Report on Management Accounting Systems, Techniques, and Application

VerifiedAdded on 2023/01/11

|20

|5714

|22

Report

AI Summary

This report provides a comprehensive overview of management accounting systems and techniques. It begins by defining management accounting and its principles, highlighting its roles in planning, costing, budgeting, decision-making, and performance measurement. The report distinguishes between management accounting and financial accounting, detailing various management accounting systems such as cost accounting, job costing, inventory management, and price optimization. It also explores different methods in management accounting reports, including ABC costing, batch costing, budget reports, and income reports. Furthermore, the report discusses the application of management accounting techniques to prepare income statements and analyzes the advantages and disadvantages of planning tools used in budgetary control. Finally, it compares two companies based on their use of management accounting systems, providing a thorough understanding of the subject matter.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1. Management accounting systems..........................................................................................1

P2. Different methods in Management accounting reports.........................................................5

TASK 2............................................................................................................................................7

P3. Application of management accounting techniques to calculate or prepare income

statement......................................................................................................................................7

TASK 3..........................................................................................................................................10

P4. Advantages and disadvantages of distinct planning tools used in budgetary control.........10

TASK 4..........................................................................................................................................13

P5. Comparison among two companies in the way they uses management accounting system

...................................................................................................................................................13

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1. Management accounting systems..........................................................................................1

P2. Different methods in Management accounting reports.........................................................5

TASK 2............................................................................................................................................7

P3. Application of management accounting techniques to calculate or prepare income

statement......................................................................................................................................7

TASK 3..........................................................................................................................................10

P4. Advantages and disadvantages of distinct planning tools used in budgetary control.........10

TASK 4..........................................................................................................................................13

P5. Comparison among two companies in the way they uses management accounting system

...................................................................................................................................................13

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION

This assignment has been completed by three distinctive Parts where Part-1 consists of LO1

that has described importance of management accounting, roles of MA, principles of MA, FA

VS MA, different management accounting systems and different methods of management

accounting reporting systems. The Part-2 has described the process of calculating unit costs and

profits of Creams Ltd by the application of both absorption costing and marginal costing

methods. Part-3 has described different planning tools and their merits and demerits for the

company’s accounting functions. However, this part has also compared the financial and non-

financial performance between Creams and Crown Company to understand the financial

problems and solutions appropriately.

TASK 1

P1. Management accounting systems

Defining the Management Accounting:

The term management is defined as the methods of essential accounting process for

collecting, recording, interpreting and storing of financial and non-monetary accounting data to

facilitate different managerial decisions regarding costing, pricing and profitability of company

(Bedford and Speklé, 2018). It is used at Creams Ltd for the facilitating of appropriate costs

calculation that is prerequisite to determine accurate price level.

Defining the Management Accounting System:

The term management accounting system is defined as the process of preparing different

management systems through the collecting of budgeting and costing data. The accounting

system is integrated by costing systems, pricing system, job costing system and inventory system

for the appropriate management of all managerial decisions.

Principles of Management Accounting:

For ensuring effective utilization of all management accounting systems, there are

required to be guided by some accounting principles like the followings:

Influence Principle: The principle asserts the attributes of having materiality and influential

capacity to make alternative decisions regarding costing, pricing and budgeting for the taking of

best managerial decisions to facilitate the company goals largely (Berry, Broadbent and Otley,

2016).

1

This assignment has been completed by three distinctive Parts where Part-1 consists of LO1

that has described importance of management accounting, roles of MA, principles of MA, FA

VS MA, different management accounting systems and different methods of management

accounting reporting systems. The Part-2 has described the process of calculating unit costs and

profits of Creams Ltd by the application of both absorption costing and marginal costing

methods. Part-3 has described different planning tools and their merits and demerits for the

company’s accounting functions. However, this part has also compared the financial and non-

financial performance between Creams and Crown Company to understand the financial

problems and solutions appropriately.

TASK 1

P1. Management accounting systems

Defining the Management Accounting:

The term management is defined as the methods of essential accounting process for

collecting, recording, interpreting and storing of financial and non-monetary accounting data to

facilitate different managerial decisions regarding costing, pricing and profitability of company

(Bedford and Speklé, 2018). It is used at Creams Ltd for the facilitating of appropriate costs

calculation that is prerequisite to determine accurate price level.

Defining the Management Accounting System:

The term management accounting system is defined as the process of preparing different

management systems through the collecting of budgeting and costing data. The accounting

system is integrated by costing systems, pricing system, job costing system and inventory system

for the appropriate management of all managerial decisions.

Principles of Management Accounting:

For ensuring effective utilization of all management accounting systems, there are

required to be guided by some accounting principles like the followings:

Influence Principle: The principle asserts the attributes of having materiality and influential

capacity to make alternative decisions regarding costing, pricing and budgeting for the taking of

best managerial decisions to facilitate the company goals largely (Berry, Broadbent and Otley,

2016).

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Relevance principle: The principle asserts the attributes of having appropriateness and

accuracy to the managerial decisions by providing needed costing data for costing decision,

needed profitability data for profit decision making effectively.

Analyze Principle: The principle asserts the attributes of having interpreting capacity of all

methods of accounting and data to critically analyse the cause and effects of each type of

accounting information to ensure best managerial data.

Trust Principle: The principle asserts the attributes of having trusted sources of data to

ensure high accountability and acceptability of data by decision makers of the company as the

decisions will be provided to be implemented by internal and external stakeholders.

