Management Accounting: Cost Analysis, Variances, and Costing Methods

VerifiedAdded on 2023/06/10

|13

|2941

|499

Report

AI Summary

This management accounting report provides a detailed analysis of various costing methods and variance calculations. It begins with an introduction to management accounting, highlighting its role in decision-making. The report uses the high-low method to evaluate variable costs and fixed operating costs, and calculates total expected costs at different occupancy rates. It also computes total variable cost, total fixed cost, and average costs per unit at varying activity levels. Furthermore, the report includes schedules for the cost of goods sold and an income statement, followed by a thorough variance analysis, including materials price variance, materials usage variance, labor rate variance, labor efficiency variance, and variable overhead variances. The report discusses potential causes for material usage and labor efficiency variances, and examines different types of variances in relation to work performance. Finally, it analyzes relevant costs for make-or-buy decisions, considering opportunity costs and incremental costs to determine the most cost-effective approach.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................1

Question 1........................................................................................................................................1

Question 2........................................................................................................................................3

(i)..................................................................................................................................................3

(ii)................................................................................................................................................4

Question 4........................................................................................................................................4

Question 5........................................................................................................................................6

(a).................................................................................................................................................6

(b).................................................................................................................................................7

(c).................................................................................................................................................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................1

Question 1........................................................................................................................................1

Question 2........................................................................................................................................3

(i)..................................................................................................................................................3

(ii)................................................................................................................................................4

Question 4........................................................................................................................................4

Question 5........................................................................................................................................6

(a).................................................................................................................................................6

(b).................................................................................................................................................7

(c).................................................................................................................................................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

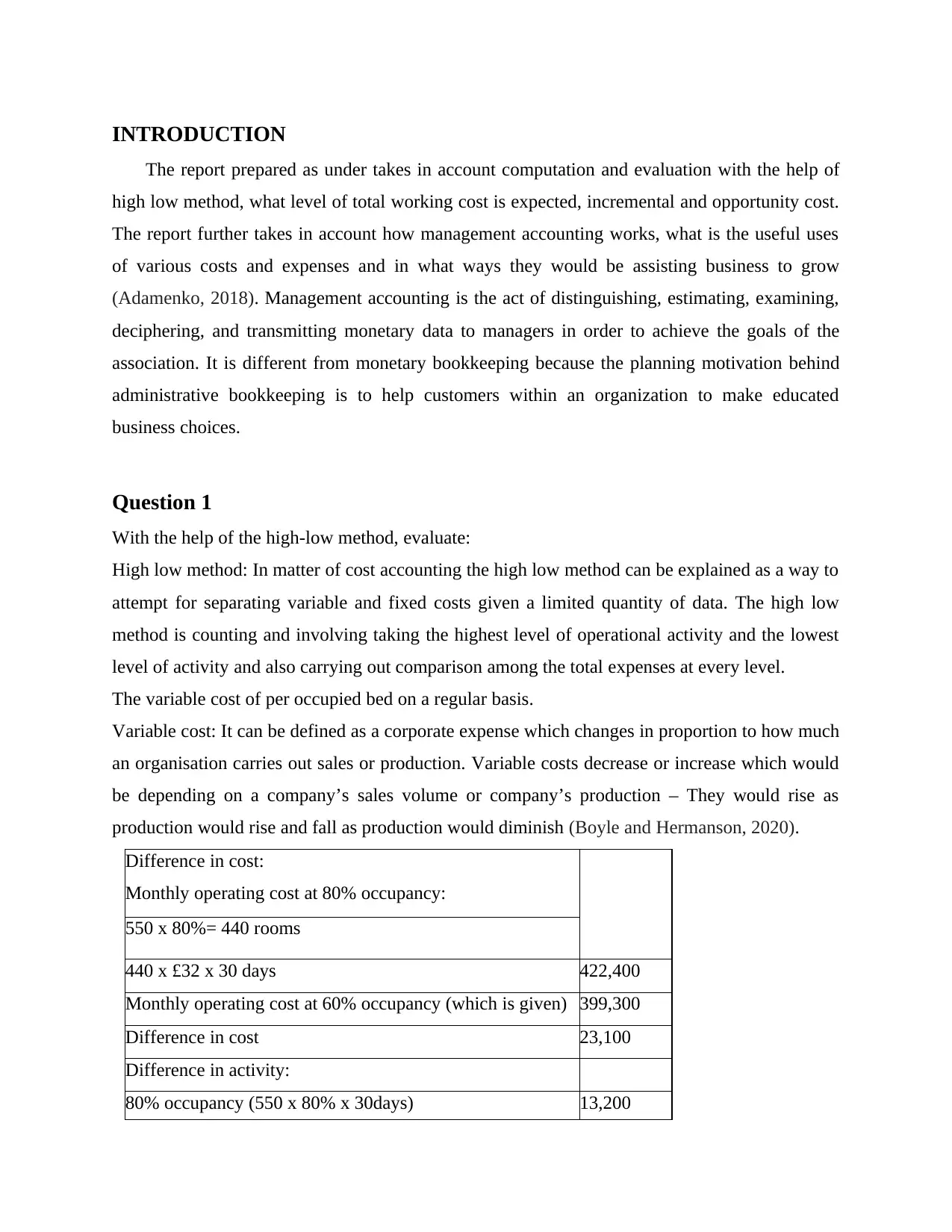

INTRODUCTION

The report prepared as under takes in account computation and evaluation with the help of

high low method, what level of total working cost is expected, incremental and opportunity cost.

The report further takes in account how management accounting works, what is the useful uses

of various costs and expenses and in what ways they would be assisting business to grow

(Adamenko, 2018). Management accounting is the act of distinguishing, estimating, examining,

deciphering, and transmitting monetary data to managers in order to achieve the goals of the

association. It is different from monetary bookkeeping because the planning motivation behind

administrative bookkeeping is to help customers within an organization to make educated

business choices.

