Management Accounting Report: Cost Analysis, BEP, and UCK Furniture

VerifiedAdded on 2022/12/26

|19

|3606

|40

Report

AI Summary

This management accounting report provides a comprehensive overview of key concepts and techniques, including cost analysis, budgeting, and break-even point (BEP) calculations. It begins by defining management accounting and its essential requirements, highlighting its role in formulating financial strategies, improving management procedures, and maintaining profitability. The report discusses various management accounting systems, such as inventory management, price optimization, and cost accounting, explaining their benefits and applications. It then delves into cost calculation techniques, including absorption and marginal costing, and demonstrates their application through income statements. The report also addresses practical problems in budgeting, flexible budgeting, and cash budgeting, illustrating their importance in predicting a company's future financial position. The analysis is contextualized with examples related to UCK Furniture, showcasing the practical application of management accounting principles in a real-world business scenario. Desklib provides access to this and many other solved assignments.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

PART 1 ...........................................................................................................................................1

SECTION 1......................................................................................................................................1

1.1 Management accounting and essential requirements of their types......................................1

1.2 Methods utilised for management accounting reporting.......................................................3

1.3 Benefits of management accounting systems.......................................................................4

1.4 Management accounting systems and reports integrated in organisational procedure and

importance of different methods.................................................................................................5

SECTION 2......................................................................................................................................6

2.1 Calculate cost using effective techniques for cost analysis..................................................6

2.2 Apply range of MA techniques.............................................................................................8

2.3 Accurately apply and interpret data for a range of business...............................................11

2.4 Calculation of BEP..............................................................................................................14

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................17

INTRODUCTION...........................................................................................................................1

PART 1 ...........................................................................................................................................1

SECTION 1......................................................................................................................................1

1.1 Management accounting and essential requirements of their types......................................1

1.2 Methods utilised for management accounting reporting.......................................................3

1.3 Benefits of management accounting systems.......................................................................4

1.4 Management accounting systems and reports integrated in organisational procedure and

importance of different methods.................................................................................................5

SECTION 2......................................................................................................................................6

2.1 Calculate cost using effective techniques for cost analysis..................................................6

2.2 Apply range of MA techniques.............................................................................................8

2.3 Accurately apply and interpret data for a range of business...............................................11

2.4 Calculation of BEP..............................................................................................................14

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................17

INTRODUCTION

Management accounting is a procedure of determining business costs as well as

operations to prepare internal financial report, statements, books & journal to aid manager’s

decision making procedure in accomplishing business objectives (Ugalde Vasquez and Naranjo-

Gil, 2020). The main aim of the report to understand the concept of management accounting and

enhance the quality of information that helps in decision making procedure. This report based on

the UCK furniture which is established in UK and provide their services. In this report consist of

different topics like MA systems and reports for the operation of entity, prepare income

statements that based on absorption and marginal costing. Along with identify practical problems

and prepare flexible and cash budget to predict future position of company.

PART 1

SECTION 1

1.1 Management accounting and essential requirements of their types

Management accounting is application of professional skills as well as knowledge use at

the time of preparation of accounting and financial information to assist internal management.

On this basis of these management apply different policies, planning and control of the

operations of firm. The only requirement of management accounting that data should present

their purpose that is supporting the management in effective decision making procedure.

Role of MA

Formulate financial strategies: The main role management accountant to apply effective

financial strategies in order to predict sales, prepare budget include all the incomes and

expenditure. To record all financial information in different statements as per the

requirement (Krishnan, 2020).

Improve management procedure: It is essential role in which analysis the performance of

management accordingly take further decisions. For the main activities it will increase

the major efficiency by clear and smooth inner and external procedure.

Maintain profitability: There are analysing various types of tool that use by management

accountant to maintain profitability of business. With the help of analysis, the accountant

measure revenues against fixed as well as variable cost to know breakeven point.

Principle of MA

1

Management accounting is a procedure of determining business costs as well as

operations to prepare internal financial report, statements, books & journal to aid manager’s

decision making procedure in accomplishing business objectives (Ugalde Vasquez and Naranjo-

Gil, 2020). The main aim of the report to understand the concept of management accounting and

enhance the quality of information that helps in decision making procedure. This report based on

the UCK furniture which is established in UK and provide their services. In this report consist of

different topics like MA systems and reports for the operation of entity, prepare income

statements that based on absorption and marginal costing. Along with identify practical problems

and prepare flexible and cash budget to predict future position of company.

PART 1

SECTION 1

1.1 Management accounting and essential requirements of their types

Management accounting is application of professional skills as well as knowledge use at

the time of preparation of accounting and financial information to assist internal management.

On this basis of these management apply different policies, planning and control of the

operations of firm. The only requirement of management accounting that data should present

their purpose that is supporting the management in effective decision making procedure.

Role of MA

Formulate financial strategies: The main role management accountant to apply effective

financial strategies in order to predict sales, prepare budget include all the incomes and

expenditure. To record all financial information in different statements as per the

requirement (Krishnan, 2020).