Roles of Management Accounting:

In addition, according to above principles of this accounting, management of the

organizations can enjoy the benefits of this accounting system like the followings:

Planning: Planning means the attributes of explaining the future endeavours of pricing,

costing and financial performance of the company (Booth, 2018). Management accounting

creates plans of costs, price and other essential attributes through the application of different

planning tools like budgeting and pricing tools.

Costing: Costing means the attributes of expenditures those are incurred to meet certain

elements of the company daily and annually for the creation of resources. Management

accounting records appropriately those daily and annual expenditures of manufacturing,

marketing and supplying of goods and services by the application of marginal, ABC costing, Job

costing and absorption costing methods.

Budgeting: Budgeting is defined as the attribute to create the future assumption of

production needs, marketing needs, cash needs and other essential elements for the company.

Management accounting creates different budgeting like flexible and zero based for the

controlling of future uncertainties through the appropriate analysis of cause and effects.

Decision Making: Decision making is the attributes of taking pricing decision, costing

decision, production needs decisions and inventory decision. In this case, management

accounting creates different accounting systems such as job costing systems for costing decision

and price optimizing system for pricing decisions effectively for the company goals

achievement.

2

accuracy to the managerial decisions by providing needed costing data for costing decision,

needed profitability data for profit decision making effectively.

Analyze Principle: The principle asserts the attributes of having interpreting capacity of all

methods of accounting and data to critically analyse the cause and effects of each type of

accounting information to ensure best managerial data.

Trust Principle: The principle asserts the attributes of having trusted sources of data to

ensure high accountability and acceptability of data by decision makers of the company as the

decisions will be provided to be implemented by internal and external stakeholders.

Roles of Management Accounting:

In addition, according to above principles of this accounting, management of the

organizations can enjoy the benefits of this accounting system like the followings:

Planning: Planning means the attributes of explaining the future endeavours of pricing,

costing and financial performance of the company (Booth, 2018). Management accounting

creates plans of costs, price and other essential attributes through the application of different

planning tools like budgeting and pricing tools.

Costing: Costing means the attributes of expenditures those are incurred to meet certain

elements of the company daily and annually for the creation of resources. Management

accounting records appropriately those daily and annual expenditures of manufacturing,

marketing and supplying of goods and services by the application of marginal, ABC costing, Job

costing and absorption costing methods.

Budgeting: Budgeting is defined as the attribute to create the future assumption of

production needs, marketing needs, cash needs and other essential elements for the company.

Management accounting creates different budgeting like flexible and zero based for the

controlling of future uncertainties through the appropriate analysis of cause and effects.

Decision Making: Decision making is the attributes of taking pricing decision, costing

decision, production needs decisions and inventory decision. In this case, management

accounting creates different accounting systems such as job costing systems for costing decision

and price optimizing system for pricing decisions effectively for the company goals

achievement.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Performance Measurement: Performance management is the attributes of measuring

company’s financial and non-monetary performance regarding profitability, cost control,

resource utilization and acquisition (Dekker, 2016). Management accounting applies different

standards and comparisons of measuring such performance for controlling the future

uncertainties and ensures high productivity effectively.

Distinctions between Management Accounting and Financial Accounting:

Financial accounting: FA means the financial accounting that is somewhat difference

from management accounting where two branches are practiced in same organization. In Creams

Ltd, Financial accounting is used to deal with standard data to calculate company’s performance

for providing to external parties. Financial accounting’s goal is to convince the investors to

execute investment in the organizations. The reports of financial accounting are needed to be

audited by registered auditors for the purpose of government acceptance. Only financial

information of the company functions are treated by financial accounting (Dewi and et. al.,

2018).

Management accounting: Management accounting deals with actual data to calculate

company’s performance for providing to internal parties. Management accounting’s goal is to

convince higher management by the measurement of internal functions’ performance. The

reports of management accounting are not required to be audited by such auditors by verified by

intern CEO of the company. Both financial and non-financial information are treated by

management accounting effectively.

Different types of management accounting systems and their essential requirements:

Management accounting also deals with application of many types of accounting systems

those are needed to determine least price, cost control and inventory management accurately.

The management accounting systems are discussed below with their essential requirements:

a) Cost Accounting System: There are many types of functional costs and expenditures such

as production, marketing and distribution where there are variable costs and fixed costs of

in those functional areas of the company (Eckardt, Selen and Wynder, 2015).

Management accounting suggests applying this accounting system to calculate and

3

company’s financial and non-monetary performance regarding profitability, cost control,

resource utilization and acquisition (Dekker, 2016). Management accounting applies different

standards and comparisons of measuring such performance for controlling the future

uncertainties and ensures high productivity effectively.

Distinctions between Management Accounting and Financial Accounting:

Financial accounting: FA means the financial accounting that is somewhat difference

from management accounting where two branches are practiced in same organization. In Creams

Ltd, Financial accounting is used to deal with standard data to calculate company’s performance

for providing to external parties. Financial accounting’s goal is to convince the investors to

execute investment in the organizations. The reports of financial accounting are needed to be

audited by registered auditors for the purpose of government acceptance. Only financial

information of the company functions are treated by financial accounting (Dewi and et. al.,

2018).

Management accounting: Management accounting deals with actual data to calculate

company’s performance for providing to internal parties. Management accounting’s goal is to

convince higher management by the measurement of internal functions’ performance. The

reports of management accounting are not required to be audited by such auditors by verified by

intern CEO of the company. Both financial and non-financial information are treated by

management accounting effectively.