Question 1

With the help of the high-low method, evaluate:

High low method: In matter of cost accounting the high low method can be explained as a way to

attempt for separating variable and fixed costs given a limited quantity of data. The high low

method is counting and involving taking the highest level of operational activity and the lowest

level of activity and also carrying out comparison among the total expenses at every level.

The variable cost of per occupied bed on a regular basis.

Variable cost: It can be defined as a corporate expense which changes in proportion to how much

an organisation carries out sales or production. Variable costs decrease or increase which would

be depending on a company’s sales volume or company’s production – They would rise as

production would rise and fall as production would diminish (Boyle and Hermanson, 2020).

Difference in cost:

Monthly operating cost at 80% occupancy:

550 x 80%= 440 rooms

440 x £32 x 30 days 422,400

Monthly operating cost at 60% occupancy (which is given) 399,300

Difference in cost 23,100

Difference in activity:

80% occupancy (550 x 80% x 30days) 13,200

The report prepared as under takes in account computation and evaluation with the help of

high low method, what level of total working cost is expected, incremental and opportunity cost.

The report further takes in account how management accounting works, what is the useful uses

of various costs and expenses and in what ways they would be assisting business to grow

(Adamenko, 2018). Management accounting is the act of distinguishing, estimating, examining,

deciphering, and transmitting monetary data to managers in order to achieve the goals of the

association. It is different from monetary bookkeeping because the planning motivation behind

administrative bookkeeping is to help customers within an organization to make educated

business choices.

Question 1

With the help of the high-low method, evaluate:

High low method: In matter of cost accounting the high low method can be explained as a way to

attempt for separating variable and fixed costs given a limited quantity of data. The high low

method is counting and involving taking the highest level of operational activity and the lowest

level of activity and also carrying out comparison among the total expenses at every level.

The variable cost of per occupied bed on a regular basis.

Variable cost: It can be defined as a corporate expense which changes in proportion to how much

an organisation carries out sales or production. Variable costs decrease or increase which would

be depending on a company’s sales volume or company’s production – They would rise as

production would rise and fall as production would diminish (Boyle and Hermanson, 2020).

Difference in cost:

Monthly operating cost at 80% occupancy:

550 x 80%= 440 rooms

440 x £32 x 30 days 422,400

Monthly operating cost at 60% occupancy (which is given) 399,300

Difference in cost 23,100

Difference in activity:

80% occupancy (550 x 80% x 30days) 13,200

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

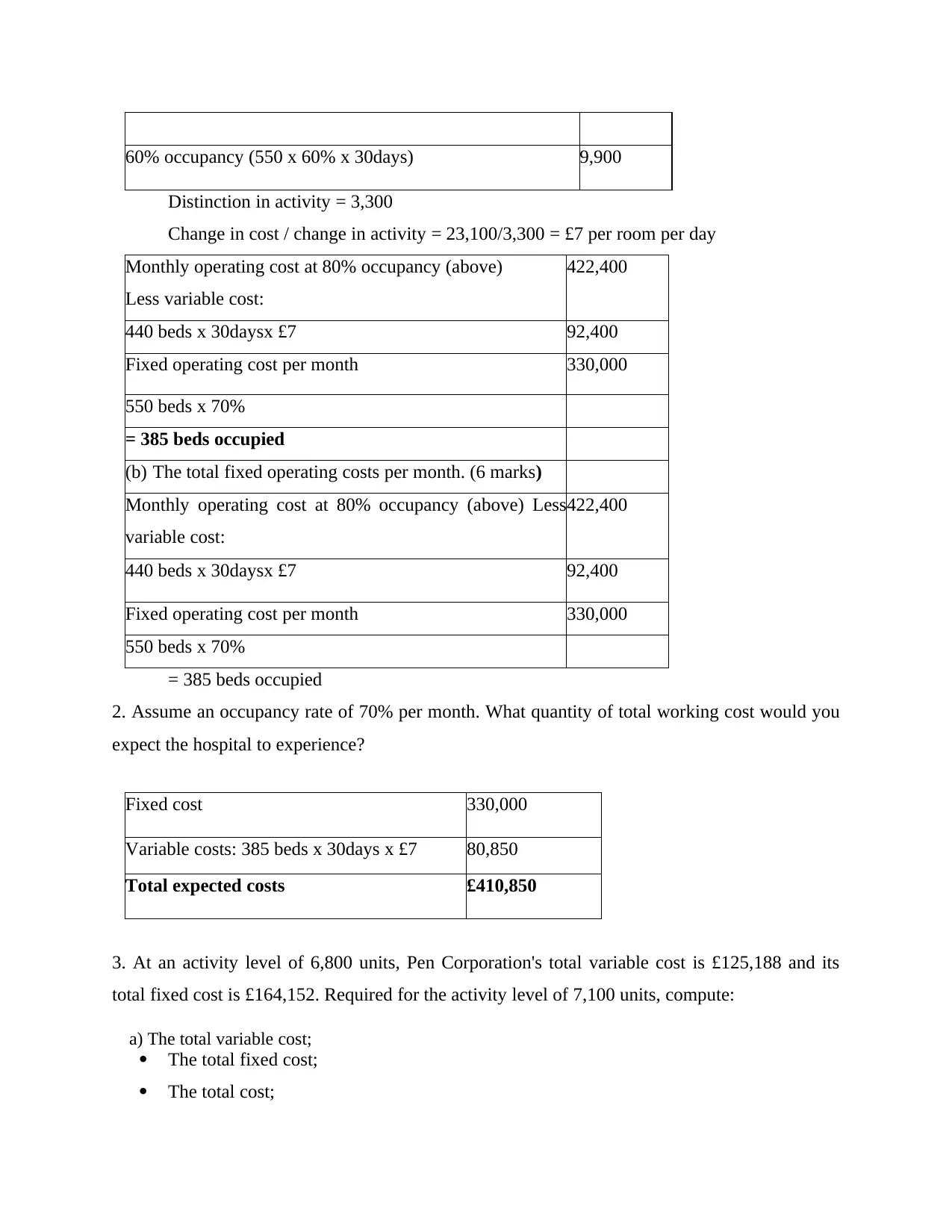

60% occupancy (550 x 60% x 30days) 9,900

Distinction in activity = 3,300

Change in cost / change in activity = 23,100/3,300 = £7 per room per day

Monthly operating cost at 80% occupancy (above)