Improve management procedure: It is essential role in which analysis the performance of

management accordingly take further decisions. For the main activities it will increase

the major efficiency by clear and smooth inner and external procedure.

Maintain profitability: There are analysing various types of tool that use by management

accountant to maintain profitability of business. With the help of analysis, the accountant

measure revenues against fixed as well as variable cost to know breakeven point.

Principle of MA

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Designing and compiling: All the accounting information, reports and other activities that

based on past, present and future outcomes should be analysed and compiled to analysis

the specific business issue. It means this system designed to presenting all the related data

to sort out a specific issue.

Management by exception: This principle is followed by the management to present all

the required information and control budgetary system. In this principle compare actual

with budgeted accordingly apply changes in different costs (Diab, 2020).

The management accounting different from the financial accounting because and

Difference between financial accounting and management accounting:

Basis Management Accounting Financial Accounting

Meaning Management accounting is system

in which supply related information

to managers to develop plans and

collect all financial information.

Financial accounting is an accounting

system in which concentrated on

preparation of financial statement to

provide financial information to

related users.

Purpose To supply financial information to

external parties.

To activity the management in proper

planning and effective decision

making procedure for detailed

information on different activity.

Uses Financial accounting use by the

company to present monetary

information to external users

MA use to present financial

information to internal users.

Different types of MA system

Inventory management system: Inventory management system is a process to keep eye

on the production activities by using an unending inventory system. In simple language it can say

that when product is moving from one process to another at every stage from raw material to

final product so keep on tracking the product and also save the things in computerised system.

This all things help the manager to check on the activities and take the final decision. In the

context of UCK furniture this system is used to put track on people purchasing product for

2

based on past, present and future outcomes should be analysed and compiled to analysis

the specific business issue. It means this system designed to presenting all the related data

to sort out a specific issue.

Management by exception: This principle is followed by the management to present all

the required information and control budgetary system. In this principle compare actual

with budgeted accordingly apply changes in different costs (Diab, 2020).

The management accounting different from the financial accounting because and

Difference between financial accounting and management accounting:

Basis Management Accounting Financial Accounting

Meaning Management accounting is system

in which supply related information

to managers to develop plans and

collect all financial information.

Financial accounting is an accounting

system in which concentrated on

preparation of financial statement to

provide financial information to

related users.

Purpose To supply financial information to

external parties.

To activity the management in proper

planning and effective decision

making procedure for detailed

information on different activity.

Uses Financial accounting use by the

company to present monetary

information to external users

MA use to present financial

information to internal users.

Different types of MA system

Inventory management system: Inventory management system is a process to keep eye

on the production activities by using an unending inventory system. In simple language it can say

that when product is moving from one process to another at every stage from raw material to

final product so keep on tracking the product and also save the things in computerised system.

This all things help the manager to check on the activities and take the final decision. In the

context of UCK furniture this system is used to put track on people purchasing product for

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

further procedure. The essential requirement of this system to analysis at which stage require to

raw material and when require to order for purchase (Osim, Umoffong and Goddymkpa, 2020).

Price optimization system: Price optimization system is a mathematical process where

company check the price of the product at different level at what price customer is ready to buy

and still company earns the decant profit. The process helps company to know the price of

product where company can sell their product at maximum quantity with the level of competition

and the manufacturing cost of product. UCK furniture started using price optimization system by

analysing customer behaviour in their grocery stores which product customer is ready to buy at

what price to take the pricing and promotional decision.

Cost accounting system: Cost accounting system is system where company analyse the

cost of product by using fixed cost and variable cost. If companies want to survive or want to

earn good profit companies should know about the product that which product is profitable and

which one is not. Cost accounting system helps the companies to know the cost of product at

every level initial level, work in progress level and final level. UCK furniture is biggest super

market chain in UK so its very important for them to analyse the right cost of product. The

essential requirement of this system to analysing cost of product that manufacturer by the

company (Schaltegger, 2020).

1.2 Methods utilised for management accounting reporting

Management accounting reports: It refers as document which are preparing by the

organisation to determine the performance of each department. In these reports recorded all the

data of each division after that take right decision effectively. All the business entities use

various types of system to produce this report and supports to maintain good performance. Such

as, UCK furniture prepare this these reports in detailed manner after that take right decisions.

Inventory-management report: This report is prepared by the organisation to know

about their inventory its include the inventory waste and labour cost per hour. This report help

the companies to save the large amount of funds by utilizing the resources properly. As inventory

is most important thing for the organisation this report tells companies how they are utilizing

their inventory or where they are wasting it. UCK furniture uses this report in utilizing their

inventory they check whether every raw material of every product is used properly or not. It help

the company to save large amount of inventory by saving it from wasting.

3

raw material and when require to order for purchase (Osim, Umoffong and Goddymkpa, 2020).

Price optimization system: Price optimization system is a mathematical process where

company check the price of the product at different level at what price customer is ready to buy

and still company earns the decant profit. The process helps company to know the price of

product where company can sell their product at maximum quantity with the level of competition

and the manufacturing cost of product. UCK furniture started using price optimization system by

analysing customer behaviour in their grocery stores which product customer is ready to buy at

what price to take the pricing and promotional decision.

