Management Accounting Report: Financial Problem Solutions for Business

VerifiedAdded on 2023/01/18

|18

|5545

|54

Report

AI Summary

This report provides a comprehensive overview of management accounting principles, focusing on their application within Brush Electrical Machines, a manufacturer of electrical generators. The report begins by defining management accounting and outlining its essential requirements, including financial reporting, resource allocation, and budgetary control, with specific examples like cost accounting, inventory management, and job costing systems. The report then delves into different methods of management accounting reporting, such as budget reports, accounts receivable aging reports, cost managerial accounting reports, and inventory and manufacturing reports. These reports are crucial for providing critical insights into business performance and operational efficiency. The core of the report involves calculating costs using absorption and marginal costing methods, providing a practical application of these techniques. Furthermore, the report explores the advantages and disadvantages of various planning tools used for budgetary control. Finally, the report examines how management accounting systems are used to resolve financial problems within an organization, providing a holistic view of the subject.

MANAGEMENT

ACCOUNTING

1

ACCOUNTING

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK1.............................................................................................................................................3

P1. Management accounting and provide essential requirements of various types of

management accounting system.............................................................................................3

P2 Explain different methods of management accounting reporting.....................................4

TASK2.............................................................................................................................................6

P3 Calculate cost by income statement using Absorption and Marginal costing...................6

TASK3.............................................................................................................................................7

P4 Advantages and Disadvantages of various planning tools for budgetary control.............7

TAKS4...........................................................................................................................................10

P5 Uses of management accounting systems in resolving financial problems in an

organisation..........................................................................................................................10

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

2

INTRODUCTION...........................................................................................................................3

TASK1.............................................................................................................................................3

P1. Management accounting and provide essential requirements of various types of

management accounting system.............................................................................................3

P2 Explain different methods of management accounting reporting.....................................4

TASK2.............................................................................................................................................6

P3 Calculate cost by income statement using Absorption and Marginal costing...................6

TASK3.............................................................................................................................................7

P4 Advantages and Disadvantages of various planning tools for budgetary control.............7

TAKS4...........................................................................................................................................10

P5 Uses of management accounting systems in resolving financial problems in an

organisation..........................................................................................................................10

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

2

INTRODUCTION

Accounting tool and technique is one of the crucial work for business in organisation.

This helps in presenting information related to finances to different users or stakeholders who

have keen interest in company and its operations. Therefore, term management accounting

relates to providing information and various resources which may be required to managers in

taking suitable decisions (Angelone, Neopost Technologies, 2015). Business organisation which

will be considered for this report is Brush Electrical Machines which is involved in manufacturer

of electrical generators. This report will contain understanding of management accounting. The

required cost will be calculated by using appropriate techniques of cost analyses so that income

statement can be prepared. This will make use of planning tools used in management accounting.

The last part of report will make comparisons of different ways through which companies are

adopting management accounting system in order to respond to different financial problems.

TASK1

P1. Management accounting and provide essential requirements of various types of management

accounting system.

Management Accounting: It is also known as managerial accounting and can be explained as

process of supporting managers with financial information for decision making. It is also use by

internal team of company because it uses statistical data to create base for decision making

process. It includes concepts and methods that are necessary to plan effectively for selecting best

alternatives from business decisions for evaluations of performance and controlling actions.

From Brush Electrical Machines point, there are many applications of management accounting

for instance, it helps in decision making, aids in planning process regularly, identify problematic

areas of operations and creates base for strategic management.

Essential requirements of various management accounting systems

Presentation of financial position: Application of various type of management

accounting systems provide useful information to managers which help them, in present

financial reports. Further, data collected from different systems help in take right

financial decisions.

Allocation of resources: there are various inventory management systems that help

managers in maintain an optimum level of stock within the organisation. EOQ is a tool

3

Accounting tool and technique is one of the crucial work for business in organisation.

This helps in presenting information related to finances to different users or stakeholders who

have keen interest in company and its operations. Therefore, term management accounting

relates to providing information and various resources which may be required to managers in

taking suitable decisions (Angelone, Neopost Technologies, 2015). Business organisation which

will be considered for this report is Brush Electrical Machines which is involved in manufacturer

of electrical generators. This report will contain understanding of management accounting. The

required cost will be calculated by using appropriate techniques of cost analyses so that income

statement can be prepared. This will make use of planning tools used in management accounting.

The last part of report will make comparisons of different ways through which companies are

adopting management accounting system in order to respond to different financial problems.

TASK1

P1. Management accounting and provide essential requirements of various types of management

accounting system.

Management Accounting: It is also known as managerial accounting and can be explained as

process of supporting managers with financial information for decision making. It is also use by

internal team of company because it uses statistical data to create base for decision making

process. It includes concepts and methods that are necessary to plan effectively for selecting best

alternatives from business decisions for evaluations of performance and controlling actions.

From Brush Electrical Machines point, there are many applications of management accounting

for instance, it helps in decision making, aids in planning process regularly, identify problematic

areas of operations and creates base for strategic management.

Essential requirements of various management accounting systems

Presentation of financial position: Application of various type of management

accounting systems provide useful information to managers which help them, in present

financial reports. Further, data collected from different systems help in take right

financial decisions.

Allocation of resources: there are various inventory management systems that help

managers in maintain an optimum level of stock within the organisation. EOQ is a tool

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

that provide useful information to managers and help in identify the right time to reorder

the stocks to maintain an appropriate level of stock required to fulfil the requirements of

key customers. All this improve efficiency and reduce cost of company’s operations and

at the same time help in achieve set goals and objectives of the enterprise.

Budgetary control: This is another significant tool that support in identify the future risks

associated with company’s project. All this help managers be aware about future risks

that are about to rise and help in formulate contingency plans for effective management.

Below is some management accounting which are used by Brush Electrical Machines in its

decision making process Cost accounting system: It is also known as product costing system which is a structure

used by business to find out cost of products for controlling cost, valuation of stock and

profit analysis(Appelbaum and et. al., 2017). Main benefit of this system to Brush

Electrical Machines is that it estimate accurate cost to measure profit margins and areas

of operations which are profitable to company. It also finds out value of stock, work-in-

progress and finished products of for financial statement which helps in decision making. Inventory management system: It is combination of procedures and technology that

monitors, maintain stock of company like assets, raw material or finished products.

Without this system goods will be in imbalance so to keep harmony in flow and record of

every stock inventory management system is necessary. In Brush Electrical Machines it

is used to maintained integrity in record of assets, location of item, information of

supplier and value of stock for generators. Job costing system: It is special costing method which is applied to execute specific

customer order work in strict manner. It totally depends on numbers of orders from

consumer so delivery is made on immediate basis (Chenhall and Moers, 2015). Main aim

of this accounting system is to estimate cost and profit or loss for each processes. Brush

Electrical Machines applies this system to find out which area of operation is more or less

profitable and to compare actual cost with budgeted cost of electric generators. There is a

specific process which is followed by organisation to use this accounting system:

following are the steps:

Receiving enquiry: It include procedure of get the customer’s views about quality of products

and time period require to complete.

