Management Accounting Report: Techniques, Integration and Benefits

VerifiedAdded on 2023/06/08

|15

|4401

|433

Report

AI Summary

This report provides a comprehensive overview of management accounting, encompassing its core principles, roles, and the techniques employed within a business context. The report delves into the significance of management accounting in identifying, measuring, and interpreting financial data to achieve organizational goals. It explores the application of various techniques, including marginal costing and absorption costing, through practical examples. The report further examines the integration of management accounting within an organization, highlighting the benefits it offers, such as improved decision-making and cost management. Additionally, it compares and contrasts different planning tools used in management accounting and evaluates their effectiveness in addressing financial challenges. The report emphasizes the role of management accounting in both short-term and long-term planning, financial record-keeping, and capital structure maintenance. The report concludes by reflecting on the practical application of management accounting principles and the importance of continuous improvement and quality management.

Management accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

PART 1............................................................................................................................................3

MAIN BODY..................................................................................................................................3

Principle of management accounting...........................................................................................3

Role of management accounting and system...............................................................................4

Utilization of techniques and methods of management accounting systems..............................5

Presenting ways management accounting is integrated within the organisation.........................7

Explaining benefits of the function to organization....................................................................8

Conclusion reflects application of management accounting......................................................8

PART 2............................................................................................................................................9

Comparing and contrasting three planning tools used in management accounting.....................9

Comparing about the adaption and application of the management accounting and evaluating

its effectiveness in dealing the financial problems....................................................................11

CONCLUSION..............................................................................................................................13

REFERENCES................................................................................................................................1

INTRODUCTION...........................................................................................................................3

PART 1............................................................................................................................................3

MAIN BODY..................................................................................................................................3

Principle of management accounting...........................................................................................3

Role of management accounting and system...............................................................................4

Utilization of techniques and methods of management accounting systems..............................5

Presenting ways management accounting is integrated within the organisation.........................7

Explaining benefits of the function to organization....................................................................8

Conclusion reflects application of management accounting......................................................8

PART 2............................................................................................................................................9

Comparing and contrasting three planning tools used in management accounting.....................9

Comparing about the adaption and application of the management accounting and evaluating

its effectiveness in dealing the financial problems....................................................................11

CONCLUSION..............................................................................................................................13

REFERENCES................................................................................................................................1

INTRODUCTION

Management accounting is mainly defined as the practice which helps in identifying,

measuring and interpreting the financial data of a business which helps in attaining the set

organizational gaols. This function mainly helps in providing the details of the company and

helps in taking the timely decision for attaining the long term growth in the business. It plays key

role in preparing the reports and results in taking the long term and short term decision in the

company for attaining the goals by recording the financial transactions of a particular business.

This report manly provide details about the medium size manufacturing company with

explaining the principles of the management accounting. Also, defining the role of management

accounting and it systems. Future using variety techniques and methods which helps in defining

and presenting the calculations for an income statements using costing. Also, evaluating the

management accounting and its integration within the business and the benefits of using this

functions. Further, comparing and contrasting three planning tools used in management

accounting with defining its advantages and disadvantages. Also, adopting the management

accounting for dealing with all the financial problems.

PART 1

MAIN BODY

Principle of management accounting

Designing and compiling: Accounting information, records, reports and other evidence of

present, past and future should meet the needs of the particular business Along with this, it

should be designed in such a way that it represents the relevant data so that particular problem

can be solved. The information should meet the essentials of management (Santoro and et.al.,

2018).

Management by exception: This principle is followed when presenting the data related to

management and it means that budget control and standard costing methods are followed by the

company.

Control at sources Accounting: In this principle a qualitative and quantitative report is

formed in which work details like cost, machinery, repair and maintenance is recorded. Which

helps in controlling the extra cost.

Influence: Communication present crucial data and it present the start and end of the

management accounting and it strengthen the process of decision making(Reyes-Menendez and

Management accounting is mainly defined as the practice which helps in identifying,

measuring and interpreting the financial data of a business which helps in attaining the set

organizational gaols. This function mainly helps in providing the details of the company and

helps in taking the timely decision for attaining the long term growth in the business. It plays key

role in preparing the reports and results in taking the long term and short term decision in the

company for attaining the goals by recording the financial transactions of a particular business.

This report manly provide details about the medium size manufacturing company with

explaining the principles of the management accounting. Also, defining the role of management

accounting and it systems. Future using variety techniques and methods which helps in defining

and presenting the calculations for an income statements using costing. Also, evaluating the

management accounting and its integration within the business and the benefits of using this

functions. Further, comparing and contrasting three planning tools used in management

accounting with defining its advantages and disadvantages. Also, adopting the management

accounting for dealing with all the financial problems.

PART 1

MAIN BODY

Principle of management accounting

Designing and compiling: Accounting information, records, reports and other evidence of

present, past and future should meet the needs of the particular business Along with this, it

should be designed in such a way that it represents the relevant data so that particular problem

can be solved. The information should meet the essentials of management (Santoro and et.al.,

2018).