Cost accounting system: Cost accounting system is system where company analyse the

cost of product by using fixed cost and variable cost. If companies want to survive or want to

earn good profit companies should know about the product that which product is profitable and

which one is not. Cost accounting system helps the companies to know the cost of product at

every level initial level, work in progress level and final level. UCK furniture is biggest super

market chain in UK so its very important for them to analyse the right cost of product. The

essential requirement of this system to analysing cost of product that manufacturer by the

company (Schaltegger, 2020).

1.2 Methods utilised for management accounting reporting

Management accounting reports: It refers as document which are preparing by the

organisation to determine the performance of each department. In these reports recorded all the

data of each division after that take right decision effectively. All the business entities use

various types of system to produce this report and supports to maintain good performance. Such

as, UCK furniture prepare this these reports in detailed manner after that take right decisions.

Inventory-management report: This report is prepared by the organisation to know

about their inventory its include the inventory waste and labour cost per hour. This report help

the companies to save the large amount of funds by utilizing the resources properly. As inventory

is most important thing for the organisation this report tells companies how they are utilizing

their inventory or where they are wasting it. UCK furniture uses this report in utilizing their

inventory they check whether every raw material of every product is used properly or not. It help

the company to save large amount of inventory by saving it from wasting.

3

Cost accounting report: This report is prepared by the organisation to identify the cost

of product. It includes the raw material cost, labour cost and any other cost. It helps the company

to know about the produce price and selling price of product. By this report company can decide

their profitability on their report. Such as UCK furniture uses this report to identify the right

valuation of their product. It helps company to provide the cheap product in market which create

the large customer base for the company (Elhossade, Abdo and Mas’ud, 2020).

Account receivable report: This report is prepared by the organisation to know about

their credit available in market. It's include the company’s policies of credit return from the

people. It helps company to know about the defaulters and any other collection issue. Such as

UCK furniture uses this report to know about their bad debt and control them. It makes the

company to save large amount of money.

1.3 Benefits of management accounting systems

Relevance: Data collected by the company should be relevant to business activities and

necessary to analysis of data on periodic manner. It is duty of accountant to record all the

transactions that impact on the business activities in direct and indirect manner. Thus, it is

required to recognise reliable data and record in accounting books.

Update information: All the accounting information should be updated as per the

changes. When company apply changes in sales strategy so it impact on the results in direct

manner. Thus accordingly require to apply changes in information and provide up to date

information to manager.

Reliability: Data should impact on steady and agreeable data on collection procedure

across collection points. This procedure related to progress activities and sources data should be

clearly identified and available from manual, automated and other records for systems.

Understandable: Accounting information should be understandable that helps to get

effective ideas and easily read by the users. On the basis of such information planning about the

future activities and organize for proper decision making. Understanding is brief, complete and

effective explanation are providing in the report (Oppi, Cavicchi and Vagnoni, 2020).

Accuracy: The data record by the accountant in accounting books should be accurate

because it helps to manager in decision making procedure. If accountant do not record all the

transactions properly so data use and should be captured although if it has different uses.

Management accounting Uses Application

4

of product. It includes the raw material cost, labour cost and any other cost. It helps the company

to know about the produce price and selling price of product. By this report company can decide

their profitability on their report. Such as UCK furniture uses this report to identify the right

valuation of their product. It helps company to provide the cheap product in market which create

the large customer base for the company (Elhossade, Abdo and Mas’ud, 2020).

Account receivable report: This report is prepared by the organisation to know about

their credit available in market. It's include the company’s policies of credit return from the

people. It helps company to know about the defaulters and any other collection issue. Such as

UCK furniture uses this report to know about their bad debt and control them. It makes the

company to save large amount of money.

1.3 Benefits of management accounting systems

Relevance: Data collected by the company should be relevant to business activities and

necessary to analysis of data on periodic manner. It is duty of accountant to record all the

transactions that impact on the business activities in direct and indirect manner. Thus, it is

required to recognise reliable data and record in accounting books.

Update information: All the accounting information should be updated as per the

changes. When company apply changes in sales strategy so it impact on the results in direct

manner. Thus accordingly require to apply changes in information and provide up to date

information to manager.

Reliability: Data should impact on steady and agreeable data on collection procedure

across collection points. This procedure related to progress activities and sources data should be

clearly identified and available from manual, automated and other records for systems.

Understandable: Accounting information should be understandable that helps to get

effective ideas and easily read by the users. On the basis of such information planning about the

future activities and organize for proper decision making. Understanding is brief, complete and

effective explanation are providing in the report (Oppi, Cavicchi and Vagnoni, 2020).

Accuracy: The data record by the accountant in accounting books should be accurate

because it helps to manager in decision making procedure. If accountant do not record all the

transactions properly so data use and should be captured although if it has different uses.

