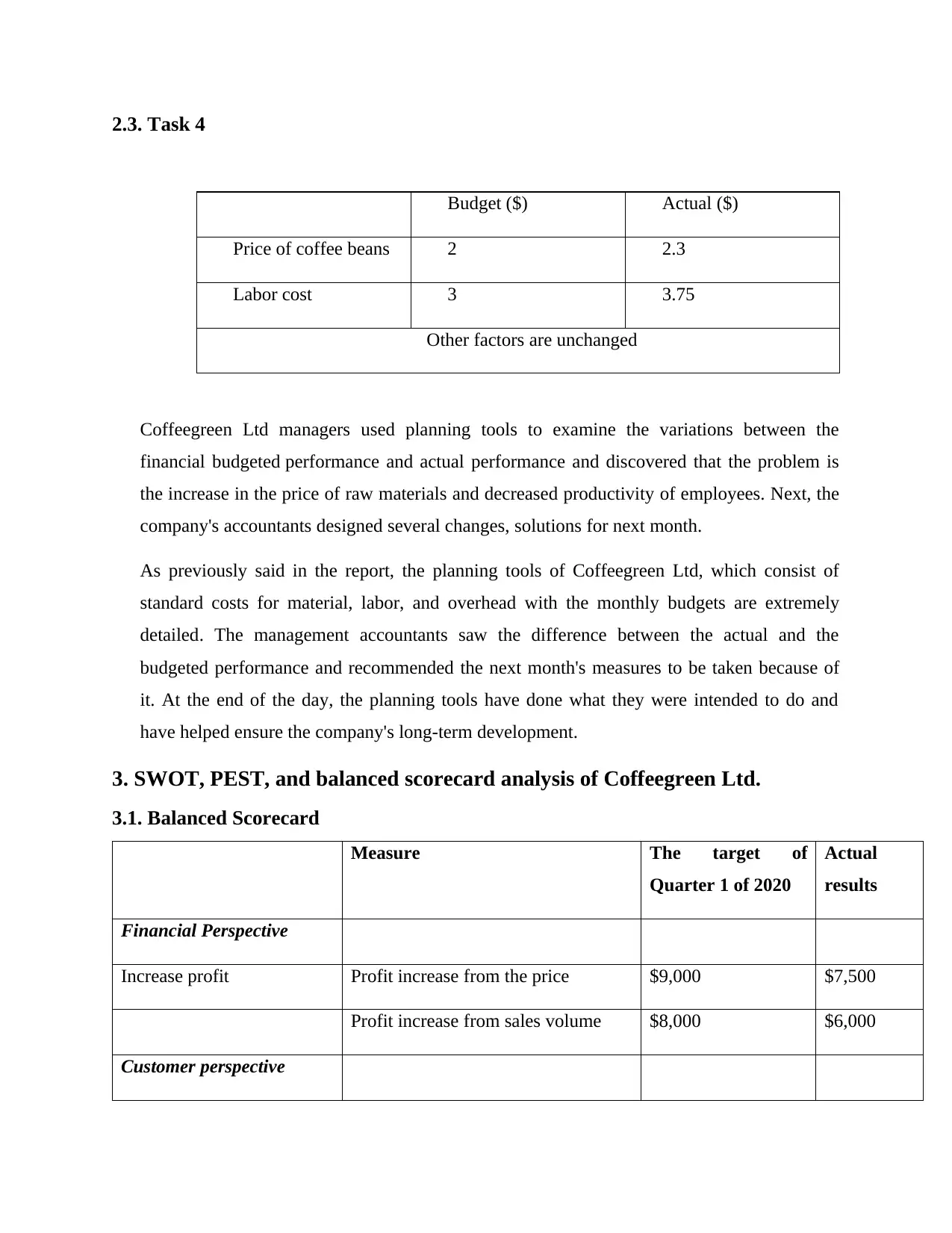

2.3. Task 4

Budget ($) Actual ($)

Price of coffee beans 2 2.3

Labor cost 3 3.75

Other factors are unchanged

Coffeegreen Ltd managers used planning tools to examine the variations between the

financial budgeted performance and actual performance and discovered that the problem is

the increase in the price of raw materials and decreased productivity of employees. Next, the

company's accountants designed several changes, solutions for next month.

As previously said in the report, the planning tools of Coffeegreen Ltd, which consist of

standard costs for material, labor, and overhead with the monthly budgets are extremely

detailed. The management accountants saw the difference between the actual and the

budgeted performance and recommended the next month's measures to be taken because of

it. At the end of the day, the planning tools have done what they were intended to do and

have helped ensure the company's long-term development.