Less variable cost:

422,400

440 beds x 30daysx £7 92,400

Fixed operating cost per month 330,000

550 beds x 70%

= 385 beds occupied

(b) The total fixed operating costs per month. (6 marks)

Monthly operating cost at 80% occupancy (above) Less

variable cost:

422,400

440 beds x 30daysx £7 92,400

Fixed operating cost per month 330,000

550 beds x 70%

= 385 beds occupied

2. Assume an occupancy rate of 70% per month. What quantity of total working cost would you

expect the hospital to experience?

Fixed cost 330,000

Variable costs: 385 beds x 30days x £7 80,850

Total expected costs £410,850

3. At an activity level of 6,800 units, Pen Corporation's total variable cost is £125,188 and its

total fixed cost is £164,152. Required for the activity level of 7,100 units, compute:

a) The total variable cost;

The total fixed cost;

The total cost;

Distinction in activity = 3,300

Change in cost / change in activity = 23,100/3,300 = £7 per room per day

Monthly operating cost at 80% occupancy (above)

Less variable cost:

422,400

440 beds x 30daysx £7 92,400

Fixed operating cost per month 330,000

550 beds x 70%

= 385 beds occupied

(b) The total fixed operating costs per month. (6 marks)

Monthly operating cost at 80% occupancy (above) Less

variable cost:

422,400

440 beds x 30daysx £7 92,400

Fixed operating cost per month 330,000

550 beds x 70%

= 385 beds occupied

2. Assume an occupancy rate of 70% per month. What quantity of total working cost would you

expect the hospital to experience?

Fixed cost 330,000

Variable costs: 385 beds x 30days x £7 80,850

Total expected costs £410,850

3. At an activity level of 6,800 units, Pen Corporation's total variable cost is £125,188 and its

total fixed cost is £164,152. Required for the activity level of 7,100 units, compute:

a) The total variable cost;

The total fixed cost;

The total cost;

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

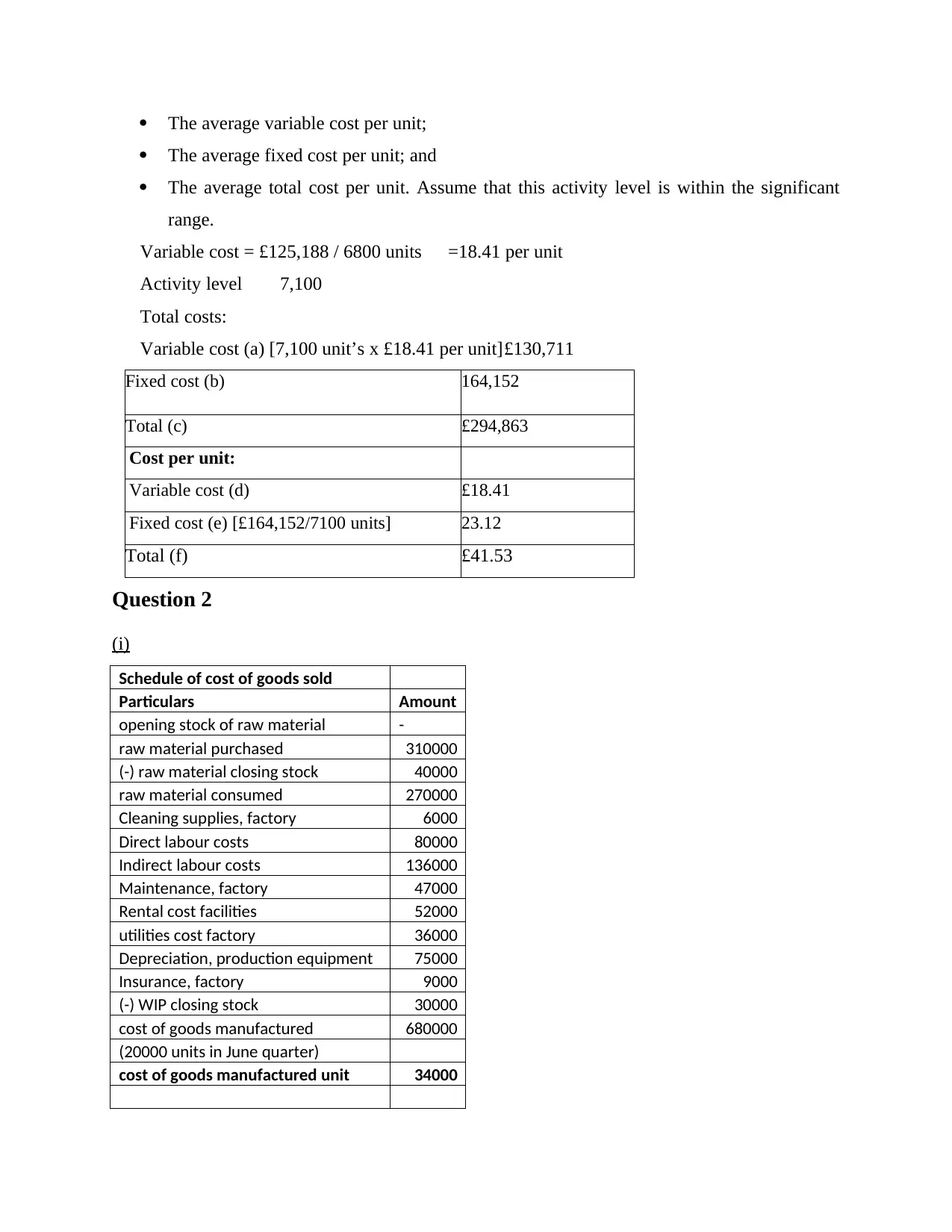

The average variable cost per unit;

The average fixed cost per unit; and

The average total cost per unit. Assume that this activity level is within the significant

range.