Management accounting Uses Application

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

System

Cost accounting system It is using by the business to

predict the cost of product as

well as services in effective

manner. After that set price of

different products.

It is apply in the UCK

furniture to analysis cost of

each product that manufacturer

in the business.

Inventory-management system The usage of this system to

manage stock in proper

manner and determine that at

different level how many

quantity required at different

stages.

An entity apply this system to

monitor inventory at different

level and order for further

manufacturing in UCK

furniture.

Price optimisation system It is most important system

that use by the business to

conduct research from market

and carry out results of

different customers perception

in regard of their product.

This system is apply on the

UCK furniture to set effective

price structure to generate

profitability on broad manner

and take right decision.

1.4 Management accounting systems and reports integrated in organisational procedure and

importance of different methods

Different types of MA systems and reports are contributing in organisational procedure in

effective manner. UCK furniture use different system to track the performance and increase

efficiency in appropriate manner (Fadjar and Sardjudin, 2020). UCK furniture use various types

of system like price optimisation, cost accounting and inventory management system to manage

all business activities effectively. Through cost accounting predict cost of products and the report

help to manage cost in appropriate manner. Reports are using to analysis each department and

deal with different problems that can support in right decision making.

5

Cost accounting system It is using by the business to

predict the cost of product as

well as services in effective

manner. After that set price of

different products.

It is apply in the UCK

furniture to analysis cost of

each product that manufacturer

in the business.

Inventory-management system The usage of this system to

manage stock in proper

manner and determine that at

different level how many

quantity required at different

stages.

An entity apply this system to

monitor inventory at different

level and order for further

manufacturing in UCK

furniture.

Price optimisation system It is most important system

that use by the business to

conduct research from market

and carry out results of

different customers perception

in regard of their product.

This system is apply on the

UCK furniture to set effective

price structure to generate

profitability on broad manner

and take right decision.

1.4 Management accounting systems and reports integrated in organisational procedure and

importance of different methods

Different types of MA systems and reports are contributing in organisational procedure in

effective manner. UCK furniture use different system to track the performance and increase

efficiency in appropriate manner (Fadjar and Sardjudin, 2020). UCK furniture use various types

of system like price optimisation, cost accounting and inventory management system to manage

all business activities effectively. Through cost accounting predict cost of products and the report

help to manage cost in appropriate manner. Reports are using to analysis each department and

deal with different problems that can support in right decision making.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

