HNBS 305 Management Accounting Project: Financial Analysis

VerifiedAdded on 2023/03/21

|12

|2447

|65

Project

AI Summary

This project delves into the core principles of management accounting, providing a comprehensive analysis of costing methods, budgeting techniques, and financial performance evaluation. The project begins with an examination of costing methods, including fixed and variable costs, historical and replacement costs, absorption costing, and marginal costing, with practical examples and calculations. It then explores various management accounting techniques and develops a financial report to interpret data for a business. The project further addresses budgetary control, comparing the advantages and disadvantages of forecasting, scenario, and contingency tools, alongside expense estimations and cash budget preparation. Finally, the project analyzes accounting systems for financial issue resolution, evaluates financial performance using ratios like ROCE and asset turnover, and suggests measures to improve the financial health of two companies, including an evaluation of planning tools used in management accounting.

Management Accounting

(Project 2)

(Project 2)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

1.1: Costing methods uses for evaluating net profit ..............................................................3

1.2: Various range of management accounting techniques....................................................4

1.3: Develop financial report that apply and interpret data for a business ............................5

TASK 2............................................................................................................................................5

2.1: Advantages and disadvantages of various types of planning tools used for budgetary

control.....................................................................................................................................5

2.2: Estimate the expenses for July and August.....................................................................7

2.3: Cash budget ....................................................................................................................7

TASK 3............................................................................................................................................8

3.1: Adoption of accounting system to deal with financial issues.........................................8

3.2: Analyse measures to improve financial performance of both company's.......................8

3.3: Evaluate planning tools use in management accounting.................................................9

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

1.1: Costing methods uses for evaluating net profit ..............................................................3

1.2: Various range of management accounting techniques....................................................4

1.3: Develop financial report that apply and interpret data for a business ............................5

TASK 2............................................................................................................................................5

2.1: Advantages and disadvantages of various types of planning tools used for budgetary

control.....................................................................................................................................5

2.2: Estimate the expenses for July and August.....................................................................7

2.3: Cash budget ....................................................................................................................7

TASK 3............................................................................................................................................8

3.1: Adoption of accounting system to deal with financial issues.........................................8

3.2: Analyse measures to improve financial performance of both company's.......................8

3.3: Evaluate planning tools use in management accounting.................................................9

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION

Management accounting is an essential aspect for every small or large business

organisation. This will assists in better understanding of accounting systems those are being

crucial in analysing positive outcomes for the company. The second part of this project is

focusing various costing methods those are helpful in determining accurate net profitability of an

organisation during the time. Some specific tolls and techniques which is use in planning tools to

control budgets. Understanding of different financial issues and effective measure to resolve

them are discuss under this project reports (Bennett and James, 2017).

TASK 1

1.1: Costing methods uses for evaluating net profit

In every business organisation, they need to make proper evaluation of total costs which

will be related with the production process. The costs are directly or indirectly associated with

the manufacturing of goods and services. This would simply said that the value of money render

for receiving something. This is use to formulate anything and that represent financial evaluation

of material, resources and risk factors or utilities those are associated with a product. The

different types of costs are discuss underneath:

Fixed and variable cost: This happens to be the utmost important costs which will be

applicable during the time of producing specific products. Variable cost are remain

changing with the production units, whereas fixed costs are unchanged whether

production is going on or stop. These two costs are having direct relationship with

production. Therefore, it kept increasing and decreasing with the level of output.

Historical and replacement cost: These are said to be sum total of capital which is paid

during the time of buying past and get consider as main base for financial accounts.

Likewise, a replacement costs is a present amount that is to be paid in current time for

replacing the assets (Galliers and Leidner, 2014).

Absorption costing: It refers as all those costs which is incur by the company on overall

production of products. This includes both variable and fixed costs because of which it is

known as full costing method. The type of costs carry under this costing is direct

material, labour and other overhead cost. Likewise, under this costs a portion of fixed

3

Management accounting is an essential aspect for every small or large business

organisation. This will assists in better understanding of accounting systems those are being

crucial in analysing positive outcomes for the company. The second part of this project is

focusing various costing methods those are helpful in determining accurate net profitability of an

organisation during the time. Some specific tolls and techniques which is use in planning tools to

control budgets. Understanding of different financial issues and effective measure to resolve

them are discuss under this project reports (Bennett and James, 2017).

TASK 1

1.1: Costing methods uses for evaluating net profit

In every business organisation, they need to make proper evaluation of total costs which

will be related with the production process. The costs are directly or indirectly associated with

the manufacturing of goods and services. This would simply said that the value of money render

for receiving something. This is use to formulate anything and that represent financial evaluation

of material, resources and risk factors or utilities those are associated with a product. The

different types of costs are discuss underneath:

Fixed and variable cost: This happens to be the utmost important costs which will be

applicable during the time of producing specific products. Variable cost are remain

changing with the production units, whereas fixed costs are unchanged whether

production is going on or stop. These two costs are having direct relationship with

production. Therefore, it kept increasing and decreasing with the level of output.

Historical and replacement cost: These are said to be sum total of capital which is paid

during the time of buying past and get consider as main base for financial accounts.

Likewise, a replacement costs is a present amount that is to be paid in current time for

replacing the assets (Galliers and Leidner, 2014).

Absorption costing: It refers as all those costs which is incur by the company on overall

production of products. This includes both variable and fixed costs because of which it is

known as full costing method. The type of costs carry under this costing is direct

material, labour and other overhead cost. Likewise, under this costs a portion of fixed

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

overhead cost is allocated to every units of products along with manufacturing variable

costs.