Variable cost = £125,188 / 6800 units =18.41 per unit

Activity level 7,100

Total costs:

Variable cost (a) [7,100 unit’s x £18.41 per unit]£130,711

Fixed cost (b) 164,152

Total (c) £294,863

Cost per unit:

Variable cost (d) £18.41

Fixed cost (e) [£164,152/7100 units] 23.12

Total (f) £41.53

Question 2

(i)

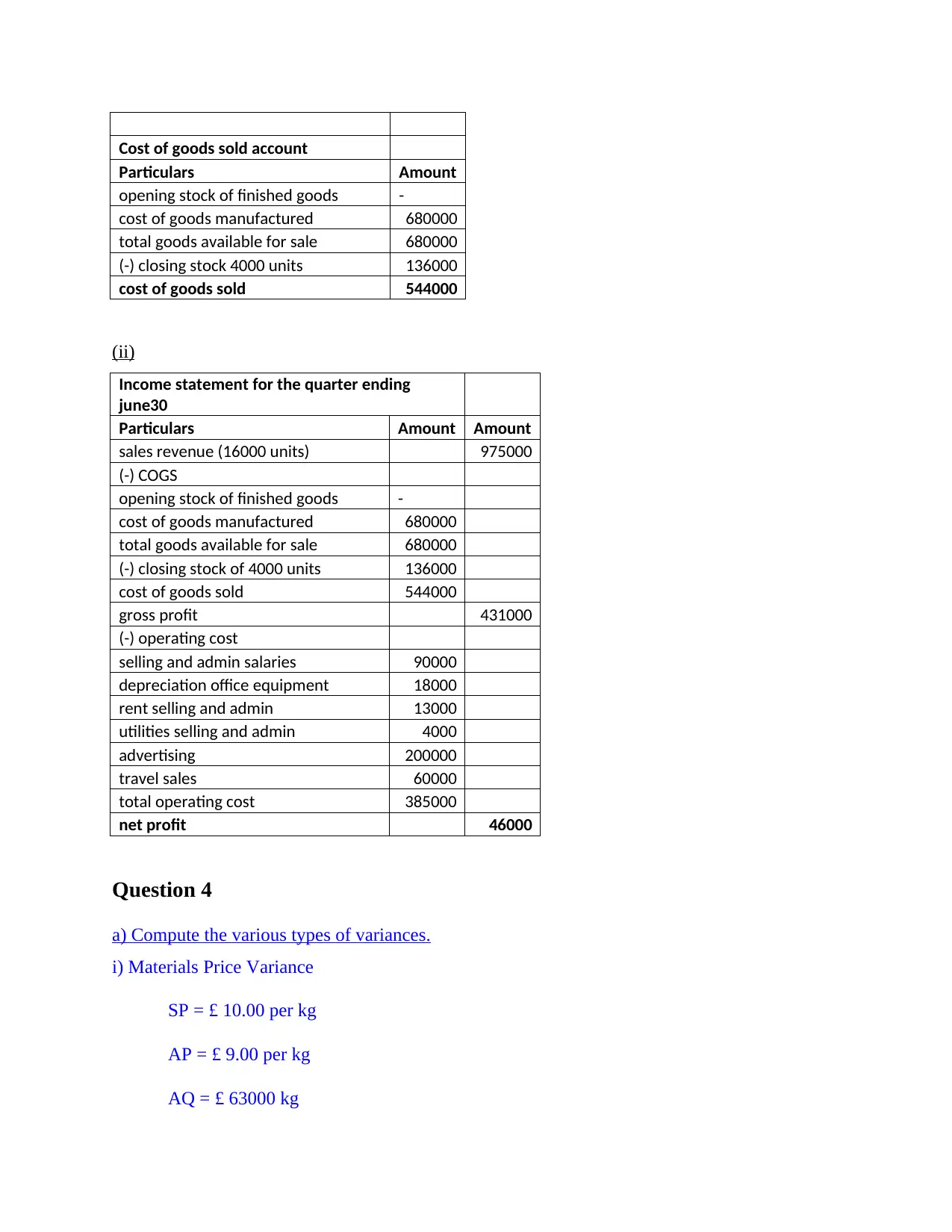

Schedule of cost of goods sold

Particulars Amount

opening stock of raw material -

raw material purchased 310000

(-) raw material closing stock 40000

raw material consumed 270000

Cleaning supplies, factory 6000

Direct labour costs 80000

Indirect labour costs 136000

Maintenance, factory 47000

Rental cost facilities 52000

utilities cost factory 36000

Depreciation, production equipment 75000

Insurance, factory 9000

(-) WIP closing stock 30000

cost of goods manufactured 680000

(20000 units in June quarter)

cost of goods manufactured unit 34000

The average fixed cost per unit; and

The average total cost per unit. Assume that this activity level is within the significant

range.

