Management Accounting: Costing, Budgeting and Performance Analysis

VerifiedAdded on 2024/05/21

|31

|5584

|470

Report

AI Summary

This report provides a comprehensive overview of management accounting principles and tools applicable to business organizations, particularly focusing on how these can be used to address challenges faced by a company named UK tech ltd. It delves into the essential requirements and types of management accounting, distinguishing it from financial accounting. The report explains costing methods like actual, normal, and standard costing, along with inventory management techniques such as Economic Order Quantity (EOQ), LIFO, FIFO, and Just-in-Time (JIT). It also covers job costing and different types of management accounting reports, including cost, inventory, investment, and budget reports. Furthermore, the document explains marginal and absorption costing, budgeting processes, and the importance of budgets for planning and control. Finally, it discusses the balanced scorecard approach for ensuring quality in business operations, highlighting how management accounting can lead organizations to sustainable success by addressing financial problems effectively.

Management Accounting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction:.........................................................................................................................................3

TASK 1................................................................................................................................................4

Introduction:.....................................................................................................................................4

A: Explain management accounting and give the essential requirements for different types of

management accounting...................................................................................................................4

B: Financial reporting:.....................................................................................................................8

M1 & D1..........................................................................................................................................9

TASK 2..............................................................................................................................................10

Explain marginal and absorption costing.......................................................................................10

M2: you will need to accurately apply the techniques and reconcile the profits to produce

appropriate financial reporting document......................................................................................13

D2: you will need to accurately apply and interpret the data for the business activities...............14

TASK 3..............................................................................................................................................15

Introduction:...................................................................................................................................15

A: Different kinds of budgets and their advantages and disadvantages.........................................15

B. The budget preparation process including determination of pricing and different costing

systems that can be used.................................................................................................................17

Budget preparation process covers following steps:......................................................................17

C. The importance of budget as a tool for planning and control purposes....................................18

M3: Analyse the use of planning tools and their application for preparing and forecasting

budgets...........................................................................................................................................19

Conclusion:.....................................................................................................................................19

2

Introduction:.........................................................................................................................................3

TASK 1................................................................................................................................................4

Introduction:.....................................................................................................................................4

A: Explain management accounting and give the essential requirements for different types of

management accounting...................................................................................................................4

B: Financial reporting:.....................................................................................................................8

M1 & D1..........................................................................................................................................9

TASK 2..............................................................................................................................................10

Explain marginal and absorption costing.......................................................................................10

M2: you will need to accurately apply the techniques and reconcile the profits to produce

appropriate financial reporting document......................................................................................13

D2: you will need to accurately apply and interpret the data for the business activities...............14

TASK 3..............................................................................................................................................15

Introduction:...................................................................................................................................15

A: Different kinds of budgets and their advantages and disadvantages.........................................15

B. The budget preparation process including determination of pricing and different costing

systems that can be used.................................................................................................................17

Budget preparation process covers following steps:......................................................................17

C. The importance of budget as a tool for planning and control purposes....................................18

M3: Analyse the use of planning tools and their application for preparing and forecasting

budgets...........................................................................................................................................19

Conclusion:.....................................................................................................................................19

2

TASK4...............................................................................................................................................20

Explain Balance scorecard.............................................................................................................20

M4: how, in responding to financial problems, management accounting can lead Organizations to

sustainable success.........................................................................................................................22

D3: you will need to evaluate how planning tools for accounting respond appropriately to solving

financial problems to lead to sustainable success..........................................................................24

Conclusion:.........................................................................................................................................25

References..........................................................................................................................................26

3

Explain Balance scorecard.............................................................................................................20

M4: how, in responding to financial problems, management accounting can lead Organizations to

sustainable success.........................................................................................................................22

D3: you will need to evaluate how planning tools for accounting respond appropriately to solving

financial problems to lead to sustainable success..........................................................................24

Conclusion:.........................................................................................................................................25

References..........................................................................................................................................26

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction:

Availability of information and effective management is a must for every business organization and

it reduces problems and losses and ensures profitability for business operations. UK tech ltd is also

facing the same type of problems and this assignment report is prepared to give basic knowledge of

management system and its fundamental tools which can be used by the manager of the company to

solve above problems. The report explains different tools of management accounting and

management information along with the importance of information system which can be used by

UK tech ltd to control its business activities. The report also denotes the cost management and cost

measurement techniques which can be used by UK tech ltd to control its production cost. To control

the cost, budgeting is a must and useful tool and this report explain the budgeting system and

budget preparation process along with the advantages and disadvantages of budgets. To ensure the

profitability of business operations effective execution of strategy is must and this report also

defines the balanced scorecard approach which can be used by UK tech ltd to ensure the quality of

business operations.