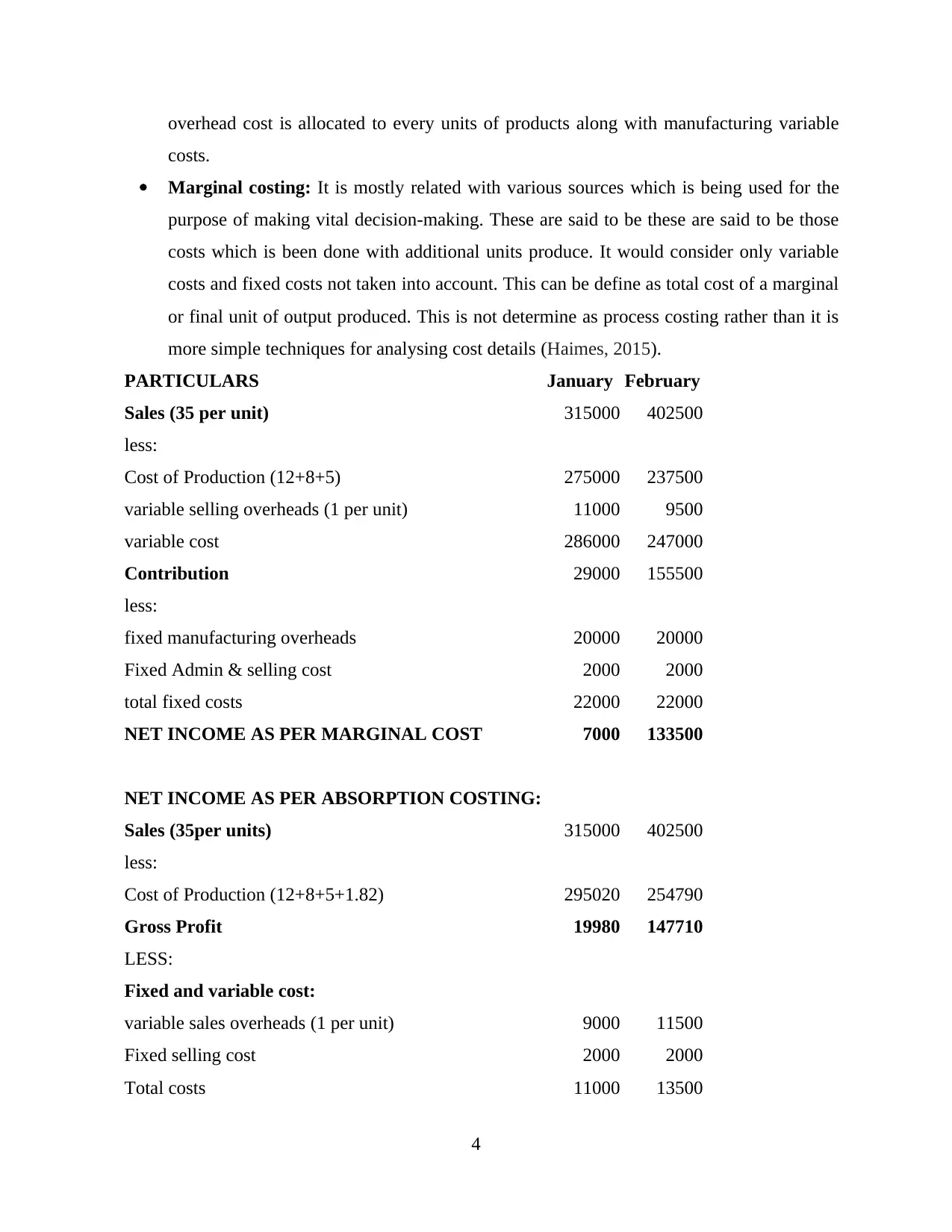

Marginal costing: It is mostly related with various sources which is being used for the

purpose of making vital decision-making. These are said to be these are said to be those

costs which is been done with additional units produce. It would consider only variable

costs and fixed costs not taken into account. This can be define as total cost of a marginal

or final unit of output produced. This is not determine as process costing rather than it is

more simple techniques for analysing cost details (Haimes, 2015).

PARTICULARS January February

Sales (35 per unit) 315000 402500

less:

Cost of Production (12+8+5) 275000 237500

variable selling overheads (1 per unit) 11000 9500

variable cost 286000 247000

Contribution 29000 155500

less:

fixed manufacturing overheads 20000 20000

Fixed Admin & selling cost 2000 2000

total fixed costs 22000 22000

NET INCOME AS PER MARGINAL COST 7000 133500

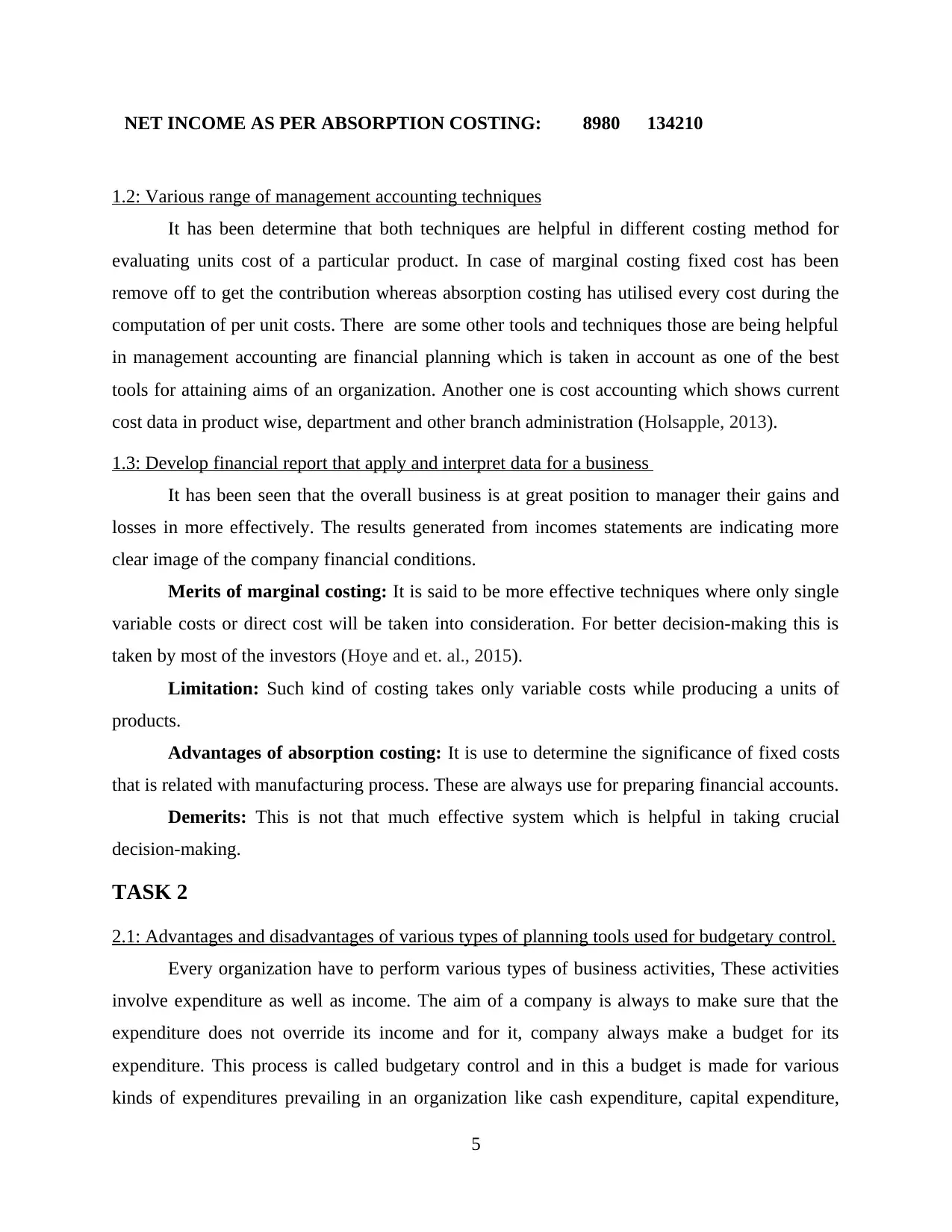

NET INCOME AS PER ABSORPTION COSTING:

Sales (35per units) 315000 402500

less:

Cost of Production (12+8+5+1.82) 295020 254790

Gross Profit 19980 147710

LESS:

Fixed and variable cost:

variable sales overheads (1 per unit) 9000 11500

Fixed selling cost 2000 2000

Total costs 11000 13500

4

costs.

Marginal costing: It is mostly related with various sources which is being used for the

purpose of making vital decision-making. These are said to be these are said to be those

costs which is been done with additional units produce. It would consider only variable

costs and fixed costs not taken into account. This can be define as total cost of a marginal

or final unit of output produced. This is not determine as process costing rather than it is

more simple techniques for analysing cost details (Haimes, 2015).

PARTICULARS January February

Sales (35 per unit) 315000 402500

less:

Cost of Production (12+8+5) 275000 237500

variable selling overheads (1 per unit) 11000 9500

variable cost 286000 247000

Contribution 29000 155500

less:

fixed manufacturing overheads 20000 20000

Fixed Admin & selling cost 2000 2000

total fixed costs 22000 22000

NET INCOME AS PER MARGINAL COST 7000 133500

NET INCOME AS PER ABSORPTION COSTING:

Sales (35per units) 315000 402500

less:

Cost of Production (12+8+5+1.82) 295020 254790

Gross Profit 19980 147710

LESS:

Fixed and variable cost:

variable sales overheads (1 per unit) 9000 11500

Fixed selling cost 2000 2000

Total costs 11000 13500

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

NET INCOME AS PER ABSORPTION COSTING: 8980 134210

1.2: Various range of management accounting techniques

It has been determine that both techniques are helpful in different costing method for

evaluating units cost of a particular product. In case of marginal costing fixed cost has been

remove off to get the contribution whereas absorption costing has utilised every cost during the

computation of per unit costs. There are some other tools and techniques those are being helpful

in management accounting are financial planning which is taken in account as one of the best

tools for attaining aims of an organization. Another one is cost accounting which shows current

cost data in product wise, department and other branch administration (Holsapple, 2013).

1.3: Develop financial report that apply and interpret data for a business

It has been seen that the overall business is at great position to manager their gains and

losses in more effectively. The results generated from incomes statements are indicating more

clear image of the company financial conditions.

Merits of marginal costing: It is said to be more effective techniques where only single

variable costs or direct cost will be taken into consideration. For better decision-making this is

taken by most of the investors (Hoye and et. al., 2015).

Limitation: Such kind of costing takes only variable costs while producing a units of

products.

Advantages of absorption costing: It is use to determine the significance of fixed costs

that is related with manufacturing process. These are always use for preparing financial accounts.

Demerits: This is not that much effective system which is helpful in taking crucial

decision-making.

TASK 2

2.1: Advantages and disadvantages of various types of planning tools used for budgetary control.