Variable cost = £125,188 / 6800 units =18.41 per unit

Activity level 7,100

Total costs:

Variable cost (a) [7,100 unit’s x £18.41 per unit]£130,711

Fixed cost (b) 164,152

Total (c) £294,863

Cost per unit:

Variable cost (d) £18.41

Fixed cost (e) [£164,152/7100 units] 23.12

Total (f) £41.53

Question 2

(i)

Schedule of cost of goods sold

Particulars Amount

opening stock of raw material -

raw material purchased 310000

(-) raw material closing stock 40000

raw material consumed 270000

Cleaning supplies, factory 6000

Direct labour costs 80000

Indirect labour costs 136000

Maintenance, factory 47000

Rental cost facilities 52000

utilities cost factory 36000

Depreciation, production equipment 75000

Insurance, factory 9000

(-) WIP closing stock 30000

cost of goods manufactured 680000

(20000 units in June quarter)

cost of goods manufactured unit 34000

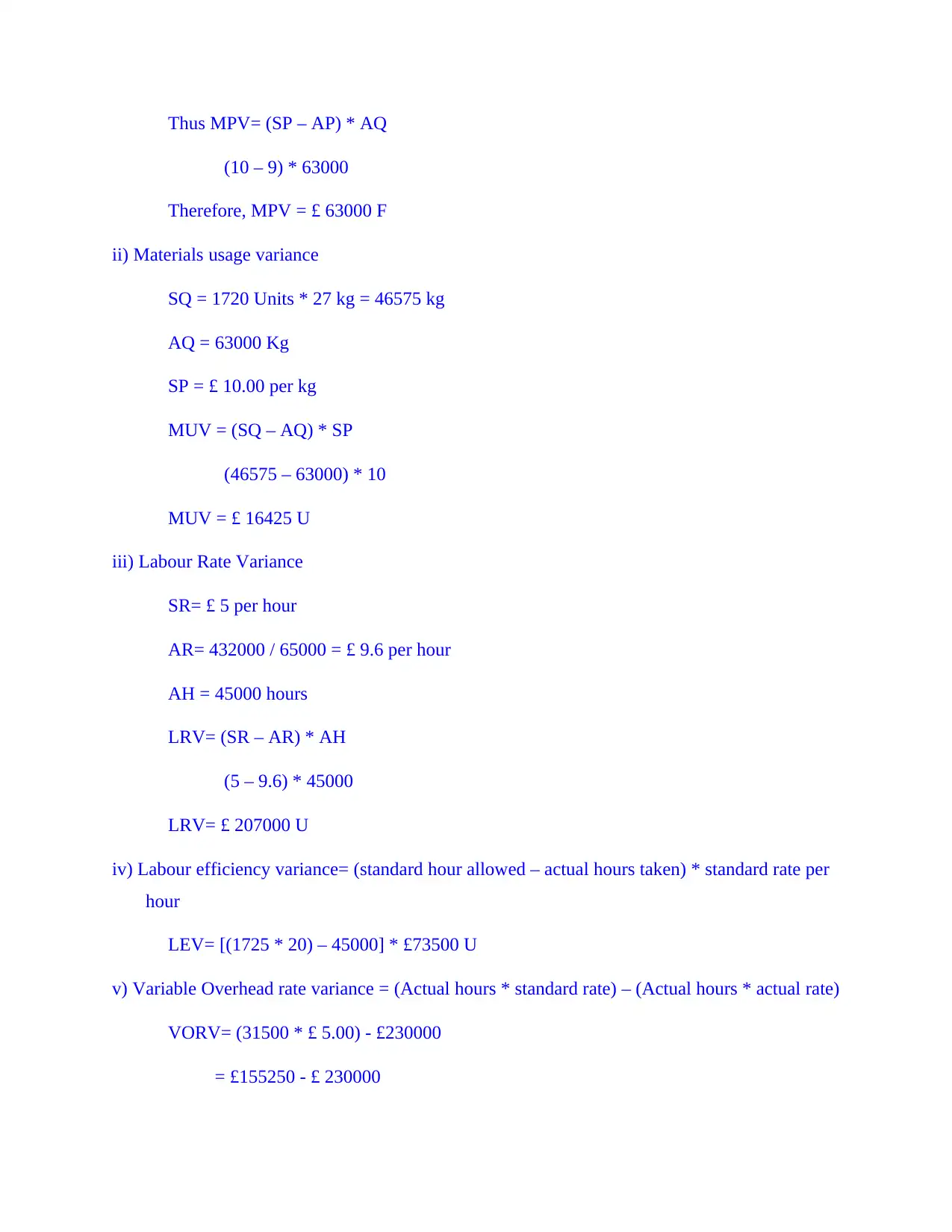

Cost of goods sold account

Particulars Amount

opening stock of finished goods -

cost of goods manufactured 680000

total goods available for sale 680000

(-) closing stock 4000 units 136000

cost of goods sold 544000

(ii)

Income statement for the quarter ending

june30

Particulars Amount Amount

sales revenue (16000 units) 975000

(-) COGS

opening stock of finished goods -

cost of goods manufactured 680000

total goods available for sale 680000

(-) closing stock of 4000 units 136000

cost of goods sold 544000

gross profit 431000

(-) operating cost

selling and admin salaries 90000

depreciation office equipment 18000

rent selling and admin 13000

utilities selling and admin 4000

advertising 200000

travel sales 60000

total operating cost 385000

net profit 46000

Question 4

a) Compute the various types of variances.

i) Materials Price Variance

SP = £ 10.00 per kg

AP = £ 9.00 per kg

AQ = £ 63000 kg

Particulars Amount

opening stock of finished goods -

cost of goods manufactured 680000

total goods available for sale 680000

(-) closing stock 4000 units 136000

cost of goods sold 544000

(ii)

Income statement for the quarter ending

june30

Particulars Amount Amount

sales revenue (16000 units) 975000

(-) COGS

opening stock of finished goods -

cost of goods manufactured 680000

total goods available for sale 680000

(-) closing stock of 4000 units 136000

cost of goods sold 544000

gross profit 431000

(-) operating cost

selling and admin salaries 90000

depreciation office equipment 18000

rent selling and admin 13000

utilities selling and admin 4000

advertising 200000

travel sales 60000

total operating cost 385000

net profit 46000

Question 4

a) Compute the various types of variances.

