Management Accounting Report: Techniques, Benefits, and Analysis

VerifiedAdded on 2020/02/17

|18

|5443

|129

Report

AI Summary

This report delves into the core concepts of management accounting, emphasizing its role in providing timely and accurate financial information for managerial decision-making. It explores different types of management accounting systems, including cost accounting, inventory management, and job-costing systems, highlighting their importance in assessing costs, managing inventory, and tracking project-related expenses. The report also examines various management accounting reports, such as cost reports, budget reports, and performance reports, and discusses the benefits of implementing a management accounting system, including expense reduction, improved cash flow, and better business decisions. Furthermore, it contrasts marginal costing and absorption costing techniques, providing a detailed analysis of their differences in income statement presentation and cost allocation. The report also covers the benefits and limitations of budgeting, the application of planning tools, and a comparative analysis of accounting systems in different organizations.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

TASK 1 ...........................................................................................................................................3

P1 Explain management accounting and its types.................................................................3

P2 Different types of management accounting reports..........................................................5

M 1 benefits of management accounting system...................................................................6

D1: Critical evaluation of accounting reporting system ........................................................6

TASK 2............................................................................................................................................7

P3 Explain the difference between the two management accounting techniques..................7

M2 Application of range of management accounting tool.....................................................9

D2 Financial report and interpretation of the data................................................................10

TASK 3..........................................................................................................................................10

P4 Benefit and limitations of budgets and how they are helpful in planning......................10

M3 Different planning tools.................................................................................................11

D3 Evaluation of manner in which planning tools solves the financial issues....................12

TASK 4..........................................................................................................................................12

P5 Comparing among two different organisations accounting system ...............................12

M4 Analysing the financial problems .................................................................................15

CONCLUSION .............................................................................................................................15

REFERENCES .............................................................................................................................16

INTRODUCTION...........................................................................................................................3

TASK 1 ...........................................................................................................................................3

P1 Explain management accounting and its types.................................................................3

P2 Different types of management accounting reports..........................................................5

M 1 benefits of management accounting system...................................................................6

D1: Critical evaluation of accounting reporting system ........................................................6

TASK 2............................................................................................................................................7

P3 Explain the difference between the two management accounting techniques..................7

M2 Application of range of management accounting tool.....................................................9

D2 Financial report and interpretation of the data................................................................10

TASK 3..........................................................................................................................................10

P4 Benefit and limitations of budgets and how they are helpful in planning......................10

M3 Different planning tools.................................................................................................11

D3 Evaluation of manner in which planning tools solves the financial issues....................12

TASK 4..........................................................................................................................................12

P5 Comparing among two different organisations accounting system ...............................12

M4 Analysing the financial problems .................................................................................15

CONCLUSION .............................................................................................................................15

REFERENCES .............................................................................................................................16

INTRODUCTION

Management accounting means a concept which means the process of preparing report

and accounts that are responsible to provide accurate and timely financial and statistical

information that are required by the managers to make day to day and short term decisions.

Management accounting plays an important role in organization because it generates monthly or

weekly reports for an organization. Management accountant of company is responsible to

comply all the rules regarding accounting systems (Financial information and decision making,

2016). There are different types of management accounting systems. Also, different methods

used for management accounting reporting which has been used by company. Concept of

budgetary control is also discussed in the report. There are various advantages and disadvantages

of budgetary control. a good management system involves a responsibility to manage a wide

variety of critical management accounting information using management accounting system and

techniques such as cost volume profit analysis, marginal costing and absorption costing to

produce relevant management report for informed decision making. Management accounting

techniques should be adopted with effective knowledge and analysis. Management accounting

has functions like; budgetary control, performance indicators and variances. also, there are

different advantages and disadvantages of budgetary control.

TASK 1

P1 Explain management accounting and its types

Administration bookkeeping is a term which implies it is a calling that includes

cooperating in administration basic leadership, conceiving arranging and execution

administration frameworks and furthermore giving aptitude in money related revealing and

control to help administration in the detailing and usage of an association's procedure. It stretches

out to 3 essential regions:

Strategic management: Vital administration in this, it is mindful to propel the part of the

administration bookkeeper as a vital accomplice in the association (Hansen and Otley, 2003).

Performance management: Execution administration it includes to build up the act of

basic leadership of business and furthermore deals with the execution of the association.

Management accounting means a concept which means the process of preparing report

and accounts that are responsible to provide accurate and timely financial and statistical

information that are required by the managers to make day to day and short term decisions.

Management accounting plays an important role in organization because it generates monthly or

weekly reports for an organization. Management accountant of company is responsible to

comply all the rules regarding accounting systems (Financial information and decision making,

2016). There are different types of management accounting systems. Also, different methods

used for management accounting reporting which has been used by company. Concept of

budgetary control is also discussed in the report. There are various advantages and disadvantages

of budgetary control. a good management system involves a responsibility to manage a wide

variety of critical management accounting information using management accounting system and

techniques such as cost volume profit analysis, marginal costing and absorption costing to

produce relevant management report for informed decision making. Management accounting

techniques should be adopted with effective knowledge and analysis. Management accounting

has functions like; budgetary control, performance indicators and variances. also, there are

different advantages and disadvantages of budgetary control.