Every organization have to perform various types of business activities, These activities

involve expenditure as well as income. The aim of a company is always to make sure that the

expenditure does not override its income and for it, company always make a budget for its

expenditure. This process is called budgetary control and in this a budget is made for various

kinds of expenditures prevailing in an organization like cash expenditure, capital expenditure,

5

1.2: Various range of management accounting techniques

It has been determine that both techniques are helpful in different costing method for

evaluating units cost of a particular product. In case of marginal costing fixed cost has been

remove off to get the contribution whereas absorption costing has utilised every cost during the

computation of per unit costs. There are some other tools and techniques those are being helpful

in management accounting are financial planning which is taken in account as one of the best

tools for attaining aims of an organization. Another one is cost accounting which shows current

cost data in product wise, department and other branch administration (Holsapple, 2013).

1.3: Develop financial report that apply and interpret data for a business

It has been seen that the overall business is at great position to manager their gains and

losses in more effectively. The results generated from incomes statements are indicating more

clear image of the company financial conditions.

Merits of marginal costing: It is said to be more effective techniques where only single

variable costs or direct cost will be taken into consideration. For better decision-making this is

taken by most of the investors (Hoye and et. al., 2015).

Limitation: Such kind of costing takes only variable costs while producing a units of

products.

Advantages of absorption costing: It is use to determine the significance of fixed costs

that is related with manufacturing process. These are always use for preparing financial accounts.

Demerits: This is not that much effective system which is helpful in taking crucial

decision-making.

TASK 2

2.1: Advantages and disadvantages of various types of planning tools used for budgetary control.

Every organization have to perform various types of business activities, These activities

involve expenditure as well as income. The aim of a company is always to make sure that the

expenditure does not override its income and for it, company always make a budget for its

expenditure. This process is called budgetary control and in this a budget is made for various

kinds of expenditures prevailing in an organization like cash expenditure, capital expenditure,

5

revenue expenditure etc. A budget may also be prepared for sales, and other expenses. Proper

Budget makes it easy for companies to keep an eye on the workings of workforce and check

whether they are working in line with what is budgeted (Kanellou and Spathis, 2013). For the

purpose of making budget various tools are being frequently used by accountants, These tools

helps in estimation or forecasting of various expenses and incomes. These tools are described as

follows :

Forecasting Tools: Business forecasting helps in achieving efficiency in organizational

performance. A company who can accurately forecast its outcome in terms of sales and

profitability will be able to compete in markets in a better manner than their competitors. It is a

critical step for the purpose of creation of a business plan. Usually forecasting is not completely

accurate however it helps companies to have a macro view as what can happen in a given time

period.

Advantages : It helps in predicting future, it provides a sense of direction to company

where it can expect itself after a particular period. The demand of customers is not steady it is

keep on changing, but if it is properly forecasted before the company will be able to serve

customers well without any delay. It also save on staffing cost as the quality of goods to be

produced is already known (Kouvelis and Yu, 2013).

Disadvantages : Forecasting is based on estimation and therefore it cant be accurate all

the time. If decisions will be made based on a wrong forecast it may lead to disastrous outcomes

for companies. All forecasting tools usually are expensive and small and medium scale business

usually are unable to use the same because of financial constraints.

Scenario Tools : Scenario planning tries to focus on an outlook for future. It is a method

through which a company forms a idea of predictable future scenarios and how those scenarios

may affect strategic objectives framed by the company.

Advantages : Scenario planning is a strategic decision making tool, it is a process that

creates a number of possible future outcomes which are uncertain. With the help of scenario

planning, a manger can asses external environment well and this helps him to match internal

resources with it for the purpose of an optimal allocation of its scarce resources.

Disadvantages: Scenario planning is not always accurate and it is based on assumption.

It is quite costly to implement scenario planning. It is a cumbersome process, the time required

for scenario planning may range from 6 to 12 Months which is quite high.

6

Budget makes it easy for companies to keep an eye on the workings of workforce and check

whether they are working in line with what is budgeted (Kanellou and Spathis, 2013). For the

purpose of making budget various tools are being frequently used by accountants, These tools

helps in estimation or forecasting of various expenses and incomes. These tools are described as

follows :

Forecasting Tools: Business forecasting helps in achieving efficiency in organizational

performance. A company who can accurately forecast its outcome in terms of sales and

profitability will be able to compete in markets in a better manner than their competitors. It is a

critical step for the purpose of creation of a business plan. Usually forecasting is not completely

accurate however it helps companies to have a macro view as what can happen in a given time

period.

Advantages : It helps in predicting future, it provides a sense of direction to company

where it can expect itself after a particular period. The demand of customers is not steady it is

keep on changing, but if it is properly forecasted before the company will be able to serve

customers well without any delay. It also save on staffing cost as the quality of goods to be

produced is already known (Kouvelis and Yu, 2013).

Disadvantages : Forecasting is based on estimation and therefore it cant be accurate all

the time. If decisions will be made based on a wrong forecast it may lead to disastrous outcomes

for companies. All forecasting tools usually are expensive and small and medium scale business

usually are unable to use the same because of financial constraints.

Scenario Tools : Scenario planning tries to focus on an outlook for future. It is a method

through which a company forms a idea of predictable future scenarios and how those scenarios

may affect strategic objectives framed by the company.

Advantages : Scenario planning is a strategic decision making tool, it is a process that

creates a number of possible future outcomes which are uncertain. With the help of scenario

planning, a manger can asses external environment well and this helps him to match internal

resources with it for the purpose of an optimal allocation of its scarce resources.

Disadvantages: Scenario planning is not always accurate and it is based on assumption.

It is quite costly to implement scenario planning. It is a cumbersome process, the time required

for scenario planning may range from 6 to 12 Months which is quite high.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Contingencies Tools: A organization faces various Risks of uncertain events, These

events can be any external as well as internal contingencies like a fire occurred at factory, an

uncertain political outcome etc.