Different types of management accounting systems and their essential requirements:

Management accounting also deals with application of many types of accounting systems

those are needed to determine least price, cost control and inventory management accurately.

The management accounting systems are discussed below with their essential requirements:

a) Cost Accounting System: There are many types of functional costs and expenditures such

as production, marketing and distribution where there are variable costs and fixed costs of

in those functional areas of the company (Eckardt, Selen and Wynder, 2015).

Management accounting suggests applying this accounting system to calculate and

3

measure such expenses effectively by arranging the following requirements

appropriately:

Variable expenditures.

Fixed expenditures.

Semi variable expenditures.

Standard costing.

Appropriate software to store data.

The essential requirement of cost accounting system at Creams Ltd is to establish accurate

cost for its all units that are manufactured by the company. Along with this, the system is also

used for estimating cost all the commodities for the purpose of profitability analysis, controlling

of cost as well as valuation of its inventory.

b) Job Costing System: There are many jobs in the production like raw materials collection,

direct labour, indirect labours, factory overheads and administrative costs those are

needed to be calculated effectively. In that case, Management accounting suggests

applying this accounting system to calculate and measure such job costs effectively to

assign appropriately to each job by arranging the following requirements appropriately:

Direct labour cost.

Direct factory costs.

Indirect costs.

Overhead costs.

Appropriate software to store data.

In context to job costing system, its essential requirement in Creams Ltd is to keep record of

all the expenses that are related to a specific commodity by arrange and preparing separate

record of job associated with all the product line. Addition to it, another essential requirement of

this system in the company is to accumulate information about direct labor, direct material and

overhead related with the job (Hiebl, 2014).

c) Inventory Management System: There are some types of inventories such as work in

process inventory, finished goods inventory and raw materials inventory those are needed

to be arranged and maintained all costs regarding those stock levels. Management

accounting suggests applying this accounting system to calculate and measure such

4

appropriately:

Variable expenditures.

Fixed expenditures.

Semi variable expenditures.

Standard costing.

Appropriate software to store data.

The essential requirement of cost accounting system at Creams Ltd is to establish accurate

cost for its all units that are manufactured by the company. Along with this, the system is also

used for estimating cost all the commodities for the purpose of profitability analysis, controlling

of cost as well as valuation of its inventory.

b) Job Costing System: There are many jobs in the production like raw materials collection,

direct labour, indirect labours, factory overheads and administrative costs those are

needed to be calculated effectively. In that case, Management accounting suggests

applying this accounting system to calculate and measure such job costs effectively to

assign appropriately to each job by arranging the following requirements appropriately:

Direct labour cost.

Direct factory costs.

Indirect costs.

Overhead costs.

Appropriate software to store data.

In context to job costing system, its essential requirement in Creams Ltd is to keep record of

all the expenses that are related to a specific commodity by arrange and preparing separate

record of job associated with all the product line. Addition to it, another essential requirement of

this system in the company is to accumulate information about direct labor, direct material and

overhead related with the job (Hiebl, 2014).

c) Inventory Management System: There are some types of inventories such as work in

process inventory, finished goods inventory and raw materials inventory those are needed

to be arranged and maintained all costs regarding those stock levels. Management

accounting suggests applying this accounting system to calculate and measure such

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

expenses effectively to manage good stock levels by arranging the following

requirements appropriately:

Production data.

Stock data.

Application of inventory tools such LIFO, FIFO, Average and JIT system.

Appropriate software to calculate stock levels.

Essential requirement of inventory management system at Creams Ltd is to track goods and

materials across the supply chain and warehouse of the entity. It also helps in checking flow of

stock as well as ensuring that materials are supplied to the demanded place of the company in

accurate time and at minimum possible rates (Hoque, 2018). The firm also requires the system

for keeping accurate record of the entire inventory which enters or leaves the premise or its

warehouse.

d) Price Optimization System: There is needed to determine appropriate and least price tags

for the produced goods of the company by the calculation of all relevant costs and apply

the profit margin. Management accounting suggests applying this accounting system to

calculate and measure best prices effectively by arranging the following requirements

appropriately:

Accurate costing information.

Accurate pricing strategies.

Accurate profit margin.

Appropriate software to store data.

In Creams Ltd, essential requirement of price optimisation system is to calculate the ways

in which demand of the offerings varies at distinct level of prices. The system is also required at

the company for setting suitable prices of the commodities that it is planning or is offering in the

market. Furthermore, the system also assists in knowing exact price of commodities and services

after researching about rival products or market needs (Kaplan and Atkinson, 2015).

