Management Accounting: Cost Analysis and Financial Reporting Methods

VerifiedAdded on 2024/06/07

|26

|4705

|379

Report

AI Summary

This report serves as a comprehensive analysis of management accounting principles, focusing on cost analysis and financial reporting techniques. It begins by explaining management accounting and its essential requirements, including inventory management, cost management, and price optimization systems. The report evaluates the benefits of these systems within an organizational context, emphasizing planning, performance review, and departmental communication. Different management accounting reporting methods, such as demand, performance, and budget reports, are discussed. The integration of management accounting systems and reporting within organizational processes is critically evaluated. The report includes detailed calculations using marginal and absorption costing to prepare income statements under different scenarios, including variance analysis for labor and material costs. The document concludes with a reconciliation of profits under both costing methods and an interpretation of data for business activities.

Management Accounting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction..................................................................................................................................3

Task 1.............................................................................................................................................4

P1................................................................................................................................................4

M1................................................................................................................................................8

P2................................................................................................................................................9

D1..............................................................................................................................................10

Task 2...........................................................................................................................................11

P3..............................................................................................................................................11

M2..............................................................................................................................................13

D2..............................................................................................................................................16

P4..............................................................................................................................................17

M3..............................................................................................................................................19

P5..............................................................................................................................................20

M4..............................................................................................................................................22

D3..............................................................................................................................................23

Conclusion..................................................................................................................................24

References..................................................................................................................................25

2

Introduction..................................................................................................................................3

Task 1.............................................................................................................................................4

P1................................................................................................................................................4

M1................................................................................................................................................8

P2................................................................................................................................................9

D1..............................................................................................................................................10

Task 2...........................................................................................................................................11

P3..............................................................................................................................................11

M2..............................................................................................................................................13

D2..............................................................................................................................................16

P4..............................................................................................................................................17

M3..............................................................................................................................................19

P5..............................................................................................................................................20

M4..............................................................................................................................................22

D3..............................................................................................................................................23

Conclusion..................................................................................................................................24

References..................................................................................................................................25

2

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

Being the management accountant in a business, the report includes the different

management accounting system of the business and their essential requirements. It

includes the benefits of the different management accounting system and its

application. Different management accounting tools will be explained such as marginal

and absorption which helps in determining the cost of the business. Different planning

tools which are used in the management accounting will also explain and how it

integrates with the business activities. The report also states the advantages and

disadvantages of the different budgetary control system and different planning tools

which helps in preparing the forecasting budget. In this report, the different

management accounting tools are adapted to respond to the financial problem of the

business.

4

Being the management accountant in a business, the report includes the different

management accounting system of the business and their essential requirements. It

includes the benefits of the different management accounting system and its

application. Different management accounting tools will be explained such as marginal

and absorption which helps in determining the cost of the business. Different planning

tools which are used in the management accounting will also explain and how it

integrates with the business activities. The report also states the advantages and

disadvantages of the different budgetary control system and different planning tools

which helps in preparing the forecasting budget. In this report, the different

management accounting tools are adapted to respond to the financial problem of the