i) Materials Price Variance

SP = £ 10.00 per kg

AP = £ 9.00 per kg

AQ = £ 63000 kg

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Thus MPV= (SP – AP) * AQ

(10 – 9) * 63000

Therefore, MPV = £ 63000 F

ii) Materials usage variance

SQ = 1720 Units * 27 kg = 46575 kg

AQ = 63000 Kg

SP = £ 10.00 per kg

MUV = (SQ – AQ) * SP

(46575 – 63000) * 10

MUV = £ 16425 U

iii) Labour Rate Variance

SR= £ 5 per hour

AR= 432000 / 65000 = £ 9.6 per hour

AH = 45000 hours

LRV= (SR – AR) * AH

(5 – 9.6) * 45000

LRV= £ 207000 U

iv) Labour efficiency variance= (standard hour allowed – actual hours taken) * standard rate per

hour

LEV= [(1725 * 20) – 45000] * £73500 U

v) Variable Overhead rate variance = (Actual hours * standard rate) – (Actual hours * actual rate)

VORV= (31500 * £ 5.00) - £230000

= £155250 - £ 230000

(10 – 9) * 63000

Therefore, MPV = £ 63000 F

ii) Materials usage variance

SQ = 1720 Units * 27 kg = 46575 kg

AQ = 63000 Kg

SP = £ 10.00 per kg

MUV = (SQ – AQ) * SP

(46575 – 63000) * 10

MUV = £ 16425 U

iii) Labour Rate Variance

SR= £ 5 per hour

AR= 432000 / 65000 = £ 9.6 per hour

AH = 45000 hours

LRV= (SR – AR) * AH

(5 – 9.6) * 45000

LRV= £ 207000 U

iv) Labour efficiency variance= (standard hour allowed – actual hours taken) * standard rate per

hour

LEV= [(1725 * 20) – 45000] * £73500 U

v) Variable Overhead rate variance = (Actual hours * standard rate) – (Actual hours * actual rate)

VORV= (31500 * £ 5.00) - £230000

= £155250 - £ 230000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

VORV = £ 74750 U

vi) Variable Overhead efficiency variance= (Standard hour * standard rate) – (Actual Hours *

standard rate)

VOEV = [(1725 * 15) * £ 5.00] – (31050 * £5.00)

VOEV = £ 25875 U

b) Discuss four possible causes for each of the following variances:

a) Material Usage:

The modification can be due to of the ineffective and careless workers

It might be possible that there are undisciplined people working in the business who

have wasted the materials.

The techniques and tools which are being used are not in a good condition which

might lead to ineffective production or it is possible that there might be some issues

or defect observed in the machines being used at the time of production.

Repetitive changes in the designing and development of product and variations in

case of material mix or there can be usage of material mix apart from the standard

mix.

b) Labour efficiency:

The enterprise is noticed to use poor quality based raw material, thus in order for

completing the work, time required is more.

It is possible that there might be alterations possible in case of production mechanism

and techniques as well.

Poor satisfaction lead to lack of incentives which are being given to the workers.

The working environment observed is not accurate and there are many conflicts,

arguments and stress prevailing in the workers. Also, there is a delay in giving

instructions which can lead to the time loss which would be affecting the efficiency of

labour.

vi) Variable Overhead efficiency variance= (Standard hour * standard rate) – (Actual Hours *

standard rate)

VOEV = [(1725 * 15) * £ 5.00] – (31050 * £5.00)

VOEV = £ 25875 U

b) Discuss four possible causes for each of the following variances:

a) Material Usage:

The modification can be due to of the ineffective and careless workers

It might be possible that there are undisciplined people working in the business who

have wasted the materials.

The techniques and tools which are being used are not in a good condition which

might lead to ineffective production or it is possible that there might be some issues

or defect observed in the machines being used at the time of production.

Repetitive changes in the designing and development of product and variations in

case of material mix or there can be usage of material mix apart from the standard

mix.

b) Labour efficiency:

The enterprise is noticed to use poor quality based raw material, thus in order for

completing the work, time required is more.

It is possible that there might be alterations possible in case of production mechanism

and techniques as well.

Poor satisfaction lead to lack of incentives which are being given to the workers.

The working environment observed is not accurate and there are many conflicts,

arguments and stress prevailing in the workers. Also, there is a delay in giving

instructions which can lead to the time loss which would be affecting the efficiency of

labour.

Description on the variance to be examined in relation to the work performance:

Variance analysis can be explained as a process which helps to assess the variation between the

actual performance and estimated budgets. It is counted as a quantitative approach which aids the

business companies for having a better monitor power over the company. This would be helpful

for the enterprise to investigate the reasons which can be held responsible for the deviations

observed.

Variable Overhead spending: It can be computed by exclusion of standard based

overhead expense incurred per unit with the actual cost obtained and further multiplying

it with the total quantity of output.

Purchase price variance: It can be measured by taking in account the payment which is

being made for actual pricing strategy of raw materials and deducting the standardised

cost.

Labour rate variance: It focuses on the wages which are being paid to labours and is

indicated to the difference between actual cost being incurred for the direct cost and

labour and cost which is being mentioned and highlighted in the budget being prepared.

Material Yield variance: It can be explained as the difference between standard and

output in production processes.

Fixed overhead spending variance: If the variation is observed to be unfavourable then it

states that the fixed overhead costs are higher than the budgeted one. If favourable then

they are less than budgeted ones when made comparisons.

Question 5

(a)

Statement of Relevant Cost

Make Buy

Direct Material $210,000 -

Direct Labor $150,000 -

Variable Manufacturing Overhead $45,000 -

Fixed Manufacturing Overhead (Traceable) $30,000 -

(90,000 × 1/3)

Variance analysis can be explained as a process which helps to assess the variation between the

actual performance and estimated budgets. It is counted as a quantitative approach which aids the

business companies for having a better monitor power over the company. This would be helpful

for the enterprise to investigate the reasons which can be held responsible for the deviations

observed.