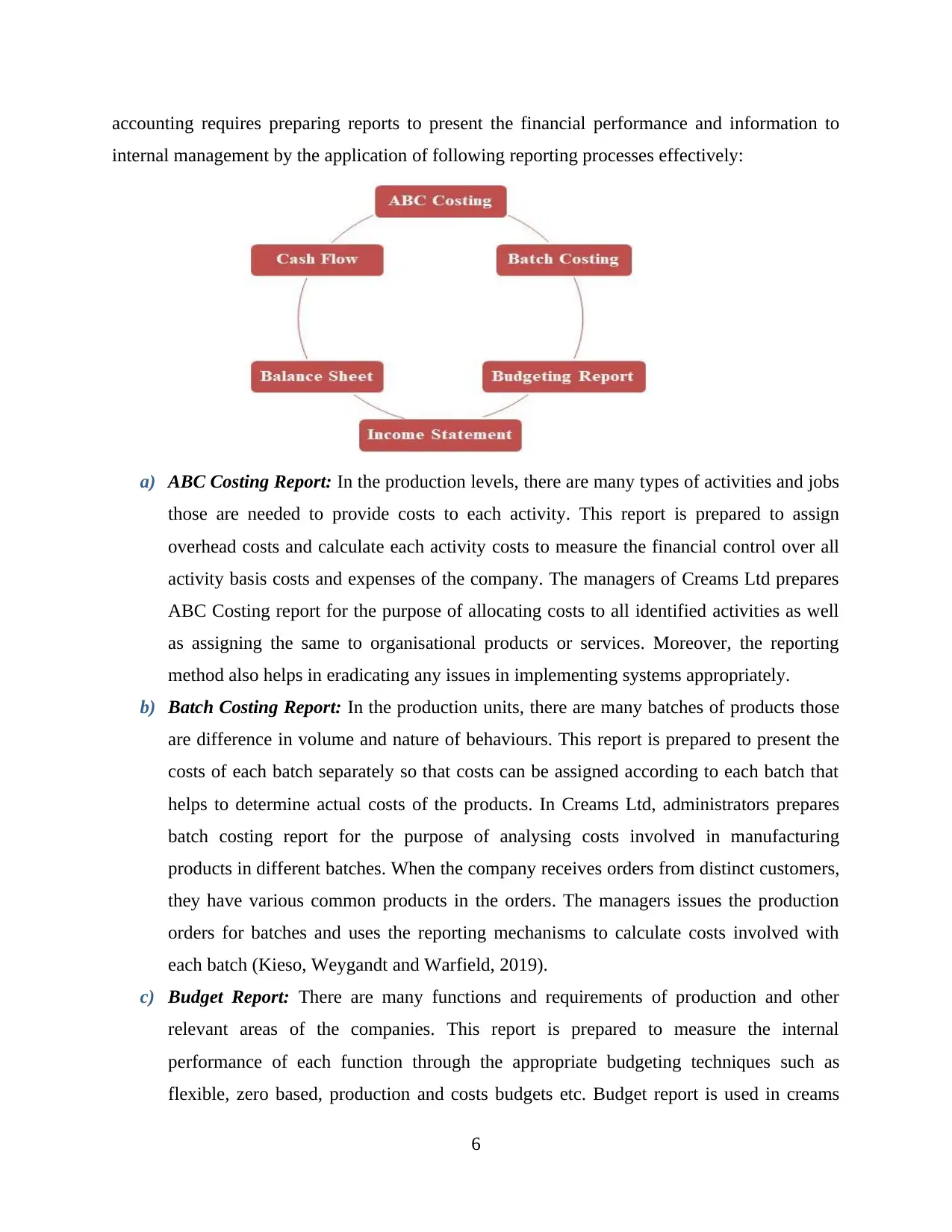

P2. Different methods in Management accounting reports

Methods of Management Accounting Reports:

The tools that are used to understand numbers behind the things or workings going in the

organisation are termed as management accounting reports. In Creams Ltd, Management

5

requirements appropriately:

Production data.

Stock data.

Application of inventory tools such LIFO, FIFO, Average and JIT system.

Appropriate software to calculate stock levels.

Essential requirement of inventory management system at Creams Ltd is to track goods and

materials across the supply chain and warehouse of the entity. It also helps in checking flow of

stock as well as ensuring that materials are supplied to the demanded place of the company in

accurate time and at minimum possible rates (Hoque, 2018). The firm also requires the system

for keeping accurate record of the entire inventory which enters or leaves the premise or its

warehouse.

d) Price Optimization System: There is needed to determine appropriate and least price tags

for the produced goods of the company by the calculation of all relevant costs and apply

the profit margin. Management accounting suggests applying this accounting system to

calculate and measure best prices effectively by arranging the following requirements

appropriately:

Accurate costing information.

Accurate pricing strategies.

Accurate profit margin.

Appropriate software to store data.

In Creams Ltd, essential requirement of price optimisation system is to calculate the ways

in which demand of the offerings varies at distinct level of prices. The system is also required at

the company for setting suitable prices of the commodities that it is planning or is offering in the

market. Furthermore, the system also assists in knowing exact price of commodities and services

after researching about rival products or market needs (Kaplan and Atkinson, 2015).

P2. Different methods in Management accounting reports

Methods of Management Accounting Reports:

The tools that are used to understand numbers behind the things or workings going in the

organisation are termed as management accounting reports. In Creams Ltd, Management

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

accounting requires preparing reports to present the financial performance and information to

internal management by the application of following reporting processes effectively:

a) ABC Costing Report: In the production levels, there are many types of activities and jobs

those are needed to provide costs to each activity. This report is prepared to assign

overhead costs and calculate each activity costs to measure the financial control over all

activity basis costs and expenses of the company. The managers of Creams Ltd prepares

ABC Costing report for the purpose of allocating costs to all identified activities as well

as assigning the same to organisational products or services. Moreover, the reporting

method also helps in eradicating any issues in implementing systems appropriately.

b) Batch Costing Report: In the production units, there are many batches of products those

are difference in volume and nature of behaviours. This report is prepared to present the

costs of each batch separately so that costs can be assigned according to each batch that

helps to determine actual costs of the products. In Creams Ltd, administrators prepares

batch costing report for the purpose of analysing costs involved in manufacturing

products in different batches. When the company receives orders from distinct customers,

they have various common products in the orders. The managers issues the production

orders for batches and uses the reporting mechanisms to calculate costs involved with

each batch (Kieso, Weygandt and Warfield, 2019).