4

Availability of information and effective management is a must for every business organization and

it reduces problems and losses and ensures profitability for business operations. UK tech ltd is also

facing the same type of problems and this assignment report is prepared to give basic knowledge of

management system and its fundamental tools which can be used by the manager of the company to

solve above problems. The report explains different tools of management accounting and

management information along with the importance of information system which can be used by

UK tech ltd to control its business activities. The report also denotes the cost management and cost

measurement techniques which can be used by UK tech ltd to control its production cost. To control

the cost, budgeting is a must and useful tool and this report explain the budgeting system and

budget preparation process along with the advantages and disadvantages of budgets. To ensure the

profitability of business operations effective execution of strategy is must and this report also

defines the balanced scorecard approach which can be used by UK tech ltd to ensure the quality of

business operations.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 1

Introduction:

In this report, the basic concept of management accounting is explained along with the various

management accounting tools like inventory management and job costing. Different types of

management system reports and importance of information are also explained in this report.

A: Explain management accounting and give the essential requirements for different

types of management accounting.

Management accounting: management accounting is a process which supports managers to

formulate and execute the business strategy so that business can achieve its goals. In other words,

management accounting is a system which includes various techniques and tools to assist the

managers in policy formulation and decision-making by providing appropriate and enough financial

information and data (Anthony, 2018). It generates profit for business organisations by reducing

expenses and fulfils various discloser requirements.

Management system comes with three relevant steps planning, controlling and monitoring to avail

the correct and convenient data to managers of the company so that business can manage in a

profitable manner. UK tech ltd is also facing the problem of availability of information and the

same affects the quality of managerial decisions. The company can adopt management system to

eliminate above problems. Management accounting is different from financial accounting and the

same is explained below:

Table 1 Distinguishing Management Accounting from Financial Accounting.

Reason Management accounting Financial accounting

Basic concept

Management accounting is used to

give correct and convenient

information to managers so that they

can make an appropriate strategy.

Financial accounting is a process used

to generate the financial statement of an

organization to convey the financial

information to related parties.

Reporting No specified format Specified reporting format

5

Introduction:

In this report, the basic concept of management accounting is explained along with the various

management accounting tools like inventory management and job costing. Different types of

management system reports and importance of information are also explained in this report.

A: Explain management accounting and give the essential requirements for different

types of management accounting.

Management accounting: management accounting is a process which supports managers to

formulate and execute the business strategy so that business can achieve its goals. In other words,

management accounting is a system which includes various techniques and tools to assist the

managers in policy formulation and decision-making by providing appropriate and enough financial

information and data (Anthony, 2018). It generates profit for business organisations by reducing

expenses and fulfils various discloser requirements.

Management system comes with three relevant steps planning, controlling and monitoring to avail

the correct and convenient data to managers of the company so that business can manage in a

profitable manner. UK tech ltd is also facing the problem of availability of information and the

same affects the quality of managerial decisions. The company can adopt management system to

eliminate above problems. Management accounting is different from financial accounting and the

same is explained below:

Table 1 Distinguishing Management Accounting from Financial Accounting.

Reason Management accounting Financial accounting

Basic concept

Management accounting is used to

give correct and convenient

information to managers so that they

can make an appropriate strategy.

Financial accounting is a process used

to generate the financial statement of an

organization to convey the financial

information to related parties.

Reporting No specified format Specified reporting format

5

format

Type of

information

Management accounting marks the

monetary and non-monetary

information to assist the decision-

making.

Financial accounting shows the

financial position of the company.

users Management information reports are

used by internal management to

increase the quality of strategy

planning (SINGH, 2018).