Management by exception: This principle is followed when presenting the data related to

management and it means that budget control and standard costing methods are followed by the

company.

Control at sources Accounting: In this principle a qualitative and quantitative report is

formed in which work details like cost, machinery, repair and maintenance is recorded. Which

helps in controlling the extra cost.

Influence: Communication present crucial data and it present the start and end of the

management accounting and it strengthen the process of decision making(Reyes-Menendez and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

et.al., 2020). Moreover, sound communication is important to maintain the smooth flow of data

within the company and authority can take decision in order to deal with harmful situation.

Relevance: Information is valuable for the company so management accounting should check

the best available resource so that it can take and implement decision for solving the issues.

Moreover, accounts should be related with past, present and future information, external and

internal data as well as financial and non-financial details.

Value: It has been estimated as management accounting links with company details and core

enterprise model that provide intensive knowledge regarding the macro economic and market

situation. Along with this, it deals with evaluating information along with identifying

opportunities and risks. Situational analysis helps company in reviewing their risk and

opportunity available in the market area.

Role of management accounting and system

There is various role of management accounting that are discussed in details below:

Planning long and short term:

It plays important role in identifying the future business and economic events so that company

can make long and short term aims related to strategies, accounting and market study. However,

when company have details regarding their financial and non-financial recorded it can easily

develop tactics to grab the opportunity or solve problems.

Developing management information system: The routine report is given to managerial

personal at all levels so that it can take corrective actions at the right time. Along with this,

management accountant helps in making the important decisions.

Maintaining optimum capital structure: It play major role in raising the funds and their

application. The accounts manager has to maintain the mix of equity and debts so that it can gain

tax benefits Moreover, it is risk because interest on debt has to be paid even if company is

running into loss (Raut and et.al., 2019). Thus, management account maintains the capital

structure and give due consideration to capital theories and trading equity.

Participation in management process:

The management accountant is occupied with the position of the company as manager has to

performs staff functions and give author to other members. It has to teach their executives to

control information and shift the important data as well report the clear information to external

parties.

within the company and authority can take decision in order to deal with harmful situation.

Relevance: Information is valuable for the company so management accounting should check

the best available resource so that it can take and implement decision for solving the issues.

Moreover, accounts should be related with past, present and future information, external and

internal data as well as financial and non-financial details.

Value: It has been estimated as management accounting links with company details and core

enterprise model that provide intensive knowledge regarding the macro economic and market

situation. Along with this, it deals with evaluating information along with identifying

opportunities and risks. Situational analysis helps company in reviewing their risk and

opportunity available in the market area.

Role of management accounting and system

There is various role of management accounting that are discussed in details below:

Planning long and short term:

It plays important role in identifying the future business and economic events so that company

can make long and short term aims related to strategies, accounting and market study. However,

when company have details regarding their financial and non-financial recorded it can easily

develop tactics to grab the opportunity or solve problems.

Developing management information system: The routine report is given to managerial

personal at all levels so that it can take corrective actions at the right time. Along with this,

management accountant helps in making the important decisions.

Maintaining optimum capital structure: It play major role in raising the funds and their

application. The accounts manager has to maintain the mix of equity and debts so that it can gain

tax benefits Moreover, it is risk because interest on debt has to be paid even if company is

running into loss (Raut and et.al., 2019). Thus, management account maintains the capital

structure and give due consideration to capital theories and trading equity.

Participation in management process:

The management accountant is occupied with the position of the company as manager has to

performs staff functions and give author to other members. It has to teach their executives to

control information and shift the important data as well report the clear information to external