TASK 1

P1 Explain management accounting and its types

Administration bookkeeping is a term which implies it is a calling that includes

cooperating in administration basic leadership, conceiving arranging and execution

administration frameworks and furthermore giving aptitude in money related revealing and

control to help administration in the detailing and usage of an association's procedure. It stretches

out to 3 essential regions:

Strategic management: Vital administration in this, it is mindful to propel the part of the

administration bookkeeper as a vital accomplice in the association (Hansen and Otley, 2003).

Performance management: Execution administration it includes to build up the act of

basic leadership of business and furthermore deals with the execution of the association.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Risk management: Hazard administration structure for rehearses and furthermore it

distinguishes, measures, oversees and report dangers to the accomplishment of the targets of an

association.

The individual who is in charge of readiness and introduction of budgetary and other choice

arranged data in such an approach to help administration in plan of strategies is known as

administration bookkeeper. Administration bookkeeping is in charge of giving point by point and

disaggregated data about items, singular exercises, divisions, plants, operations and errands. it

doesn't centers around the organization all in all. Administration bookkeeping is in charge of

administration of the business group and furthermore report connections and obligation to the

company's back association. There are diverse sorts of administrative bookkeeping frameworks

that are utilized by the organization in particular;

Cost accounting system: It is a structure utilized by organizations to gauge the

cost of their items for benefit examination, stock assessment and cost control. As,

assessing the exact expenses of items is basic for gainful operations,so a firm

should think about which results of the organization are productive for and which

ones are not (Harris and Mongiello, 2012). It can be just discovered when it has

the right cost has been evaluated of the item.

This is critical kind of administration bookkeeping framework since cost bookkeeping

framework encourages the organization to gauge the end estimation of materials stock, work in

advance and completed products.

This is important type of management accounting system because cost accounting system

helps the company to estimate the closing value of materials inventory, work in progress and

finished goods.

▪ Inventory management system – it is the continuous procedure of moving parts

and items into and out of an organization's areas. Administration of organizations

deals with their stock once a day as they put in new requests for items requested

by clients and ship requests to the clients.

It is important for the company because the company, for solving an issue of proper inventory

management. The companies turned to software that can help them keep tracking regarding all

their inventory, orders, vendors and more. All inventory are compiled in the software so that it

would be easy for them to keep a eye check on their inventory.

distinguishes, measures, oversees and report dangers to the accomplishment of the targets of an

association.

The individual who is in charge of readiness and introduction of budgetary and other choice

arranged data in such an approach to help administration in plan of strategies is known as

administration bookkeeper. Administration bookkeeping is in charge of giving point by point and

disaggregated data about items, singular exercises, divisions, plants, operations and errands. it

doesn't centers around the organization all in all. Administration bookkeeping is in charge of

administration of the business group and furthermore report connections and obligation to the

company's back association. There are diverse sorts of administrative bookkeeping frameworks

that are utilized by the organization in particular;

Cost accounting system: It is a structure utilized by organizations to gauge the

cost of their items for benefit examination, stock assessment and cost control. As,

assessing the exact expenses of items is basic for gainful operations,so a firm

should think about which results of the organization are productive for and which

ones are not (Harris and Mongiello, 2012). It can be just discovered when it has

the right cost has been evaluated of the item.

This is critical kind of administration bookkeeping framework since cost bookkeeping

framework encourages the organization to gauge the end estimation of materials stock, work in

advance and completed products.

This is important type of management accounting system because cost accounting system

helps the company to estimate the closing value of materials inventory, work in progress and

finished goods.

▪ Inventory management system – it is the continuous procedure of moving parts

and items into and out of an organization's areas. Administration of organizations

deals with their stock once a day as they put in new requests for items requested

by clients and ship requests to the clients.

It is important for the company because the company, for solving an issue of proper inventory

management. The companies turned to software that can help them keep tracking regarding all

their inventory, orders, vendors and more. All inventory are compiled in the software so that it

would be easy for them to keep a eye check on their inventory.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

▪ Job – costing system- An occupation costing framework includes the way toward

gathering data about the expenses related with particular creation or

administration work. This data might be required to give data with respect to

expenses to clients, under an agreement where costs are repaid. It is additionally

valuable for deciding the precision of organization's assessing framework.

P2 Different types of management accounting reports

There are different types of management accounting reports which the company uses for

establishing managerial accounting system in company. Management accounting mainly focuses

internally on information received through financially accounting. Managerial accounting is used

for planning, controlling and decision making. There are many types of management accounting

reports that include:

Cost reports: it is the tool which the company uses for calculating costs of items

produced. This report is consist of raw product costs, overhead, labour and any additional

costs into consideration. Then, the totals are divided by amounts of products produced.