Financial statements are used by

external and internal peoples to

determinate the financial situation of

the company. Like investors, creditors

Time-Gap Management reports are prepared

according to the needs (S, 2014).

Generally, financial statements are

prepared annually after the completion

of the financial year.

Legal Needs

There is No legal need for the

Preparation of management

accounting reports.

Preparation of financial statements is

necessary by law.

Monitoring

needs.

As management accounting is used to

generate the internal reports for

management there is no requirement

for auditing and other investigation

activities.

Financial accounting is used to report

the financial position of an organization

and to save the external parties auditing

is required (S, 2014).

Importance of management accounting information as a decision-making tool for department

managers

Management accounting generates different types of information reports which provide useful

information to managers so that they can take quality decisions. As a decision-making tool

management accounting information has following benefits:

Data to analyse: management accounting information provides data about the business operation

so that manager can identify every aspect of business expenses and take decision accordingly

(Freedman, 2018).

6

Type of

information

Management accounting marks the

monetary and non-monetary

information to assist the decision-

making.

Financial accounting shows the

financial position of the company.

users Management information reports are

used by internal management to

increase the quality of strategy

planning (SINGH, 2018).

Financial statements are used by

external and internal peoples to

determinate the financial situation of

the company. Like investors, creditors

Time-Gap Management reports are prepared

according to the needs (S, 2014).

Generally, financial statements are

prepared annually after the completion

of the financial year.

Legal Needs

There is No legal need for the

Preparation of management

accounting reports.

Preparation of financial statements is

necessary by law.

Monitoring

needs.

As management accounting is used to

generate the internal reports for

management there is no requirement

for auditing and other investigation

activities.

Financial accounting is used to report

the financial position of an organization

and to save the external parties auditing

is required (S, 2014).

Importance of management accounting information as a decision-making tool for department

managers

Management accounting generates different types of information reports which provide useful

information to managers so that they can take quality decisions. As a decision-making tool

management accounting information has following benefits:

Data to analyse: management accounting information provides data about the business operation

so that manager can identify every aspect of business expenses and take decision accordingly

(Freedman, 2018).

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Evaluation of performance and profitability: management information gives details about the

efficiency of every department. Management can use this information to prepare budgets according

to the capacity of the department (Freedman, 2018). On the basis of management information

management can also define the profitability of future projects and take do or not decisions.

Cost accounting system:

Cost accounting is a system of measurement of production expenses. It denotes the material, labour

and overhead costs which are incurred by a business during the normal course of operation. To

determinate the costs following methods can be used:

Actual costing: Actual costing involves only use actual expenses and does not use any type

of budgeted amounts. It is used to determinate the cost of the product by explaining the

actual cost of material. The actual cost of labour and the actual cost of overheads.

Normal costing: Normal costing is also a similar costing system which involves Actual

expenses of material and labour and budgeted amounts of overhead to determinate the cost

of the product.

Standard costing: standard costing is a costing system which is used to determinate the

differences between decided standards and actual results.