3. SWOT, PEST, and balanced scorecard analysis of Coffeegreen Ltd.

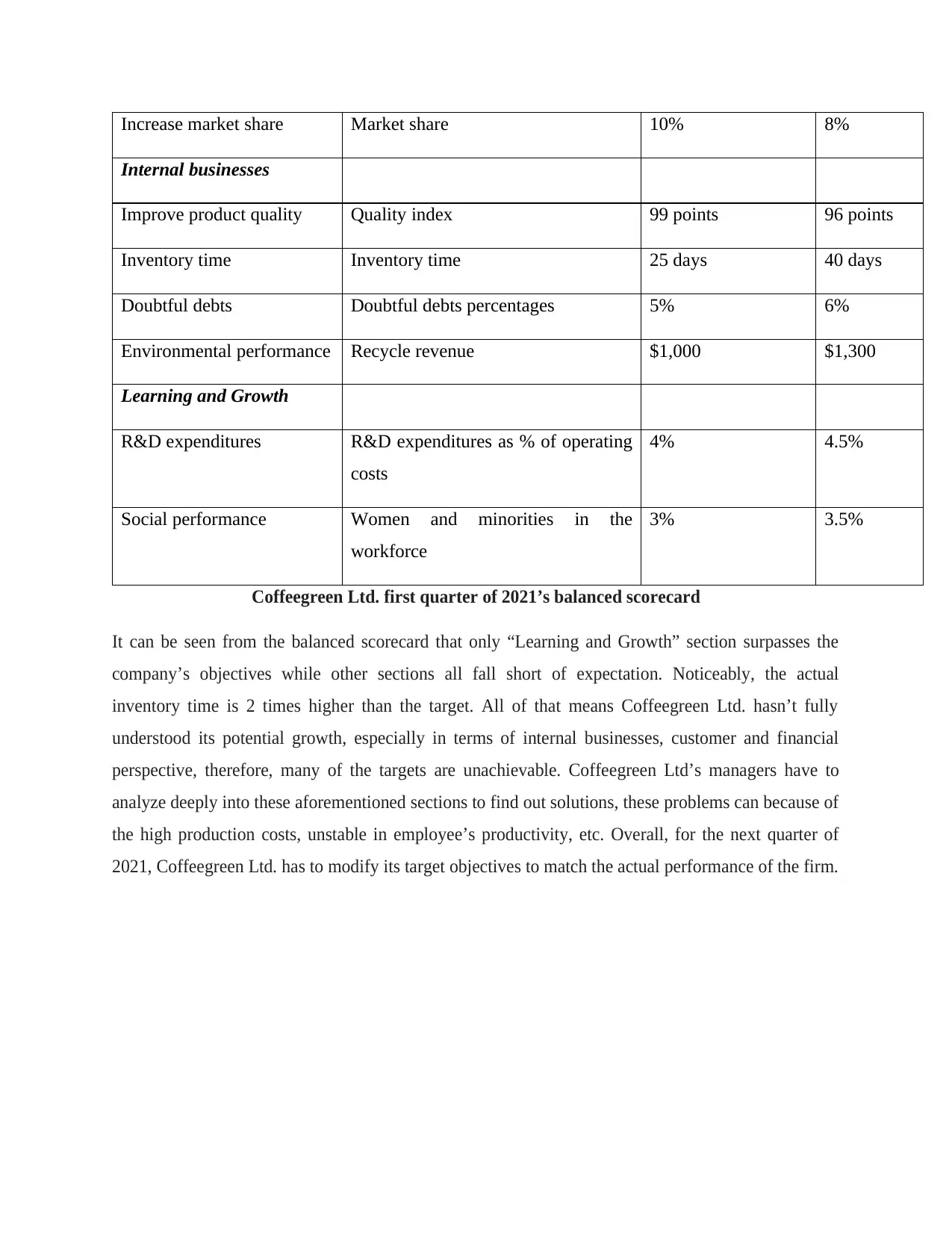

3.1. Balanced Scorecard

Measure The target of

Quarter 1 of 2020

Actual

results

Financial Perspective

Increase profit Profit increase from the price $9,000 $7,500

Profit increase from sales volume $8,000 $6,000

Customer perspective

Budget ($) Actual ($)

Price of coffee beans 2 2.3

Labor cost 3 3.75

Other factors are unchanged

Coffeegreen Ltd managers used planning tools to examine the variations between the

financial budgeted performance and actual performance and discovered that the problem is

the increase in the price of raw materials and decreased productivity of employees. Next, the

company's accountants designed several changes, solutions for next month.