All of this information is summarised in cost report of company. However, this report

allows managers of company to see the costs prices of goods versus selling prices. It

helps the managers to plan and also control profit margin (Nikbakht and et.al., 2006). It

also includes job costs report which shows expenses for a specific product. They are

compared with the estimate of revenue so that company would be able to evaluate the job

's profitability. It identifies higher earning areas of the business of company namely, so

that it can focus its efforts there instead of wasting time and money on jobs with low

profit margin. Job cost reports are also used to analyse expenses while the project is in

progress so managers of company can correct areas of waste before the costs escalate.

Budget report- it is an another report which has been used by company to enable the

managerial accounting reporting in the said organization. it helps the small business

owners to analyse their company's performance and in case if the business of company is

comparatively big, then managers analyse the performance of their department and also

control costs (Nobanee, Abdullatif and AlHajjar, 2011). The estimated budget for the

particular time is is based on the actual expenses. Budget report can also be used for the

providing incentives to employees. In this case some of the funds budgeted may be given

out up as bonuses to employees of the company.

gathering data about the expenses related with particular creation or

administration work. This data might be required to give data with respect to

expenses to clients, under an agreement where costs are repaid. It is additionally

valuable for deciding the precision of organization's assessing framework.

P2 Different types of management accounting reports

There are different types of management accounting reports which the company uses for

establishing managerial accounting system in company. Management accounting mainly focuses

internally on information received through financially accounting. Managerial accounting is used

for planning, controlling and decision making. There are many types of management accounting

reports that include:

Cost reports: it is the tool which the company uses for calculating costs of items

produced. This report is consist of raw product costs, overhead, labour and any additional

costs into consideration. Then, the totals are divided by amounts of products produced.

All of this information is summarised in cost report of company. However, this report

allows managers of company to see the costs prices of goods versus selling prices. It

helps the managers to plan and also control profit margin (Nikbakht and et.al., 2006). It

also includes job costs report which shows expenses for a specific product. They are

compared with the estimate of revenue so that company would be able to evaluate the job

's profitability. It identifies higher earning areas of the business of company namely, so

that it can focus its efforts there instead of wasting time and money on jobs with low

profit margin. Job cost reports are also used to analyse expenses while the project is in

progress so managers of company can correct areas of waste before the costs escalate.

Budget report- it is an another report which has been used by company to enable the

managerial accounting reporting in the said organization. it helps the small business

owners to analyse their company's performance and in case if the business of company is

comparatively big, then managers analyse the performance of their department and also

control costs (Nobanee, Abdullatif and AlHajjar, 2011). The estimated budget for the

particular time is is based on the actual expenses. Budget report can also be used for the

providing incentives to employees. In this case some of the funds budgeted may be given

out up as bonuses to employees of the company.

Performance reports- performance report can be used as another managerial reporting

method as it is used to compare actual expenditures and revenues to budgeted amounts.

The differences calculated are analysed at the time when new budgets and all information

regarding these amounts is listed on a performance report. These reports are calculated

every year. It helps the manager of company to plan for future demand in production and

also in case of cost increases (Shim and Siegel, 2008).

M 1 benefits of management accounting system

There are many benefits of management accounting system to the company. Business

owners can design management accounting systems according to their company and its

operations. management operations has several benefits to the company. The benefits are as

follows: Reduce expenses - management accounting system can help in reducing the operational

expenses. Management accountant use management accounting information to review the

costs of economic resources and other business operations (Kaplan and Atkinson, 2015).

With the help of this, business owners also assess the quality on the economic resources

used to produce goods and services. Improve cash flow- budgets are he major parts of management accounting system. To

have a financial road map for future business expenditures, many business owners often

use budgets .management accountant will go through these information to create a master

budget for the entire company.

1. Business decisions- management accounting helps in improving business decisions of the

company as it provides quantitative analyses for various decisions opportunities. Top

management of business reviews each opportunity through the prism of quantitative

analysis to ensure that they have clear information relating to business.

From the above accounting system its has been found that productive and efficiency of

the cited company are major aspect. So, it can help the company to minimise their operational

expenses. It also help to reviews the total cost of economic resources and other business

activities. The major advantages in this system that provided effective tool for decision making.

D1: Critical evaluation of accounting reporting system

In an organisation, accounting system is said to be major aspect that need to be use in

appropriate manner so that more effective results can be drawn. In the opinion of Horngren and

method as it is used to compare actual expenditures and revenues to budgeted amounts.

The differences calculated are analysed at the time when new budgets and all information

regarding these amounts is listed on a performance report. These reports are calculated

every year. It helps the manager of company to plan for future demand in production and

also in case of cost increases (Shim and Siegel, 2008).

