Management Accounting Report: Unilever Financial Analysis Report

VerifiedAdded on 2020/01/07

|18

|5195

|177

Report

AI Summary

This report provides a comprehensive overview of management accounting, focusing on financial analysis and profitability. It explores key concepts such as absorption costing, marginal costing, and various management accounting techniques used to assess a company's financial health and make informed decisions. The report details the tools used in financial management, including financial statement analysis, cost accounting, fund flow analysis, and cash flow analysis. It further illustrates how to compute net profits using both absorption and marginal costing methods, providing practical examples. The report also addresses the importance of management accounting in achieving pre-set goals and objectives, particularly within a company like Unilever, and highlights the role of management accountants in risk identification and competitive advantage. Overall, the report offers valuable insights into financial performance, cost management, and strategic decision-making within an organization.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...............................................................................................................3

TASK.1................................................................................................................................3

P.1 .......................................................................................................................................3

P.2 ..............................................................................................................................5

TASK.2................................................................................................................................7

P.3 ..............................................................................................................................7

TASK 3..............................................................................................................................12

P.4 ............................................................................................................................12

P.5 ............................................................................................................................15

CONCLUSION..................................................................................................................16

REFERENCES..................................................................................................................17

INTRODUCTION...............................................................................................................3

TASK.1................................................................................................................................3

P.1 .......................................................................................................................................3

P.2 ..............................................................................................................................5

TASK.2................................................................................................................................7

P.3 ..............................................................................................................................7

TASK 3..............................................................................................................................12

P.4 ............................................................................................................................12

P.5 ............................................................................................................................15

CONCLUSION..................................................................................................................16

REFERENCES..................................................................................................................17

INTRODUCTION

Management accounting is a procedure through which company can report of

administration and financial statements which gives an entire explanation of the

company. All the material data that is essential for the shareholders which can influence

their decisions with respect to a business association are incorporated in the company's

financial statements. These days, it is fundamental to watch out all the data of the

business for sustainable advancement(Renz, 2016). Management Accounting is one the

most vital device by which organization would become acquainted with about the

organization's data and transform those information into sound decision making. A

qualified management accountant is the individual who make the organization to pick

cost leadership procedure in their business, so that an ever increasing number of results

can be allowed by the organization. With the help of management accounting, company

can easily makes an effective and efficient strategy that will also helps to make the

company to survive in the long run and also make the company to have the core

competence in the market.

TASK.1

P.1

Management accounting assist the firm to make the policies fro the attainment of

the pre set goals and objectives(Pipan and Czarniawska, 2010). Management accounting

deals in the inner management of the organization and also assist inner departments to

make the policy fro the effective run. With the help of management accounting,

company would able to make the company's operational process profitable. In the time of

modern era, each organization is deeply concerned in making the company more viable

and this could only be happened with the help of qualified management accountants.

Management accountants are the individuals who know how to run the company so that it

could generate the profits for the firm(Quinn, 2011). Management accountants assist the

the company to do research for the financial and non-financial data, so that the top level

authority can make the strategies or policies for the effective operations of the company.

Management accountants also helps to identify the risk within the organization and

Management accounting is a procedure through which company can report of

administration and financial statements which gives an entire explanation of the

company. All the material data that is essential for the shareholders which can influence

their decisions with respect to a business association are incorporated in the company's

financial statements. These days, it is fundamental to watch out all the data of the

business for sustainable advancement(Renz, 2016). Management Accounting is one the

most vital device by which organization would become acquainted with about the

organization's data and transform those information into sound decision making. A

qualified management accountant is the individual who make the organization to pick

cost leadership procedure in their business, so that an ever increasing number of results

can be allowed by the organization. With the help of management accounting, company

can easily makes an effective and efficient strategy that will also helps to make the

company to survive in the long run and also make the company to have the core

competence in the market.

TASK.1

P.1

Management accounting assist the firm to make the policies fro the attainment of

the pre set goals and objectives(Pipan and Czarniawska, 2010). Management accounting

deals in the inner management of the organization and also assist inner departments to

make the policy fro the effective run. With the help of management accounting,

company would able to make the company's operational process profitable. In the time of

modern era, each organization is deeply concerned in making the company more viable

and this could only be happened with the help of qualified management accountants.

Management accountants are the individuals who know how to run the company so that it

could generate the profits for the firm(Quinn, 2011). Management accountants assist the

the company to do research for the financial and non-financial data, so that the top level

authority can make the strategies or policies for the effective operations of the company.

Management accountants also helps to identify the risk within the organization and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

makes effective policies to overcome those risks. Managerial accounting makes the

company so eligible so that the company can take the competitive advantage over the

competitors in the relevant market.

However, there are various kinds of management accounting techniques which

are required in the company (Nandan, 2010). Firms today face the issues of how to adjust

their techniques, plans of action, and practices to respond to social and natural difficulties

while making financial achievement and incentive for their shareholders.