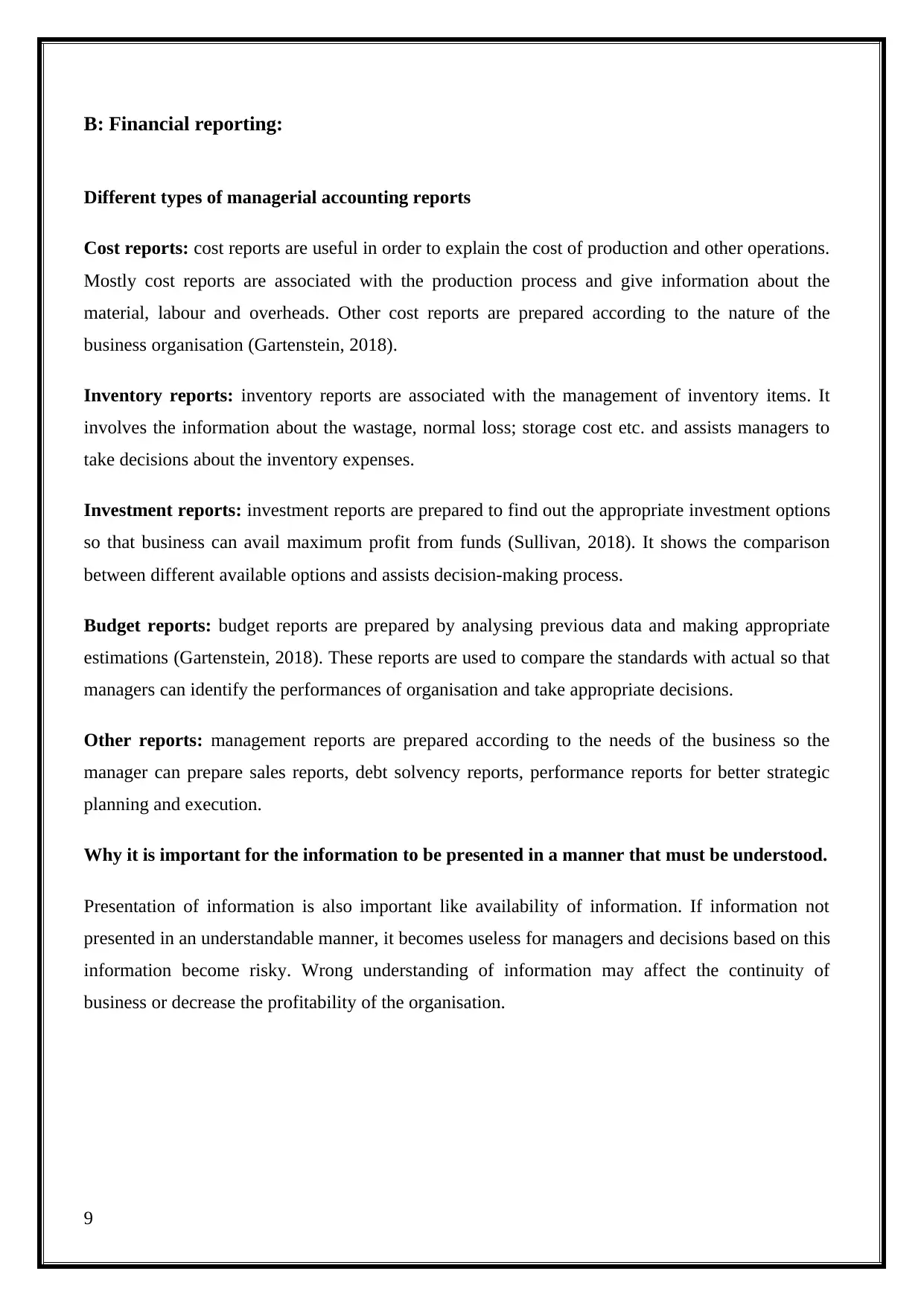

Inventory management system:

Inventory management system is a method of managing the current asset ‘Inventory’ and involves

the various steps which are used to control the flow of inventory items (Hamlett, 2018). It controls

the flow of inventory items and assists the process of ordering, purchasing, use for production and

supply to customers. Following techniques are available to manage the inventory:

7

efficiency of every department. Management can use this information to prepare budgets according

to the capacity of the department (Freedman, 2018). On the basis of management information

management can also define the profitability of future projects and take do or not decisions.

Cost accounting system:

Cost accounting is a system of measurement of production expenses. It denotes the material, labour

and overhead costs which are incurred by a business during the normal course of operation. To

determinate the costs following methods can be used:

Actual costing: Actual costing involves only use actual expenses and does not use any type

of budgeted amounts. It is used to determinate the cost of the product by explaining the

actual cost of material. The actual cost of labour and the actual cost of overheads.

Normal costing: Normal costing is also a similar costing system which involves Actual

expenses of material and labour and budgeted amounts of overhead to determinate the cost

of the product.

Standard costing: standard costing is a costing system which is used to determinate the

differences between decided standards and actual results.

Inventory management system:

Inventory management system is a method of managing the current asset ‘Inventory’ and involves

the various steps which are used to control the flow of inventory items (Hamlett, 2018). It controls

the flow of inventory items and assists the process of ordering, purchasing, use for production and

supply to customers. Following techniques are available to manage the inventory:

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Image 1, Techniques of Inventory management system

By Author, 2018

Job costing system:

This system is a cost measurement technique used to determinate the cost of special batches. When

an organization produce product on order basis or produced items is different from each this system

is used to find out the cost of every single product or batch. This system is necessary in the case of

cost-plus contracts.

