Management Accounting Report: Flexed Budget, Variance Analysis

VerifiedAdded on 2023/06/07

|12

|3246

|361

Report

AI Summary

This management accounting report analyzes the performance of Amana's business, a souvenir seller affected by the Covid-19 pandemic. It includes a monthly control report comparing original and flexed budgets, highlighting unfavorable variances in revenue, material costs, and labor costs due to reduced tourism and increased production expenses. The report recommends focusing on product quality and exploring alternative suppliers to improve profit margins. Furthermore, it compares the options of setting up an own website versus using Amazon for online sales, concluding that an own website would generate greater profit despite higher initial costs. The report also discusses the pros and cons associated with the two alternatives of going online.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

PART A.......................................................................................................................................3

PART B.......................................................................................................................................7

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................11

Books and Journals....................................................................................................................11

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

PART A.......................................................................................................................................3

PART B.......................................................................................................................................7

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................11

Books and Journals....................................................................................................................11

INTRODUCTION

Management accounting aids the management in carrying out their function of planning

& controlling in an effective manner (Han and et.al., 2020). Here the management makes use of

all the available information of both financial as well as non – financial nature to enhance the

overall organizational efficiency. Hence, management accounting is useful for the internal

purposes of the business as several prudent decisions are made on the basis of reports prepared

under it. The present report is based on one such aspect of the management accounting where on

the basis of actual results and original budget, the flexed budget would be prepared for the

Amana’s business and accordingly, the variances that have occurred between the actual results

and flexed budget would be identified. Amana’s business is one such business whose

performance have affected severely due to the implications of lockdowns resulting from the

pandemic Covid – 19 during the year 2020. Therefore, the performance of the business in terms

of units produced and sold has negatively affected as they are dealing in souvenirs for tourists.

Accordingly, the original budget becomes impractical to be compared with the actual results and

thus, the flexed budget have been prepared for the Amana’s business. In a flexed budget, the

figures of several expenses varies with the actual performance in terms of units produced and

sold while keeping many other expenses as fixed.