c) Budget Report: There are many functions and requirements of production and other

relevant areas of the companies. This report is prepared to measure the internal

performance of each function through the appropriate budgeting techniques such as

flexible, zero based, production and costs budgets etc. Budget report is used in creams

6

internal management by the application of following reporting processes effectively:

a) ABC Costing Report: In the production levels, there are many types of activities and jobs

those are needed to provide costs to each activity. This report is prepared to assign

overhead costs and calculate each activity costs to measure the financial control over all

activity basis costs and expenses of the company. The managers of Creams Ltd prepares

ABC Costing report for the purpose of allocating costs to all identified activities as well

as assigning the same to organisational products or services. Moreover, the reporting

method also helps in eradicating any issues in implementing systems appropriately.

b) Batch Costing Report: In the production units, there are many batches of products those

are difference in volume and nature of behaviours. This report is prepared to present the

costs of each batch separately so that costs can be assigned according to each batch that

helps to determine actual costs of the products. In Creams Ltd, administrators prepares

batch costing report for the purpose of analysing costs involved in manufacturing

products in different batches. When the company receives orders from distinct customers,

they have various common products in the orders. The managers issues the production

orders for batches and uses the reporting mechanisms to calculate costs involved with

each batch (Kieso, Weygandt and Warfield, 2019).

c) Budget Report: There are many functions and requirements of production and other

relevant areas of the companies. This report is prepared to measure the internal

performance of each function through the appropriate budgeting techniques such as

flexible, zero based, production and costs budgets etc. Budget report is used in creams

6

Ltd for recording different types of budgets that are depended on organisation financial

needs along with available data. Moreover, it is prepared as per the requirement of

business and recording expenses or income that are forecasted for upcoming period.

d) Income Report: In the functions of the companies, there are both types of sources of

generating revenues and incurring costs by the effective completion of the works. This

report is prepared to present the net income or net loss by differentiating between total

revenues and total expenses of a definite time. In Creams Ltd, managers prepare income

report for the objective of recording the incomes received from different sources and with

different products. It is prepared in different forms that are operating income report, net

income report and many more. It helps in differentiating among total revenues earned and

capital invested in manufacturing different products.

e) Balance Sheet Report: There are some resources and assets against retained earnings and

liabilities of the companies (Maskell, Baggaley and Grasso, 2017). This report is

prepared to present a good balance between such assets and liabilities of day of

accounting year to measure accurate financial performance of the companies effectively.

Balance sheet report is prepared by finance department of Creams Ltd for the purpose of

analysing where the company stand in the market. The report gives snapshot of the

financial position of the company on given day and it prepared at the end of each quarter

or annual year.

f) Cash Flow Report: There are needs of sourcing cash to meet the obligation of cash

expenses of the companies. This report is prepared to present the cash balance of a

definite time through the assumption of cash sources and cash needs appropriately for the

company cash obligations. In Creams Ltd, cash flow report is prepared for making up

financial statements as well as annual reports. The main concern to prepare cash flow

report is to present overview of financial transactions occurred in business over

designated duration.

TASK 2

P3. Application of management accounting techniques to calculate or prepare income statement