As previously said in the report, the planning tools of Coffeegreen Ltd, which consist of

standard costs for material, labor, and overhead with the monthly budgets are extremely

detailed. The management accountants saw the difference between the actual and the

budgeted performance and recommended the next month's measures to be taken because of

it. At the end of the day, the planning tools have done what they were intended to do and

have helped ensure the company's long-term development.

3. SWOT, PEST, and balanced scorecard analysis of Coffeegreen Ltd.

3.1. Balanced Scorecard

Measure The target of

Quarter 1 of 2020

Actual

results

Financial Perspective

Increase profit Profit increase from the price $9,000 $7,500

Profit increase from sales volume $8,000 $6,000

Customer perspective

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Increase market share Market share 10% 8%

Internal businesses

Improve product quality Quality index 99 points 96 points

Inventory time Inventory time 25 days 40 days

Doubtful debts Doubtful debts percentages 5% 6%

Environmental performance Recycle revenue $1,000 $1,300

Learning and Growth

R&D expenditures R&D expenditures as % of operating

costs

4% 4.5%

Social performance Women and minorities in the

workforce

3% 3.5%

Coffeegreen Ltd. first quarter of 2021’s balanced scorecard

It can be seen from the balanced scorecard that only “Learning and Growth” section surpasses the

company’s objectives while other sections all fall short of expectation. Noticeably, the actual

inventory time is 2 times higher than the target. All of that means Coffeegreen Ltd. hasn’t fully

understood its potential growth, especially in terms of internal businesses, customer and financial

perspective, therefore, many of the targets are unachievable. Coffeegreen Ltd’s managers have to

analyze deeply into these aforementioned sections to find out solutions, these problems can because of

the high production costs, unstable in employee’s productivity, etc. Overall, for the next quarter of

2021, Coffeegreen Ltd. has to modify its target objectives to match the actual performance of the firm.

Internal businesses

Improve product quality Quality index 99 points 96 points

Inventory time Inventory time 25 days 40 days

Doubtful debts Doubtful debts percentages 5% 6%

Environmental performance Recycle revenue $1,000 $1,300

Learning and Growth

R&D expenditures R&D expenditures as % of operating

costs

4% 4.5%

Social performance Women and minorities in the

workforce

3% 3.5%

Coffeegreen Ltd. first quarter of 2021’s balanced scorecard

It can be seen from the balanced scorecard that only “Learning and Growth” section surpasses the

company’s objectives while other sections all fall short of expectation. Noticeably, the actual

inventory time is 2 times higher than the target. All of that means Coffeegreen Ltd. hasn’t fully

understood its potential growth, especially in terms of internal businesses, customer and financial

perspective, therefore, many of the targets are unachievable. Coffeegreen Ltd’s managers have to

analyze deeply into these aforementioned sections to find out solutions, these problems can because of

the high production costs, unstable in employee’s productivity, etc. Overall, for the next quarter of

2021, Coffeegreen Ltd. has to modify its target objectives to match the actual performance of the firm.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

3.2 PEST

3.2.1. Political

The decision toosignoCPTPPoandoEVFAoofoVietnameseogovernmento helps blurred the

foreign trade barriers, which makes it easier for a lot of Vietnamese businesses to expand the

market. As a result, there will be an increase in the number of new companies with big foreign

investment capital. In Coffeegreen Ltd.’s case, with the rapid growth trend in coffee production,

this seems to be a threat for the firm since there will be more new competitors with huge foreign

investment capitals. However, it’s sure that our government will try to support domestic

companies like Coffeegreen Ltd. in many ways such as promoting the slogan: “Vietnamese use

Vietnamese products”, applying Vietnam’s Law on Competition on these competitors, which

focuses on competition restraining agreements, market dominance, economic concentration, and

unfair practices (Das, 2019).

3.2.2. Economic

Due to the outbreak of Covid-19, the trading activities worldwide has been delayed, which poses

a great threat to not only our country’s economy but also every production company, included

Coffeegreen Ltd. However, thanks to many perceive methods and decisions from our

government, Vietnam is one of the best countries in the world in terms of coping with Covid-19.

Therefore, Vietnamese inflation in 2020 remained below 4% and the country’s growth rate was

2,2% (Lee, 2021)

According to the Ministry of Agriculture and RuraloDevelopment, Vietnam gained

approximately 2,7obillion $ by exporting 1,7omillion tons of coffee ino2020, which is incredible

since it accounted for over10% of global coffee value (VN to build upscale coffee brand, 2021)

3.2.3. Social

To be gain profit by exporting products to the foreign market, Coffeegreen Ltd must

ensure quality products meet the requirements of food safety and hygiene from many countries,

particularly from German, since German is the number one market for coffee exporting (Tran,