MAIN BODY

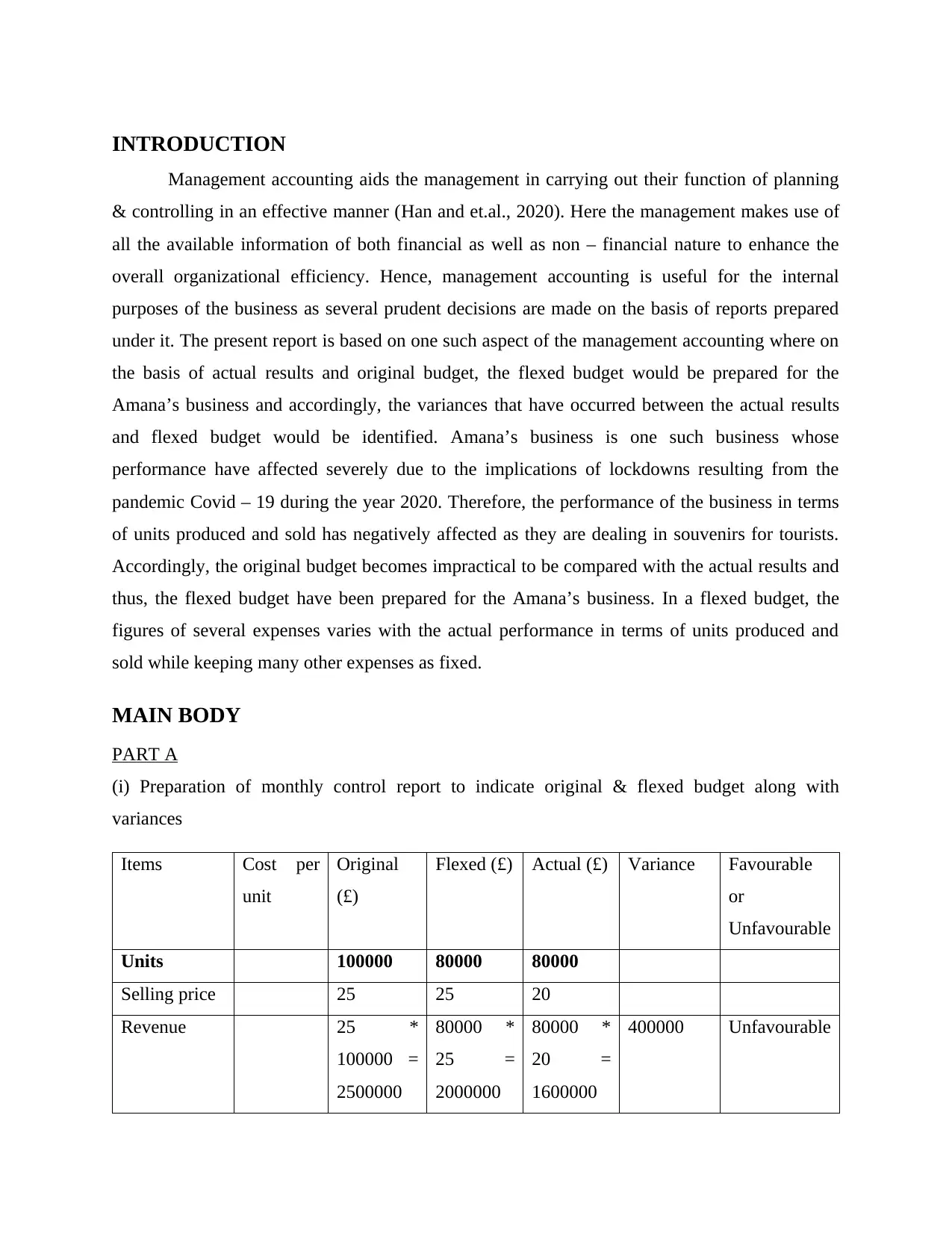

PART A

(i) Preparation of monthly control report to indicate original & flexed budget along with

variances

Items Cost per

unit

Original

(£)

Flexed (£) Actual (£) Variance Favourable

or

Unfavourable

Units 100000 80000 80000

Selling price 25 25 20

Revenue 25 *

100000 =

2500000

80000 *

25 =

2000000

80000 *

20 =

1600000

400000 Unfavourable

Management accounting aids the management in carrying out their function of planning

& controlling in an effective manner (Han and et.al., 2020). Here the management makes use of

all the available information of both financial as well as non – financial nature to enhance the

overall organizational efficiency. Hence, management accounting is useful for the internal

purposes of the business as several prudent decisions are made on the basis of reports prepared

under it. The present report is based on one such aspect of the management accounting where on

the basis of actual results and original budget, the flexed budget would be prepared for the

Amana’s business and accordingly, the variances that have occurred between the actual results

and flexed budget would be identified. Amana’s business is one such business whose

performance have affected severely due to the implications of lockdowns resulting from the

pandemic Covid – 19 during the year 2020. Therefore, the performance of the business in terms

of units produced and sold has negatively affected as they are dealing in souvenirs for tourists.

Accordingly, the original budget becomes impractical to be compared with the actual results and

thus, the flexed budget have been prepared for the Amana’s business. In a flexed budget, the

figures of several expenses varies with the actual performance in terms of units produced and

sold while keeping many other expenses as fixed.

MAIN BODY

PART A

(i) Preparation of monthly control report to indicate original & flexed budget along with

variances

Items Cost per

unit

Original

(£)

Flexed (£) Actual (£) Variance Favourable

or

Unfavourable

Units 100000 80000 80000

Selling price 25 25 20

Revenue 25 *

100000 =

2500000

80000 *

25 =

2000000

80000 *

20 =

1600000

400000 Unfavourable

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Variable

costs:

Materials 2.5 250000 200000 280000 80000 Unfavourable

Labour 4 400000 320000 440000 120000 Unfavourable

Overhead 1.5 150000 120000 120000 0 -

Contributio

n

17 1700000 1360000 760000 600000 Unfavourable

Fixed

Overheads:

Warehouse

rental

200000 200000 200000 170000 30000 Favourable

Insurance 100000 100000 100000 100000 0 -

Full time

warehouse

Supervisor

Salary

50000 50000 50000 35000 15000 Favourable

Profit 1350000 1010000 455000 555000 Unfavourable

(ii) Amana’s performance for the year ending 2020

Amana’s business is a family owned business dealing or selling souvenirs to the tourists

travelling to England and nearby destinations. Therefore, with the advent of pandemic and

resulting lockdowns in the year 2020, the performance of this business get negatively affected as

evidenced in the control report prepared above where it can be observed that the selling price of

the souvenirs have reduced leading to lower revenue earned during the year. Further, the units

sold has also been reduced because of lower demand due to travelling restrictions imposed by the

government. To deal with the reduced demand, the management may have reduced their selling

price, so that customer’s confidence can be increased. As a result of dual consequences, the

profit margins of souvenirs sellers has also reduced. The control report above is showing both

actual activity as well as the flexed activity of the business, where the profit margins actually

obtained through selling souvenirs at £20 per unit is found to be lower than the profit margins

costs:

Materials 2.5 250000 200000 280000 80000 Unfavourable

Labour 4 400000 320000 440000 120000 Unfavourable

Overhead 1.5 150000 120000 120000 0 -

Contributio

n

17 1700000 1360000 760000 600000 Unfavourable

Fixed

Overheads:

Warehouse

rental

200000 200000 200000 170000 30000 Favourable

Insurance 100000 100000 100000 100000 0 -

Full time

warehouse

Supervisor

Salary

50000 50000 50000 35000 15000 Favourable

Profit 1350000 1010000 455000 555000 Unfavourable

(ii) Amana’s performance for the year ending 2020

Amana’s business is a family owned business dealing or selling souvenirs to the tourists

travelling to England and nearby destinations. Therefore, with the advent of pandemic and

resulting lockdowns in the year 2020, the performance of this business get negatively affected as

evidenced in the control report prepared above where it can be observed that the selling price of

the souvenirs have reduced leading to lower revenue earned during the year. Further, the units

sold has also been reduced because of lower demand due to travelling restrictions imposed by the

government. To deal with the reduced demand, the management may have reduced their selling

price, so that customer’s confidence can be increased. As a result of dual consequences, the

profit margins of souvenirs sellers has also reduced. The control report above is showing both

actual activity as well as the flexed activity of the business, where the profit margins actually

obtained through selling souvenirs at £20 per unit is found to be lower than the profit margins

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

indicated in the flexed budget at £25 per unit. However, units sold is same in both the cases that

is, actual results and flexed budget which is amounting to 80000 units. The reason for the

depleted revenue of Amana’s business is the lockdowns imposed in 2020 and 2021 where the

expected demand has not realized because of non-arrival of tourists as well as the business model

being the physical one only. Many businesses are able to realized their expected revenue by

immediately moving their operations over the online platform, however, the same is not true in

case of Amana where the use of websites is restricted to marketing activities only.

Moving on to the cost performance of the business, it has been identified that the cost of

labor & materials have risen during 2020 which resulted in variances of unfavorable nature in it.

The reason for which the negative variation has occurred in the costs of labor & materials is due

to the actual costs being higher than what has been expected while preparing the original budget.

There are several reason cited for such cost variations, where the one is customer’s purchasing

power being poor leading to lower confidence among businesses & producers to produce more

(Anoushiravani and et.al., 2020). This in turn have resulted in reduced production rate in the

market which makes it difficult to recover the fixed costs of the business. Thus, due to the rise of

such situations, the prices of raw materials gets increased. With this, the cost that this business is

paying to a China based manufacturer gets increased and this burden of rising costs have not

been passed on to the customers and instead they have reduced the souvenir’s price to encourage

higher demand from customers. This pricing strategy is not considered as a sustainable strategy

of enhancing revenue as it results in lower profit margins which makes it difficult to concentrate

on activities pertaining to marketing & branding as well as the better quality of souvenirs. Due to

this, it is not possible to ensure growth & development of the business in future (Aladejebi,

2020). Through the control report, it has been determined that the performance of Amana’s

business has deteriorated in many ways like decrease in the number of units sold, rising costs of

production, reduced selling price of souvenirs and all these have resulted in reduced profit

margins for their business.

Further, the nature of overheads is such where there may only fixed or variable

component both, and accordingly, in case of being fixed only, then it does not change with the

activity level of the business which in turn accounts for as a fixed cost in the books. However,

there are many instances where the overheads changed with the activity level by being on per

is, actual results and flexed budget which is amounting to 80000 units. The reason for the

depleted revenue of Amana’s business is the lockdowns imposed in 2020 and 2021 where the

expected demand has not realized because of non-arrival of tourists as well as the business model

being the physical one only. Many businesses are able to realized their expected revenue by

immediately moving their operations over the online platform, however, the same is not true in

case of Amana where the use of websites is restricted to marketing activities only.

Moving on to the cost performance of the business, it has been identified that the cost of

labor & materials have risen during 2020 which resulted in variances of unfavorable nature in it.

The reason for which the negative variation has occurred in the costs of labor & materials is due

to the actual costs being higher than what has been expected while preparing the original budget.

There are several reason cited for such cost variations, where the one is customer’s purchasing

power being poor leading to lower confidence among businesses & producers to produce more

(Anoushiravani and et.al., 2020). This in turn have resulted in reduced production rate in the

market which makes it difficult to recover the fixed costs of the business. Thus, due to the rise of

such situations, the prices of raw materials gets increased. With this, the cost that this business is

paying to a China based manufacturer gets increased and this burden of rising costs have not

been passed on to the customers and instead they have reduced the souvenir’s price to encourage

higher demand from customers. This pricing strategy is not considered as a sustainable strategy

of enhancing revenue as it results in lower profit margins which makes it difficult to concentrate

on activities pertaining to marketing & branding as well as the better quality of souvenirs. Due to

this, it is not possible to ensure growth & development of the business in future (Aladejebi,

2020). Through the control report, it has been determined that the performance of Amana’s

business has deteriorated in many ways like decrease in the number of units sold, rising costs of

production, reduced selling price of souvenirs and all these have resulted in reduced profit

margins for their business.

