Management Accounting Report: Cost Analysis and Budgetary Control

VerifiedAdded on 2020/06/04

|17

|3987

|29

Report

AI Summary

This comprehensive report delves into the core principles of management accounting, emphasizing its crucial role in organizational decision-making. It explores various types of management accounting, including cost accounting, price optimization, job costing, and inventory management, highlighting their significance in controlling costs and optimizing resources. The report discusses different methods of management accounting reporting, such as segmental reports, performance reports, and inventory management reports, and explains how these tools aid in financial analysis and decision-making. Furthermore, it provides detailed computations using marginal and absorption costing techniques to prepare income statements, along with an appendix containing working notes. The report also outlines the merits and demerits of different planning tools used in budgetary control, such as zero-based budgeting, and examines how companies adapt management accounting systems to address financial challenges. The report concludes by summarizing the key benefits of management accounting systems, including reduced expenses and improved decision-making capabilities.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

(P1) Management accounting and essential requirements of its various types......................1

(P2) Discuss the methods used for management accounting reporting..................................3

(P3) Compute costs using techniques of cost analysis to prepare income statement using

absorption and marginal costing.............................................................................................5

APPENDIX......................................................................................................................................7

Working Note 1......................................................................................................................7

Working Note 2......................................................................................................................7

Working Note 3......................................................................................................................7

(P4) Outline merits and demerits of different types of planning tools used in budgetary control

................................................................................................................................................8

(P5) Discuss how company is adapting management accounting systems to respond to

financial................................................................................................................................10

problems..............................................................................................................................10

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

(P1) Management accounting and essential requirements of its various types......................1

(P2) Discuss the methods used for management accounting reporting..................................3

(P3) Compute costs using techniques of cost analysis to prepare income statement using

absorption and marginal costing.............................................................................................5

APPENDIX......................................................................................................................................7

Working Note 1......................................................................................................................7

Working Note 2......................................................................................................................7

Working Note 3......................................................................................................................7

(P4) Outline merits and demerits of different types of planning tools used in budgetary control

................................................................................................................................................8

(P5) Discuss how company is adapting management accounting systems to respond to

financial................................................................................................................................10

problems..............................................................................................................................10

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

Management accounting is needed for organisation to make vibrant internal decisions

which is required so that organisation may achieve its objectives in effectual manner. The

enclosed report deals with importance of management accounting in firm as it produces effective

results (Advantages of Management Accounting, 2015). It has been used as budgeting forecasting

tool which is essential so that organisation may anticipate its output in effectual manner.

TASK 1

(P1) Management accounting and essential requirements of its various types

Management accounting is quite useful for managers as it helps them to take decisions

which are required for the effective functioning and working of company. Zylla also prepares

management accounting as it is really helpful for them for making fruitful decisions.

Management accounting is used only for the purpose of internal reporting as well as decisions

are made by managers by using management accounting reports. External parties are not allowed

to take in information for their use as it is only for management to take decisions about the

company so that performance can be maximised. Outside parties are not allowed to view the

information.

Management accounting is derived from financial accounting. It is so because as

financial accounting gives information regarding financial statements such as balance sheet,

income statement and prepares cash flow statement. These financial statements provide clear

picture of financial strength of organisation in effective way. This information is then interpreted

into meaningful report which is available to managers. By analysing the accounting information,

management comes to know about financial strength of firm. This information is known as

management accounting information (Collier, 2015). Managers take valuable information from it

to take vibrant decisions which are necessary for development of organisation in effectual

manner.

Management accounting report guides managers in making effective decision making and

any deviations or discrepancies are observed, it helps to rectify the same. This is the essence of

management accounting which helps organisation to produce effective results so that it may

flourish throughout its survival in effectually. Internal factors are taken into account because it is

1

Management accounting is needed for organisation to make vibrant internal decisions

which is required so that organisation may achieve its objectives in effectual manner. The

enclosed report deals with importance of management accounting in firm as it produces effective

results (Advantages of Management Accounting, 2015). It has been used as budgeting forecasting

tool which is essential so that organisation may anticipate its output in effectual manner.

TASK 1

(P1) Management accounting and essential requirements of its various types

Management accounting is quite useful for managers as it helps them to take decisions

which are required for the effective functioning and working of company. Zylla also prepares

management accounting as it is really helpful for them for making fruitful decisions.

Management accounting is used only for the purpose of internal reporting as well as decisions

are made by managers by using management accounting reports. External parties are not allowed

to take in information for their use as it is only for management to take decisions about the

company so that performance can be maximised. Outside parties are not allowed to view the

information.