M 1 benefits of management accounting system

There are many benefits of management accounting system to the company. Business

owners can design management accounting systems according to their company and its

operations. management operations has several benefits to the company. The benefits are as

follows: Reduce expenses - management accounting system can help in reducing the operational

expenses. Management accountant use management accounting information to review the

costs of economic resources and other business operations (Kaplan and Atkinson, 2015).

With the help of this, business owners also assess the quality on the economic resources

used to produce goods and services. Improve cash flow- budgets are he major parts of management accounting system. To

have a financial road map for future business expenditures, many business owners often

use budgets .management accountant will go through these information to create a master

budget for the entire company.

1. Business decisions- management accounting helps in improving business decisions of the

company as it provides quantitative analyses for various decisions opportunities. Top

management of business reviews each opportunity through the prism of quantitative

analysis to ensure that they have clear information relating to business.

From the above accounting system its has been found that productive and efficiency of

the cited company are major aspect. So, it can help the company to minimise their operational

expenses. It also help to reviews the total cost of economic resources and other business

activities. The major advantages in this system that provided effective tool for decision making.

D1: Critical evaluation of accounting reporting system

In an organisation, accounting system is said to be major aspect that need to be use in

appropriate manner so that more effective results can be drawn. In the opinion of Horngren and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

et. al., (2005) an positive strategies can be made so that cited company would be able to manage

their financial transactions. As overall goodwill and profitability is depend upon the type of

reporting system used by the company. Job costing and inventory systems are the most effective

reporting system an organisation should have.

TASK 2

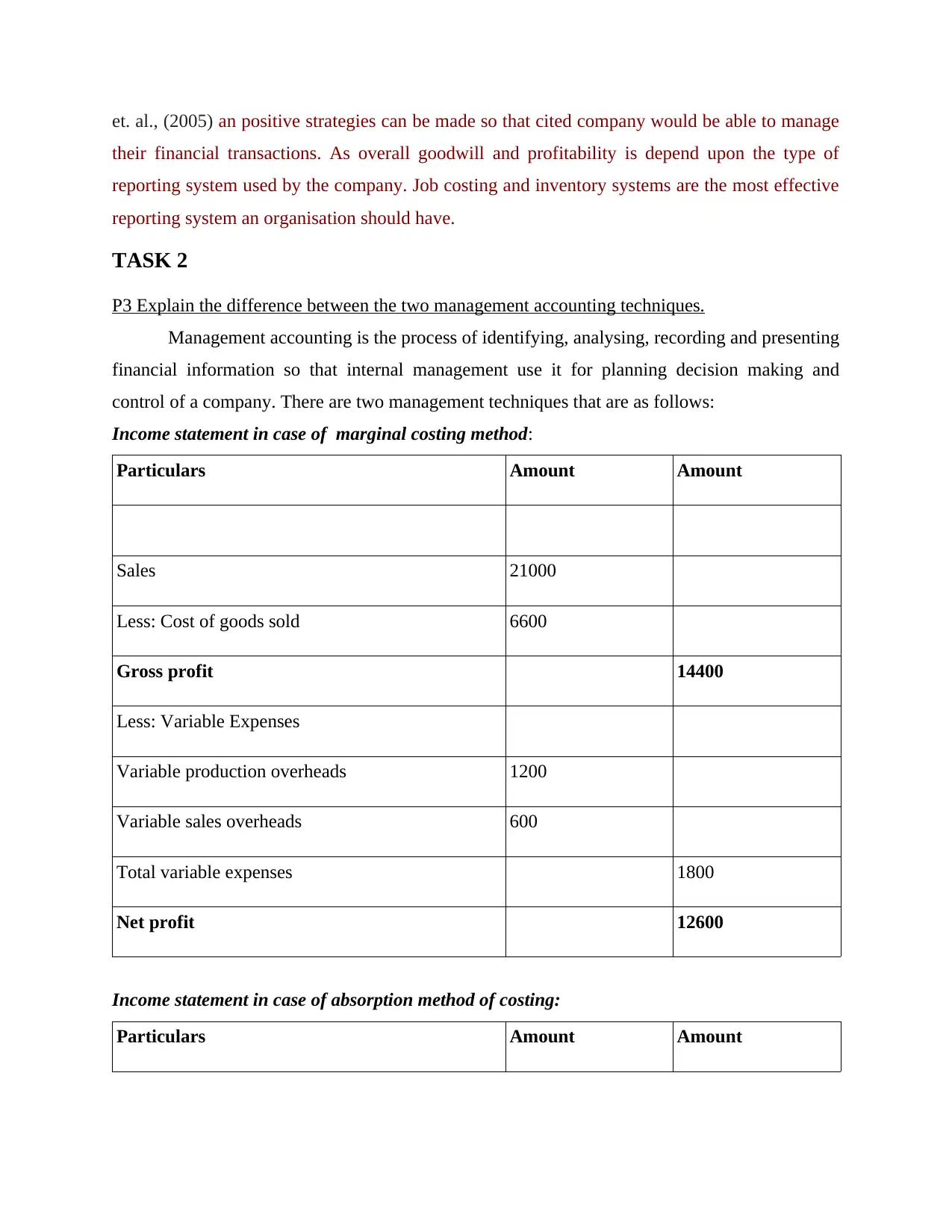

P3 Explain the difference between the two management accounting techniques.