The report proposes various ways management accountant can control their

associations towards economical business achievement:

Price optimization system: It is considered as more effective system of

accounting which is used by the company to determine the price which is

applicable for the customer on which they are agree to buy there products.

Costing accounting system: It is related with those costs which incurred during

production process. It is summarized with various costs such as normal,standard

and actual costing.

Inventory accounting system: It is associated with management and controlling

of stock of the company from getting wastage. There are various methods and

techniques which a managers uses in order to maintain the stocks. Some of them

are EOQ and ABC costing.

Job costing system: Under this system, each products are categories as individual

products rather than all products. It is based on timing of product which are

produce by the company during the time period.

There are various requirement which has been required for the different kinds of

management accounting. Some of them are mentioned below:

Traditional management accounting: through this accounting system company can

concentrates the cost by means of job order of techniques of of process costing. Unilever

plc can easily allocate the cost of the product which are linked to the direct labor, direct

material and other overheads which are related to the production of the goods.

Needs of traditional management accounting: job order costing methodology is applied in

the manufacturing sector(Macintosh and Quattrone, 2012).

company so eligible so that the company can take the competitive advantage over the

competitors in the relevant market.

However, there are various kinds of management accounting techniques which

are required in the company (Nandan, 2010). Firms today face the issues of how to adjust

their techniques, plans of action, and practices to respond to social and natural difficulties

while making financial achievement and incentive for their shareholders.

The report proposes various ways management accountant can control their

associations towards economical business achievement:

Price optimization system: It is considered as more effective system of

accounting which is used by the company to determine the price which is

applicable for the customer on which they are agree to buy there products.

Costing accounting system: It is related with those costs which incurred during

production process. It is summarized with various costs such as normal,standard

and actual costing.

Inventory accounting system: It is associated with management and controlling

of stock of the company from getting wastage. There are various methods and

techniques which a managers uses in order to maintain the stocks. Some of them

are EOQ and ABC costing.

Job costing system: Under this system, each products are categories as individual

products rather than all products. It is based on timing of product which are

produce by the company during the time period.

There are various requirement which has been required for the different kinds of

management accounting. Some of them are mentioned below:

Traditional management accounting: through this accounting system company can

concentrates the cost by means of job order of techniques of of process costing. Unilever

plc can easily allocate the cost of the product which are linked to the direct labor, direct

material and other overheads which are related to the production of the goods.

Needs of traditional management accounting: job order costing methodology is applied in

the manufacturing sector(Macintosh and Quattrone, 2012).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

This is the methodology by which company can easily trace the various kinds of

costs associated to the manufacturing of the goods. Along with this tool, company also

need to make the strategy so that the cost of the products can be minimized. On the other

way, process costing is the technique which is used to determine the cost of different

manufacturing processes.

Lean accounting: this is the new concept in management accounting. Lean

accounting technique emerged in the new this era. This accounting does not concentrates

to cost of the products only. But also it helps for framing the strategy for the business in

order to achieve the goals and long term objectives.

Requirement of lean accounting: with the help of lean accounting, unilever plc’s

management accountants can make the strategy for the cost reduction of the products. It

is evaluated that if all the employees have idea about the lean accounting then they could

understand how to bifurcate cost in different department in systematic manner. This type

of accounting information provides wide range of data to top management to make

strategic decisions. In addition to this, Leann accounting also make effective changes in

value chain activities of organizations which provides absorption of cost in different

working department of Unilever plc. Management of organizations use this information

to make strategic decisions and also provides wide range of information to auditors of

company to audit internal and external functions of organizations.

P.2

There are various tools to report the management accounting. These methods can be used

to make for the company’s future projects of the company. These tools are mentioned

here under:

Financial management is truly vital for Unilevr plc as getting ready for planning

factors. Primary target for any entity is profitability. They need to build their benefit by

diminishing cost and keeping up quality in their products and management. Financial

planning can be considered as an important device for the accomplishment of different

business targets. Arranging of different variables identified with fund through financials

can help partner of Unilever plc to settle on better decision making related with the

costs associated to the manufacturing of the goods. Along with this tool, company also

need to make the strategy so that the cost of the products can be minimized. On the other

way, process costing is the technique which is used to determine the cost of different

manufacturing processes.

Lean accounting: this is the new concept in management accounting. Lean

accounting technique emerged in the new this era. This accounting does not concentrates

to cost of the products only. But also it helps for framing the strategy for the business in

order to achieve the goals and long term objectives.

Requirement of lean accounting: with the help of lean accounting, unilever plc’s

management accountants can make the strategy for the cost reduction of the products. It

is evaluated that if all the employees have idea about the lean accounting then they could

understand how to bifurcate cost in different department in systematic manner. This type

of accounting information provides wide range of data to top management to make

strategic decisions. In addition to this, Leann accounting also make effective changes in

value chain activities of organizations which provides absorption of cost in different

working department of Unilever plc. Management of organizations use this information

to make strategic decisions and also provides wide range of information to auditors of

company to audit internal and external functions of organizations.