parties.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

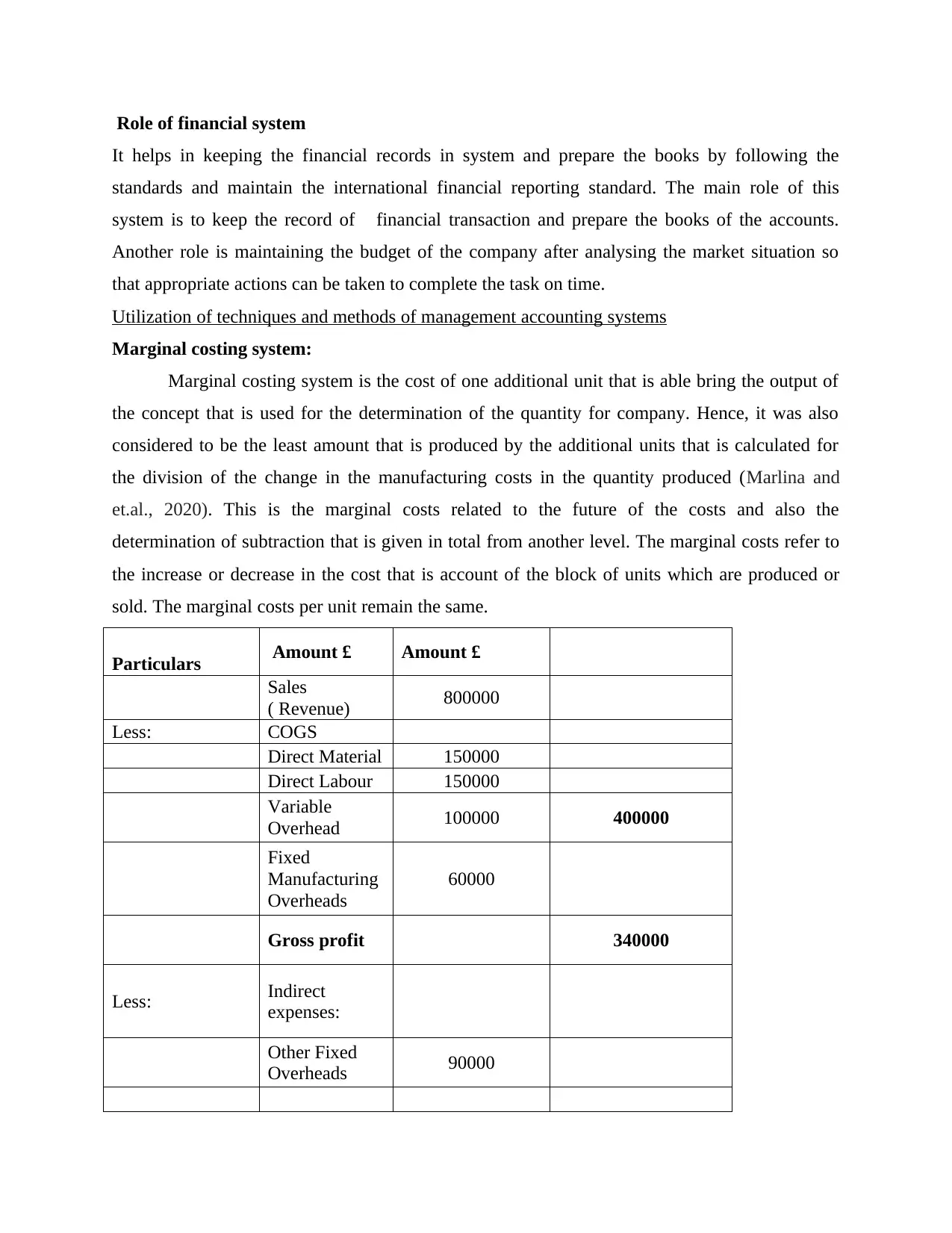

Role of financial system

It helps in keeping the financial records in system and prepare the books by following the

standards and maintain the international financial reporting standard. The main role of this

system is to keep the record of financial transaction and prepare the books of the accounts.

Another role is maintaining the budget of the company after analysing the market situation so

that appropriate actions can be taken to complete the task on time.

Utilization of techniques and methods of management accounting systems

Marginal costing system:

Marginal costing system is the cost of one additional unit that is able bring the output of

the concept that is used for the determination of the quantity for company. Hence, it was also

considered to be the least amount that is produced by the additional units that is calculated for

the division of the change in the manufacturing costs in the quantity produced (Marlina and

et.al., 2020). This is the marginal costs related to the future of the costs and also the

determination of subtraction that is given in total from another level. The marginal costs refer to

the increase or decrease in the cost that is account of the block of units which are produced or

sold. The marginal costs per unit remain the same.

Amount £ Amount £

Particulars

Sales

( Revenue) 800000

Less: COGS

Direct Material 150000

Direct Labour 150000

Variable

Overhead 100000 400000

Fixed

Manufacturing

Overheads

60000

Gross profit 340000

Less: Indirect

expenses:

Other Fixed

Overheads 90000

It helps in keeping the financial records in system and prepare the books by following the

standards and maintain the international financial reporting standard. The main role of this

system is to keep the record of financial transaction and prepare the books of the accounts.

Another role is maintaining the budget of the company after analysing the market situation so

that appropriate actions can be taken to complete the task on time.

Utilization of techniques and methods of management accounting systems

Marginal costing system:

Marginal costing system is the cost of one additional unit that is able bring the output of

the concept that is used for the determination of the quantity for company. Hence, it was also

considered to be the least amount that is produced by the additional units that is calculated for

the division of the change in the manufacturing costs in the quantity produced (Marlina and

et.al., 2020). This is the marginal costs related to the future of the costs and also the

determination of subtraction that is given in total from another level. The marginal costs refer to

the increase or decrease in the cost that is account of the block of units which are produced or

sold. The marginal costs per unit remain the same.