4

the stocks to maintain an appropriate level of stock required to fulfil the requirements of

key customers. All this improve efficiency and reduce cost of company’s operations and

at the same time help in achieve set goals and objectives of the enterprise.

Budgetary control: This is another significant tool that support in identify the future risks

associated with company’s project. All this help managers be aware about future risks

that are about to rise and help in formulate contingency plans for effective management.

Below is some management accounting which are used by Brush Electrical Machines in its

decision making process Cost accounting system: It is also known as product costing system which is a structure

used by business to find out cost of products for controlling cost, valuation of stock and

profit analysis(Appelbaum and et. al., 2017). Main benefit of this system to Brush

Electrical Machines is that it estimate accurate cost to measure profit margins and areas

of operations which are profitable to company. It also finds out value of stock, work-in-

progress and finished products of for financial statement which helps in decision making. Inventory management system: It is combination of procedures and technology that

monitors, maintain stock of company like assets, raw material or finished products.

Without this system goods will be in imbalance so to keep harmony in flow and record of

every stock inventory management system is necessary. In Brush Electrical Machines it

is used to maintained integrity in record of assets, location of item, information of

supplier and value of stock for generators. Job costing system: It is special costing method which is applied to execute specific

customer order work in strict manner. It totally depends on numbers of orders from

consumer so delivery is made on immediate basis (Chenhall and Moers, 2015). Main aim

of this accounting system is to estimate cost and profit or loss for each processes. Brush

Electrical Machines applies this system to find out which area of operation is more or less

profitable and to compare actual cost with budgeted cost of electric generators. There is a

specific process which is followed by organisation to use this accounting system:

following are the steps:

Receiving enquiry: It include procedure of get the customer’s views about quality of products

and time period require to complete.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Estimate the price: This is done on the basis of preferences of customers.

Receive order: In this, order is places after getting assurance from clients.

Production order: As the name implies, in this order for production takes place.

Cost recording: Under this, each and every cost which take place during production of

product is recorded.

Completion of job: under this, report is offered to accountant to carry out final costing.

Price Optimisation system: It consists of mathematical analysis that determine how

customer will react to different prices. It also combines information of cost and stock

level to suggests price that will increase profits for company. This model helps

organisation to find out pricing strategies for specific customer segments and their

responses to change in price. Brush Electrical Machines uses this model to estimate initial

price, promotional pricing and discount pricing for electric generators. This will help

company to attract customer and generate revenue that will effect profitability.

P2 Explain different methods of management accounting reporting

Accounting reports: These are essential part to make sure that company have adequate

information about every processes and operations. A detailed report is prepared every quarter to

provide overall view of business performance. These are important for new product line of Brush

Electrical Machines so that management will get critical understanding about electrical generates

from these reports. Below are some reports that are prepared regularly by Brush Electrical

machine: Budget Report: It is the most fundamental report in management accounting which

helps businesses to understand and control cost in processes and operations. It estimates

budgets through analysing past years expenses and earnings for unseen situations that

might arise (Chiarini and Vagnoni, 2015). It creates budget for each department and

overall business to achieve organisational goals or objectives while controlling its

expenses under estimated budget. In Brush Electrical Machines this report helps

managers to provide extra benefits to productive employees, reduce cost and negotiate

with suppliers. This report will help management to keep record of cost involved in

every process and evaluate performance by comparing actual cost with estimated one.

5

Receive order: In this, order is places after getting assurance from clients.

Production order: As the name implies, in this order for production takes place.

Cost recording: Under this, each and every cost which take place during production of

product is recorded.

Completion of job: under this, report is offered to accountant to carry out final costing.

Price Optimisation system: It consists of mathematical analysis that determine how

customer will react to different prices. It also combines information of cost and stock

level to suggests price that will increase profits for company. This model helps

organisation to find out pricing strategies for specific customer segments and their

responses to change in price. Brush Electrical Machines uses this model to estimate initial

price, promotional pricing and discount pricing for electric generators. This will help

company to attract customer and generate revenue that will effect profitability.

P2 Explain different methods of management accounting reporting

Accounting reports: These are essential part to make sure that company have adequate

information about every processes and operations. A detailed report is prepared every quarter to

provide overall view of business performance. These are important for new product line of Brush

Electrical Machines so that management will get critical understanding about electrical generates

from these reports. Below are some reports that are prepared regularly by Brush Electrical

machine: Budget Report: It is the most fundamental report in management accounting which

helps businesses to understand and control cost in processes and operations. It estimates

budgets through analysing past years expenses and earnings for unseen situations that

might arise (Chiarini and Vagnoni, 2015). It creates budget for each department and

overall business to achieve organisational goals or objectives while controlling its

expenses under estimated budget. In Brush Electrical Machines this report helps

managers to provide extra benefits to productive employees, reduce cost and negotiate

with suppliers. This report will help management to keep record of cost involved in

every process and evaluate performance by comparing actual cost with estimated one.

5

Account Receivable Aging Reports: This report is important tool for all those businesses

which extend credit to customer and manages cash flow. It includes different columns

for bills of 30, 60 and 90 days or more to monitor defaulters on time. This will help

Brush Electrical Machines to strict its credit policy, analyse regularly receivables

accounts, keep check on defaulters and to maintain cash flow (Cooper, Ezzamel and Qu,

2017). There are always some bad debts in accounting period of business but company

should not make this as habit. Cost Managerial Accounting Reports: It calculates cost of product that business

manufacture that includes raw material, labour and other costs. It provides summary of

information related to expenses incur to manufacture product that helps in determining

its selling price. Brush Electrical Machines prepare this report to estimate profit

margins, waste stock, per hour labour cost and variable cost to have clear understanding

of all expenses incurred in generators. Through this report company is able to distribute

resources for optimal uses. Inventory and Manufacturing Report: Brush Electrical Machines which manufacture

electrical generators and want to have zero defects in processes, this report will be

valuable. It includes costs of inventory, waste material, labour charges, other variables

involves in production process (Cooper, 2017). In electrical generators this will

highlight area of operations where improvement is needed and take corrective actions

within time. It also identifies departments which performs efficiently and effectively to

reward their efforts in achieving organisational gaols.