SECTION 2

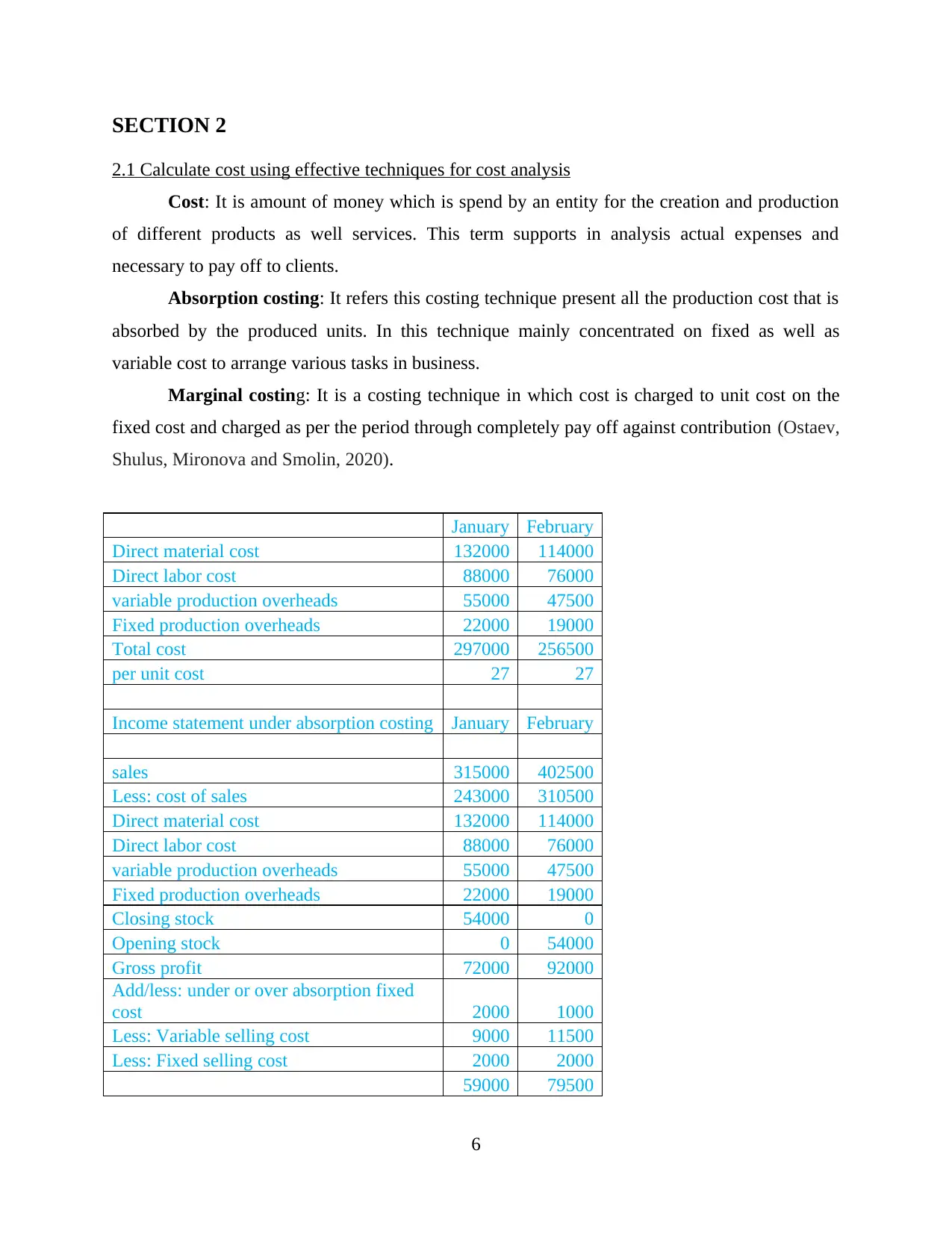

2.1 Calculate cost using effective techniques for cost analysis

Cost: It is amount of money which is spend by an entity for the creation and production

of different products as well services. This term supports in analysis actual expenses and

necessary to pay off to clients.

Absorption costing: It refers this costing technique present all the production cost that is

absorbed by the produced units. In this technique mainly concentrated on fixed as well as

variable cost to arrange various tasks in business.

Marginal costing: It is a costing technique in which cost is charged to unit cost on the

fixed cost and charged as per the period through completely pay off against contribution (Ostaev,

Shulus, Mironova and Smolin, 2020).