Management accounting is the process of identifying, analysing, recording and presenting

financial information so that internal management use it for planning decision making and

control of a company. There are two management techniques that are as follows:

Income statement in case of marginal costing method:

Particulars Amount Amount

Sales 21000

Less: Cost of goods sold 6600

Gross profit 14400

Less: Variable Expenses

Variable production overheads 1200

Variable sales overheads 600

Total variable expenses 1800

Net profit 12600

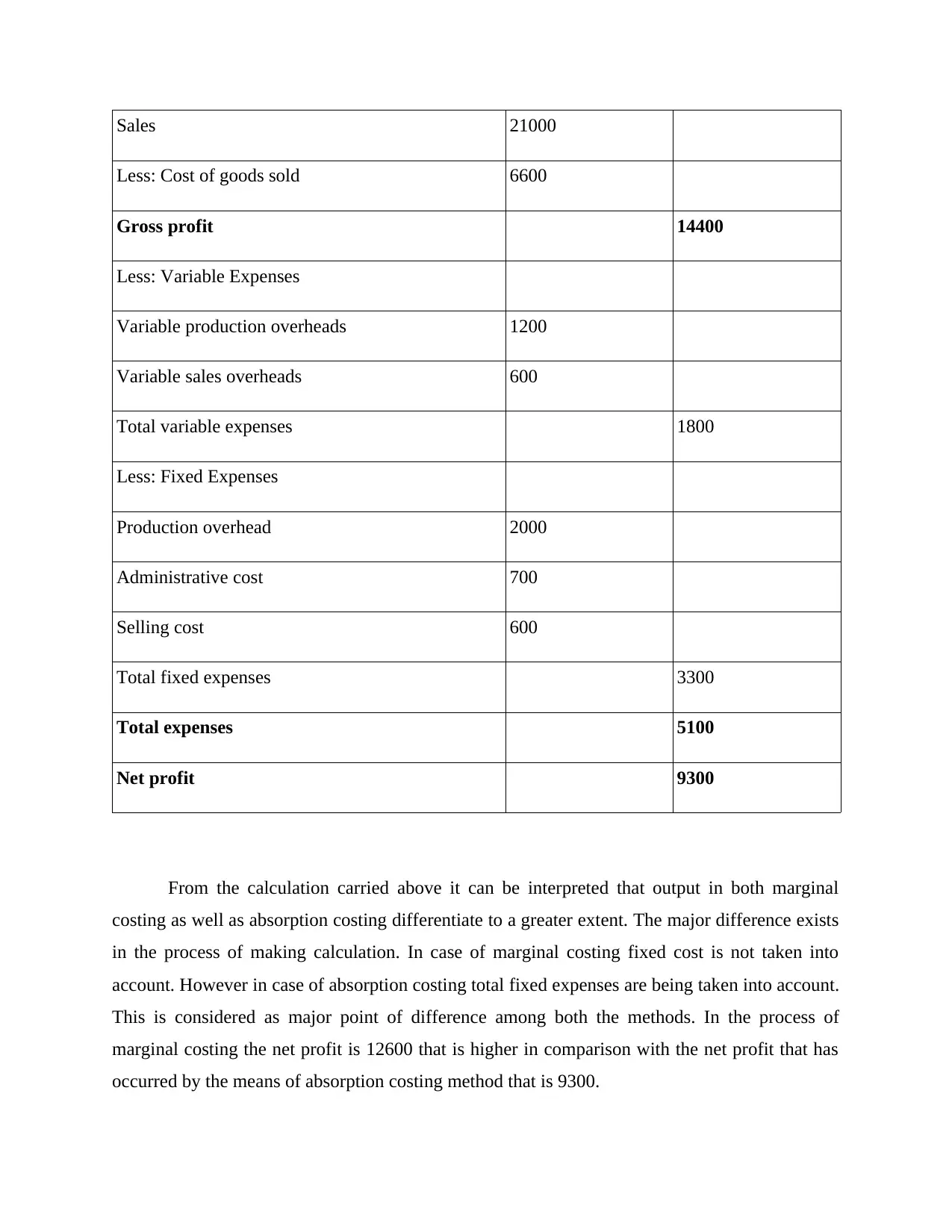

Income statement in case of absorption method of costing:

Particulars Amount Amount

their financial transactions. As overall goodwill and profitability is depend upon the type of

reporting system used by the company. Job costing and inventory systems are the most effective

reporting system an organisation should have.

TASK 2

P3 Explain the difference between the two management accounting techniques.