In order to perform business activities integration of management accounting systems and

reports is necessary to provide organisation with information needed for operations. These

reports and systems work together so that business processes will be carried out with ease. In

context with Brush Electrical Machines it uses different accounting systems like inventory

management and cost accounting system to find out cost and estimate profits margins. These

reports helps in establishing base for comparing actual performance with estimated one and take

corrective actions in case of deviations. If these systems and reports will be used simultaneously,

it is not possible for Brush Electrical Machines to gather information about each operations and

6

which extend credit to customer and manages cash flow. It includes different columns

for bills of 30, 60 and 90 days or more to monitor defaulters on time. This will help

Brush Electrical Machines to strict its credit policy, analyse regularly receivables

accounts, keep check on defaulters and to maintain cash flow (Cooper, Ezzamel and Qu,

2017). There are always some bad debts in accounting period of business but company

should not make this as habit. Cost Managerial Accounting Reports: It calculates cost of product that business

manufacture that includes raw material, labour and other costs. It provides summary of

information related to expenses incur to manufacture product that helps in determining

its selling price. Brush Electrical Machines prepare this report to estimate profit

margins, waste stock, per hour labour cost and variable cost to have clear understanding

of all expenses incurred in generators. Through this report company is able to distribute

resources for optimal uses. Inventory and Manufacturing Report: Brush Electrical Machines which manufacture

electrical generators and want to have zero defects in processes, this report will be

valuable. It includes costs of inventory, waste material, labour charges, other variables

involves in production process (Cooper, 2017). In electrical generators this will

highlight area of operations where improvement is needed and take corrective actions

within time. It also identifies departments which performs efficiently and effectively to

reward their efforts in achieving organisational gaols.

In order to perform business activities integration of management accounting systems and

reports is necessary to provide organisation with information needed for operations. These

reports and systems work together so that business processes will be carried out with ease. In

context with Brush Electrical Machines it uses different accounting systems like inventory

management and cost accounting system to find out cost and estimate profits margins. These

reports helps in establishing base for comparing actual performance with estimated one and take

corrective actions in case of deviations. If these systems and reports will be used simultaneously,

it is not possible for Brush Electrical Machines to gather information about each operations and

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

find out its profits margins. This will reduce organisational overall profitability in terms of

revenue and productivity, hence they are important.

TASK2

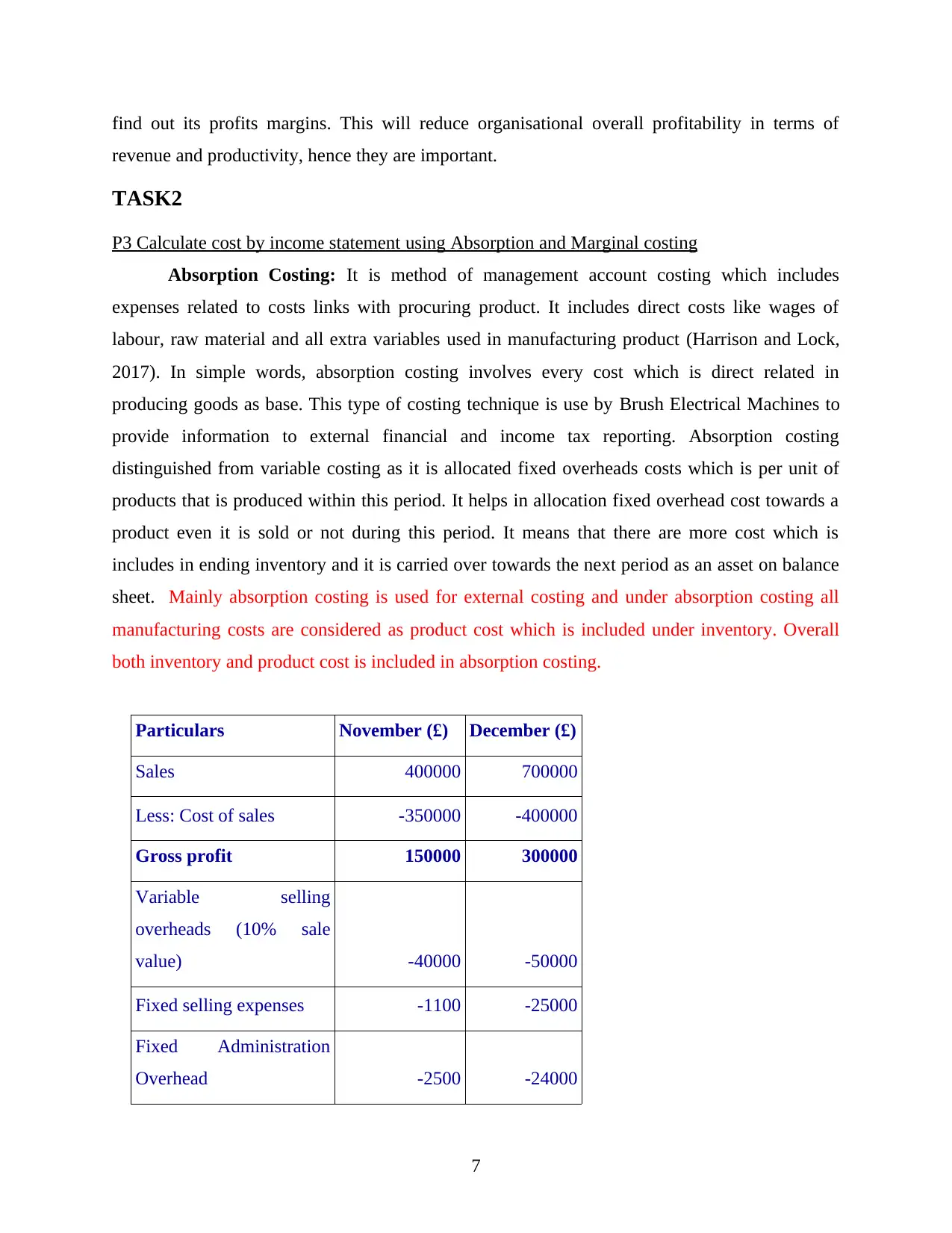

P3 Calculate cost by income statement using Absorption and Marginal costing

Absorption Costing: It is method of management account costing which includes

expenses related to costs links with procuring product. It includes direct costs like wages of

labour, raw material and all extra variables used in manufacturing product (Harrison and Lock,

2017). In simple words, absorption costing involves every cost which is direct related in

producing goods as base. This type of costing technique is use by Brush Electrical Machines to

provide information to external financial and income tax reporting. Absorption costing

distinguished from variable costing as it is allocated fixed overheads costs which is per unit of

products that is produced within this period. It helps in allocation fixed overhead cost towards a

product even it is sold or not during this period. It means that there are more cost which is

includes in ending inventory and it is carried over towards the next period as an asset on balance

sheet. Mainly absorption costing is used for external costing and under absorption costing all

manufacturing costs are considered as product cost which is included under inventory. Overall

both inventory and product cost is included in absorption costing.

Particulars November (£) December (£)

Sales 400000 700000

Less: Cost of sales -350000 -400000

Gross profit 150000 300000

Variable selling

overheads (10% sale

value) -40000 -50000

Fixed selling expenses -1100 -25000

Fixed Administration

Overhead -2500 -24000

7

revenue and productivity, hence they are important.