Amount £ Amount £

Particulars

Sales

( Revenue) 800000

Less: COGS

Direct Material 150000

Direct Labour 150000

Variable

Overhead 100000 400000

Fixed

Manufacturing

Overheads

60000

Gross profit 340000

Less: Indirect

expenses:

Other Fixed

Overheads 90000

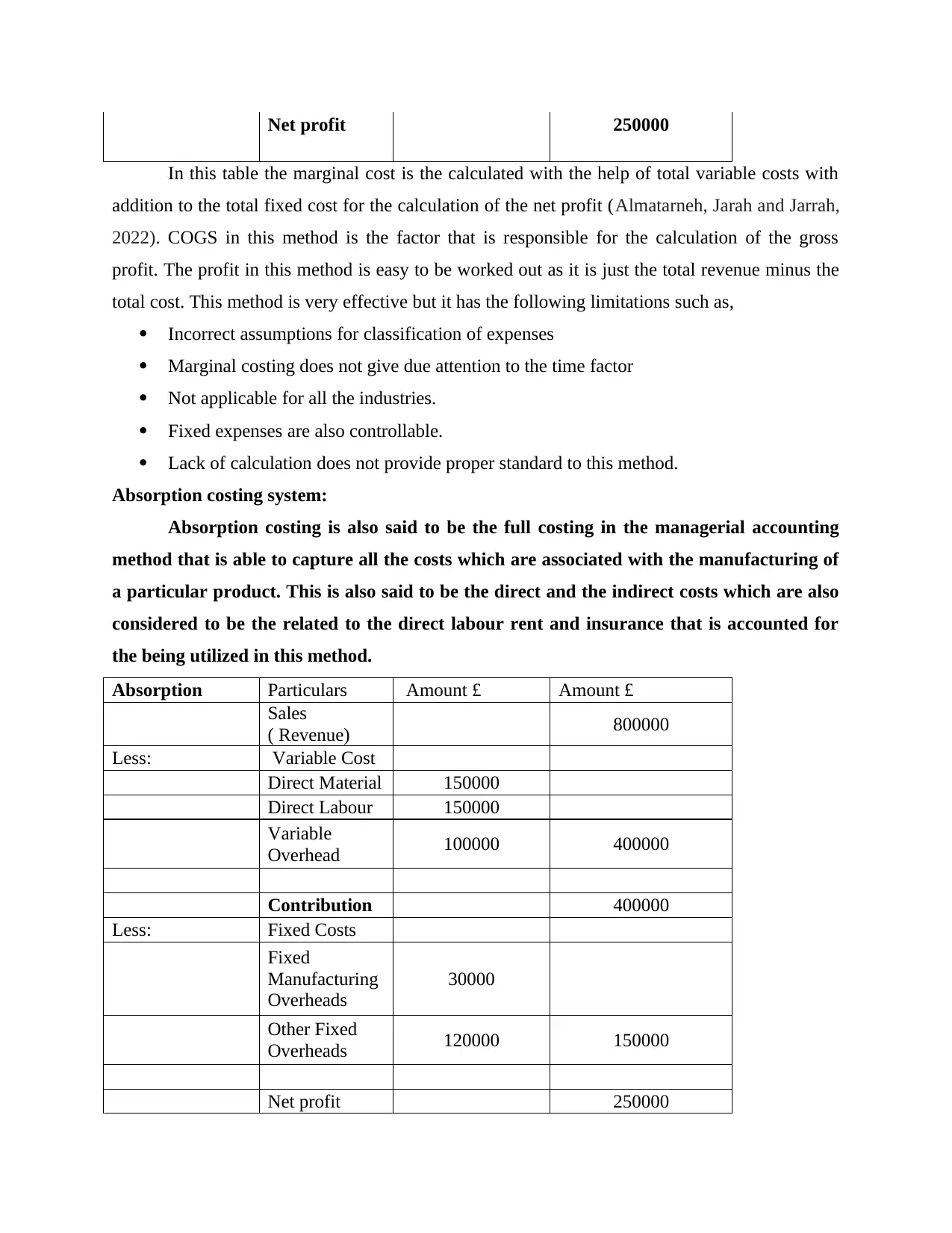

Net profit 250000

In this table the marginal cost is the calculated with the help of total variable costs with

addition to the total fixed cost for the calculation of the net profit (Almatarneh, Jarah and Jarrah,

2022). COGS in this method is the factor that is responsible for the calculation of the gross

profit. The profit in this method is easy to be worked out as it is just the total revenue minus the

total cost. This method is very effective but it has the following limitations such as,

Incorrect assumptions for classification of expenses

Marginal costing does not give due attention to the time factor

Not applicable for all the industries.

Fixed expenses are also controllable.

Lack of calculation does not provide proper standard to this method.

Absorption costing system:

Absorption costing is also said to be the full costing in the managerial accounting

method that is able to capture all the costs which are associated with the manufacturing of

a particular product. This is also said to be the direct and the indirect costs which are also

considered to be the related to the direct labour rent and insurance that is accounted for

the being utilized in this method.

Absorption Particulars Amount £ Amount £

Sales

( Revenue) 800000

Less: Variable Cost

Direct Material 150000

Direct Labour 150000

Variable

Overhead 100000 400000

Contribution 400000

Less: Fixed Costs

Fixed

Manufacturing

Overheads

30000

Other Fixed

Overheads 120000 150000

Net profit 250000

In this table the marginal cost is the calculated with the help of total variable costs with

addition to the total fixed cost for the calculation of the net profit (Almatarneh, Jarah and Jarrah,

2022). COGS in this method is the factor that is responsible for the calculation of the gross

profit. The profit in this method is easy to be worked out as it is just the total revenue minus the

total cost. This method is very effective but it has the following limitations such as,

Incorrect assumptions for classification of expenses

Marginal costing does not give due attention to the time factor

Not applicable for all the industries.