business.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Task 1

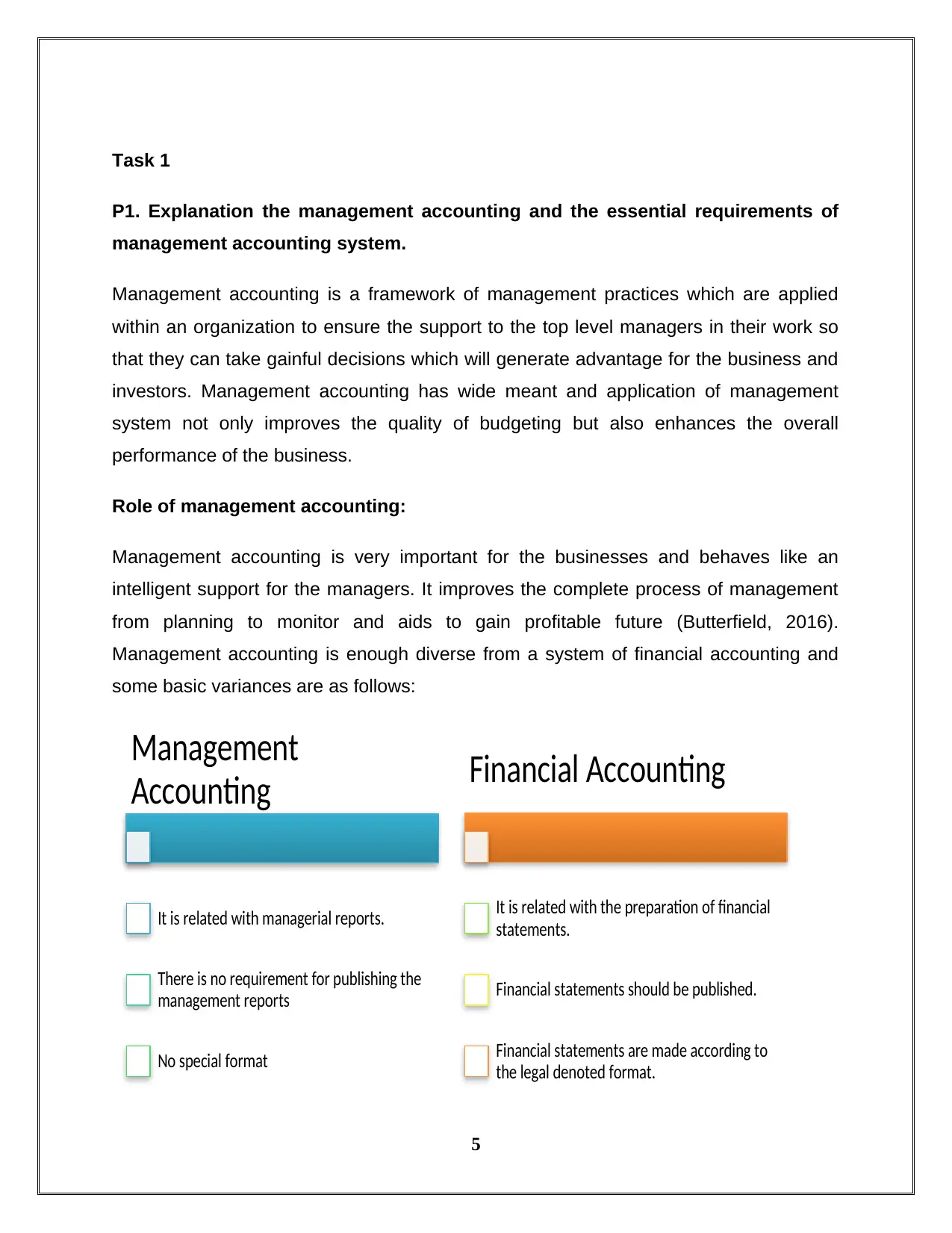

P1. Explanation the management accounting and the essential requirements of

management accounting system.

Management accounting is a framework of management practices which are applied

within an organization to ensure the support to the top level managers in their work so

that they can take gainful decisions which will generate advantage for the business and

investors. Management accounting has wide meant and application of management

system not only improves the quality of budgeting but also enhances the overall

performance of the business.

Role of management accounting:

Management accounting is very important for the businesses and behaves like an

intelligent support for the managers. It improves the complete process of management

from planning to monitor and aids to gain profitable future (Butterfield, 2016).

Management accounting is enough diverse from a system of financial accounting and

some basic variances are as follows:

5

Management

Accounting

It is related with managerial reports.

There is no requirement for publishing the

management reports

No special format

Financial Accounting

It is related with the preparation of financial

statements.

Financial statements should be published.

Financial statements are made according to

the legal denoted format.

P1. Explanation the management accounting and the essential requirements of

management accounting system.

Management accounting is a framework of management practices which are applied

within an organization to ensure the support to the top level managers in their work so

that they can take gainful decisions which will generate advantage for the business and

investors. Management accounting has wide meant and application of management

system not only improves the quality of budgeting but also enhances the overall

performance of the business.