TASK2

P3 Calculate cost by income statement using Absorption and Marginal costing

Absorption Costing: It is method of management account costing which includes

expenses related to costs links with procuring product. It includes direct costs like wages of

labour, raw material and all extra variables used in manufacturing product (Harrison and Lock,

2017). In simple words, absorption costing involves every cost which is direct related in

producing goods as base. This type of costing technique is use by Brush Electrical Machines to

provide information to external financial and income tax reporting. Absorption costing

distinguished from variable costing as it is allocated fixed overheads costs which is per unit of

products that is produced within this period. It helps in allocation fixed overhead cost towards a

product even it is sold or not during this period. It means that there are more cost which is

includes in ending inventory and it is carried over towards the next period as an asset on balance

sheet. Mainly absorption costing is used for external costing and under absorption costing all

manufacturing costs are considered as product cost which is included under inventory. Overall

both inventory and product cost is included in absorption costing.

Particulars November (£) December (£)

Sales 400000 700000

Less: Cost of sales -350000 -400000

Gross profit 150000 300000

Variable selling

overheads (10% sale

value) -40000 -50000

Fixed selling expenses -1100 -25000

Fixed Administration

Overhead -2500 -24000

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Under/overabsorbed prod

expenses -4000 -21000

Net Profit 102400 180000

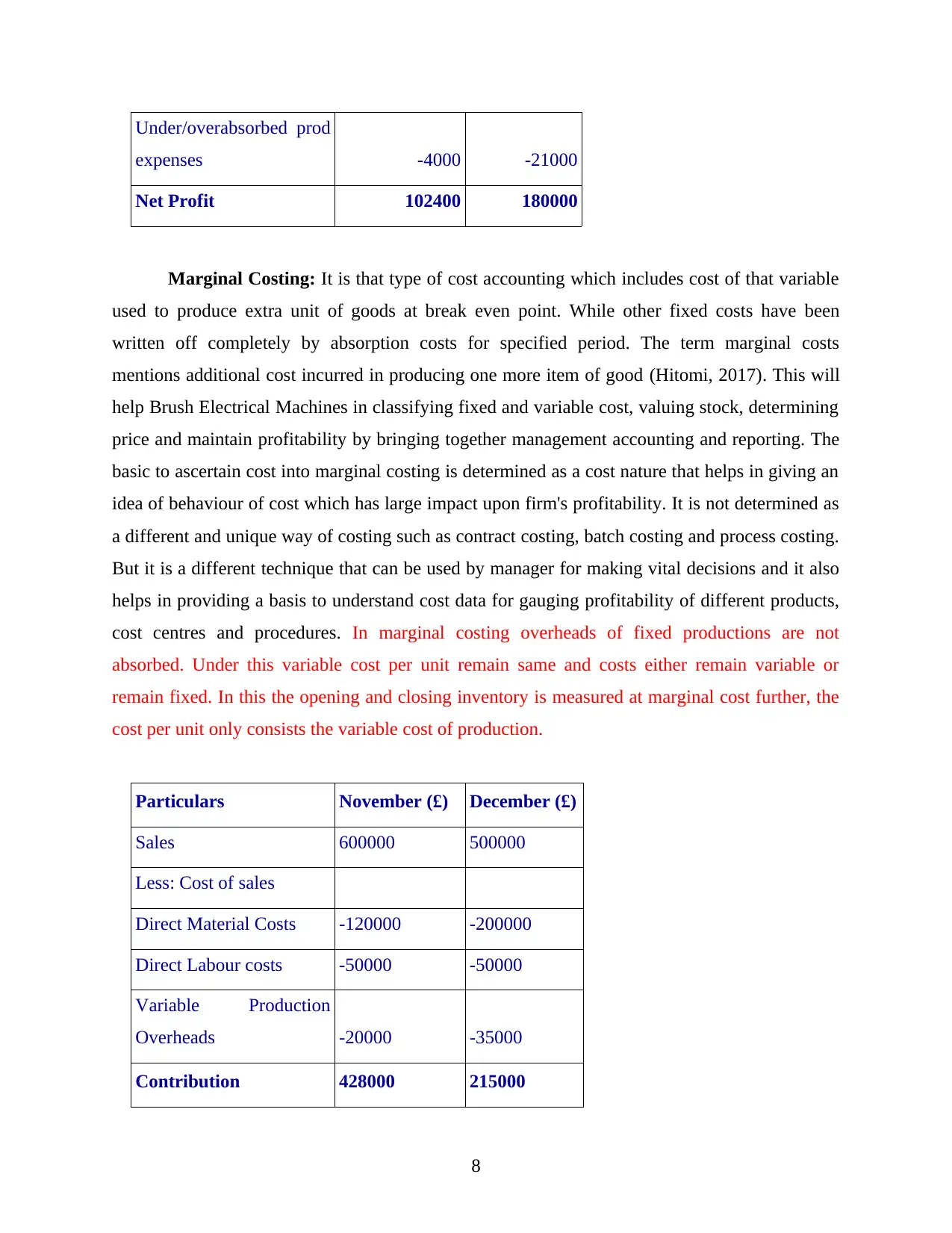

Marginal Costing: It is that type of cost accounting which includes cost of that variable

used to produce extra unit of goods at break even point. While other fixed costs have been

written off completely by absorption costs for specified period. The term marginal costs

mentions additional cost incurred in producing one more item of good (Hitomi, 2017). This will

help Brush Electrical Machines in classifying fixed and variable cost, valuing stock, determining

price and maintain profitability by bringing together management accounting and reporting. The

basic to ascertain cost into marginal costing is determined as a cost nature that helps in giving an

idea of behaviour of cost which has large impact upon firm's profitability. It is not determined as

a different and unique way of costing such as contract costing, batch costing and process costing.

But it is a different technique that can be used by manager for making vital decisions and it also

helps in providing a basis to understand cost data for gauging profitability of different products,

cost centres and procedures. In marginal costing overheads of fixed productions are not

absorbed. Under this variable cost per unit remain same and costs either remain variable or

remain fixed. In this the opening and closing inventory is measured at marginal cost further, the

cost per unit only consists the variable cost of production.

Particulars November (£) December (£)

Sales 600000 500000

Less: Cost of sales

Direct Material Costs -120000 -200000

Direct Labour costs -50000 -50000

Variable Production

Overheads -20000 -35000

Contribution 428000 215000

8

expenses -4000 -21000

Net Profit 102400 180000

Marginal Costing: It is that type of cost accounting which includes cost of that variable

used to produce extra unit of goods at break even point. While other fixed costs have been

written off completely by absorption costs for specified period. The term marginal costs

mentions additional cost incurred in producing one more item of good (Hitomi, 2017). This will

help Brush Electrical Machines in classifying fixed and variable cost, valuing stock, determining

price and maintain profitability by bringing together management accounting and reporting. The

basic to ascertain cost into marginal costing is determined as a cost nature that helps in giving an

idea of behaviour of cost which has large impact upon firm's profitability. It is not determined as

a different and unique way of costing such as contract costing, batch costing and process costing.

But it is a different technique that can be used by manager for making vital decisions and it also

helps in providing a basis to understand cost data for gauging profitability of different products,

cost centres and procedures. In marginal costing overheads of fixed productions are not

absorbed. Under this variable cost per unit remain same and costs either remain variable or

remain fixed. In this the opening and closing inventory is measured at marginal cost further, the

cost per unit only consists the variable cost of production.