Fixed expenses are also controllable.

Lack of calculation does not provide proper standard to this method.

Absorption costing system:

Absorption costing is also said to be the full costing in the managerial accounting

method that is able to capture all the costs which are associated with the manufacturing of

a particular product. This is also said to be the direct and the indirect costs which are also

considered to be the related to the direct labour rent and insurance that is accounted for

the being utilized in this method.

Absorption Particulars Amount £ Amount £

Sales

( Revenue) 800000

Less: Variable Cost

Direct Material 150000

Direct Labour 150000

Variable

Overhead 100000 400000

Contribution 400000

Less: Fixed Costs

Fixed

Manufacturing

Overheads

30000

Other Fixed

Overheads 120000 150000

Net profit 250000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The difference between absorption costing and variable costing is that it uses the

allocation of fixed overhead costs that is present in each unit of product produced in the given

period. The allocation of the costing is also considered to be the product that is sold in the period

that influences the results. It has also been found that the absorption costing results in a relatively

higher net income that is compared to the variable costing.

Presenting ways management accounting is integrated within the organisation

The first phase is known as pre integration stage that involves gathering information so that it

communicated to other employees to accomplish the goals of successful integration. However, it

will be good for the company to maintain face to face and feasible form of communication.

Along with this, there is need to maintain smooth flow and continuous communication with

accounting staff and other employees so to reduce possible radiances at the early stage (Ratten

and et.al., 2020). This phase helps in analysing the list of priorities area so that immediate

actions can be taken for controlling continues flow of information.

The phase two aims at developing plan related to integration and some important steps are need

to be followed such as selection of integration., setting goals, preparing blue prints, developing

training charts so that roles and responsibility can be defining to installation team. Lastly,

report lines need to be made to decide on the integration options which need to be used for

implementation.

Phase three is known as implementation and choice in which integration strategy need to be

decide and what structure will be followed by MAS and control system. There are three

integration strategy which can be used by management accountant likes immediate observation,

gradual integration and two management accounting systems The crucial activates which

normally performed at this stage is co – ordination and closing flown of MAS system (Pal and

et.al., 2021).

Phase four is known as review and evaluation in which lessons are learned and feedback have

been taken so to improve future management integration. This stage basically includes

improvement of MAS and staff retention so that issues can be solve properly. However, action

plan is made in which strategies are identified to solve the issues relayed to accounting system.

allocation of fixed overhead costs that is present in each unit of product produced in the given

period. The allocation of the costing is also considered to be the product that is sold in the period

that influences the results. It has also been found that the absorption costing results in a relatively

higher net income that is compared to the variable costing.

Presenting ways management accounting is integrated within the organisation

The first phase is known as pre integration stage that involves gathering information so that it

communicated to other employees to accomplish the goals of successful integration. However, it

will be good for the company to maintain face to face and feasible form of communication.

Along with this, there is need to maintain smooth flow and continuous communication with

accounting staff and other employees so to reduce possible radiances at the early stage (Ratten

and et.al., 2020). This phase helps in analysing the list of priorities area so that immediate

actions can be taken for controlling continues flow of information.

The phase two aims at developing plan related to integration and some important steps are need

to be followed such as selection of integration., setting goals, preparing blue prints, developing

training charts so that roles and responsibility can be defining to installation team. Lastly,

report lines need to be made to decide on the integration options which need to be used for

implementation.

Phase three is known as implementation and choice in which integration strategy need to be

decide and what structure will be followed by MAS and control system. There are three

integration strategy which can be used by management accountant likes immediate observation,

gradual integration and two management accounting systems The crucial activates which

normally performed at this stage is co – ordination and closing flown of MAS system (Pal and

et.al., 2021).

Phase four is known as review and evaluation in which lessons are learned and feedback have

been taken so to improve future management integration. This stage basically includes

improvement of MAS and staff retention so that issues can be solve properly. However, action

plan is made in which strategies are identified to solve the issues relayed to accounting system.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Explaining benefits of the function to organization

Managerial accounting allow owner, employees and manger to make decision through

controlling the budget and comparing it with actual revenue as well as expense. It acts as

resource and planning tool that focuses on the future and present.

Continuous improvement: Accounting management function helps in improving the

effectiveness of system that results in good quality of services. Business mainly do this by

eliminating the waste and increasing the productivity.