Role of management accounting:

Management accounting is very important for the businesses and behaves like an

intelligent support for the managers. It improves the complete process of management

from planning to monitor and aids to gain profitable future (Butterfield, 2016).

Management accounting is enough diverse from a system of financial accounting and

some basic variances are as follows:

5

Management

Accounting

It is related with managerial reports.

There is no requirement for publishing the

management reports

No special format

Financial Accounting

It is related with the preparation of financial

statements.

Financial statements should be published.

Financial statements are made according to

the legal denoted format.

(Image 1: Difference in financial and management accounting)

(By Author, 2018)

Management accounting includes following activities:

• Planning: planning for the future activities to improve the quality of working.

• Controlling: management practices are applied to establish effective control of the

business process.

• Review: Review of applied strategy to improve the results.

Application of management system is necessary for a modern environment to maintain

quality in business activities because it is necessary to stay in the market. Following are

some management applications with requirements that can be applied in a business:

Inventory management system:

Inventory includes raw material, WIP stock and finished goods items which are held for

the sale purpose. Inventory management is one of the most activities of management

because it affects the organizational revenue (Viktorovna and Ivanovich, 2016). The

system of Inventory management could be well-defined as a combination of some

hardware, software and accounting practices which jointly makes a system to improve

the control of inventory flow. Following method is available for inventory management:

6

Just-In-Time Economic

Order Quantity

ABC Inventory

Analysis

FIFO Weighted

Average

(By Author, 2018)

Management accounting includes following activities:

• Planning: planning for the future activities to improve the quality of working.

• Controlling: management practices are applied to establish effective control of the

business process.

• Review: Review of applied strategy to improve the results.

Application of management system is necessary for a modern environment to maintain

quality in business activities because it is necessary to stay in the market. Following are

some management applications with requirements that can be applied in a business:

Inventory management system:

Inventory includes raw material, WIP stock and finished goods items which are held for

the sale purpose. Inventory management is one of the most activities of management

because it affects the organizational revenue (Viktorovna and Ivanovich, 2016). The

system of Inventory management could be well-defined as a combination of some

hardware, software and accounting practices which jointly makes a system to improve

the control of inventory flow. Following method is available for inventory management:

6

Just-In-Time Economic

Order Quantity

ABC Inventory

Analysis

FIFO Weighted

Average

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(Image 1: Different Inventory control Frameworks)

(By Author, 2018)

Some requirements of this system are as follows;

• Bodily security and timely review of inventory warehouses.

• Right and timely recording of inventory purchase and sales transactions (Viktorovna

and Ivanovich, 2016).

• Proper use of control methods to control the ordering and purchasing costs.

• Appropriate recording and treatment of abnormal losses.

Cost management system:

As most applied the system to manage the costs, cost management system can be

defined as an application which supports the managers in cost controlling activities to

maintain the product cost at a reasonable level (Savić, et. al., 2014). Cost management

is related to the complete recording and classification of cost related data to maintain it

at a reasonable level. Costs are classified as follows:

Direct cost: it is that cost that is connected to the consumption of direct labour, material

and overheads.

Indirect cost; a cost that is not directly related with the product but occur to produce the

product.

Fixed cost: a cost which is charged on a fixed period like rent income (Donizetti, 2016).

Variable cost: a cost which occurs according to the production volume like mat6irial

cost.

Some requirements of the system:

7

(By Author, 2018)

Some requirements of this system are as follows;

• Bodily security and timely review of inventory warehouses.

• Right and timely recording of inventory purchase and sales transactions (Viktorovna

and Ivanovich, 2016).

• Proper use of control methods to control the ordering and purchasing costs.

• Appropriate recording and treatment of abnormal losses.

Cost management system:

As most applied the system to manage the costs, cost management system can be

defined as an application which supports the managers in cost controlling activities to

maintain the product cost at a reasonable level (Savić, et. al., 2014). Cost management

is related to the complete recording and classification of cost related data to maintain it

at a reasonable level. Costs are classified as follows:

Direct cost: it is that cost that is connected to the consumption of direct labour, material

and overheads.