Management accounting is derived from financial accounting. It is so because as

financial accounting gives information regarding financial statements such as balance sheet,

income statement and prepares cash flow statement. These financial statements provide clear

picture of financial strength of organisation in effective way. This information is then interpreted

into meaningful report which is available to managers. By analysing the accounting information,

management comes to know about financial strength of firm. This information is known as

management accounting information (Collier, 2015). Managers take valuable information from it

to take vibrant decisions which are necessary for development of organisation in effectual

manner.

Management accounting report guides managers in making effective decision making and

any deviations or discrepancies are observed, it helps to rectify the same. This is the essence of

management accounting which helps organisation to produce effective results so that it may

flourish throughout its survival in effectually. Internal factors are taken into account because it is

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

necessary that company should make internal atmosphere better to achieve its set targets. It is

necessary that employees fulfil their assigned roles in best and efficient manner so that they may

help organisation to accomplish set goals and objectives.

Different types of management accounting are as follows:

1. Cost accounting-

It is a type of accounting which aims to control the cost of firm so that resources are

completely optimised by firm. Cost accounting helps in assessing expenses of processes,

products as well as projects which assists Zylla in determining its expenses in effective way

(DRURY, 2013). It provides information to management by imparting cost behaviour and cost

profit volume analysis. Cost accounting helps firm to be effective in its way so that it can control

costs in that way which help in quoting its price of products. Cost accounting will measure and

records the expenses and then will compare output results with input that helps management in

assessing financial performance of company in effectual manner. It also consists of operating

costs which are incurred on daily basis by organisation.

2. Price optimisation-

It is a type of management accounting which involves preparation of mathematical

models that are used to determine whether demand varies with the price of product or not. It is

used to check that how much money customers can pay with regards to price. It assesses how

demand fluctuates with the change in price levels. It then combines data to suggest price that will

aid in maximising profits. Zylla effectively utilises price optimisation technique so that it may

quote the price of products in that way by which customers will prefer to buy it at that price

level.

3. Job costing:

It is a useful method which assess the cost of manufacturing such as labour cost, cost of

material and overhead costs. These are related to specific job. Job costing is an effective tool

2

necessary that employees fulfil their assigned roles in best and efficient manner so that they may

help organisation to accomplish set goals and objectives.

Different types of management accounting are as follows:

1. Cost accounting-

It is a type of accounting which aims to control the cost of firm so that resources are

completely optimised by firm. Cost accounting helps in assessing expenses of processes,

products as well as projects which assists Zylla in determining its expenses in effective way

(DRURY, 2013). It provides information to management by imparting cost behaviour and cost

profit volume analysis. Cost accounting helps firm to be effective in its way so that it can control

costs in that way which help in quoting its price of products. Cost accounting will measure and

records the expenses and then will compare output results with input that helps management in

assessing financial performance of company in effectual manner. It also consists of operating

costs which are incurred on daily basis by organisation.

2. Price optimisation-

It is a type of management accounting which involves preparation of mathematical

models that are used to determine whether demand varies with the price of product or not. It is

used to check that how much money customers can pay with regards to price. It assesses how

demand fluctuates with the change in price levels. It then combines data to suggest price that will

aid in maximising profits. Zylla effectively utilises price optimisation technique so that it may

quote the price of products in that way by which customers will prefer to buy it at that price

level.

3. Job costing:

It is a useful method which assess the cost of manufacturing such as labour cost, cost of

material and overhead costs. These are related to specific job. Job costing is an effective tool

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

which is used by company to track the expenses which are incurred on specific jobs and how in

future it can be reduced so that expenses incurred in performing job can be minimised

(Schaltegger and Burritt, 2010). This method helps organisation to save its resources and full

optimisation of resources are made and expenses are cut down too much extent. Job costing

involves three parts such as cost of material which means expenses of using components and

then allocating these costs once components are utilised. Labour costs and overhead costs are

analysed so that related to each jobs can be analysed and may be reduced so that it may improve

the profits of firm.

4. Inventory management:

This method of management accounting is essential from the perspective of managers. It

defines the process of ordering the required inventory for the production purpose and adequate

amount of required inventory is stored in the warehouse of company. Te inventory management

is used by Zylla which helps to reduce the inventory so that it may not lead to spoilage of it. This

additional expense will increase its cost and will deteriorate the revenue. Inventory process

includes components, raw materials and finished goods. For Zylla firm, inventory is valuable and

precious asset which needs to be preserved so that it may not deteriorates the benefits from it. If

large inventory is acquired by company then this will lead to spoilage of it and as a result, it will

have negative impact on firm's revenue.