Variable Overhead spending: It can be computed by exclusion of standard based

overhead expense incurred per unit with the actual cost obtained and further multiplying

it with the total quantity of output.

Purchase price variance: It can be measured by taking in account the payment which is

being made for actual pricing strategy of raw materials and deducting the standardised

cost.

Labour rate variance: It focuses on the wages which are being paid to labours and is

indicated to the difference between actual cost being incurred for the direct cost and

labour and cost which is being mentioned and highlighted in the budget being prepared.

Material Yield variance: It can be explained as the difference between standard and

output in production processes.

Fixed overhead spending variance: If the variation is observed to be unfavourable then it

states that the fixed overhead costs are higher than the budgeted one. If favourable then

they are less than budgeted ones when made comparisons.

Question 5

(a)

Statement of Relevant Cost

Make Buy

Direct Material $210,000 -

Direct Labor $150,000 -

Variable Manufacturing Overhead $45,000 -

Fixed Manufacturing Overhead (Traceable) $30,000 -

(90,000 × 1/3)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

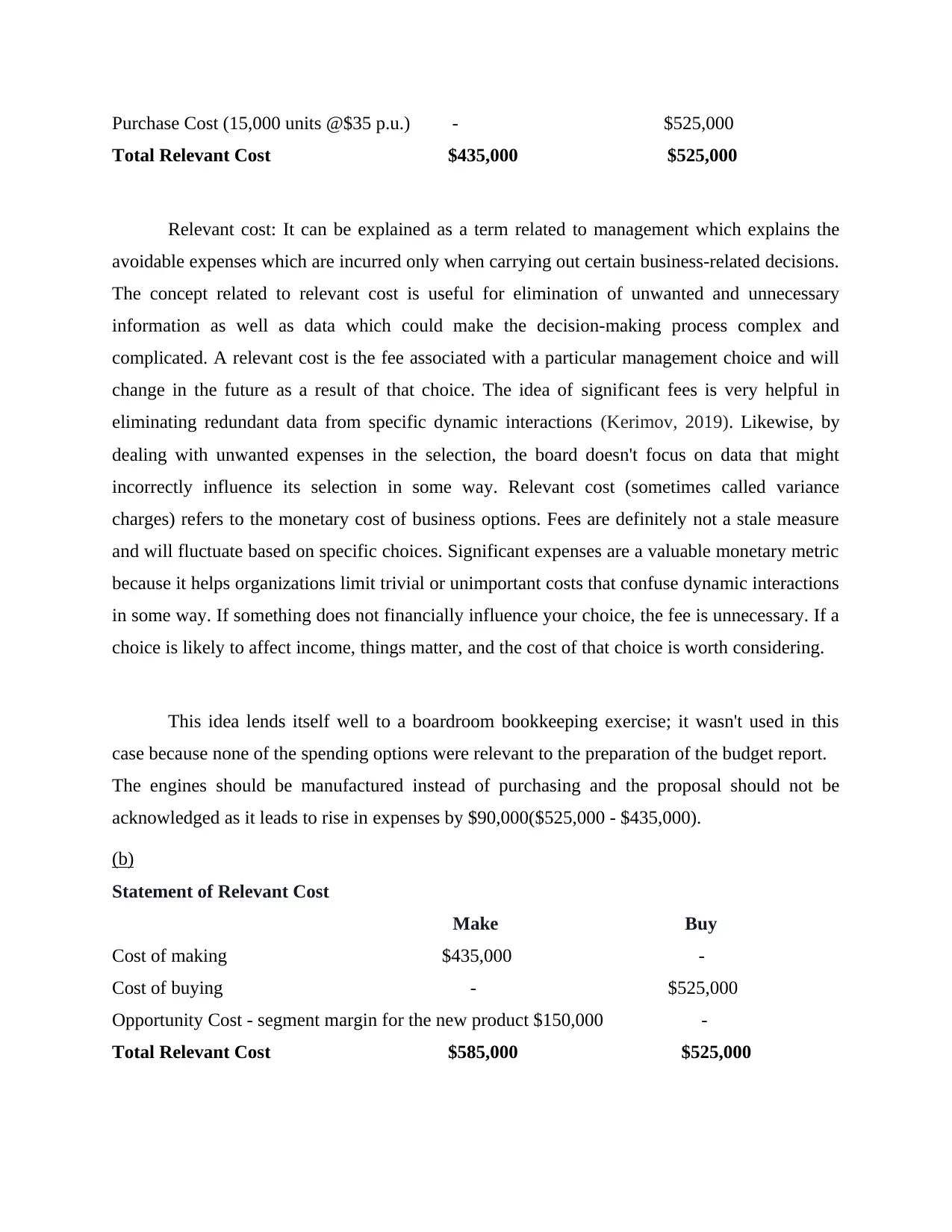

Purchase Cost (15,000 units @$35 p.u.) - $525,000

Total Relevant Cost $435,000 $525,000

Relevant cost: It can be explained as a term related to management which explains the

avoidable expenses which are incurred only when carrying out certain business-related decisions.

The concept related to relevant cost is useful for elimination of unwanted and unnecessary

information as well as data which could make the decision-making process complex and

complicated. A relevant cost is the fee associated with a particular management choice and will

change in the future as a result of that choice. The idea of significant fees is very helpful in

eliminating redundant data from specific dynamic interactions (Kerimov, 2019). Likewise, by

dealing with unwanted expenses in the selection, the board doesn't focus on data that might

incorrectly influence its selection in some way. Relevant cost (sometimes called variance

charges) refers to the monetary cost of business options. Fees are definitely not a stale measure

and will fluctuate based on specific choices. Significant expenses are a valuable monetary metric

because it helps organizations limit trivial or unimportant costs that confuse dynamic interactions

in some way. If something does not financially influence your choice, the fee is unnecessary. If a

choice is likely to affect income, things matter, and the cost of that choice is worth considering.