8

Techniques of

Inventory

management

Economic Order quantity

FIFO

method

Just-in-time

LIFO

method

By Author, 2018

Job costing system:

This system is a cost measurement technique used to determinate the cost of special batches. When

an organization produce product on order basis or produced items is different from each this system

is used to find out the cost of every single product or batch. This system is necessary in the case of

cost-plus contracts.

8

Techniques of

Inventory

management

Economic Order quantity

FIFO

method

Just-in-time

LIFO

method

B: Financial reporting:

Different types of managerial accounting reports

Cost reports: cost reports are useful in order to explain the cost of production and other operations.

Mostly cost reports are associated with the production process and give information about the

material, labour and overheads. Other cost reports are prepared according to the nature of the

business organisation (Gartenstein, 2018).

Inventory reports: inventory reports are associated with the management of inventory items. It

involves the information about the wastage, normal loss; storage cost etc. and assists managers to

take decisions about the inventory expenses.

Investment reports: investment reports are prepared to find out the appropriate investment options

so that business can avail maximum profit from funds (Sullivan, 2018). It shows the comparison

between different available options and assists decision-making process.

Budget reports: budget reports are prepared by analysing previous data and making appropriate

estimations (Gartenstein, 2018). These reports are used to compare the standards with actual so that

managers can identify the performances of organisation and take appropriate decisions.

Other reports: management reports are prepared according to the needs of the business so the

manager can prepare sales reports, debt solvency reports, performance reports for better strategic

planning and execution.

Why it is important for the information to be presented in a manner that must be understood.

Presentation of information is also important like availability of information. If information not

presented in an understandable manner, it becomes useless for managers and decisions based on this

information become risky. Wrong understanding of information may affect the continuity of

business or decrease the profitability of the organisation.

9

Different types of managerial accounting reports

Cost reports: cost reports are useful in order to explain the cost of production and other operations.

Mostly cost reports are associated with the production process and give information about the

material, labour and overheads. Other cost reports are prepared according to the nature of the

business organisation (Gartenstein, 2018).

Inventory reports: inventory reports are associated with the management of inventory items. It

involves the information about the wastage, normal loss; storage cost etc. and assists managers to

take decisions about the inventory expenses.

Investment reports: investment reports are prepared to find out the appropriate investment options

so that business can avail maximum profit from funds (Sullivan, 2018). It shows the comparison

between different available options and assists decision-making process.

Budget reports: budget reports are prepared by analysing previous data and making appropriate

estimations (Gartenstein, 2018). These reports are used to compare the standards with actual so that

managers can identify the performances of organisation and take appropriate decisions.

Other reports: management reports are prepared according to the needs of the business so the

manager can prepare sales reports, debt solvency reports, performance reports for better strategic

planning and execution.

Why it is important for the information to be presented in a manner that must be understood.

Presentation of information is also important like availability of information. If information not

presented in an understandable manner, it becomes useless for managers and decisions based on this

information become risky. Wrong understanding of information may affect the continuity of

business or decrease the profitability of the organisation.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

M1 & D1

Control of expenses:

Management accounting tool gives detailed knowledge of the business operations. By applying

management practices UK Ltd can find out the appropriate level of every expense and take steps to

reduce it (Gartenstein, 2018). Control on expenses will directly increase the profitability of the

company.

Different cost report gives information about the expenses which are incurred during the business

operations (Guinea, 2016). Managers can identify extra costs of organizational processes and take

corrective actions.

Evaluation of efficiency:

Efficiency saves cost for business and UK Ltd can check out the efficiency of business operations

and departments. It makes every department manager responsible for his work and thus helps to

improve performance.

Every business process requires efficiency in operations and management reports give the

assistance to maintain the same. These reports avail complete knowledge about the departmental

efficiency so the manager can manage the operations effectively.

Strategy planning and implementation:

Management accounting system assists managers in the decision-making process. In the relation of

UK Tech Ltd, managers can make a highly appropriate strategy so that business can achieve its

aims.