Further, the nature of overheads is such where there may only fixed or variable

component both, and accordingly, in case of being fixed only, then it does not change with the

activity level of the business which in turn accounts for as a fixed cost in the books. However,

there are many instances where the overheads changed with the activity level by being on per

unit basis. The same is what true for the business of Amana where on taking into account the

overheads expenses associated with business, it has been found out that the rate at which the

overheads are charged to per unit has been fixed but it is changing with the level of production

(Alshater, Atayah and Khan, 2022). As the units produced and sold have been changed in the

budget period from 100000 to 80000 units, there seems a favorable variance in overheads cost of

the business. In other words, due to less number of units produced during the year 2020, there

were reduction in the overheads accordingly. No variation has been identified within the figures

obtained for actual and flexed budget which means the rate at which the overhead was charged

remains the same during the budget period that is 2020.

Comparing the rental expenses associated with the warehouse, the same has been reduced

during the year as against what has been budgeted in original & flexed budget (Knight and et.al.,

2020). This in turn have resulted in favorable variance as indicated in the above control report.

The reason for which such variances have occurred may include the lesser space requirement

linked with lower level of production because of the emergence of Covid – 19. The control

report shows that the actual insurance cost is consistent with the original as well as the flexed

budget which means it is a pure fixed cost and accordingly, not changing with the changing level

of business activity in 2020.

In the end of the control report, we can see the salary expenses associated with the full

time supervisor has reduced and accordingly, giving favorable variance (Yang, Liu and Chen,

2020). The reason for this can be cited as the business closure resulting from the lockdowns

imposed in 2020 which leads to lower payment to the warehouse supervisor.

Recommendations to the CEO with regards to the areas of improvement

After conducting the evaluation of performance during 2020 of Amana’s business, there are

several areas that needs the attention of management for the overall improvement of business

performance such as the following:

Rising Material & labor cost

Reduced selling price of souvenirs

Reduced profit margins

overheads expenses associated with business, it has been found out that the rate at which the

overheads are charged to per unit has been fixed but it is changing with the level of production

(Alshater, Atayah and Khan, 2022). As the units produced and sold have been changed in the

budget period from 100000 to 80000 units, there seems a favorable variance in overheads cost of

the business. In other words, due to less number of units produced during the year 2020, there

were reduction in the overheads accordingly. No variation has been identified within the figures

obtained for actual and flexed budget which means the rate at which the overhead was charged

remains the same during the budget period that is 2020.

Comparing the rental expenses associated with the warehouse, the same has been reduced

during the year as against what has been budgeted in original & flexed budget (Knight and et.al.,

2020). This in turn have resulted in favorable variance as indicated in the above control report.

The reason for which such variances have occurred may include the lesser space requirement

linked with lower level of production because of the emergence of Covid – 19. The control

report shows that the actual insurance cost is consistent with the original as well as the flexed

budget which means it is a pure fixed cost and accordingly, not changing with the changing level

of business activity in 2020.

In the end of the control report, we can see the salary expenses associated with the full

time supervisor has reduced and accordingly, giving favorable variance (Yang, Liu and Chen,

2020). The reason for this can be cited as the business closure resulting from the lockdowns

imposed in 2020 which leads to lower payment to the warehouse supervisor.

Recommendations to the CEO with regards to the areas of improvement

After conducting the evaluation of performance during 2020 of Amana’s business, there are

several areas that needs the attention of management for the overall improvement of business

performance such as the following:

Rising Material & labor cost

Reduced selling price of souvenirs

Reduced profit margins

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

For the improvement of these areas, the management should go with the following suggestion:

The management should concentrate on the quality of their product to enhance its

demand in the market rather than going with the reduction in selling price (Prayag, 2020).

By doing so, they would be able to keep up with the target profit margins by not

compromising with their product’s quality. The selling price should not be reduced

because the material & labor costs are rising and in such situation, the demand could not

be raised without compromising on quality and profit margins as well.

For the reduction in the material & labor cost, it would be recommended to the

management to find another supplier for their raw materials who could supply the

required material at a lower cost (Nishimura, 2019). Accordingly, it would resolve dual

issues of the business that is, improvement in profit margins as well as the reduction in

the materials & labor costs.