Management accounting is the process of identifying, analysing, recording and presenting

financial information so that internal management use it for planning decision making and

control of a company. There are two management techniques that are as follows:

Income statement in case of marginal costing method:

Particulars Amount Amount

Sales 21000

Less: Cost of goods sold 6600

Gross profit 14400

Less: Variable Expenses

Variable production overheads 1200

Variable sales overheads 600

Total variable expenses 1800

Net profit 12600

Income statement in case of absorption method of costing:

Particulars Amount Amount

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Sales 21000

Less: Cost of goods sold 6600

Gross profit 14400

Less: Variable Expenses

Variable production overheads 1200

Variable sales overheads 600

Total variable expenses 1800

Less: Fixed Expenses

Production overhead 2000

Administrative cost 700

Selling cost 600

Total fixed expenses 3300

Total expenses 5100

Net profit 9300

From the calculation carried above it can be interpreted that output in both marginal

costing as well as absorption costing differentiate to a greater extent. The major difference exists

in the process of making calculation. In case of marginal costing fixed cost is not taken into

account. However in case of absorption costing total fixed expenses are being taken into account.

This is considered as major point of difference among both the methods. In the process of

marginal costing the net profit is 12600 that is higher in comparison with the net profit that has

occurred by the means of absorption costing method that is 9300.

Less: Cost of goods sold 6600

Gross profit 14400

Less: Variable Expenses

Variable production overheads 1200

Variable sales overheads 600

Total variable expenses 1800

Less: Fixed Expenses

Production overhead 2000

Administrative cost 700

Selling cost 600

Total fixed expenses 3300

Total expenses 5100

Net profit 9300

From the calculation carried above it can be interpreted that output in both marginal

costing as well as absorption costing differentiate to a greater extent. The major difference exists

in the process of making calculation. In case of marginal costing fixed cost is not taken into

account. However in case of absorption costing total fixed expenses are being taken into account.

This is considered as major point of difference among both the methods. In the process of

marginal costing the net profit is 12600 that is higher in comparison with the net profit that has

occurred by the means of absorption costing method that is 9300.

The methods of management accounting that is marginal as well as absorption costing

can be differentiated on the basis of several points. These have been enumerated in the manner as

below: Meaning: The concept of marginal costing is regarded as the tool that assist in making

determination of the total cost involved in production. In contrast to this absorption

costing is referred to as the apportionment of the total costs to cost centre for the sake of

assessing the total cost involves in product. Cost recognition: Under marginal costing the variable cost is regarded as the cost of the

product whereas period costs is considered as the fixed one. On the other hand in case of

absorption costing both fixed as well as variable costs is regarded as cost of product. Classification of the overheads: In case of marginal costing the overheads are being

classified into fixed as well as variable. On the other hand in absorption costing

categorization of overhead is being done on the basis of production, administration as

well as selling and distribution. Profitability: Within the method of marginal costing the profitability is being measured

by the means of profit-volume ratio (Bromwich and Bhimani, 2005). In contrast to this in

case of absorption costing because of inclusion of the fixed cost the profitability is

influenced to a significant level. Cost per unit: Under marginal costing the variances within the opening as well as closing

stock does not affect the cost per unit related with the output. In contrast to this under

absorption costing the variances within the opening as well as closing stock influence

cost per unit.

Cost data: In case of marginal costing it is presented towards outlining total contribution

of every product. In contrary to this under absorption costing the data of cost is being

demonstrated in conventional manner.

M2 Application of range of management accounting tool

Management accounting makes use various methods in order to comply with its

responsibilities and duties related with the management. This is comprised of tools that are

enumerated in the manner as below:

Financial statement analysis: Financial statements is regarded as the indicator of the two

important factors that is comprised of profitability as well as financial effectiveness. Analysis

can be differentiated on the basis of several points. These have been enumerated in the manner as

below: Meaning: The concept of marginal costing is regarded as the tool that assist in making

determination of the total cost involved in production. In contrast to this absorption

costing is referred to as the apportionment of the total costs to cost centre for the sake of

assessing the total cost involves in product. Cost recognition: Under marginal costing the variable cost is regarded as the cost of the

product whereas period costs is considered as the fixed one. On the other hand in case of

absorption costing both fixed as well as variable costs is regarded as cost of product. Classification of the overheads: In case of marginal costing the overheads are being

classified into fixed as well as variable. On the other hand in absorption costing

categorization of overhead is being done on the basis of production, administration as

well as selling and distribution. Profitability: Within the method of marginal costing the profitability is being measured

by the means of profit-volume ratio (Bromwich and Bhimani, 2005). In contrast to this in

case of absorption costing because of inclusion of the fixed cost the profitability is

influenced to a significant level. Cost per unit: Under marginal costing the variances within the opening as well as closing

stock does not affect the cost per unit related with the output. In contrast to this under

absorption costing the variances within the opening as well as closing stock influence

cost per unit.

Cost data: In case of marginal costing it is presented towards outlining total contribution

of every product. In contrary to this under absorption costing the data of cost is being

demonstrated in conventional manner.