Particulars November (£) December (£)

Sales 600000 500000

Less: Cost of sales

Direct Material Costs -120000 -200000

Direct Labour costs -50000 -50000

Variable Production

Overheads -20000 -35000

Contribution 428000 215000

8

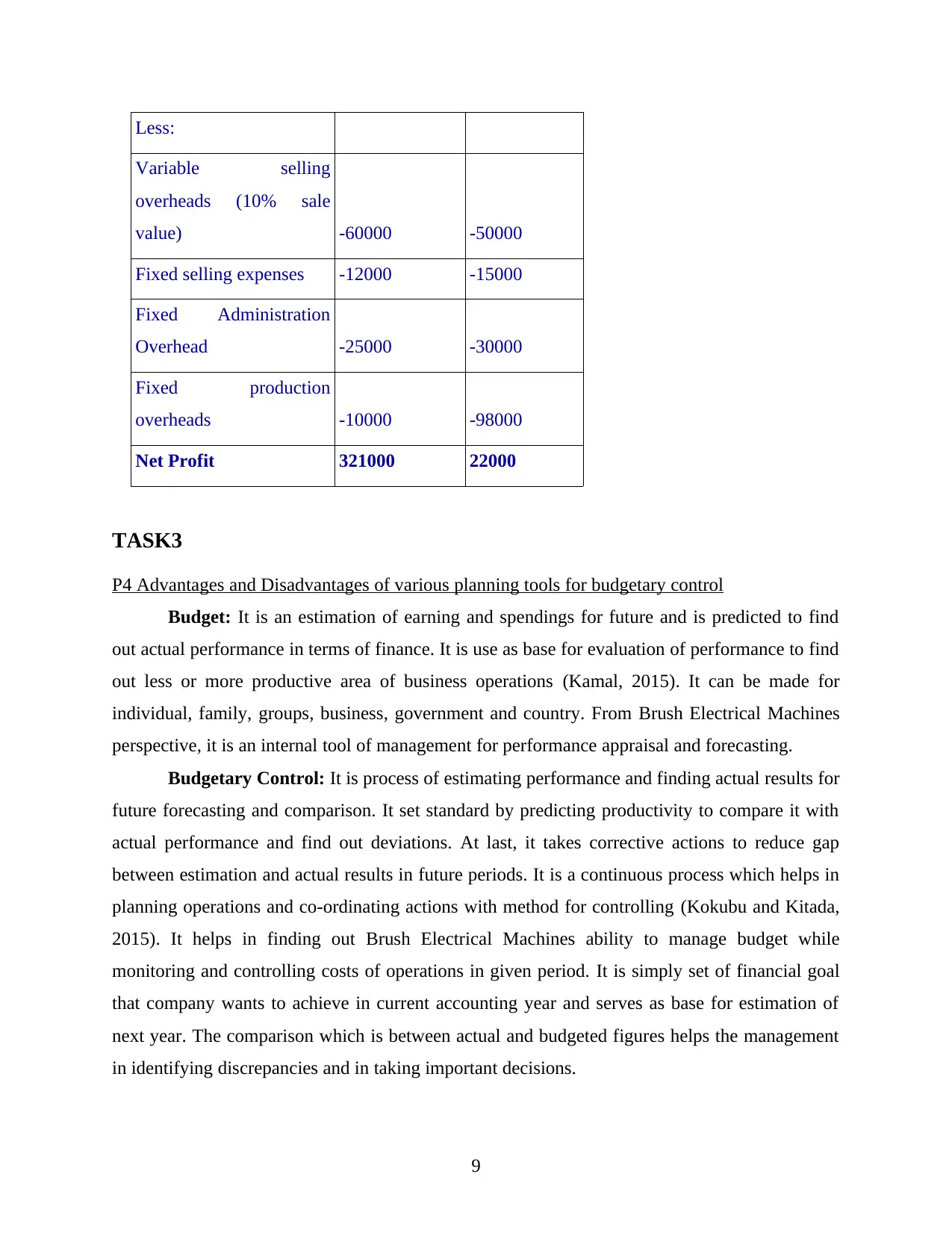

Less:

Variable selling

overheads (10% sale

value) -60000 -50000

Fixed selling expenses -12000 -15000

Fixed Administration

Overhead -25000 -30000

Fixed production

overheads -10000 -98000

Net Profit 321000 22000

TASK3

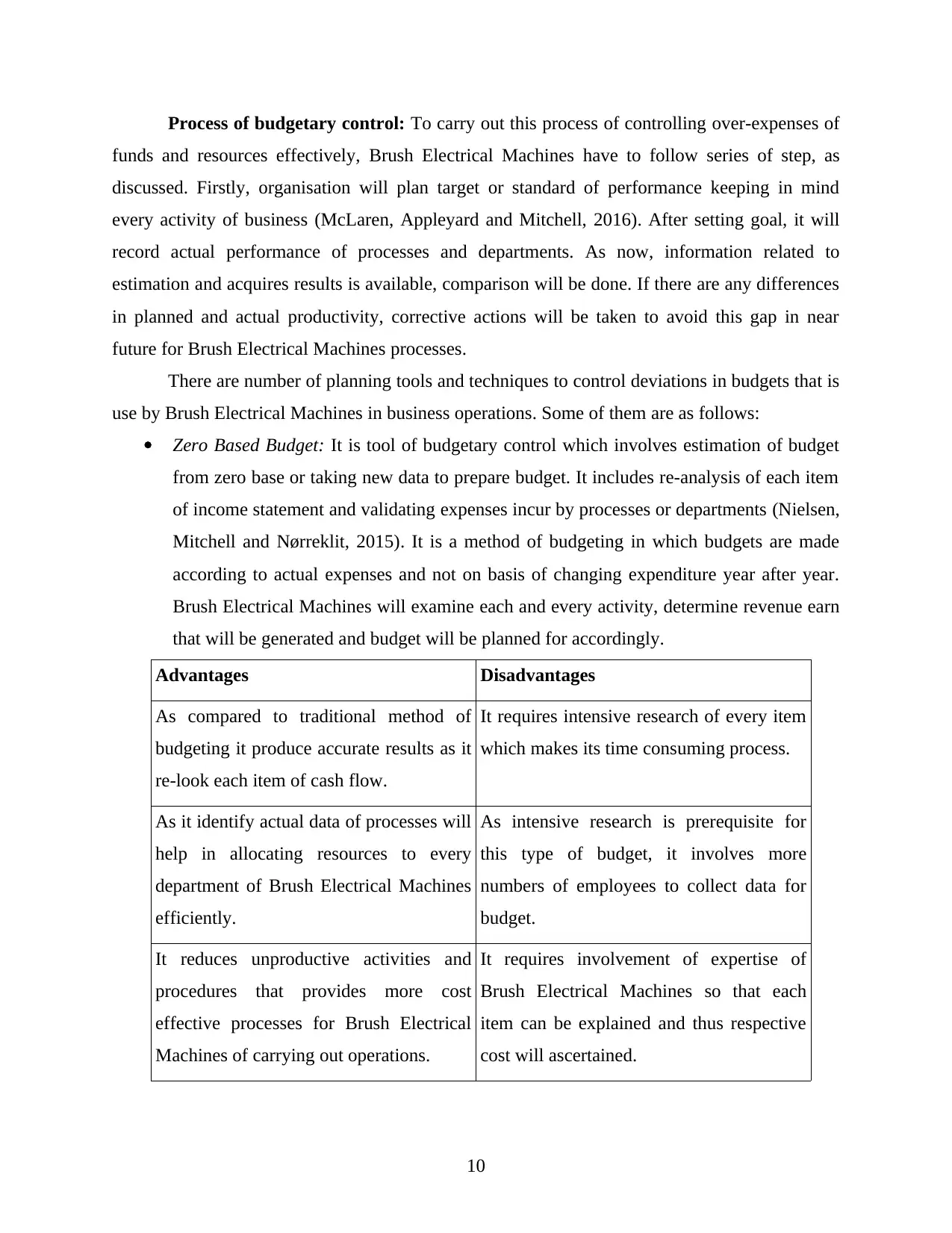

P4 Advantages and Disadvantages of various planning tools for budgetary control

Budget: It is an estimation of earning and spendings for future and is predicted to find

out actual performance in terms of finance. It is use as base for evaluation of performance to find

out less or more productive area of business operations (Kamal, 2015). It can be made for

individual, family, groups, business, government and country. From Brush Electrical Machines

perspective, it is an internal tool of management for performance appraisal and forecasting.

Budgetary Control: It is process of estimating performance and finding actual results for

future forecasting and comparison. It set standard by predicting productivity to compare it with

actual performance and find out deviations. At last, it takes corrective actions to reduce gap

between estimation and actual results in future periods. It is a continuous process which helps in

planning operations and co-ordinating actions with method for controlling (Kokubu and Kitada,

2015). It helps in finding out Brush Electrical Machines ability to manage budget while

monitoring and controlling costs of operations in given period. It is simply set of financial goal

that company wants to achieve in current accounting year and serves as base for estimation of

next year. The comparison which is between actual and budgeted figures helps the management

in identifying discrepancies and in taking important decisions.

9

Variable selling

overheads (10% sale

value) -60000 -50000

Fixed selling expenses -12000 -15000

Fixed Administration

Overhead -25000 -30000

Fixed production

overheads -10000 -98000

Net Profit 321000 22000

TASK3

P4 Advantages and Disadvantages of various planning tools for budgetary control

Budget: It is an estimation of earning and spendings for future and is predicted to find

out actual performance in terms of finance. It is use as base for evaluation of performance to find

out less or more productive area of business operations (Kamal, 2015). It can be made for

individual, family, groups, business, government and country. From Brush Electrical Machines

perspective, it is an internal tool of management for performance appraisal and forecasting.

Budgetary Control: It is process of estimating performance and finding actual results for

future forecasting and comparison. It set standard by predicting productivity to compare it with

actual performance and find out deviations. At last, it takes corrective actions to reduce gap

between estimation and actual results in future periods. It is a continuous process which helps in

planning operations and co-ordinating actions with method for controlling (Kokubu and Kitada,

2015). It helps in finding out Brush Electrical Machines ability to manage budget while

monitoring and controlling costs of operations in given period. It is simply set of financial goal

that company wants to achieve in current accounting year and serves as base for estimation of

next year. The comparison which is between actual and budgeted figures helps the management

in identifying discrepancies and in taking important decisions.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Process of budgetary control: To carry out this process of controlling over-expenses of

funds and resources effectively, Brush Electrical Machines have to follow series of step, as

discussed. Firstly, organisation will plan target or standard of performance keeping in mind

every activity of business (McLaren, Appleyard and Mitchell, 2016). After setting goal, it will

record actual performance of processes and departments. As now, information related to

estimation and acquires results is available, comparison will be done. If there are any differences

in planned and actual productivity, corrective actions will be taken to avoid this gap in near

future for Brush Electrical Machines processes.

There are number of planning tools and techniques to control deviations in budgets that is

use by Brush Electrical Machines in business operations. Some of them are as follows:

Zero Based Budget: It is tool of budgetary control which involves estimation of budget

from zero base or taking new data to prepare budget. It includes re-analysis of each item

of income statement and validating expenses incur by processes or departments (Nielsen,

Mitchell and Nørreklit, 2015). It is a method of budgeting in which budgets are made

according to actual expenses and not on basis of changing expenditure year after year.

Brush Electrical Machines will examine each and every activity, determine revenue earn

that will be generated and budget will be planned for accordingly.

Advantages Disadvantages

As compared to traditional method of

budgeting it produce accurate results as it

re-look each item of cash flow.

It requires intensive research of every item

which makes its time consuming process.

As it identify actual data of processes will

help in allocating resources to every

department of Brush Electrical Machines

efficiently.

As intensive research is prerequisite for

this type of budget, it involves more

numbers of employees to collect data for

budget.

It reduces unproductive activities and

procedures that provides more cost

effective processes for Brush Electrical

Machines of carrying out operations.

It requires involvement of expertise of

Brush Electrical Machines so that each

item can be explained and thus respective

cost will ascertained.

10

funds and resources effectively, Brush Electrical Machines have to follow series of step, as

discussed. Firstly, organisation will plan target or standard of performance keeping in mind

every activity of business (McLaren, Appleyard and Mitchell, 2016). After setting goal, it will

record actual performance of processes and departments. As now, information related to

estimation and acquires results is available, comparison will be done. If there are any differences

in planned and actual productivity, corrective actions will be taken to avoid this gap in near

future for Brush Electrical Machines processes.

There are number of planning tools and techniques to control deviations in budgets that is

use by Brush Electrical Machines in business operations. Some of them are as follows:

Zero Based Budget: It is tool of budgetary control which involves estimation of budget

from zero base or taking new data to prepare budget. It includes re-analysis of each item

of income statement and validating expenses incur by processes or departments (Nielsen,

Mitchell and Nørreklit, 2015). It is a method of budgeting in which budgets are made

according to actual expenses and not on basis of changing expenditure year after year.

Brush Electrical Machines will examine each and every activity, determine revenue earn

that will be generated and budget will be planned for accordingly.

Advantages Disadvantages

As compared to traditional method of

budgeting it produce accurate results as it

re-look each item of cash flow.

It requires intensive research of every item

which makes its time consuming process.

As it identify actual data of processes will

help in allocating resources to every

department of Brush Electrical Machines

efficiently.

As intensive research is prerequisite for

this type of budget, it involves more

numbers of employees to collect data for

budget.

It reduces unproductive activities and

procedures that provides more cost

effective processes for Brush Electrical

Machines of carrying out operations.