Again, for the reduction in the per unit cost of labor, the manufacturer in China should be

recommended to find cheap labor and adopt efficient technology. This would be helpful

for the business in enhancing the productivity of its labors because efficient technology

consumes less production hours.

With regards to the business profitability which is another important area requiring

immediate attention of the management (Iliemena and Amedu, 2019). The best way

through which the management can meet their target profit figures involves greater

emphasis on product’s quality, branding & marketing. However, such ways could not be

adopted while reducing the souvenir’s prices. Accordingly, it would be better for the

Amana’s business to go with the strategy of sustainable pricing rather than reducing their

selling prices for greater customer attention.

PART B

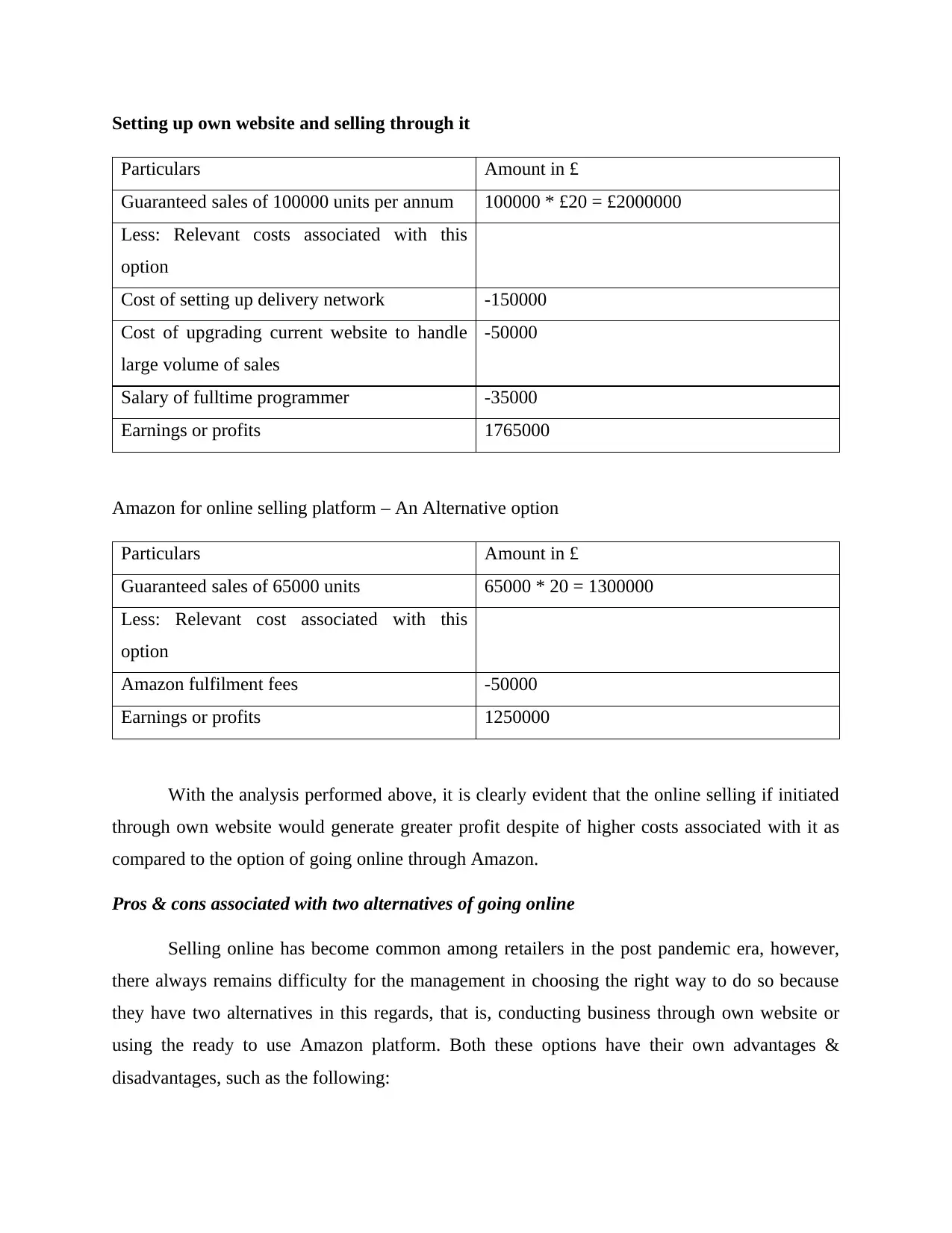

Comparison among two options for selling products online

The following analysis of the 2 business options available with the management of souvenirs

sellers will be done by assuming the price per unit of souvenirs as £20 (it is the only price at

which the souvenirs were sold in 2020). During analysis & comparison of options available with

Amana’s CEO, both the benefits and relevant costs will be taken into account.