P.2

There are various tools to report the management accounting. These methods can be used

to make for the company’s future projects of the company. These tools are mentioned

here under:

Financial management is truly vital for Unilevr plc as getting ready for planning

factors. Primary target for any entity is profitability. They need to build their benefit by

diminishing cost and keeping up quality in their products and management. Financial

planning can be considered as an important device for the accomplishment of different

business targets. Arranging of different variables identified with fund through financials

can help partner of Unilever plc to settle on better decision making related with the

company. Then again management accounting can make the financial statements which

could fulfil the need of the firm.

Analysis of financial statements: There are a few financial statements which are

required to be frame by the Unilever plc. Unilever plc is required to make the income

statements, statement of changes in financial position. Such kind of financial statements

of the company display the mirror the financial position. Administration of Unilever plc

can analyze these announcements for various time frame with the goal that they can get

data about their current financial position via such analysis.

Cost Accounting: Cost accounting is a strategy through which association can

assign its cost and it can exhibit its cost figures according to the unit of item. Cost

accounting also helps the organization to understand the cost related issues and try to

solve them with the help of cost accountants within the firm (Lukka and Modell, 2010).

Cost accounting is basically is needed in the manufacturing firm and company also

makes the process related strategy for the reduction of the cost of goods with the help of

cost accountants. Through a superior cost allocation framework, Unilever plc and its

administration can execute better procedures which can help them in the cost decrease.

Fund Flow Analysis: fund flow analysis assist the company to understand the

movement of funds for the certain period. Management accountants also assess the fund

flow information with the past data and then compare them so that the effective and

efficient policies can frame.

Cash Flow Analysis: Cash flow analysis assist the company to know the entire

cash out flow and inflow information and on the basis of such information company

would able to make their plans and strategy(Jansen, 2011). Management of Unilever plc

can utilize cash flow analysis investigate the stream of cash during financial year.

movement of cash and its following can help an organization to utilize available funds in

the needy area. As a cash flow is isolated into three areas i.e. cash flow from working,

contributing and financing exercises. Therefore, investigation of cash flow helps the

company to provide the detailed information with the relevant information to know the

exact cash needed in the particular future projects.

could fulfil the need of the firm.

Analysis of financial statements: There are a few financial statements which are

required to be frame by the Unilever plc. Unilever plc is required to make the income

statements, statement of changes in financial position. Such kind of financial statements

of the company display the mirror the financial position. Administration of Unilever plc

can analyze these announcements for various time frame with the goal that they can get

data about their current financial position via such analysis.

Cost Accounting: Cost accounting is a strategy through which association can

assign its cost and it can exhibit its cost figures according to the unit of item. Cost

accounting also helps the organization to understand the cost related issues and try to

solve them with the help of cost accountants within the firm (Lukka and Modell, 2010).

Cost accounting is basically is needed in the manufacturing firm and company also

makes the process related strategy for the reduction of the cost of goods with the help of

cost accountants. Through a superior cost allocation framework, Unilever plc and its

administration can execute better procedures which can help them in the cost decrease.

Fund Flow Analysis: fund flow analysis assist the company to understand the

movement of funds for the certain period. Management accountants also assess the fund

flow information with the past data and then compare them so that the effective and

efficient policies can frame.

Cash Flow Analysis: Cash flow analysis assist the company to know the entire

cash out flow and inflow information and on the basis of such information company

would able to make their plans and strategy(Jansen, 2011). Management of Unilever plc

can utilize cash flow analysis investigate the stream of cash during financial year.

movement of cash and its following can help an organization to utilize available funds in

the needy area. As a cash flow is isolated into three areas i.e. cash flow from working,

contributing and financing exercises. Therefore, investigation of cash flow helps the

company to provide the detailed information with the relevant information to know the

exact cash needed in the particular future projects.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Budget report: It help the small scale business owners to determine their

company's performance and if the business is enough to manage there operations the

managers are analyses the performance of the company.

Accounts receivable aging: It is crucial tool used for managing cash flows for

the company that extend credit to its customers. It help to divide the customer balances

by how long they have been owned.

Inventory and manufacturing: By using the companies physical stocks can use

management accounting reports to make their process more effective.

Job costing report: It shows the expenses for a particular project. They mostly

matched with the projects estimation of the total revenues so that company can analyze

the jobs profitability.

TASK.2

P.3

There are so many ways by which company can compute the net profits.

Management accounting tools assist the company to calculate the net profits of the firm.

Via absorption costing and marginal costing, Unilever plc can calculate the net profits.

Absorption costing: it is the methodology which is used to extract the different costs

which are linked to the various manufacturing processes. Additionally, this methodology

also assist the company to assess the stock of a firm (Luft and Shields, 2010). Forecasting

is also the chief components of the association. Through this techniques entire

manufacturing expenses are ascertained when they actually occurred, budget expenses

could vary from the actual one. Via absorption costing, over and under absorption could

be treated accordingly.