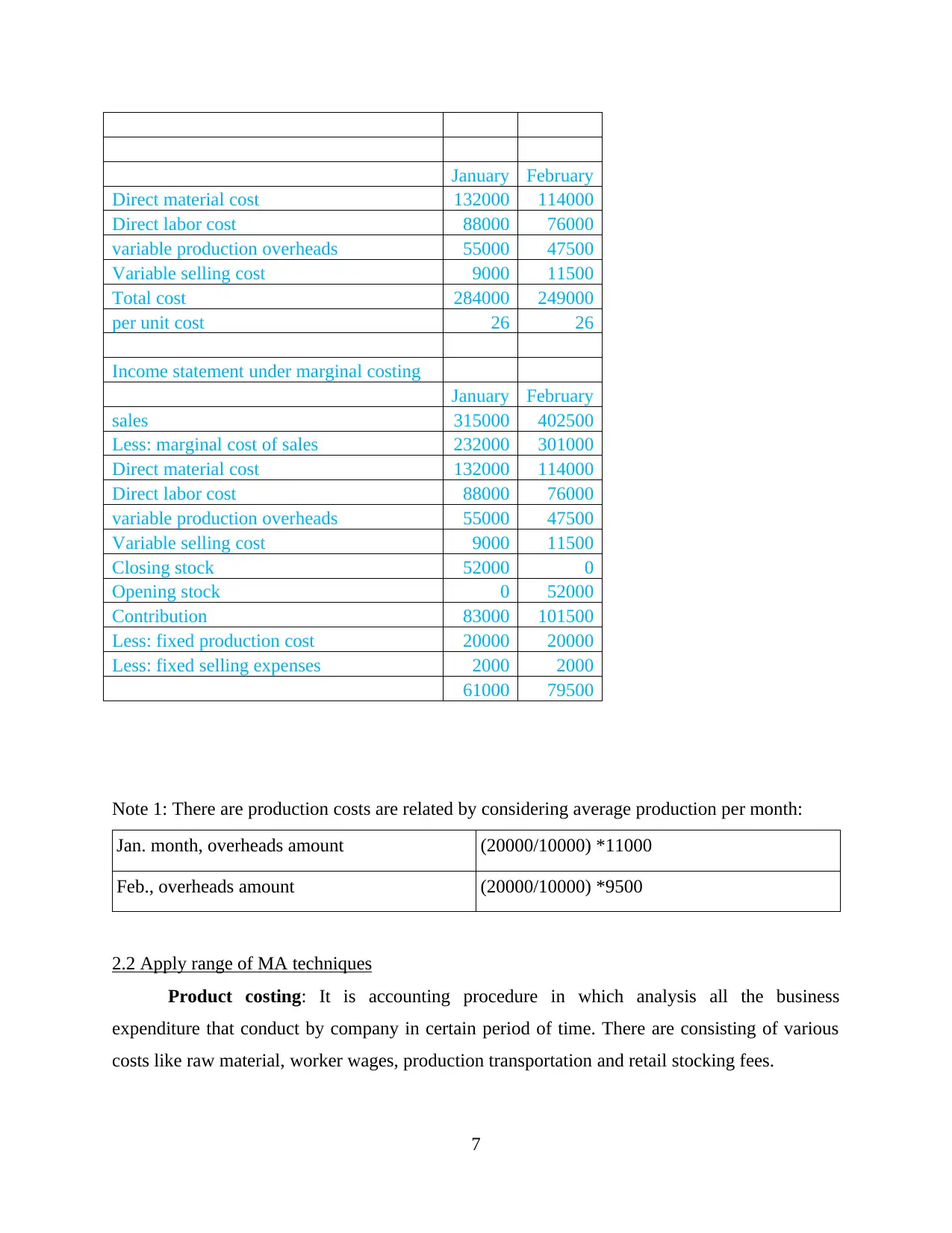

January February

Direct material cost 132000 114000

Direct labor cost 88000 76000

variable production overheads 55000 47500

Fixed production overheads 22000 19000

Total cost 297000 256500

per unit cost 27 27

Income statement under absorption costing January February

sales 315000 402500

Less: cost of sales 243000 310500

Direct material cost 132000 114000

Direct labor cost 88000 76000

variable production overheads 55000 47500

Fixed production overheads 22000 19000

Closing stock 54000 0

Opening stock 0 54000

Gross profit 72000 92000

Add/less: under or over absorption fixed

cost 2000 1000

Less: Variable selling cost 9000 11500

Less: Fixed selling cost 2000 2000

59000 79500

6

2.1 Calculate cost using effective techniques for cost analysis

Cost: It is amount of money which is spend by an entity for the creation and production

of different products as well services. This term supports in analysis actual expenses and

necessary to pay off to clients.

Absorption costing: It refers this costing technique present all the production cost that is

absorbed by the produced units. In this technique mainly concentrated on fixed as well as

variable cost to arrange various tasks in business.

Marginal costing: It is a costing technique in which cost is charged to unit cost on the

fixed cost and charged as per the period through completely pay off against contribution (Ostaev,

Shulus, Mironova and Smolin, 2020).

January February

Direct material cost 132000 114000

Direct labor cost 88000 76000

variable production overheads 55000 47500

Fixed production overheads 22000 19000

Total cost 297000 256500

per unit cost 27 27

Income statement under absorption costing January February

sales 315000 402500

Less: cost of sales 243000 310500

Direct material cost 132000 114000

Direct labor cost 88000 76000

variable production overheads 55000 47500

Fixed production overheads 22000 19000

Closing stock 54000 0

Opening stock 0 54000

Gross profit 72000 92000

Add/less: under or over absorption fixed

cost 2000 1000

Less: Variable selling cost 9000 11500

Less: Fixed selling cost 2000 2000

59000 79500

6

January February

Direct material cost 132000 114000

Direct labor cost 88000 76000

variable production overheads 55000 47500

Variable selling cost 9000 11500

Total cost 284000 249000

per unit cost 26 26

Income statement under marginal costing

January February

sales 315000 402500

Less: marginal cost of sales 232000 301000

Direct material cost 132000 114000

Direct labor cost 88000 76000

variable production overheads 55000 47500

Variable selling cost 9000 11500

Closing stock 52000 0

Opening stock 0 52000

Contribution 83000 101500

Less: fixed production cost 20000 20000

Less: fixed selling expenses 2000 2000

61000 79500

Note 1: There are production costs are related by considering average production per month:

Jan. month, overheads amount (20000/10000) *11000

Feb., overheads amount (20000/10000) *9500

2.2 Apply range of MA techniques

Product costing: It is accounting procedure in which analysis all the business

expenditure that conduct by company in certain period of time. There are consisting of various

costs like raw material, worker wages, production transportation and retail stocking fees.

7

Direct material cost 132000 114000

Direct labor cost 88000 76000

variable production overheads 55000 47500

Variable selling cost 9000 11500

Total cost 284000 249000

per unit cost 26 26

Income statement under marginal costing

January February

sales 315000 402500

Less: marginal cost of sales 232000 301000

Direct material cost 132000 114000

Direct labor cost 88000 76000

variable production overheads 55000 47500

Variable selling cost 9000 11500

Closing stock 52000 0

Opening stock 0 52000

Contribution 83000 101500

Less: fixed production cost 20000 20000

Less: fixed selling expenses 2000 2000

61000 79500

Note 1: There are production costs are related by considering average production per month:

Jan. month, overheads amount (20000/10000) *11000

Feb., overheads amount (20000/10000) *9500

2.2 Apply range of MA techniques

Product costing: It is accounting procedure in which analysis all the business

expenditure that conduct by company in certain period of time. There are consisting of various

costs like raw material, worker wages, production transportation and retail stocking fees.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Fixed cost: It is mainly based on particular period of time that do not change with

production activities. There are consisting of those cost that are not changing for longer period of

time (Wahyuni and Triatmanto, 2020).

Variable cost: There are including those costs that change directly and proportionally for

the modification in business activity level or volume such as direct labour, taxes and operational

expenditure.