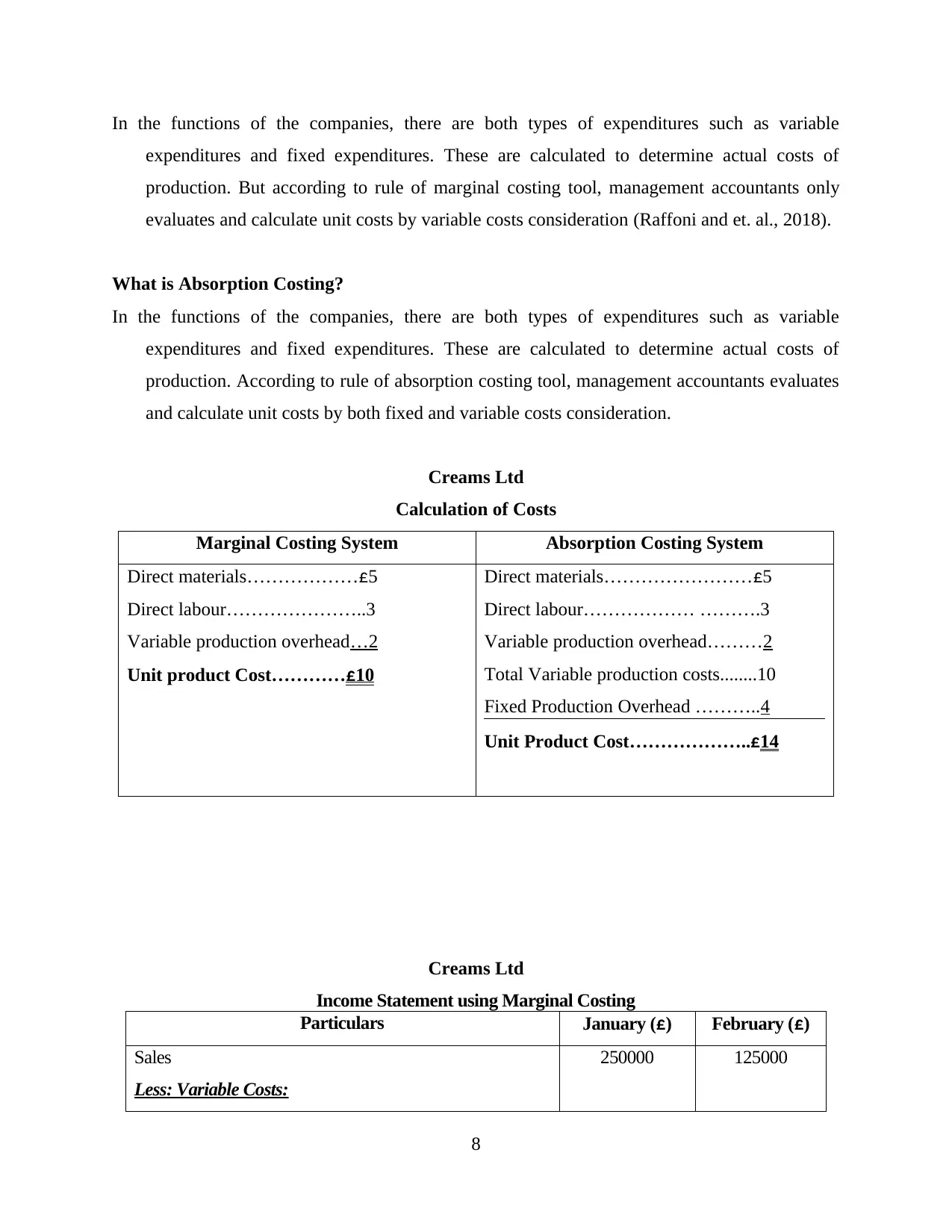

What is Marginal Costing?

7

needs along with available data. Moreover, it is prepared as per the requirement of

business and recording expenses or income that are forecasted for upcoming period.

d) Income Report: In the functions of the companies, there are both types of sources of

generating revenues and incurring costs by the effective completion of the works. This

report is prepared to present the net income or net loss by differentiating between total

revenues and total expenses of a definite time. In Creams Ltd, managers prepare income

report for the objective of recording the incomes received from different sources and with

different products. It is prepared in different forms that are operating income report, net

income report and many more. It helps in differentiating among total revenues earned and

capital invested in manufacturing different products.

e) Balance Sheet Report: There are some resources and assets against retained earnings and

liabilities of the companies (Maskell, Baggaley and Grasso, 2017). This report is

prepared to present a good balance between such assets and liabilities of day of

accounting year to measure accurate financial performance of the companies effectively.

Balance sheet report is prepared by finance department of Creams Ltd for the purpose of

analysing where the company stand in the market. The report gives snapshot of the

financial position of the company on given day and it prepared at the end of each quarter

or annual year.

f) Cash Flow Report: There are needs of sourcing cash to meet the obligation of cash

expenses of the companies. This report is prepared to present the cash balance of a

definite time through the assumption of cash sources and cash needs appropriately for the

company cash obligations. In Creams Ltd, cash flow report is prepared for making up

financial statements as well as annual reports. The main concern to prepare cash flow

report is to present overview of financial transactions occurred in business over

designated duration.

TASK 2

P3. Application of management accounting techniques to calculate or prepare income statement

What is Marginal Costing?

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

In the functions of the companies, there are both types of expenditures such as variable

expenditures and fixed expenditures. These are calculated to determine actual costs of

production. But according to rule of marginal costing tool, management accountants only

evaluates and calculate unit costs by variable costs consideration (Raffoni and et. al., 2018).

What is Absorption Costing?

In the functions of the companies, there are both types of expenditures such as variable

expenditures and fixed expenditures. These are calculated to determine actual costs of

production. According to rule of absorption costing tool, management accountants evaluates

and calculate unit costs by both fixed and variable costs consideration.