Income Statement as per absorption costing :

Selling price £35

Unit costs

Direct materials £6

Direct Labour £5

company's performance and if the business is enough to manage there operations the

managers are analyses the performance of the company.

Accounts receivable aging: It is crucial tool used for managing cash flows for

the company that extend credit to its customers. It help to divide the customer balances

by how long they have been owned.

Inventory and manufacturing: By using the companies physical stocks can use

management accounting reports to make their process more effective.

Job costing report: It shows the expenses for a particular project. They mostly

matched with the projects estimation of the total revenues so that company can analyze

the jobs profitability.

TASK.2

P.3

There are so many ways by which company can compute the net profits.

Management accounting tools assist the company to calculate the net profits of the firm.

Via absorption costing and marginal costing, Unilever plc can calculate the net profits.

Absorption costing: it is the methodology which is used to extract the different costs

which are linked to the various manufacturing processes. Additionally, this methodology

also assist the company to assess the stock of a firm (Luft and Shields, 2010). Forecasting

is also the chief components of the association. Through this techniques entire

manufacturing expenses are ascertained when they actually occurred, budget expenses

could vary from the actual one. Via absorption costing, over and under absorption could

be treated accordingly.

Income Statement as per absorption costing :

Selling price £35

Unit costs

Direct materials £6

Direct Labour £5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

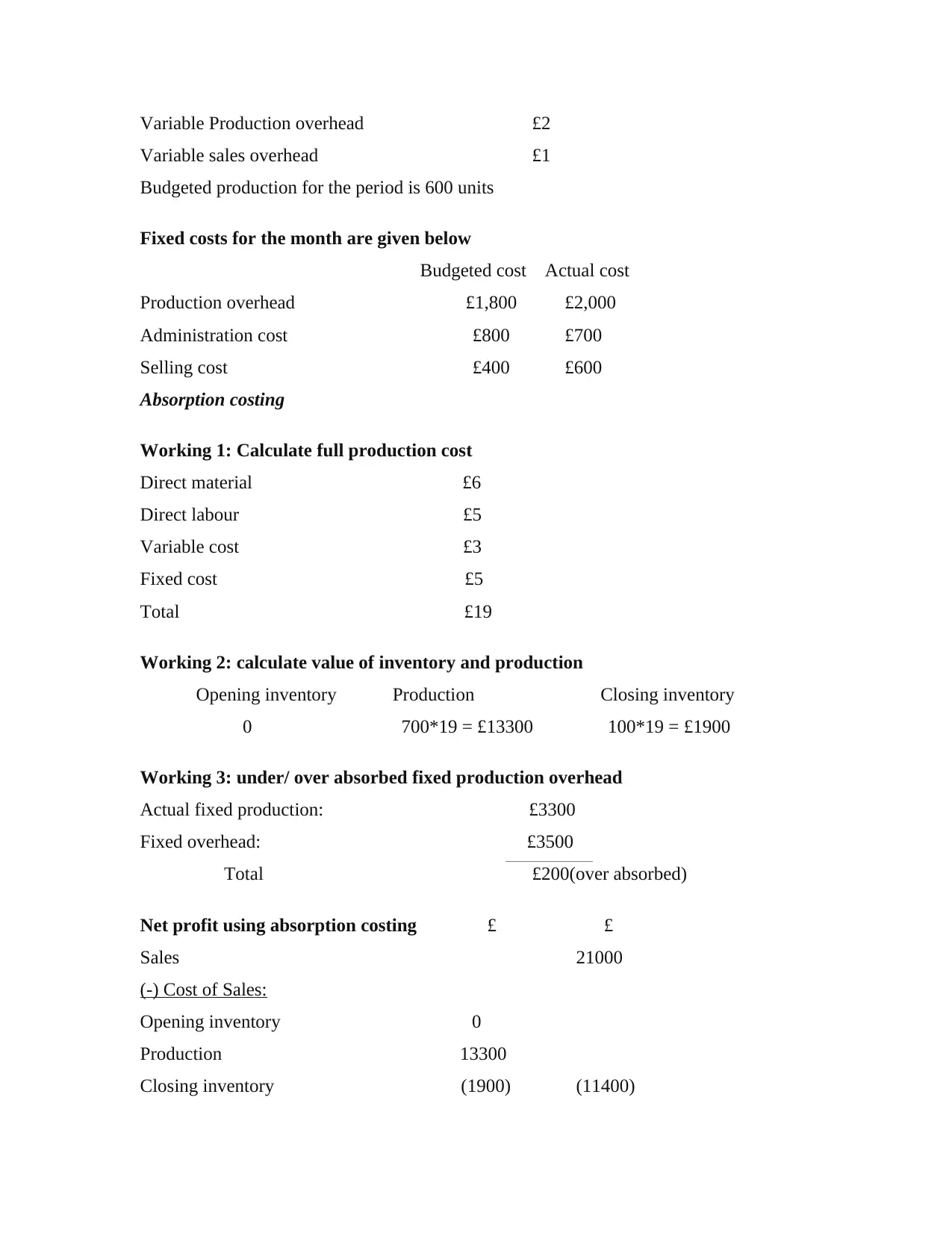

Variable Production overhead £2

Variable sales overhead £1

Budgeted production for the period is 600 units

Fixed costs for the month are given below

Budgeted cost Actual cost

Production overhead £1,800 £2,000

Administration cost £800 £700

Selling cost £400 £600

Absorption costing

Working 1: Calculate full production cost

Direct material £6

Direct labour £5

Variable cost £3

Fixed cost £5

Total £19

Working 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 700*19 = £13300 100*19 = £1900