Cost of inventory: This cost is analysed by the administration that how much stock is

required to keep and outcomes are varying as per the clients. There are mentioned different types

of inventory cost such as: Ordering cost: In this cost consist of wages and related payroll taxes as well as benefits to

assure about the labour cost in which organisation can allocate stock as per the

requirement. Holding cost: This cost refers that require to proper space to hold that stock which is

consisted risk as well as loss. On the basis of this cost analysis the cost of space, money

as well as obsolescence.

Administration cost: This cost defines that wages pay by organisation as per the

employees to associate with costs of goods sold. It is beneficial to manage certain cost of

stock and deduct to minimise cost (Łada, Kozarkiewicz and Haslam, 2020).

8

production activities. There are consisting of those cost that are not changing for longer period of

time (Wahyuni and Triatmanto, 2020).

Variable cost: There are including those costs that change directly and proportionally for

the modification in business activity level or volume such as direct labour, taxes and operational

expenditure.

Cost of inventory: This cost is analysed by the administration that how much stock is

required to keep and outcomes are varying as per the clients. There are mentioned different types

of inventory cost such as: Ordering cost: In this cost consist of wages and related payroll taxes as well as benefits to

assure about the labour cost in which organisation can allocate stock as per the

requirement. Holding cost: This cost refers that require to proper space to hold that stock which is

consisted risk as well as loss. On the basis of this cost analysis the cost of space, money

as well as obsolescence.

Administration cost: This cost defines that wages pay by organisation as per the

employees to associate with costs of goods sold. It is beneficial to manage certain cost of

stock and deduct to minimise cost (Łada, Kozarkiewicz and Haslam, 2020).