Advantages: With the help of proper contingency plans a company can operate the best

possible operations in an event of uncertainty. The responsibilities of staff are well assigned way

before in contingency planning and in an uncertain event they know their duties well and it saves

time and cost (Laudon and Laudon, 2016).

Disadvantages: It is a reactive model of business management. It means it does not plan

to lower the risk of a particular task or a project, it only solves problem if any contingencies

occurs in that task in future. Therefore, it can lead to a lack of skilled personnel to meet a

particular challenge of a project.

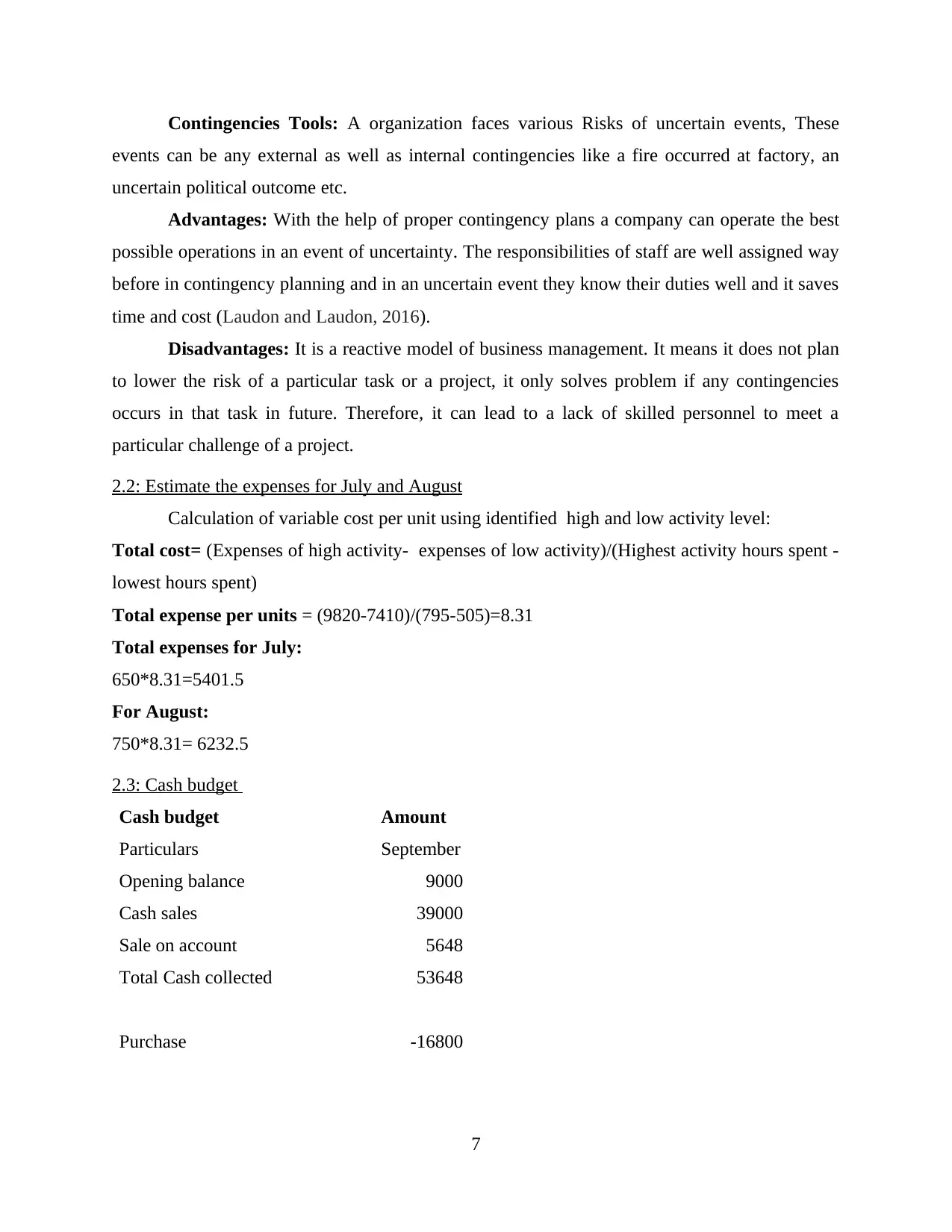

2.2: Estimate the expenses for July and August

Calculation of variable cost per unit using identified high and low activity level:

Total cost= (Expenses of high activity- expenses of low activity)/(Highest activity hours spent -

lowest hours spent)

Total expense per units = (9820-7410)/(795-505)=8.31

Total expenses for July:

650*8.31=5401.5

For August:

750*8.31= 6232.5

2.3: Cash budget

Cash budget Amount

Particulars September

Opening balance 9000

Cash sales 39000

Sale on account 5648

Total Cash collected 53648

Purchase -16800

7

events can be any external as well as internal contingencies like a fire occurred at factory, an

uncertain political outcome etc.

Advantages: With the help of proper contingency plans a company can operate the best

possible operations in an event of uncertainty. The responsibilities of staff are well assigned way

before in contingency planning and in an uncertain event they know their duties well and it saves

time and cost (Laudon and Laudon, 2016).

Disadvantages: It is a reactive model of business management. It means it does not plan

to lower the risk of a particular task or a project, it only solves problem if any contingencies

occurs in that task in future. Therefore, it can lead to a lack of skilled personnel to meet a

particular challenge of a project.