Indirect cost; a cost that is not directly related with the product but occur to produce the

product.

Fixed cost: a cost which is charged on a fixed period like rent income (Donizetti, 2016).

Variable cost: a cost which occurs according to the production volume like mat6irial

cost.

Some requirements of the system:

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

• Cost accounting system requires correct classification and recording of different costs

to ascertain the right cost of the product.

• If a company is engaged in the production of the product in batches separate

recording of costs as per batches.

Price optimization system:

POS is a tool of management which is used to be applied with an organization to study

the customer reaction for the prices so that management can understand the

purchasing acceptance of the product and set a reasonable price level (Yuan, et. al.,

2014). Price optimization system is applied to find a level of the price at which, sales

and revenue will be maximum.

Some requirements of this system;

• Historical data on sales and prices.

• If an organization prepares fact reports management can use those reports also.

• The report which shows product acceptance and popularity of the product.

• Trend analysis report.

8

to ascertain the right cost of the product.

• If a company is engaged in the production of the product in batches separate

recording of costs as per batches.

Price optimization system:

POS is a tool of management which is used to be applied with an organization to study

the customer reaction for the prices so that management can understand the

purchasing acceptance of the product and set a reasonable price level (Yuan, et. al.,

2014). Price optimization system is applied to find a level of the price at which, sales

and revenue will be maximum.

Some requirements of this system;

• Historical data on sales and prices.

• If an organization prepares fact reports management can use those reports also.

• The report which shows product acceptance and popularity of the product.

• Trend analysis report.

8

M1. Evaluate the benefits of management accounting systems and their

application within an organisational context

Applications of Management accounting is very useful for the businesses because it

works as an intelligent supporter for business activities from the stage of planning to

monitor. List of a management system for a business is very long and some of them are

as follows;

The superiority of planning: Super planning is must be stable in the current market

because every business is facing heavy competition and a good planning for a future

business activity helps to reduce the expenses and improve profits (Matambele, 2014).

By doing this, an organization can improve the flexibility of activities which will provide a

competitive advantage.

Review of staff performance: performance review is another benefit of the

management system. Performance reports which are made under management

reporting give complete and accurate information about the performance of each

department. Departmental performance report shows the individual efficiency of staff.

By using these tools, company management can evaluate the performance of staff and

take corrective action.

Departmental Communication and coordination: Flow of information and

coordination is necessary between different departments because it aids the

department managers to understand the current requirement of entity, for example, if a

company facing trouble in achieving the sales targets, production department should

understand the reasons because it is possible that the same problems are arising due

to quality issues (Matambele, 2014).

9

application within an organisational context

Applications of Management accounting is very useful for the businesses because it

works as an intelligent supporter for business activities from the stage of planning to

monitor. List of a management system for a business is very long and some of them are

as follows;

The superiority of planning: Super planning is must be stable in the current market

because every business is facing heavy competition and a good planning for a future

business activity helps to reduce the expenses and improve profits (Matambele, 2014).

By doing this, an organization can improve the flexibility of activities which will provide a

competitive advantage.

Review of staff performance: performance review is another benefit of the

management system. Performance reports which are made under management

reporting give complete and accurate information about the performance of each

department. Departmental performance report shows the individual efficiency of staff.

By using these tools, company management can evaluate the performance of staff and

take corrective action.

Departmental Communication and coordination: Flow of information and

coordination is necessary between different departments because it aids the

department managers to understand the current requirement of entity, for example, if a

company facing trouble in achieving the sales targets, production department should

understand the reasons because it is possible that the same problems are arising due

to quality issues (Matambele, 2014).

