Management Accounting: Analyzing Offers and Profitability

VerifiedAdded on 2019/09/20

|14

|2584

|265

Report

AI Summary

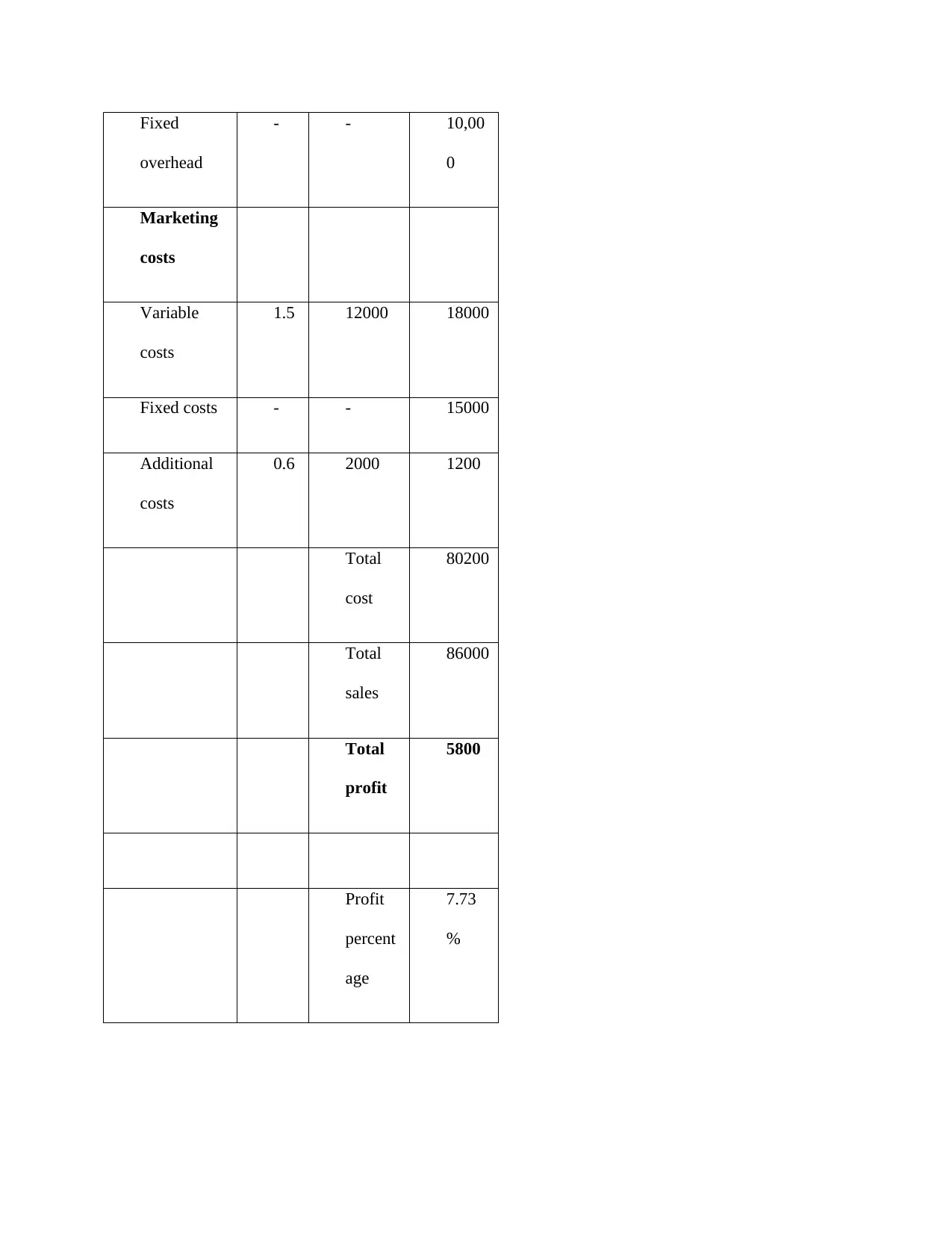

This report provides an introduction to management accounting, focusing on monthly profit calculations, factors for accepting orders, and evaluations of various offers. It analyzes the company's profitability, considering direct materials, labor, and overhead costs. The report explores scenarios involving additional sales, long-term government contracts, and offers from foreign markets and outside suppliers. It calculates break-even sales prices, discusses factors like brand image and synergy, and provides detailed cost and profit analyses for each scenario. The report concludes by emphasizing the importance of profit maximization and strategic decision-making in achieving the company's long-term goals, including outsourcing decisions and their impact on overall profitability.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.