It requires involvement of expertise of

Brush Electrical Machines so that each

item can be explained and thus respective

cost will ascertained.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

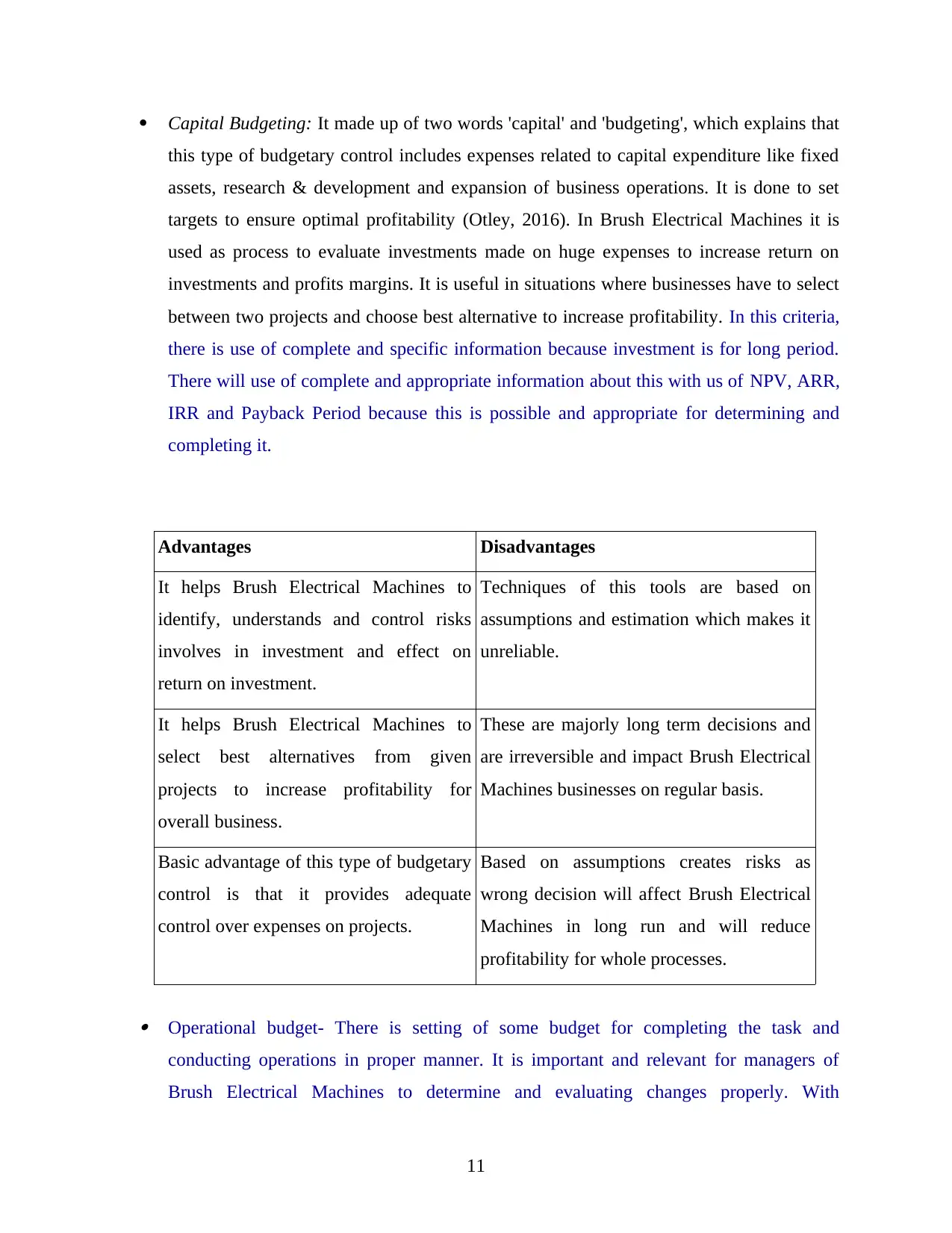

Capital Budgeting: It made up of two words 'capital' and 'budgeting', which explains that

this type of budgetary control includes expenses related to capital expenditure like fixed

assets, research & development and expansion of business operations. It is done to set

targets to ensure optimal profitability (Otley, 2016). In Brush Electrical Machines it is

used as process to evaluate investments made on huge expenses to increase return on

investments and profits margins. It is useful in situations where businesses have to select

between two projects and choose best alternative to increase profitability. In this criteria,

there is use of complete and specific information because investment is for long period.

There will use of complete and appropriate information about this with us of NPV, ARR,

IRR and Payback Period because this is possible and appropriate for determining and

completing it.

Advantages Disadvantages

It helps Brush Electrical Machines to

identify, understands and control risks

involves in investment and effect on

return on investment.

Techniques of this tools are based on

assumptions and estimation which makes it

unreliable.

It helps Brush Electrical Machines to

select best alternatives from given

projects to increase profitability for

overall business.

These are majorly long term decisions and

are irreversible and impact Brush Electrical

Machines businesses on regular basis.

Basic advantage of this type of budgetary

control is that it provides adequate

control over expenses on projects.

Based on assumptions creates risks as

wrong decision will affect Brush Electrical

Machines in long run and will reduce

profitability for whole processes.

Operational budget- There is setting of some budget for completing the task and

conducting operations in proper manner. It is important and relevant for managers of

Brush Electrical Machines to determine and evaluating changes properly. With

11

this type of budgetary control includes expenses related to capital expenditure like fixed

assets, research & development and expansion of business operations. It is done to set

targets to ensure optimal profitability (Otley, 2016). In Brush Electrical Machines it is

used as process to evaluate investments made on huge expenses to increase return on

investments and profits margins. It is useful in situations where businesses have to select

between two projects and choose best alternative to increase profitability. In this criteria,

there is use of complete and specific information because investment is for long period.

There will use of complete and appropriate information about this with us of NPV, ARR,

IRR and Payback Period because this is possible and appropriate for determining and

completing it.

Advantages Disadvantages

It helps Brush Electrical Machines to

identify, understands and control risks

involves in investment and effect on

return on investment.

Techniques of this tools are based on

assumptions and estimation which makes it

unreliable.

It helps Brush Electrical Machines to

select best alternatives from given

projects to increase profitability for

overall business.

These are majorly long term decisions and

are irreversible and impact Brush Electrical

Machines businesses on regular basis.

Basic advantage of this type of budgetary

control is that it provides adequate

control over expenses on projects.

Based on assumptions creates risks as

wrong decision will affect Brush Electrical

Machines in long run and will reduce

profitability for whole processes.

Operational budget- There is setting of some budget for completing the task and

conducting operations in proper manner. It is important and relevant for managers of

Brush Electrical Machines to determine and evaluating changes properly. With

11

performing activities, it will be easy for completing and making activities proper. In order

to determine and evaluate operational budget, managers of Brush Electrical Machines

must use of forecasting, variance analysis, standard costing, flexible budgeting, etc. with

the help of which proper analysis is possible for considering it.