Working 3: under/ over absorbed fixed production overhead

Actual fixed production: £3300

Fixed overhead: £3500

Total £200(over absorbed)

Net profit using absorption costing £ £

Sales 21000

(-) Cost of Sales:

Opening inventory 0

Production 13300

Closing inventory (1900) (11400)

Variable sales overhead £1

Budgeted production for the period is 600 units

Fixed costs for the month are given below

Budgeted cost Actual cost

Production overhead £1,800 £2,000

Administration cost £800 £700

Selling cost £400 £600

Absorption costing

Working 1: Calculate full production cost

Direct material £6

Direct labour £5

Variable cost £3

Fixed cost £5

Total £19

Working 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 700*19 = £13300 100*19 = £1900

Working 3: under/ over absorbed fixed production overhead

Actual fixed production: £3300

Fixed overhead: £3500

Total £200(over absorbed)

Net profit using absorption costing £ £

Sales 21000

(-) Cost of Sales:

Opening inventory 0

Production 13300

Closing inventory (1900) (11400)

(Under)/ Over absorbed fixed prod. O/h 200

Gross Profit 9800

Less Expenses

Variable sales 1800

Fixed administration 700

Fixed selling 600 (3100)

Net Profit 6700

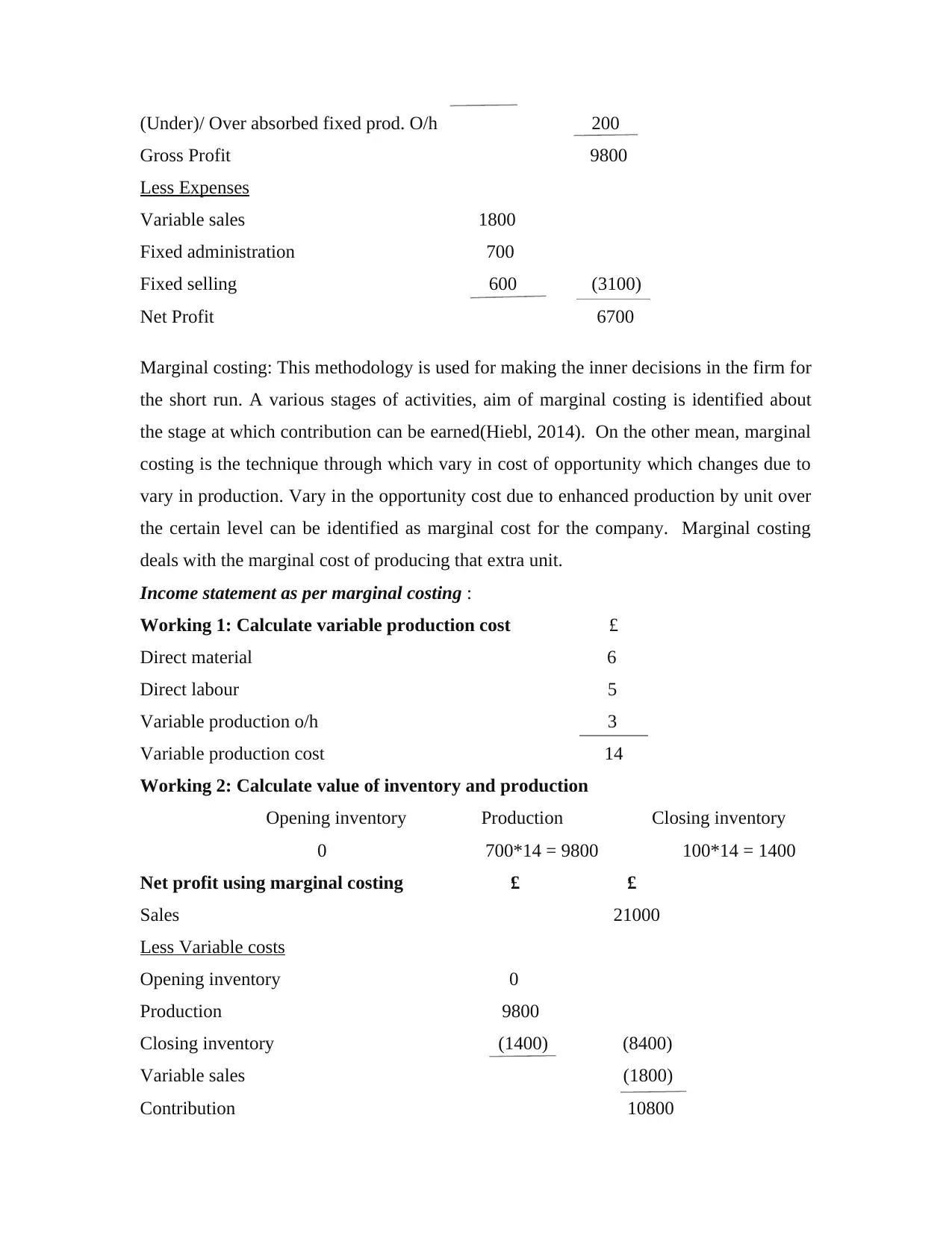

Marginal costing: This methodology is used for making the inner decisions in the firm for

the short run. A various stages of activities, aim of marginal costing is identified about

the stage at which contribution can be earned(Hiebl, 2014). On the other mean, marginal

costing is the technique through which vary in cost of opportunity which changes due to

vary in production. Vary in the opportunity cost due to enhanced production by unit over

the certain level can be identified as marginal cost for the company. Marginal costing

deals with the marginal cost of producing that extra unit.

Income statement as per marginal costing :

Working 1: Calculate variable production cost £

Direct material 6

Direct labour 5

Variable production o/h 3

Variable production cost 14

Working 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

0 700*14 = 9800 100*14 = 1400

Net profit using marginal costing £ £

Sales 21000

Less Variable costs

Opening inventory 0

Production 9800

Closing inventory (1400) (8400)

Variable sales (1800)

Contribution 10800

Gross Profit 9800

Less Expenses

Variable sales 1800

Fixed administration 700

Fixed selling 600 (3100)

Net Profit 6700

Marginal costing: This methodology is used for making the inner decisions in the firm for

the short run. A various stages of activities, aim of marginal costing is identified about

the stage at which contribution can be earned(Hiebl, 2014). On the other mean, marginal

costing is the technique through which vary in cost of opportunity which changes due to

vary in production. Vary in the opportunity cost due to enhanced production by unit over

the certain level can be identified as marginal cost for the company. Marginal costing

deals with the marginal cost of producing that extra unit.

Income statement as per marginal costing :

Working 1: Calculate variable production cost £

Direct material 6

Direct labour 5

Variable production o/h 3

Variable production cost 14

Working 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

0 700*14 = 9800 100*14 = 1400

Net profit using marginal costing £ £

Sales 21000

Less Variable costs

Opening inventory 0

Production 9800

Closing inventory (1400) (8400)

Variable sales (1800)