Cost management: It contributes in enhancing the organization by developing cost

management system. Along with this, company do not have to prepare the budget of each

department instead it can do it at activity level like purchasing the inventory and payment receipt

process. However, when company can measure their costs and inputs it can reduce the costs

which add value to business (Kraus, Kraus and Osetskyi, 2020). It also measures and evaluates

the effectiveness of all major activities by developing innovative strategies that will enhance the

performance and productivity of firm. For example: If accounting manager of XY company

create a blue print of inventory purchasing process and match that with total costs. If it realizes

that it takes more cost with certain suppliers so it can reduce their order of size from these.

Quality Management: When accounting system of company measure the quality and monitor

the cost then it directly contributes to the improvement of organization. However, when the

quality and cost are measure then small changes can be identified which will positively

impact on the quality of company. Along with this, it focuses on the enhancing the quality at the

smallest level that do not directly involve production and helps company in continuously

meeting the change and building higher quality services.

Conclusion reflects application of management accounting

The function of management accounting can perform various functions so it is known as

multidimensional. It mainly contributes in improving internal activities of the business. It

contributes in providing details regarding non-financial and financial data to the manage which

contributes in taking the right decision for the growth of firm (Grab, Olaru and Gavril, 2019).

Moreover, it benefits organization by recording business transaction and deciding the goals for

short and long term. It also contributes in improving the decision of the company in effective

manner by addressing threats. Furthermore, it can be state that management accounting

Managerial accounting allow owner, employees and manger to make decision through

controlling the budget and comparing it with actual revenue as well as expense. It acts as

resource and planning tool that focuses on the future and present.

Continuous improvement: Accounting management function helps in improving the

effectiveness of system that results in good quality of services. Business mainly do this by

eliminating the waste and increasing the productivity.

Cost management: It contributes in enhancing the organization by developing cost

management system. Along with this, company do not have to prepare the budget of each

department instead it can do it at activity level like purchasing the inventory and payment receipt

process. However, when company can measure their costs and inputs it can reduce the costs

which add value to business (Kraus, Kraus and Osetskyi, 2020). It also measures and evaluates

the effectiveness of all major activities by developing innovative strategies that will enhance the

performance and productivity of firm. For example: If accounting manager of XY company

create a blue print of inventory purchasing process and match that with total costs. If it realizes

that it takes more cost with certain suppliers so it can reduce their order of size from these.

Quality Management: When accounting system of company measure the quality and monitor

the cost then it directly contributes to the improvement of organization. However, when the

quality and cost are measure then small changes can be identified which will positively

impact on the quality of company. Along with this, it focuses on the enhancing the quality at the

smallest level that do not directly involve production and helps company in continuously

meeting the change and building higher quality services.

Conclusion reflects application of management accounting

The function of management accounting can perform various functions so it is known as

multidimensional. It mainly contributes in improving internal activities of the business. It

contributes in providing details regarding non-financial and financial data to the manage which

contributes in taking the right decision for the growth of firm (Grab, Olaru and Gavril, 2019).

Moreover, it benefits organization by recording business transaction and deciding the goals for

short and long term. It also contributes in improving the decision of the company in effective

manner by addressing threats. Furthermore, it can be state that management accounting

ensure that inventory level is crucial and need to be manage properly so that cost can be

managing and hindrance can be minimum. It also ensures that business activity is in control

and work of employees can be analysed properly so that proper training can be given to them.

Thus, it can say that management accounting been fists company in many ways and develop

budgetary plan so that no misuse of capital is done.

PART 2

Comparing and contrasting three planning tools used in management accounting

Planning tools are mainly used for effective forecasting, with systematically planning for

eliminating the problems being analysed at the initial steps while transacting in business. The

three planning tools which are mainly used in management accounting are as follows:

Activity based budgeting

This planning tool is mainly used as the system which helps in recording and analysing

all the business activities and its costs. All the business activities which are incurring the cost is

mainly created potential way for attaining the efficiency (Rikhardsson and Yigitbasioglu, 2018).

This planning tool mainly helps in reducing the cost of the company by attaining more profit

from the sales. With using this tool in the business it creates the process more complex on nature

as it mainly depends on the previous defined budgets for the company in analysing the current

budgets. Thus, with using this tool it mainly benefits the company to forecast and make the new

budget with reviewing the previous years profits as by properly allocating the resources and

activities of the organization for attaining the efficiency.

Benefits limitations

The activity based budgeting mainly

helps in evaluating all the cost being

involved and eliminates the irrelevant

activity.

With evaluating this cost it helps in

attaining the competitiveness while

operating in the dynamic environment.

This tool mainly help in eliminating

Using this tool is complex in nature

which requires to employ the resources

in multiple activities.

This process is very time-consuming in

nature by employing wide range of

resources.

The activity based budgeting mainly

focuses for addressing and

managing and hindrance can be minimum. It also ensures that business activity is in control

and work of employees can be analysed properly so that proper training can be given to them.

Thus, it can say that management accounting been fists company in many ways and develop

budgetary plan so that no misuse of capital is done.