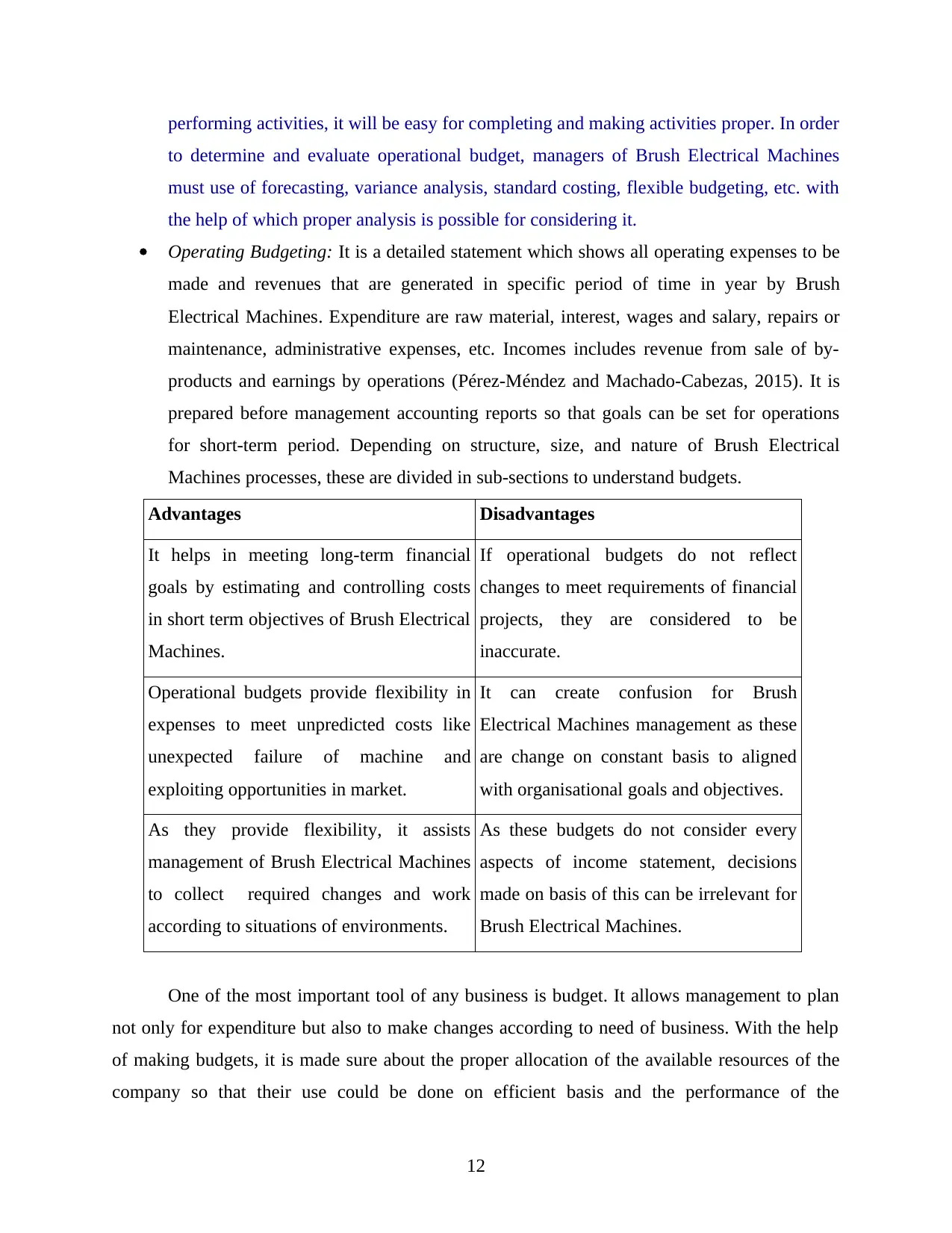

Operating Budgeting: It is a detailed statement which shows all operating expenses to be

made and revenues that are generated in specific period of time in year by Brush

Electrical Machines. Expenditure are raw material, interest, wages and salary, repairs or

maintenance, administrative expenses, etc. Incomes includes revenue from sale of by-

products and earnings by operations (Pérez-Méndez and Machado-Cabezas, 2015). It is

prepared before management accounting reports so that goals can be set for operations

for short-term period. Depending on structure, size, and nature of Brush Electrical

Machines processes, these are divided in sub-sections to understand budgets.

Advantages Disadvantages

It helps in meeting long-term financial

goals by estimating and controlling costs

in short term objectives of Brush Electrical

Machines.

If operational budgets do not reflect

changes to meet requirements of financial

projects, they are considered to be

inaccurate.

Operational budgets provide flexibility in

expenses to meet unpredicted costs like

unexpected failure of machine and

exploiting opportunities in market.

It can create confusion for Brush

Electrical Machines management as these

are change on constant basis to aligned

with organisational goals and objectives.

As they provide flexibility, it assists

management of Brush Electrical Machines

to collect required changes and work

according to situations of environments.

As these budgets do not consider every

aspects of income statement, decisions

made on basis of this can be irrelevant for

Brush Electrical Machines.

One of the most important tool of any business is budget. It allows management to plan

not only for expenditure but also to make changes according to need of business. With the help

of making budgets, it is made sure about the proper allocation of the available resources of the

company so that their use could be done on efficient basis and the performance of the

12

to determine and evaluate operational budget, managers of Brush Electrical Machines

must use of forecasting, variance analysis, standard costing, flexible budgeting, etc. with

the help of which proper analysis is possible for considering it.

Operating Budgeting: It is a detailed statement which shows all operating expenses to be

made and revenues that are generated in specific period of time in year by Brush

Electrical Machines. Expenditure are raw material, interest, wages and salary, repairs or

maintenance, administrative expenses, etc. Incomes includes revenue from sale of by-

products and earnings by operations (Pérez-Méndez and Machado-Cabezas, 2015). It is

prepared before management accounting reports so that goals can be set for operations

for short-term period. Depending on structure, size, and nature of Brush Electrical

Machines processes, these are divided in sub-sections to understand budgets.

Advantages Disadvantages

It helps in meeting long-term financial

goals by estimating and controlling costs

in short term objectives of Brush Electrical

Machines.

If operational budgets do not reflect

changes to meet requirements of financial

projects, they are considered to be

inaccurate.

Operational budgets provide flexibility in

expenses to meet unpredicted costs like

unexpected failure of machine and

exploiting opportunities in market.

It can create confusion for Brush

Electrical Machines management as these

are change on constant basis to aligned

with organisational goals and objectives.

As they provide flexibility, it assists

management of Brush Electrical Machines

to collect required changes and work

according to situations of environments.

As these budgets do not consider every

aspects of income statement, decisions

made on basis of this can be irrelevant for

Brush Electrical Machines.

One of the most important tool of any business is budget. It allows management to plan

not only for expenditure but also to make changes according to need of business. With the help

of making budgets, it is made sure about the proper allocation of the available resources of the

company so that their use could be done on efficient basis and the performance of the

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.