(P2) Discuss the methods used for management accounting reporting

The methods used for management accounting reporting are as follows-

1. Segmental report:

This report deals with operating segments of the company by using financial statements

in effective way (Fullerton, Kennedy and Widener, 2014.). It is being used by creditors and

investors of company so that they are able to make decisions regarding financial strength of

company whether to provide funds to firm or not. It is very much useful information that aids

creditors and investors in decision making process. Segment reporting is used and require for

public firm and not for private ones. It includes revenue information, types of products which are

sold by each segment and many more.

2. Performance report:

3

future it can be reduced so that expenses incurred in performing job can be minimised

(Schaltegger and Burritt, 2010). This method helps organisation to save its resources and full

optimisation of resources are made and expenses are cut down too much extent. Job costing

involves three parts such as cost of material which means expenses of using components and

then allocating these costs once components are utilised. Labour costs and overhead costs are

analysed so that related to each jobs can be analysed and may be reduced so that it may improve

the profits of firm.

4. Inventory management:

This method of management accounting is essential from the perspective of managers. It

defines the process of ordering the required inventory for the production purpose and adequate

amount of required inventory is stored in the warehouse of company. Te inventory management

is used by Zylla which helps to reduce the inventory so that it may not lead to spoilage of it. This

additional expense will increase its cost and will deteriorate the revenue. Inventory process

includes components, raw materials and finished goods. For Zylla firm, inventory is valuable and

precious asset which needs to be preserved so that it may not deteriorates the benefits from it. If

large inventory is acquired by company then this will lead to spoilage of it and as a result, it will

have negative impact on firm's revenue.

(P2) Discuss the methods used for management accounting reporting

The methods used for management accounting reporting are as follows-

1. Segmental report:

This report deals with operating segments of the company by using financial statements

in effective way (Fullerton, Kennedy and Widener, 2014.). It is being used by creditors and

investors of company so that they are able to make decisions regarding financial strength of

company whether to provide funds to firm or not. It is very much useful information that aids

creditors and investors in decision making process. Segment reporting is used and require for

public firm and not for private ones. It includes revenue information, types of products which are

sold by each segment and many more.

2. Performance report:

3

This report is quite useful for organisation as it addresses the outcomes of work of an

individual. Performance report is essential requirement of Zylla company so that it may track the

performance of employees by analysing with the budgeted outcome to be compared and matched

with the actual results (Renz, 2016). This is essential so that if any variance is found in

performance, it can be resolved by taking corrective action by organisation in effectual manner.

It is method which found out the deviations if prevailing in the performance of workers and take

measures to remove it totally to enhance performance of employees.

3. Inventory management report:

The inventory management report deals with inventory to make effective the process of

manufacturing in the concern organisation. Zylla company efficiently uses this report so that it

may track the inventory waste if any. It also includes labour costs as well as overhead costs.

Inventory management reports is useful for managers so that they may make decisions whether

inventory is in adequate manner or it is excessive in firm's godown. Excessive inventory leads to

wastage of resources and adds to additional expenses to organisation. It leads to decrease in

profits.

4. Accounts receivables ageing report:

This report deals with the information of the customer invoices that are become overdue

for payment. It lists down unpaid invoices and credit memos of customer. It helps management

to make effective transparency as to how many payments are pending from customers on their

invoices (Cooper, Ezzamel and Qu, 2017). Manager may be able to manage the cash flows of

organisation. Manager can use accounts receivables ageing report to find out difficulty that is

being aroused in collection process. If customers are not paying their obligations, then firm need

to tighten its credit policies.

5. Job cost report:

Job cost report deals with the cost that is involved in carrying out job. By analysing job

expense, company may be able to ficus on high profit margin areas and exclude the low profit

margin so that wastage of resources are not incurred on low profit earning jobs. It helps mangers

to analyse the specific job areas so that profit may not get reduced. This helps company to

manage its job's profitability to those areas which yield best results to it in effectual manner. It

4

individual. Performance report is essential requirement of Zylla company so that it may track the

performance of employees by analysing with the budgeted outcome to be compared and matched

with the actual results (Renz, 2016). This is essential so that if any variance is found in

performance, it can be resolved by taking corrective action by organisation in effectual manner.

It is method which found out the deviations if prevailing in the performance of workers and take

measures to remove it totally to enhance performance of employees.

3. Inventory management report:

The inventory management report deals with inventory to make effective the process of

manufacturing in the concern organisation. Zylla company efficiently uses this report so that it

may track the inventory waste if any. It also includes labour costs as well as overhead costs.

Inventory management reports is useful for managers so that they may make decisions whether

inventory is in adequate manner or it is excessive in firm's godown. Excessive inventory leads to

wastage of resources and adds to additional expenses to organisation. It leads to decrease in

profits.