Contribution 10800

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

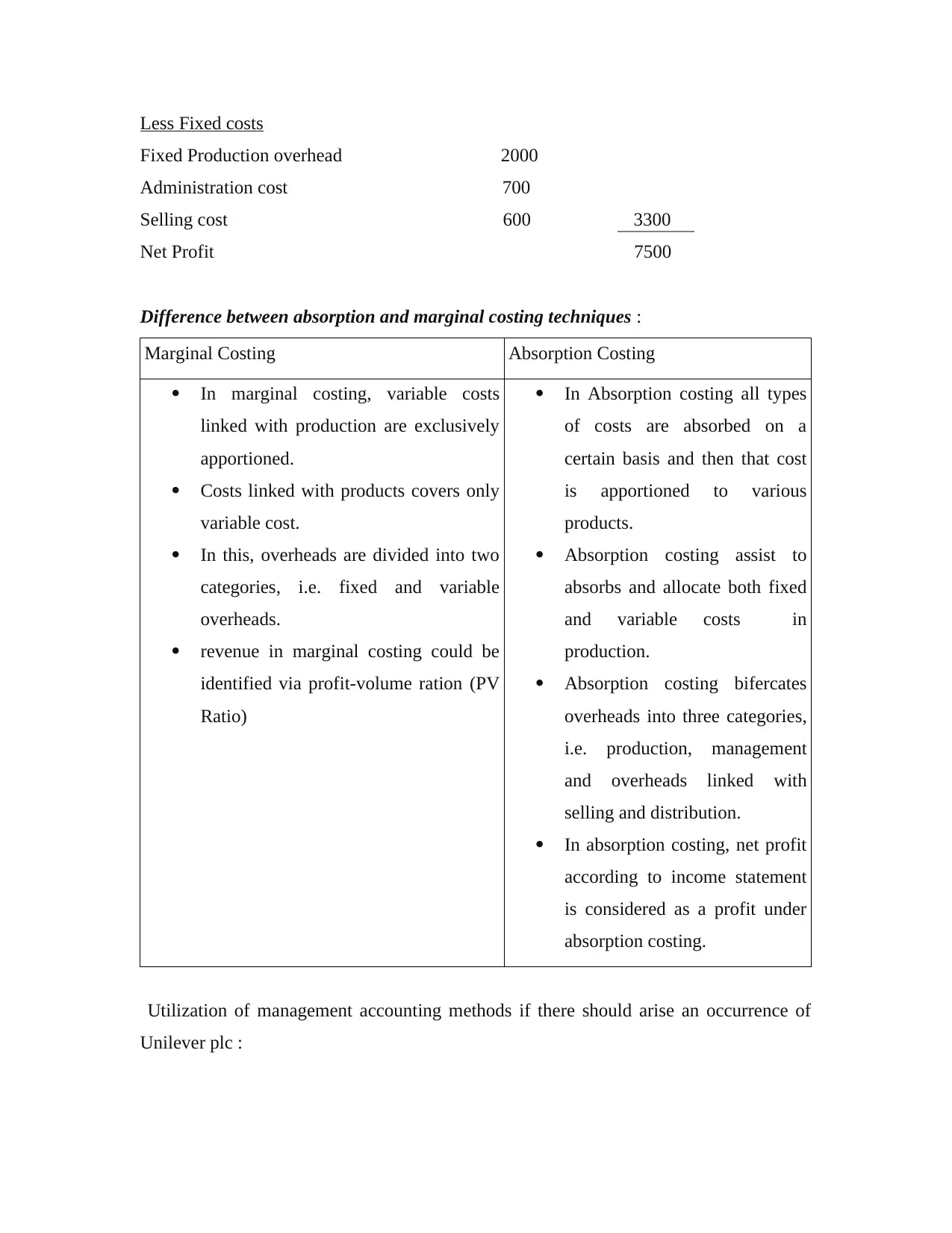

Less Fixed costs

Fixed Production overhead 2000

Administration cost 700

Selling cost 600 3300

Net Profit 7500

Difference between absorption and marginal costing techniques :

Marginal Costing Absorption Costing

In marginal costing, variable costs

linked with production are exclusively

apportioned.

Costs linked with products covers only

variable cost.

In this, overheads are divided into two

categories, i.e. fixed and variable

overheads.

revenue in marginal costing could be

identified via profit-volume ration (PV

Ratio)

In Absorption costing all types

of costs are absorbed on a

certain basis and then that cost

is apportioned to various

products.

Absorption costing assist to

absorbs and allocate both fixed

and variable costs in

production.

Absorption costing bifercates

overheads into three categories,

i.e. production, management

and overheads linked with

selling and distribution.

In absorption costing, net profit

according to income statement

is considered as a profit under

absorption costing.

Utilization of management accounting methods if there should arise an occurrence of

Unilever plc :

Fixed Production overhead 2000

Administration cost 700

Selling cost 600 3300

Net Profit 7500

Difference between absorption and marginal costing techniques :

Marginal Costing Absorption Costing

In marginal costing, variable costs

linked with production are exclusively

apportioned.

Costs linked with products covers only

variable cost.

In this, overheads are divided into two

categories, i.e. fixed and variable

overheads.

revenue in marginal costing could be

identified via profit-volume ration (PV

Ratio)

In Absorption costing all types

of costs are absorbed on a

certain basis and then that cost

is apportioned to various

products.

Absorption costing assist to

absorbs and allocate both fixed

and variable costs in

production.

Absorption costing bifercates

overheads into three categories,

i.e. production, management

and overheads linked with

selling and distribution.

In absorption costing, net profit