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

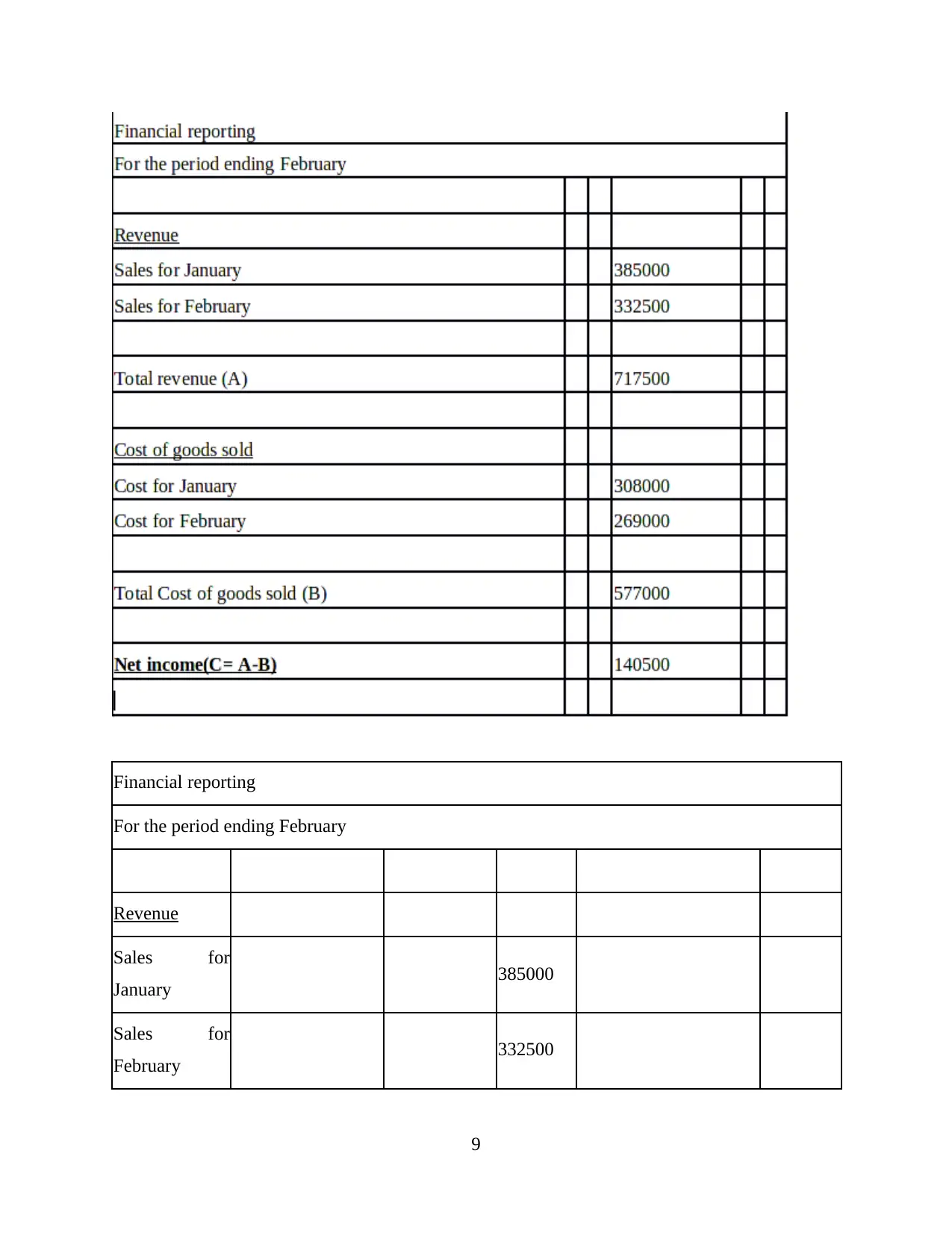

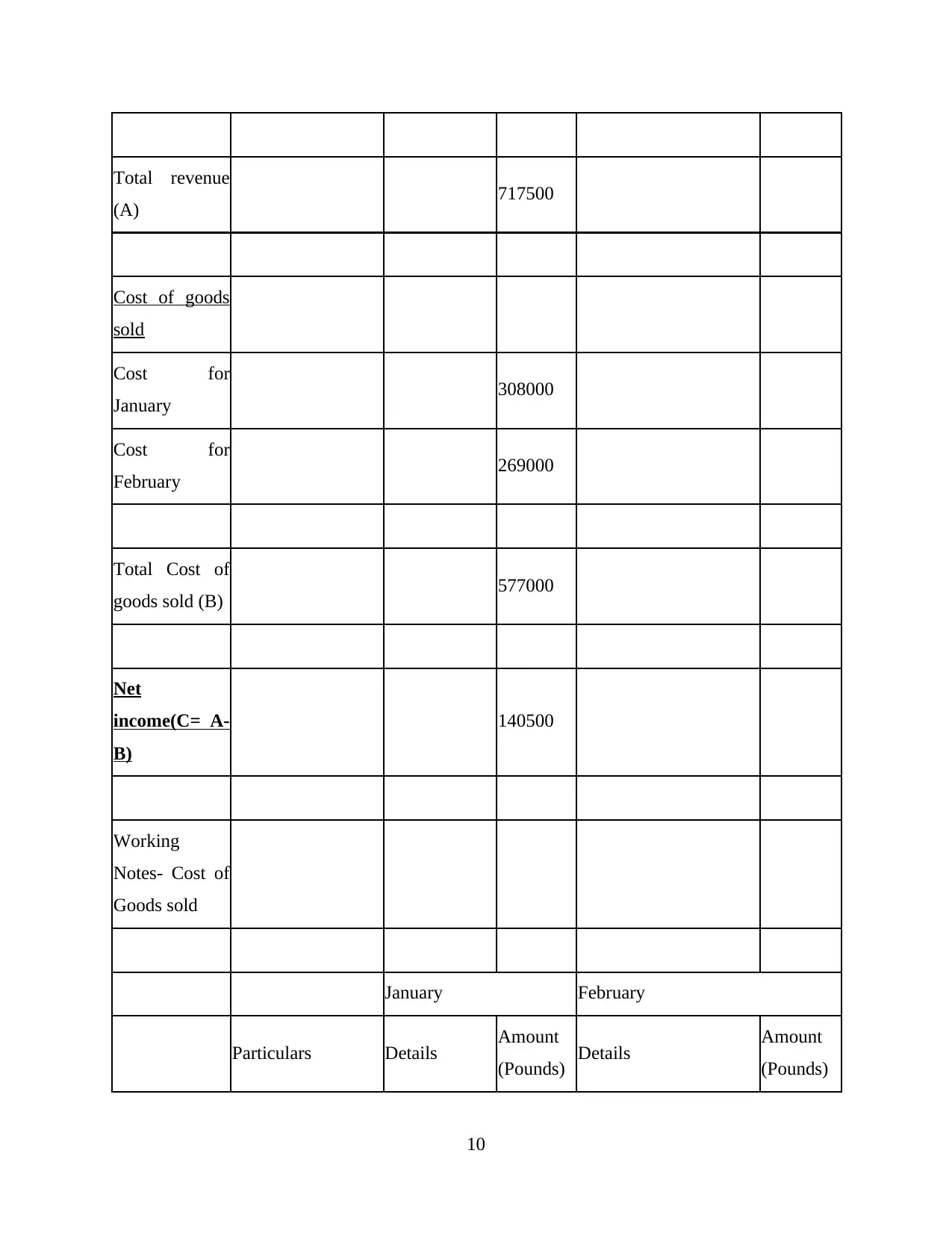

Financial reporting

For the period ending February

Revenue

Sales for

January 385000

Sales for

February 332500

9

For the period ending February

Revenue

Sales for

January 385000

Sales for

February 332500

9

Total revenue

(A) 717500

Cost of goods

sold

Cost for

January 308000

Cost for

February 269000

Total Cost of

goods sold (B) 577000

Net

income(C= A-

B)

140500

Working

Notes- Cost of

Goods sold

January February

Particulars Details Amount

(Pounds) Details Amount

(Pounds)

10

(A) 717500

Cost of goods

sold

Cost for

January 308000

Cost for

February 269000

Total Cost of

goods sold (B) 577000

Net

income(C= A-

B)

140500

Working

Notes- Cost of

Goods sold

January February

Particulars Details Amount

(Pounds) Details Amount

(Pounds)

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.