The management should concentrate on the quality of their product to enhance its

demand in the market rather than going with the reduction in selling price (Prayag, 2020).

By doing so, they would be able to keep up with the target profit margins by not

compromising with their product’s quality. The selling price should not be reduced

because the material & labor costs are rising and in such situation, the demand could not

be raised without compromising on quality and profit margins as well.

For the reduction in the material & labor cost, it would be recommended to the

management to find another supplier for their raw materials who could supply the

required material at a lower cost (Nishimura, 2019). Accordingly, it would resolve dual

issues of the business that is, improvement in profit margins as well as the reduction in

the materials & labor costs.

Again, for the reduction in the per unit cost of labor, the manufacturer in China should be

recommended to find cheap labor and adopt efficient technology. This would be helpful

for the business in enhancing the productivity of its labors because efficient technology

consumes less production hours.

With regards to the business profitability which is another important area requiring

immediate attention of the management (Iliemena and Amedu, 2019). The best way

through which the management can meet their target profit figures involves greater

emphasis on product’s quality, branding & marketing. However, such ways could not be

adopted while reducing the souvenir’s prices. Accordingly, it would be better for the

Amana’s business to go with the strategy of sustainable pricing rather than reducing their

selling prices for greater customer attention.

PART B

Comparison among two options for selling products online

The following analysis of the 2 business options available with the management of souvenirs

sellers will be done by assuming the price per unit of souvenirs as £20 (it is the only price at

which the souvenirs were sold in 2020). During analysis & comparison of options available with

Amana’s CEO, both the benefits and relevant costs will be taken into account.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Setting up own website and selling through it

Particulars Amount in £

Guaranteed sales of 100000 units per annum 100000 * £20 = £2000000

Less: Relevant costs associated with this

option

Cost of setting up delivery network -150000

Cost of upgrading current website to handle

large volume of sales

-50000

Salary of fulltime programmer -35000

Earnings or profits 1765000

Amazon for online selling platform – An Alternative option

Particulars Amount in £

Guaranteed sales of 65000 units 65000 * 20 = 1300000

Less: Relevant cost associated with this

option

Amazon fulfilment fees -50000

Earnings or profits 1250000

With the analysis performed above, it is clearly evident that the online selling if initiated

through own website would generate greater profit despite of higher costs associated with it as

compared to the option of going online through Amazon.

Pros & cons associated with two alternatives of going online

Selling online has become common among retailers in the post pandemic era, however,

there always remains difficulty for the management in choosing the right way to do so because

they have two alternatives in this regards, that is, conducting business through own website or

using the ready to use Amazon platform. Both these options have their own advantages &

disadvantages, such as the following:

Particulars Amount in £

Guaranteed sales of 100000 units per annum 100000 * £20 = £2000000

Less: Relevant costs associated with this

option

Cost of setting up delivery network -150000

Cost of upgrading current website to handle

large volume of sales

-50000

Salary of fulltime programmer -35000

Earnings or profits 1765000

Amazon for online selling platform – An Alternative option

Particulars Amount in £

Guaranteed sales of 65000 units 65000 * 20 = 1300000

Less: Relevant cost associated with this

option

Amazon fulfilment fees -50000

Earnings or profits 1250000

With the analysis performed above, it is clearly evident that the online selling if initiated

through own website would generate greater profit despite of higher costs associated with it as

compared to the option of going online through Amazon.

Pros & cons associated with two alternatives of going online

Selling online has become common among retailers in the post pandemic era, however,

there always remains difficulty for the management in choosing the right way to do so because

they have two alternatives in this regards, that is, conducting business through own website or

using the ready to use Amazon platform. Both these options have their own advantages &

disadvantages, such as the following:

Competition: Amazon platforms is open for all business to sell their products online and

accordingly there are millions of sellers for the similar products making it quite difficult to create

their unique brand image because cut throat competition is always there for quality & price

(Kaplan and Gallani, 2021). However, there are ways with the adoption of which businesses can

be outperform other sellers which includes ratings, sponsored ads and reviews. Another problem

resulting from competition at Amazon is the lesser control that could be exercised over the

business pricing & return related policies. This is because keeping own policies aligned with

other players is necessary for greater visibility of the brand. Therefore, in such situation, going

with own website option is considered to advantageous because higher sales and accordingly

profitability is possible here in the absence of competition.