2020). As stated in the brief, the coffee produced by Coffeegreen Ltd is high-quality Arabica

coffee, which can attract the attention in the market easily since Arabica is the most favored

flavor in the world (Kalebjian, n.d.). While most Western countries are known for their attention

3.2.1. Political

The decision toosignoCPTPPoandoEVFAoofoVietnameseogovernmento helps blurred the

foreign trade barriers, which makes it easier for a lot of Vietnamese businesses to expand the

market. As a result, there will be an increase in the number of new companies with big foreign

investment capital. In Coffeegreen Ltd.’s case, with the rapid growth trend in coffee production,

this seems to be a threat for the firm since there will be more new competitors with huge foreign

investment capitals. However, it’s sure that our government will try to support domestic

companies like Coffeegreen Ltd. in many ways such as promoting the slogan: “Vietnamese use

Vietnamese products”, applying Vietnam’s Law on Competition on these competitors, which

focuses on competition restraining agreements, market dominance, economic concentration, and

unfair practices (Das, 2019).

3.2.2. Economic

Due to the outbreak of Covid-19, the trading activities worldwide has been delayed, which poses

a great threat to not only our country’s economy but also every production company, included

Coffeegreen Ltd. However, thanks to many perceive methods and decisions from our

government, Vietnam is one of the best countries in the world in terms of coping with Covid-19.

Therefore, Vietnamese inflation in 2020 remained below 4% and the country’s growth rate was

2,2% (Lee, 2021)

According to the Ministry of Agriculture and RuraloDevelopment, Vietnam gained

approximately 2,7obillion $ by exporting 1,7omillion tons of coffee ino2020, which is incredible

since it accounted for over10% of global coffee value (VN to build upscale coffee brand, 2021)

3.2.3. Social

To be gain profit by exporting products to the foreign market, Coffeegreen Ltd must

ensure quality products meet the requirements of food safety and hygiene from many countries,

particularly from German, since German is the number one market for coffee exporting (Tran,

2020). As stated in the brief, the coffee produced by Coffeegreen Ltd is high-quality Arabica

coffee, which can attract the attention in the market easily since Arabica is the most favored

flavor in the world (Kalebjian, n.d.). While most Western countries are known for their attention

to human rights, labor laws, animal rights, and environmental protection, other countries from

the rest of the world are still increasingly concerned with corruption, nepotism, privacy

violations, and economic inequity. Therefore, if companies from these countries want to gain

profit by exporting their products to the Western market, they have to follow those

aforementioned requirements. Luckily, as stated in the brief, Coffeegreen Ltd with

environmentally friendly technology, high social responsibility in maintaining women's rights

and recycling its wastes, Coffeegreen Ltd seems to advantages.

3.2.4. Technology

Due to the rapid development of technology, many industries will always have new challenges to

face and great achievements to reach, particularly in the coffee industry. The high-tech

equipment is provided by Coffeegreen Ltd.'s German partner, who helps them meet the food

safety and hygiene standards, as well as the requirement of advanced technology. Although the

new technology provided by the German partner gives the company a great competitive

advantage, the expenses are high when consider functioning and maintaining that technology,

which may cause the company to face some complicated problems.

3.3 SWOT

Strengths

+ Having advanced technology from German

partner

+ Abundant in coffee resources

+ Coffee is a consumable good with high and

stable demand in the market

+ Having environmental friendly technology,

high social responsibility in maintaining women

rights, and recycling

Weaknesses

+ Production cost is uncompetitive

+ Quality of workers is not secured

the rest of the world are still increasingly concerned with corruption, nepotism, privacy

violations, and economic inequity. Therefore, if companies from these countries want to gain

profit by exporting their products to the Western market, they have to follow those

aforementioned requirements. Luckily, as stated in the brief, Coffeegreen Ltd with

environmentally friendly technology, high social responsibility in maintaining women's rights

and recycling its wastes, Coffeegreen Ltd seems to advantages.

3.2.4. Technology

Due to the rapid development of technology, many industries will always have new challenges to

face and great achievements to reach, particularly in the coffee industry. The high-tech

equipment is provided by Coffeegreen Ltd.'s German partner, who helps them meet the food

safety and hygiene standards, as well as the requirement of advanced technology. Although the

new technology provided by the German partner gives the company a great competitive

advantage, the expenses are high when consider functioning and maintaining that technology,

which may cause the company to face some complicated problems.

3.3 SWOT

Strengths

+ Having advanced technology from German

partner

+ Abundant in coffee resources

+ Coffee is a consumable good with high and

stable demand in the market

+ Having environmental friendly technology,

high social responsibility in maintaining women

rights, and recycling

Weaknesses

+ Production cost is uncompetitive

+ Quality of workers is not secured

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.