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

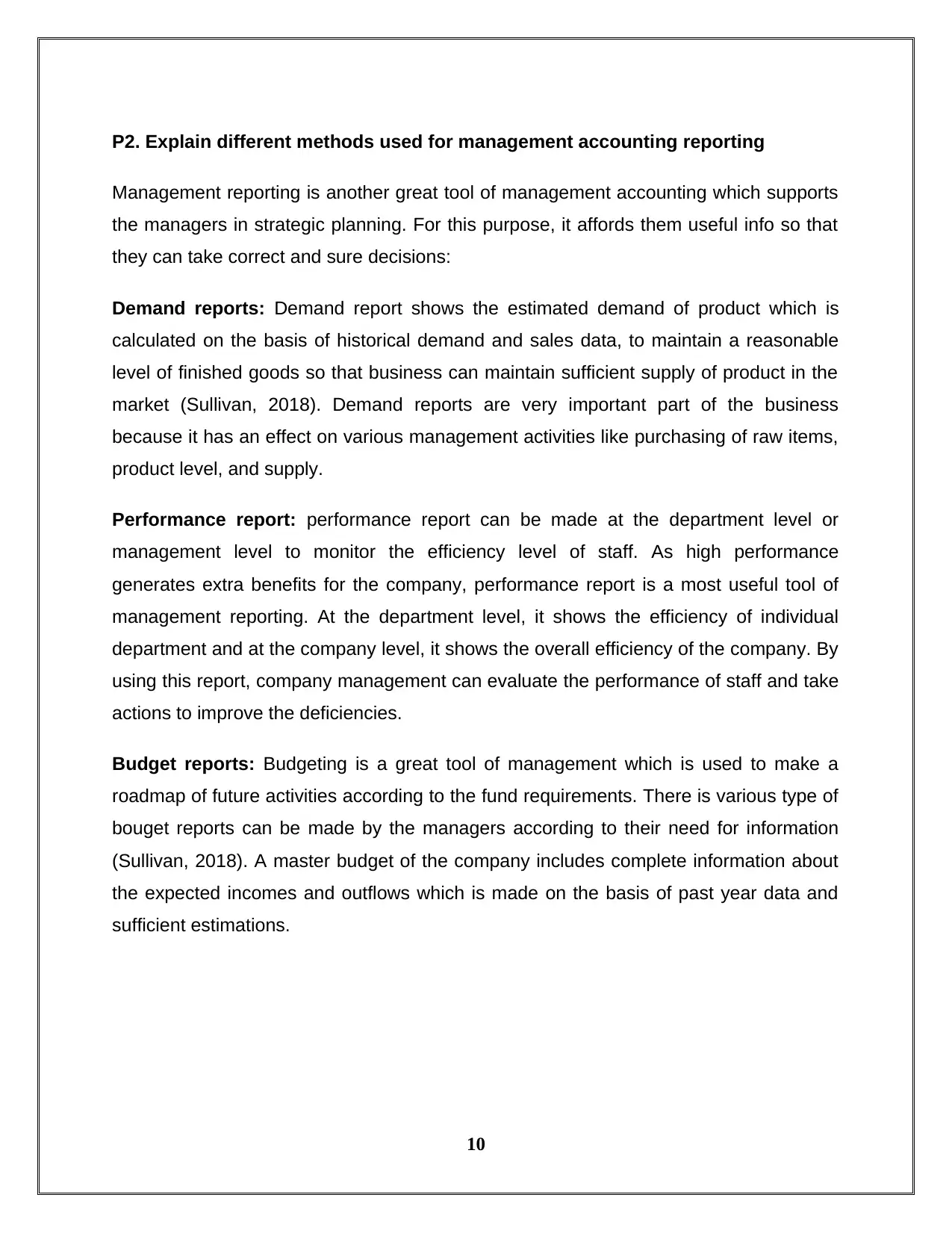

P2. Explain different methods used for management accounting reporting

Management reporting is another great tool of management accounting which supports

the managers in strategic planning. For this purpose, it affords them useful info so that

they can take correct and sure decisions:

Demand reports: Demand report shows the estimated demand of product which is

calculated on the basis of historical demand and sales data, to maintain a reasonable

level of finished goods so that business can maintain sufficient supply of product in the

market (Sullivan, 2018). Demand reports are very important part of the business

because it has an effect on various management activities like purchasing of raw items,

product level, and supply.