4. Accounts receivables ageing report:

This report deals with the information of the customer invoices that are become overdue

for payment. It lists down unpaid invoices and credit memos of customer. It helps management

to make effective transparency as to how many payments are pending from customers on their

invoices (Cooper, Ezzamel and Qu, 2017). Manager may be able to manage the cash flows of

organisation. Manager can use accounts receivables ageing report to find out difficulty that is

being aroused in collection process. If customers are not paying their obligations, then firm need

to tighten its credit policies.

5. Job cost report:

Job cost report deals with the cost that is involved in carrying out job. By analysing job

expense, company may be able to ficus on high profit margin areas and exclude the low profit

margin so that wastage of resources are not incurred on low profit earning jobs. It helps mangers

to analyse the specific job areas so that profit may not get reduced. This helps company to

manage its job's profitability to those areas which yield best results to it in effectual manner. It

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

beforehand assesses the job cost so that expense on it may not incur and wastage of resources is

not made by company (Suomala, Lyly-Yrjänäinen and Lukka, 2014).

The benefits of management accounting systems are:

1. Reduce expenses-

Zylla company can reduce its operational expenses too much extent with the help of

management accounting system. This helps it to have adequate quantum of profit which can be

used in further activities.

2. Decisions-

Business decisions are made inn effectual manner as management accounting provides

good source of information which is required by manager to make better internal decisions for

organisation in effective way.

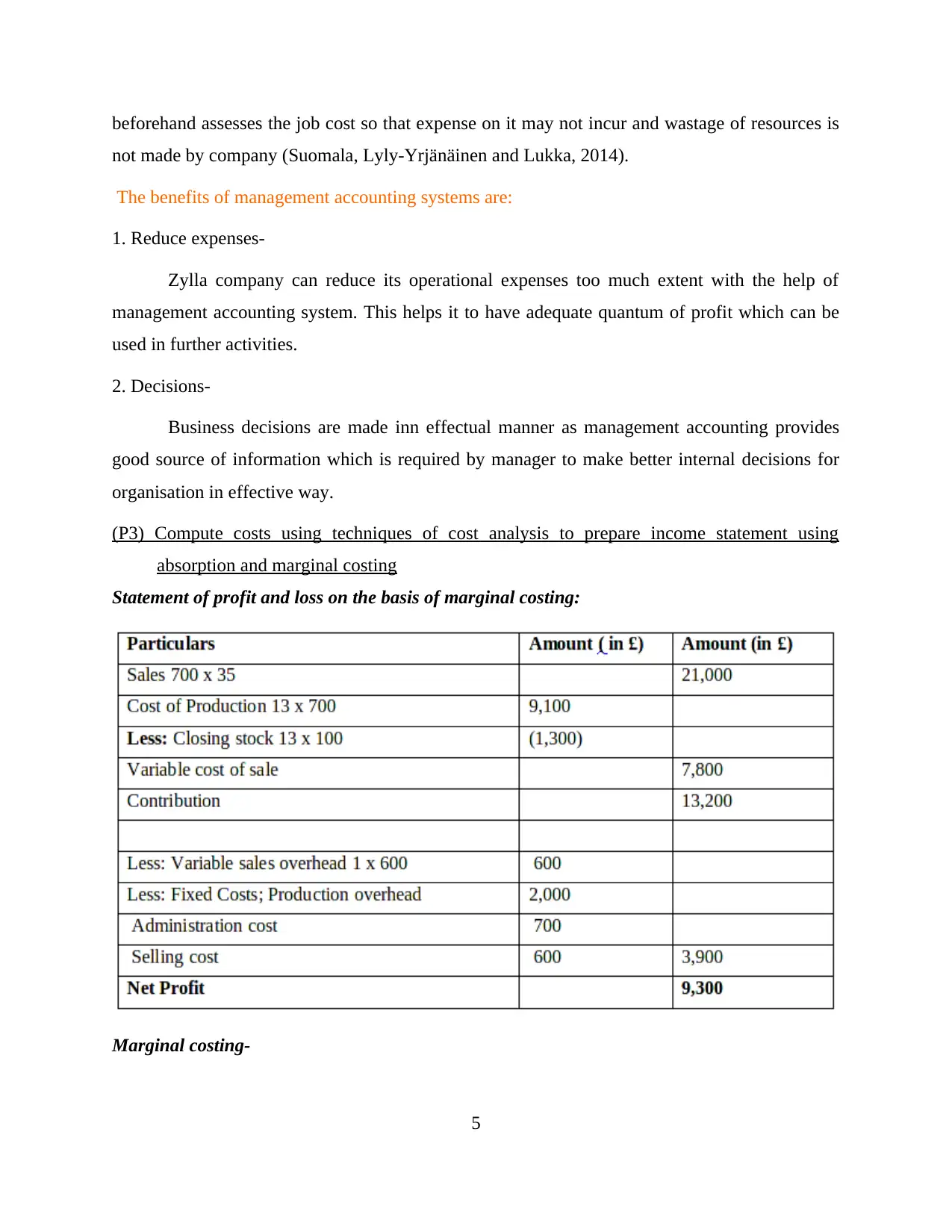

(P3) Compute costs using techniques of cost analysis to prepare income statement using

absorption and marginal costing

Statement of profit and loss on the basis of marginal costing:

Marginal costing-

5

not made by company (Suomala, Lyly-Yrjänäinen and Lukka, 2014).

The benefits of management accounting systems are:

1. Reduce expenses-

Zylla company can reduce its operational expenses too much extent with the help of

management accounting system. This helps it to have adequate quantum of profit which can be

used in further activities.

2. Decisions-

Business decisions are made inn effectual manner as management accounting provides

good source of information which is required by manager to make better internal decisions for

organisation in effective way.

(P3) Compute costs using techniques of cost analysis to prepare income statement using

absorption and marginal costing

Statement of profit and loss on the basis of marginal costing:

Marginal costing-

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Marginal costing is useful in analysing cost (Ax and Greve, 2017). It is the increase or

decrease in total production cost if one unit is increased in the output. In the above table, net

profit is 9300 which is quite good for the firm. Marginal costs may be used for production related

decisions.

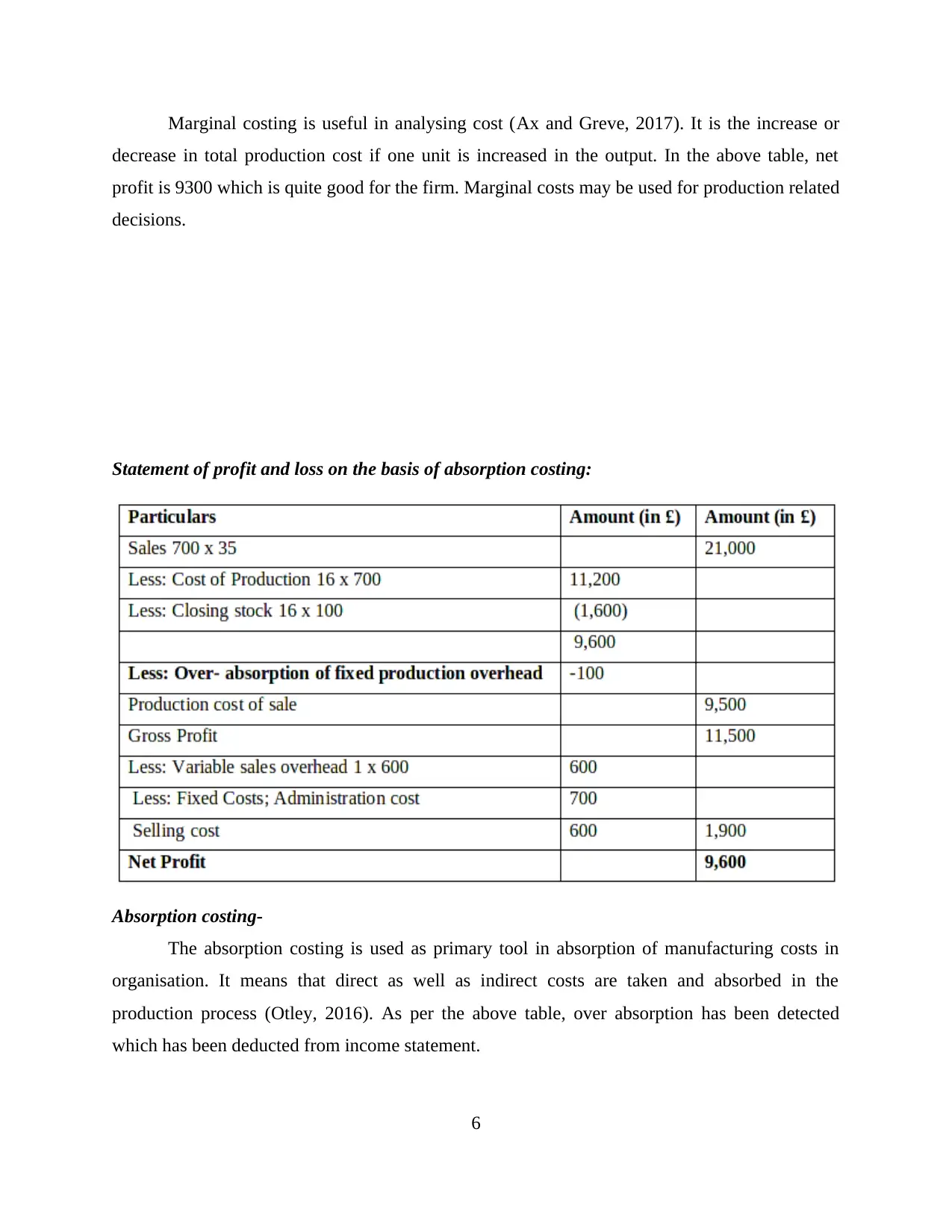

Statement of profit and loss on the basis of absorption costing:

Absorption costing-

The absorption costing is used as primary tool in absorption of manufacturing costs in

organisation. It means that direct as well as indirect costs are taken and absorbed in the

production process (Otley, 2016). As per the above table, over absorption has been detected

which has been deducted from income statement.

6

decrease in total production cost if one unit is increased in the output. In the above table, net

profit is 9300 which is quite good for the firm. Marginal costs may be used for production related

decisions.

Statement of profit and loss on the basis of absorption costing:

Absorption costing-

The absorption costing is used as primary tool in absorption of manufacturing costs in

organisation. It means that direct as well as indirect costs are taken and absorbed in the

production process (Otley, 2016). As per the above table, over absorption has been detected

which has been deducted from income statement.

6

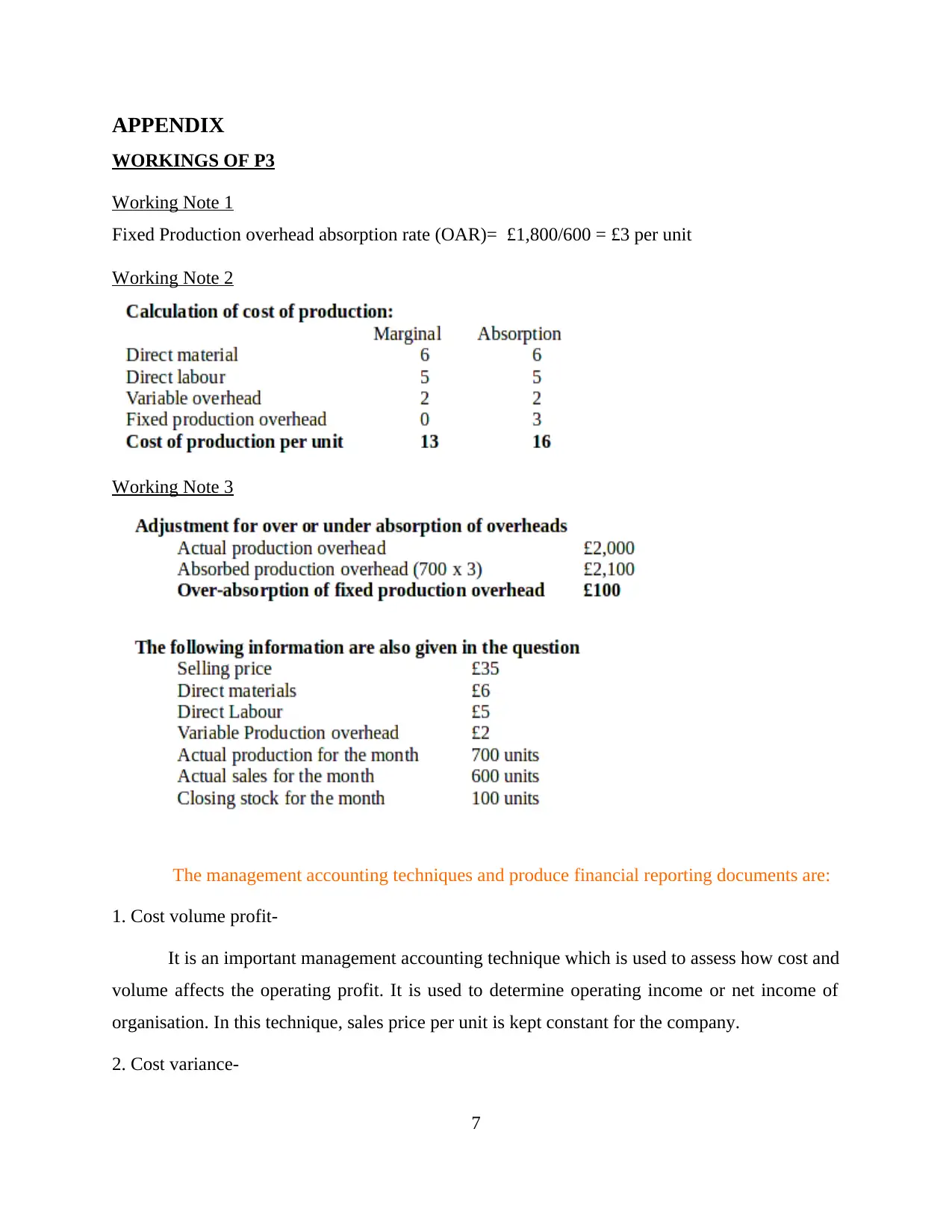

APPENDIX

WORKINGS OF P3

Working Note 1

Fixed Production overhead absorption rate (OAR)= £1,800/600 = £3 per unit

Working Note 2

Working Note 3

The management accounting techniques and produce financial reporting documents are:

1. Cost volume profit-

It is an important management accounting technique which is used to assess how cost and

volume affects the operating profit. It is used to determine operating income or net income of

organisation. In this technique, sales price per unit is kept constant for the company.

2. Cost variance-

7

WORKINGS OF P3

Working Note 1

Fixed Production overhead absorption rate (OAR)= £1,800/600 = £3 per unit

Working Note 2

Working Note 3

The management accounting techniques and produce financial reporting documents are:

1. Cost volume profit-

It is an important management accounting technique which is used to assess how cost and

volume affects the operating profit. It is used to determine operating income or net income of

organisation. In this technique, sales price per unit is kept constant for the company.

2. Cost variance-

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cost variance is the difference between actual cost and budgeted cost. It is the variance

which rises out of these costs (Anessi-Pessina and et.al, 2016). It is useful for producing financial

reporting documents.

3. Revaluation accounting-

It is an adjustment made to value of asset to correctly analyse its current market value.

(P4) Outline merits and demerits of different types of planning tools used in budgetary control

1. Zero based budgeting-

This budgeting is quite useful for the management. In this budgeting, preparation of

budget involve from the completely new one for the current year. It means that budget is

prepared with reference to zero bas and past budget is not being utilised in this budget type.

Merits:

1. It is accurate in preparing the budget. Unlike other budgeting it does not take into

account the past figures in the preparation of budget. As such, accuracy is being achieved in zero

based budgeting.