M2 Application of range of management accounting tool

Management accounting makes use various methods in order to comply with its

responsibilities and duties related with the management. This is comprised of tools that are

enumerated in the manner as below:

Financial statement analysis: Financial statements is regarded as the indicator of the two

important factors that is comprised of profitability as well as financial effectiveness. Analysis

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

and interpretation of the financial statement enables towards fuller diagnosis in relation with the

profitability and the firm's financial soundness (Hansen, Mowen and Guan, 2007). Analysis is

regarded as the methodical classification of the provided data within financial statements. The

categorization that is methodical enables towards making comparison of the several inter-

connected figures with one another. Interpretation provides explanation in relation with the

meaning and significance of the information.

Funds flow analysis: It is considered as the essential tool for the management accountant.

It reveals the alterations within the working capital position to a greater extent. This is comprised

of the sources from where the working capital is being gained as well as the purpose for which it

has been utilized (Zimmerman and Yahya-Zadeh, 2011). It is effective revealing the alterations

that are taking place beside the balance sheet.

Cash flow analysis: It makes determination of the sources as well as application in

relation with the cash. This is being prepared based upon the actual or the information estimated.

It makes determination of the alterations within the position of cash from a particular period to

another. A cash flow or cash budget that is projected one assist the management in determining

the amount of cash that exists towards meeting the obligation for trading creditors, payment of

loan from bank and paying dividend to the holders of shares.

Standard costing: Costing is being carried out in order to prepare and make use of

standard costing, their comparison with actual costs as well as analysis of the variance. It makes

disclosure of the cost of deviations from the standards. It possess the aim towards making

assessment of the product cost, procedure or operation in standard operating conditions.

Budgetary control: It is considered as important management tool that can be used by Morrison

in order to control costs and increase the profitability to a significant level. It assist in making

comparison of the present performance with the pre planned performance (Ahrens and Chapman,

2007). Thus it results in bringing improvements in the deviations that have emerged.

Management reporting: It is considered as the organized method of offering every manager with

whole data. This includes the data that is required by him in order to make decisions in an

effective manner. It has effectiveness in developing understanding as well as stimulating the

actions to a greater extent.

D2 Financial report and interpretation of the data

This is being covered in P3 part.

profitability and the firm's financial soundness (Hansen, Mowen and Guan, 2007). Analysis is

regarded as the methodical classification of the provided data within financial statements. The

categorization that is methodical enables towards making comparison of the several inter-

connected figures with one another. Interpretation provides explanation in relation with the

meaning and significance of the information.

Funds flow analysis: It is considered as the essential tool for the management accountant.

It reveals the alterations within the working capital position to a greater extent. This is comprised

of the sources from where the working capital is being gained as well as the purpose for which it

has been utilized (Zimmerman and Yahya-Zadeh, 2011). It is effective revealing the alterations

that are taking place beside the balance sheet.

Cash flow analysis: It makes determination of the sources as well as application in

relation with the cash. This is being prepared based upon the actual or the information estimated.

It makes determination of the alterations within the position of cash from a particular period to

another. A cash flow or cash budget that is projected one assist the management in determining

the amount of cash that exists towards meeting the obligation for trading creditors, payment of

loan from bank and paying dividend to the holders of shares.

Standard costing: Costing is being carried out in order to prepare and make use of

standard costing, their comparison with actual costs as well as analysis of the variance. It makes

disclosure of the cost of deviations from the standards. It possess the aim towards making

assessment of the product cost, procedure or operation in standard operating conditions.

Budgetary control: It is considered as important management tool that can be used by Morrison

in order to control costs and increase the profitability to a significant level. It assist in making

comparison of the present performance with the pre planned performance (Ahrens and Chapman,

2007). Thus it results in bringing improvements in the deviations that have emerged.

Management reporting: It is considered as the organized method of offering every manager with

whole data. This includes the data that is required by him in order to make decisions in an

effective manner. It has effectiveness in developing understanding as well as stimulating the

actions to a greater extent.

D2 Financial report and interpretation of the data

This is being covered in P3 part.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 3

P4 Benefit and limitations of budgets and how they are helpful in planning

Budgetary control is a tool which a cited company may use in management of their

business operation. It set the perfect plan for the future ability that a company would be planning

to reach. The actual and standard cost which are incurred during that particular time period.

There are certain objectives of budgetary control which are mentioned underneath:

To plan the future forecasting of total sales and Net profit-volume of the company.

The main purpose of this budgetary control is to minimise the losses and control extra

costs.

The overall decision is based on the budget plan designed by the cited company.

There are many advantages and disadvantages of budgetary control :

Advantages:

It is said to be identified plan which is used to target the future of the company growth.

Planning tools enable the management to determines goals and objectives of company so

as budget can be prepared accordingly.

It also secures better coordination among various departments (Macintosh and Quattrone,

2010).

It help to control extra cost which are incurred on the production of products.

Budgetary control also facilitate centralized control with centralised activity.