Management system involves the various budgeting tools which are very useful in budgeting

process (Ghanbari and Vaseli, 2015). These budgeted reports are used by managers to set out the

best strategy as per the organisational process.

Conclusion:

This report concludes that management accounting system is very useful for UK tech ltd and by

using this; the company can manage its operations in a curative manner to incur the higher profits.

10

Control of expenses:

Management accounting tool gives detailed knowledge of the business operations. By applying

management practices UK Ltd can find out the appropriate level of every expense and take steps to

reduce it (Gartenstein, 2018). Control on expenses will directly increase the profitability of the

company.

Different cost report gives information about the expenses which are incurred during the business

operations (Guinea, 2016). Managers can identify extra costs of organizational processes and take

corrective actions.

Evaluation of efficiency:

Efficiency saves cost for business and UK Ltd can check out the efficiency of business operations

and departments. It makes every department manager responsible for his work and thus helps to

improve performance.

Every business process requires efficiency in operations and management reports give the

assistance to maintain the same. These reports avail complete knowledge about the departmental

efficiency so the manager can manage the operations effectively.

Strategy planning and implementation:

Management accounting system assists managers in the decision-making process. In the relation of

UK Tech Ltd, managers can make a highly appropriate strategy so that business can achieve its

aims.

Management system involves the various budgeting tools which are very useful in budgeting

process (Ghanbari and Vaseli, 2015). These budgeted reports are used by managers to set out the

best strategy as per the organisational process.

Conclusion:

This report concludes that management accounting system is very useful for UK tech ltd and by

using this; the company can manage its operations in a curative manner to incur the higher profits.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 2

Explain marginal and absorption costing.

Cost: cost is an amount which is paid by someone to get something. In the relation of business

organization, cost involves all the expenses which are paid to acquire some rights or produce a

product. On the basis of nature, then the cost can be divided into following categories:

Fixed cost

Variable cost

Semi-variable cost

Determination of cost is very important to find out the appropriate price and corrects profit. Cost

volume profit (CPV) is another tool to manage and control the costs. In this method, manager

determinates the relation between cots and profits and its impact on profits.

Absorption costing: a costing system which involves all production expenses in the cost of

production without considering their fixed or variable nature is called absorption costing. It is also

known as full costing and all manufacturing expenses all charged on per unit cost.

11

Explain marginal and absorption costing.

Cost: cost is an amount which is paid by someone to get something. In the relation of business

organization, cost involves all the expenses which are paid to acquire some rights or produce a

product. On the basis of nature, then the cost can be divided into following categories:

Fixed cost

Variable cost

Semi-variable cost

Determination of cost is very important to find out the appropriate price and corrects profit. Cost

volume profit (CPV) is another tool to manage and control the costs. In this method, manager

determinates the relation between cots and profits and its impact on profits.

Absorption costing: a costing system which involves all production expenses in the cost of

production without considering their fixed or variable nature is called absorption costing. It is also

known as full costing and all manufacturing expenses all charged on per unit cost.