according to income statement

is considered as a profit under

absorption costing.

Utilization of management accounting methods if there should arise an occurrence of

Unilever plc :

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Unilever plc is a company which has so many employees in its hierarchical

structure. it can be seen that the income of the company is high when contrasted with

different organizations working in a similar segment and performing same operations.

Management accounting and its strategies are used in the firm for better operational

business. They organize with each other in helping management of the Unilever plc for

accomplishment of its destinations and goals. Presently business condition administrative

work forces needs to track for execution of Unilever plc so that they can follow that

business association and its improvement is going in the correct direction and also helps

to attaining the set targets(Herbert and Seal, 2012). There are a few procedures of

management accounting which can be utilized by administration of Unilever plc , these

methods are said beneath :

Cost Volume Profit Analysis(CVP Analysis): Cost volume profit analysis is a

strategy which is utilized by administration of association for deciding the effect of

change in cost of item and its volume on Unilever plc's working income and net income.

Company is required to create an assumption that selling price will stay consistent amid

course of business, assurance of CVP analysis relies on upon the way that cost of

manufacturing is settled amid a given time (Weißenberger and Angelkort, 2011). In given

period actual production overhead, selling cost and administration expense is more than

the planned cost, as aggregate budgeted total cost of these three component was £ 2600

however actual cost is £ 3300.On the other hand Budgeted selection of candidates

through Unilever plc was 600 competitors during a specific era yet the real populace of

enrollment was 700 applicants amid a specific period. Subsequently management

accountant can break down through cost volume profit analysis that how volume of

enlisted applicants impacts the total cost.