PART 2

Comparing and contrasting three planning tools used in management accounting

Planning tools are mainly used for effective forecasting, with systematically planning for

eliminating the problems being analysed at the initial steps while transacting in business. The

three planning tools which are mainly used in management accounting are as follows:

Activity based budgeting

This planning tool is mainly used as the system which helps in recording and analysing

all the business activities and its costs. All the business activities which are incurring the cost is

mainly created potential way for attaining the efficiency (Rikhardsson and Yigitbasioglu, 2018).

This planning tool mainly helps in reducing the cost of the company by attaining more profit

from the sales. With using this tool in the business it creates the process more complex on nature

as it mainly depends on the previous defined budgets for the company in analysing the current

budgets. Thus, with using this tool it mainly benefits the company to forecast and make the new

budget with reviewing the previous years profits as by properly allocating the resources and

activities of the organization for attaining the efficiency.

Benefits limitations

The activity based budgeting mainly

helps in evaluating all the cost being

involved and eliminates the irrelevant

activity.

With evaluating this cost it helps in

attaining the competitiveness while

operating in the dynamic environment.

This tool mainly help in eliminating

Using this tool is complex in nature

which requires to employ the resources

in multiple activities.

This process is very time-consuming in

nature by employing wide range of

resources.

The activity based budgeting mainly

focuses for addressing and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

while carrying the bottlenecks in the

business activities.

accomplishing the short term gaol of

the company.

Zero based budgeting

Zero based budgeting is mainly the process which helps in allocating this funds by

various activities for attaining efficiency of the particular programs. With using this the budgets

are mainly created with addressing the monetary needs for the coming month as this mainly

helps the managers in the company to attain and tackle the lowering cost of the company. This

tool is mainly known as the zero based budgeting due to incurring all the expenses from

maintaining the zero based. The main purpose is using the zero based budgeting as it helps in

aligning all strategic goals with the company and its resources as for making the annual budget.

Benefits limitation

With using this budgeting method it mainly

helps in looking each and every activity which

is representing the cash flow and compute the

operational cost which helps in attaining

accuracy.

This tool also helps in attaining efficiency by

allocating resources in proper manner.

With using this tool it helps in defining the

obstacle processes in the manufacturing and

the other departments

Using this tool in the business is time-

consuming processes.

It requires large number of employees to

anticipate and make the entire budget from the

starting.

Require high training expertise to maintaining

and make this budgeting in the business.

It is mainly used in determining the long term

goals in the company.

Cash budget

This tool is mainly used for estimating the cash flows being occurred in the business. It

helps in estimating the flow on the week, months on the yearly basis. The company mainly form

this budget as for estimating the cash flow as the in flows and outflows from the business. This

tool mainly helps in operating the business in the dynamic market by analysing the cash being

attained within the business. The main goals of making the budget in the business as it mainly

helps in determining and forecasting the cash available in the business which results in finding

out the earned revenues and the incurred expenses as suffering from the deficit or surplus. The

business activities.

accomplishing the short term gaol of

the company.

Zero based budgeting

Zero based budgeting is mainly the process which helps in allocating this funds by

various activities for attaining efficiency of the particular programs. With using this the budgets

are mainly created with addressing the monetary needs for the coming month as this mainly

helps the managers in the company to attain and tackle the lowering cost of the company. This

tool is mainly known as the zero based budgeting due to incurring all the expenses from

maintaining the zero based. The main purpose is using the zero based budgeting as it helps in

aligning all strategic goals with the company and its resources as for making the annual budget.

Benefits limitation

With using this budgeting method it mainly

helps in looking each and every activity which

is representing the cash flow and compute the

operational cost which helps in attaining

accuracy.

This tool also helps in attaining efficiency by

allocating resources in proper manner.

With using this tool it helps in defining the

obstacle processes in the manufacturing and

the other departments

Using this tool in the business is time-

consuming processes.

It requires large number of employees to

anticipate and make the entire budget from the

starting.

Require high training expertise to maintaining

and make this budgeting in the business.

It is mainly used in determining the long term

goals in the company.

Cash budget

This tool is mainly used for estimating the cash flows being occurred in the business. It

helps in estimating the flow on the week, months on the yearly basis. The company mainly form

this budget as for estimating the cash flow as the in flows and outflows from the business. This

tool mainly helps in operating the business in the dynamic market by analysing the cash being

attained within the business. The main goals of making the budget in the business as it mainly

helps in determining and forecasting the cash available in the business which results in finding

out the earned revenues and the incurred expenses as suffering from the deficit or surplus. The

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

company mainly uses the cash budgets and making plans for optimal utilizing the budgets. As by

investing the surplus and the minimum capital in the productive ventures for attaining the profits

in the company.

Benefits limitations

By making the cash budget in the

company it mainly helps in

communicating as b determining the

financial potion of the company while

operating in the dynamic business

environment.

With making the budgets it helps in

analysing the earned and remaining

surplus and deficits being faced by the

firm.

With making budget it helps in

avoiding an occurrence of debt.

It limits the spending power of the

company by determining the pertaining

cash.

With using the cash budget it mainly

creates the danger of theft by tracking

the cash movements.

It impacts in adopting the change in the

company also eliminating the earning

of rewards in the company.