2.2: Estimate the expenses for July and August

Calculation of variable cost per unit using identified high and low activity level:

Total cost= (Expenses of high activity- expenses of low activity)/(Highest activity hours spent -

lowest hours spent)

Total expense per units = (9820-7410)/(795-505)=8.31

Total expenses for July:

650*8.31=5401.5

For August:

750*8.31= 6232.5

2.3: Cash budget

Cash budget Amount

Particulars September

Opening balance 9000

Cash sales 39000

Sale on account 5648

Total Cash collected 53648

Purchase -16800

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

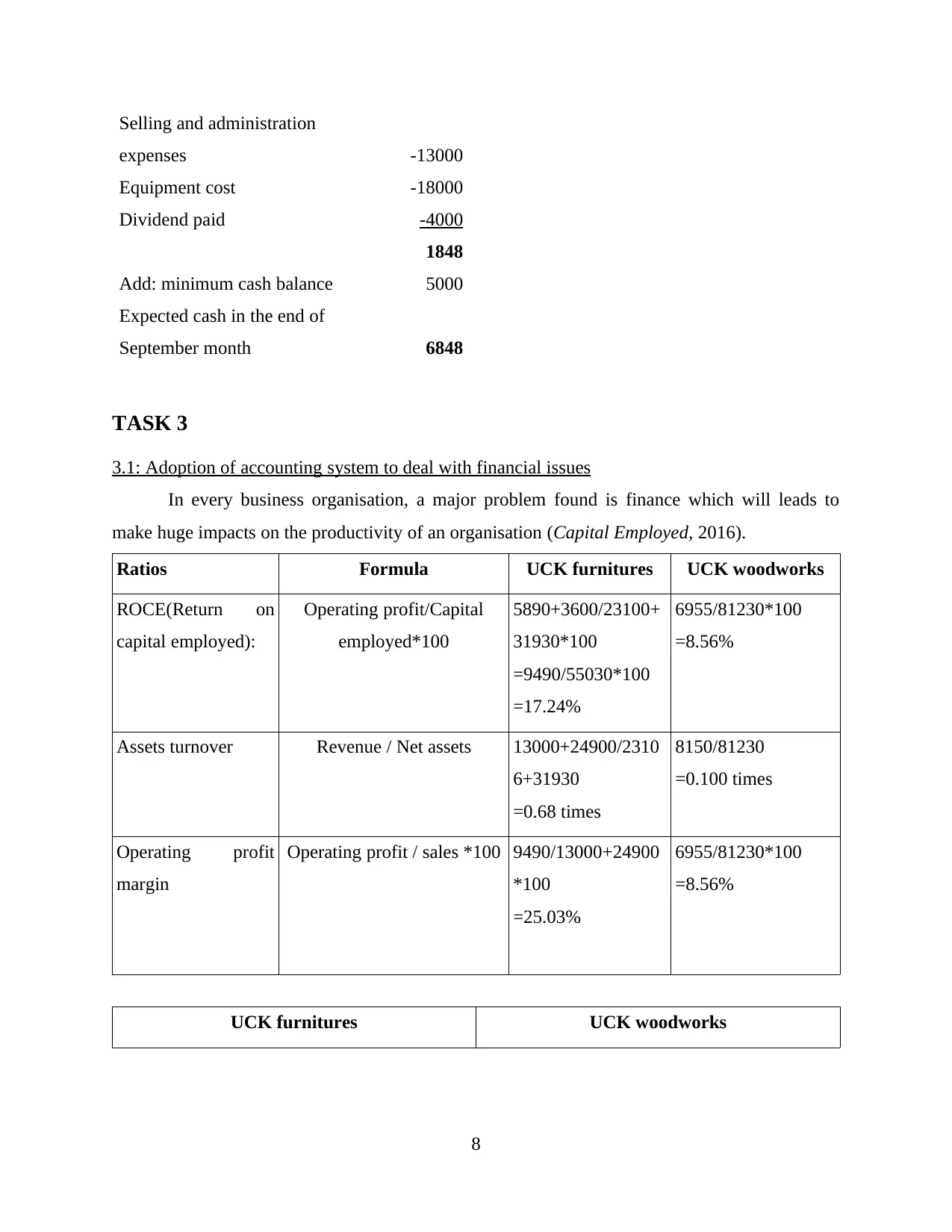

Selling and administration

expenses -13000

Equipment cost -18000

Dividend paid -4000

1848

Add: minimum cash balance 5000

Expected cash in the end of

September month 6848

TASK 3

3.1: Adoption of accounting system to deal with financial issues

In every business organisation, a major problem found is finance which will leads to

make huge impacts on the productivity of an organisation (Capital Employed, 2016).

Ratios Formula UCK furnitures UCK woodworks

ROCE(Return on

capital employed):

Operating profit/Capital

employed*100

5890+3600/23100+

31930*100

=9490/55030*100

=17.24%

6955/81230*100

=8.56%

Assets turnover Revenue / Net assets 13000+24900/2310

6+31930

=0.68 times

8150/81230

=0.100 times

Operating profit

margin

Operating profit / sales *100 9490/13000+24900

*100

=25.03%

6955/81230*100

=8.56%

UCK furnitures UCK woodworks

8

expenses -13000

Equipment cost -18000

Dividend paid -4000

1848

Add: minimum cash balance 5000

Expected cash in the end of

September month 6848

TASK 3

3.1: Adoption of accounting system to deal with financial issues

In every business organisation, a major problem found is finance which will leads to

make huge impacts on the productivity of an organisation (Capital Employed, 2016).