Creams Ltd

Calculation of Costs

Marginal Costing System Absorption Costing System

Direct materials………………£5

Direct labour…………………..3

Variable production overhead…2

Unit product Cost…………£10

Direct materials……………………£5

Direct labour……………… ……….3

Variable production overhead………2

Total Variable production costs........10

Fixed Production Overhead ………..4

Unit Product Cost………………..£14

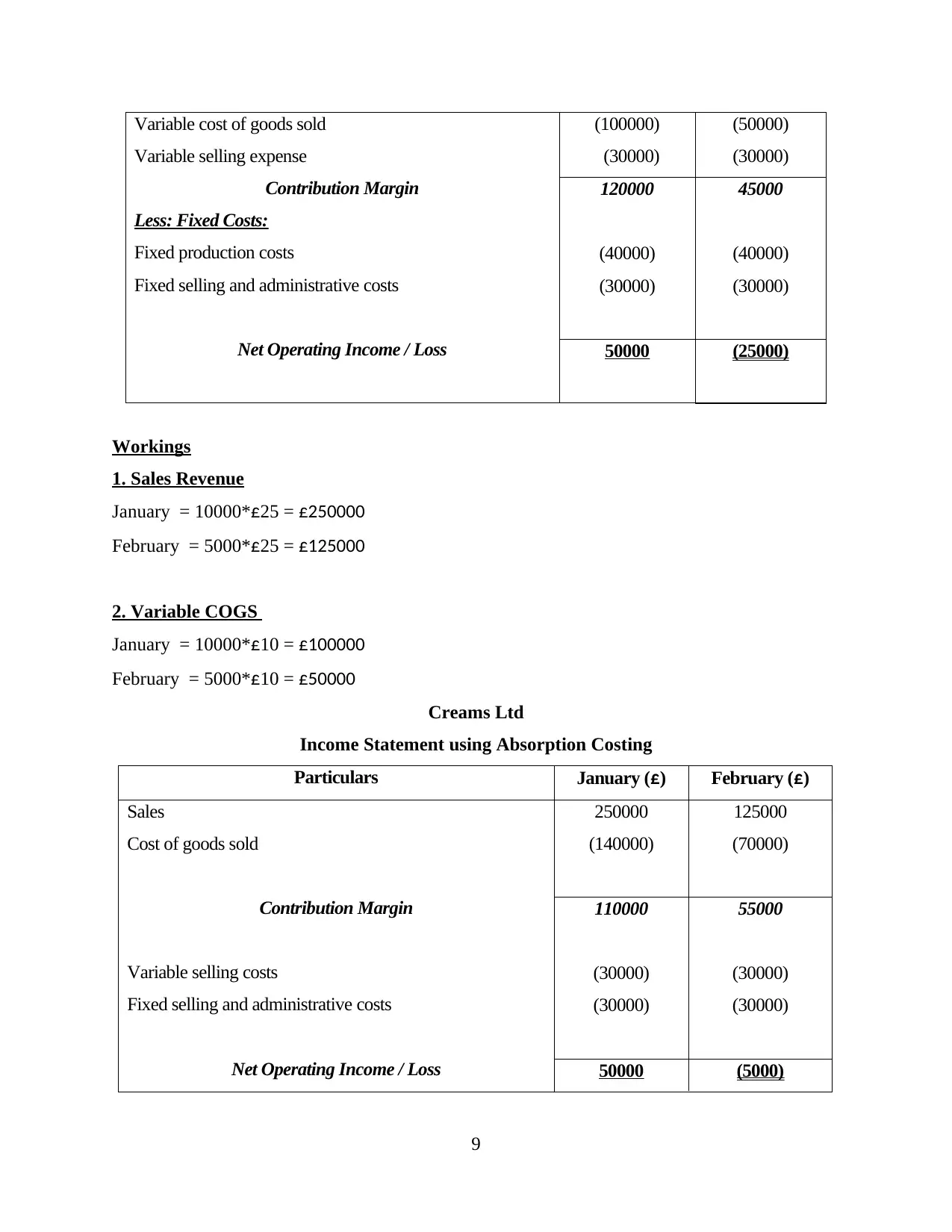

Creams Ltd

Income Statement using Marginal Costing

Particulars January (£) February (£)

Sales

Less: Variable Costs:

250000 125000

8

expenditures and fixed expenditures. These are calculated to determine actual costs of

production. But according to rule of marginal costing tool, management accountants only

evaluates and calculate unit costs by variable costs consideration (Raffoni and et. al., 2018).

What is Absorption Costing?

In the functions of the companies, there are both types of expenditures such as variable

expenditures and fixed expenditures. These are calculated to determine actual costs of

production. According to rule of absorption costing tool, management accountants evaluates

and calculate unit costs by both fixed and variable costs consideration.

Creams Ltd

Calculation of Costs

Marginal Costing System Absorption Costing System

Direct materials………………£5

Direct labour…………………..3

Variable production overhead…2

Unit product Cost…………£10

Direct materials……………………£5

Direct labour……………… ……….3

Variable production overhead………2

Total Variable production costs........10

Fixed Production Overhead ………..4

Unit Product Cost………………..£14

Creams Ltd

Income Statement using Marginal Costing

Particulars January (£) February (£)

Sales

Less: Variable Costs:

250000 125000

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Variable cost of goods sold

Variable selling expense

Contribution Margin

Less: Fixed Costs:

Fixed production costs

Fixed selling and administrative costs

Net Operating Income / Loss

(100000)

(30000)

(50000)

(30000)

120000

(40000)

(30000)

45000

(40000)

(30000)

50000 (25000)