Performance report: performance report can be made at the department level or

management level to monitor the efficiency level of staff. As high performance

generates extra benefits for the company, performance report is a most useful tool of

management reporting. At the department level, it shows the efficiency of individual

department and at the company level, it shows the overall efficiency of the company. By

using this report, company management can evaluate the performance of staff and take

actions to improve the deficiencies.

Budget reports: Budgeting is a great tool of management which is used to make a

roadmap of future activities according to the fund requirements. There is various type of

bouget reports can be made by the managers according to their need for information

(Sullivan, 2018). A master budget of the company includes complete information about

the expected incomes and outflows which is made on the basis of past year data and

sufficient estimations.

10

Management reporting is another great tool of management accounting which supports

the managers in strategic planning. For this purpose, it affords them useful info so that

they can take correct and sure decisions:

Demand reports: Demand report shows the estimated demand of product which is

calculated on the basis of historical demand and sales data, to maintain a reasonable

level of finished goods so that business can maintain sufficient supply of product in the

market (Sullivan, 2018). Demand reports are very important part of the business

because it has an effect on various management activities like purchasing of raw items,

product level, and supply.

Performance report: performance report can be made at the department level or

management level to monitor the efficiency level of staff. As high performance

generates extra benefits for the company, performance report is a most useful tool of

management reporting. At the department level, it shows the efficiency of individual

department and at the company level, it shows the overall efficiency of the company. By

using this report, company management can evaluate the performance of staff and take

actions to improve the deficiencies.

Budget reports: Budgeting is a great tool of management which is used to make a

roadmap of future activities according to the fund requirements. There is various type of

bouget reports can be made by the managers according to their need for information

(Sullivan, 2018). A master budget of the company includes complete information about

the expected incomes and outflows which is made on the basis of past year data and