Ratios Formula UCK furnitures UCK woodworks

ROCE(Return on

capital employed):

Operating profit/Capital

employed*100

5890+3600/23100+

31930*100

=9490/55030*100

=17.24%

6955/81230*100

=8.56%

Assets turnover Revenue / Net assets 13000+24900/2310

6+31930

=0.68 times

8150/81230

=0.100 times

Operating profit

margin

Operating profit / sales *100 9490/13000+24900

*100

=25.03%

6955/81230*100

=8.56%

UCK furnitures UCK woodworks

8

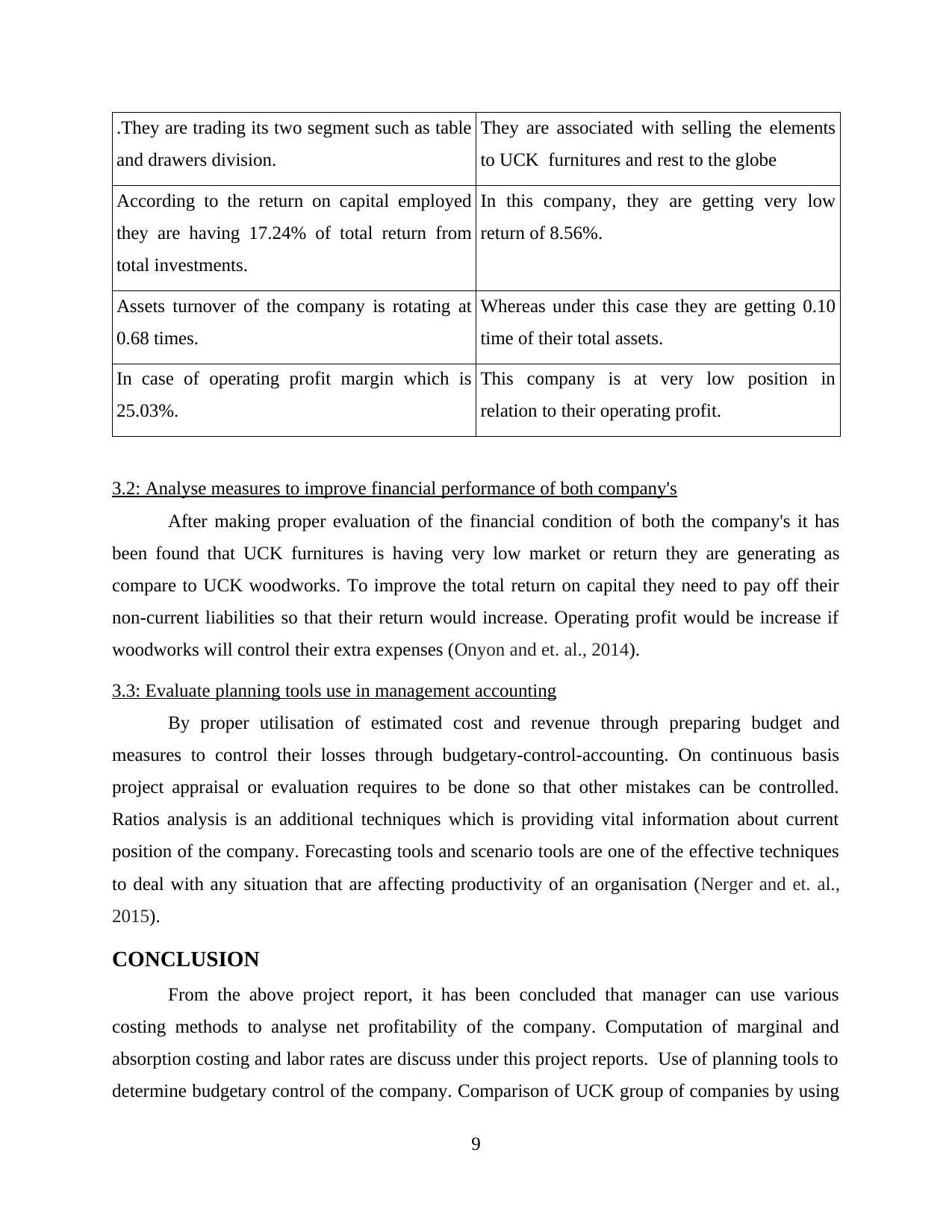

.They are trading its two segment such as table

and drawers division.

They are associated with selling the elements

to UCK furnitures and rest to the globe

According to the return on capital employed

they are having 17.24% of total return from

total investments.

In this company, they are getting very low

return of 8.56%.

Assets turnover of the company is rotating at

0.68 times.

Whereas under this case they are getting 0.10

time of their total assets.

In case of operating profit margin which is

25.03%.

This company is at very low position in

relation to their operating profit.

3.2: Analyse measures to improve financial performance of both company's

After making proper evaluation of the financial condition of both the company's it has

been found that UCK furnitures is having very low market or return they are generating as

compare to UCK woodworks. To improve the total return on capital they need to pay off their

non-current liabilities so that their return would increase. Operating profit would be increase if

woodworks will control their extra expenses (Onyon and et. al., 2014).

3.3: Evaluate planning tools use in management accounting

By proper utilisation of estimated cost and revenue through preparing budget and

measures to control their losses through budgetary-control-accounting. On continuous basis

project appraisal or evaluation requires to be done so that other mistakes can be controlled.

Ratios analysis is an additional techniques which is providing vital information about current

position of the company. Forecasting tools and scenario tools are one of the effective techniques

to deal with any situation that are affecting productivity of an organisation (Nerger and et. al.,

2015).

CONCLUSION

From the above project report, it has been concluded that manager can use various

costing methods to analyse net profitability of the company. Computation of marginal and

absorption costing and labor rates are discuss under this project reports. Use of planning tools to

determine budgetary control of the company. Comparison of UCK group of companies by using

9

and drawers division.

They are associated with selling the elements

to UCK furnitures and rest to the globe

According to the return on capital employed

they are having 17.24% of total return from

total investments.