Cost / Ownership: Cost of storage in case of Amazon largely rely upon the product’s

weight & size along with the duration for which it is stored (Bergmann, and et.al., 2020). The

analysis of alternative options done above indicates the total cost associated with each option and

accordingly the cost of setting up own website comes to £235000 while the cost of going with

Amazon platform comes to £50000. The reason for the differences in cost is due to the less

expenditure associated with initial investment for the option of Amazon. Usually it is the

tendency of the businesses to exercise greater ownership and the same could be possible in going

with own website because Amazon only facilitates renting out of the platform. Another difficulty

for the businesses arise while selling on Amazon is to establish their own identity but

simultaneously there is an opportunity of greater branding over this platform which sometimes

creates unique propositions for the business.

Convenience: As discussed above, that Amazon requires less amount to be invested

initially as compared to own website (Juliana, Gani and Jermias, 2021). The reason for this is

that Amazon provides with the readymade platform for targeting huge audience which makes it

convenient for the business to go online in an easier way. Accordingly, for greater convenience,

Amazon is the better option due to less efforts required for initiating trading activities online

with a lower cost amounted £50000 on account of fulfilment fees. This fee is charged for several

benefits additionally offered by it such as quick delivery, sufficient storage facility, lower

charges for shipping, prime tag, etc.

accordingly there are millions of sellers for the similar products making it quite difficult to create

their unique brand image because cut throat competition is always there for quality & price

(Kaplan and Gallani, 2021). However, there are ways with the adoption of which businesses can

be outperform other sellers which includes ratings, sponsored ads and reviews. Another problem

resulting from competition at Amazon is the lesser control that could be exercised over the

business pricing & return related policies. This is because keeping own policies aligned with

other players is necessary for greater visibility of the brand. Therefore, in such situation, going

with own website option is considered to advantageous because higher sales and accordingly

profitability is possible here in the absence of competition.

Cost / Ownership: Cost of storage in case of Amazon largely rely upon the product’s

weight & size along with the duration for which it is stored (Bergmann, and et.al., 2020). The

analysis of alternative options done above indicates the total cost associated with each option and

accordingly the cost of setting up own website comes to £235000 while the cost of going with

Amazon platform comes to £50000. The reason for the differences in cost is due to the less

expenditure associated with initial investment for the option of Amazon. Usually it is the

tendency of the businesses to exercise greater ownership and the same could be possible in going

with own website because Amazon only facilitates renting out of the platform. Another difficulty

for the businesses arise while selling on Amazon is to establish their own identity but

simultaneously there is an opportunity of greater branding over this platform which sometimes

creates unique propositions for the business.

Convenience: As discussed above, that Amazon requires less amount to be invested

initially as compared to own website (Juliana, Gani and Jermias, 2021). The reason for this is

that Amazon provides with the readymade platform for targeting huge audience which makes it

convenient for the business to go online in an easier way. Accordingly, for greater convenience,

Amazon is the better option due to less efforts required for initiating trading activities online

with a lower cost amounted £50000 on account of fulfilment fees. This fee is charged for several

benefits additionally offered by it such as quick delivery, sufficient storage facility, lower

charges for shipping, prime tag, etc.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CONCLUSION

From the analysis performed in this report, it has been concluded that business closures

associated with the governmental restrictions and lockdowns imposed for many times in the year

2020, the performance of business have deteriorated much especially those businesses who were

not being able to immediately shift their business activities online. The same problem is being

identified in the business case of Amana which remains operative through the year 2020 with

their physical stores. However, to cope up with the inability to clear their stocks, the

management resorts to decreasing their per unit sales price despite of rising corresponding

material & labor costs. This led to reduced profit margins of the business. Further, it has been

analyzed that for going online, CEO is having 2 options with them where the use of Amazon

platform is found as feasible due to lower costs involves while the option of using own website is

found to be appropriate on account of greater profitability & sales.

From the analysis performed in this report, it has been concluded that business closures

associated with the governmental restrictions and lockdowns imposed for many times in the year

2020, the performance of business have deteriorated much especially those businesses who were

not being able to immediately shift their business activities online. The same problem is being

identified in the business case of Amana which remains operative through the year 2020 with

their physical stores. However, to cope up with the inability to clear their stocks, the

management resorts to decreasing their per unit sales price despite of rising corresponding

material & labor costs. This led to reduced profit margins of the business. Further, it has been

analyzed that for going online, CEO is having 2 options with them where the use of Amazon

platform is found as feasible due to lower costs involves while the option of using own website is

found to be appropriate on account of greater profitability & sales.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Aladejebi, O., 2020. Managing small businesses in Nigeria during covid-19 crisis: impact and

survival strategies. IOSR Journal of Business and Management. 22(8). pp.24-34.