This idea lends itself well to a boardroom bookkeeping exercise; it wasn't used in this

case because none of the spending options were relevant to the preparation of the budget report.

The engines should be manufactured instead of purchasing and the proposal should not be

acknowledged as it leads to rise in expenses by $90,000($525,000 - $435,000).

(b)

Statement of Relevant Cost

Make Buy

Cost of making $435,000 -

Cost of buying - $525,000

Opportunity Cost - segment margin for the new product $150,000 -

Total Relevant Cost $585,000 $525,000

Total Relevant Cost $435,000 $525,000

Relevant cost: It can be explained as a term related to management which explains the

avoidable expenses which are incurred only when carrying out certain business-related decisions.

The concept related to relevant cost is useful for elimination of unwanted and unnecessary

information as well as data which could make the decision-making process complex and

complicated. A relevant cost is the fee associated with a particular management choice and will

change in the future as a result of that choice. The idea of significant fees is very helpful in

eliminating redundant data from specific dynamic interactions (Kerimov, 2019). Likewise, by

dealing with unwanted expenses in the selection, the board doesn't focus on data that might

incorrectly influence its selection in some way. Relevant cost (sometimes called variance

charges) refers to the monetary cost of business options. Fees are definitely not a stale measure

and will fluctuate based on specific choices. Significant expenses are a valuable monetary metric

because it helps organizations limit trivial or unimportant costs that confuse dynamic interactions

in some way. If something does not financially influence your choice, the fee is unnecessary. If a

choice is likely to affect income, things matter, and the cost of that choice is worth considering.

This idea lends itself well to a boardroom bookkeeping exercise; it wasn't used in this

case because none of the spending options were relevant to the preparation of the budget report.

The engines should be manufactured instead of purchasing and the proposal should not be

acknowledged as it leads to rise in expenses by $90,000($525,000 - $435,000).

(b)

Statement of Relevant Cost

Make Buy

Cost of making $435,000 -

Cost of buying - $525,000

Opportunity Cost - segment margin for the new product $150,000 -

Total Relevant Cost $585,000 $525,000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The engines are suggested to be acquired instead of being produced and the offer must be

acknowledged as it would lead toward saving cost by $60,000($5,85,000 - $5,25,000).

(c)

Incremental costs: They are extra costs incurred for creating an additional item, it just

investigates those costs that are expected to fluctuate as an element of a given condition, and the

excess is considered irrelevant. It can be explained as an additional cost which is faced by a firm

as a consequence of adjustments in a pricing strategy linked with production, equipment’s and

upgradation in technology or installing a supplementary product for quoting an example. It can

also be explained as an interest which would be helpful in determining the incremental change in

expense in a number of circumstances. For instance, the incremental expenses of an employee’s

termination would involve the expense of additional benefit which is given to the people as an

outcome of termination. Or the incremental costs of shutting down a production line which

would involve the cost related to place employees, sell unwanted equipment’s and converting the

facility to some other purposes (Li, 2018).

Opportunity cost: When a respective person gives comments regarding “opportunity cost”

of an item, they have been discussing regarding the valuation of the product’s next highest

valued substitute utilisation. If someone is able to devote a bunch of money for attending movies

for instance, you are not able to expend additional time in reading textbooks at home or use the

funds towards something else. If reading such books is next best option considered after

watching a movie is the price of ticket and further the fun which would lose out on by not going

through the textbooks. It would present the possible benefits which a respective person, business

misses or investors on when selecting one alternative over other. Because opportunity costs are

unwanted through definition, they can be simply ignored. It can be defined as an economic

terminology which states the value of what you need to give up in related to choose something

else (Ng and Harrison, 2021).

acknowledged as it would lead toward saving cost by $60,000($5,85,000 - $5,25,000).

(c)

Incremental costs: They are extra costs incurred for creating an additional item, it just

investigates those costs that are expected to fluctuate as an element of a given condition, and the

excess is considered irrelevant. It can be explained as an additional cost which is faced by a firm

as a consequence of adjustments in a pricing strategy linked with production, equipment’s and

upgradation in technology or installing a supplementary product for quoting an example. It can

also be explained as an interest which would be helpful in determining the incremental change in

expense in a number of circumstances. For instance, the incremental expenses of an employee’s

termination would involve the expense of additional benefit which is given to the people as an

outcome of termination. Or the incremental costs of shutting down a production line which

would involve the cost related to place employees, sell unwanted equipment’s and converting the

facility to some other purposes (Li, 2018).

Opportunity cost: When a respective person gives comments regarding “opportunity cost”

of an item, they have been discussing regarding the valuation of the product’s next highest

valued substitute utilisation. If someone is able to devote a bunch of money for attending movies

for instance, you are not able to expend additional time in reading textbooks at home or use the

funds towards something else. If reading such books is next best option considered after

watching a movie is the price of ticket and further the fun which would lose out on by not going

through the textbooks. It would present the possible benefits which a respective person, business

misses or investors on when selecting one alternative over other. Because opportunity costs are

unwanted through definition, they can be simply ignored. It can be defined as an economic

terminology which states the value of what you need to give up in related to choose something

else (Ng and Harrison, 2021).

CONCLUSION

The report takes in account and helps to ascertain various reasons behind incurring costs and

which ways would help business to grow. There are many issues which would help the enterprise

to function smoothly in a competitive environment. Companies must consider tools and activities

which would help in growth, development and expansion. The report explains the working and

significance of management accounting in a business for its running and working as well.

The report takes in account and helps to ascertain various reasons behind incurring costs and

which ways would help business to grow. There are many issues which would help the enterprise

to function smoothly in a competitive environment. Companies must consider tools and activities

which would help in growth, development and expansion. The report explains the working and

significance of management accounting in a business for its running and working as well.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.