It enables the company to run its operations smoothly as, everything has been planned

and provided in advance.

Limitation:

Budgets are more complex as it takes so much time.

Budgets are not able to overcome the small losses and costs of a company (Chapman,

2005).

It is based on total uncertainty.

Also, some of the decision are delayed because of inappropriate budget plan.

M3 Different planning tools

There is presence of several tools that can be used for the purpose of planning in

management accounting. This is comprised of following:

P4 Benefit and limitations of budgets and how they are helpful in planning

Budgetary control is a tool which a cited company may use in management of their

business operation. It set the perfect plan for the future ability that a company would be planning

to reach. The actual and standard cost which are incurred during that particular time period.

There are certain objectives of budgetary control which are mentioned underneath:

To plan the future forecasting of total sales and Net profit-volume of the company.

The main purpose of this budgetary control is to minimise the losses and control extra

costs.

The overall decision is based on the budget plan designed by the cited company.

There are many advantages and disadvantages of budgetary control :

Advantages:

It is said to be identified plan which is used to target the future of the company growth.

Planning tools enable the management to determines goals and objectives of company so

as budget can be prepared accordingly.

It also secures better coordination among various departments (Macintosh and Quattrone,

2010).

It help to control extra cost which are incurred on the production of products.

Budgetary control also facilitate centralized control with centralised activity.

It enables the company to run its operations smoothly as, everything has been planned

and provided in advance.

Limitation:

Budgets are more complex as it takes so much time.

Budgets are not able to overcome the small losses and costs of a company (Chapman,

2005).

It is based on total uncertainty.

Also, some of the decision are delayed because of inappropriate budget plan.

M3 Different planning tools

There is presence of several tools that can be used for the purpose of planning in

management accounting. This is comprised of following:

Budgets

Cost-volume-profit analysis

Product costing

In order to get positive outcome from the business operations of an organisation. It is

important to create a perfect plan to achieve aims and objectives. The overall stability of the

company is depend upon the extra cost which are incurred during production process should be

control. As because company would get cost advantages over its products which help the cited

company's to obtain positive results.

D3 Evaluation of manner in which planning tools solves the financial issues Budgets: It is considered as the most significant tool of planning. It is effective in

directing the management and assist them in making decision in an effective manner. Cost-volume-profit analysis: It can be used by Morrison when it is planning for

expansion. It is powerful tool that presents the amount of sales that firms needs to make

in order avoid the situation of loss (Ax and Bjørnenak, 2005).

Product costing: This is suitable tool which assist in making planning regarding the

product cost.

TASK 4

P5 Comparing among two different organisations accounting system

The accounting system of an organization plays important role which assists corporation

like Morrisons to carry out all operation or costing related techniques in an effectual manner.

According to the given case scenario, in case Morrisons face any issue related to accounting

problem then it would be possible to adopt necessary account practices so as to ensure the

certainty and secure the good position of the business in the marketplace with the increased rate

of return. The major role of management accountant is to perform series of task for the purpose

of greater level of financial security of the business along with handling all related mater. This

proves to be effective for successful operation of the same along with its aim to create

competitive edge in the marketplace (Modell, 2005). At this juncture, varied practices are

followed in order to address the financial issues. For example, operational control system is

applied in Morrisons whereby management of corporation effectively ensure to total quality

management for the sake of better production activities. It can also be done with the help of

Cost-volume-profit analysis

Product costing

In order to get positive outcome from the business operations of an organisation. It is

important to create a perfect plan to achieve aims and objectives. The overall stability of the

company is depend upon the extra cost which are incurred during production process should be

control. As because company would get cost advantages over its products which help the cited

company's to obtain positive results.

D3 Evaluation of manner in which planning tools solves the financial issues Budgets: It is considered as the most significant tool of planning. It is effective in

directing the management and assist them in making decision in an effective manner. Cost-volume-profit analysis: It can be used by Morrison when it is planning for

expansion. It is powerful tool that presents the amount of sales that firms needs to make

in order avoid the situation of loss (Ax and Bjørnenak, 2005).

Product costing: This is suitable tool which assist in making planning regarding the

product cost.

TASK 4

P5 Comparing among two different organisations accounting system

The accounting system of an organization plays important role which assists corporation

like Morrisons to carry out all operation or costing related techniques in an effectual manner.

According to the given case scenario, in case Morrisons face any issue related to accounting

problem then it would be possible to adopt necessary account practices so as to ensure the

certainty and secure the good position of the business in the marketplace with the increased rate

of return. The major role of management accountant is to perform series of task for the purpose

of greater level of financial security of the business along with handling all related mater. This

proves to be effective for successful operation of the same along with its aim to create

competitive edge in the marketplace (Modell, 2005). At this juncture, varied practices are

followed in order to address the financial issues. For example, operational control system is

applied in Morrisons whereby management of corporation effectively ensure to total quality

management for the sake of better production activities. It can also be done with the help of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.