sufficient estimations.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

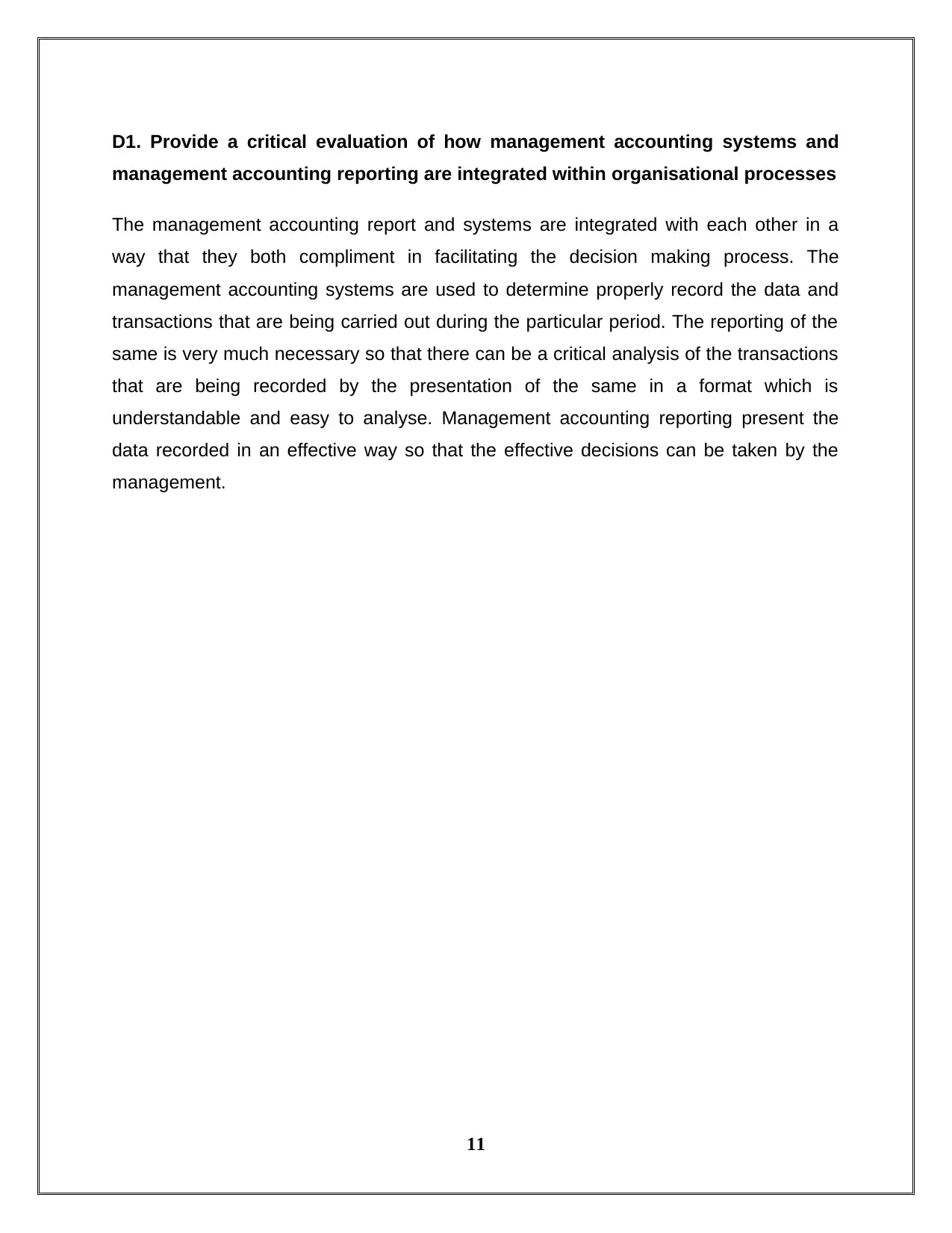

D1. Provide a critical evaluation of how management accounting systems and

management accounting reporting are integrated within organisational processes

The management accounting report and systems are integrated with each other in a

way that they both compliment in facilitating the decision making process. The

management accounting systems are used to determine properly record the data and

transactions that are being carried out during the particular period. The reporting of the

same is very much necessary so that there can be a critical analysis of the transactions

that are being recorded by the presentation of the same in a format which is

understandable and easy to analyse. Management accounting reporting present the

data recorded in an effective way so that the effective decisions can be taken by the

management.

11

management accounting reporting are integrated within organisational processes

The management accounting report and systems are integrated with each other in a

way that they both compliment in facilitating the decision making process. The

management accounting systems are used to determine properly record the data and

transactions that are being carried out during the particular period. The reporting of the

same is very much necessary so that there can be a critical analysis of the transactions

that are being recorded by the presentation of the same in a format which is

understandable and easy to analyse. Management accounting reporting present the

data recorded in an effective way so that the effective decisions can be taken by the

management.