2. It is also efficient enough as it takes in account only actual numbers and not using past

or historic budget. As a result, efficiency is observed in zero based budgeting.

Demerits:

1. It is time consuming as it takes entire budget from the scratch. It consumes time as full

budget need top be created which is a disadvantage of using zero budgeting tool.

2. It also requires lot of human resources as entire line items need to be framed for

preparing budget which requires lot of man power (Malmi, 2016).

2. Incremental budgeting-

This budgeting is quite easy to prepare the budget fort the firm in effectual manner. It

tales into account historical data and only changes are made on incremental basis. This means

that if any department require funds, then this budget just increments the fund value for their

demand fulfilment.

Merits:

8

which rises out of these costs (Anessi-Pessina and et.al, 2016). It is useful for producing financial

reporting documents.

3. Revaluation accounting-

It is an adjustment made to value of asset to correctly analyse its current market value.

(P4) Outline merits and demerits of different types of planning tools used in budgetary control

1. Zero based budgeting-

This budgeting is quite useful for the management. In this budgeting, preparation of

budget involve from the completely new one for the current year. It means that budget is

prepared with reference to zero bas and past budget is not being utilised in this budget type.

Merits:

1. It is accurate in preparing the budget. Unlike other budgeting it does not take into

account the past figures in the preparation of budget. As such, accuracy is being achieved in zero

based budgeting.

2. It is also efficient enough as it takes in account only actual numbers and not using past

or historic budget. As a result, efficiency is observed in zero based budgeting.

Demerits:

1. It is time consuming as it takes entire budget from the scratch. It consumes time as full

budget need top be created which is a disadvantage of using zero budgeting tool.

2. It also requires lot of human resources as entire line items need to be framed for

preparing budget which requires lot of man power (Malmi, 2016).

2. Incremental budgeting-

This budgeting is quite easy to prepare the budget fort the firm in effectual manner. It

tales into account historical data and only changes are made on incremental basis. This means

that if any department require funds, then this budget just increments the fund value for their

demand fulfilment.

Merits:

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1. This method is very easy to use and to implement as it does not involve any complex

computations. It recreates the past budget on the incremental basis.

2. It ensures continuity of resource or funds for various department without much delay.

As a result, time is saved and functioning of departments are not stopped (.Covaleski, Dirsmith

and Samuel, 2017).

Demerits:

1. The incremental budgeting may lead to wastage of funds and unnecessary use of it as

departments may use the funds because it is easily available to them.