Absorption Costing : From the above income statement which is set up according

to strategy for absorption costing all out manufacturing cost per unit of Unilever plc was

£ 19 which incorporates £ 6 for direct material, £ 5 for direct work, £ 3 is for variable

cost and £ 5 reflects to fixed cost allocated on certain basis. As per absorption costing,

structure. it can be seen that the income of the company is high when contrasted with

different organizations working in a similar segment and performing same operations.

Management accounting and its strategies are used in the firm for better operational

business. They organize with each other in helping management of the Unilever plc for

accomplishment of its destinations and goals. Presently business condition administrative

work forces needs to track for execution of Unilever plc so that they can follow that

business association and its improvement is going in the correct direction and also helps

to attaining the set targets(Herbert and Seal, 2012). There are a few procedures of

management accounting which can be utilized by administration of Unilever plc , these

methods are said beneath :

Cost Volume Profit Analysis(CVP Analysis): Cost volume profit analysis is a

strategy which is utilized by administration of association for deciding the effect of

change in cost of item and its volume on Unilever plc's working income and net income.

Company is required to create an assumption that selling price will stay consistent amid

course of business, assurance of CVP analysis relies on upon the way that cost of

manufacturing is settled amid a given time (Weißenberger and Angelkort, 2011). In given

period actual production overhead, selling cost and administration expense is more than

the planned cost, as aggregate budgeted total cost of these three component was £ 2600

however actual cost is £ 3300.On the other hand Budgeted selection of candidates

through Unilever plc was 600 competitors during a specific era yet the real populace of

enrollment was 700 applicants amid a specific period. Subsequently management

accountant can break down through cost volume profit analysis that how volume of

enlisted applicants impacts the total cost.

Absorption Costing : From the above income statement which is set up according

to strategy for absorption costing all out manufacturing cost per unit of Unilever plc was

£ 19 which incorporates £ 6 for direct material, £ 5 for direct work, £ 3 is for variable

cost and £ 5 reflects to fixed cost allocated on certain basis. As per absorption costing,

company discovers under and over absorption so that the better cost management should

be possible by it

TASK 3

P.4

Budgetary control is the process through which cost control in the organization is

done for maximizing the profit. The process of budgetary control system helps the

management to take maximum use of their available resources by effectively allocating

them. Through budgetary control system the management gets the declaration of of the

policies of the organization therefore it also act as a means of communication between

the employees. This help in increasing coordination's among the different departments of

the organization. Through this system the adverse effects of the changes that take place

are minimized as budget is prepared after analyzing all the relevant factors(Ward, 2012).

There are different planning tools which can be used for sating the different budgets. One

is the cash budget. It is a forecast done on the receipts and cash disbursements. It breaks

down the cash flow of the organization into different time periods like weekly monthly or

yearly. It helps in maintaining control in the organization shows the present cash status of

the company which help in taking the investment decisions to the company.

After knowing the cash capacity long term decisions can be taken which may give

long term benefits to the organization(Fullerton, Kennedy and Widener, 2014). In this

capital expenditure and balance sheet budget is prepared. In this the budgets are related to

to the machinery, short and long term bonds etc. it gives the expected balance sheet that

what will be the balance sheet of the organization if the budget is followed properly. It

has its own disadvantage also which can not be avoided. Once the budget is prepared it is

followed very rigidly which effects the flexibility of the organization. Therefore there are

very few cases when the budget is revised.

Another planning tool is used in the operating budgets. In this planning is done

for making the budgets for sales expense project or the revenues. In this planning is done

be possible by it

TASK 3

P.4

Budgetary control is the process through which cost control in the organization is

done for maximizing the profit. The process of budgetary control system helps the

management to take maximum use of their available resources by effectively allocating

them. Through budgetary control system the management gets the declaration of of the

policies of the organization therefore it also act as a means of communication between

the employees. This help in increasing coordination's among the different departments of

the organization. Through this system the adverse effects of the changes that take place

are minimized as budget is prepared after analyzing all the relevant factors(Ward, 2012).

There are different planning tools which can be used for sating the different budgets. One

is the cash budget. It is a forecast done on the receipts and cash disbursements. It breaks

down the cash flow of the organization into different time periods like weekly monthly or

yearly. It helps in maintaining control in the organization shows the present cash status of

the company which help in taking the investment decisions to the company.

After knowing the cash capacity long term decisions can be taken which may give

long term benefits to the organization(Fullerton, Kennedy and Widener, 2014). In this

capital expenditure and balance sheet budget is prepared. In this the budgets are related to

to the machinery, short and long term bonds etc. it gives the expected balance sheet that

what will be the balance sheet of the organization if the budget is followed properly. It

has its own disadvantage also which can not be avoided. Once the budget is prepared it is

followed very rigidly which effects the flexibility of the organization. Therefore there are

very few cases when the budget is revised.

Another planning tool is used in the operating budgets. In this planning is done

for making the budgets for sales expense project or the revenues. In this planning is done

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.