11

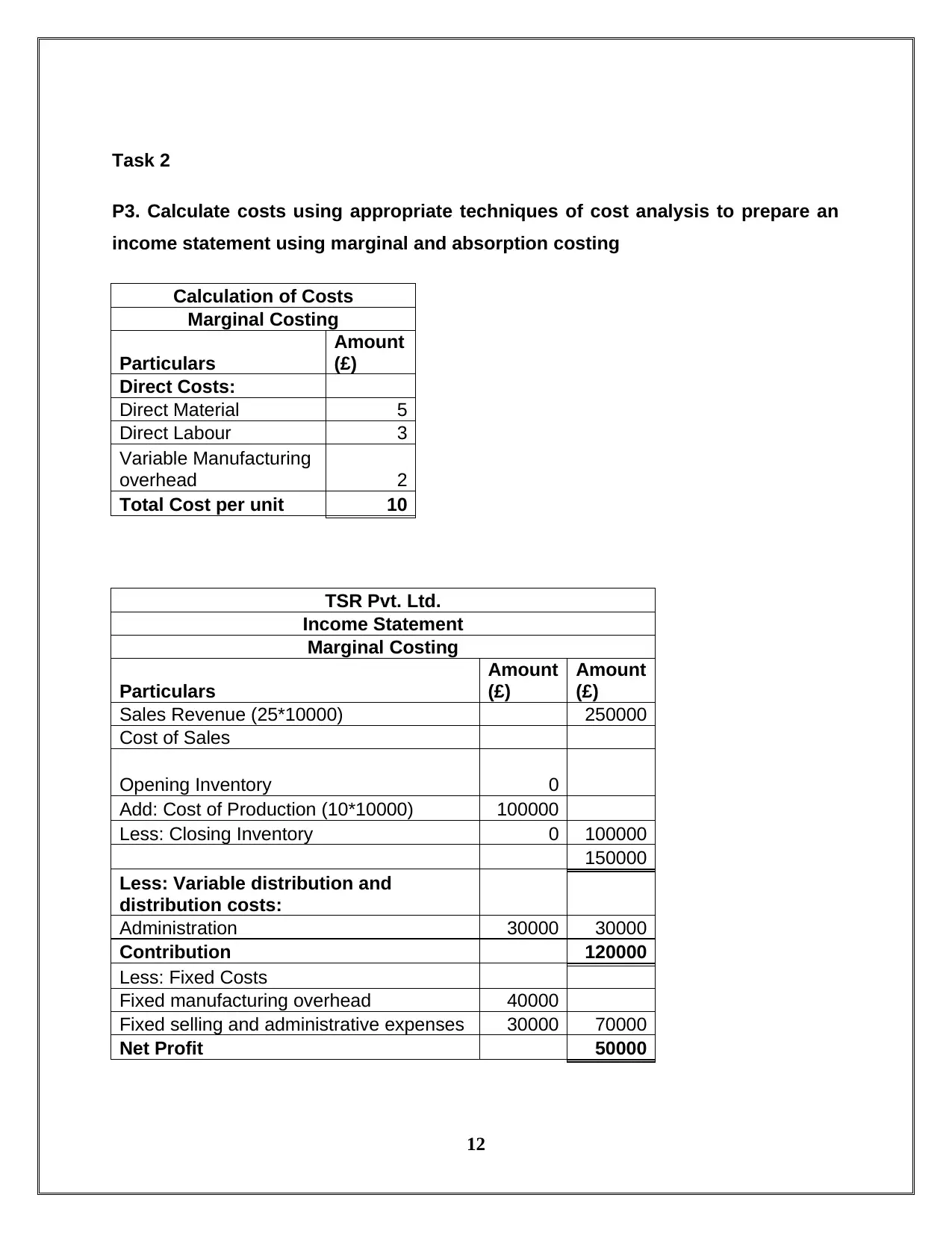

Task 2

P3. Calculate costs using appropriate techniques of cost analysis to prepare an

income statement using marginal and absorption costing

Calculation of Costs

Marginal Costing

Particulars

Amount

(£)

Direct Costs:

Direct Material 5

Direct Labour 3

Variable Manufacturing

overhead 2

Total Cost per unit 10

TSR Pvt. Ltd.

Income Statement

Marginal Costing

Particulars

Amount

(£)

Amount

(£)

Sales Revenue (25*10000) 250000

Cost of Sales

Opening Inventory 0

Add: Cost of Production (10*10000) 100000

Less: Closing Inventory 0 100000

150000

Less: Variable distribution and

distribution costs:

Administration 30000 30000

Contribution 120000

Less: Fixed Costs

Fixed manufacturing overhead 40000

Fixed selling and administrative expenses 30000 70000

Net Profit 50000

12

P3. Calculate costs using appropriate techniques of cost analysis to prepare an

income statement using marginal and absorption costing

Calculation of Costs

Marginal Costing

Particulars

Amount

(£)

Direct Costs:

Direct Material 5

Direct Labour 3

Variable Manufacturing

overhead 2

Total Cost per unit 10

TSR Pvt. Ltd.

Income Statement

Marginal Costing

Particulars

Amount

(£)

Amount

(£)

Sales Revenue (25*10000) 250000

Cost of Sales

Opening Inventory 0

Add: Cost of Production (10*10000) 100000

Less: Closing Inventory 0 100000

150000

Less: Variable distribution and

distribution costs:

Administration 30000 30000

Contribution 120000

Less: Fixed Costs

Fixed manufacturing overhead 40000

Fixed selling and administrative expenses 30000 70000

Net Profit 50000

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 26

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.