Workings

1. Sales Revenue

January = 10000*£25 = £250000

February = 5000*£25 = £125000

2. Variable COGS

January = 10000*£10 = £100000

February = 5000*£10 = £50000

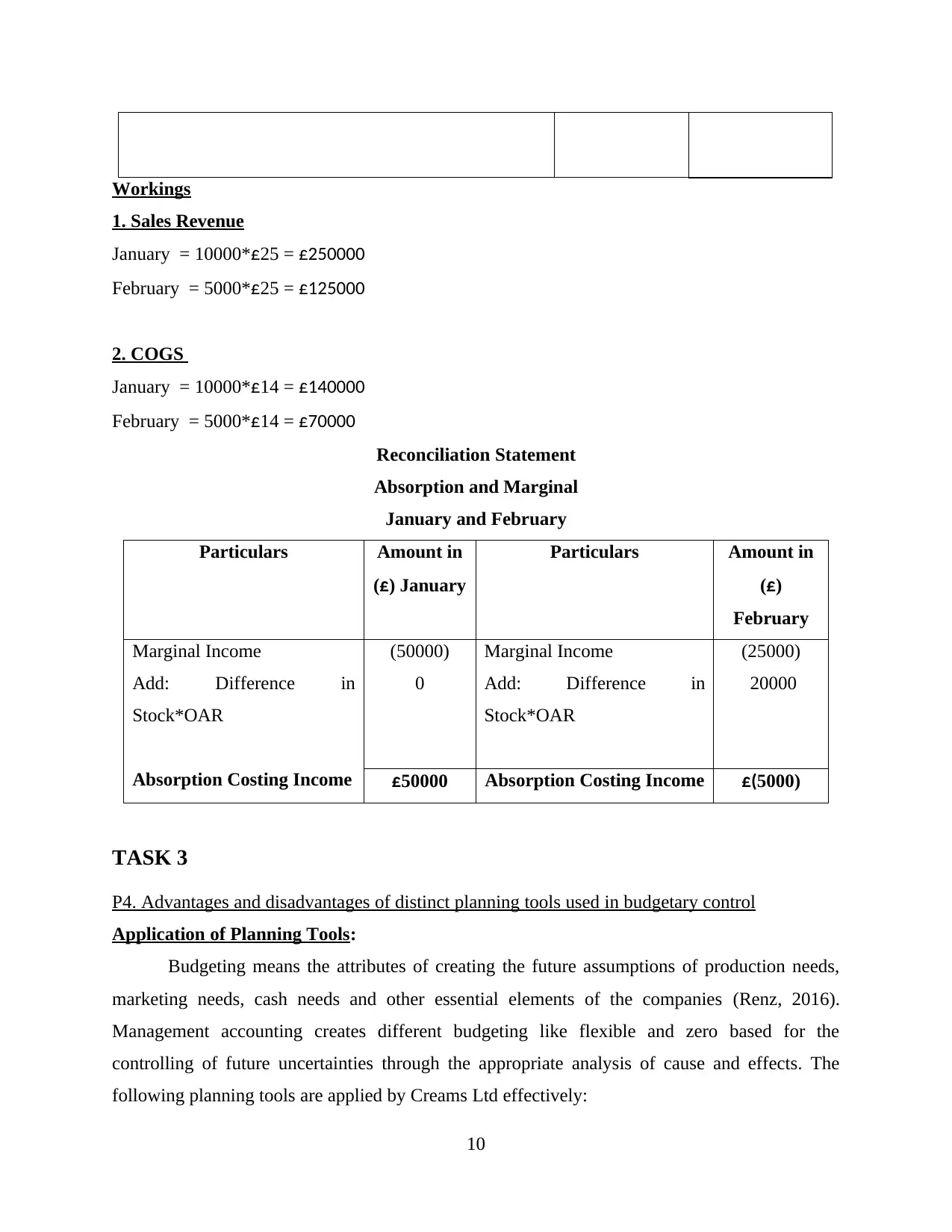

Creams Ltd

Income Statement using Absorption Costing

Particulars January (£) February (£)

Sales

Cost of goods sold

Contribution Margin

Variable selling costs

Fixed selling and administrative costs

Net Operating Income / Loss

250000

(140000)

125000

(70000)

110000

(30000)

(30000)

55000

(30000)

(30000)

50000 (5000)

9

Variable selling expense

Contribution Margin

Less: Fixed Costs:

Fixed production costs

Fixed selling and administrative costs

Net Operating Income / Loss

(100000)

(30000)

(50000)

(30000)

120000

(40000)

(30000)

45000

(40000)

(30000)

50000 (25000)

Workings

1. Sales Revenue

January = 10000*£25 = £250000

February = 5000*£25 = £125000

2. Variable COGS

January = 10000*£10 = £100000

February = 5000*£10 = £50000

Creams Ltd

Income Statement using Absorption Costing

Particulars January (£) February (£)

Sales

Cost of goods sold

Contribution Margin

Variable selling costs

Fixed selling and administrative costs

Net Operating Income / Loss

250000

(140000)

125000

(70000)

110000

(30000)

(30000)

55000

(30000)

(30000)

50000 (5000)

9

Workings

1. Sales Revenue

January = 10000*£25 = £250000

February = 5000*£25 = £125000

2. COGS

January = 10000*£14 = £140000

February = 5000*£14 = £70000

Reconciliation Statement

Absorption and Marginal

January and February

Particulars Amount in

(£) January

Particulars Amount in

(£)

February

Marginal Income

Add: Difference in

Stock*OAR

Absorption Costing Income

(50000)

0

Marginal Income

Add: Difference in

Stock*OAR

(25000)

20000

£50000 Absorption Costing Income £(5000)

TASK 3

P4. Advantages and disadvantages of distinct planning tools used in budgetary control

Application of Planning Tools:

Budgeting means the attributes of creating the future assumptions of production needs,

marketing needs, cash needs and other essential elements of the companies (Renz, 2016).

Management accounting creates different budgeting like flexible and zero based for the

controlling of future uncertainties through the appropriate analysis of cause and effects. The

following planning tools are applied by Creams Ltd effectively:

10

1. Sales Revenue

January = 10000*£25 = £250000

February = 5000*£25 = £125000

2. COGS

January = 10000*£14 = £140000

February = 5000*£14 = £70000

Reconciliation Statement

Absorption and Marginal

January and February

Particulars Amount in

(£) January

Particulars Amount in

(£)

February

Marginal Income

Add: Difference in

Stock*OAR

Absorption Costing Income

(50000)

0

Marginal Income

Add: Difference in

Stock*OAR

(25000)

20000

£50000 Absorption Costing Income £(5000)

TASK 3

P4. Advantages and disadvantages of distinct planning tools used in budgetary control

Application of Planning Tools:

Budgeting means the attributes of creating the future assumptions of production needs,

marketing needs, cash needs and other essential elements of the companies (Renz, 2016).

Management accounting creates different budgeting like flexible and zero based for the

controlling of future uncertainties through the appropriate analysis of cause and effects. The

following planning tools are applied by Creams Ltd effectively:

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.