In this company, they are getting very low

return of 8.56%.

Assets turnover of the company is rotating at

0.68 times.

Whereas under this case they are getting 0.10

time of their total assets.

In case of operating profit margin which is

25.03%.

This company is at very low position in

relation to their operating profit.

3.2: Analyse measures to improve financial performance of both company's

After making proper evaluation of the financial condition of both the company's it has

been found that UCK furnitures is having very low market or return they are generating as

compare to UCK woodworks. To improve the total return on capital they need to pay off their

non-current liabilities so that their return would increase. Operating profit would be increase if

woodworks will control their extra expenses (Onyon and et. al., 2014).

3.3: Evaluate planning tools use in management accounting

By proper utilisation of estimated cost and revenue through preparing budget and

measures to control their losses through budgetary-control-accounting. On continuous basis

project appraisal or evaluation requires to be done so that other mistakes can be controlled.

Ratios analysis is an additional techniques which is providing vital information about current

position of the company. Forecasting tools and scenario tools are one of the effective techniques

to deal with any situation that are affecting productivity of an organisation (Nerger and et. al.,

2015).

CONCLUSION

From the above project report, it has been concluded that manager can use various

costing methods to analyse net profitability of the company. Computation of marginal and

absorption costing and labor rates are discuss under this project reports. Use of planning tools to

determine budgetary control of the company. Comparison of UCK group of companies by using

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ratios and other tools. Overall evaluation is done by using effective techniques to maintain

proper balance among their financial situations.

10

proper balance among their financial situations.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

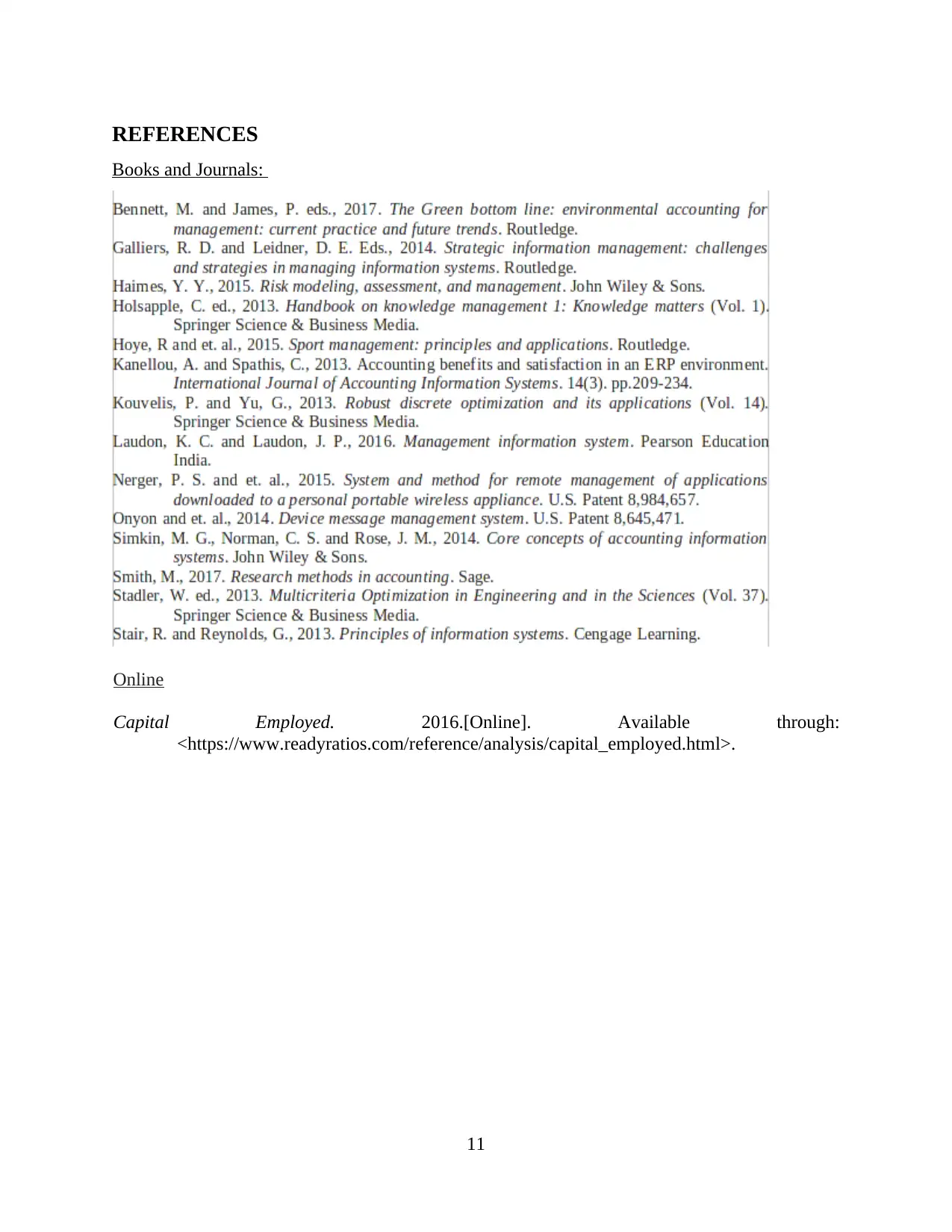

Books and Journals:

Online

Capital Employed. 2016.[Online]. Available through:

<https://www.readyratios.com/reference/analysis/capital_employed.html>.

11

Books and Journals:

Online

Capital Employed. 2016.[Online]. Available through:

<https://www.readyratios.com/reference/analysis/capital_employed.html>.

11

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.