Alshater, M. M., Atayah, O. F. and Khan, A., 2022. What do we know about business and

economics research during COVID-19: a bibliometric review. Economic Research-

Ekonomska Istraživanja. 35(1). pp.1884-1912.

Anoushiravani, A. A., and et.al., 2020. Economic impacts of the COVID-19 crisis: an

orthopaedic perspective. The Journal of bone and joint surgery. American volume.

Bergmann, M., and et.al., 2020. Digitization of the budgeting process: determinants of the use of

business analytics and its effect on satisfaction with the budgeting process. Journal of

Management Control. 31(1) pp.25-54.

Han, H., and et.al., 2020. Coronavirus disease (COVID-19), traveler behaviors, and international

tourism businesses: Impact of the corporate social responsibility (CSR), knowledge,

psychological distress, attitude, and ascribed responsibility. Sustainability. 12(20).

p.8639.

Iliemena, R. O. and Amedu, J. M. A., 2019. Effect of standard costing on profitability of

manufacturing companies: study of Edo State Nigeria. Journal of Resources

Development and Management. 53(0).

Juliana, C., Gani, L. and Jermias, J., 2021. Performance implications of misalignment among

business strategy, leadership style, organizational culture and management accounting

systems. International Journal of Ethics and Systems.

Kaplan, R. S. and Gallani, S., 2021. Variance Analysis: New Insights from Health Care

ApplicationsVariance Analysis: New Insights from Health Care Applications. Issues in

Accounting Education.

Books and Journals

Aladejebi, O., 2020. Managing small businesses in Nigeria during covid-19 crisis: impact and

survival strategies. IOSR Journal of Business and Management. 22(8). pp.24-34.

Alshater, M. M., Atayah, O. F. and Khan, A., 2022. What do we know about business and

economics research during COVID-19: a bibliometric review. Economic Research-

Ekonomska Istraživanja. 35(1). pp.1884-1912.

Anoushiravani, A. A., and et.al., 2020. Economic impacts of the COVID-19 crisis: an

orthopaedic perspective. The Journal of bone and joint surgery. American volume.

Bergmann, M., and et.al., 2020. Digitization of the budgeting process: determinants of the use of

business analytics and its effect on satisfaction with the budgeting process. Journal of

Management Control. 31(1) pp.25-54.

Han, H., and et.al., 2020. Coronavirus disease (COVID-19), traveler behaviors, and international

tourism businesses: Impact of the corporate social responsibility (CSR), knowledge,

psychological distress, attitude, and ascribed responsibility. Sustainability. 12(20).

p.8639.

Iliemena, R. O. and Amedu, J. M. A., 2019. Effect of standard costing on profitability of

manufacturing companies: study of Edo State Nigeria. Journal of Resources

Development and Management. 53(0).

Juliana, C., Gani, L. and Jermias, J., 2021. Performance implications of misalignment among

business strategy, leadership style, organizational culture and management accounting

systems. International Journal of Ethics and Systems.

Kaplan, R. S. and Gallani, S., 2021. Variance Analysis: New Insights from Health Care

ApplicationsVariance Analysis: New Insights from Health Care Applications. Issues in

Accounting Education.

Knight, D. W., and et.al., 2020. Impact of COVID-19: research note on tourism and hospitality

sectors in the epicenter of Wuhan and Hubei Province, China. International Journal of

Contemporary Hospitality Management.

Nishimura, A., 2019. Profit Opportunity, Strategic Innovation, and Management Accounting.

In Management, Uncertainty, and Accounting (pp. 97-127). Palgrave Macmillan,

Singapore.

Prayag, G., 2020. Time for reset? COVID-19 and tourism resilience. Tourism Review

International. 24(2-3). pp.179-184.

Yang, Y., Liu, H. and Chen, X., 2020. COVID-19 and restaurant demand: early effects of the

pandemic and stay-at-home orders. International Journal of Contemporary Hospitality

Management.

sectors in the epicenter of Wuhan and Hubei Province, China. International Journal of

Contemporary Hospitality Management.

Nishimura, A., 2019. Profit Opportunity, Strategic Innovation, and Management Accounting.

In Management, Uncertainty, and Accounting (pp. 97-127). Palgrave Macmillan,

Singapore.

Prayag, G., 2020. Time for reset? COVID-19 and tourism resilience. Tourism Review

International. 24(2-3). pp.179-184.

Yang, Y., Liu, H. and Chen, X., 2020. COVID-19 and restaurant demand: early effects of the

pandemic and stay-at-home orders. International Journal of Contemporary Hospitality

Management.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.