Thus, management accounting tools are being used for accessing and providing the

necessary data which helps in effective controlling and efficiently working and developing the

processes which helps in simplifying all the decision as by detecting all the flaws and for

attaining long term growth in the business for scaling and leading to attain growth.

Comparing about the adaption and application of the management accounting and evaluating its

effectiveness in dealing the financial problems

Management accounting systems which are mainly used for responding to the financial

problems mainly includes:

Variance analysis

This tool is mainly used for measuring the planned and actual performance. This mainly

help in determining the deviations being occurred by analysing the gap of the actuality attained

and the planned positions (Maheshwari, Maheshwari and Maheshwari, 2021). The main aim of

this is to analyse the pricing of the raw materials, workers.

investing the surplus and the minimum capital in the productive ventures for attaining the profits

in the company.

Benefits limitations

By making the cash budget in the

company it mainly helps in

communicating as b determining the

financial potion of the company while

operating in the dynamic business

environment.

With making the budgets it helps in

analysing the earned and remaining

surplus and deficits being faced by the

firm.

With making budget it helps in

avoiding an occurrence of debt.

It limits the spending power of the

company by determining the pertaining

cash.

With using the cash budget it mainly

creates the danger of theft by tracking

the cash movements.

It impacts in adopting the change in the

company also eliminating the earning

of rewards in the company.

Thus, management accounting tools are being used for accessing and providing the

necessary data which helps in effective controlling and efficiently working and developing the

processes which helps in simplifying all the decision as by detecting all the flaws and for

attaining long term growth in the business for scaling and leading to attain growth.

Comparing about the adaption and application of the management accounting and evaluating its

effectiveness in dealing the financial problems

Management accounting systems which are mainly used for responding to the financial

problems mainly includes:

Variance analysis

This tool is mainly used for measuring the planned and actual performance. This mainly

help in determining the deviations being occurred by analysing the gap of the actuality attained

and the planned positions (Maheshwari, Maheshwari and Maheshwari, 2021). The main aim of

this is to analyse the pricing of the raw materials, workers.

Advantages: These systems helps in planning to attain profits by charging low cost and

managing all uncertainty.

Disadvantages: require expertise to use this system and it is very complex and length

process.

KPI( key performance indicators)

These tools are mainly used for analysing the improvement being made are attained or

not by analysing the growth (Banta, 2018). With using this system it helps in attaining the

desired results by responding effective to the problems being faced.

Advantages: This system mainly helps in attaining success by measuring the growth.

Disadvantages: By using this system it results in difficult to communicate the processes

which reduce the output attained.

Benchmarking

This system is mainly used for analysing the metrics used in the business which mainly

helps in defining the change to be adapted to attain the set target position by improving the

business performance (Gunarathne, Leeand Hitigala Kaluarachchilage, 2021). With using this it

helps in positively responding to the financial issues being faced.

Advantages: By using this system it helps in improving the operations by reducing the cost with

adopting all the practices to attain success.

disadvantage: as By using this system it mainly results in ever-increasing the dependency and

reduces the consumer satisfaction (Wang and et.al., 2019). Also, hinders in providing the full

information in the company.

Balance scorecard

This system is mainly us by the businesses to attain the set goals by identifying the

improvements and the lacking areas in the company to attain the set performance.

Advantages: as By using this system in th company it helps in aligning the goals by uisning

different methods for attaining and measuring success of the company. Further more this helps in

building and structuring the company in proper manner.

Disadvantages: with This system is rigid in nature as it is complicated to apply and measure the

success of the company.

Recommendations for the company

managing all uncertainty.

Disadvantages: require expertise to use this system and it is very complex and length

process.

KPI( key performance indicators)

These tools are mainly used for analysing the improvement being made are attained or

not by analysing the growth (Banta, 2018). With using this system it helps in attaining the

desired results by responding effective to the problems being faced.

Advantages: This system mainly helps in attaining success by measuring the growth.

Disadvantages: By using this system it results in difficult to communicate the processes

which reduce the output attained.

Benchmarking

This system is mainly used for analysing the metrics used in the business which mainly

helps in defining the change to be adapted to attain the set target position by improving the

business performance (Gunarathne, Leeand Hitigala Kaluarachchilage, 2021). With using this it

helps in positively responding to the financial issues being faced.

Advantages: By using this system it helps in improving the operations by reducing the cost with

adopting all the practices to attain success.

disadvantage: as By using this system it mainly results in ever-increasing the dependency and

reduces the consumer satisfaction (Wang and et.al., 2019). Also, hinders in providing the full

information in the company.

Balance scorecard

This system is mainly us by the businesses to attain the set goals by identifying the

improvements and the lacking areas in the company to attain the set performance.

Advantages: as By using this system in th company it helps in aligning the goals by uisning

different methods for attaining and measuring success of the company. Further more this helps in

building and structuring the company in proper manner.

Disadvantages: with This system is rigid in nature as it is complicated to apply and measure the

success of the company.

Recommendations for the company

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.