11

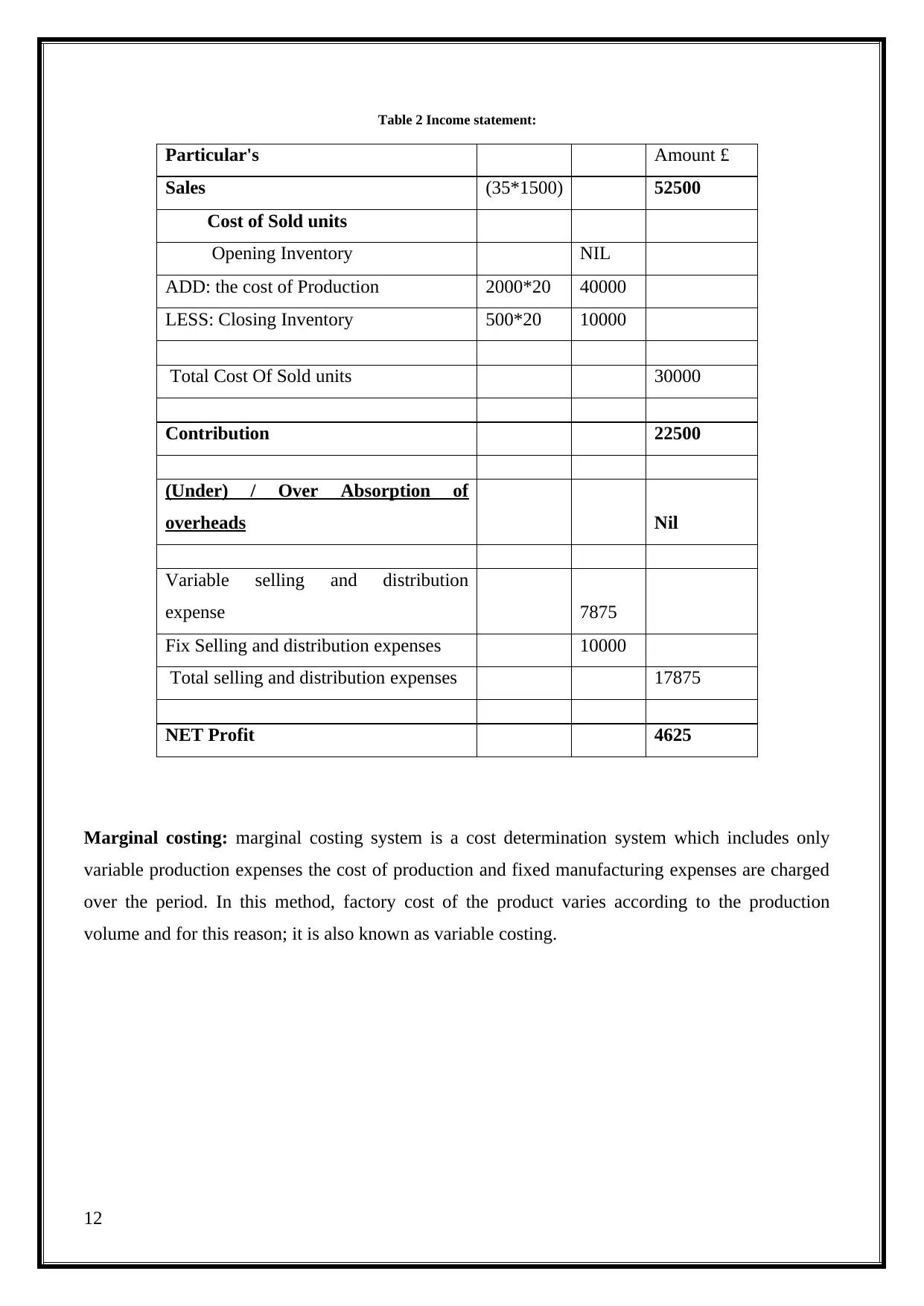

Table 2 Income statement:

Particular's Amount £

Sales (35*1500) 52500

Cost of Sold units

Opening Inventory NIL

ADD: the cost of Production 2000*20 40000

LESS: Closing Inventory 500*20 10000

Total Cost Of Sold units 30000

Contribution 22500

(Under) / Over Absorption of

overheads Nil

Variable selling and distribution

expense 7875

Fix Selling and distribution expenses 10000

Total selling and distribution expenses 17875

NET Profit 4625

Marginal costing: marginal costing system is a cost determination system which includes only

variable production expenses the cost of production and fixed manufacturing expenses are charged

over the period. In this method, factory cost of the product varies according to the production

volume and for this reason; it is also known as variable costing.

12

Particular's Amount £

Sales (35*1500) 52500

Cost of Sold units

Opening Inventory NIL

ADD: the cost of Production 2000*20 40000

LESS: Closing Inventory 500*20 10000

Total Cost Of Sold units 30000

Contribution 22500

(Under) / Over Absorption of

overheads Nil

Variable selling and distribution

expense 7875

Fix Selling and distribution expenses 10000

Total selling and distribution expenses 17875

NET Profit 4625

Marginal costing: marginal costing system is a cost determination system which includes only

variable production expenses the cost of production and fixed manufacturing expenses are charged

over the period. In this method, factory cost of the product varies according to the production

volume and for this reason; it is also known as variable costing.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 31

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.