2. Incremental budgeting may lead to higher spending as budget is maintained next year.

It may not lead to optimization of funds.

3. Fixed budgeting-

This budgeting states that whatever sales is generated or some other activities increases

or decreases, company's budget will remain fixed. It means that remains static when any

activities either increases or decreases. It is also called static budget. Fixed budgets are based on

the collected data before the period begins.

Merits:

1. Major advantage of fixed budget is that it need not be updated throughout the period.

As a result, no fluctuations are observed and is easy to implement in firm.

2. It offers string insight into expenses of the company and profits as variance analysis is

performed (Ueno and Scarbrough, 2016).

Demerits:

1. It is not flexible as budget cannot be updated in the year because it is static one. It is

not suitable for changing environment in which organisation operates.

2. If any changes are to be incorporated regarding allocation of resources, it cannot alter

it.

9

computations. It recreates the past budget on the incremental basis.

2. It ensures continuity of resource or funds for various department without much delay.

As a result, time is saved and functioning of departments are not stopped (.Covaleski, Dirsmith

and Samuel, 2017).

Demerits:

1. The incremental budgeting may lead to wastage of funds and unnecessary use of it as

departments may use the funds because it is easily available to them.

2. Incremental budgeting may lead to higher spending as budget is maintained next year.

It may not lead to optimization of funds.

3. Fixed budgeting-

This budgeting states that whatever sales is generated or some other activities increases

or decreases, company's budget will remain fixed. It means that remains static when any

activities either increases or decreases. It is also called static budget. Fixed budgets are based on

the collected data before the period begins.

Merits:

1. Major advantage of fixed budget is that it need not be updated throughout the period.

As a result, no fluctuations are observed and is easy to implement in firm.

2. It offers string insight into expenses of the company and profits as variance analysis is

performed (Ueno and Scarbrough, 2016).

Demerits:

1. It is not flexible as budget cannot be updated in the year because it is static one. It is

not suitable for changing environment in which organisation operates.

2. If any changes are to be incorporated regarding allocation of resources, it cannot alter

it.

9

4. Variance analysis-

This is helpful tool in budget as through this organisation ia able to match the budgted

results with the actual results and as such, if any variances is found corrective actions may be

taken by it.

5. Capital budgeting-

The capital investment appraisal technique like NPV (Net Present Value) is useful for

organisation so that they may forecast whether to invest in particular project or not. Greater NPV

is better for the firm.

6. Contingency planning-

This is important as in the event of risks, organisation may face several deviations and as

such, it is necessary to execute other plans. In simple words, contingency plan means having

other plans if one fails in the event of contingency.

The use of different planning tools and their application for forecasting budgets are as

follows:

1. Cash flow forecasting-

Cash flow forecasting is more useful for preparing and forecasting budget. It helps firm

owner to find out peaks and low in bank finance.

2. Fund flow statement-

It shows inflows and outflows of funds between two balance sheets of company and is

used to forecast budget (Kolb and Kolb, 2011).

(P5) Discuss how company is adapting management accounting systems to respond to financial

problems.

Key performance indicators (KPI)-

It is a type of measurement of performance. It highlights how effectively company is

achieving its objectives. It focuses on overall performance of organisation. KPI is used to track

factors which are utmost essential for corporate managers to evaluate the success of organisation

in effectual manner. KPI Indicates that organisation is performing well and is achieving its goals

10

This is helpful tool in budget as through this organisation ia able to match the budgted

results with the actual results and as such, if any variances is found corrective actions may be

taken by it.

5. Capital budgeting-

The capital investment appraisal technique like NPV (Net Present Value) is useful for

organisation so that they may forecast whether to invest in particular project or not. Greater NPV

is better for the firm.

6. Contingency planning-

This is important as in the event of risks, organisation may face several deviations and as

such, it is necessary to execute other plans. In simple words, contingency plan means having

other plans if one fails in the event of contingency.

The use of different planning tools and their application for forecasting budgets are as

follows:

1. Cash flow forecasting-

Cash flow forecasting is more useful for preparing and forecasting budget. It helps firm

owner to find out peaks and low in bank finance.

2. Fund flow statement-

It shows inflows and outflows of funds between two balance sheets of company and is

used to forecast budget (Kolb and Kolb, 2011).

(P5) Discuss how company is adapting management accounting systems to respond to financial

problems.

Key performance indicators (KPI)-

It is a type of measurement of performance. It highlights how effectively company is

achieving its objectives. It focuses on overall performance of organisation. KPI is used to track

factors which are utmost essential for corporate managers to evaluate the success of organisation

in effectual manner. KPI Indicates that organisation is performing well and is achieving its goals

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.